whither the click? how oniine advertising works · whither the click? how oniine advertising works...

TRANSCRIPT

Whither the Click?

How Oniine Advertising Works

GIAN M. FULGONI

comScore, Inc.

MARIE PAULINE MORN

comScore, Inc.

Online advertising spending In the United States exceeds $20 billion annually.

However, click rates on display advertisements average oniy 0.1 percent. Are iow

ciick rates evidence that display advertisements have no impact on consumer

behavior? Or, does dispiay advertising work in a manner simiiar to traditional

"branding" advertising, with multiple exposures being required to effect a change

in consumer behavior? This article shows that the click is not an accurate indicator

of the effectiveness of online display advertisements. Even when click rates are

minimal, display advertisements can generate meaningfui increases in site visitation,

trademark search, and both oniine and offline sales.

BACKGROUND

In today's economically challenging times, adver-

tisers and their agencies appear to be moving

their online display advertising dollars from cus-

tomer relationship management campaigns that

require payment based on the number of people

exposed to the campaign to "pay-for-performance"

programs {"CPC" or "CPA") that require payment

when the consumer performs some desired action

such as clicking on an advertisement.

At the same time, however, research is showing

that a click may not be a relevant measure of the

impact of display advertising. Click rates on static

display advertisements fell dramatically in recent

years, to average levels of only 0.2 percent in

2006. The comScore studies referenced in this ar-

ticle show that average click rates on display

advertisements in 2008 fell even further, to less

than 0.1 percent. Other research conducted in Eu-

rope has shown similar very low click rates (eMar-

keter, 2009). Further research has shown that 6

percent of the online population accounts for 50

percent of all clicks and that heavy clickers are not

representative of the total online population, skew-

ing heavily toward the 25-44 age group and to

households with an income less than $40,000

(Starcom Media Vest Group Press Release, 2008).

Are low click rates evidence that an advertise-

ment has not had any impact on consumer behav-

ior? Or, does online display advertising work in a

similar manner to traditional offline advertising,

with multiple exposures over time being needed

to effect a change in consumer behavior?

The results presented in this article will show

the manner in which online display advertise-

ments work in affecting consumer behavior, re-

vealing that there are, indeed, latency effects,

branding effects, and sales lifts—even when click

rates are minimal.

DESCRIPTION OF DATA SOURCES AND STUDIES

CONDUCTED

This article references results from more than 170

online advertising effectiveness studies conducted

by comScore. comScore has built a unique market-

research database consisting of two million global

internet users (one million of whom are residents

in the United States) who have explicitly agreed

to the tracking of their orüine behavior. For each

panelist, software was installed on his/her com-

puter to unobtrusively capture the details of their

internet activities, including every site visited, con-

tent viewed, content entered, time spent, product

or service bought, and price paid. Every display

1 3 4 JDUHnHL DF HDUEHTISIHG RiSEReCIJ June 2 o o g DOI: 10.2501/S0021849909090175

HO\N ONLINE ADVERTISING WORKS

EMPIRICAL GENERALIZATIONSEven with no clicks or minimal clicks, online display advertisements can generate

substantial lift in site visitation, trademark search queries, and lift in both online and

offline sales.

and search advertisement that was re-

ceived by the panelists was also captured,

including whether the advertisement was

clicked on or not.

The panel was statistically weighted and

projected using a variety of demographic

•ind behavioral variables to represent the

internet user population, and the data

have been validated through comparisons

to third-party data. (One such compari-

son is to the U.S. Department of Com-

merce quarterly estimates of e-commerce

sales, see Figure 1.)

The database was encrypted for com-

plete privacy protection, and no person-

ally identifiable information was released.

The data were matched (using name

and address) with third-party offline

databases producing a "single-source"

datamart that contained both online and

offline behavior. Panelists had the option

of completing customized surveys deliv-

ered to them either via email or by a

"contextual pop" on their computer screen

during their time in the panel triggered

by their online behavior—such as visit-

Q2 2008 comScore: $34.8 BillionQ2 2008 DOC: $34.6 Billion

$45.0

$40.0

$35.0-

$30.0

I $25.0

^ $20.0

r •

rnim i l I

iiiiiiiii I

lQ 3Q lQ 3Q lQ 3Q lQ 3Q lQ 3Q lQ 3Q lQ 3Q lQÜl '01 '02 '02 '03 '03 '04 '04 '05 '05 '06 '06 '07 '07 '08

I U.S. Department of Commerce • comScore

comScore Estimate = (Total Nontravel - Event Tickets + Estimated Auction Fees)

Figure 1 Validation of comScore Sales Data: Comparison ofcomScore Data to U.S. Department of Commerce

ing a certain site or viewing specificcontent.

RESEARCH DESIGN

To maximize accurate identification of a

specific campaign that was being tracked

as part of a study, advertising agencies

and/or publishers that were involved in

online advertising were provided with a

tag, which was appended to the display

advertisement. This allowed for the sys-

tematic and accurate identification of the

consumers who were exposed to a spe-

cific advertisement. Depending on the spe-

cific requirements of the project, the tag

also may have included parameters for

segmentation purposes, such as an iden-

tification of the site that published the

advertisements and the type of creative

message used.

Test groups: Based on passively ob-served exposure to an advertisement, atest group of panelists exposed to thecampaign was generated. Test cells couldvary depending on the specific objectivesof the campaign and could be mixed andmatched accordingly.

Control group: A control group of pan-elists not exposed to the campaign alsowas generated. This group had no expo-sure to the advertisements, but exhibitedthe following characteristics when com-pared to the test group(s):

• similar historical usage of the internet

overall;

• similar historical visitation to the sites

where the advertisements were in

rotation;

• similar historical total search behavior

online;

• similar distribution on the following

household demographics: age, income,

census region or residence, and connec-

tion speed;

• similar historical offline buying behav-

ior (if relevant to the study at hand).

June 2 0 0 9 J Q H L OF eDOERTISlOG BESEHIICH 1 3 5

HOW ONLINE ADVERTISING WORKS

With the exception of the exposure to the

online display advertising test campaign,

the test and control groups were virtually

identical, including their exposure to other

forms of media.

Passively collected behavioral data cap-

tured the view-through value of the over-

all campaign by measuring consumers'

internet activity across key behavioral met-

rics, This behavior was measured irrespec-

tive of whether an advertisement was

clicked on or not.

The database contains data and analysis

on more than 200 studies, of which certain

subsets are available for various types of

analysis. Results included in the database

were tested at a 90 percent confidence level

using a one-tail t-test. Reportable mea-

sures must also have minimum sample size

requirements, which vary depending on the

type of behavior being analyzed.

DETAILED RESULTS

The impact of display advertisements on

visitation to an advertiser's site

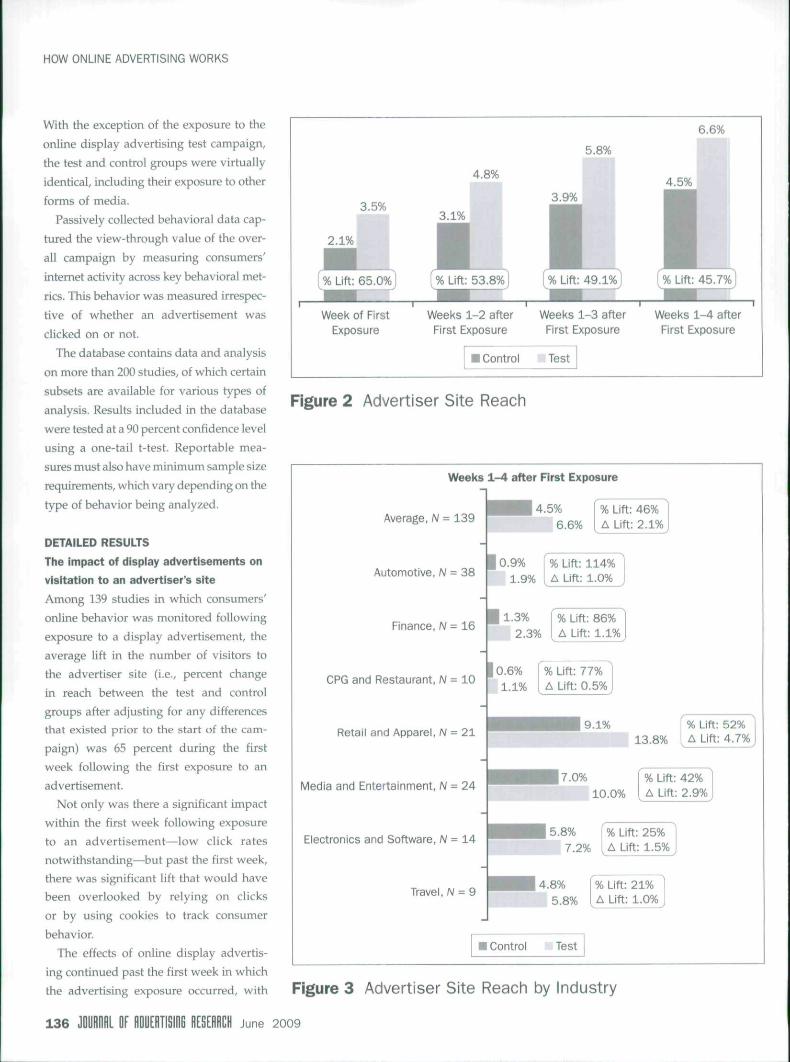

Among 139 studies in which consumers'online behavior was monitored followingexposure to a display advertisement, theaverage lift in the number of visitors tothe advertiser site (i.e., percent changein reach between the test and controlgroups after adjusting for any differencesthat existed prior to the start of the cam-paign) was 65 percent during the firstweek following the first exposure to anadvertisement.

Not only was there a sigrüficant impactwithin the first week following exposureto an advertisement—low click ratesnotwithstanding—but past the first week,there was significant lift that would havebeen overlooked by relying on clicksor by using cookies to track consumerbehavior.

The effects of online display advertis-ing continued past the first week in whichthe advertising exposure occurred, with

3.5%

2.1%

í% Lift: 65.0%^ '

1 ^ ^ ^

Week of FirstExposure

5.8%

4.8%

3.9%

1 1[%Uft: 53.8%] {% Lift: 49.1%]

1 ^ ^ ^ 1 1

Weeks 1-2 after Weeks 1-3 after \First Exposure First Exposure

• Control Test

6.6%1

4.5%•^% Lift: 45.7%]

A/eeks 1-4 afterFirst Exposure

Figure 2 Advertiser Site Reach

Weeks 1-4 after First Exposure

Average, N = 1394.5%

6.6%% Lift: 46%A Lift: 2.1%

Automotive. N = 38

Finance, N = lQ

CPG and Restaurant, N = 10

Retail and Apparel, N = 21

Media and Entertainment, N = 24

Electronics and Software, N = 14

Travel, N = 9

0.9% I % Lift: 114%1.9% A Lift: 1.0%

1.3% % Lift: 86%2.3% A Lift: 1.1%

0.6% % Lift: 77%1.1% A Lift: 0.5%

9.1%13.8%

% Lift: 52%A Lift: 4.7%

7.0% % Lift: 42%10.0% A Lift: 2.9%

5.8% % Lift: 25%7.2% A Lift: 1.5%

4.8% % Lift: 21%5.8% A Lift: 1.0%

I Control Test

Figure 3 Advertiser Site Reach by Industry

1 3 6 JQUmiHL Oí HDUEßllSlOB June 2009

HOW ONLINE ADVERTISING WORKS

the higgest difference in site visitation be-

tween the control and test group occur-

ring closest to the initial exposure (see

Figure 2).

These lifts varied greatly across indus-

tries, with Automotive advertisements gen-

erating the greatest percent lift in visiting

to the advertiser site among the catego-

ries studied. It also is the industry with

the smallest base values, however, with

advertisements that typically refer users

to highly specific auto-model websites. In

general, industries where baseline visit-

ing to the advertiser site is low generated

the highest percent lift. But, even where

site visitation is high, there were substan-

tial (20-50 percent) increases in site visi-

tation caused by Ihe display campaigns; it

is clear, therefore, that lift is not simply

being caused by low site-visitation levels.

The Retail and Apparel (+4.7 points).

Media and Entertainment {+3.0 points),

and Electronics and Software (+1.4 points)

industries generated the greatest absolute

increase in reach lift.

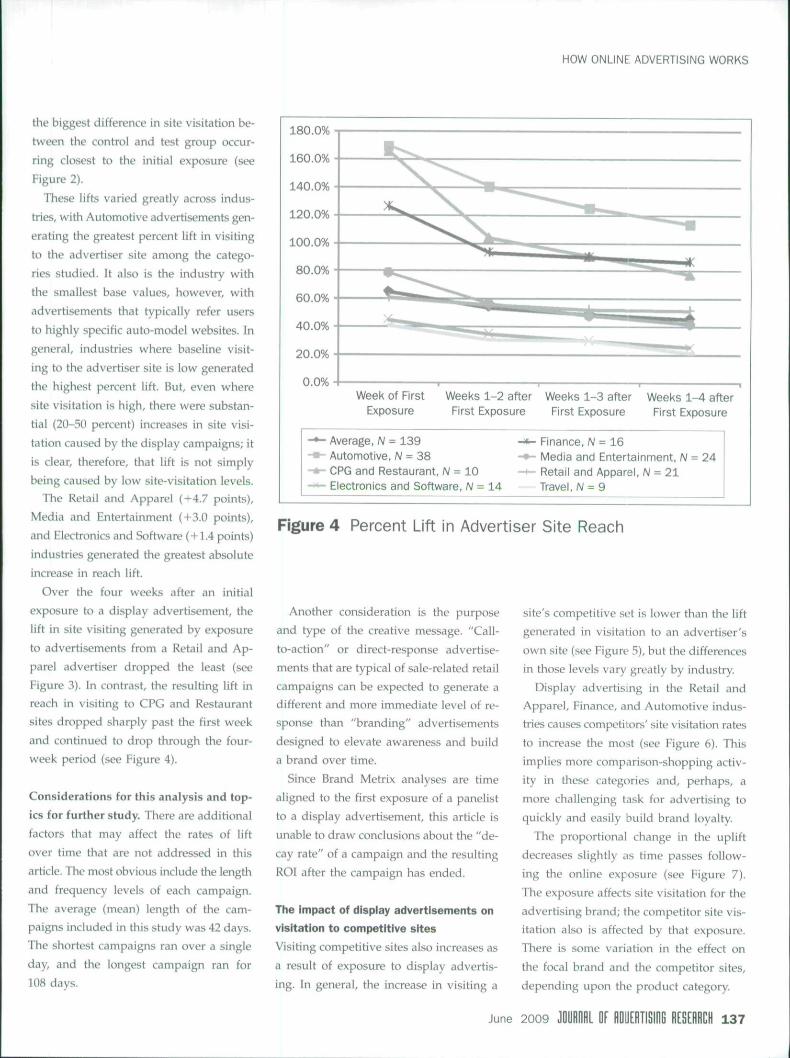

Over the four weeks after an initial

exposure to a display advertisement, the

lift in site visiting generated by exposure

to advertisements from a Retail and Ap-

parel advertiser dropped the least {see

Figure 3). In contrast, the resulting lift in

reach in visiting to CPG and Restaurant

sites dropped sharply past the first week

.ind continued to drop through the four-

week period (see Figure 4).

Considerations for this analysis and top-

ics for further study. There are additional

factors that may affect the rates of lift

over time that are not addressed in this

article. The most obvious include the length

and frequency levels of each campaign.

The average (mean) length of the cam-

paigns included in this study was 42 days.

The shortest campaigns ran over a single

day, and the longest campaign ran for

108 days.

180.0%

160.0%

20.0%

0.0%Week of First Weeks 1-2 after Weeks 1-3 after Weeks 1-4 after

Exposure First Exposure First Exposure First Exposure

- ^ Average, iV = 139•«- Automotive, N = 38-•*- CPG and Restaurant, N = 10— Electronics and Software, N =

Finance. W = 16Media and Entertainment, N = 24Retail and Apparei, N = 21Travel, N = 9

Figure 4 Percent Lift in Advertiser Site Reach

Another consideration is the purposeand type of the creative message. "Call-to-action" or direct-response advertise-ments that are typical of sale-related retailcampaigns can be expected to generate adifferent and more immediate level of re-sponse than "branding" advertisementsdesigned to elevate awareness and builda brand over time.

Since Brand Metrix analyses are timealigned to the first exposure of a panelistto a display advertisement, this article isunable to draw conclusions about the "de-cay rate" of a campaign and the resultingROI after the campaign has ended.

The impact of display advertisements on

visitation to competitive sites

Visiting competitive sites also increases as

a result of exposure to display advertis-

ing. In general, the increase in visiting a

site's competitive set is lower than the liftgenerated in visitation to an advertiser'sown site (see Figure 5), but the differencesin those levels vary greatly by industry.

Display advertising in the Retail andApparel, Finance, and Automotive indus-tries causes competitors' site visitation ratesto increase the most (see Figure 6). Thisimplies more comparison-shopping activ-ity in these categories and, perhaps, amore challenging task for advertising toquickly and easily build brand loyalty.

The proportional change in the upliftdecreases slightly as time passes follow-ing the online exposure (see Figure 7).The exposure affects site visitation for theadvertising brand; Ihe competitor site vis-itation also is affected by that exposure.There is some variation in the effect onthe focal brand and the competitor sites,depending upon the product category.

June 2009 M M l OF fiOOEflTISIIlG RESÍñflCH 1 3 7

HOW ONLINE ADVERTISING WORKS

16.6%14.9%

12.Í13.5%

12.1%

9.7% 10.3%

7.7% LWeek of First

ExposureWeeks 1-2 after

First ExposureWeeks 1-3 after

First ExposureWeeks 1-4 afterFirst Exposure

I Control Test

Figure 5 Competitive Site Reach

10.0%

0.0%Week of First

ExposureWeeks 1-2 afterFirst Exposure

Weeks 1-3 afterFirst Exposure

Weeks 1-4 afterFirst Exposure

Average, N = 117Automotive. N = 40CPG and Restaurant, N = 7Electronics and Software, N = 16

Finance, N = lAMedia and Entertainment. N = 12Retail and Apparel, N = 16Travel, N = 6

Figure 6 Percent Lift in Competitive Site Reach

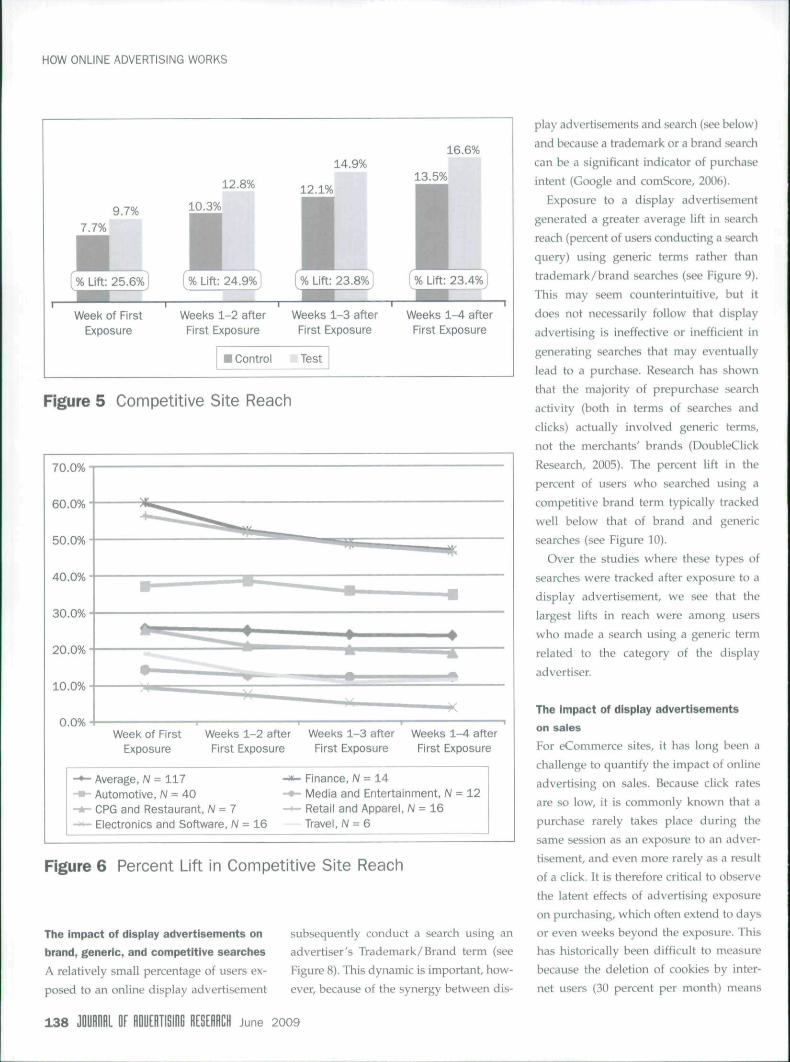

The impact of display advertisements on

brand, generic, and competitive searches

A relatively small percentage of users ex-posed to an online display advertisement

subsequently conduct a search using anadvertiser's Trademark/Brand term (seeFigure 8). This dynamic is important, how-ever, because of the synergy between dis-

play advertisements and search (see below)

and because a trademark or a brand search

can be a significant indicator of purchase

intent (Google and comScore, 2006).

Exposure to a display advertisement

generated a greater average lift in search

reach (percent of users conducting a search

query) using generic terms rather than

trademark/brand searches (see Figure 9).

This may seem counterintuitive, but it

does not necessarily follow that display

advertising is ineffective or inefficient in

generating searches that may eventually

lead to a purchase. Research has shown

that the majority of prepurchase search

activity (both in terms of searches and

clicks) actually involved generic terms,

not the merchants' brands (DoubleClick

Research, 2005). The percent lift in the

percent of users who searched using a

competitive brand term typically tracked

well below that of brand and generic

searches (see Figure 10).

Over the studies where these types of

searches were tracked after exposure to a

display advertisement, we see that the

largest lifts in reach were among users

who made a search using a generic term

related to the category of the display

advertiser.

The impact of display advertisements

on sales

For eCommerce sites, it has long been achallenge to quantify the impact of onlineadvertising on sales. Because click ratesare so low, it is commonly known that apurchase rarely takes place during thesame session as an exposure to an adver-tisement, and even more rarely as a resultof a click. It is therefore critical to observethe latent effects of advertising exposureon purchasing, which often extend to daysor even weeks beyond the exposure. Thishas historically been difficult to measurebecause the deletion of cookies by inter-net users (30 percent per month) means

1 3 8 JOUHUHL or flDUERTISHlG fttSEHRCII June 2 0 0 9

HOW ONLINE ADVERTISING WORKS

200.0%

150.0%

100.0%

50.0%

0.0%

200.0%

150.0%

100.0%

50.0%

0.0%

70.0%60.0%50.0%40.0%30.0%20.0%10.0%

0.0%

Average

A 39%29%

25% 22%

Week1

Week1-2

Week Week1-3 1-4

70.0%60.0%50.0%40.0%30.0%20.0%10.0%

0.0%

Retail and Apparel

A 4% 4% 6%Week

1Week Week Week

1-3 1-4

Automotive

i.132%-102%

79%

Week1

Week1-2

Week1-3

Week1-4

140.0%120.0%100.0%

80.0%60.0%40.0%20.0%

0.0%

Finance Travei

6C%

41.%

Week1

Week1-2

Week Week1-3 1-4

140%

Food

: ^

and

3%*

CPG Media and Entertainment Eiectronics and Software

Week1

Week1-2

Week1-3

Week1-4

Week1

Week1-2

Week Week1-3 1-4

Advertiser Comp Set Points Difference

Figure 7 Advertiser versus Competitive Set Percent Lift in Site Reach

0.3%

0.2%

%üf t : 52.3%]

r ^Week of First

Exposure

0.5%

n(% Lift: 46.0%'

T ^ rWeeks 1-2 after

First Exposure

• Oontrol

0.7%

0.5%

1[% Lift: 40.3%]

— ^ 1Weeks 1-3 after

First Exposure

Test

0.9%

0.6%

[% Lift; 38.1%]

1 ^ 1Weeks 1-4 after

First Exposure

Figure 8 Percent Making a Trademark or Brand Search

that cookies cannot be used to accuratelytrack the behavior of computers over time(comScore Press Release, 2007).

For bricks-and-mortar retailers, the chal-lenge extends even further, to the necessityof quantifying the effects of online adver-tising on offline sales. The magnitude ofthe lift in offline sales generated by onlineadvertising is significant and would cer-tainly not be captured by a pay-per-clickcookie-based measurement approach. Thecurrent lack of visibility into offline pur-chasing consistently leads to dramatic un-derestimation of display advertising ROL

In examining the impact of displayadvertisements on buyer penetration

June 2 0 0 9 JQUROIJL OF HDUERTiSiHG RESEHHCIJ 1 3 9

HOW ONLINE ADVERTISING WORKS

0.6%

0.3%

[% Lift: 68.7%J

r — ^Week of First

Exposure

0.9%

0.6%

[% Lift: 58.0%)

1 ^ r

Weeks 1-2 afterFirst Exposure

• Control

1.3%

0.8%••(%Üft:52.7%J

— ^ ^ ^ — — 1

Weeks 1-3 afterFirst Exposure

Test

1.5%

1.0%

H[% Lift: 47.4%J

1 ^ ,

Weeks 1-4 afterFirst Exposure

Figure 9 Percent Making a Generic Search

1.2% ^'^°'^°

, ^ .%L in : 13.6%

••r—1 — ^

Week of FirstExposure

2.1%1.9%

1,^M ,%Lift: 10.2%

• • 1—1 ^ rWeeks 1-2 afterFirst Exposure

• Control

2.7%2.4%

IIr ^ .[%Lift: 10.5%J

— ^ 1Weeks 1-3 after

First Exposure

Test

3.2%2.9%

1I( % Lift: 9^9%)

1 ^ rWeeks 1-4 afterFirst Exposure

Figure 10 Percent Making a Competitive Search

(see Figures 11 and 12), we see that the

percentage lift is much higher online

than offline, with an average onUne

buyer penetration lift of 42.1 percent,

compared to a lift of 10.1 percent in

offline buyer penetration. However,

because the bases are larger for offline

purchasing, the net impact in new or

additional buyers is larger offline than

online.

Per-buyer purchasing both on- and off-

line show minimal gains (see Figure 13).

The synergistic Impact of display and

search advertisements on saies

In this series of studies, we examined

the impact of search and display sepa-

rately as well as in combination. The im-

pact of search advertisements alone on

consumers' buying behavior was found

to be clearly greater than that of display

advertisements alone. This is true both

in terms of the advertisements' impact

on online buying as well as the impact

on offline sales. This is not surprising

(% Lift: 42.1%)

1.0% ^-^^

^ - ^ r-

Online

• Control

(%

JLift: 10.1%)

. , «

Offline

Test

Figure H Buyer Penetration

(% Lift: 27.1%)

$994$1,263. ^ r-

Online

• Control

(%

$9

JLift: 16.6%)

$11.550,905•L

OfflineTest

Figure 12 Dollars perThousand Exposed

( % Lift: 1.4% )

$105 $106

Online

• Control

' % Lift: 3.5% )

$130$134

Offline

Test

Figure 13 Dollars per Buyer

because consumers responding to search

advertisements are much more likely to

be "in the market" for buying the adver-

tised product.

1 4 0 JOÜRflfiL OF flOyERTISIflG (lESEflflCH June 2 0 0 9

HOW ONLINE ADVERTiSiNG WORKS

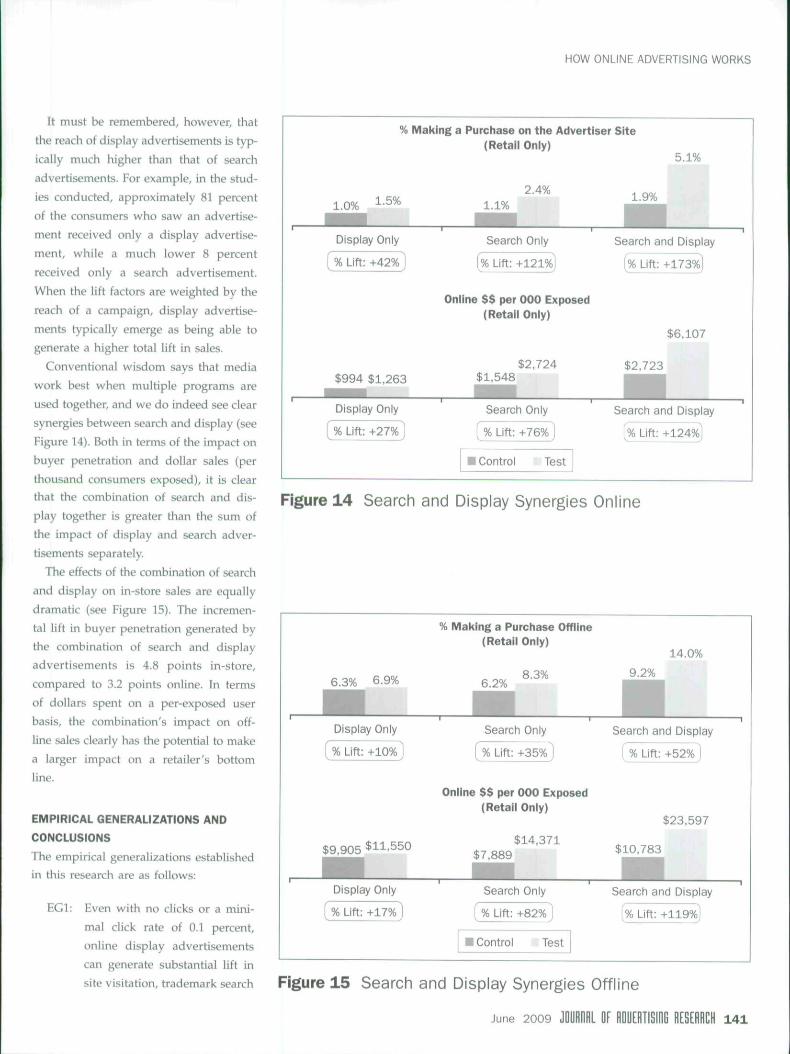

It must be remembered, however, that

the reach of display advertisements is typ-

ically much higher than that of search

advertisements. For example, in the stud-

ies conducted, approximately 81 percent

of the consumers who saw an advertise-

ment received only a display advertise-

ment, while a much lower 8 percent

received only a search advertisement.

When the lift factors are weighted by the

reach of a campaign, display advertise-

ments typically emerge as being able to

generate a higher total lift in sales.

Conventional wisdom says that media

work best when multiple programs are

used together, and we do indeed see clear

synergies between search and display (see

Figure 14). Both in terms of the impact on

buyer penetration and dollar sales (per

thousand consumers exposed), it is clear

that the combination of search and dis-

play together is greater than the sum of

the impact of display and search adver-

tisements separately.

The effects of the combination of search

and display on in-store sales are equally

dramatic (see Figure 15). The incremen-

tal lift in buyer penetration generated by

the combination of search and display

advertisements is 4.8 points in-store,

compared to 3.2 points online. In terms

of dollars spent on a per-exposed user

basis, the combination's impact on off-

line sales clearly has the potential to make

a larger impact on a retailer's bottom

line.

EMPfRICAL GENERALIZATIONS AND

CONCLUSIONS

The empirical generalizations establishedin this research are as follows:

EGl: Even with no clicks or a mini-

mal click rate of 0.1 percent,

online display advertisements

can generate substantial lift in

site visitation, trademark search

%

1.0% ^-^^

Display Only

( % Lift: +42% )

$994 $1,263

Display Only

( % Lift: +27% )

Making a Purchase on the Advertiser(Retail Only)

2.4%1.1%

Search Only

(% Lift: +121%)

Online $$ per 000 Exposed(Retail Only)

$2,724$1,548

Search Only

[ % Lift: +76% ]

• Control Test

Site

5.1%

1.9%

Search and Display

[% Lift: +173%]

$6,107

$2,723

Search and Display

[% Lift; +124%]

Figure 14 Search and Display Synergies Online

% Making a Purchase Offline(Retail Only)

14.0%

6.3% 6.9% 6.2%8.3% 9.2%

Display Only Search Only

% Lift:+10% 1 i% Lift:+35%

Search and Display

1 % Lift: +52%

Online $$ per 000 Exposed(Retail Oniy)

$23,597

$9,905 $11,550$14,371

$7,889 $10,783

Display Only

% Lift: +17%

Search Only

% Lift: +82%

Search and Display

Lift: +119%

I Control Test

Figure 15 Search and Display Synergies Offline

June 2009 L DF eDUERTISlOG RESeHRCH 1 4 1

HOW ONLINE ADVERTiSING WORKS

Among 139 studies in which consumers' oniine

behavior was monitored foiiowing exposure to a dispiay

advertisement, the average iift in the number of

visitors to the advertiser site was 46 percent.

queries, and increases in both

online and offline sales.

EG2: For retailers, search advertising

generally causes a greater lift in

sales among those exposed to

search advertisements than an

online display advertising cam-

paign does among those ex-

posed to the display campaign,

but the higher reach of display

advertising campaigns typically

means that they are able to gen-

erate larger overall sales in-

creases than search campaigns.

EG3: Overlaying a retailer's display

advertising campaign on a

search campaign produces syn-

ergy, with the effect of the

combination being greater than

the sum of the two separate

campaigns.

Our results show that a low level of

clicks does not mean that online display

advertising is having no effect. By exam-

ining 139 online display advertising cam-

paigns conducted across a variety of

vertical industries {including Retail and

Apparel, Travel, CPG and Restaurant, Fi-

nance, Automotive, Consumer Electronics

and Software, and Media and Entertain-

ment), we show that display advertising,

despite a lack of clicks, can have a signif-

icant positive impact on;

• visitation to the advertiser's website (lift

of at least 46 percent over a four-week

period);

• the likelihood of consumers conduct-

ing a search query using the advertis-

er's branded terms (a lift of at least 38

percent over a four-week period);

• consumers' likelihood of buying the ad-

vertised brand online (an average 27

percent lift in online sales);

• consumers' likelihood of buying at the

advertiser's retail store (an average lift

of 17 percent).

In the Retail category, it is also clear

that while the lift in sales from a display

advertisement is lower than the lift from

a search advertisement, the reach of a

display campaign is typically far higher

than that of a search campaign. When

the sales lift is weighted by reach, dis-

play campaigns generally outperform

search campaigns. The combination of a

display and search campaign, however,

delivers substantial synergy, with the sales

lift from the combined strategy being

greater than the sum of the individual

components,

GiAN M. FuLGONi is the executive chairman and co-

founder of comScore Inc. (NASDAQiSCOR). a global

leader in measuring the digital world,

MARIE PAUUNE MORN currently holds the position of

director of product management at comScore, Inc.

She joined comScore in 2001 and has held various

positions in product management and marketing

solutions.

REFERENCES

COMSCORE PRESS RELEASE. "Cookie-Based

Counting Overstates Size of Web Site Audi-

ences," April 16, 2007: [URL: http://www.

comscore.com/press/release.asp?press=1389I.

DOUBLECLICK RESEARCH. "Search Before the

Purchase: Understanding Buyer Search Activ-

ity as it Builds to Online Purchase," February

2005: [URL: http://www.doubleclick.com/

insight/pdfs/searchpurchase_0502.pdf], ac-

cessed November 1, 2008.

EMARKETER. "The Latest Ad Click Count,"

March U, 2009: [URL: http://www.emarketer.

com/Article.aspx?id = 1006969].

GOOGLE AND COMSCORE. "comScore Press

Release Study Confirms the Importance of

Search in Influencing Offline Buying," March

21, 2006: [URL: http://www.comscore.com/

press/release.asp?press=796].

STARCOM MEDIAVEST GROUP PRESS RELEASE.

"New Study Shows that Hea\y Clickers Dis-

tort Reality of Display Advertising Click-

Through Metrics," February 12, 2008: [URL:

http://www.smvgroup.com/news_popup_flash.

asp?pr=1643].

1 4 2 JDUROHL OF HDUEHÎI510G HESEaRCIJ June 2 0 0 g