which way for working capital - banking with citi | citi. · pdf file ·...

TRANSCRIPT

Which Way for Working Capital

Statement of Confidentiality and Usage Restrictions

This document contains trade secrets and other information that is company sensitive, proprietary, and confidential, the disclosure of which would provide a competitive advantage to others. As a result, the reproduction, copying, or

redistribution of this document or the contents contained herein, in whole or in part, for any purpose is strictly prohibited without the prior written consent of REL. © 2011 The Hackett Group, Inc. All rights reserved. World-Class Defined and

Enabled.

Daniel Windaus

Senior Director &

Head of Private Equity Advisory,

REL Europe

+44 7919 016116

Page 3

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

REL is the only global consulting firm dedicated exclusivelyto Working Capital management

Specialists in Working Capital focused exclusively on

three critical end-to-end processes:– Forecast-to-Fulfill (Inventory)

– Customer-to-Cash (Receivables)

– Source-to-Settle (Payables)

Unmatched 30 year track record

More than 400 working capital engagements

Project experience in more than 60 countries

10 offices across America, Asia and Europe

Unique implementation focus and capability

More than >25bn released NWC in the last 10 years

Page 4

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

REL has delivered Working Capital improvements across many industries for over 400 clients

Page 5

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

REL is the most published firm on Working Capital Management

Managing NWC during the recovery

2011 Working Capital Survey

The shift in gravity towards

Developing Markets

Page 7

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Page 8

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

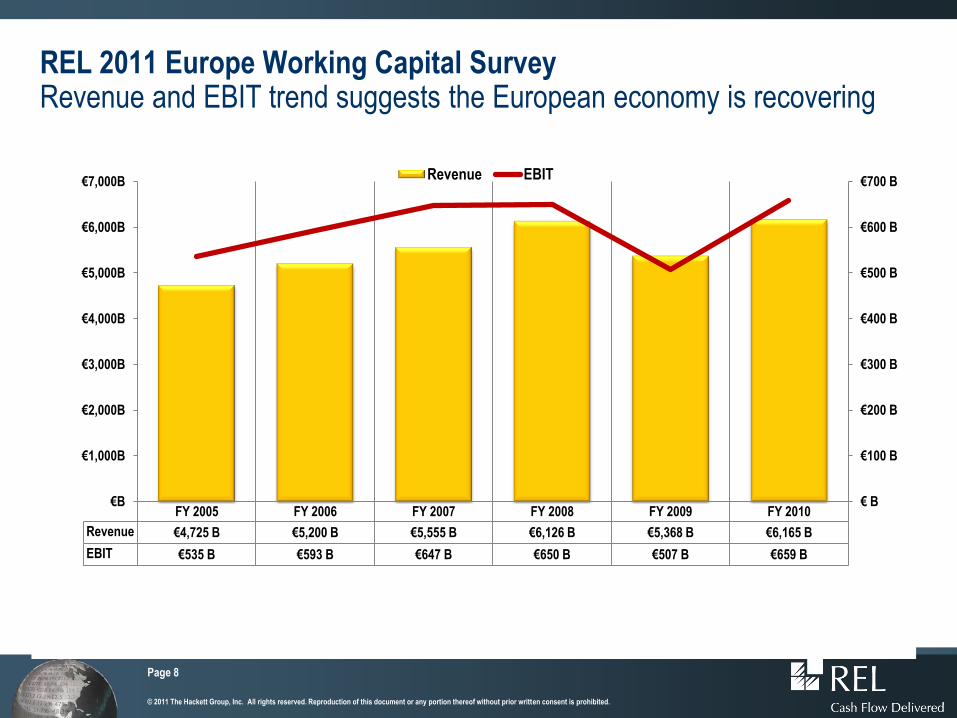

REL 2011 Europe Working Capital SurveyRevenue and EBIT trend suggests the European economy is recovering

FY 2005 FY 2006 FY 2007 FY 2008 FY 2009 FY 2010

Revenue €4,725 B €5,200 B €5,555 B €6,126 B €5,368 B €6,165 B

EBIT €535 B €593 B €647 B €650 B €507 B €659 B

€ B

€100 B

€200 B

€300 B

€400 B

€500 B

€600 B

€700 B

€B

€1,000B

€2,000B

€3,000B

€4,000B

€5,000B

€6,000B

€7,000BRevenue EBIT

Page 9

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

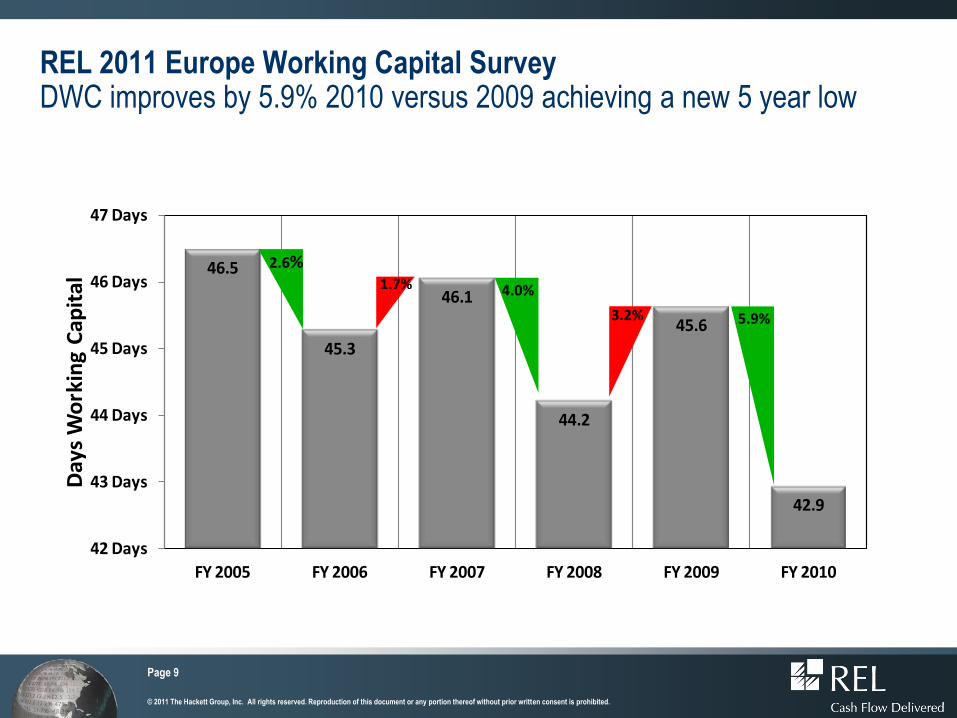

REL 2011 Europe Working Capital SurveyDWC improves by 5.9% 2010 versus 2009 achieving a new 5 year low

46.5

45.3

46.1

44.2

45.6

42.9

42 Days

43 Days

44 Days

45 Days

46 Days

47 Days

FY 2005 FY 2006 FY 2007 FY 2008 FY 2009 FY 2010

Day

s W

ork

ing

Cap

ital

5.9%3.2%

4.0%1.7%

2.6%

Page 10

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

In 2010 the Working Capital improvement is driven by the asset side

DWC DSO DIO

Days Working Capital

2008 20102009

44.2

45.6

42.9

5.9%3.2%

Days Sales Outstanding

2008 20102009

50.8

53.8

52.2

6.1% 3.0%

Days Inventory On Hand

2008 20102009

37.0

38.8

37.6

4.9% 2.9%

Page 11

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Who contributed to the DSO improvement? 59% of industries and 49.7% of companies improved their DSO performance 2010 versus 2009

DSO

€107 B

€108 B

€118 B

€121 B

€159 B

€190 B

€206 B

€212 B

€258 B

€792 B

Chemicals

Multi-Utilities

Pharmaceuticals

Construction and Engineering

Metals and Mining

Electric Utilities

Food Products

Food and Staples Retailing

Automobiles

Oil, Gas and Consumable Fuels

EU 1000 - DSO Improvers By Industry and Revenue

9%

10%

12%

8%

16%

12%

9%

19%

17%

10%

Chemicals

Multi-Utilities

Pharmaceuticals

Construction and Engineering

Metals and Mining

Electric Utilities

Food Products

Food and Staples Retailing

Automobiles

Oil, Gas and Consumable Fuels

EU 1000 - DSO Improvers Average YOY% Improvement - By Industry

23%

7%

6%

6%

5%

5%

3%

3%

3%

3%

% Improvers Revenue

65%

Page 12

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Who contributed to the DIO improvement? 53% of industries and 51.2% of companies improved their DIO performance 2010 versus 2009

DIO

€105 B

€115 B

€123 B

€128 B

€180 B

€188 B

€204 B

€293 B

€342 B

€714 B

Food and Staples Retailing

Food Products

Machinery

Construction and Engineering

Multi-Utilities

Pharmaceuticals

Metals and Mining

Automobiles

Electric Utilities

Oil, Gas and Consumable Fuels

EU 1000 - DIO Improvers By Industry and Revenue

4%

14%

13%

15%

21%

14%

15%

12%

14%

21%

Food and Staples Retailing

Food Products

Machinery

Construction and Engineering

Multi-Utilities

Pharmaceuticals

Metals and Mining

Automobiles

Electric Utilities

Oil, Gas and Consumable Fuels

EU 1000 - DIO Improvers Average YOY% Improvement - By Industry

21%

10%

8%

6%

5%

5%

4%

4%

3%

3%

% Improvers Revenue

69%

Page 13

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

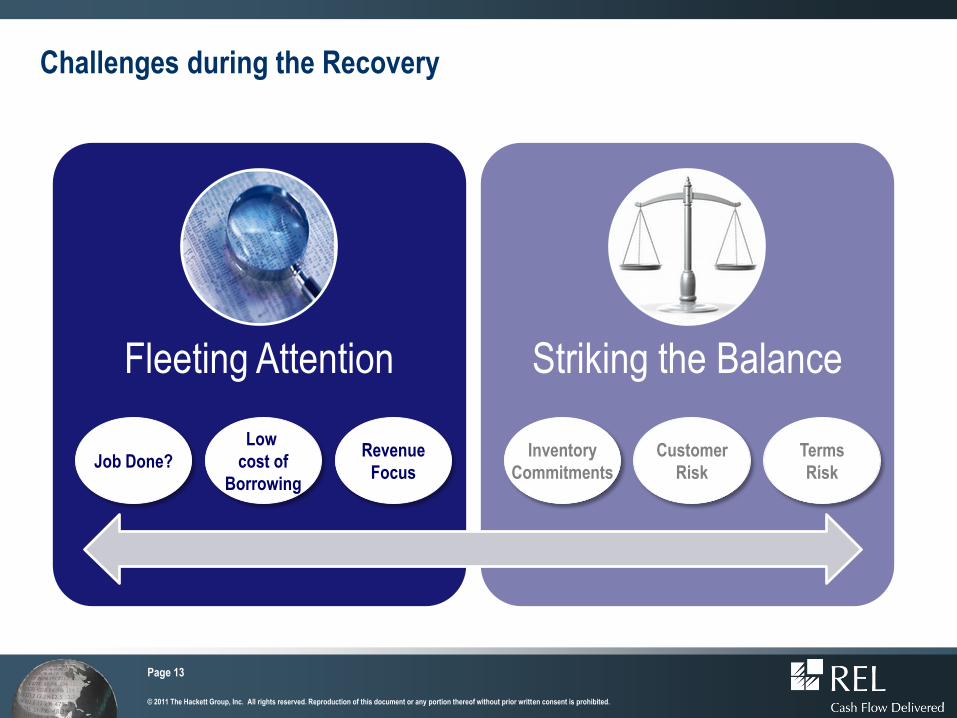

Challenges during the Recovery

Fleeting Attention Striking the Balance

Customer

Risk

Terms

Risk

Inventory

Commitments

Low

cost of

Borrowing

Revenue

FocusJob Done?

Page 14

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Working capital management is all about trade-offs and is as necessary in a recovery as it is in a recession….

Forecasting Lead TimesOrder

QuantitiesPurchase

CostCustomer

Service

Product

RangePayment

Terms

Cash, Cost, Service & Risk

Cost

Order Quantity

Inventory

Service Level

Terms

Risk

Cost

Terms

Page 15

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

BRICKM Overview

The shift in gravity towards

Developing Markets

• Contributed 1/3 of world GDP growth over the last 10 years

• Trend expected to regain momentum and continue

Page 16

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Notwithstanding the economic correction of 2009, EU businesses have significant and increasing trade exposure to BRICMK economies

0

100

200

300

400

500

600

700

800

2005 2006 2007 2008 2009

Exports to Russia Exports to ChinaExports to India Exports to BrazilExports to Mexico Exports to S Korea

0

100

200

300

400

500

600

700

800

2005 2006 2007 2008 2009

Imports to Russia Imports to ChinaImports to India Imports to BrazilImports to Mexico Imports to S Korea

What does this mean for Net Working Capital of European businesses ?

Page 17

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Across the BRICMK, Total Working Capital consumption is in line with that of European based companies

52

3637

44

38

51

4343

IndiaRussiaBrazilBRICMKEU China Mexico

+1(+2%)

-6(-14%)

-5(-12%)

0(0%)

DW

C

North Korea

Page 18

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Sourcing from Emerging markets is typically focussed on price rather than cash advantage, potentially impacting European DPOs

50

42

32

42

32

56

42

5247

Mexico

DSO

Russia

DSO

Republic

of Korea

DSO

-20

BRICM

K DSO

Brazil

DSO

EU

DSO

India

DSO

China

DSO

-10-10

(-19%)-20

EU

DPO

+$168bn

+40%

EU Imports from

BRICMK markets, 2005

v 2009

+$6.7bn

+23%

+$4 bn

+34%

+$12bn

+50%

+$103bn

+53%

+$2.5bn

+23%

$3.24bn

+8%

Page 19

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Five year development in BRICMK DSO

42

44

39

42 42 42

37 Days

38 Days

39 Days

40 Days

41 Days

42 Days

43 Days

44 Days

45 Days

2005 2006 2007 2008 2009 2010

Page 20

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

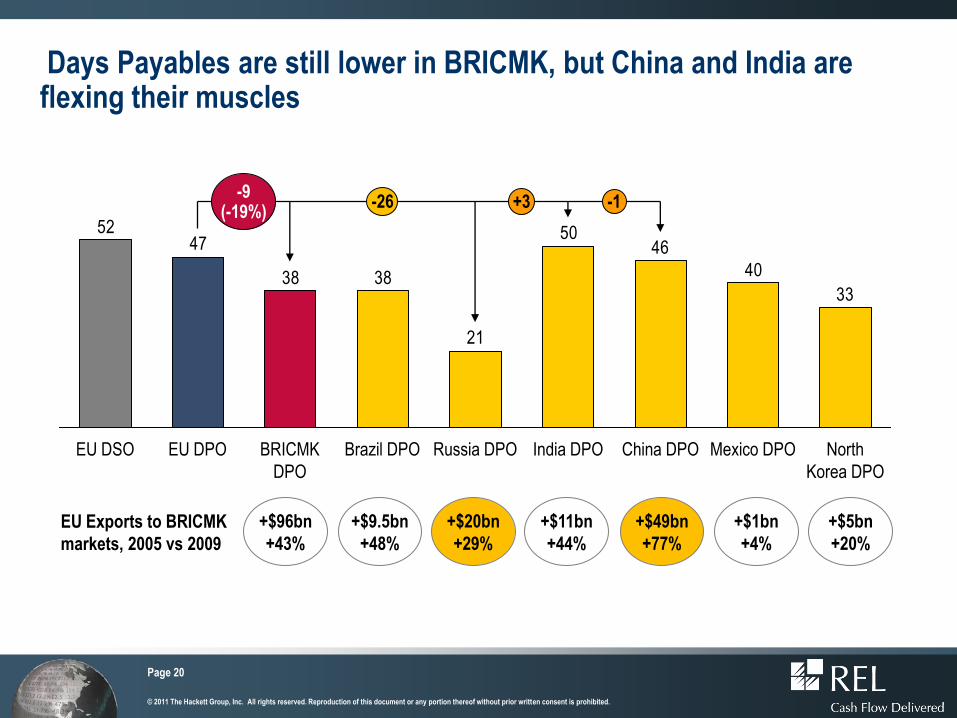

Days Payables are still lower in BRICMK, but China and India are flexing their muscles

33

40

4650

21

3838

4752

India DPORussia DPOBrazil DPOBRICMK

DPO

EU DPOEU DSO China DPO Mexico DPO

+3 -1-26-9

(-19%)

North

Korea DPO

+$96bn

+43%

EU Exports to BRICMK

markets, 2005 vs 2009

+$9.5bn

+48%

+$20bn

+29%

+$11bn

+44%

+$49bn

+77%

+$1bn

+4%

+$5bn

+20%

Page 21

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

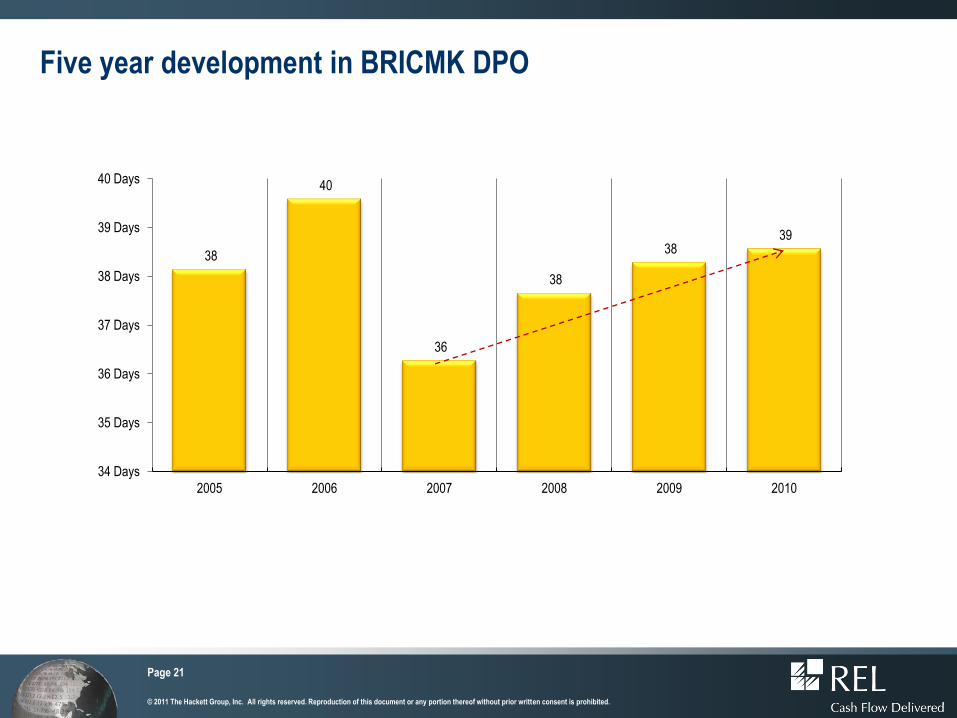

Five year development in BRICMK DPO

38

40

36

38

38 39

34 Days

35 Days

36 Days

37 Days

38 Days

39 Days

40 Days

2005 2006 2007 2008 2009 2010

Page 22

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Supply Chain Challenges Inventory Challenges Risk Challenge

Increased exposure to BRICMKs results in NWC challenges

Uncertainty

Increased NWC

Buffers

• Longer lead times

• Decreased reaction potential

• Longer times to deliver (transit)

• Increase to cover uncertain

demand patterns

• Increase in Safety stock

• Potential increase in SLOBS

• Ability to forecast

• Political Risk (Middle East)

• Infrastructure Risk (power

cuts, Road closures – India)

• Currency

Page 23

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Strategies to address the NWC challenge

•

• Bridging the terms gap

• Bills of Exchange

• Move to open account with normal terms – why be different

• Understand any government legislation

• Partnership approach

• Regular communications

• Understand the culture

Supplier Communi-

cation

Payment Terms

Inventory Management

Supply Chain Financing • Rebalance flexibility and

safety stock triggers

• Balance cost of transport

with cost of inventory

• Minimise order cycle times

using electronic scheduling

• Use bonded warehouses

Page 24

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

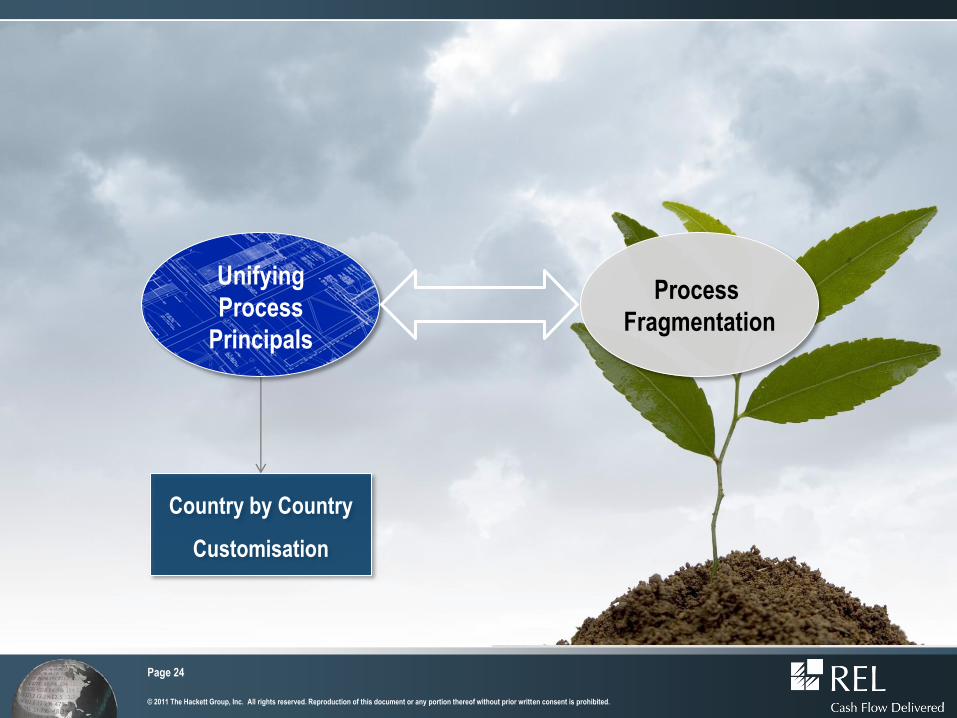

BRICKM Overview

Country by Country

Customisation

Unifying

Process

Principals

Process

Fragmentation

Page 25

© 2011 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

BRICKM Overview

Thank You