who cares about accounting kcba - kcba > home page cares about accounting? july 22, 2010 barbara...

TRANSCRIPT

Who Cares About Accounting? July 22, 2010

Barbara A. Schafer CPA CLM 1

P R E S E N T E D B Y

BARBARA A . SCHAFER , C PA , C LM

C O N S U L T I N G @ B A R B A R A S C H A F E R . C O M

MARCH 7 , 2 0 1 1

Who Cares About Accounting?

What is Accounting?5

A language. A way to talk about money.

A system that•records

•reviews•analyzes

•interpretsfinancial information.

Why do it?6

The purpose of accounting is to provide useful

information to internal and external users and

decision makers.

� timely

� accurate

� relevant

Who Cares About Accounting? July 22, 2010

Barbara A. Schafer CPA CLM 2

Who will be using this information?7

Internally� Owner(s)� Management� DepartmentsExternally� Clients (invoices, statements)� Banks and other lenders� Tax preparer, IRS, state/local agencies� Potential partners� Auditors

Key Terms8

� Cash basis

� Accrual basis

Cash Basis9

Revenue is recognized when cash is received; expense is recognized when cash is paid. Examples:

� Revenue - Professional Fee Revenue is recorded when cash is received.

� Expense - A supply purchase is recorded when payment is made, in cash or by check.

Who Cares About Accounting? July 22, 2010

Barbara A. Schafer CPA CLM 3

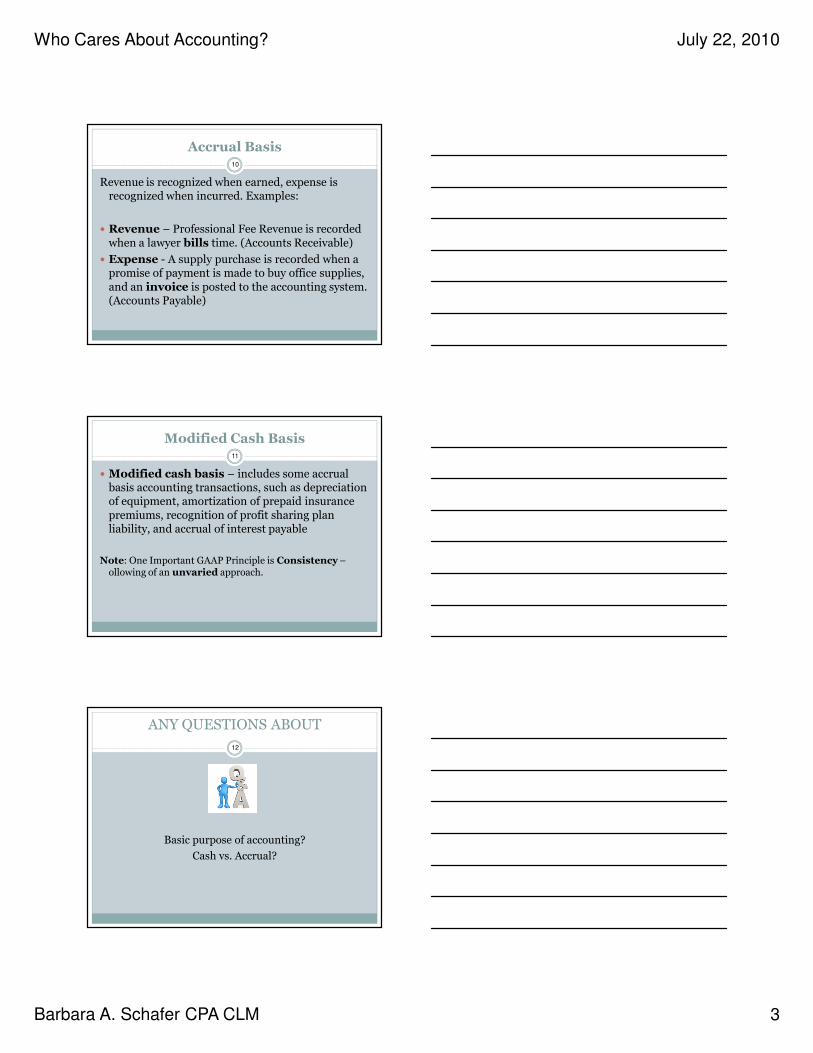

Accrual Basis10

Revenue is recognized when earned, expense is recognized when incurred. Examples:

� Revenue – Professional Fee Revenue is recorded when a lawyer bills time. (Accounts Receivable)

� Expense - A supply purchase is recorded when a promise of payment is made to buy office supplies, and an invoice is posted to the accounting system. (Accounts Payable)

Modified Cash Basis11

� Modified cash basis – includes some accrual basis accounting transactions, such as depreciation of equipment, amortization of prepaid insurance premiums, recognition of profit sharing plan liability, and accrual of interest payable

Note: One Important GAAP Principle is Consistency–ollowing of an unvaried approach.

ANY QUESTIONS ABOUT

12

Basic purpose of accounting?

Cash vs. Accrual?

Who Cares About Accounting? July 22, 2010

Barbara A. Schafer CPA CLM 4

4 Basic Financial Statements13

1. Balance Sheet

2. Income Statement (Revenues and Expenses, Profit and Loss, P/L)

3. Cash Flow Statement

4. Statement of Changes in Owners’ Equity (Retained Earnings, Partners’/Members’ Capital Accounts)

Why is it called a Balance Sheet?14

ASSETS = LIABILITIES + OWNERS’ EQUITY

What you have Where it came from

Always represents a moment in time - “As of June 30, 2011”

Simple Example of a Balance Sheet

15

Day 1 of a new entity - Tom’s Law Firm

Tom takes $500 from his personal checking account and gets a loan from the bank for $1,500.

He opens a business checking account and deposits the $2,000.

Who Cares About Accounting? July 22, 2010

Barbara A. Schafer CPA CLM 5

Tom, Attorney at Law

Balance SheetAs of January 1, 2009

16

Assets

Cash in Bank $2,000

Total Assets $2,000

Liabilities

Loan from Bank 1,500

Owner’s Equity

Tom’s Capital 500

Total Liabilities and Equity $2,000

ASSETS17

� Cash in Operating Account� Cash in Money Market Account� S-T Investment in Charles Schwab Accounts

� Client Costs Advanced� Loans to Partners� Computer Equipment

� Software� Furniture (FF&E)� Office Equipment

� Leasehold Improvements� Artwork� Buildings

� Land

Liabilities18

Liabilities

� Loans from Partners

� Bank Loans (Long Term Debt)

� Line of Credit

� Profit Sharing Plan Payable

Who Cares About Accounting? July 22, 2010

Barbara A. Schafer CPA CLM 6

Balance Sheet

19 Cash

Basi s

A ccrual

Bas is

Assets

Current Asse ts

Cash in Bank 850,000$ 850,000$

Petty Cash 2,000 2 ,000

I nvestment i n Char les Schwab Accounts 3,150,000 3,150,000

Prepaid Rent 8,000 8 ,000

A ccounts Receivabl e (A/ R) 1,000,000

Work i n Process (WI P) 500,000

C l ient Costs Advanced 15,000 45,000

T otal Current Assets 4,025,000 4 ,705,000

Fixed Asse ts

Furniture F ixtures & Equi pment (FF&E) 500,000 51 5,000

L ess: Accumulated Depreciati on (165,000) (165,000)

L easehold Improvements 400,000 400,000

L ess: Accumulated Amortiz ation (20,000) (20,000)

A rtwork 80,000 80,000

T otal F ixed A ssets 795,000 81 0,000

Total A sssets 4, 820,000$ 5,515, 000$

Liab ilitie s a nd Equity

Current L iabilities

Accounts Payab l e 50,000

A ccrued Wages Payab le 35,000

Profit Shari ng Pl an Payable 200,000 200,000

Current Portion Long Term Debt 50,000 50,000

T otal Current L iab il ities 250,000 335,000

Long Te rm Debt 120,000 120,000

Total Liab ilites 370,000 455, 000

Pa rtners' Equity

M embers' Cap ital Accounts 1,517,750 1 ,747,750

Current Peri od Earni ngs 2,932,250 3,31 2,250

Total Equity 4, 450,000 5,060, 000

Total Liab ilities a nd Equity 4, 820,000$ 5,515, 000$

T om Di ck and Harriet, L LC

Balance S heet

As of December 31, 2008

Any Questions About

20

Balance Sheets?

Income Statement21

� Often referred to as P & L or P/L (Profit and Loss)

� For a specific period of time, “For the Three Months Ending March 31, 2009”

� “Tells the story of a firm’s sources of revenue and the income remaining after the cost of business and operating expenses are deducted”

� Describes how income is generated, and how much it cost to generate that income

� Bottom Line is “Net Income”

� Over time, determines the continued existence of the firm

Who Cares About Accounting? July 22, 2010

Barbara A. Schafer CPA CLM 7

Revenues

� Professional Fees

� Retainers

� Client Cost Recoveries

� Interest on Client Accounts

22

Expenses23

� Wages, taxes and benefits

� Rent

� Supplies

� Meals and Entertainment

� Marketing and Promotion

� Computer system maintenance

� Copier lease payments

Income Statement24

Revenues

Modified Cash

Basis Accrual Basis

Professional Fees 10,450,000 10,875,000

Arbitration Fees 25,000 15,000

Cl ient Cost Recoveries 120,000 170,000

Interest Income 2,500 2,500

Other Income 4,000 4,000

Total Revenues 10,601,500 11,066,500

Expenses

Wages, Taxes & Benefits 7,550,000 7,585,000

Depreciation & Amortization 15,000 15,000

Employee Education 7,000 32,000

Insurance 12,000 12,000

Marketing 750 2,500

Meals & Entertainment 1,500 14,000

Office Supplies 15,000 17,500

Postage 4,000 4,000

Rent 44,000 48,000

Repairs & M aintenance 5,000 7,250

Retreats 15,000 17,000

Total Expenses 7,669,250 7,754,250

Net Income 2,932,250 3,312,250

Income Statement

For the Twelve Months Ending December 31, 2008

Who Cares About Accounting? July 22, 2010

Barbara A. Schafer CPA CLM 8

Any Questions About

25

Income Statements?

Depreciation26

This word is found on both the Balance Sheet and the Income Statement

� On the Balance Sheet - “Accumulated Depreciation”� On the Income Statement - “Depreciation Expense”

Definition: Systematic rational allocation of cost over the life of an asset

� Cost = what you paid, historical cost� Life = estimated period of usefulness related to the

generation of income - usually the IRS defined life

Any Questions About

27

Depreciation?

Who Cares About Accounting? July 22, 2010

Barbara A. Schafer CPA CLM 9

Cash Flow Statement28

Describes what happened to the balance in the Cash account.

Three types of activities:

� Operating (results of operations, or Net Income)

� Investing (purchase of an asset)

� Financing (loan proceeds or payment of loan principal)

Note: Displays beginning cash balance and ending cash balance. Must tie out to the balance sheet.

Cash Flow Statement29

Tom Dick and Harriet, LLC

Statement of Cash Flows

For the Twelve Months Ending December 31, 2008

CashBasis Accrual Basis

Operating Activities

Net Income 2,932,250 3,312,250

Adjustments to reconcile net income to net cash

provided by operating activities

Depreciation and Amortization 15,000 15,000

Changes in operating assets and liabilities

Accounts receivable (377,000)

Client Cost Advances 5,000 7,500

Accounts payable (15,500)

Accrued expenses 25,000

Net Cash Provided by Operating Activities 2,952,250 2,967,250

Investing Activities

Purchase of Equipment and Improvements (25,000) (40,000)

Financing Activities

Any Questions About30

Cash Flow Statements?

Who Cares About Accounting? July 22, 2010

Barbara A. Schafer CPA CLM 10

Statement of Owners’ Equity31

Nomenclature depends on the form of Entity:

� Sole Proprietorship = Owner’s Equity

� Partnership = Partner Capital Accounts

� LLC = Member Capital Accounts

� Corporation = Common Stock, Preferred Stock, Paid in Capital, Retained Earnings

Effects of Types of Entities32

1. Ownership - control

2. Taxability of entity

3. Liability of owners

Three Effects

33

Sole Proprietorship

� Single owner

� Taxed on personal tax return (Schedule C and Self Employment forms)

� Unlimited personal liabilityPartnership

� Two or more owners

� Not a taxable entity (Partners taxed as individuals through K-1)� Joint and several liability (Depends on form or partnership, limited

or general)Corporation

� One or more owners, separate “person” under the law

� Taxable entity� Owners shielded from liability (debts and acts of corporation)

Who Cares About Accounting? July 22, 2010

Barbara A. Schafer CPA CLM 11

What does Equity Look Like?

34

Sole Proprietorship

� “Owner’s Equity”

� Distributions to owner are disclosed on Statement of Changes in Owners’ Equity

Partnership� “Partner Capital Accounts”

� May be multiple lines, one for each partner

� Current earnings are allocated based on partners’ percentage of ownership

� Distributions to partners are disclosed on Statement of Changes in Owners’ Equity as Partner Draws

Corporation� Common stock (or other forms of stock, such as preferred)

� Paid in Capital (may be described as APIC)

� Retained Earnings� Dividend distributions will be disclosed on Statement of Changes in

Owners’ Equity

Any Questions About

35

Business Entities?

Attorney Trust Accounts36

� Critical activity of law firm accounting

� Funds paid on behalf of client

� Held until work is performed or order comes from outside authority (court)

� Note – outstanding checks over 3 years old are unclaimed property

� Helpful information about trust accounting can be found in the WSBA publicationManaging Client Trust Accounts: Rules, Regulations, and Common Sense, available atwww.wsba.org/media/¬publications/-pamphlets/managing.htm.

Who Cares About Accounting? July 22, 2010

Barbara A. Schafer CPA CLM 12

Any Questions About

37

Trust Accounts?

Timekeeper Production Reports38

� How many hours did each timekeeper work?

� How many dollars?

� Who billed – hours and dollars?

� Who collected, and how much? (Ties to the Income Statement)

� A/R Aging Report – How old (and likely to be collected) are each timekeeper’s billings?

Like the Income Statement, over time these reports are indicators of the firm’s (and each timekeeper’s) continued success.

Profitability Reports39

� Hot topic

� Calculation of OVERHEAD

� May be allocated by department, by timekeeper, by location

� May be performed monthly, quarterly, just during attorney compensation process

� No “right” way – internal report

Who Cares About Accounting? July 22, 2010

Barbara A. Schafer CPA CLM 13

Any Questions About

40

Production, Profitability or Overhead?

Any Questions About

41

Anything we haven’t discussed?