what can save active investment management? - nomura · 10/3/2017 · what can save active...

TRANSCRIPT

© Nomura

Making choices in new dimensions

3 October 2017

What can save active investment

management?

Global Markets

Quantitative Strategies

EMEA

Anthony Morris

In their report for the Norwegian Government Pension Fund, Ang,

Goetzmann and Schaefer (2009) found that active management added

value in which asset class?

1. Equities

3.7%

2. Fixed Income

7.41%

3. Private Equity

11.11%

4. Real Estate

11.11%

5. None of the above

66.67%

Who has the biggest impact on your fund’s performance?

1. CIO

13.73%

2. PM

19.61%

3. Investment committee

29.41%

4. Operations/other back office

37.25%

What can save active management?

1. Artificial intelligence

18.37%

2. Cloud computing

0%

3. Big Data

22.45%

4. Meditation

14.29%

5. Ray Dalio’s management culture

6.12%

6. Jared and Ivanka

6.12%

7. MiFID 2/other regulation

10.2%

8. Other

22.45%

What is the world’s oldest profession?

1. Prostitution

35.85%

2. Military

9.43%

3. Hunting/Gathering/Farming

43.4%

4. Fiduciary management

11.32%

Source: Nomura.

Active management will survive

The Threat: active management, as currently done, fails to demonstrate value-added

The Opportunities: there are other ways to be active

Making choices in new dimensions

“The evidence…indicates that these 115 mutual funds

were on average not able to predict security prices well

enough to outperform a buy-the-market-and-hold

policy…”

-Michael Jensen (1967)

From “The Performance of Mutual Funds in the Period 1945-1964”, presented at the Annual

Meeting of the American Finance Association, Washington D.C.

50 years ago, the problem surfaced

“…there is very little evidence that any individual fund

was able to do significantly better than that which we

expected from mere random chance…”

-Michael Jensen (1967)

From “The Performance of Mutual Funds in the Period 1945-1964”, presented at the Annual

Meeting of the American Finance Association, Washington D.C.

50 years ago, the problem surfaced

Source: “Bonds are different: Active versus passive in 12 points”, Baz et al (2017), PIMCO Quantitative Research.

- Are bonds any different?

50 years later, the problem is still with us

-3

-2

-1

0

1

2

3

1st quartile 2nd quartile 3rd quartile 4th quartile

t-s

tat

of

alp

ha

Quartiles of US Fixed Income Fund Managers

Alpha t-stat

99% confidence

95% confidence

90% confidence

“There is no evidence that active fixed income

management has added value”

Ang, Goetzmann, and Schaeffer (2009)

Source: “Evaluation of Active Management of the Norwegian Government Pension

Fund—Global”, released December 14, 2009

The biggest threat to active management?

"The evidence does indicate....a pressing need on the

part of the funds themselves to evaluate much more

closely both the costs and the benefits of their

research and trading activities…"

-Michael Jensen (1967)

From “The Performance of Mutual Funds in the Period 1945-1964”, presented at the Annual

Meeting of the American Finance Association, Washington D.C.

Jensen’s advice—rethink the business model

Source: “Bonds are different: Active versus passive in 12 points”, Baz et al (2017), PIMCO Quantitative Research.

Diagnosis: No alpha, and everyone bets on High Yield

Active fixed income has become a carry cliché

-4

-3

-2

-1

0

1

2

3

4

1st quartile 2nd quartile 3rd quartile 4th quartile

t-s

tat

Quartiles of US Fixed Income Fund Managers

t-stat of alpha

t-stat of High Yield exposure

99% confidence

95% confidence

90% confidence

Source: Nomura, Bloomberg.

Active outperforms passive, but not the benchmark

50

100

200

400C

um

ula

tive

to

tal

retu

rns

(lo

g-s

ca

led

)

BBG Barclays US HY bondindex

Big US HY Active Managers

JNK US Equity

Source: Nomura, Bloomberg.

- CDS index: better liquidity, diversification, performance, and zero credit analysts/traders

New way to be active—upgrade format

50

100

200

400

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Cu

mu

lati

ve

ex

ce

ss

re

turn

s (

log

-s

ca

led

)Nomura HY CDS Index BBG Barclays US HY bond index (ex. ret over duration)

High Yield is a bundle of at least three exposures—but are they the best available?

New way to be active—decompose and recreate

Source: Nomura, Bloomberg. Analysis based on monthly returns from 1997-2017.

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Duration HY Credit MBS Curve Rates Vol Alpha(p.a.)

Beta

to

fac

tor

Big US Manager

15Source: Nomura, Bloomberg.

- HY Credit : Nomura US HY CDS Index instead of US HY Cash Bond index

- MBS : Nomura USD iVRP instead of US MBS Index

- Rates Vol : Nomura USD iVRP instead of US 1m10y

Making active better by upgrading formats

50

100

200

400

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

Cu

mu

lati

ve

ex

ce

ss

re

turn

s (

log

-s

ca

led

)

Recreated using betterformatsDecomposed and recreated

Source: Nomura, Bloomberg.

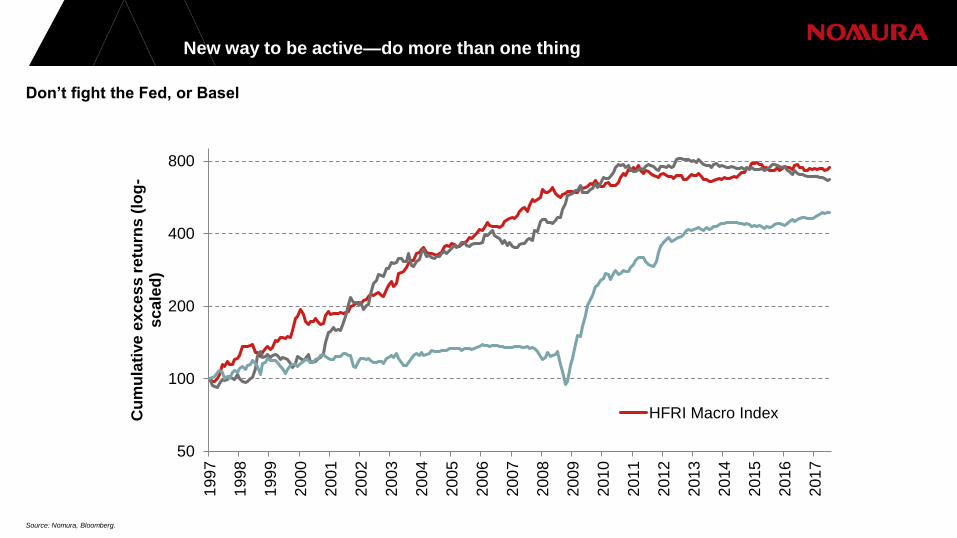

Don’t fight the Fed, or Basel

New way to be active—do more than one thing

50

100

200

400

800

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

Cu

mu

lati

ve

ex

ce

ss

re

turn

s (

log

-s

ca

led

)

HFRI Macro Index

Active management will survive

But not all active managers will

Survivors will need to be active in different ways

The Threat: active management, as currently done, fails to demonstrate value-added

“Stock-picking” and market-timing are the core activity of active managers

But zero evidence that this generates value over benchmarks

The Opportunities: there are other ways to be active

Improving formats (e.g. CDS index vs corporate bonds)

Do more than one thing (e.g. not just carry or trend)

Unbundling (decompose, recreate better)

Markets (going where curves are still steep)

Making choices in new dimensions

Disclaimer

Conflicts of interest: Nomura International plc (NIP) is the Index Sponsor of the index, and is therefore responsible for maintaining the index, as well as calculating and publishing the levels of

the index, based on a proprietary models and relying on market information. Actual or potential conflicts of interest may arise in relation to the multiple roles NIP has in relation to the index, e.g.

NIP or any of its affiliates may (i) be the counterparty to any investment product entered into based on the index; (ii) engage in pre-hedging, hedging and/or trading activities, in the normal

course of business, in the index or the underlying instruments or in financial instruments that are linked to any of the foregoing, or trade otherwise in the normal course of business (either for

proprietary accounts or their client accounts) in such instruments, which in each case may adversely affect the level of the index; and/or (iii) publish, from time to time, research that may

influence the level of the index, or may express opinions or provide recommendations that are inconsistent with the investment views inherent in the index. Potentially market sensitive

information is shared with the respective trading desk in order to risk manage NIP’s (or its affiliates’) Index linked investment products in the normal course of its hedging activities.

Investment objectives: There can be no assurance that the index will achieve the stated investment objective. The index methodology has been designed with the benefit of hindsight on the

basis of certain historically observed trends and correlations which may not prove to be correct in any future period. Any back-tested performance information may not therefore be an accurate

or reliable indication of any fundamental aspect of the index methodology and the actual future performance of the index may bear little or no relation to the hypothetical back-tested or historical

performance of the index.

Index adjustments/cancellation: NIP as the Index Sponsor has the authority to amend the methodology of the index and/or make such adjustments to the index methodology as it considers

appropriate, in its sole discretion acting in good faith, in order to take into account events or changes in the relevant underlying markets or to preserve the investability and objective of the index

- including cancelling the index in certain circumstances.

Discretion: NIP maintains certain discretion to determine whether certain types of disruption events have occurred and any resulting adjustments. NIP has no obligation to take the interests of

any other party into consideration when exercising discretion or making determinations with respect to the index.

Lack of operating history: The index has only recently been established as a tradable strategy and therefore has no sufficient data upon which to evaluate long-term performance. Any back-

testing or similar analysis on the index must be considered illustrative only and may be based on estimates or assumptions not used in determining actual levels of the index.

Index charges: Certain index charges are deducted from the index level and/or any transaction linked to the index, which include fees that accrue to the benefit of the NIP as Index Sponsor in

consideration for establishing and maintaining the index.

Impact of index pre-hedging and hedging: NIP designed the index with the intention of earning a profit through entering into transactions linked to the index, including pre-hedging and

hedging transactions. Such pre-hedging and hedging activities may involve trading in the underlying instruments and taking long or short positions in related instruments which could adversely

affect the performance of the index.

Past Performance is no guide to future performance: the actual performance of the index during any future period may bear little relation to the historical performance of the index. No one

can predict with any degree of certainty the future performance of the index.

The foregoing are not an exhaustive set of risks: Independent due diligence should be undertaken and advice should be sought as deemed appropriate from suitably qualified professional

advisors in order to ensure that the risks and suitability of an exposure to the index are understood.

Important risks and disclosures in relation to the index

Potential risks for the Index

19

Disclaimer

20

The information contained herein (the “Information”) is provided to you by the Quantitative Strategies, Index Structuring and / or Structured Sales Departments of Nomura International plc (“NIP”). NIP is part of the Nomura group of

companies (“Nomura”) and is authorised by the Prudential Regulation Authority (“PRA”), regulated by the UK Financial Conduct Authority and the PRA and is a member of the London Stock Exchange. The Information is confidential and

has been furnished solely for your information and must not be referred to, disclosed, transmitted, reproduced or redistributed, in whole or in part, to another person.

The Information is subject to the following terms:

• It is provided to you without compensation to promote investment services generally and Nomura and its affiliates do not accept any liability whatsoever for any direct, indirect or consequential loss arising from any direct or indirect use

of the Information or its content.

• It is intended for (a) professional clients and eligible counterparties as they are defined under the regulatory rules in the European Economic Area (“EEA”) and (b) institutional investors as defined in the U.S. and is not subject to the

independence and disclosure standards applicable to debt research reports prepared for retail investors.

• Nomura is not a designated investment adviser and the Information is therefore provided on the basis that you have such knowledge and experience to evaluate its merits and risks and are capable of undertaking your own objective

analysis of the Information with respect to your specific requirements.

• It may have been prepared in accordance with regulatory requirements which differ from those demanded under applicable jurisdictions where you are located.

• Nomura is not soliciting any action based on the Information and it should not be considered as an offer to buy or sell any f inancial instruments or other products which may be mentioned in it.

• It does not constitute a personal recommendation under applicable regulatory rules in the EEA or take into account the particular investment objectives, financial situations or needs of individual investors nor does it constitute tailor

made investment advice as this term may be defined under applicable regulations in any jurisdiction.

• Any views expressed in the Information may differ from the views offered in Nomura’s independent research reports prepared for any investors including retail investors or from views that may be expressed by other financial

institutions or market participants on the same subject matter as the Information.

Where Information refers to an index or indices:

• As the index sponsor and index calculation agent, NIP is responsible for and has determinative influence over the index’ composition, calculation and maintenance and the potentially subjective judgments it makes in this respect could

have an adverse effect on the levels of the index.

• NIP maintains certain discretion in relation to the index determination: (i) whether certain types of disruption events have occurred, (ii) any resulting adjustments and calculations and (iii) to make such other determinations or

adjustments necessary to calculate the levels of the index. NIP has no obligation to take the interests of any other party into consideration when exercising such discretion or making such determinations with respect to the index.

• NIP as the Index Sponsor has the authority to amend the methodology of the index and/or make such adjustments to the index methodology as it considers appropriate, in its sole discretion acting in good faith, in order to take into

account events or changes in the relevant underlying markets or to preserve the investability and objective of the Index (including cancelling the Index in certain circumstances).

• NIP may decide to permanently cancel and discontinue calculating and publishing the index at any time. There is no guarantee that the index will continue to be calculated for the full duration of any transaction linked to the index. If the

index is terminated, any transaction linked to the index may be terminated early at a value reflecting a level of the index that may be considerably less than the last published level of the index, and such level may even be zero or

negative.

• NIP developed the index methodology with the benefit of hindsight. Any back-tested performance information may not therefore be an accurate or reliable indication of any fundamental aspect of the index methodology and the actual

future performance of the index may bear little or no relation to the hypothetical back-tested or historical performance of the index.

• Certain index charges may be deducted from the index level and/or any transaction linked to the index, which include fees that accrue to the benefit of the NIP as Index Sponsor in consideration for establishing and maintaining the

index.

Disclaimer

21

• Actual or potential conflicts of interest may arise in relation to the multiple roles NIP has in relation to the index, e.g. NIP or any of its affiliates may (i) be the counterparty to any investment product entered into based on the index; (ii)

engage in pre-hedging, hedging and/or trading activities, in the normal course of business, in the index or the underlying instruments or in financial instruments that are linked to any of the foregoing, or trade otherwise in the normal

course of business (either for proprietary accounts or their client accounts) in such instruments, which in each case may adversely affect the level of the index and/or (iii) publish, from time to time, research that may influence the level

of the index, or may express opinions or provide recommendations that are inconsistent with the investment views inherent in the index. Potentially market sensitive information is shared with the respective trading desk in order to risk

manage NIP’s (or its affiliates’) Index-linked investment products in the normal course of its hedging activities. NIP manages conflicts by maintaining a restricted list, a personal account dealing policy and policies and procedures for

managing conflicts of interest arising from the allocation and pricing of financial instruments and impartial investment research and disclosure to clients via client documentation. Disclosure information is available at:

http://www.nomuranow.com/disclosures/

• NIP designed the index with the intention of earning a profit through entering into transactions linked to the index, including pre-hedging and hedging transactions. Such pre-hedging and hedging activities may involve trading in the

underlying instruments and taking long or short positions in related instruments which could adversely affect the performance of the index. In reaching a determination as to the appropriateness of any proposed transaction linked to an

index, the recipient of this Information should undertake a thorough independent review of the legal, regulatory, credit, tax, accounting and economic consequences of such action.

• Nomura may in its sole discretion from time to time provide to investors in products linked to the Index (i) reports in relation to the notional investment of the Index in its underlying instruments and (ii) the proportion of such notional

investment represented by the investor’s respective investment in such products or similar information (each the “Investor Information”). The Investor Information is provided solely for general information purposes. No

representation, guarantee, warranty or undertaking whatsoever, express or implied, is made as to the accuracy, completeness or reliability of the Investor Information. No responsibility or liability (including, without limitation, any liability

in negligence) is or will be accepted by Nomura, its affiliates or by any person connected with either of them, directly or indirectly, connected with the Investor Information. Any use of Investor Information by an investor is in full

knowledge that it should not rely on such information and that any such use will be at the investor’s own risk. No legal relationship (whether in contract, tort or otherwise) exists between any investor and Nomura in its capacity as the

Index Sponsor, or by virtue of the provision of the Investor Information.

Where the material is distributed into AEJ, the following additional blocks must be added:

This information is distributed (i) in Hong Kong by NIP (Hong Kong) Limited (“NIHK”), which is regulated by the Hong Kong Securities and Futures Commission (“SFC”); (ii) in Singapore by Nomura Singapore Limited (Registration number

197201440E), which is regulated by the Monetary Authority of Singapore (“MAS”); (iii) in Japan by Nomura Securities Co, Ltd. only for “professional investors” as defined by the Financial Instruments and Exchange Act of Japan; (iv) in

Australia by NIP, NIHK, NSL or Nomura Australia Limited (“NAL”) (A.C.N 003 032 513), a holder of an AFS licence (No. 246412) with the Australian Securities and Investment Commission (only for “wholesale investor” as defined by the

Corporations Act). Please note that neither NIP, NIHK nor NSL holds an Australian financial services licence as each is exempt from the requirement to hold this licence in respect of the financial services it provides. NIP is regulated by the

Financial Conduct Authority and Prudential Regulation Authority under UK laws, NSL is regulated by the MAS under Singapore laws, while NIHK is regulated by the SFC under Hong Kong laws, all of which differ from Australian laws; (v) in

Malaysia by Nomura Securities Malaysia Sdn Bhd; or (vi) in Korea by Nomura Financial Investment (Korea) Co., Ltd. only for “professional investors” as defined by the Financial Investment Services and Capital Market Act. This

information has not been reviewed by any regulatory authority in Hong Kong, Singapore, Republic of China (Taiwan), Australia or any other jurisdiction.

Where the material is distributed into Saudi Arabia, the following additional block must be added:

This document has not been approved for distribution to persons other than ‘Authorised Persons’, ‘Exempt Persons’ or ‘Institutions’ (as defined by the Capital Markets Authority) in the Kingdom of Saudi Arabia (‘Saudi Arabia’) by NIP.

Neither this document nor any copy thereof may be taken or transmitted or distributed, directly or indirectly, by any person other than those authorised to do so into Saudi Arabia. By accepting to receive this document, you represent that

you are not located in Saudi Arabia or that you are an ‘Authorised Person’, an ‘Exempt Person’ or an ‘Institution’ in Saudi Arabia and agree to be bound by the foregoing limitations. Any failure to comply with these restrictions may

constitute a violation of the laws of Saudi Arabia.

Disclaimer

22

Where the material is distributed into UAE and/or Qatar, the following additional blocks must be added:

NIP in the Dubai International Financial Centre ("DIFC") (Registered No. 0777) is regulated by the Dubai Financial Services Authority ("DFSA"). NIplc - DIFC Branch may only undertake the financial services activities that fall within the

scope of its existing DFSA licence. This is not investment research as defined by the DFSA. Related financial products are intended only for a ‘Market Counterparty’ or a ‘Professional Client’ as defined by the DFSA and therefore no other

person should act upon it. The information is not intended to lead to the conclusion of a contract of any nature what so ever within the territory of the DIFC. The recipient of the information understands, acknowledges and agrees that the

contents of this document have not been approved by the DFSA or any other regulatory body or authority in the United Arab Emirates. Nothing contained in this report is intended to constitute ‘Advising on Financial Products' or 'Arranging

Deals in Investments’ or ‘Arranging Credit and Advising on Credit’ as defined by the DFSA and is not intended to endorse or recommend a particular course of action. By accepting to receive this document, you represent that you are a’

Market Counterparty’ or a ‘Professional Client’ and you agree to be bound by the foregoing limitations.

NIP in the Qatar Financial Centre ("QFC") (Registered No. 00106) is authorised by the Qatar Financial Centre Regulatory Authority ("QFCRA"). Principal place of business in Qatar: Qatar Financial Centre, Office 804,8th Floor, QFC

Tower, Diplomatic Area, West Bay, PO Box 23245 , Doha, Qatar. NIplc - QFC Branch may only undertake the regulated activities that fall within the scope of its existing QFCRA licence. This is not investment research as defined by the

QFCRA. Related financial products are intended only for a ‘Market Counterparty’ or a ‘Business Customer’ as defined by the QFCRA and therefore no other person should act upon it. The information is not intended to lead to the

conclusion of a contract of any nature what so ever within the territory of the QFC. The recipient of the information understands, acknowledges and agrees that the contents of this document have not been approved by the QFCRA or any

other regulatory body or authority in Qatar. Nothing contained in this report is intended to constitute ‘Advising on Investments’ or ‘Arranging Deals in Investments’ or ‘Arranging Credit Facilities’ as defined by the QFCRA and is not intended

to endorse or recommend a particular course of action. By accepting to receive this document, you represent that you are a ‘Market Counterparty’ or a ‘Business Customer’ and you agree to be bound by the foregoing limitations.

If distributed into the US, the following section will also apply to US clients:

Nomura Securities International, Inc, (“NSI”) is a registered broker-dealer in the United States and a member of Financial Industry Regulatory Authority (“FINRA”) and Securities Investor Protection Corporation (“SIPC”).

With respect to U.S. regulation, it may constitute a debt research report and therefore it is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports

prepared for retail investors. The views expressed herein may differ from the views offered in Nomura’s debt research reports prepared for retail investors. This report may not be independent of the proprietary interests of

Nomura. Nomura trades, or may trade, the securities covered in this report for its own account. Such trading interests may be contrary to the recommendation(s) offered in this report.

Short Volatility/Variance: Each of the Nomura Volatility Risk Premium Indices (the “indices” and each an “index”) reflects a short position in

volatility. This means that should realised volatility or implied volatility increase, which is often the case in distressed equity markets, the index is

likely to post negative returns. Losses can be significant and the indices can go to zero. The losses increase with the amplitude of daily

movements, positive or negative, of the S&P 500 Index.

Convexity Risk: The return of each variance swap depends on variance (which is volatility squared). This means that in respect of realised

volatility, the return is convex and not linear. This means that the losses incurred in a scenario where volatility spikes can be significantly larger

than should the return of the variance swap have been linear in volatility. Similarly, the loss incurred by the increase in volatility (in absolute terms)

will be greater than the gain made by a decrease in volatility by the same amount.

Indices Calculated at Bid – Early Unwind Costs: The indices are calculated based on listed bid prices of option contracts on the underlying

equity index. On dates other than variance swap contract expiry dates, in respect of any investment products linked to the strategy Nomura

International plc as product provider has no commitment to provide unwind levels, and if provided, unwind levels cannot be defined methodically

but will be determined by Nomura International plc as product provider taking into account the prevailing bid-offer for volatility in the market for the

relevant notional exposure.

Potential Limited Exposure to the Variance Swap Contracts: The indices enter notional short positions in the variance swap contracts on

trading days when the implied strike level is greater than or equal to the exponentially weighted underlying equity index returns over the last twenty

trading days. On trading days where it is not, no notional short position is entered into. This means that the indices can have a reduced or even

zero notional short position and exposure at times. No assurance can be made that such criterion will be successful in avoiding variance swap

contracts which would subsequently lead to a loss. Furthermore, such criterion may mean that for a variance swap contract which may otherwise

have posted a gain, the weight could be zero and cause the indices to miss out on such positive performance.

Important risks and disclosures in relation to the Nomura Volatility Risk Premium Indices and

Certificate

Potential risks for the Nomura Volatility Risk Premium Indices and

Certificate

28

Implied Variance Levels Determination: The indices determine the implied variance strikes for any variance swap contracts notionally sold that

day and determine the mark-to-market value of variance swap contracts previously entered into and held by the indices. The implied variance

levels are determined based on the bid prices of option contracts on the underlying equity index listed on the CBOE and such levels may differ

from the levels Nomura International plc or any other market participant determines for implied variance levels.

Movements in Implied Volatility Will Affect the Value of the Indices: The indices take notional short positions in variance swap contracts on the

underlying equity index. The relationship of variance swap contract’s price to implied volatility is such that, all else being equal, the price of the

variance swap contract is expected to fall as implied volatility decreases, and the price of the variance swap contract is expected to rise as implied

volatility increases. The indices’ notional short exposure to the variance swap contracts is therefore effectively similar to a short position in the

implied volatility of the underlying equity index. Therefore, each day, changes in implied volatility levels will affect the value of the

indices. Specifically, increases in implied volatility will increase the prices of the variance swap contracts in which the indices hold notional short

positions, which will reduce the value of the indices.

Performance Risk: The indices seek to achieve returns based on the “volatility risk premium” relating to prices of variance swap contracts on the

underlying equity index. A volatility risk premium strategy is designed to capture returns based on the difference between implied (i.e. expected)

volatility and realised (i.e. actual) volatility that is often observed in U.S. equity options markets. As the indices target returns based on the volatility

risk premium related to the underlying equity index, the strategy will tend to perform well when the implied volatility of the underlying equity index,

measured at the time the notional short positions in the variance swap contracts are taken, is greater than its actual realised volatility. On the other

hand, the strategy will tend to perform poorly when the actual realised volatility of the underlying equity index exceeds its implied volatility,

measured at the time the notional short positions in the variance swap contracts are taken. For example, the indices will perform poorly when the

underlying equity index is unstable and experiences large, sudden changes in value, in which case the indices can experience sharp, severe

losses. Additionally, there is no limit to the amount by which the value of the indices may decline. Therefore, the value of the indices may decline to

zero or may even be negative.

Important risks and disclosures in relation to the Nomura Volatility Risk Premium Indices and

Certificate

Potential risks for the Nomura Volatility Risk Premium Indices and

Certificate

28