weygandt, kieso, kimmel, trenholm, kinnear accounting principles, third canadian edition © 2009...

TRANSCRIPT

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

Prepared by:

Debbie Musil

Kwantlen University College

Chapter 5Chapter 5Accounting Accounting

for for Merchandising Merchandising

OperationsOperations

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

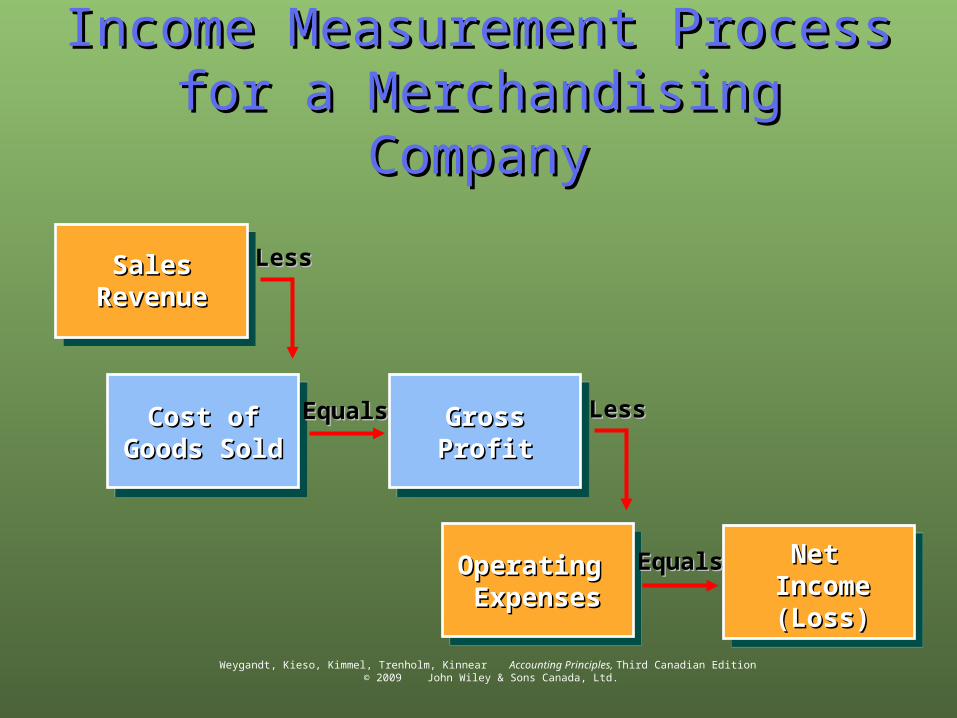

Income Measurement Process for a Income Measurement Process for a Merchandising CompanyMerchandising Company

SalesSalesRevenueRevenue

Cost ofCost ofGoods SoldGoods Sold

Cost ofCost ofGoods SoldGoods Sold

LessLess

GrossGrossProfitProfit

GrossGrossProfitProfit

EqualsEquals

Operating Operating ExpensesExpenses

Net Net IncomeIncome(Loss)(Loss)

EqualsEquals

LessLess

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

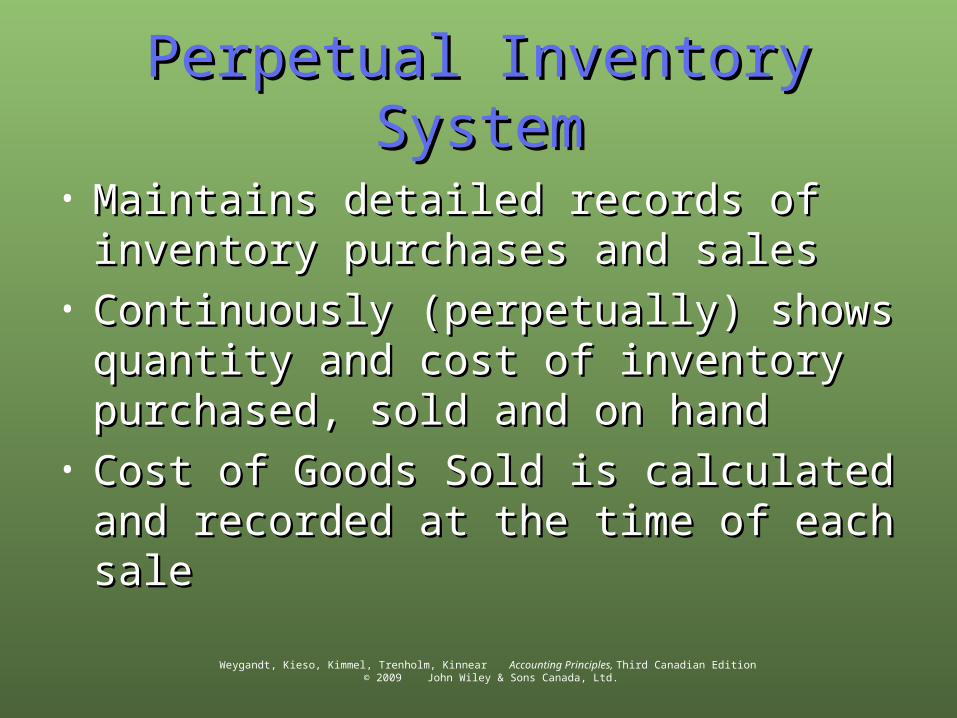

Perpetual Inventory SystemPerpetual Inventory System

• Maintains detailed records of inventory Maintains detailed records of inventory purchases and salespurchases and sales

• Continuously (perpetually) shows quantity Continuously (perpetually) shows quantity and cost of inventory purchased, sold and and cost of inventory purchased, sold and on handon hand

• Cost of Goods Sold is calculated and Cost of Goods Sold is calculated and recorded at the time of each salerecorded at the time of each sale

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

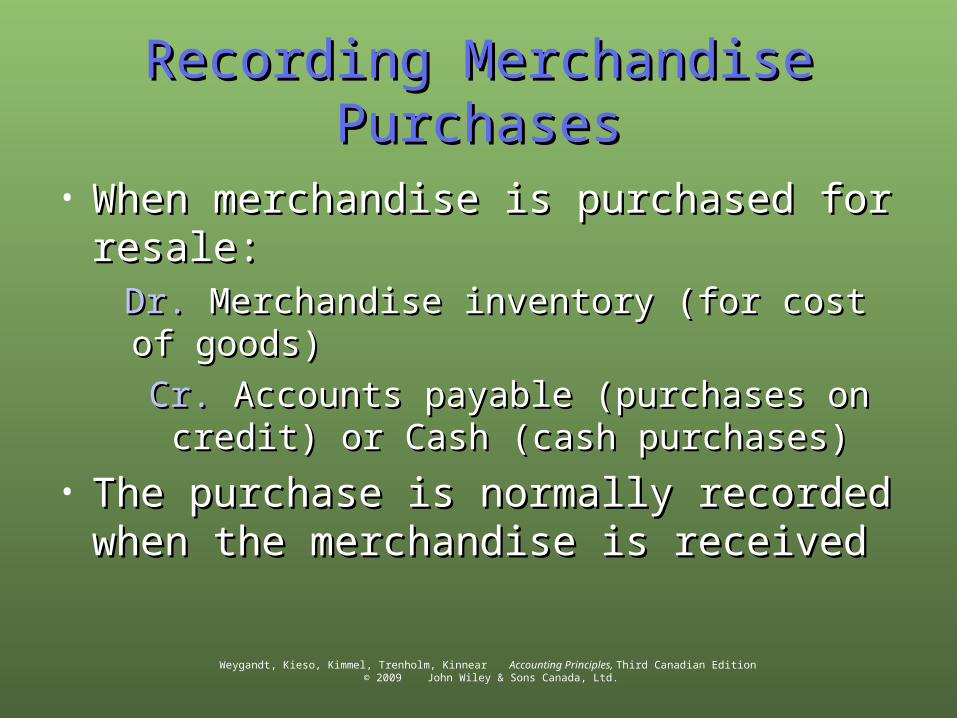

Recording Merchandise PurchasesRecording Merchandise Purchases

• When merchandise is purchased for When merchandise is purchased for resale:resale: Dr.Dr. Merchandise inventory (for cost of goods) Merchandise inventory (for cost of goods)

Cr.Cr. Accounts payable (purchases on credit) Accounts payable (purchases on credit) or Cash (cash purchases)or Cash (cash purchases)

• The purchase is normally recorded when The purchase is normally recorded when the merchandise is receivedthe merchandise is received

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

Freight CostsFreight Costs

• Purchase agreement indicates when ownership of Purchase agreement indicates when ownership of the goods is transferred from buyer to sellerthe goods is transferred from buyer to seller

• FOB Shipping Point:FOB Shipping Point:• Buyer accepts ownership at place of shipping and pays Buyer accepts ownership at place of shipping and pays

for shipping costsfor shipping costs• Buyer debits Buyer debits Merchandise InventoryMerchandise Inventory for cost of shipping for cost of shipping

• FOB Destination:FOB Destination:• Buyer accepts ownership when goods are delivered to Buyer accepts ownership when goods are delivered to

buyer’s place of business and seller pays freight costsbuyer’s place of business and seller pays freight costs• Seller debits Seller debits Freight OutFreight Out for cost of shipping for cost of shipping

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

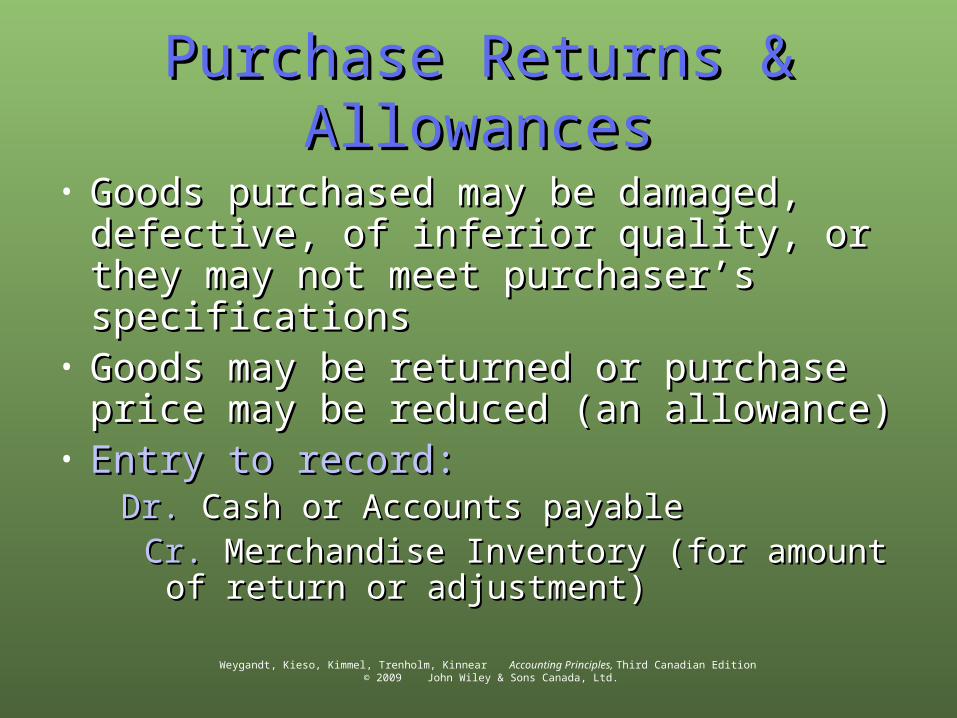

Purchase Returns & AllowancesPurchase Returns & Allowances

• Goods purchased may be damaged, Goods purchased may be damaged, defective, of inferior quality, or they may defective, of inferior quality, or they may not meet purchaser’s specificationsnot meet purchaser’s specifications

• Goods may be returned or purchase price Goods may be returned or purchase price may be reduced (an allowance)may be reduced (an allowance)

• Entry to record:Entry to record: Dr.Dr. Cash or Accounts payable Cash or Accounts payable

Cr.Cr. Merchandise Inventory (for amount of Merchandise Inventory (for amount of return or adjustment)return or adjustment)

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

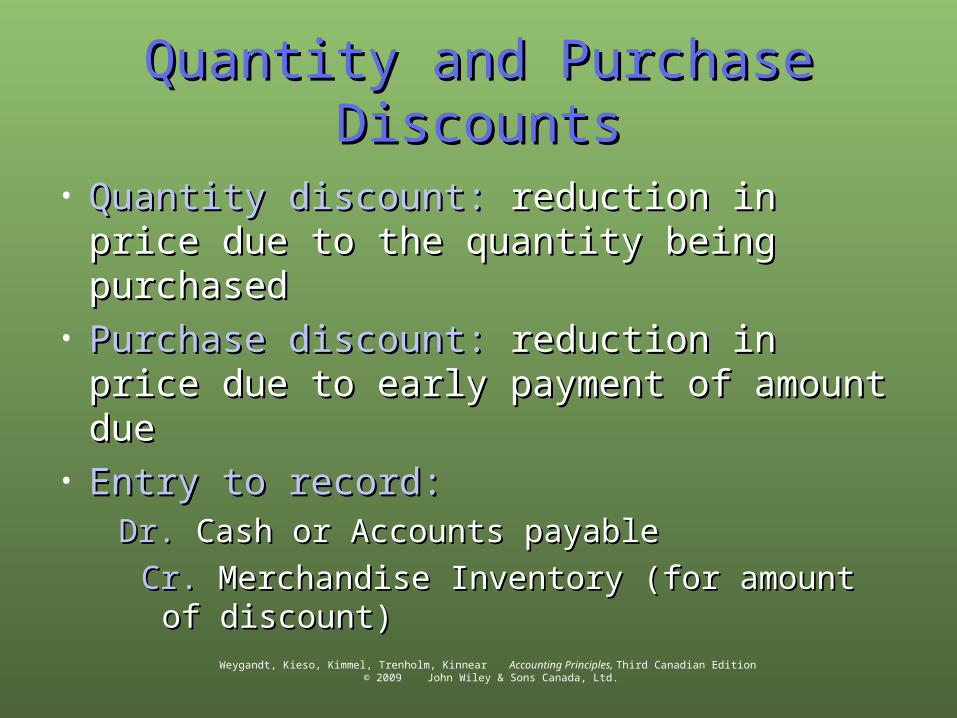

Quantity and Purchase DiscountsQuantity and Purchase Discounts

• Quantity discount:Quantity discount: reduction in price due to reduction in price due to the quantity being purchasedthe quantity being purchased

• Purchase discount:Purchase discount: reduction in price due reduction in price due to early payment of amount dueto early payment of amount due

• Entry to record:Entry to record: Dr.Dr. Cash or Accounts payable Cash or Accounts payable

Cr.Cr. Merchandise Inventory (for amount of Merchandise Inventory (for amount of discount)discount)

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

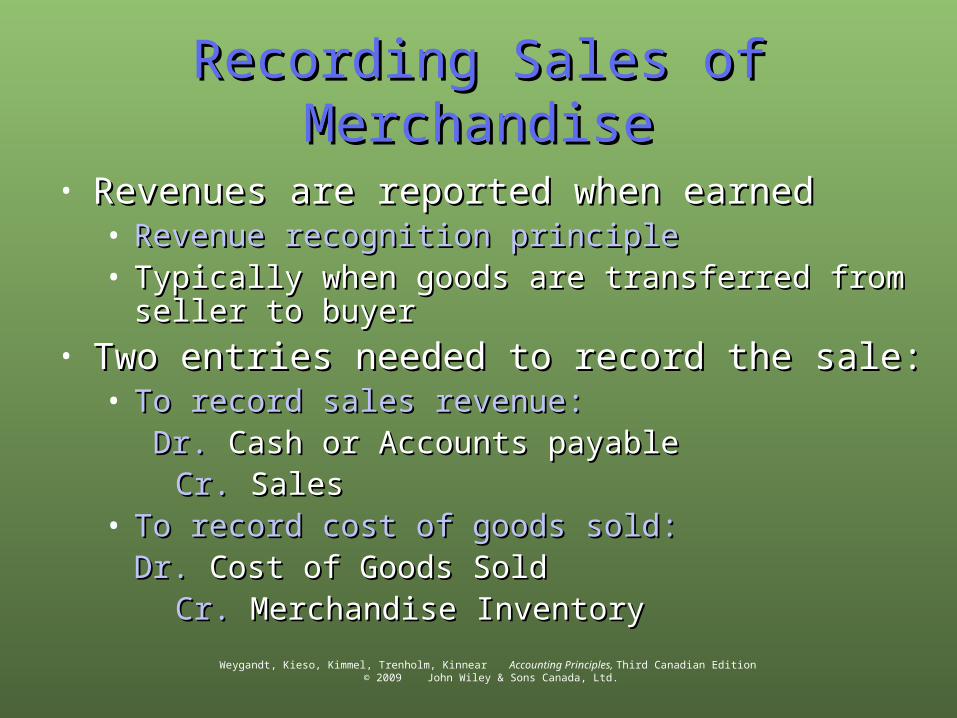

Recording Sales of MerchandiseRecording Sales of Merchandise

• Revenues are reported when earnedRevenues are reported when earned• Revenue recognition principleRevenue recognition principle• Typically when goods are transferred from seller to Typically when goods are transferred from seller to

buyerbuyer• Two entries needed to record the sale:Two entries needed to record the sale:

• To record sales revenue:To record sales revenue: Dr.Dr. Cash or Accounts payable Cash or Accounts payable

Cr.Cr. Sales Sales• To record cost of goods sold:To record cost of goods sold: Dr.Dr. Cost of Goods Sold Cost of Goods Sold

Cr.Cr. Merchandise Inventory Merchandise Inventory

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

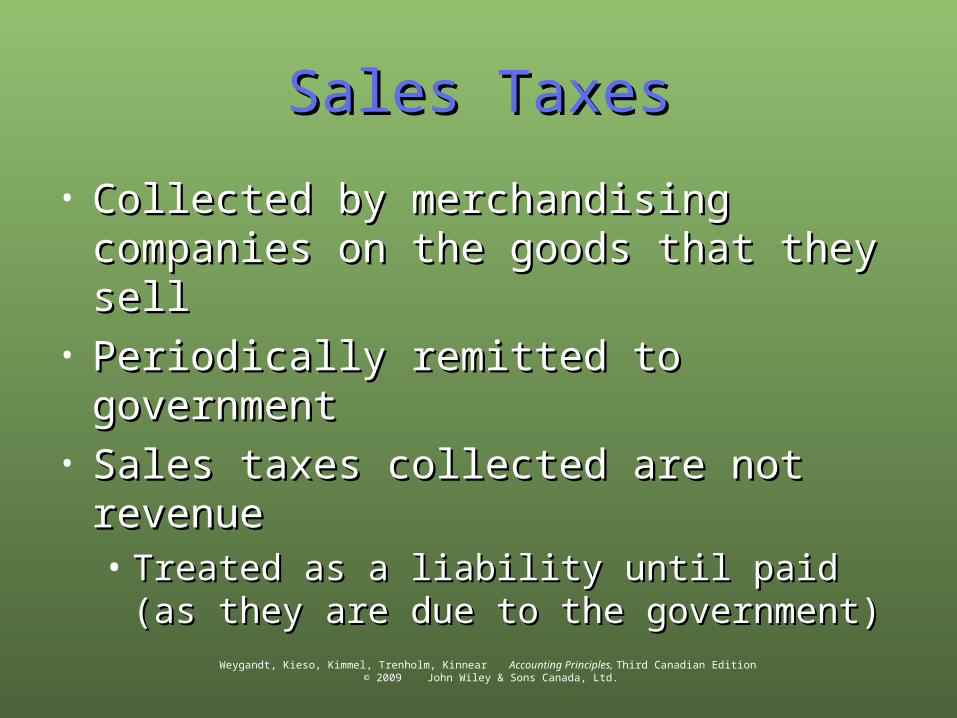

Sales TaxesSales Taxes

• Collected by merchandising companies on Collected by merchandising companies on the goods that they sellthe goods that they sell

• Periodically remitted to governmentPeriodically remitted to government• Sales taxes collected are not revenueSales taxes collected are not revenue

• Treated as a liability until paid (as they are Treated as a liability until paid (as they are due to the government)due to the government)

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

Sales Returns & AllowancesSales Returns & Allowances

• Sales returns:Sales returns: when customers return when customers return merchandise to seller for credit or refundmerchandise to seller for credit or refund

• Sales allowances:Sales allowances: when seller grants customers a when seller grants customers a price reductionprice reduction

• Seller’s entry required:Seller’s entry required:Dr.Dr. Sales returns and allowances Sales returns and allowances

Cr.Cr. Accounts receivable or cash Accounts receivable or cash

• If merchandise returned, additional entry required:If merchandise returned, additional entry required: Dr.Dr. Merchandise inventory Merchandise inventory

Cr.Cr. Cost of goods sold Cost of goods sold

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

Quantity and Sales DiscountsQuantity and Sales Discounts

• Quantity discount:Quantity discount:• Reduction in selling price due to the volume of Reduction in selling price due to the volume of

goods purchasedgoods purchased• Sale is recorded at reduced priceSale is recorded at reduced price

• Sales discount:Sales discount:• Discount offered for early payment of billDiscount offered for early payment of bill• Discount amount taken is credited to Discount amount taken is credited to Sales Sales

DiscountsDiscounts (a contra revenue account) (a contra revenue account)• Original amount in Sales is not changedOriginal amount in Sales is not changed

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

Completing the Accounting CycleCompleting the Accounting Cycle

• Same types of adjusting entries as a service Same types of adjusting entries as a service companycompany

• One additional adjustment for inventoryOne additional adjustment for inventory• To ensure the recorded inventory amount agrees with To ensure the recorded inventory amount agrees with

the actual quantity on handthe actual quantity on hand• A physical count is an important control feature A physical count is an important control feature

• A perpetual system indicates what should be thereA perpetual system indicates what should be there• An inventory count will determine what existsAn inventory count will determine what exists

• Additional accounts to be closed: Additional accounts to be closed: Sales, Sales Sales, Sales Returns and Allowances, Sales Discounts, Cost Returns and Allowances, Sales Discounts, Cost of Goods Sold, Freight Outof Goods Sold, Freight Out

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

Multiple-Step Income StatementMultiple-Step Income Statement

Sales revenueSales 480,000$ Less: Sales returns and allowances 16,700$ Sales discounts 4,300 21,000

Net sales 459,000 Cost of goods sold 315,000 Gross profit 144,000

Operating expenses Salaries expense 45,000$ Rent expense 19,000 Utilities expense 17,000 Advertising expense 16,000 Amortization expense 8,000 Freight out 7,000 Insurance expense 2,000

Total operating expenses 114,000 Income from operations 30,000

Other revenuesInterest revenue 3,000$ Gain on sale of equipment 600

Total non-operating revenue and gain 3,600 Other expenses

Interest on expense 1,800$ Casualty loss from vandalism 200

Total non-operating expense and loss 2,000 Net non-operating revenue 1,600

Net income 31,600$

HIGHPOINT ELECTRONICIncome Statement

Year Ended May 31, 2008Sales revenue

Sales 480,000$ Less: Sales returns and allowances 16,700$ Sales discounts 4,300 21,000

Net sales 459,000 Cost of goods sold 315,000 Gross profit 144,000

Operating expenses Salaries expense 45,000$ Rent expense 19,000 Utilities expense 17,000 Advertising expense 16,000 Amortization expense 8,000 Freight out 7,000 Insurance expense 2,000

Total operating expenses 114,000 Income from operations 30,000

Other revenuesInterest revenue 3,000$ Gain on sale of equipment 600

Total non-operating revenue and gain 3,600 Other expenses

Interest on expense 1,800$ Casualty loss from vandalism 200

Total non-operating expense and loss 2,000 Net non-operating revenue 1,600

Net income 31,600$

HIGHPOINT ELECTRONICIncome Statement

Year Ended May 31, 2008

Calculation of Net sales and Calculation of Net sales and Gross profitGross profit

Calculation of Income from Calculation of Income from operationsoperations

Calculation of Non-operating Calculation of Non-operating activities and Net incomeactivities and Net income

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

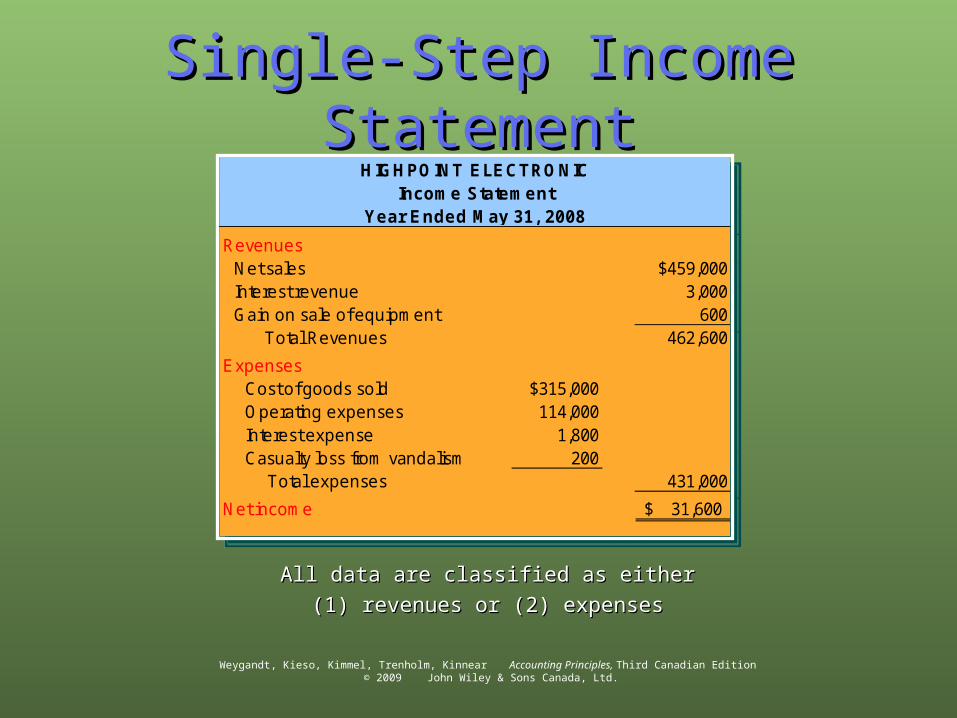

Single-Step Income StatementSingle-Step Income Statement

All data are classified as eitherAll data are classified as either

(1) revenues or (2) expenses(1) revenues or (2) expenses

RevenuesNet sales $459,000Interest revenue 3,000Gain on sale of equipment 600

Total Revenues 462,600

ExpensesCost of goods sold $315,000Operating expenses 114,000Interest expense 1,800Casualty loss from vandalism 200

Total expenses 431,000

Net income 31,600$

HIGHPOINT ELECTRONICIncome Statement

Year Ended May 31, 2008Revenues

Net sales $459,000Interest revenue 3,000Gain on sale of equipment 600

Total Revenues 462,600

ExpensesCost of goods sold $315,000Operating expenses 114,000Interest expense 1,800Casualty loss from vandalism 200

Total expenses 431,000

Net income 31,600$

HIGHPOINT ELECTRONICIncome Statement

Year Ended May 31, 2008

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

Classified Balance SheetClassified Balance Sheet

Current assetsCash 9,500$ Accounts receivable 16,100 Merchandise inventory 40,000 P repaid insurance 1,800

Total current assets 67,400 P roperty, plant, and equipment

Store equipment 80,000$ Less: Accumulated amortization 24,000 56,000

Total assets 123,400$

HIGHPOINT ELECTRONICBalance Sheet (partial)

May 31, 2008

AssetsCurrent assets

Cash 9,500$ Accounts receivable 16,100 Merchandise inventory 40,000 P repaid insurance 1,800

Total current assets 67,400 P roperty, plant, and equipment

Store equipment 80,000$ Less: Accumulated amortization 24,000 56,000

Total assets 123,400$

HIGHPOINT ELECTRONICBalance Sheet (partial)

May 31, 2008

AssetsMerchandise Merchandise Inventory Inventory reported as a reported as a current asset current asset following following Accounts Accounts ReceivableReceivable

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

Periodic Inventory SystemPeriodic Inventory SystemPurchasesPurchases

• Calculation of Cost of Goods Sold is only Calculation of Cost of Goods Sold is only performed at end of periodperformed at end of period• When physical inventory count is doneWhen physical inventory count is done

• Causes accounting entries to be differentCauses accounting entries to be different• Detailed records are not kept throughout Detailed records are not kept throughout

the periodthe period• Cost of Goods Sold is calculated at the Cost of Goods Sold is calculated at the

end of the accounting periodend of the accounting period

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

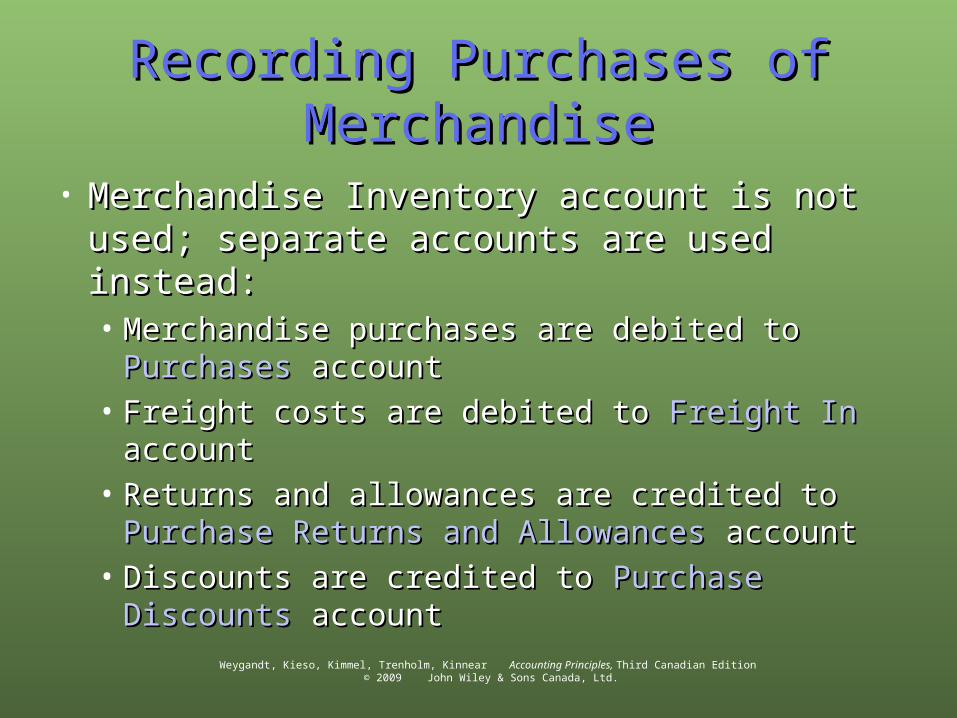

Recording Purchases of Recording Purchases of MerchandiseMerchandise

• Merchandise Inventory account is not Merchandise Inventory account is not used; separate accounts are used instead:used; separate accounts are used instead:• Merchandise purchases are debited to Merchandise purchases are debited to

PurchasesPurchases account account• Freight costs are debited to Freight costs are debited to Freight InFreight In account account• Returns and allowances are credited to Returns and allowances are credited to

Purchase Returns and AllowancesPurchase Returns and Allowances account account• Discounts are credited to Discounts are credited to Purchase DiscountsPurchase Discounts

accountaccount

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

Periodic Inventory SystemPeriodic Inventory SystemSalesSales

• At time of sale, only Sales Revenue is At time of sale, only Sales Revenue is recordedrecordedDr.Dr. Accounts receivable or Cash Accounts receivable or Cash

Cr.Cr. Sales Sales• No entry is made to recognize cost of salesNo entry is made to recognize cost of sales

• Freight costs, sales returns, allowances Freight costs, sales returns, allowances and discounts are treated the same as and discounts are treated the same as under a perpetual inventory systemunder a perpetual inventory system

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

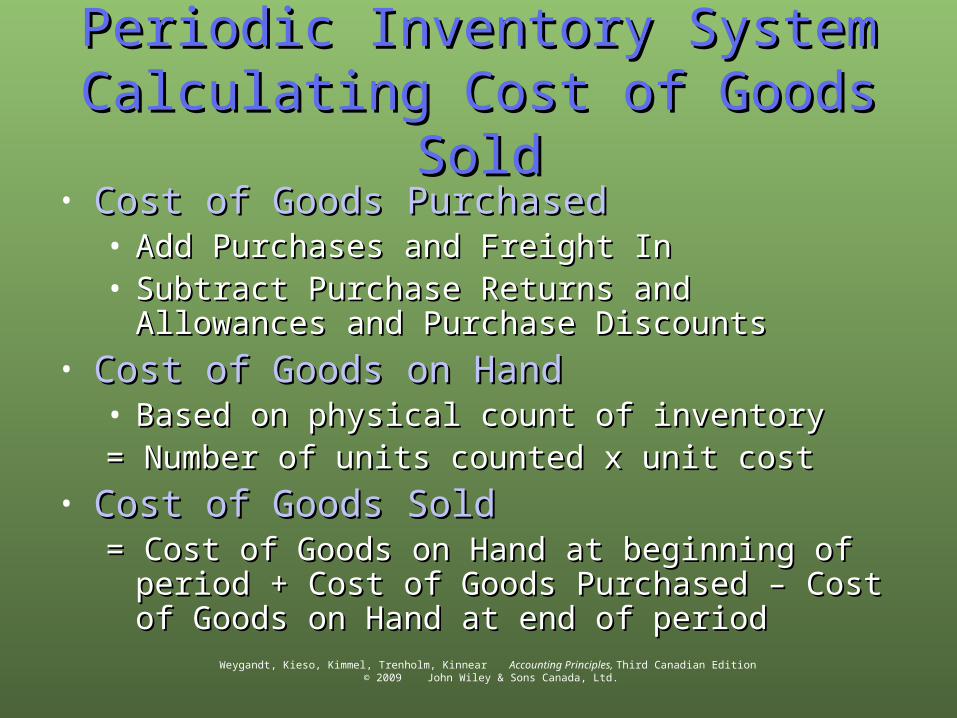

Periodic Inventory SystemPeriodic Inventory SystemCalculating Cost of Goods SoldCalculating Cost of Goods Sold

• Cost of Goods PurchasedCost of Goods Purchased• Add Purchases and Freight InAdd Purchases and Freight In• Subtract Purchase Returns and Allowances and Subtract Purchase Returns and Allowances and

Purchase DiscountsPurchase Discounts• Cost of Goods on HandCost of Goods on Hand

• Based on physical count of inventoryBased on physical count of inventory= Number of units counted x unit cost= Number of units counted x unit cost

• Cost of Goods SoldCost of Goods Sold= Cost of Goods on Hand at beginning of period + Cost = Cost of Goods on Hand at beginning of period + Cost

of Goods Purchased – Cost of Goods on Hand at end of Goods Purchased – Cost of Goods on Hand at end of periodof period

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

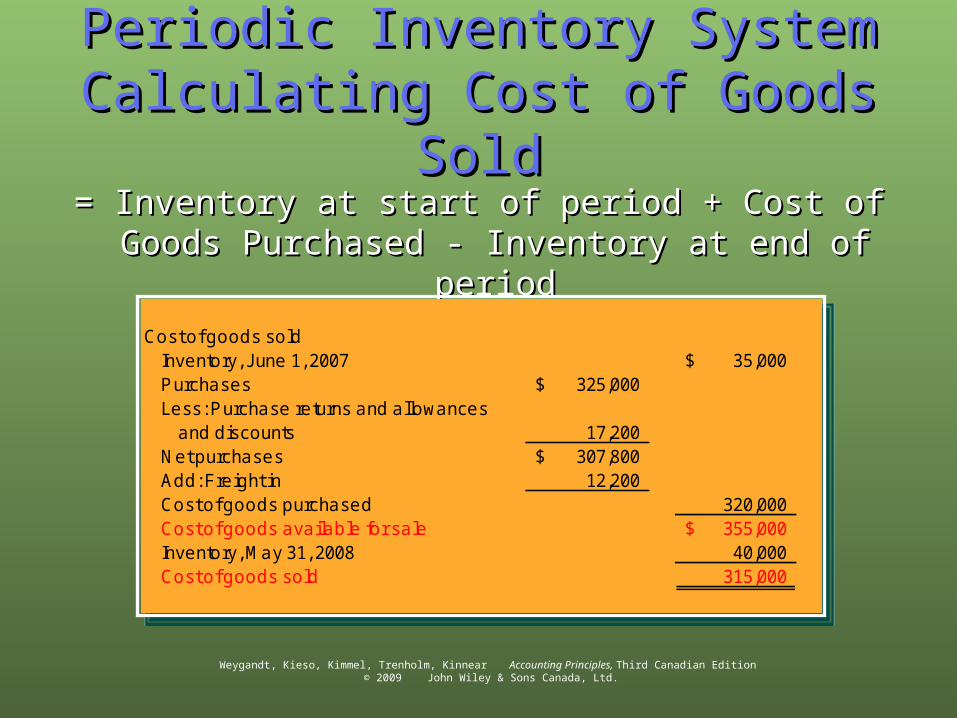

Periodic Inventory SystemPeriodic Inventory SystemCalculating Cost of Goods SoldCalculating Cost of Goods Sold

= Inventory at start of period + Cost of Goods = Inventory at start of period + Cost of Goods Purchased - Inventory at end of periodPurchased - Inventory at end of period

Cost of goods soldInventory, J une 1, 2007 35,000$ Purchases 325,000$ Less: Purchase returns and allowances

and discounts 17,200 Net purchases 307,800$ Add: Freight in 12,200 Cost of goods purchased 320,000 Cost of goods available for sale 355,000$ Inventory, May 31, 2008 40,000 Cost of goods sold 315,000

Cost of goods soldInventory, J une 1, 2007 35,000$ Purchases 325,000$ Less: Purchase returns and allowances

and discounts 17,200 Net purchases 307,800$ Add: Freight in 12,200 Cost of goods purchased 320,000 Cost of goods available for sale 355,000$ Inventory, May 31, 2008 40,000 Cost of goods sold 315,000

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

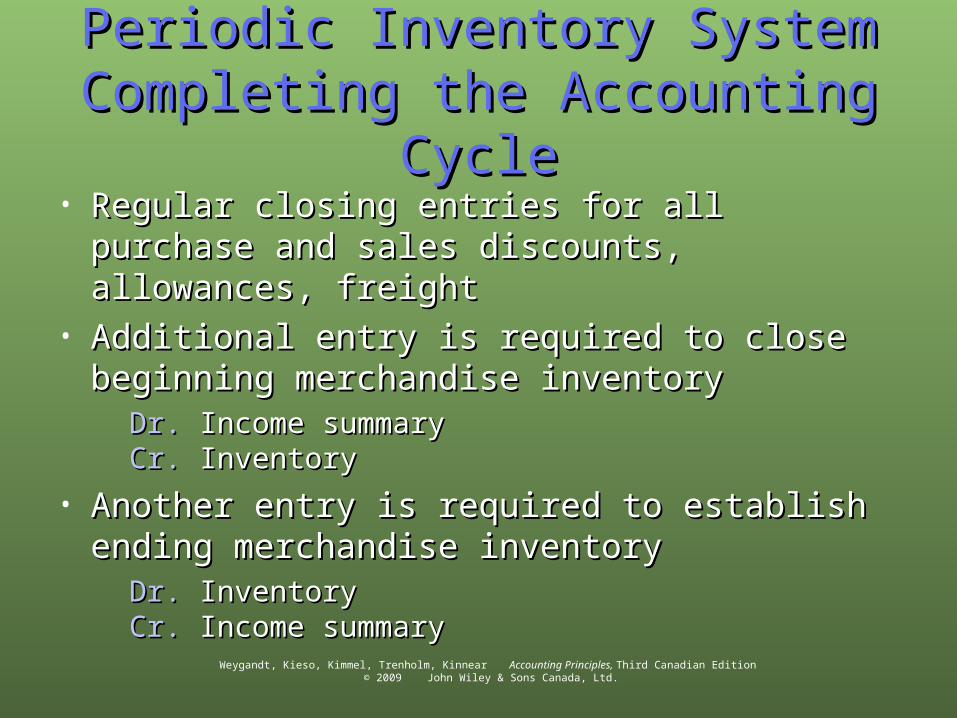

Periodic Inventory SystemPeriodic Inventory SystemCompleting the Accounting CycleCompleting the Accounting Cycle

• Regular closing entries for all purchase and Regular closing entries for all purchase and sales discounts, allowances, freightsales discounts, allowances, freight

• Additional entry is required to close beginning Additional entry is required to close beginning merchandise inventorymerchandise inventory

Dr.Dr. Income summary Income summaryCr.Cr. Inventory Inventory

• Another entry is required to establish ending Another entry is required to establish ending merchandise inventorymerchandise inventory

Dr.Dr. Inventory InventoryCr.Cr. Income summary Income summary

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

Using the Information in the Using the Information in the Financial StatementsFinancial Statements

• Profitability ratios:Profitability ratios: measure income or measure income or operating success for a specific time periodoperating success for a specific time period

• Gross profit margin: Gross profit margin: • Gross profit expressed as a percentageGross profit expressed as a percentage• Measures the effectiveness of a company’s Measures the effectiveness of a company’s

purchasing and pricing policiespurchasing and pricing policies

= Gross Profit = Gross Profit ÷÷ Net Sales Net Sales

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

Using the Information in the Using the Information in the Financial Statements 2Financial Statements 2

• Profit margin: Profit margin: • The percentage of sales that results in net The percentage of sales that results in net

incomeincome• Measures the ability of a company to cover all Measures the ability of a company to cover all

expenses and provide a return to ownersexpenses and provide a return to owners

= Net Income = Net Income ÷÷ Net Sales Net Sales

Weygandt, Kieso, Kimmel, Trenholm, Kinnear Accounting Principles, Third Canadian Edition © 2009 John Wiley & Sons Canada, Ltd.

COPYRIGHTCOPYRIGHT

Copyright © 2009 John Wiley & Sons Canada, Ltd. All rights reserved. Reproduction or translation of this work beyond that permitted by Access Copyright (The Canadian Copyright Licensing Agency) is unlawful. Requests for further information should be addressed to the Permissions Department, John Wiley & Sons Canada, Ltd. The purchaser may make back-up copies for his or her own use only and not for distribution or resale. The author and the publisher assume no responsibility for errors, omissions, or damages caused by the use of these programs or from the use of the information contained herein.