where america goes to work - building owners and … · where america goes to work: ... cassidy...

TRANSCRIPT

where america goes to work:The ConTribuTion of

offiCe building operaTions To The eConomy, 2012

Prepared for the Building Owners and Managers Association (BOMA) International

by Stephen S. Fuller, PhDDwight Schar Faculty Chair and University Professor,

Director, Center for Regional Analysis, George Mason University

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

1

table of contents

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

National Economic Impacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Research Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Economic Impacts of Operating Expenditures in 94 Office Markets Served by BOMA Local Associations . . . . .10

Metropolitan-Level Impact of Office Operating Expenditures in Selected Areas, 2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

Direct and Indirect Jobs Impacts of Office Building Operations in 2011. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .16

Additional Economic Impacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17

Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18

Appendix A: Glossary of Terms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19

Appendix B: Office Market Inventory & Annual Operating Costs by State & Metropolitan Area for 93 BOMA Local Associations, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20

Appendix C: Direct and Indirect Jobs Associated with Operation Expenditures for Office Buildings in 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24

Appendix D: Economic Multipliers and Impact Calculations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28

Appendix E: Aggregate Economic Impact Multipliers for Building Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29

Appendix F: BOMA Local Association Territories Defined . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .33

ISBN# 978-0-9840153-4-4 Copyright © 2012 by Building Owners and Managers Association (BOMA) International. All rights reserved. No portion of this document may be reproduced without permission.

BOMA International 1101 15th Street, NW Suite 800 Washington, DC 20005

202.408.2662

www.boma.org

Copyright © 2012 by boMA internAtionAl . All rights reserved.

acknowledgements

legal notice

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

2

BOMA International wishes to extend its appreciation to those companies and individuals who contributed to the development of Where America Goes to Work: The Contribution of Office Building Operations to the Economy, 2012.

Building Owners and Managers Association International (“BOMA”) is a nonprofit corporation, incorporated in the State of Illinois, which is exempt from federal taxation under Section 501(c)(6) of the Internal Revenue Code, whose purposes include to actively and responsibly represent and promote the interests of the commercial real estate industry and disseminate education programs on the commercial real estate industry. This document was prepared by Dr. Stephen S. Fuller of George Mason University for BOMA to provide information to those in the commercial real estate industry and other interested parties about the economic impact of office building operations (including management, maintenance and repair, servicing, and utilities) in the ninety-three office markets served by BOMA local associations. Because the market boundaries of BOMA local associations are not always coterminous with the metro areas that they represent, the data presented in this document may differ according to the geographic areas in question.

BOMA publications are intended to provide current and accurate information, and are designed to assist readers in becoming more familiar with the subject matter covered. BOMA published this document for a general audience in accordance with all applicable laws, including the antitrust laws. Such publications are distributed with the understanding that BOMA does not render any legal, accounting, or professional advice. Use of this publication is voluntary and reliance on this document should be undertaken based on an independent review by the user. Infor-mation provided in this document is “as is” without warranty of any kind, either express or implied, including but not limited to the implied warranties of merchantability, fitness for a particular purpose, or freedom from infringe-ment. BOMA hereby disclaims all liability for any claims, losses, or damages in connection with use or application of this document.

This document is the sole and exclusive property of BOMA. Reproduction or redistribution in whole or in part without the express written consent of BOMA is prohibited.

CB Richard Ellis CoStar Group Inc. Joseph W. Markling Chair Elect, BOMA International CBRE Los Angeles, California

Copyright © 2012 by boMA internAtionAl . All rights reserved.

about the author

Professor Stephen S. Fuller, Ph.D joined the faculty at George Mason University in 1994 as Professor of Public Policy and Regional Development. In 2001, he was appointed University Professor and in 2002 he was named to the Dwight Schar Faculty Chair. He also serves as Director of the Center for Regional Analysis.

Prior to joining the George Mason University faculty, he served on the faculty at George Washington University for twenty-five years, including nine as Chairman of the Department of Urban Planning and Real Estate Development. Dr. Fuller received a B.A. in Economics from Rutgers University and his Doctorate in Regional Planning and Economic Development from Cornell University. He has authored more than 800 articles, papers, and reports in the field of urban and regional economic development

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

3

about boma international

The Building Owners and Managers Association (BOMA) International is an international federation of more than 100 local associations and affiliated organizations. Founded in 1907, its 16,500-plus members own or manage more than nine billion square feet of commercial properties. BOMA International’s mission is to enhance the human, intellectual and physical assets of the commercial real estate industry through advocacy, education, research, standards and information. On the Web at www.boma.org.

boma inTernaTional offiCers

Boyd R. ZoccolaChair & Chief Elected OfficerExecutive Vice PresidentHokanson Companies, Inc.

Joseph W. MarklingChair-ElectManaging Director, Strategic Accounts GroupCBRE

Richard W. Greninger, CPMVice ChairManaging PartnerCarr Properties

Rebecca B. Hanner, CPM, RPASecretary/TreasurerSenior Vice President/PrincipalCassidy Turley

Henry H. Chamberlain, APR, FASAE, CAEPresident & Chief Operating OfficerBOMA International

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

4

executive summary

The commercial real estate industry plays a significant role in the U.S. economy. Perhaps this is most obvious during the construction phase, as cranes dot the horizon, workers scramble across scaffolding and trucks deliver a seemingly endless stream of equipment and supplies. But the far larger—and longer lasting—impact actually comes after the ribbon cutting, when the significant annual operating expenses associated with office buildings help support the local economy’s vitality, create new jobs, generate personal income and contribute to the local tax base year after year.

Without question, the value of office buildings within their local markets—and as aggregated at the state and national levels—starts with development and construction expenditures. The economic impacts of these expendi-tures are substantial, but their duration is limited, lasting only from planning to groundbreaking to the ribbon cutting. But once completed, these office buildings represent a continuing and accumulating stream of expenditures to support their operations, with ongoing expenditures for management, maintenance and repair, building services and utilities. Combined, these continuing expenditures have a huge, positive effect on the many local businesses that provide contract-building services and, in turn, generate demand for a wide range of workers with differing educational levels and job skills.

Just how big is its impact? Consider the 9.9 billion square feet of commercial and government-owned office space located within the 94 markets served by the Building Owners and Managers Association (BOMA) International’s 93 local associations1 : combined, the space generated $79.7 billion in direct operating expenditures in 2011 to the benefit of workers and businesses within their host jurisdictions— enough to build One World Trade Center 20 times over.

How is this possible? Keep in mind that this annual spending is largely a function of the inventory of office space that continues to grow in dynamic markets in response to the economy’s continuing shift away from goods-producing jobs (steel, lumber, electronics) and into services-producing jobs (professional and business services such as health-care, education, financial, and legal). Inventory and expenditures also grow with the economy’s general expansion. And, even in a weak economy or during recessions, the expenditures associated with office building operations are not as cyclically sensitive as other segments of the economy, such as manufacturing, construction and retail trade.

The result is significant: BOMA’s 9.9 billion square feet of locally represented office space, and the $79.7 billion of direct operating expenditures generates additional economic impacts:

• For each dollar spent on office building operations, the national economy gained $2.57, with the result that $79.7 billion in annual operating expenditures contributed a total of $205.1 billion to the gross domestic product (GDP) in 2011—equivalent to the state of California’s annual budget;

• For each dollar spent on office building operations, workers in the United States realized an increase of $0.76 in personal earnings, generating a total of $61.0 billion in new earnings for workers residing within these 94 office market areas and respective state economies in 2011;

• For each $1 million in expenditures for office building operations, 19.6 jobs were supported nationwide. As a result, $79.7 billion in annual operating expenditures supported a total of 1,561,517 indirect jobs across all sectors of the national economy in 2011—about the same number employed by McDonald’s worldwide—in addition to an estimated 2.2 million more jobs directly related to the on-site management and operations of these office buildings; and

• The 9.9 billion square feet of commercial and government-owned office space located in the 94 markets served by BOMA’s 93 local associations provided workspace for an estimated 44.3 million office jobs. Their $116,200 per office worker contribution to GDP occurs in this office space and is supported by building and management services and paid for by these operating expenditures. Additionally, their presence within these office buildings’ host jurisdictions has their own significant annual economic and fiscal benefits accruing locally, at the state level and nationwide.

1 BOMA Local Association Carolinas/West Virginia encompasses two distinct metropolitan markets, both worth mentioning in this report: “Charlotte, Greensboro, Winston Salem (Triad)” and the rest of “Carolinas/West Virginia”. Additionally, BOMA/Raleigh-Durham is its own distinct market and BOMA Local Association.

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

5

The eConomiC impaCTs of offiCe building operaTing expendiTures in 94 markeTs served by boma loCal assoCiaTions, 2009

Total Office Space (SF) 9,908,990,533 Average Annual Operating Cost (SF) $8.05Total Building Operating Expenditures $79,738,709,975Impacts on US Economy Contribution to GDP $205,058,622,205 New Personal Earnings $60,976,280,704 Direct Jobs Supported 2,229,523 Indirect Jobs Supported 1,561,517

Sources: BOMA International, CoStar Group Inc., GMU Center for Regional Analysis

The benefits to local jurisdictions from office building operating expenditures don’t stop there: one must also add in secondary benefits resulting from how the money generated by building operations is spent—and re-spent—through the local, state and national economies. Whether that means supporting an in-building dry cleaner, hailing a taxi at the curb, hiring an attorney from the law firm located on the top floor, taking business associates out to lunch at a nearby restaurant, or grabbing a soda from a sidewalk vendor, it all goes toward supporting significant job growth directly and indirectly, and helping generate new personal earnings that further stimulates the economy.

These direct and indirect economic impacts are important because of their magnitude, dependability and long-term growth pattern.

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

6

introduction

In 2011, there were an estimated 42.9 billion square feet of office, industrial and retail building space in the United States (CoStar Group Inc.). While commercial building construction generates important economic activity and job growth, the annual operating expenditures to manage and maintain the occupied office building inventory represents a significant and continuous contribution to the nation’s economic vitality. Consider for a moment the continuing impact that 42.9 billion square feet of space can generate in just one year via annual operating expenditures, and then multiply that over the course of the buildings’ lifetimes. Then take into account the impact that recurring annual spending can have on the economies within which these buildings are located.

In order to better document the magnitude and significance of these annual operating expenditures, BOMA International commissioned an analysis of the expenditures for office building operations in the 94 markets served by its 93 local associations. This analysis included all office buildings—inclusive of tenant-occupied buildings, buildings owned by their occupants and government-owned office buildings. The findings of this research clearly demonstrate the importance of office building operations as a source of income and employment, which benefits the respective buildings’ local and state economies.

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

7

national economic impacts

In 2011, the 9.9 billion square feet of commercial office space existing in the 94 market areas encompassing BOMA’s 93 local associations generated annual expenditures totaling $79.7 billion. This spending supported local employment and business activities associated directly with these buildings in four broad categories and average proportions: utilities (30%), repairs and maintenance (23%), management (26%), and building services (21%). These operating expenditures averaged $8.05 per square foot across all 94 office markets, reflecting a wide range of costs among smaller and larger markets. While operating expenses also include taxes, fees, insurance and other fixed expenditures, these are not included in this analysis, as they do not generate direct local economic benefits. Total office building operating expenditures and their contribution to the national economy are summarized in Table 1.

Table 1:

The eConomiC impaCTs of offiCe building operaTing expendiTures in 94 markeTs served by boma’s 93 loCal assoCiaTions, 2011

Total Office Space (SF) 9,908,990,533Average Annual Operating Cost (SF) $8.05Total Building Operating Expenditures $79,738,709,975Impacts on US Economy contribution to gdp $205,058,622,205 New Personal Earnings $60,976,280,704 direct Jobs supported 2,229,523 Indirect Jobs Supported 1,561,517

Sources: BOMA International, GMU Center for Regional Analysis

Payroll Spending Helps Bring National Impact to $205 Billion

The payroll and non-payroll spending associated with these expenditures for office building operations generated additional spending within the local and state economies, as payroll dollars were re-spent for consumer goods and services, and as non-payroll expenditures ultimately supported additional payroll and business spending.

The $79.7 billion in direct office building operating expenditures in 2011 contributed a total of $205.1 billion to the U.S. economy (GDP), which reflects the initial $79.9 billion in direct expenditures and their indirect economic impacts, for a total of $125.3 billion.

So just how much is $205 billion? About the same worth as Google or twice that of Facebook.

Said another way, it means that for each $1 in building operating expenditures, on average a total of $2.57 was generated to the benefit of the U.S. economy. This contribution to GDP reflected an aggregate multiplier (calculated from data provided by the U.S. Bureau of Economic Analysis) of 2.5716.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

8

$61 Billion in New Personal Earnings

Benefits can be found for the workers residing near the commercial buildings, as direct office building operating expenditures were re-spent within the local, state and national economies, they generated new personal earnings (wages and salaries) for workers residing within the host jurisdictions and therefore benefiting from increased business and consumer sales.

In 2011, the $79.7 billion in direct office building operating expenditures generated a total of $61.0 billion in new personal earnings as a result of the jobs supported directly by this spending and the re-spending of these dollars for consumer goods and services. These new personal earnings will directly expand the tax bases in the local and state jurisdictions served by these office markets. At the national level, where these annual office building operating expenditures have their greatest cumulative impact, for each $1 in direct operating expenditures, $0.765 of new personal earnings were generated.

3.8 Million Jobs Supported

This annual spending for office-building operations in the 94 markets served by BOMA’s 93 local associations supported a workforce ranging from 2.0 to 2.5 million workers (estimated to range around 20 to 25 full-time equivalent jobs per 100,000 gross square feet of office building). While this “ jobs requirement” provides an important source of local employment—totaling an estimated 2.2 million jobs—the direct and indirect spending associated with office building operations (including the payroll spending of these direct, on-site workers) was found to support an additional 1,561,517 jobs ranging across the local and state economies. The jobs were concen-trated in consumer goods and services (retail sales and services supporting local residents, health and education, and housing). At the national level, the aggregate jobs multiplier for office building operations is 19.6 jobs per $1 million in expenditures for building operations.

Copyright © 2012 by boMA internAtionAl . All rights reserved.

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

9

research approach

The CoStar Group Inc. which provided the office building inventory data used in this economic impact analysis, reflects the office market at the end of 2011. Office market inventory data were developed for all 93 BOMA local associations reflecting all office buildings without limitation as to ownership or size.

The operating cost data for these office buildings were developed from 2010 data from BOMA International’s Experience Exchange Report for private and government-owned office buildings and converted to 2011 equivalent dollar values by the application of the annual CPI inflation rate (3.0%) for 2011. For office markets where operating cost data were not collected, estimates were made based on markets having similar characteristics in the same state where these were available or for markets in adjacent states. Average operating cost data were used and these averages were averaged and weighted in markets including multiple sub-markets.

In 26 market areas, metropolitan area-level office market data were collected and are reported separately. In 25 cases, these metropolitan area data are reported within their principal host state (e.g., New York for NYC metro area). For the Washington, D.C., metropolitan area, spanning the District of Columbia and portions of Maryland and Virginia, the metropolitan area data are reported alphabetically under the District of Columbia and not within the two separate states. Minneapolis and St. Paul, Minn., are reported as separate market areas although the multipliers used were for the combined metropolitan area.

The economic impacts of the direct spending for building operations in 2011 are calculated using multipliers (Regional Input-Output Modeling System, RIMS II) purchased from the Bureau of Economic Analysis of the U.S. Department of Commerce. State multipliers were used to calculate the statewide impacts of local office building operating expenditures, and metropolitan area level multipliers were used to calculate the economic impacts for the 26 metropolitan areas reported separately. The state-level economic impacts for 25 of these metropolitan areas (the Washington, D.C., metro area is excluded) were also calculated and are reported in Table 2 in a subsequent section of this report.

The economic impact of office building expenditures are a function of what is being purchased, whether it is locally supplied, and how labor intensive these services or products are (i.e., the more labor intensive, the greater the payroll effect, the more likely the benefits will be retained locally and the broader the impact across the retail and consumer services sectors in the local economy). Building operating expenditures were disaggregated into four groups: utilities, management/administrative, maintenance and repair, and building services. The share of total operating expenditures associated with each of these four categories of expenses was calculated across a sample of office markets nationally yielding the following distribution: utilities, 30 percent; maintenance and repairs, 23 percent; building management, 26 percent; and building services, 21 percent. The percentage that each category represented of total expenditures was used to develop aggregate multipliers weighted to reflect this mix of sectors. These aggregate multipliers were used to calculate the economic impacts of office building operating expenditures by state and metropolitan area. (Appendix E).

These multipliers and the economic impact calculations are discussed in Appendix D, and the multipliers are presented by state and metropolitan area in Appendix E. These multipliers will remain valid for several years and can be used to update the 2011 impact calculations as office market data become available for 2012 going forward possibly for several additional years.

The results of these analyses—the economic impacts of office building operating expenditures in 2011 of their host states’ economies, the 26 metropolitan area economies and the nation—are presented and discussed in the following pages.

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

10

economic impacts of operating expenditures in 94 office markets served by boma local associations

For an easily comparable view of expenditures, Table 2 presents the total 2011 expenditures for office building operations in the office markets served by all 93 BOMA local associations. It also illustrates the buildings’ impacts on their respective state (and metropolitan area) economies.

Organized by state, the data show the total operating expenditures and associated economic impacts specified for each state’s local associations. Local associations representing metropolitan-wide office markets are identified separately (*). The Washington, D.C., metropolitan area (MSA ) is listed under the District of Columbia, while the other 25 metropolitan areas identified separately are listed under their principal host state. For these metropolitan areas, their statewide economic impacts are also reported in Table 2. There are no data provided for several states due to the absence of a BOMA local association serving their office markets.

The 26 metropolitan areas included in Table 2 also generate metropolitan–level economic impacts that are typically smaller than their statewide impacts due to their more limited geographic boundaries. These metropolitan-level economic impacts are presented in Table 3.

Understanding Table 2

The tables reporting economic impacts for each market area consist of four data columns. The first column—Total Expenditure—is the total annual outlay (or expenditures) for office building operations for all commercial and government office buildings within the market area (statewide or metropolitan area) as identified. The square footage of this office space, provided by the CoStar Group Inc., was multiplied by the average operating cost in its respective market area, as reported by BOMA for these respective office markets in 2010 and adjusted for inflation to 2011, to determine total operating expenditures.

The second column in this table—Total Output—represents the total contribution of the annual expenditures for office building operations in each office market (as reported for each of the 93 local associations) to their respective state’s economy—gross state product. In the cases of the 26 metropolitan areas (*) reported separately, the Total Output value represents the contribution of the office building operating expenditures to their respective state’s economy. These metropolitan area’s metropolitan-level economic impact are calculated separately and presented in Table 3.

The third column in the table—Per Earnings—represents the new personal earnings (wages and salaries) generated as a result of the office building operating expenditures reported in column one for each of BOMA’s 93 local associations. These personal earnings represent new income that accrues to workers residing within the state or metropolitan area in which the local associations are located. This is new income earned by workers in businesses that benefit from the payroll spending of employees involved in the office building operations and the re-spending of these expenditures across all sectors of the respective state or metropolitan area economies.

The fourth column in the table—Jobs—represents the indirect employment impact of the total office building operating expenditures in column one for each of BOMA’s local associations. The jobs supported by expenditures for office building operations include those in the businesses benefiting from payroll spending (these tend to be local and focus on consumer goods and services), as well as jobs involved in producing and transporting the materials used to clean and repair office buildings (these jobs may not be local or even within the state). These jobs are generated as a result of the office building operating expenditures throughout the breadth of the local, state and national econo-mies, and they are in addition to the direct, on-site employment that operates and services these office buildings.

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

11

Table 2:

eConomiC impaCTs of offiCe building operaTions by sTaTe and meTropoliTan area for 93 boma loCal assoCiaTions, 2011

sTaTe

ToTal expendiTure

ToTal ouTpuT

per earnings

Jobs

alabama Birmingham

Greater Huntsville 303,432,440

172,148,415

559,889,594

317,646,017

169,770,754

96,317,210

5,187

2,943

alaska

Anchorage

99,721,273 172,844,091 51,282,363 1,339

arizona

Greater Tucson

Greater Phoenix*

146,487,501

959,031,646

268,253,918

1,756,218,070

84,333,147

552,116,437

2,173

14,229

arkansas

Greater Little Rock

Northwest Arkansas

171,760,775

53,729,232

291,355,055

91,140,037

85,727,692

26,816,851

2,647

828

california

Greater Los Angeles*

Inland Empire

Oakland-East Bay

Orange County

Sacramento

San Diego*

San Francisco*

Silicon Valley

3,441,780,374

492,185,788

876,804,371

1,077,093,334

988,341,501

725,279,717

2,019,295,398

1,162,686,157

7,321,138,379

1,046,946,600

1,865,083,020

2,291,125,083

2,102,337,775

1,542,769,321

4,295,317,955

2,473,192,744

2,189,567,746

313,115,309

557,799,267

685,217,698

628,756,177

461,403,373

1,284,621,211

739,669,541

48,737

6,970

12,416

15,252

13,995

10,270

28,594

16,464

colorado

Denver Metro*

Southern Colorado

1,023,019,413

158,804,057

2,190,420,626

340,020,607

662,010,185

102,764,328

16,158

2,508

connecticut

Greater Hartford

Southern Connecticut

786,422,717

1,746,600,677

1,376,182,346

3,056,423,684

409,596,476

909,690,764

9,131

20,279

delaware

district of columbia Washington MSA* 4,220,461,446 7,510,117,001 2,366,104,639 61,923

florida

Ft. Lauderdale and the Palm Beaches

Jacksonville

Miami-Dade*

Orlando*

Southwest Florida

Greater Tampa Bay*

Tallahassee

932,890,589

624,772,733

898,721,230

547,979,885

197,875,965

864,714,252

222,116,701

1,745,441,090

1,168,951,658

1,681,510,118

1,025,272,009

370,226,524

1,617,882,959

415,581,013

554,430,870

371,311,807

534,123,508

325,672,665

117,600,654

513,912,650

132,007,287

15,131

10,133

14,576

8,888

3,209

14,025

3,603

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

12

sTaTe

ToTal expendiTure

ToTal ouTpuT

per earnings

Jobs

georgia Atlanta* 1,909,220,336

3,770,360,776

1,144,432,491

31,294

hawaii Hawaii 260,263,775

454,048,114 141,114,238 3,613

idaho Boise 147,405,420 232,207,021

71,866,038

2,155

illinois Chicago*

Peoria

Suburban Chicago

1,703,430,987

102,785,914

1,588,074,053

3,517,087,586

212,222,898

3,278,909,203

1,045,054,911

63,059,158

974,283,432

24,256

1,464

22,614

indiana Indianapolis*

Michiana569,593,447

57,613,935

1,053,774,649

106,588,488

305,124,944

30,863,151

8,592

869

iowa Iowa 574,529,065 893,231,828 264,102,393 7,943

kansas Wichita 186,792,701 326,816,246 89,374,143 2,436

kentucky Louisville 513,365,361

947,619,067

265,405,272 8,045

louisiana New Orleans

Shreveport303,624,705

50,570,072

576,811,034

96,070,495

173,585,280

28,911,416

4,964

827

maine

maryland Baltimore 1,189,296,948 2,125,806,451 614,391,993 15,670

massachusetts Boston* 3,067,189,682

5,550,052,124

1,651,215,431 37,503

michigan Metropolitan Detroit*

Mid-Michigan

West Michigan

1,258,440,207

160,411,001

316,002,522

2,334,674,632

297,596,574

586,251,986

719,866,810

91,760,065

180,763,238

19,098

2,434

4,796

minnesota Duluth

Minneapolis*

St. Paul*

38,331,847

778,519,108

211,874,202

71,569,813

1,453,581,590

395,592,653

21,430,607

435,255,241

118,454,841

556

11,293

3,073

mississippi Mississippi 118,675,516 207,481,947 61,118,603 1,928

missouri Kansas City

St. Louis*784,039,040

840,412,691

1,460,885,046

1,565,925,000

405,091,019

434,217,706

10,691

11,460

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

13

sTaTe

ToTal expendiTure

ToTal ouTpuT

per earnings

Jobs

nebraska Omaha 235,080,300 357,066,524 104,700,769 3,125

nevadaNevada 564,802,441 936,594,378 287,294,669 7,036

new Jersey New Jersey 3,455,880,532 6,662,187,739 1,869,731,588 41,826

new mexico New Mexico 308,225,501 551,636,420 166,889,931 4,857

new york Capital Region-Albany

Greater Buffalo

Central New York

New York*

Greater Rochester

Long Island

Westchester

449,817,029

205,465,241

168,913,121

8,649,842,359

331,623,978

965,098,519

565,321,608

761,653,133

347,904,225

286,012,312

14,646,354,225

561,522,633

1,634,154,033

957,231,379

208,825,306

95,386,211

78,417,072

4,015,646,066

153,954,774

448,042,162

262,447,730

4,641

2,120

1,743

89,252

3,422

9,958

5,833

north carolina Raleigh-Durham*

Carolinas-West Virginia

Charlotte,Greensboro, Winston Salem (Triad)

259,270,171

1,298,292,568

2,471,641,062

459,326,146

2,300,070,693

4,378,788,965

139,763,993

699,866,680

1,332,380,132

4,127

20,665

39,341

ohio Akron

Greater Cincinnati

Cleveland*

Columbus

Dayton

Toledo

185,147,096

847,329,391

762,738,143

690,318,126

261,355,248

194,761,466

366,087,649

1,675,407,457

1,508,146,875

1,364,952,224

516,772,504

385,097,951

107,953,717

494,052,348

444,729,729

402,503,790

152,388,404

113,559,568

2,907

13,304

11,976

10,839

4,103

3,058

oklahoma Oklahoma City

Tulsa301,350,944

327,177,978

601,672,474

653,238,315

175,354,306

190,382,902

5,155

5,597

oregonPortland Metropolitan* 913,475,115

1,616,810,761 477,838,833 13,152

pennsylvaniaCentral Pennsylvania

Philadelphia*

Pittsburgh

328,172,525

1,956,719,167

1,117,348,098

672,630,940

4,010,542,480

2,290,145,713

196,800,797

1,173,419,047

670,059,129

4,936

29,428

16,804

tennesseeChattanooga

Knoxville

Memphis

Nashville*

102,823,267

228,481,085

327,570,151

472,255,679

200,053,976

444,535,085

637,323,762

918,825,372

58,619,544

130,257,067

186,747,743

269,232,963

1,548

3,440

4,932

7,111

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

14

sTaTe

ToTal expendiTure

ToTal ouTpuT

per earnings

Jobs

texasAustin

Corpus Christi

Dallas*

Fort Worth

Houston*

San Antonio

544,746,962

62,421,565

1,679,155,632

385,026,793

2,103,242,727

395,128,669

1,228,227,901

140,740,405

3,785,951,903

868,110,669

4,742,130,899

890,887,126

363,982,488

41,708,093

1,121,958,060

257,262,582

1,405,319,487

264,012,332

9,487

1,087

29,243

6,705

36,628

6,881

utahUtah

457,884,863 965,720,387 288,512,337 8,668

virginiaVirginia 941,015,475 1,745,633,579 498,493,538 13,510

washingtonSeattle-King County*

Spokane

South Puget Sound

Tri Cities (Kennewick)

1,112,145,025

147,070,841

214,175,317

43,895,549

2,096,848,239

277,288,688

403,808,071

82,761,063

621,934,853

82,245,103

119,771,335

24,547,313

15,817

2,092

3,046

624

wisconsinWisconsin 1,061,882,524 1,896,929,952 580,470,649 16,176

State Total

Spill over

US total

79,738,709,975

–

79,738,709,975

152,236,237,741

52,822,384,464

205,058,622,205

45,033,948,171

15,942,332,533

60,976,280,704

1,125,385

436,132

1,561,517

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

15

metropolitan-level economic impact of office operating expenditures in 26 selected metropolitan areas, 2011

The economic impacts of office operating expenditures in 26 metropolitan areas on their respective states’ economies are reported in Table 2. This spending also has economic impacts that are captured within their respective metropolitan area economies. These metropolitan-level economic impacts can be measured by applying metropolitan area-level multipliers to the values of these metropolitan area office-operating expenditures. These exclusive, metropolitan-level impacts are presented in Table 3 for 26 of the metropolitan areas and are a sub-set of the state-level economic impacts reported in Table 2.

Table 3: boma meTropoliTan area offiCe markeTs’ sTaTe-level eConomiC impaCTs, 2011

meTropoliTan area

ToTal expendiTures

ToTal ouTpuT

per earnings

Jobs

Atlanta* 1,909,220,336 3,981,571,841 1,320,105,619 36,050

Boston* 3,067,189,682 5,574,384,671 1,661,031,955 40,291

Chicago* 1,703,430,987 3,653,054,375 1,202,397,808 32,804

Cleveland* 762,738,143 1,499,737,687 434,618,109 12,205

Dallas* 1,679,155,632 3,822,754,330 1,274,765,134 32,831

Denver Metro* 1,023,019,413 2,308,343,429 733,953,857 18,112

Houston* 2,103,242,727 4,529,779,898 1,536,602,688 38,984

Indianapolis* 569,593,447 1,188,747,790 375,123,992 10,845

Greater Los Angeles* 3,441,780,374 7,112,666,257 2,161,013,690 52,236

Metropolitan Detroit* 1,258,440,207 2,535,492,745 804,430,217 21,133

Miami-Dade* 898,721,230 1,714,369,651 582,746,979 16,042

Minneapolis* 778,519,108 1,557,777,624 509,477,489 14,485

Nashville* 472,255,679 1,021,739,802 327,273,186 8,920

New York* 8,649,842,359 16,166,903,215 5,072,478,915 123,732

Orlando* 547,979,885 1,083,459,801 336,883,786 9,297

Philadelphia* 1,956,719,167 4,087,389,426 1,329,217,309 33,229

Greater Phoenix* 959,031,646 1,978,672,174 656,762,134 16,880

Portland Metropolitan* 913,475,115 1,922,786,559 622,249,200 16,470

Raleigh-Durham* 259,270,171 502,338,031 149,986,498 4,506

San Diego* 725,279,717 1,413,353,310 457,386,774 10,388

San Francisco* 2,019,295,398 3,908,517,732 1,147,708,199 26,633

Seattle-King County* 1,112,145,025 1,974,063,399 596,268,895 15,557

St. Louis* 840,412,691 1,807,135,208 588,113,238 14,339

St. Paul* 211,874,202 423,949,634 138,654,447 3,942

Greater Tampa Bay* 864,714,252 1,792,065,809 587,070,070 16,162

Washington MSA* 4,220,461,446 7,510,117,001 2,366,104,639 61,923 Note: calculated using metro multipliers Source: CoStar Group Inc.

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

16

the direct and indirect Jobs impacts of office building operations in 2011

One of the most important benefits of office building operations’ annual spending is the 1.6 million jobs that this spending supports. These jobs represent workers who are supported by the re-spending of payroll dollars earned by on-site workers, who manage, maintain and service the office buildings, as well as by their tenants, including workers who may be employed by vendors that service the office buildings. (See also indirect jobs, Table 2.)

Since the number of direct jobs associated with office building operations varies depending on the range of services provided to tenants, the size and complexity of the building, their quality and their location, this analysis is based on an estimated 20 to 25 full-time job equivalents per 100,000 square feet of office space.

As shown in Table 4, the 9.9 billion square feet of office space nationwide would therefore directly support an estimated 2.2 million jobs, in addition to the 1.6 million indirect jobs, for a combined total of 3.8 million jobs dependent on expenditures for office building operations in 2011. The total jobs impact of office building operations for all 93 local associations are presented in Appendix C.

Table 4:

direCT and indireCT Jobs assoCiaTed wiTh expendiTures for offiCe building operaTions in 2011

offiCe direCT indireCT ToTal area invenTory Jobs Jobs Jobs

States* 9,908.99 2,229,523 1,125,385 3,354,908 Spillover** 436,132 436,132 U.S. 2,229,523 1,561,517 3,791,040

Sources: CoStar Group Inc.; GMU Center for Regional Analysis *the sum of 93 BOMA local associations, square feet in millions. ** jobs generated or supported outside of the state in which the

direct expenditures for office building operations are occurring.

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

17

additional economic impacts: the effects of in-office workers

A growing share of the U.S. workforce goes to an office building each workday. Office buildings have become the “factory floor” of the 21st Century. So while it is important to document the significant annual impact that the construction and operation of office buildings have on local, state and national economies, as this analysis has done, it is critical to also consider the effects these office buildings have on the people who actually work within them.

Without question, these building spaces and their effective operations enable office workers to be productive and to generate the professional, business and consumer services that are driving the nation’s economic recovery and that will account for much of its growth going forward.

Those office workers represent a significant population: assuming an 85 percent occupancy rate (190 square feet per worker), the 9.9 billion square feet of office space accounted for by office markets served by BOMA’s 93 local associations provide workspace for an estimated 44.3 million workers. That’s more than 5 1/2 times the population of New York City according to 2010 U.S. Census data. In 2011, the average contribution of these office workers to GDP was $116,200. In total these 44.3 million office jobs represented $5.1 trillion of the nation’s $15 trillion GDP.

Given the sheer size this workforce represents, the full measure of the annual value of this office space clearly extends far beyond the $205.1 billion in contributions to gross domestic product (GDP) generated by the operating expenditures required to support tenants in 2011. Rather, it should also reflect the total value of office space generated in this office space plus the contribution these jobs and associated payroll have on their host jurisdictions’ economies.

Table 5:

eConomiC impaCTs of offiCe building operaTing expendiTures, 2011 (dollars in billions) ToTal ToTal personal Jobs ouTlays ouTpuT earnings supporTed

State Impacts* $79.7 $152.2 $45.0 1,125,385 Metro Area Impacts** $42.7 $84.6 $26.8 684,057 U.S. Impacts*** $79.7 $205.1 $61.0 1,561,517

Source: GMU Center for Regional Analysis *includes office markets for all 93 BOMA local associations reflecting state-level economic impacts; **metropolitan areas impacts included within state impact totals. *** state impacts plus spillover impacts, impacts generated in one state but accruing to another

but not included in that state’s impact total.

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

18

conclusions

The commercial real estate industry is a major source of economic activity at the local, state and national levels, creating jobs and expanding personal earnings from the moment the ground is broken for the construction of a new building, through its ribbon cutting, and continuing throughout the lifetime of the building.

Given that the national office market is much larger than the 9.9 billion square feet represented by the 93 BOMA local associations that are included in this analysis, the magnitude of real estate’s impact becomes even more impressive when one considers that the 9.9 billion square feet represented by BOMA:

• Results in $80 billion of direct operating expenditures;

• Contributes $205 billion toward the gross domestic product;

• Creates $61 million in new earnings;

• Supports 3.8 million jobs; and

• Houses 44 million office workers.

Each annually recurring expenditure, in turn, grows each year as the inventory of building space increases, while maintaining a productive work environment for millions of workers and businesses; generating a relatively stable source of jobs and personal income; and contributing to the local tax base year after year, throughout the ups and downs of a business cycle.

A Closer Look

The key findings of this research, summarized in more detail below, are also illustrated in Table 5:

• The operating expenditures for the 9.9 billion square feet of office buildings included in this analysis totaled $79.7 billion in 2011;

• These $79.7 billion in annual expenditures for office building operations added a total of $205.1 billion to the nation’s economy (GDP) in 2011, reflecting a total output multiplier of 2.57;

• These $79.7 billion in annual expenditures for office building operations generated a total of $61.0 billion in new personal earnings, or 76 cents for each dollar spent accruing to workers residing within states served by the 94 office markets represented by BOMA’s local associations; and

• The $79.7 billion in annual expenditures for office building operations supported a significant workforce, both locally and beyond the local labor markets:

– direct employment by office building managers was estimated to total approximately 2.2 million workers (on-site and directly supported);

– the indirect job impact of this spending and re-spending of payroll dollars in the state and national economies is estimated to support 1.6 million jobs (19.6 jobs per $1 million in direct operating expenditures) across all sectors; and

– the 9.9 billion square feet of office space benefiting from these operating expenditures have the capacity to provide a quality working environment to more than 44.3 million office workers.

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

19

appendix a

glossary of Terms

Direct Outlays/Expenditures — The annual spending associated with the operations (maintenance and repair, utilities, management, services to buildings) of office buildings.

Economic Impact — The generation of new spending measured in dollars within a jurisdiction as a result of direct expenditures associated with office building operations, including the direct expenditures plus the indirect and induced economic activity these direct expenditures generate as they are re-cycled through the local, state and nation-al economies.

Gross Regional Product (GRP), Gross State Product (GSP), Gross Domestic Product (GDP) — The value of goods and services produced within the economy of the respective geographic area (metropolitan area, state and national).

Indirect Benefit — The additional economic benefits—measured in dollars or jobs—resulting from the accumulated additional value generated by the direct outlays or expenditures, as these dollars are re-spent within the metropoli-tan, state and national economies. Indirect benefits are inclusive of “induced” benefits that are benefits generated by the payroll spending associated with the operations of office buildings. These additional benefits—indirect and induced—generally affect the broad base of the local economy as measured by increased jobs and personal earnings in retail and consumer services, education and health, transportation, housing, utilities, and government.

Multiplier — A number used to calculate the total economic impact of direct spending for office building operations. Types of multipliers include: (1) output multiplier—measures the contribution (impact) of a direct expenditure on the overall economy; (2) personal earnings multiplier—measures the total personal earnings (wages and salaries) gener-ated within the jurisdiction as a result of the direct expenditures and the jobs they support; and (3) employment multiplier—measures the total number of jobs that can be supported by this direct expenditure (per $1 million).

Office Building Inventory — Square feet of office space in buildings within the service areas of BOMA’s 93 local associations inclusive of publicly owned and occupied buildings, owner-occupied buildings and tenant-occupied buildings.

Operating Costs — Costs (expenditures) associated with the day-to-day operation of the office building inventory, including maintenance and repairs, utilities, management/administrative, and services to buildings, including cleaning, security and grounds. Taxes, fixed expenses, direct leasing expenses and parking costs are excluded costs.

Spillover Impacts — Economic impacts that are generated by direct spending for office building operations in a given state or metropolitan area that are realized by another state due to workers commuting across state lines (earning wages in one state and spending these earnings in their home state) and payments to vendors located in another state. These economic impacts are not reflected in the benefitting states’ multipliers but are captured in the U.S. multipliers and reported in the U.S. totals.

Total Output — The sum of the direct and indirect impacts (expenditures) reflecting the combination of the initial expenditures and their subsequent accumulated value as these are cycled through the economy inclusive of benefits generated by the re-spending of personal earnings; contribution to GDP (gross domestic product), GSP (gross state product) or GRP (gross regional product).

Unit of Analysis — The 94 markets represented by BOMA’s 93 local associations are defined by their general office market areas, normally a political unit (state, metropolitan area) for which economic information is reported. In this analysis, the state is the primary unit of analysis, with selected metropolitan areas being reported separately along with an estimate for the nation. Metropolitan area impacts are reported both at the metropolitan area scale and for their respective states, as their impacts extend beyond the metropolitan area boundaries.

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

20

appendix b

offiCe markeT invenTory and annual operaTion CosTs, by sTaTe and meTropoliTan areas, 2011

sTaTe sq.fT. CosT/sf

alabama

Birmingham 46,581,430 6.51

Greater Huntsville 19,472,794 8.84

alaska

Anchorage 12,396,514 8.04

arizona

Greater Tucson 23,533,983 6.22

Greater Phoenix* 156,487,174 6.13

arkansas

Greater Little Rock 28,060,386 6.12

Northwest Arkansas 16,038,250 3.35

california

Greater Los Angeles* 399,705,065 8.61

Inland Empire 68,590,024 7.18

Oakland-East Bay 110,994,307 7.90

Orange County 150,318,163 7.17

Sacramento 156,699,840 6.31

San Diego* 112,305,433 6.46

San Francisco* 187,247,466 10.78

Silicon Valley 121,173,006 9.60

colorado Denver Metro* 162,291,296 6.30

Southern Colorado 31,027,569 5.12

connecticut

Greater Hartford 85,844,739 9.16

Southern Connecticut 97,305,023 17.95

delaware

district of columbia

Washington MSA* 445,868,921 9.47

florida

Ft. Lauderdale and the Palm Beaches 123,256,828 7.57

Jacksonville 86,197,646 7.25

Miami-Dade* 99,492,005 9.03

Orlando* 83,914,717 6.53

Southwest Florida 31,632,173 6.26

Greater Tampa Bay* 143,264,232 6.04

Tallahassee 20,114,133 11.04

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

21

sTaTe sq.fT. CosT/sf

georgia

Atlanta* 298,488,241 6.40

hawaii

Hawaii 32,353,814 8.04

idaho

Boise 31,401,396 4.69

illinois

Chicago* 213,120,682 7.99

Peoria 15,460,160 6.65

Suburban Chicago 238,864,238 6.65

indiana

Indianapolis* 86,137,593 6.61

Michiana 9,134,590 6.31

iowa

Iowa 89,046,893 6.45

kansas

Wichita 21,055,423 8.87

kentucky

Louisville 90,108,616 5.70

louisiana

New Orleans 47,134,664 6.44

Shreveport 7,812,870 6.47

maine

maryland

Baltimore 126,676,429 9.39

massachusetts

Boston* 310,516,586 9.88

michigan

Metropolitan Detroit* 193,320,666 6.51

Mid-Michigan 22,290,318 7.20

West Michigan 47,902,836 6.60

minnesota

Duluth 5,030,181 7.62

Minneapolis* 106,757,598 7.29

St. Paul* 26,680,040 7.94

mississippi

Mississippi 25,908,887 4.58

missouri

Kansas City 109,104,896 7.19

St. Louis* 131,814,968 6.38

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

22

sTaTe sq.fT. CosT/sf

nebraska

Omaha 36,611,371 6.42

nevada

Nevada 77,812,758 7.26

new Jersey New Jersey 391,374,212 8.83

new mexico New Mexico 50,525,185 6.10

new york Capital Region-Albany 58,005,074 7.75

Greater Buffalo 40,972,077 5.01

Central New York 26,264,211 6.43

New York* 618,402,445 13.99

Greater Rochester 42,201,092 7.86

Long Island 83,862,507 11.51

Westchester 49,123,780 11.51

north carolina Raleigh-Durham* 45,354,705 5.72

Carolinas-West Virginia 201,223,796 6.45

Charlotte,Greensboro, Winston Salem (Triad) 368,610,064 6.71

ohio

Akron 27,935,100 6.63

Greater Cincinnati 135,006,580 6.28

Cleveland* 98,212,529 7.77

Columbus 97,750,712 7.06

Dayton 41,573,731 6.29

Toledo 28,155,826 6.92

oklahoma Oklahoma City 48,819,079 6.17

Tulsa 43,168,946 7.58

oregon

Portland Metropolitan* 108,951,971 8.38

pennsylvania

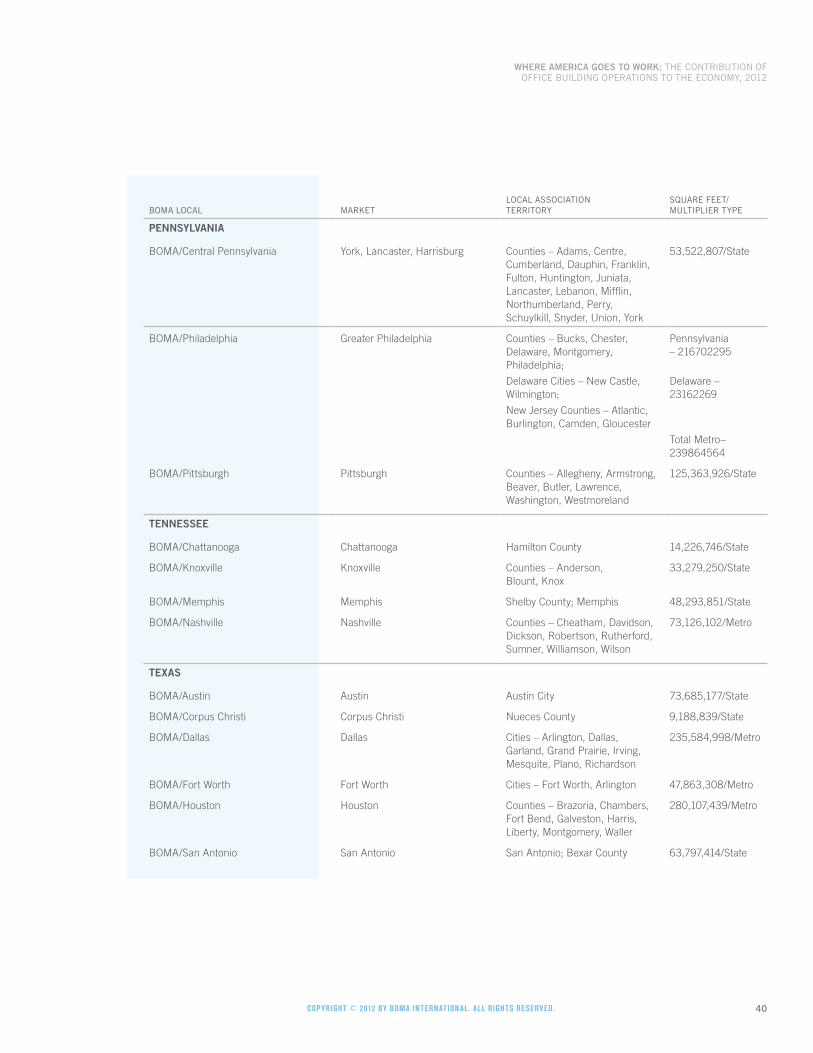

Central Pennsylvania 53,522,807 6.13

Philadelphia* 239,864,564 8.16

Pittsburgh 125,363,926 8.91

tennessee Chattanooga 14,226,746 7.23

Knoxville 33,279,250 6.87

Memphis 48,293,851 6.78

Nashville* 73,126,102 6.46

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

23

sTaTe sq.fT. CosT/sf

texas

Austin 73,685,177 7.39

Corpus Christi 9,188,839 6.79

Dallas* 235,584,998 7.13

Fort Worth 47,863,308 8.04

Houston* 280,107,439 7.51

San Antonio 63,797,414 6.19

utah

Utah 86,661,608 5.28

virginia

Virginia 155,042,235 6.07

washington

Seattle-King County* 144,351,932 7.70

Spokane 21,135,030 6.96

South Puget Sound 32,264,560 6.64

Tri Cities (Kennewick) 9,208,967 4.77

wisconsin Wisconsin 136,568,327 7.78

State Total 9,908,990,533 8.05

Source: CoStar Group Inc., BOMA International 2011 Experience Exchange Report®

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

24

appendix c

direCT and indireCT Jobs assoCiaTed wiTh operaTing ouTlays/expendiTures for offiCe buildings in 2011

sTaTe offiCe invenTory direCT Jobs indireCT Jobs ToTal Jobs

alabama

Birmingham 46,581,430 10,481 5,187 15,668

Greater Huntsville 19,472,794 4,381 2,943 7,324

alaska

Anchorage 12,396,514 2,789 1,339 4,128

arizona

Greater Tucson 23,533,983 5,295 2,173 7,469

Greater Phoenix* 156,487,174 35,210 14,229 49,439

arkansas

Greater Little Rock 28,060,386 6,314 2,647 8,961

Northwest Arkansas 16,038,250 3,609 828 4,437

california

Greater Los Angeles* 399,705,065 89,934 48,737 138,671

Inland Empire 68,590,024 15,433 6,970 22,402

Oakland-East Bay 110,994,307 24,974 12,416 37,390

Orange County 150,318,163 33,822 15,252 49,074

Sacramento 156,699,840 35,257 13,995 49,253

San Diego* 112,305,433 25,269 10,270 35,539

San Francisco* 187,247,466 42,131 28,594 70,725

Silicon Valley 121,173,006 27,264 16,464 43,728

colorado

Denver Metro* 162,291,296 36,516 16,158 52,673

Southern Colorado 31,027,569 6,981 2,508 9,489

connecticut

Greater Hartford 85,844,739 19,315 9,131 28,446

Southern Connecticut 97,305,023 21,894 20,279 42,173

delaware

district of columbia

Washington MSA* 445,868,921 100,321 61,923 162,244

florida

Ft. Lauderdale and the Palm Beaches 123,256,828 27,733 15,131 42,863

Jacksonville 86,197,646 19,394 10,133 29,528

Miami-Dade* 99,492,005 22,386 14,576 36,962

Orlando* 83,914,717 18,881 8,888 27,769

Southwest Florida 31,632,173 7,117 3,209 10,327

Greater Tampa Bay* 143,264,232 32,234 14,025 46,259

Tallahassee 20,114,133 4,526 3,603 8,128

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

25

sTaTe offiCe invenTory direCT Jobs indireCT Jobs ToTal Jobs

georgia

Atlanta* 298,488,241 67,160 31,294 98,454

hawaii

Hawaii 32,353,814 7,280 3,613 10,892

idaho

Boise 31,401,396 7,065 2,155 9,221

illinois

Chicago* 213,120,682 47,952 24,256 72,208

Peoria 15,460,160 3,479 1,464 4,942

Suburban Chicago 238,864,238 53,744 22,614 76,358

indiana

Indianapolis* 86,137,593 19,381 8,592 27,973

Michiana 9,134,590 2,055 869 2,924

iowa

Iowa 89,046,893 20,036 7,943 27,979

kansas

Wichita 21,055,423 4,737 2,436 7,174

kentucky

Louisville 90,108,616 20,274 8,045 28,320

louisiana

New Orleans 47,134,664 10,605 4,964 15,569

Shreveport 7,812,870 1,758 827 2,585

maine

maryland

Baltimore 126,676,429 28,502 15,670 44,173

massachusetts

Boston* 310,516,586 69,866 37,503 107,370

michigan

Metropolitan Detroit* 193,320,666 43,497 19,098 62,595

Mid-Michigan 22,290,318 5,015 2,434 7,450

West Michigan 47,902,836 10,778 4,796 15,574

minnesota

Duluth 5,030,181 1,132 556 1,688

Minneapolis* 106,757,598 24,020 11,293 35,313

St. Paul* 26,680,040 6,003 3,073 9,076

mississippi

Mississippi 25,908,887 5,829 1,928 7,757

missouri

Kansas City 109,104,896 24,549 10,691 35,239

St. Louis* 131,814,968 29,658 11,460 41,118

nebraska

Omaha 36,611,371 8,238 3,125 11,363

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

26

sTaTe offiCe invenTory direCT Jobs indireCT Jobs ToTal Jobs

nevada

Nevada 77,812,758 17,508 7,036 24,544

new Jersey New Jersey 391,374,212 88,059 41,826 129,886

new mexico New Mexico 50,525,185 11,368 4,857 16,225

new york Capital Region-Albany 58,005,074 13,051 4,641 17,693

Greater Buffalo 40,972,077 9,219 2,120 11,339

Central New York 26,264,211 5,909 1,743 7,652

New York* 618,402,445 139,141 89,252 228,393

Greater Rochester 42,201,092 9,495 3,422 12,917

Long Island 83,862,507 18,869 9,958 28,827

Westchester 49,123,780 11,053 5,833 16,886

north carolina Raleigh-Durham* 45,354,705 10,205 4,127 14,332

Carolinas-West Virginia 201,223,796 45,275 20,665 65,940

Charlotte,Greensboro, Winston Salem (Triad) 368,610,064 82,937 39,341 122,278

ohio

Akron 27,935,100 6,285 2,907 9,192

Greater Cincinnati 135,006,580 30,376 13,304 43,680

Cleveland* 98,212,529 22,098 11,976 34,073

Columbus 97,750,712 21,994 10,839 32,832

Dayton 41,573,731 9,354 4,103 13,458

Toledo 28,155,826 6,335 3,058 9,393

oklahoma

Oklahoma City 48,819,079 10,984 5,155 16,139

Tulsa 43,168,946 9,713 5,597 15,310

oregon

Portland Metropolitan* 108,951,971 24,514 13,152 37,666

pennsylvania

Central Pennsylvania 53,522,807 12,043 4,936 16,978

Philadelphia* 239,864,564 53,970 29,428 83,398

Pittsburgh 125,363,926 28,207 16,804 45,011

tennessee

Chattanooga 14,226,746 3,201 1,548 4,749

Knoxville 33,279,250 7,488 3,440 10,928

Memphis 48,293,851 10,866 4,932 15,798

Nashville* 73,126,102 16,453 7,111 23,564

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

27

sTaTe offiCe invenTory direCT Jobs indireCT Jobs ToTal Jobs

texas

Austin 73,685,177 16,579 9,487 26,066

Corpus Christi 9,188,839 2,067 1,087 3,155

Dallas* 235,584,998 53,007 29,243 82,249

Fort Worth 47,863,308 10,769 6,705 17,475

Houston* 280,107,439 63,024 36,628 99,652

San Antonio 63,797,414 14,354 6,881 21,236

utah

Utah 86,661,608 19,499 8,668 28,167

virginia

Virginia 155,042,235 34,885 13,510 48,395

washington

Seattle-King County* 144,351,932 32,479 15,817 48,296

Spokane 21,135,030 4,755 2,092 6,847

South Puget Sound 32,264,560 7,260 3,046 10,306

Tri Cities (Kennewick) 9,208,967 2,072 624 2,696

wisconsin

Wisconsin 136,568,327 30,728 16,176 46,904

State Total 9,908,990,533 2,229,523 1,125,385 3,354,908

Spill over 436,132 436,132

US total 2,229,523 1,561,517 3,791,040

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

28

appendix d

eConomiC mulTipliers and impaCT CalCulaTions

The total economic impacts of annual expenditures for the operation of office buildings reflect the combination of direct expenditures and their subsequent monetary effects as these funds are circulated through the economy; that is, the re-spending of these direct expenditures will generate additional economic activity that otherwise would not have occurred. The total value of these combined direct and indirect values can be estimated by the application of appropriate multipliers that have been calculated for each state and metropolitan area by type of expenditures by the Bureau of Economic Analysis of the U.S. Department of Commerce employing its Regional Input-Output Model System (RIMS II).

For this analysis, state and metropolitan area multipliers were purchased for: construction (maintenance and repair), utilities, management and services to buildings. These multipliers were weighed by their share of operating cost expenditures for office buildings (BOMA’s income and expense data) and combined into a single series of multipliers representing building operations expenditures. These aggregate multipliers, a different set for each state and metropolitan area, see Appendix E, were applied to the market data for each of the 94 markets represented by 93 BOMA local associations (square feet of office space and average operating cost per square foot) to calculate the total economic impacts generated by these direct expenditures for office building operations in 2011.

The results of these calculations are estimates of: (1) output value—total contribution to the U.S., state and metropoli-tan area economies; (2) personal earnings—new earnings realized by residents of the state or metropolitan area in which the spending occurs; and (3) the jobs supported by these expenditures—full-time, year-round jobs throughout the state (or metropolitan area) and nation. The key variables governing the magnitude and significance of these economic impacts are their dollar value, the category of outlay (e.g., maintenance and repair, utilities, management and services to buildings), the direct employment and payroll associated with the direct spending (payroll) for building operations, and the geographic area of analysis and the complexity of the respective state economies. The size and complexity of the states’ or metropolitan areas’ economies determine the extent to which they can provide the inputs and retain the outputs of these economic activities; i.e., how self-sufficient the states or metropolitan areas are. Larger states retain a greater share of this direct spending for building operations than smaller states or their constituent metropolitan areas. At the national level, interstate transfers (spillover impacts) add to the magnitude of these secondary economic impacts. The degree to which the direct expenditures are retained internally by the state is reflected in the respective state economic multipliers. The aggregate multipliers for office building operations are presented in Appendix E.

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

29

appendix e

aggregaTe eConomiC impaCT mulTipliers for building operaTions

Jobs Jobs sTaTe ouTpuT earnings (per million) ouTpuT earnings (per million)

alabama

Birmingham 1.845187 0.559501 17.093808

Greater Huntsville 1.845187 0.559501 17.093808

alaska

Anchorage 1.733272 0.514257 13.425086

arizona

Greater Tucson 1.831241 0.575702 14.83728

Greater Phoenix* 1.831241 0.575702 14.83728 2.063198 0.684818 17.60099

arkansas

Greater Little Rock 1.696284 0.499111 15.412062

Northwest Arkansas 1.696284 0.499111 15.412062

california

Greater Los Angeles* 2.127137 0.636173 14.160471 2.066565987 0.627876696 15.17713605

Inland Empire 2.127137 0.636173 14.160471

Oakland-East Bay 2.127137 0.636173 14.160471

Orange County 2.127137 0.636173 14.160471

Sacramento 2.127137 0.636173 14.160471

San Diego* 2.127137 0.636173 14.160471 1.948701 0.630635 14.323194

San Francisco* 2.127137 0.636173 14.160471 1.935584925 0.568370631 13.18935667

Silicon Valley 2.127137 0.636173 14.160471

colorado

Denver Metro* 2.141133 0.647114 15.794342 2.25640237 0.717438836 17.70441849

Southern Colorado 2.141133 0.647114 15.794342

connecticut

Greater Hartford 1.749927 0.520835 11.61072

Southern Connecticut 1.749927 0.520835 11.61072

delaware

district of columbia Washington MSA* 1.779454 0.560627 14.672163 1.779454 0.560627 14.672163

florida

Ft. Lauderdale and the Palm Beaches 1.871003 0.594315 16.219099

Jacksonville 1.871003 0.594315 16.219099

Miami-Dade* 1.871003 0.594315 16.219099 1.907565542 0.648417951 17.84974177

Orlando* 1.871003 0.594315 16.219099 1.977189 0.614774 16.965909

Southwest Florida 1.871003 0.594315 16.219099

Greater Tampa Bay* 1.871003 0.594315 16.219099 2.072437 0.678918 18.690387

Tallahassee 1.871003 0.594315 16.219099

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

30

Jobs Jobs sTaTe ouTpuT earnings (per million) ouTpuT earnings (per million)

georgia

Atlanta* 1.974817 0.599424 16.391214 2.085443867 0.69143702 18.88191255

hawaii

Hawaii 1.744569 0.542197 13.880152

idaho

Boise 1.575295 0.48754 14.621593

illinois

Chicago* 2.064708 0.6135 14.239671 2.14452737 0.705868225 19.25774956

Peoria 2.064708 0.6135 14.239671

Suburban Chicago 2.064708 0.6135 14.239671

indiana

Indianapolis* 1.850047 0.535689 15.085162 2.087011 0.658582 19.040424

Michiana 1.850047 0.535689 15.085162

iowa

Iowa 1.55472 0.459685 13.825699

kansas

Wichita 1.74962 0.478467 13.042893

kentucky

Louisville 1.845896 0.516991 15.671616

louisiana

New Orleans 1.89975 0.57171 16.349296

Shreveport 1.89975 0.57171 16.349296

maine

maryland

Baltimore 1.787448 0.516601 13.176244

massachusetts

Boston* 1.809491 0.538348 12.227263 1.817424173 0.541548495 13.13599401

michigan

Metropolitan Detroit* 1.855213 0.572031 15.175917 2.01479 0.639228 16.793332

Mid-Michigan 1.855213 0.572031 15.175917

West Michigan 1.855213 0.572031 15.175917

minnesota

Duluth 1.867111 0.559081 14.505183

Minneapolis* 1.867111 0.559081 14.505183 2.000949763 0.654418735 18.60543816

St. Paul* 1.867111 0.559081 14.505183 2.000949763 0.654418735 18.60543816

mississippi

Mississippi 1.748313 0.515006 16.245492

missouri

Kansas City 1.863281 0.516672 13.635584

St. Louis* 1.863281 0.516672 13.635584 2.150295 0.699791 17.061854

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

31

Jobs Jobs sTaTe ouTpuT earnings (per million) ouTpuT earnings (per million)

nebraska

Omaha 1.518913 0.445383 13.293778

nevada

Nevada 1.658269 0.508664 12.457514

new Jersey New Jersey 1.927783 0.541029 12.102962

new mexico New Mexico 1.789717 0.541454 15.757311

new york Capital Region-Albany 1.693251 0.464245 10.318343

Greater Buffalo 1.693251 0.464245 10.318343

Central New York 1.693251 0.464245 10.318343

New York* 1.693251 0.464245 10.318343 1.869040214 0.586424435 14.30454837

Greater Rochester 1.693251 0.464245 10.318343

Long Island 1.693251 0.464245 10.318343

Westchester 1.693251 0.464245 10.318343

north carolina Raleigh-Durham* 1.771612 0.539067 15.916901 1.937508 0.578495 17.379335

Carolinas-West Virginia 1.771612 0.539067 15.916901

Charlotte, Greensboro, Winston Salem (Triad) 1.771612 0.539067 15.916901

ohio Akron 1.97728 0.58307 15.700768

Greater Cincinnati 1.97728 0.58307 15.700768

Cleveland* 1.97728 0.58307 15.700768 1.966255 0.569813 16.002004

Columbus 1.97728 0.58307 15.700768

Dayton 1.97728 0.58307 15.700768

Toledo 1.97728 0.58307 15.700768

oklahoma Oklahoma City 1.996584 0.581894 17.105593

Tulsa 1.996584 0.581894 17.105593

oregon

Portland Metropolitan* 1.769956 0.5231 14.397407 2.104914 0.681189 18.029765

Pennsylvania

Central Pennsylvania 2.049626 0.599687 15.039594

Philadelphia* 2.049626 0.599687 15.039594 2.088899365 0.679309188 16.98222784

Pittsburgh 2.049626 0.599687 15.039594

tennessee

Chattanooga 1.94561 0.5701 15.056689

Knoxville 1.94561 0.5701 15.056689

Memphis 1.94561 0.5701 15.056689

Nashville* 1.94561 0.5701 15.056689 2.163531 0.693 18.88829

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

32

Jobs Jobs sTaTe ouTpuT earnings (per million) ouTpuT earnings (per million)

texas

Austin 2.254676 0.668168 17.415071

Corpus Christi 2.254676 0.668168 17.415071

Dallas* 2.254676 0.668168 17.415071 2.276593222 0.759170329 19.5521667

Fort Worth 2.254676 0.668168 17.415071

Houston* 2.254676 0.668168 17.415071 2.153712379 0.730587425 18.5354143

San Antonio 2.254676 0.668168 17.415071

utah

Utah 2.10909 0.630098 18.931278

virginia

Virginia 1.855053 0.52974 14.357285

washington

Seattle-King County* 1.885409 0.559221 14.222342 1.775005377 0.536143112 13.98870181

Spokane 1.885409 0.559221 14.222342

South Puget Sound 1.885409 0.559221 14.222342

Tri Cities (Kennewick) 1.885409 0.559221 14.222342

wisconsin

Wisconsin 1.786384 0.546643 15.233359

US total 2.57163205 0.764701118 19.58292591

Source: CoStar Group Inc.

Copyright © 2012 by boMA internAtionAl . All rights reserved.

where america goes to work: The ConTribuTion of offiCe building operaTions To The eConomy, 2012

33

appendix f

boma loCal assoCiaTion TerriTories defined

boma loCal

markeT

loCal assoCiaTion TerriTory

square feeT/ mulTiplier Type

alabama

BOMA/Birmingham Birmingham Birmingham (includes Blount, Jefferson, Shelby, St. Clair, Walker Counties)

46,581,430/State

BOMA/Greater Huntsville Huntsville AL Counties – Cherokee, Cullman, Colbert, Dekalb, Franklin, Jackson, Lauderdale Lawrence, Limestone, Madison, Marion, Marshall, Morgan, Winston. TN Counties – Franklin, Giles, Lawrence, Lincoln.

19,472,794/State

alaska

BOMA/Anchorage Anchorage Anchorage 12,396,514/State

arizona

BOMA/Greater Phoenix Phoenix Maricopa County 156,487,174/Metro

BOMA/Greater Tucson Tucson Pima County 23,533,983/State

arkansas

BOMA/Greater Little Rock Little Rock Pulaski County – Includes Little Rock, North Little Rock and Jacksonville

28,060,386/State