welfare reform a situation analysis · david magor obe irrv chief executive institute of revenues...

TRANSCRIPT

Welfare Reform

A Situation Analysis

David Magor OBE IRRV Chief Executive

Institute of Revenues Rating and

Valuation

The Biggest Reform of Social

Security in 60 Years

The Enabling Power

The Second Act is in Place

• DEFICIT REDUCTION

• Government’s top

priority.

• Taxpayers were paying

almost £120 million a day

(£43 billion a year) in

debt interest - more than

council tax, stamp duty

and inheritance tax

combined last year

WELFARE REFORM

• Reforming the welfare

system - to make it

fairer, more affordable

and better able to tackle

poverty, worklessness

and welfare dependency

LOCALISATION

• Coalition principles of

increasing freedom and

sharing responsibility by

localising power and

funding.

• De-ringfencing of funding,

abolition of top-down targets

and inspection regime

• The most fundamental reform of the social security system for 60 years

• A continuing deficit target

• A further £10bn

• Under 25’s

• Financial support for the family

• So far it includes the following:

• Housing Benefit changes

• Universal Credit

• Personal Independence Payment, ESA changes and specialist disability support

• Benefit cap

• Social Fund changes

• State Pension age changes

• Single Fraud Investigation Service

• Council Tax Reduction Schemes

Welfare Reform - The Wider Picture

Personal Independence Payment

Universal Credit

The Changes

Child Benefit, Carer’s Allowance (will remain)

Income related JSA Income related ESA Income Support (including SMI) Working Tax Credits Child Tax Credits Housing Benefit

Disability Living allowance

Current system New system

Contributory JSA and ESA (DWP still considering how these will work)

Council Tax Reduction and Rate Support ( schemes being considered)

… will include support for housing and children

Pension credit

Universal Credit Programme

• Migration is being diluted

• Recapping the scheme

– A reduction in complexity via a new single system for means-tested support, for;

– Working age people, in or out of work

– Support for housing, children and childcare costs

– Additions for disabled people and carers

– Requires a change in cultural attitudes to work and claiming benefit

– To use new online channels - ‘digital by default’

– Monthly household payments

– Access to a bank account and personal budgeting

Migration - Three different types

of Universal Credit claim • New Universal Credit Claim – where legacy benefits are

closed to new entrants

• Natural Migration – where a change of circumstance no

longer results in a new legacy award, but a migration of

the entire household entitlement to Universal Credit

• Managed Migration – where DWP initiates the transfer

of an entire household from legacy benefits to one

Universal Credit entitlement –

75% of claims in the first 4 years will be as a result of migration

Natural Migration

• Natural Migration is triggered by one of a number of changes of circumstances, based on employment status or family criteria, e.g.

– Move from out of work, to in work over x hours (JSA or IS to WTC)

– Household becomes responsible for a child for the first time (New claim to CTC)

– Ceased full time education (JSA to IS)

• The Natural Migration claimant journey starts with the legacy benefit being notified of an eligible change

• Migration uses the new claim process

A three phased migration strategy

April 2014

~600k

Phase 1 - phased launch of Universal Credit. All

new claims to the current benefits and credits will

be phased out by the end of April 2014.

~5m

~End 2015

Phase 2 - managed migration begins; national

approach targeting those who will benefit most

from UC

Oct 2017

~8m

Phase 3 - prioritising on safe

closure of HB teams in the final

(geographic) stages of migration

as of September 2012

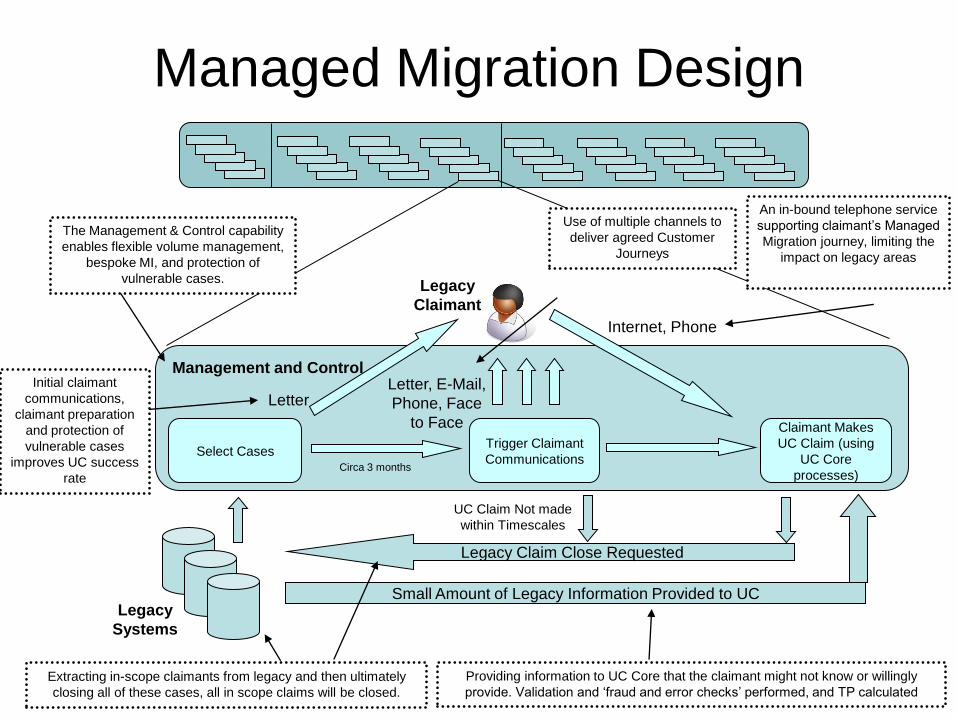

Managed Migration Design

Extracting in-scope claimants from legacy and then ultimately

closing all of these cases, all in scope claims will be closed.

Management and Control

Select Cases

Legacy

Systems

Trigger Claimant

Communications

Claimant Makes

UC Claim (using

UC Core

processes)

Legacy

Claimant

Legacy Claim Close Requested

UC Claim Not made

within Timescales

Small Amount of Legacy Information Provided to UC

Letter, E-Mail,

Phone, Face

to Face

Letter

Internet, Phone

The Management & Control capability

enables flexible volume management,

bespoke MI, and protection of

vulnerable cases.

Providing information to UC Core that the claimant might not know or willingly

provide. Validation and ‘fraud and error checks’ performed, and TP calculated

Use of multiple channels to

deliver agreed Customer

Journeys

An in-bound telephone service

supporting claimant’s Managed

Migration journey, limiting the

impact on legacy areas

Circa 3 months

Initial claimant

communications,

claimant preparation

and protection of

vulnerable cases

improves UC success

rate

Real Time Information

RTI, The Opening Salvo

The Beginning of RTI

Tom Harvey – works full time

Employer

runs

monthly

payroll

RTI to HMRC

Payment

instruction

to bank

HMRC

compare

to RTI

Bank extract hash, send to

HMRC Tom Harvey,

26,

full time

Update

taxpayer

record

HMRC

match record

Tom Harvey earnings reduced and

claims UC

Employer

runs

monthly

payroll

RTI to HMRC

Payment

instruction

to bank

HMRC

compare

to RTI

Bank extract hash, send to

HMRC Tom Harvey,

26,

full time

Update

taxpayer

record

HMRC

match record

If UC

claim,

send to

DWP

Department

for Work and

Pensions

Tom Harvey, second job

Employer 1

runs payroll RTI to HMRC,

shows amt

paid & hours

worked

Payment

instruction

to bank

HMRC

compare

to RTI

Bank extract hash, send to

HMRC

Employer 2

completes

new starter;

adds Tom

to payroll;

runs payroll

Department

for Work and

Pensions

As UC

claimed,

data to DWP

RTI to HMRC,

new starter;

amt paid &

hrs worked

Pays Tom

by cheque

HMRC

match record

Update

taxpayer

record

DWP Direct Payment

Demonstration

Projects Emerging

Learning and Findings

Early days a DWP View

It’s early days on the projects – first payments to tenants were made in July

2012

So, these are very much emerging learning and findings

And, we have committed to ensuring that we will learn throughout the projects

• We had a two day workshop in early September with the project areas

which enabled the projects to share their early findings on what went well

and not so well so far

• We will communicate our learning within DWP and with key stakeholders

There is an understanding that most of you will be interested in the amount of

arrears in the projects so far.

We are putting out a press release for the areas in October to provide an

overview including the arrears picture

In the meantime, we want to share with you some of the other things that we’ve

been learning about. Many of them will not be a surprise.

Finding: Support Assessment

Matrix

Who applicable to: Pathfinder/other live running; Universal Credit policy

development and supporting regulations; Social landlords, Local Authorities

and Support Agencies

What is being done as a result: One of the outcomes from the

September Design Review was the change to the support and exception

process used by DPDP. This process will be monitored over the project

lifecycle. The UC design area responsible for this are also working closely

with DWP and the 6 project areas.

What: The Support Assessment Matrix – used

to determine whether a tenant can go straight

onto DP with no support, straight on with some

support, or needs support for a while before DP

– needs to be supplemented with local

knowledge and insight.

Finding: Communicating with

Tenants

What: Tenants did not always respond to letters, though they responded

better to letters from their landlord than from Local Authorities and to letters in

coloured envelopes (by 42% in Shropshire). Some of the areas have had

good results with sending text messages – though, this requires having

tenants mobile phone details. Overall findings show that there is a need to

adapt the contact method depending on the demographic /geographic

characteristics of the individual area.

Who applicable to: Universal Credit policy development and supporting

regulations; Social Landlords and Local Authorities

What is being done to communicate this finding: It was captured in the

outputs from the Design Review and will be disseminated wider within DWP

to inform other testing (for example the LA led pilots) and ultimately the roll

out of Universal Credit

Finding: Tenants’ issues are

often complex

What: Tenants can often have complex and multiple

issues – e.g. they are unemployed, have literacy problems

and drug problems, The assessment process for direct

payments has uncovered the need for other services

(especially social services) to become involved.

Who applicable to: Universal Credit policy development

and supporting regulations; Social Landlords; Social

Services; Local Authorities and other Support Agencies

What is being done to communicate this finding: This

was captured in the outputs from the Design Review and

is being disseminated to the Support and Exceptions team

in DWP to inform Universal Credit and also to the

Personal Budgeting team in DWP.

Finding: the need to develop

staff

What: The project areas have found that there will be a

requirement to understand in greater detail budgeting and

finance advice for tenants.

Who this is applicable to: Local Authorities, Social

Landlords, DWP Communications

What is being done to communicate this finding: This

was captured in the outputs from the Design Review.

Money Advice Service are putting together a toolkit and

the Demonstration Projects are feeding into this. The

DWP UC Personal Budgeting team are also feeding into

this.

Finding: the need to understand

the welfare reforms

What: Staff involved in dealing with tenants will need to

understand the welfare reforms and their wider context.

Who this is applicable to: Local Authorities, Social

Landlords, DWP Communications

What is being done to communicate this finding: This

was captured in the outputs from the Design Review and

DWP Communications will be providing information, the

next Communication is scheduled for October 2012.

Finding: need to separate rent

and benefits in communications

What: Need to separate rent from benefit in all

communications to the tenant. In Universal Credit tenant

communications will need to be clear that their benefit

payment will include their rent and it is the tenants

responsibility to pay their rent. Communications that

came jointly from Local Authorities and Landlords

confused tenants.

Who is this applicable to: Universal Credit; Local

Authorities and Social Landlords.

What is being done to communicate this finding: This

was captured in the outputs from the Design Review and

will be disseminated wider within DWP Communications.

Finding: setting up bank

accounts for UC payment What: validation by the Social Landlord of the type of bank

details provided by the tenant is very important as tenants can

provide Post Office account or prepay card details which do not

accept direct debits.

Who is this applicable to: Universal Credit; Social Landlords.

What is being done to communicate this finding: This was

captured in the outputs from the Design Review and will be

disseminated wider by DWP Communications to ensure that

tenants understand that certain types of account cannot be used

for direct debits. Money Advice Service are putting together a

toolkit which may also cover this issue and the Demonstration

Projects are feeding into this.

Finding: setting up and

maintaining Direct Debit details

• What: Tenant communications understanding Direct Debits and managing these throughout their UC life, including if there is a need to stop the Direct Debit

• Who is this applicable to: Universal Credit; Social Landlords.

• What is being done to communicate this finding: This was captured in the outputs from the Design Review and will be disseminated wider by DWP Communications. Money Advice Service are putting together a toolkit which may cover this issue and the Demonstration Projects are feeding into this. The UC Personal Budgeting team are also looking at how tenants can be helped to be made financially capable.

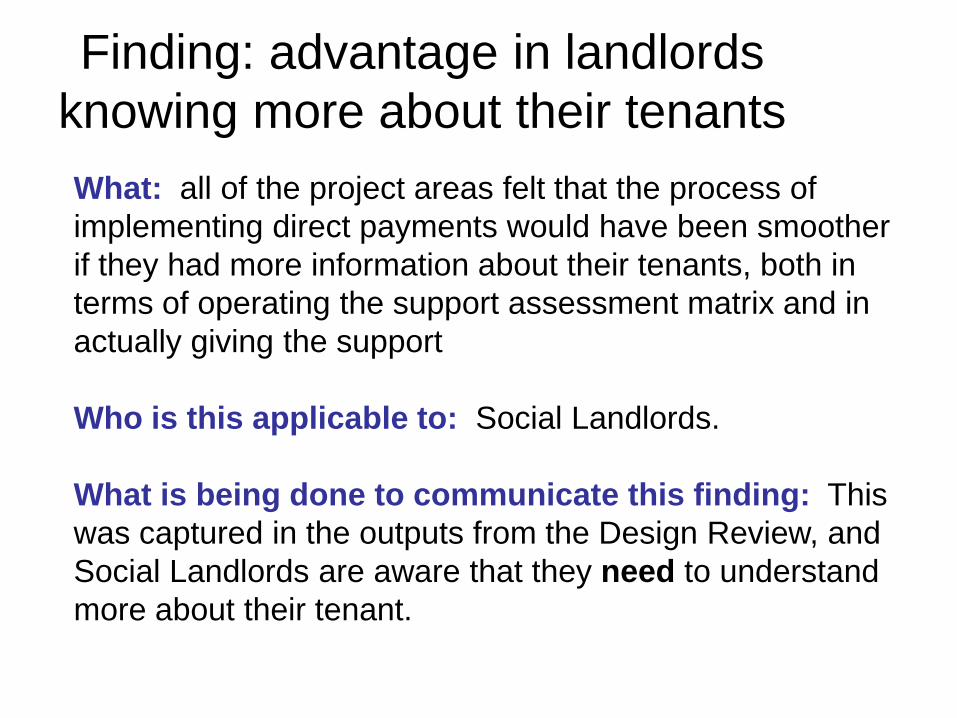

Finding: advantage in landlords

knowing more about their tenants

What: all of the project areas felt that the process of

implementing direct payments would have been smoother

if they had more information about their tenants, both in

terms of operating the support assessment matrix and in

actually giving the support

Who is this applicable to: Social Landlords.

What is being done to communicate this finding: This

was captured in the outputs from the Design Review, and

Social Landlords are aware that they need to understand

more about their tenant.

Universal Credit Calculation

Key stages in the UC calculation

process together with CTR and Data

Availability

Context • DWP currently transmits data to LAs for Housing

and Council Tax Benefit

• LAs require Universal Credit data to be transferred for CTR purposes

• The UC calculation process is markedly different from existing legacy benefits

• Devolved Administrations and LAs to clarify requirements for CTR

• Show the stages of the Universal Credit calculation

• Highlight which figures may be available for transmission to Local Authorities for the purposes of CTR assessment

• Explain which elements are still subject to design

and/or Policy activity

SUMMARY – THE KEY STAGES IN THE UC ASSESSMENT

PROCESS

STAGE 3 – CALCULATE UC ENTITLEMENT (APPLY ANY SANCTIONS, ADD ANY HARDSHIP PAYMENTS)

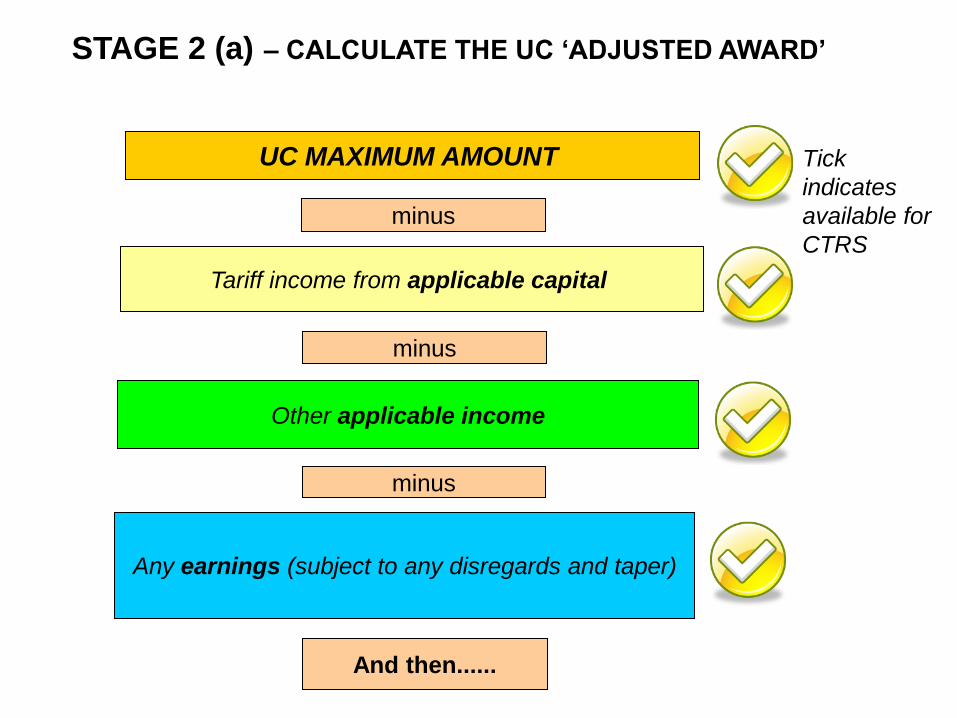

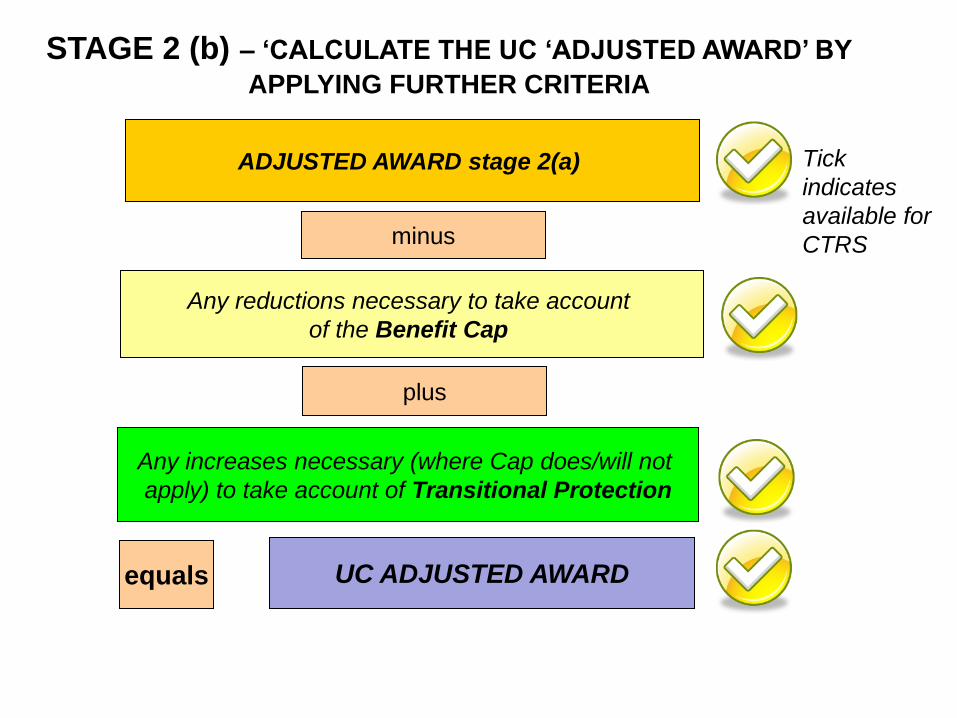

STAGE 2 – CALCULATE THE ADJUSTED UC AWARD (DEDUCT EARNINGS, CAPITAL, INCOME, BENEFIT CAP)

then

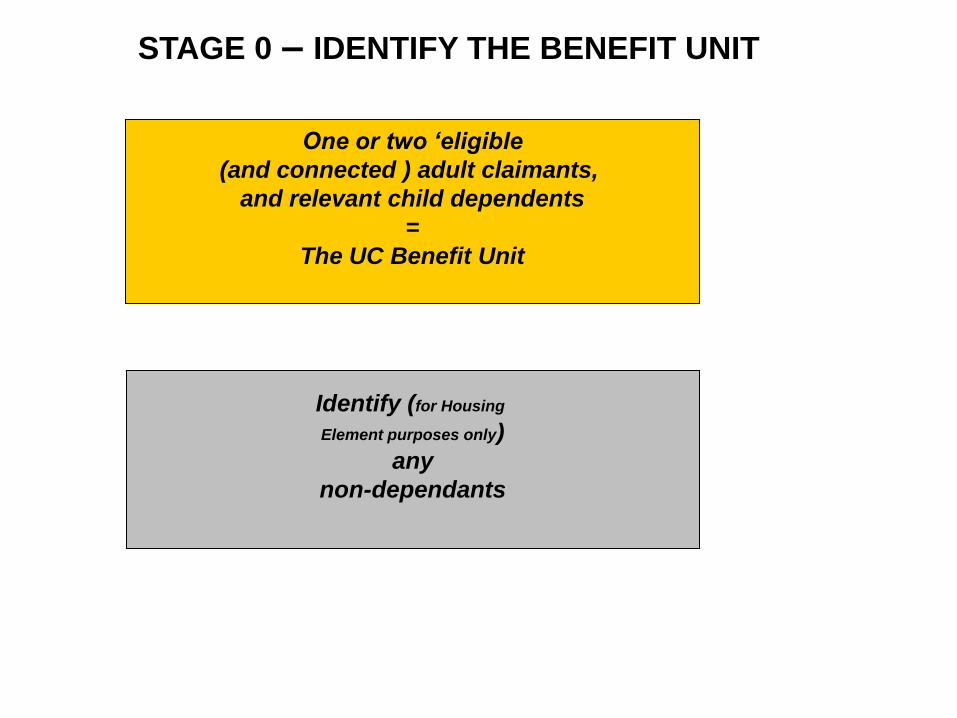

STAGE 0 – IDENTIFY WHO IS IN THE BENEFIT UNIT

(ADULTS, DEPENDENT CHILDREN AND NON-DEPENDANTS)

STAGE 1 – CALCULATE THE UC MAXIMUM AMOUNT

(TOTAL ALLOWED FOR LIVING AND HOUSING COSTS)

then

then

STAGE 4 – CALCULATE THE UC PAYMENT (ADD ANY ADVANCES, APPLY ANY DEDUCTIONS)

then

STAGE 0 – IDENTIFY THE BENEFIT UNIT

One or two ‘eligible

(and connected ) adult claimants,

and relevant child dependents

=

The UC Benefit Unit

Identify (for Housing

Element purposes only)

any

non-dependants

STAGE 1 – CALCULATE THE BENEFIT UNIT’S ‘MAXIMUM

AMOUNT’ BY ADDING UP RELEVANT AMOUNTS COVERING……

Childcare Element

Carer Element

Housing Element

L

CW

Limited capability for Work Related Activity,

or Work Element

C

are

r

Child Element/Disabled Child Additions

Standard Allowance

Ad

ult

s

Ch

ild

ren

Ho

us

ing

C

hil

dc

are

Tick

indicates

available for

CTRS

STAGE 2 (a) – CALCULATE THE UC ‘ADJUSTED AWARD’

Any earnings (subject to any disregards and taper)

Other applicable income

minus

UC MAXIMUM AMOUNT

Tariff income from applicable capital

minus

minus

And then......

Tick

indicates

available for

CTRS

STAGE 2 (b) – ‘CALCULATE THE UC ‘ADJUSTED AWARD’ BY

APPLYING FURTHER CRITERIA

Any increases necessary (where Cap does/will not

apply) to take account of Transitional Protection

minus

ADJUSTED AWARD stage 2(a)

Any reductions necessary to take account

of the Benefit Cap

plus

UC ADJUSTED AWARD equals

Tick

indicates

available for

CTRS

STAGE 3 –CALCULATE THE ‘UC ENTITLEMENT’

minus

UC ADJUSTED AWARD

Any conditionality sanctions (plus any

hardship payment amounts)

equals UC ENTITLEMENT

Tick

indicates

available for

CTRS

STAGE 4 – ESTABLISH ANY DEDUCTIONS TO BE MADE TO UC

ENTITLEMENT TO WORK OUT THE ‘UC PAYMENT’

Any short-term or

budgeting advance

UC ENTITLEMENT

plus

The UC Payment

equals

and

Any agreed

deductions

e.g. child support,

third party

rent payments)

minus

Tick

indicates

available for

CTRS

Single Fraud Investigation

Service

Progress/Current situation

4 SFIS pilots Hillingdon, Corby, Wrexham, Glasgow

1 LA Managed and in LA accommodation

Partnership working, but

Still massive uncertainty

Council Tax Reduction Schemes

Council Tax Reduction (1)

• Is your scheme developed?

• Are you out to public consultation?

• Did you meet the consultation criteria?

• What is your relationship with Major

Precepting Authorities?

• Are you talking to Local Precepting

Authorities?

Council Tax Reduction (2)

• Have you prepared you EIA?

• Have you prepared a draft tax base?

• Are you ready to manage and monitor the

collection fund?

• Have you devised your communication

strategy?

• Are you ready to finalise your scheme and

deliver it?

44

Transitional grant - overview

– Additional £100 million of funding for councils to help support

them in developing well-designed council tax support

schemes and maintain positive incentives to work.

– The voluntary grant will be available to councils (billing and

major precepting authorities) who choose to design their

local schemes so that they comply with certain criteria.

– This grant is intended to provide some headroom for those

authorities who are looking across all of their options for

funding savings to ensure that those currently in receipt of

support do not face a large tax increase –

– Funding allocations have already been published, so local

authorities know how much they could stand to receive.

– Expect that councils will make applications after 31 January

2013, and that funding will be paid in March 2013.

45

Transitional grant – criteria (1)

•Those who would be entitled to 100% support under

current council tax benefit arrangements pay between zero

and no more than 8.5% of their net council tax liability;

• Applies to both means-tested and passported

• This is before the application of non-dependant deductions /

second adult rebate – these are not caught by the scheme

criteria

• If they would be entitled to 100% support under current

rules, they cannot be required to pay more than 8.5% of their

maximum net liability (i.e. after other discounts, such as

SPD, have been applied) under the new scheme.

• This means that changes to capital rules / similar that would

make claimants currently eligible for support completely

ineligible would not be compliant with the grant.

46

Transitional grant – criteria (2)

•The taper rate does not

increase above 25%;

– Local authorities would be free to

stick to the 20% taper rate – or lower

47

Transitional grant – criteria (3)

•There is no sharp reduction in support for those entering work

– This is intended to ensure that there is no sudden drop in support as a

person’s income increases and they move off entitlement for the maximum

reduction

– It is intended to ensure that the taper operates as at present – that is, that

excess income is tapered in relation to the maximum eligible reduction

– This means schemes which cap support at a band level would not be

compliant – as the starting point for all is a greater than 8.5% minimum

liability

– Also means that schemes which, for example, require those out of work to

make no contribution but require everyone in work to make at least some

contribution before the application of the taper or non-dependant

deductions would not be compliant

The Appeal Process for CTR

The Process

• Notification

– Extent of detail

– Detailed statements

• Appeal to the local authority

– Decision

• Appeal to another place

– The Valuation Tribunal Service

– Enabling power already in place

Appealing to the VTS

• Process

• Need for regulation?

• Practice Statements

• Procedure Statements

• Sufficient expertise?

• Customer friendly?

• Is there a capacity issue?

The Hearing

• Amendment in the Bill

• Provision for cases to be heard before a

Judge in England but not in Wales

• Evidence of scheme to be formally given?

• These are liability appeals

• Will there be a crossover with UC

appeals?

• The big question “what is the potential

volume”

Is Local Government Ready

for Welfare Reform?

Local Authorities and Welfare

Reform • Local authorities, along with other public, private and

third sector organisations, have a significant role to play

in managing the changes associated with Welfare

Reform

• Local authorities will have a key role in supporting

customers and tenants during the transition to and

beyond new local services – whether you want to or not

• Local authorities will need sufficient expertise,

knowledge and capacity to effectively manage the

impact of Welfare Reform – but who is going to pay for it

• Local authorities will have to align local services with the

Government’s aims and objectives as they become

clearer

Supporting the transition

• There are a number of roles, planned and imposed by

default, for local government in preparing customers for

the changes

– By delivering new local services

– Reconfiguring service offerings to reflect post-reform world

– Some of these functions have already been started

– But, budget uncertainty is hampering change

– The impact of Welfare Reform and localism will need to be

refined, integrated and aligned strategically to existing

Local Authority services

– Time is short

Preparing customers for the

changes • Keep local government informed by

– Developing a meaningful communication strategy

– Providing generic information and advice regarding the

changes

– Tailoring the advice to ensure individual impacts are

communicated

– Signposting citizens/tenants to other sources of

information/support

– Identifying those most affected by the changes and

provide individual/tailored support and advice/guidance,

but

• Who does what ???

Development of New Local

Services

• Carry out a service review

• Adapt how existing services are delivered

• Administer local welfare provision, whatever its

going to be

• Revise council-wide/strategic approach

• Develop integrated new local services

• Create new service delivery models

• A new relationship with DWP and HMRC

Preparing the way

• Have you thought about how your authority will support

the cultural change of Universal Credit with channel shift

and personal responsibility?

• Have you considered the totality of the Welfare Reform

on your local services? Have you completed any impact

assessments on existing services?

• What will the broader advice network look like in your

authority? Have you considered aligning Welfare Reform

to other Local Authority responsibilities, specifically

those around financial and social inclusion?

In Conclusion, Some Unanswered Questions

• Is the Coalition trying to develop a new culture rather than a new system?

• Claimants are in a period of unprecedented change but are they aware of it ?

• Local Government is attempting to deliver localism, but do they know what it is ?

• CTR, one successful challenge and then what happens?

• The Government is building a 21st Century benefits system designed with flexibility and with continuous improvement from the outset in other words in reality is that chaos and uncertainty?

• What is the real position in the preparations to deliver UC ?

• Will it achieve its aim to simplify the benefits system and ensure that work pays, while providing support for those who need it?

• It is being designed as a service based on claimant journeys, what does this really mean

• Are the DWP and HMRC really working with partners and stakeholders or is the change being imposed upon them using their specialist knowledge and skills to understand and meet the challenges of the overall reform package ?

AND FINALLY !

Council tax rebate reforms risk repeat of

poll tax disaster, says IFS