welcome to the transformative agefile/ey-attractiveness-survey-malta-2018.pdf · in sum, malta...

TRANSCRIPT

Welcome to the transformative ageEY’s Attractiveness SurveyMaltaOctober 2018

EY’s attractiveness surveysEY’s attractiveness surveys are widely recognized by our clients, the media and major public stakeholders as a key source of insight into foreign direct investment (FDI). Examining the attractiveness of a particular region or country as an investment destination, the surveys are designed to help businesses to make sound financial decisions, and governments to remove barriers to future growth. A two-step methodology analyzes both the reality and perception of FDI in the respective country or region. Findings are based on the views of representative panels of international and local opinion leaders and decision-makers.

For more information, please visit ey.com/attractiveness.

Page 4Welcome

Page 6Executive summary

Page 10FDI facts at a glance

Page 18Perception

Page 26Future

Page 36EY’s bolt-on surveys: sectors in depth

Page 40 Methodology

Page 42Publications

Page 46 EY member firms in Malta

Contents

EY's Malta Attractiveness Survey 2018 3

www.ey.com/attractiveness

Disruption? Then what?Until recently, the paradigm-shifting term used to point toward the future was "disruption". No conversation was complete without it, and

it was forcefully promoted as the key to understanding practically every gnawing issue in business. Disrupting markets, processes, institutions and models started to sound like the answer, rather than the question.

It is now becoming increasingly clear that, important as it may be, disruption is the symptom rather than the cause of the fundamental changes taking place in our world. Clearly, disruption was and will remain the heads-up for a wider epochal change. But it’s only a heads up to a future we are still in the process of imagining. To come to terms with what is in store for us in the near and – even more so – distant future, we need to shift gear to a related but very distinct and much more far-reaching phenomenon. That of transformation.

Transformation is taking place everywhere around us and at all levels — in the way we communicate, buy, sell, invest, pay, work, move, instruct and learn. Even the way we decide is being transformed. Some are going as far as to contemplate our transformation as members of the human species. We are in the process of radically changing who and what we are.

Malta has made admirable strides forward to be proactive in embarking on this exciting journey, particularly with its efforts to become the blockchain island and to seriously embrace the challenge of

inTech. ositive signals a out artificial intelligence, digitalization and other emerging areas are also helpful. I am optimistic that, if we continue to pursue this path, the Transformative Age will welcome us even before we welcome it.

In this context, it is once again a pleasure to share the results of this year’s EY survey of foreign investors in Malta – what they like and dislike about this country, their hopes, plans, and warnings. Here’s a quick preview.

Although there was a decline, three out of every four investors still believe that Malta remains attractive to their usiness. E ually significant, four out of every five are committed to remain here in 10 years, while 65% have expansion plans, the highest in the last three years.

Our key attractions are tax, stability of social climate and our telecoms infrastructure. The weakest links are the stability and transparency of the political, legal and regulatory environment, R&D environment, and transport infrastructure.

Which growth sectors are current investors seeing as the carriers of our future? Tourism and FinTech have joined iGaming and digital media at the forefront — a far cry from our 2016 event, when the term "FinTech" was hardly known.

What’s the biggest risk to our attractiveness? Simple. Finding the right talent is the key challenge for 64% of current investors.

In sum, Malta remains an attractive destination for investors. But to remain so, we have to pay attention to our weaknesses and, more importantly, act upon them.

Throughout the ages, Malta was always hampered by its small size and population. But that was then. This is now. In the Transformative Age, what was a minus becomes a plus. Our small size can actually help us be more nimble and agile in our journey to the forefront of our times.

With the right mindset, a clear vision and more ambition, we can really think about the unthinkable. And from thinking it, we can proceed to making it happen.

Ronald AttardCountry Managing Partner

Welcome

EY's Malta Attractiveness Survey 20184

iGaming

Leading industries

Financial services Tourism Manufacturing

1 NSO statistics, 2018.2 Eurostat, 2018.

Area 316km1

Imports6

€5,931mExports

€3,927m18%VAT rate

3 NSO statistics, 2018.4 Eurostat, 2018.

5 NSO statistics, January–December 2017.6 NSO statistics, January–December 2017.

1964Commonwealth

membership

2004EU

membership

2008Euro

currency

Malta

Comino

Gozo

Official languages

Maltese English

436,9472

Population

€11bGDP

6.6%

GDP growth in 20173 2.2m

Inbound tourism5

Unemployment rate4

3.3%

EY's Malta Attractiveness Survey 2018 5

www.ey.com/attractiveness

Executive summary

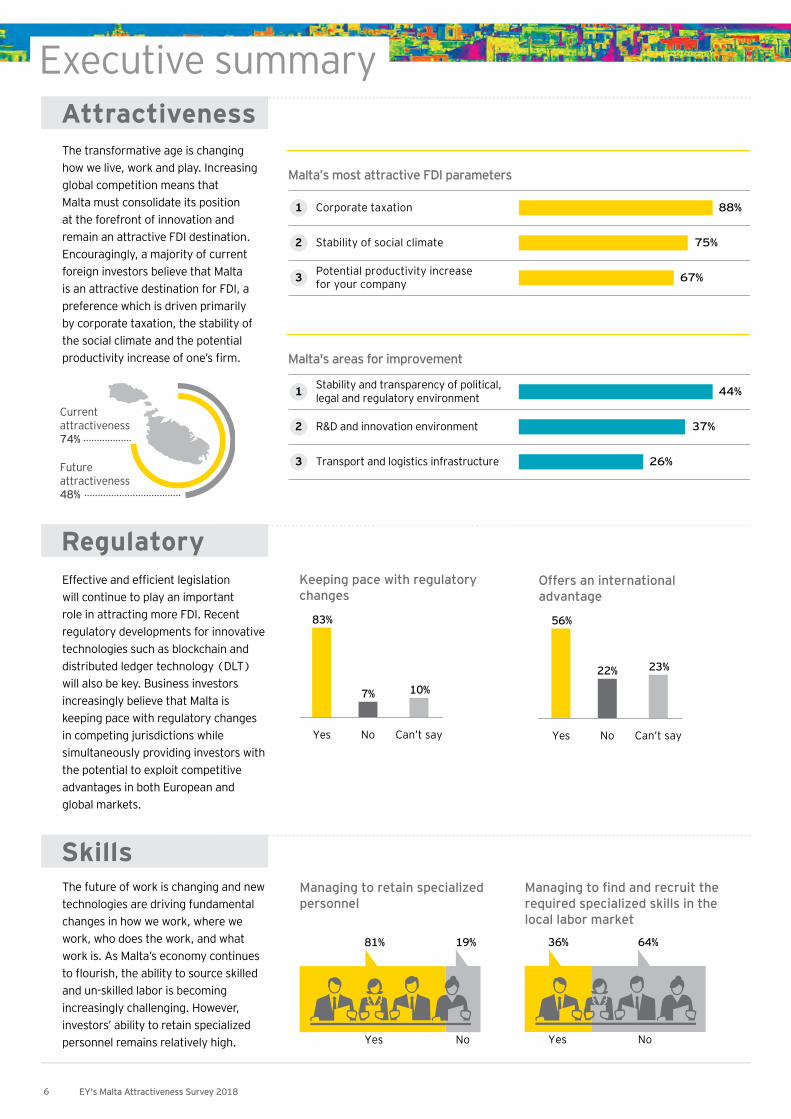

The transformative age is changing how we live, work and play. Increasing global competition means that Malta must consolidate its position at the forefront of innovation and remain an attractive FDI destination. Encouragingly, a majority of current foreign investors believe that Malta is an attractive destination for FDI, a preference which is driven primarily by corporate taxation, the stability of the social climate and the potential productivity increase of one s firm.

Effective and efficient legislation will continue to play an important role in attracting more FDI. Recent regulatory developments for innovative technologies such as blockchain and distributed ledger technology (DLT) will also be key. Business investors increasingly believe that Malta is keeping pace with regulatory changes in competing jurisdictions while simultaneously providing investors with the potential to exploit competitive advantages in both European and global markets.

The future of work is changing and new technologies are driving fundamental changes in how we work, where we work, who does the work, and what work is. As Malta’s economy continues to flourish, the a ility to source s illed and un-skilled labor is becoming increasingly challenging. However, investors’ ability to retain specialized personnel remains relatively high.

Attractiveness

Regulatory

Skills

Source: All 2018 respondents.

Keeping pace with regulatory changes

7%

No

10%

Can’t say

83%

Yes

Source: All 2018 respondents.

Offers an international advantage

22%

No

23%

Can’t say

56%

Yes

Source: All 2018 respondents.

Managing to retain specializedpersonnel

81% 19%

Yes No

Source: All 2018 respondents.

anaging to find and recruit the re uired s ecia i ed s i s in the oca abor ar et

64%

No

36%

Yes

Source: All 2018 respondents.

Malta’s most attractive FDI parameters

Corporate taxation 88%1

Stability of social climate 75%2

67%3 Potential productivity increase for your company

Source: All 2018 respondents.

Malta's areas for improvement

Stability and transparency of political, legal and regulatory environment 44%1

R&D and innovation environment 37%2

26%3 Transport and logistics infrastructureFuture attractiveness48%

Current attractiveness74%

EY's Malta Attractiveness Survey 20186

As the world forges ahead with digital transformation, decision-makers are working to ensure that the right game-changing technologies are adopted. Investors believe that around two-thirds of their staff have the right skills to keep up with these changes. The technologies expected to have the largest impact on respondents’ businesses include process automation, computing advancements and business model innovation.

For many years, Malta has positioned itself favorably on a global level. Survey respondents note that the talent shortage and economic and political instability in the EU, together with the rise in populist and protectionist feelings, will impact their future investment decision. A large majority of respondents have witnessed no change to their business since the Brexit referendum.

This is an era of unprecedented transformations with limitless opportunities. The challenge is figuring out how to leverage technology most effectively to achieve the desired business outcomes. Foreign companies continue to demonstrate their interest in retaining their business operations in Malta over the next 10 years. In addition, an increasing number of companies are planning to expand their operations.

Technology

International

Future

Technological developments and their impact on business

Source: All 2018 respondents.

Process automation 57%

Computing advancements 55%

Business model innovation 28%

Internet of things and wearable technologies 27%

Advanced materials and manufacturing techniques 10%

Autonomous vehicles 6%

None of the above 12%

Source: All 2009-18 respondents.

Right skills in place to keep up with technology

63%

Source: All 2018 respondents.

Presence in Malta in 10 years’ time

18%

3%

78%

YesNoMaybe

International risks affecting companies located in Malta

Source: All 2018 respondents.

The talent shortage 57%

The economic and political instability in the EU

(excluding Brexit)26%

The competition from emerging markets 22%

The rise in populist andprotectionist feelings among

politicians and populations22%

The impact of Brexit 19%

Effects on business sinceBrexit referendum

Source: All 2018 respondents.

4%Deteriorated

19%Improved

77%Stayed

the same

Expansion plans over the next year

Source: All 2018 respondents.

65% Yes

17% No

17% Can't say

Source: all 2018 respondents.

www.ey.com/attractiveness

EY's Malta Attractiveness Survey 2018 7

Many have expressed surprise at Malta’s economic success. They fail to understand how a small country surrounded by much larger ones that are doing so badly could be going in the opposite direction. But in the digital age, being small in landmass,

population and resources does not have to be a barrier to accomplishments. Also, one's fate is less determined by that of one's immediate neighbors. What garners results is the size of a nation’s ambition, its ability to turn that vision into a workable strategy, plus technology and talented people to turn those policies into reality.

And that is why we punch way above our weight, both in Europe and around the world. This is reflected in our positive reputation as well as our attractiveness as a country whose people want to do business and enjoy a high uality of life. Today, over one fifth of our wor ers are foreign orn, and flows last year amounted to 25% of GDP. Such success does not happen by chance. We have all worked relentlessly and in all sectors to get to where we are today.

Over the last 12 months, we have averaged real Gross Domestic Product (GDP) growth of 6% and our unemployment has fallen below 4%. But our achievements go beyond the economic, and we have been praised worldwide for our advancement in civil liberties, from strengthening freedom of the press legislation to women’s rights, upgrading our roads and health care facilities, and free transport for schoolchildren.

We have also embraced innovation, especially within T technology, ecoming the first country in the world

to pass legislation on blockchain – regulating what was previously unregulated.

This gives usiness confidence so important in a transformative age in which technology will continue to revolutionize every sector. We will continue to create an environment that helps the local and international business community to thrive: a fertile place for start-ups and entrepreneurs to be creative. And it’s working. World-renowned companies continue to relocate and expand their operations to Malta. This boosts job opportunities, generates more wealth in our economy, and puts Malta on the map through constant innovation. Globally, a country’s economic power is being increasingly judged by its technological prowess.

Naturally, we face many challenges. But we are working hard to address them. We need more skilled workers who are key to entrepreneurs’ endeavors. To do this, we are providing more information to students through an employability index, so they can see where the gaps in skills and jobs are. Our education institutes are partnering with business to create tailored courses, and we are streamlining processes to allow the recruitment of non-EU nationals. To address pressure on the housing market resulting from the high demand from those moving to Malta, we are focusing on increasing properties available on the rental market while introducing more safeguards. At the same time, we will be using part of the proceeds of our economic success to finance the largest investment in social housing and infrastructure in our country's history.

Malta will continue to be a trailblazer this year, bringing about all the necessary change to strive forward with its vision, conquering challenges and building on its achievements. And we are committed to investing in thinkers and doers to achieve even more — proving that the size of a country does not limit its ambition, economic successes and attractiveness to business.

H on. J oseph MuscatPrime Minister of Malta

EY's Malta Attractiveness Survey 20188

GDP identity from the production (output) side by sector

2012 2013 2014 2015 2016 2017

Gross value added (GV A) (%) 6, 281, 167 6, 716, 618 7, 432, 634 8, 416, 709 8, 994, 657 9, 832, 057

griculture, forestry and fishing 1 1 1 1 1 1

Mining and quarrying; manufacturing; electricity, gas, steam and air conditioning supply; water supply; sewerage, waste management and remediation activities

13 13 12 10 10 10

Construction 4 4 4 4 4 4Wholesale and retail trade; transportation and storage; accommodation and food service activities 22 23 22 23 23 22

Information and communication 6 6 6 7 7 7Financial and insurance activities 8 8 7 7 7 6Real estate activities 6 6 5 5 5 5

rofessional, scientific and technical activities administrative and support service activities 10 11 12 13 13 15

Public administration and defense; compulsory social security; education; human health and social work activities 19 19 18 17 17 17

Arts, entertainment and recreation, repair of household goods and other services 9 10 13 13 13 13

Source: NSO statistics, 2016.

Main features of country forecast: Malta2016 Annual percentage change

C urrent rices

% GDP 1998–2013

2014 2015 2016 2017 2018 2019

GDP 10191, 7 100 2. 7 8. 1 9. 9 5. 5 6. 6 5. 8 5. 1Private consumption 4790, 5 47 2. 2 2. 7 5. 6 3. 0 4. 2 4. 0 3. 7Public consumption 1671, 0 16. 4 1. 9 6. 6 3. 7 –2. 7 –0. 3 19. 8 6. 9

ross fi ed capital formation 2504, 3 24. 6 1. 8 6. 8 58. 2 1. 6 –7. 4 4. 3 7. 2

of which: equipment 1216, 5 11. 9 – 1. 7 85. 5 15. 4 –34. 2 – –Exports (goods and services) 14065, 6 138. 0 5. 4 3. 2 3. 5 4. 5 1. 6 2. 0 2. 7Imports (goods and services) 12903, 9 126. 6 5. 0 –0. 2 7. 1 1. 5 –3. 0 2. 3 2. 5Gross national income (GNI)

deflator 9586, 6 94. 1 2. 4 7. 9 10. 7 3. 3 6. 6 5. 7 4. 8

Contribution to GDP growth: Domestic demand 2. 2 4 13. 7 1. 4 0. 1 5. 7 4. 3Inventories 0. 0 –1. 2 0. 7 –0. 1 0. 6 0. 0 0. 0Net exports 0. 6 5. 4 –4. 4 4. 3 5. 9 0. 1 0. 8

Employment 1. 2 5. 1 3. 9 4. 0 5. 4 3. 9 3. 4Unemployment rate (a) 6. 8 5. 8 5. 4 4. 7 4. 0 4. 0 4. 0Compensation of employees per head 3. 7 1. 6 5. 1 2. 9 1. 1 3. 4 3. 3Unit labor cost whole economy 2. 2 –1. 2 – 0. 6 1. 5 0. 0 1. 5 1. 6Real unit labor cost –0. 2 –3. 4 –2. 9 0. 0 –2. 2 –0. 5 –0. 5Saving rate of households (b) – – – – – – –

deflator 2. 5 2. 3 2. 4 1. 5 2. 3 2. 0 2. 1Harmonized index of consumer prices 2. 5 0. 8 1. 2 0. 9 1. 3 1. 6 1. 8Terms of trade of goods 0. 3 4. 7 0. 5 –3. 4 4. 8 –0. 3 –0. 2Trade balance (goods) (c) –15. 9 –13. 4 –19. 6 –18. 3 –14. 3 –14. 4 –14. 5Current account balance (c) –3. 3 8. 8 4. 5 7. 0 12. 6 11. 5 11. 3Net lending (+) or borrowing (–) compared with rest of the world (ROW) (c)

–2. 1 10. 5 6. 2 7. 4 13. 0 12. 0 11. 8

General government balance (c) –4. 5 –1. 8 –1. 1 1. 0 3. 9 1. 1 1. 3Cyclically adjusted budget balance (d) –4. 4 –2. 1 –2. 4 0. 4 3. 3 0. 7 1. 2Structural budget balance (d) – –2. 6 –2. 5 0. 5 3. 5 0. 6 1. 1General government gross debt (c) 65. 3 63. 8 58. 7 56. 2 50. 8 47. 1 43. 4

(a) as % of total labor force. (b) gross saving divided by gross disposable income. (c) as a % of GDP. (d) as a % of potential GDP. Source: European Commission, Spring 2018 Economic Forecast.

EY's Malta Attractiveness Survey 2018 9

www.ey.com/attractiveness

1

During 2017, ME’s efforts continued to bear fruits with the approval of foreign greenfield pro ects and e pansions by foreign companies. ME also approved 97 projects in favor of Maltese investors.

E has een successful in attracting new greenfield initiatives in logistics, life sciences, advanced manufacturing, software development and digital media. These projects originated from around the globe and include but are not limited to countries such as Israel, the UK, Germany, the US, Canada, India and Switzerland. Expansions have also materialized across all major high value-added sectors such as aviation, electronics, advanced manufacturing, life sciences, ICT and digital media, further consolidating Malta’s productive sectors.

The afi viation ar , the ife ciences ar and the igital u continue to grow and are evolving into important clusters within the Maltese economy.

Taking stockThe success of Malta Enterprise (ME) in attracting investment has contri uted significantly to ensuring that the robust growth attained is sustained and nourished further.

FDI facts at a glance

FDI proj ect applications approved by ME, 2006–17

New FDI Foreign expansions

Year Proj ects approved

Average investment

per application

(€ m)

Average employment

per application

Average investment

per employee (€ )

Proj ects approved

Average investment

per application

(€ m)

Average employment

per application

Average investment

per employee (€ )

2006 24 1.19 51 23,284 17 2.43 43 56,653

2007 25 1.84 39 46,843 11 1.00 31 32,544

2008 13 1.67 40 41,892 9 0.83 16 53,571

2009 12 4.79 54 88,598 6 4.48 50 90,572

2010 2 0.16 58 2,783 2 4.10 73 56,552

2011 9 14.43 44 325,564 6 3.48 43 81,323

2012 2 1.05 19 55,263 10 2.37 22 106,757

2013 36 1.78 33 53,461 15 2.83 22 127,246

2014 28 1.33 37 35,369 15 3.66 39 92,749

2015 20 0.78 29 26,587 10 2.04 24 84,651

2016 11 12.7 48 261,910 15 3.82 41 94,243

2017 19 2.3 24 96,872 12 8.50 62 136,682

Source: ME, 2017.

EY's Malta Attractiveness Survey 2018 11

www.ey.com/attractiveness

Malta’s stock positionThe ational tatistics ffice reports that alta s stock position¹ (outward FDI investments) was estimated at €169.8 billion as at December 2017. A total of €166.4 billion was attri uta le to financial and insurance activities including

special purpose entities²) which is similar to previous years, contri uting of the total figure. This amounts to an increase of around €4.1 billion over the corresponding period in the previous year.

FDI in Malta – stock position: economic activities

J un 2014 Dec 2014 J un 2015 Dec 2015 J un 2016 Dec 2016 J un 2017 Dec 2017

€ m € m € m € m € m € m € m € m

Manufacturing 868 960 1,013 1,123 1,171 1,203 1,119 1,180

Transportation, accommodation and real estate activities 1,105 1,132 1,142 1,251 1,260 1,338 1,403 1,460

Financial and insurance activities 133,806 140,150 144,003 148,999 153,651 158,210 162,289 166,442

Information and communication 2 12 39 72 116 130 139 140

rofessional, scientific and technical activities 63 38 48 48 130 133 137 140

Other activities 250 479 337 369 358 450 361 444

Total 136, 097 142, 773 136, 195 151, 865 146, 650 161, 466 165, 451 169, 808

Source: NSO news release 024/2018 and 155/2018.

o s in a ta

2013 2014 2015 2016 2017

€ m € m € m € m

Manufacturing 101 45 138 48 3

Transportation, accommodation and real estate activities 41 32 69 89 122

Financial and insurance activities 8,839 8,457 3,894 3,257 2,664

Information and communication 4 63 34 19

rofessional, scientific and technical activities 2 6 6

Other activities 72 16 18

Total 9, 041 8, 549 4, 185 3, 433 2, 806

Source: NSO news release 155/2018.

¹ The stock position refers to the balance sheet position of FDI-related items at the end of the period. Apart from the transactions carried out during the period, the position incorporates changes in the exchange rate, valuation and others.

² pecial purpose entities are companies that, although set up in a specific country, have little or no operations in it, and have no, or a small num er of, employees. owever, since they are registered in the country, they are regarded as resident units.

EY's Malta Attractiveness Survey 201812

Malta — an iGaming hubalta was the first E em er tate to regulate the remote

gaming market in 2004 and has since established itself as a significant gaming hu with glo al relevance. ince , the i aming industry in alta has grown significantly. n , the land-based and remote gaming segments continued to grow. According to NSO’s 2017 statistics, the sector directly accounts for 11.3% of Malta’s gross value added.

The gaming industry is estimated to have generated just over €1.1 billion in terms of gross value added in 2017.

In 2017, the Malta Gaming Authority (MGA) issued a total of 165 new remote gaming licenses.

2017 2016 2015

Class 1

19 2116

Class 2

85 8889

Class 1 on 4

359

246277

Controlled skill game –

service (B2C)

11

Controlled skill game –

supply (B2B)

5

Class 3

27 3128

Class 3 on 4

22 30 30

Class 4

5966 62

Class 2 on 4

3114 12

Source: MGA Annual Report and Financial Statements, 2017.

Number of licenses issued by MGA

Forward-looking regulation toward global industry relevance

Heathcliff Farrugia hie xecutive ficer

The contribution of the gaming sector to the Maltese economy is now entrenched at around one-eighth of the total, following a period of year-on-year growth in excess of 10%. This was underpinned by the competitiveness of the jurisdiction for global operators — its reputable and robust regulatory environment, cost-effective operating structures, the availability of human capital and the overall attractive lifestyle conditions. The continued growth of the solid base of activity coupled with the attraction of new quality business is expected to sustain the gaming sector in Malta for years to come. Government and public investment promotion agencies are continuing to invest to sustain the key business

drivers that have served the industry so well over the years. At the same time, the regulator is focusing on strengthening the supervision of the sector. With the introduction of the new legal framework, additional powers given to the MGA are poised to strengthen effective supervision of this dynamic sector. This will be done through the implementation of a risk-based approach to compliance and Anti Money Laundering and Counter-Financing of Terrorism (AML/CFT) supervision, enhanced monitoring and control functions, and a thorough revamp of consumer protection standards. Simultaneously, the new framework reduces unnecessary regulatory burdens and removes duplication of checks, thereby minimizing the cost of doing business and laying the foundations for the industry to be able to embrace new technologies to better meet the needs of an ever-evolving global industry. Malta will thus continue to enhance its global relevance as an EU gaming jurisdiction of excellence by consolidating its reputation as a thought leader in industry regulation, ensuring that it remains attractive as a reputable place where operators establish themselves.

Viewpoint

EY's Malta Attractiveness Survey 2018 13

www.ey.com/attractiveness

Financial services in Malta In 2017, there was an increase in licenses, and authorizations to carry out various types of activities were registered in the investment services, trusts, pensions and insurance business sectors. According to the Malta Financial Services Authority

, companies were licensed as financial institutions under the Financial Institutions Act last year.

At the end of the year, 63 insurance undertakings held an authorization to carry on insurance and reinsurance activities in terms of the Insurance Business Act (Cap. 403). This represents a net increase of two undertakings over the previous year.

Investment services registered high levels of growth in 2017, with 162 companies licensed to provide them in terms of the Investment Services Act, 6 more than in the previous year.

The MFSA licensed 97 new funds (including sub-funds) in 2017, of which 9 were licensed as AIFs, 58 as PIF and 30 as UCITS funds.

oreover, funds were included in the list of notified s while 1 was removed from the list. The MFSA also accepted the surrender of 74 fund licenses (including sub-funds), made up of 49 PIF licenses, 12 AIF licenses, 2 retail non-UCITS and 10 UCITS licenses.

Over the course of 2017, the MFSA issued 11 new authorizations in terms of the Trusts and Trustees Act, while another two companies surrendered their authorization. This brings the number of authorizations at the end of the year to 167, 9 more than the previous year.

In addition, the MFSA issued six new acknowledgments in terms of rticle of the ecuritisation ct, of which five were securitization cell companies. Moreover, 13 cells were issued with an acknowledgment in terms of Regulation 22 of the Securitisation Cell Companies Regulations. At the end of 2017, there were 40 notified securitization vehicles, of which were securitization cell companies.

co anies ere icensed as financia institutions under the Financial Institutions Act last year.48

Beyond "nice to have"Kenneth FarrugiaC hairman, FinanceMaltaThe onset of digital transformation is gaining very strong momentum. In our

sector, it is being driven by the fast-paced developments in the FinTech space that are rapidly disrupting traditional business models, particularly in banking. These developments will in turn

ring a out significant disintermediation of the mar et.

In this context, as digital consumers are becoming more demanding, the ability to personalize experiences and customize solutions has become critical rather than just "nice to have." Consequently, long-standing institutions wishing to survive in this dynamic, challenging and fast-changing environment need to hard code a customer-centric organizational culture. It will have to be a culture that enables them to anticipate emerging changes in consumer behavior and customize relevant data interactions to ensure a better consumer journey.

Viewpoint

EY's Malta Attractiveness Survey 201814

The digitally transformed banksMario Mallia

hie xecutive ficer Bank of V alletta plc

Digitalization has been the catalyst of change and transformation of European societies and economies for decades, accelerating business activities and processes.

For 2018 and beyond, banks must contend with multiple challenges tied to regulations, legacy systems, disruptive models and technologies.

inTech firms are capturing more of the an ing value chain, providing services such as payments, cards, ATMs and traditional accounts that could erode much of the traditional bank revenues in the foreseeable future. These new entrants pose a threat to banks by raising service expectations and going between banks and their customers.

This is a time for banks to move towards being more strategically focused, technologically modern and operationally fle i le. imultaneously, they need to tac le complex regulations, new competitors and technologies.

The banking organization of the future must leverage the vast amount of insight it possesses to become the customer’s financial ecosystem hu . ith the implementation of a new core banking system in collaboration with Oracle next year, Bank of Valletta will be one of the catalysts enabling it to remain at the forefront of alta s financial sector, a forward-looking organization and a driver for Malta’s booming economy.

Welcome to the Transformative AgeMario Galea

hie xecutive ficer The global business climate in which we operate is going through a period of unprecedented transformation, simultaneously creating exciting opportunities as well as threats.In view of this, during this age of transformation, both Malta and ME are at the forefront in capitalizing on opportunities opening up in the life sciences, DLT, advanced ICT, innovative manufacturing and other sectors.

Furthermore, ME is sharpening its focus to support Malta-based industries to consolidate their base as they transform themselves to remain competitive in this new reality.

Viewpoint Viewpoint

EY's Malta Attractiveness Survey 2018 15

www.ey.com/attractiveness

Redomiciliation of companies In 2017, 106 companies transferred their operations to Malta in line with the Continuation of Companies Regulations under the Companies Act; 25% of them originated from other EU countries.

Source: MFSA Annual Report, 2017.

2016

99

2017

106

2015

92

2013

111

2014

85

Total redomiciled companies (2013–17)

Redomiciled companies in 2017 came from the following categories:

C ategory Holding 69

Other 21

Real estate 4

IT activities 2

Marketing, promotion and consultancy 2

Construction 2

Betting, gambling and gaming 1

Securities 1

Financial institutions 1

Shipping 1

Transportation 1

Wholesale trading 1

Total 106

Source: MFSA Annual Report, 2107.

Investing today for tomorrowFrank FarrugiaPresident, Malta C hamber of C ommerce, Enterprise and Industry

t first glance, this year s attractiveness scoreboard strengthens the arguments that the Malta Chamber has been making all along — the country needs to invest the proceeds of today’s economic performances to secure competitiveness tomorrow. The Malta Chamber of Commerce, Enterprise and Industry is of the opinion that this is an opportunity to initiate a thorough impact assessment of the country’s ongoing growth with a view to setting sustainable targets, identifying the ideal economic sectors for Malta. This would further recommend a way forward toward maximizing returns with the highest efficiency of resources.

Viewpoint

EY's Malta Attractiveness Survey 201816

n , the received new notifications from new entities, through the respective Home Member State regulators, intending to passport their services into Malta.

u ber o ne notifications

European credit institutions 22

Payment service 29

Electronic money 45

European insurance undertakings 20

European insurance intermediaries 226

Investment services 150

Regulated markets 1

UCITS schemes (including sub-funds) 18

EU AIFMs marketing in Malta 25

EU AIFMs managing AIFs or providing ancillary activities in Malta 19

European Venture Capital Fund (EuVECAs) marketing in Malta 10

Source: MFSA Annual Report, 2017.

Regulatory framework for virtual currencies, innovative technologies and DLT

Further to its efforts to place Malta as a hub for digital innovation, the MFSA has sought to develop a robust regulatory framework that gives blockchain and DLT industries the opportunity to innovate and develop. In 2018, the Maltese Government approved three acts, namely the Malta Digital Innovation Authority Act (MDIA), the Innovative Technology Arrangements and Services Act (ITAS) and the Virtual Financial Assets Act (VFA).

The new legislation and relevant rules aim to provide a solid regulatory and legislative framework for virtual currencies, the use of blockchain and DLT. They will help service providers to be recognized by the Government as being legitimately innovative in return for increased pu lic confidence in the accounta ility of this rapidly growing sector.

EY's Malta Attractiveness Survey 2018 17

www.ey.com/attractiveness

• Seventy-four percent of investors believe Malta is attractive for FDI.

• The highest-ranked FDI parameters are corporate taxation and the stability of the social climate.

• Developing education and skills is key to tackling skill shortages.

• a ta is ee ing ace ith regulatory changes.

2

Malta remains attractiveSeventy-four percent of foreign direct investors who responded to EY's Malta Attractiveness Survey 2018 believe that Malta is an attractive destination for FDI. This represents a four percentage point decrease over 2017. This is the second consecutive year during which the “yes” replies decreased slightly, corresponding to an increase in the “don’t know” replies. In fact, those that replied “no” have slightly decreased in number.

Analyzing the FDI attractiveness results by sector, insurance and other financial services respondents are the most positive. Respondents in the other sectors registered comparable results, with those in manufacturing being the least positive (66%) about Malta’s FDI attractiveness.

Attractivenessnsurance and other financial services respondents are the most positive.

Perception

Source: all 2013–18 respondents.

2013 2014 2015 2016 2017 2018

Foreign direct investors think that Malta is currently attractive

88%79%

84% 87%78%

74%

9%15% 11%

3%6%

6%7%

11%

11% 10%

16% Yes

No

Don't know5%

of foreign direct investors believe that Malta is an attractive destination for FDI. 74%

EY's Malta Attractiveness Survey 2018 19

www.ey.com/attractiveness

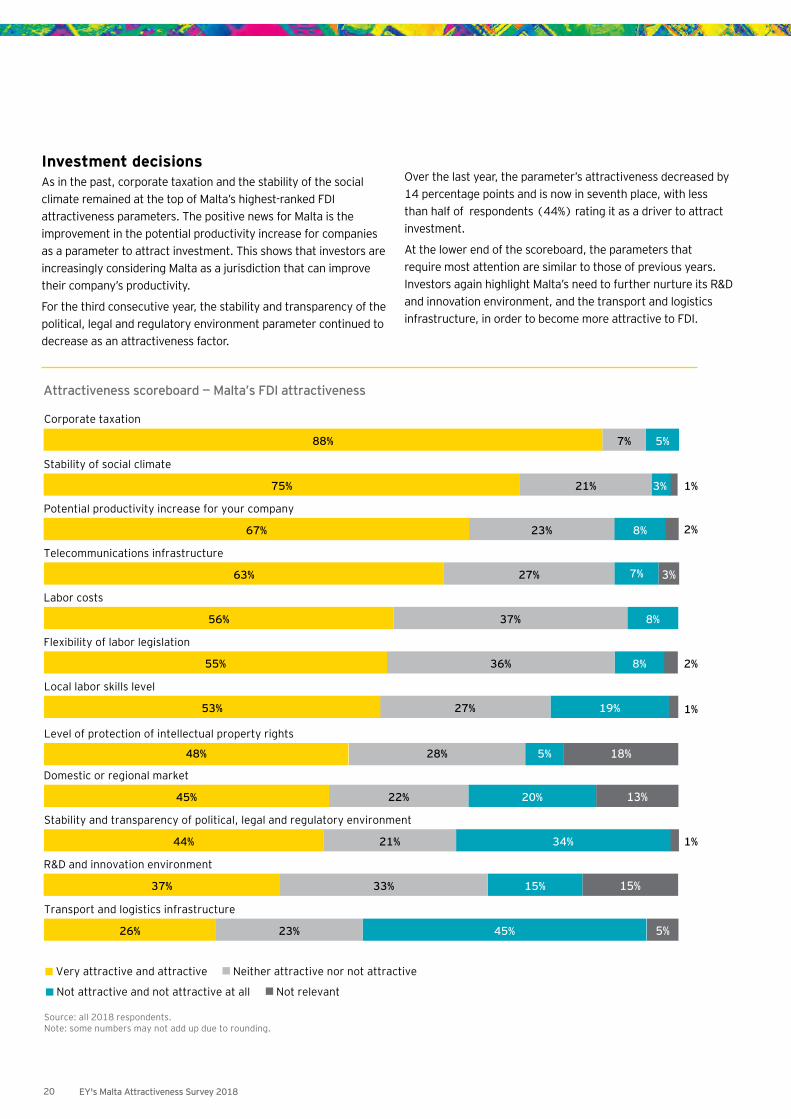

Investment decisionsAs in the past, corporate taxation and the stability of the social climate remained at the top of Malta’s highest-ranked FDI attractiveness parameters. The positive news for Malta is the improvement in the potential productivity increase for companies as a parameter to attract investment. This shows that investors are increasingly considering Malta as a jurisdiction that can improve their company’s productivity.

For the third consecutive year, the stability and transparency of the political, legal and regulatory environment parameter continued to decrease as an attractiveness factor.

Over the last year, the parameter’s attractiveness decreased by 14 percentage points and is now in seventh place, with less than half of respondents (44%) rating it as a driver to attract investment.

At the lower end of the scoreboard, the parameters that require most attention are similar to those of previous years. Investors again highlight Malta’s need to further nurture its R&D and innovation environment, and the transport and logistics infrastructure, in order to become more attractive to FDI.

8%

7%88%

Corporate taxation

Stability of social climate

Potential productivity increase for your company

5%

75% 21%

2%67% 23%

1%

Telecommunications infrastructure

63% 27% 7%

56% 37% 8%

Labor costs

Flexibility of labor legislation

Local labor skills level

Domestic or regional market

Stability and transparency of political, legal and regulatory environment

R&D and innovation environment

Transport and logistics infrastructure

55% 36% 8% 2%

53% 27% 19%

18%

Level of protection of intellectual property rights

48% 28% 5%

45% 22% 20% 13%

44%

37%

26%

21%

33%

23%

34% 1%

15% 15%

45% 5%

Very attractive and attractive Neither attractive nor not attractive

Not attractive and not attractive at all Not relevant

Source: all 2018 respondents.Note: some numbers may not add up due to rounding.

1%3%

3%

Attractiveness scoreboard — Malta’s FDI attractiveness

EY's Malta Attractiveness Survey 201820

Focus areas to remain globally competitiveIn order for Malta to remain globally competitive, respondents highlight ey areas to focus on. nce again, a significant proportion (70%) is convinced that emphasis should be on developing Malta’s education and skills. Investors would also like to see more support for high-tech and innovation industries (61%) and for small and medium-sized enterprises (59%).

A notable increase has been recorded in respondents who believe that the way forward for Malta is to tailor its regulation to keep pace with technological and other disruptions (50%).

Focus areas to remain globally competitive

Develop education and skills

Support high-tech industries and innovation

Support small and medium-sized enterprises

Invest in major infrastructure and urban projects

Allow regulation to keep pace with technological and other disruptions

Encourage environmental policies and attitudes

acilitate access to credit, including venture capital and other financial tools

Improve the quality of products and the value added to services

Reduce labor costs

Source: all 2017–18 respondents.Note: respondents could choose more than one area. Total number of mentions: 571.

Support struggling industries

Increase level of protection of intellectual property rights

Reduce taxation

Relax competition rules

None of the above

2018

70%

61%

59%

55%

50%

40%

40%

38%

31%

19%

16%

14%

3%

0%

2017

- 3%

- 3%

9%

- 8%

12%

11%

12%

11%

- 9%

3%

8%

- 3%

- 2%

0%

are convinced that emphasis should be on developing Malta’s education and skills. 70%

EY's Malta Attractiveness Survey 2018 21

www.ey.com/attractiveness

Malta’s legislative framework Eighty-three percent of investors believe that Malta is keeping pace with regulatory changes in competing jurisdictions. This proves to

e a significant increase over when only elieved so. or the third consecutive year, all insurance respondents believe Malta is keeping pace with international regulatory changes. Increases were registered across most sectors, including in iGaming and other financial services.

Fifty-six percent of respondents believe that the Maltese legislative framework creates a competitive advantage in European and global mar ets. This is reflected in an increase in yes and can t say replies over the previous two years. Respondents that indicated “no” have dropped by 11 percentage points in a single year.

The sectors with the highest num er of affirmative replies are insurance (90%) and iGaming (77%). The sectors with the highest number of “no” replies are banking (33%) and other financial services sectors .

RegulatoryThe majority of investors believe that Malta is keeping pace with regulatory changes in competing jurisdictions.

Source: all 2018 respondents.

Keeping pace with regulatory changes

10%

83%

7%18%

64%

19%

18%

71%

11%

Yes

No

Can't say

2018 2017 2016

Source: all 2018 respondents.

Offers an international advantage

23%

56%

22%

18%

50%

33%

14%

51%

34%

Yes

No

Can't say

2018 2017 2016

EY's Malta Attractiveness Survey 201822

Demand continues to outstrip supplys alta s economy continues to flourish, investors a ility to

source skilled and unskilled labor remains a challenge. Sixty-four percent of respondents face difficulties finding or recruiting the personnel they need. This figure has risen over the last four years, amounting to 47% in 2015. The sectors encountering major skill shortages include T and telecommunications , financial services (71%) and insurance (70%).

of respondents are still managing to retain their specialized personnel.81%

SkillsInvestors’ ability to source skilled and unskilled labor remains a challenge.

Find and recruit the required specialized skills in the local labor market

Source: all 2015–18 respondents.

2015 2016 2017 2018

47%36%38%

45%

Retain specialized personnel

Source: all 2015–18 respondents.

2015 2016 2017 2018

87%85% 82% 81%

Nonetheless, 81% of respondents are still managing to retain their specialized personnel, a similar result to previous years. Arguably, a high level of employee loyalty continues to exist.

As previously outlined, 70% of investors believe that it is key for Malta to continue to impart education and skills to remain attractive in the face of global competition. This result reinforces the importance of this parameter in retaining and attracting FDI to Malta.

EY's Malta Attractiveness Survey 2018 23

www.ey.com/attractiveness

The effect of international developments on businessAsked about the largest risks impacting their next investment decisions in Malta, 57% believe that the talent shortage is their most formidable challenge. The economic and political instability in the EU (excluding Brexit) is next with 26%, closely followed by competition from emerging markets and the rise in populist and protectionist feelings among politicians and populations, each with 22%.

These results can be compared with EY’s Europe Attractiveness Survey 2018, which gathers the views of 502 international decision-makers. Global and regional geopolitical instability (39%) is highlighted as the biggest source of concern for future investment decisions, followed by the economic and political stability in the EU, excluding Brexit (36%).

International Global and regional geopolitical instability is highlighted as the biggest source of concern for future investment decisions.

EY's Malta Attractiveness Survey 201824

Brexit For the second consecutive year, respondents were asked for their thoughts on Brexit and the current and projected implications it may have for their businesses. The economic and political effect of re it will most pro a ly e significant, although with such protracted negotiations, the real effect on businesses in Malta, the UK and the rest of the EU remains to be seen. According to EY’s Europe Attractiveness Survey 2018, the UK, France and Germany are classified as the top destinations for .

In 2017, we asked investors how Brexit was impacting their operations in Malta. Twelve percent indicated that their business had improved in some way, mostly in the financial services and insurance areas. nterestingly, over the past year, this figure has increased by seven percentage points. A large majority still believe that Brexit has as yet had no effect on their operations (77%), while those who feel they have deteriorated remained similar to last year (4%).

ompanies in insurance, financial services, and T and telecommunications once again generally saw more improvements, while banking, manufacturing and iGaming were mostly unaffected.

International risks affecting companies located in Malta and Europe

Talent shortage

Economic and political instability in the EU (excluding Brexit)Competition from emerging marketsRise in populist or protectionist feelings among politicians and populations

Brexit

lowdown in glo al trade flows

Lack of capital

Global and regional geopolitical instability

High volatility in currencies, commodities and other capital markets

Source: all Malta Attractiveness Survey 2018 respondents and Europe Attractiveness Survey 2018 respondents.

Unexpected rapid slowing of growth in China

None of the above

Weak innovation capacity

Malta-based companies

57%

26%

22%

22%

19%

16%

14%

13%

10%

8%

3%

12%

Europe-based companies

13%

36%

26%

34%

30%

12%

10%

39%

9%

16%

18%

2%

Difference

44%

-10%

-4%

-12%

-11%

4%

4%

-26%

1%

-8%

-15%

10%

Effects on business since Brexit referendum

Source: all 2017–18 respondents.

10% 15%2% 4%

83% 77%

4% 2% 1% 2%

ignificantlyimproved

lightly improved

No effect lightly deteriorated

ignificantly deteriorated

2017 2018

EY's Malta Attractiveness Survey 2018 25

www.ey.com/attractiveness

3

• Sixty-three percent of companies have the right s i s to ee u ith technology.

• rocess auto ation i have the biggest impact on businesses.

• eventy eight ercent i be operating in 10 years' time.

• The leading business sectors are iGaming, tourism and leisure, payments and FinTech.

Future

The transformative age Technology is reshaping whole industries and creating a fundamental shift in everything we know. The hallmark of the transformative age is the combination of unprecedented change with limitless opportunities.

TechnologyThe hallmark of the transformative age is the combination of unprecedented change with limitless opportunities.

Right skills in place to keep up with technology

Source: all 2018 respondents.

22%

73%

5%

23%

72%

4%

37%

43%

20%

Yes

No

Maybe

Board level

Managementlevel

Staff level

Technology skills at all levels combined

Source: all 2018 respondents.

No

10%

Maybe

28%

Yes

63%

Ultimately, it will be the human element that determines the extent of this transformation, founded on our skills, our hopes and our passions.

At all levels of their company, 63% believe they have the right skills in place to keep up with technology. Once again, investors are more confident a out the s ills found in their oard and management (72%). However, there are concerns about their staff's ability to keep up with rapid technological advancements (43%).

believe they have the rights skills in place to ee u ith techno ogy63%

EY's Malta Attractiveness Survey 2018 27

www.ey.com/attractiveness

To help overcome this situation, investors are suggesting that policy-makers invest in digital technologies and infrastructure (70%) as well as enhancing workforce skills for the digital age (63%).

Source: all 2018 respondents.

Enhancing investments in digital technologies and infrastructure

Enhancing workforce skills for the digital age

Strengthening the legal framework for digital business

Fostering digital innovation to modernizethe public services

Boosting digital entrepreneurship

Investing in digital R&D

None of them

70% 63% 51% 43% 42%

41%

Fostering a trustworthy ecosystem and investing in cybersecurity

34%

Strengthening the rules and regulations for data protection

19%

Other

2% 2%

Areas the Maltese Government should prioritize to support the transformation to a digital economy

Ensuring agility and dynamismNikhil Patil

hie xecutive ficer e are firmly grounded in the

transformative age. The many tools that have become a staple part of our lives, and which we largely take for granted, are seamlessly and constantly improving as a result of developments in technology. There is no escaping it. This is especially true for technology-intensive companies such as GO.

The convergence of technologies is radically transforming the services we offer to our business and private clients. We are fortunate to be living on the cusp of yet another revolutionary wave. Today, innovation is truly the name of the game.

e at firmly elieve that at the core of every innovation lies a robust and reliable communications service. Over the past years, we have been a front-runner in the level of the investments made. This has positioned us well to enable businesses of all sizes to grow and innovate. We are proud to have provided all our clients with the necessary communication services to be agile and dynamic in today’s growing markets.

Viewpoint

EY's Malta Attractiveness Survey 201828

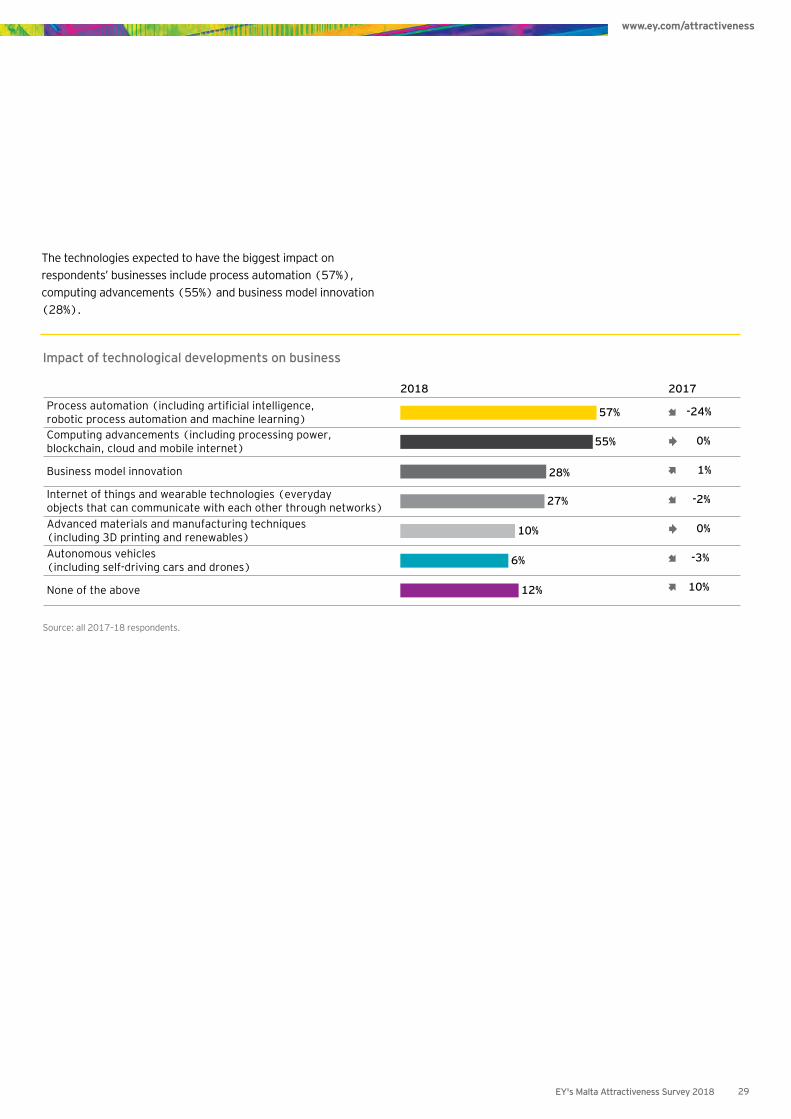

The technologies expected to have the biggest impact on respondents’ businesses include process automation (57%), computing advancements (55%) and business model innovation (28%).

Impact of technological developments on business

rocess automation including artificial intelligence, robotic process automation and machine learning)

omputing advancements including processing power, loc chain, cloud and mo ile internet

Business model innovation

Internet of things and wearable technologies (everyday objects that can communicate with each other through networks)Advanced materials and manufacturing techniques (including 3D printing and renewables)Autonomous vehicles(including self-driving cars and drones)

Source: all 2017–18 respondents.

None of the above

2018 2017

57%

55%

28%

27%

10%

6%

12%

-24%

0%

1%

-2%

0%

-3%

10%

EY's Malta Attractiveness Survey 2018 29

www.ey.com/attractiveness

Organizations are constantly adopting innovative technologies to remain ahead. This year’s survey provides insight into how foreign investors in Malta are faring with regard to technological adoption. From the list of innovative technologies provided, take-up of cloud computing (55%) is the most widespread, followed by data analytics (27%) and mobile (24%).

Blockchain and DLT are already in place for 5% of investors. However, the number of respondents expecting to have this technology in place over the next three years is expected to increase by 31 percentage points.

Cloud computing

Data analytics and big data

Mobile

Process automation (including robotic process automation)

Internet of things (IOT) and wearables

achine learning and artificial intelligence

Conversational systems, bots and virtual assistants

3D printing

Blockchain and distributed ledger technologies

Virtual reality and augmented reality

Source: all 2018 respondents.

Already in place

55%

27%

24%

22%

14%

11%

8%

7%

5%

3%

This year

8%

11%

8%

7%

3%

3%

8%

2%

7%

3%

Next three years

10%

24%

16%

19%

22%

22%

10%

6%

24%

10%

No plans yet

16%

20%

25%

21%

33%

31%

34%

23%

34%

31%

Not applicable

11%

17%

27%

31%

29%

33%

40%

63%

30%

53%

Adoption of innovative technologies

EY's Malta Attractiveness Survey 201830

In three years’ timeOur survey shows that the number of companies indicating that Malta will be attractive in the next three years has decreased by six percentage points from last year. These replies have shifted toward the “don’t know” option. In fact, the number of investors that don’t believe Malta will be attractive in three years’ is 5%, almost the same result registered in 2017.

Overall, respondents from ICT and telecommunications, iGaming, insurance and other financial services have higher levels of confidence in alta s future prospects.

FutureRespondents from ICT and telecommunications, iGaming, insurance and other financial services have higher levels of confidence in Malta's future prospects.

Source: all 2013–18 respondents.

2013 2014 2015 2016 2017 2018

Malta's FDI attractiveness in three years' time

63%

52%56% 58%

54%48%

35%

44%41%

2% 4% 4%

39%42%

4% 5%

47%

Yes

No

Don't know3%

EY's Malta Attractiveness Survey 2018 31

www.ey.com/attractiveness

Investors committed to Maltaeventy eight percent of the surveyed foreign firms elieve they

will still be operating in Malta in 10 years’ time, a result that is consistent with the last couple of years. Only 3% of investors do not believe they will be present in Malta. With increasing globalization and ease of doing business internationally, this is considered to be a positive result for Malta.

of the surveyed foreign fir s be ieve they i still be operating in Malta in 10 years’ time.78%

Source: all 2018 respondents.

Presence in Malta in 10 years’ time

18%

3%

78%

YesNoMaybe Differencefrom 2017

-2%

Banking on the futureMichel CordinaH ead of C ommercial Banking, H SBC Bank Malta plcThe Fourth Industrial Revolution

is transforming the way we do business, changing client expectations and shifting competition. Customers today expect a banking service with a seamless interface, immediacy of response and extreme portability.

At HSBC, we have the vision to create the next level of customer engagement, with innovations in artificial intelligence, cloud, the IoT, application programming interface (APIs), data analytics and blockchain powering our solutions and services. This our focus, and our US$2 billion investment in technology between 2015 and

has started to enefit our customers.

Since the 2017 EY Malta's Annual Attractiveness Event last cto er, alta has cele rated a num er of firsts in the

country by launching contactless technology and biometric logins.

HSBCnet has been digitized: our HSBCnet Mobile App now recognizes either the face or fingerprint as the password and HSBCnet Move Money now offers near real-time tracking of payment flows. urther, the overall loo and interface of net has been made intuitive, with access options that are designed for the modern-day browsing experience.

y wor ing with technology leaders and financial services regulators, HSBC is pioneering a number of initiatives for the

enefit of our customers. ur unparalleled glo al digital footprint allows us to deploy these technologies quickly and at scale to keep on transforming their experience.

Viewpoint

EY's Malta Attractiveness Survey 201832

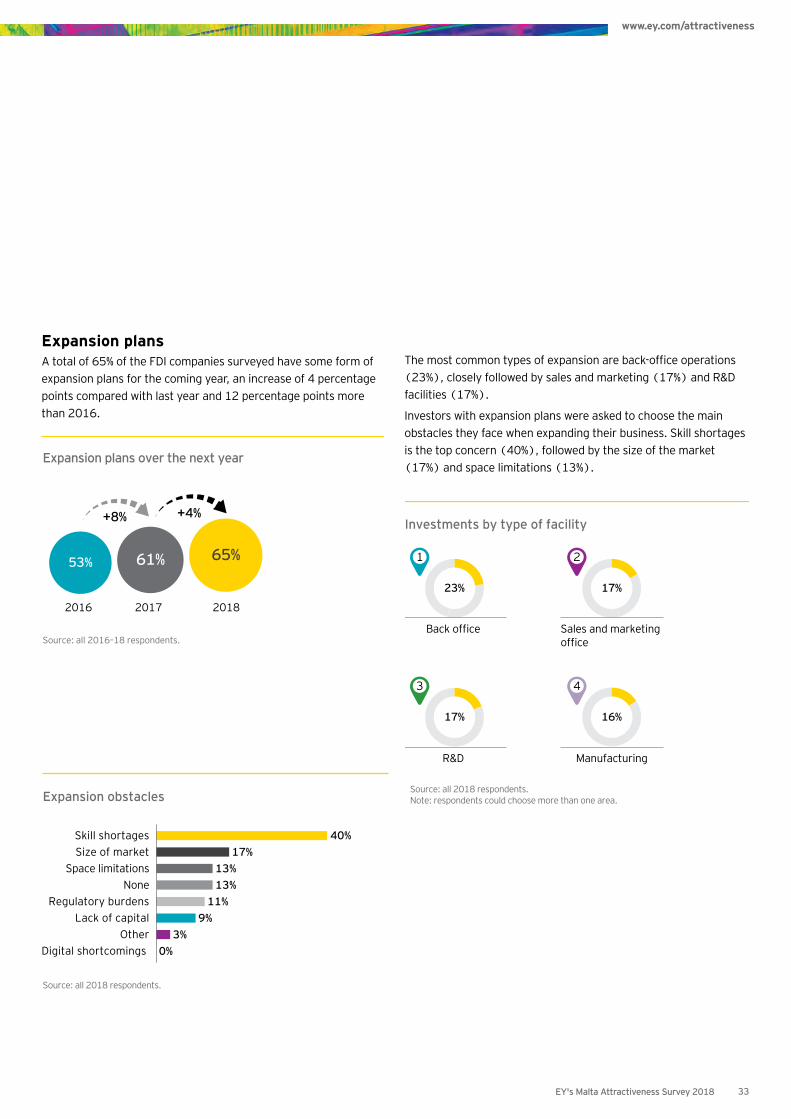

Expansion plansA total of 65% of the FDI companies surveyed have some form of expansion plans for the coming year, an increase of 4 percentage points compared with last year and 12 percentage points more than 2016.

The most common types of e pansion are ac office operations (23%), closely followed by sales and marketing (17%) and R&D facilities (17%).

Investors with expansion plans were asked to choose the main obstacles they face when expanding their business. Skill shortages is the top concern (40%), followed by the size of the market (17%) and space limitations (13%).

+4%

2018

65%

+8%

61%

2017

Source: all 2016–18 respondents.

2016

53%

Expansion plans over the next year

Source: all 2018 respondents.Note: respondents could choose more than one area.

Investments by type of facility

23%

1

ac office

17%

2

Sales and marketing office

17%

3

R&D

16%

4

Manufacturing

Source: all 2018 respondents.

Expansion obstacles

40%17%

13%

11%9%

3%0%

Skill shortagesSize of market

Space limitations13%None

Regulatory burdensLack of capital

OtherDigital shortcomings

EY's Malta Attractiveness Survey 2018 33

www.ey.com/attractiveness

Leading business sectors in the next five yearsThe key sectors envisaged to drive Malta’s growth in the next five years are i aming , tourism and leisure and payments and FinTech (45%). These results are similar to those of previous years.

However, a few “other” responses indicated innovative and distributed ledger technologies, such as blockchain, as the leading

usiness sectors in alta in the ne t five years.

Leading business sectors in the next five years

iGaming

69%

Tourism and leisure

48%

Payments and FinTech

45%

Digital media and games

42%

Real estate, infrastructure and construction

33%

Aviation

32%

Professional services (legal, accounting, research, consulting, advertising and communication and affiliate

31%

ther financial services

30%

Asset management

28%

ICT and telecommunications

27%

Fund administration

19%

Insurance

18%

Maritime

16%

Pharmaceuticals and biotechnology

15%

High technology manufacturing

14%

Banking

12%

Source: all 2018 respondents.Note: respondents could choose more than one area. Total number of mentions: 551.

EY's Malta Attractiveness Survey 201834

Malta, along with the rest of the world, is going through an unprecedented era of change and opportunity. In order to capitalize on the opportunities in the transformative age, the country needs to act quickly and rationally, focusing on the areas in which its competence will stand out against strong international competition.

This year’s survey results have again highlighted areas in which Malta is excelling and those in which more needs to be done. Skills shortages remains a serious issue. Simultaneously, however, companies may be increasingly looking to technological advancements, such as automation, to fill e isting gaps and to increase output and efficiency.

The international landscape continues to play its part, with Brexit’s deadline looming on the horizon and ongoing economic and political challenges in the EU. The Maltese economy’s resilience to international economic developments will be crucial in the years to come.

Investors in various sectors are viewing recent regulatory updates in a favora le light. Effective and efficient legislation will continue to play an important role in attracting further FDI to Malta’s shores. New laws passed will need to balance adequate protection for sta eholders with the prudence not to stifle usiness.

Finally, Malta’s image and brand is a vital element for investors when choosing to set up or even relocate their business to Malta. Positioning the island at the forefront of innovation, while remaining true to the principles and values that the country has grown accustomed to, will be even more relevant going forward than ever before.

Concluding remarks In order to capitalize on the opportunities in the transformative age, the country needs to act quickly and rationally, focusing on the areas in which its competence will stand out against strong international competition.

EY's Malta Attractiveness Survey 2018 35

www.ey.com/attractiveness

Communication transformationCommunication is a vital part of all business strategies and can have a significant impact on business growth and development. Eighty-nine percent of respondents believe that telecommunications services are highly critical (62%) or critical (27%) to their business strategy.

The vast majority of respondents are satisfied with the level of their telecommunications services, including fixed broadband as well as fixed and mobile telephony. Fixed broadband is the most highly rated of the three telecommunication services surveyed. Fifty-eight percent of investors believe that the telecommunications sector is evolving at a rate conducive to innovation, while 17% do not believe it is and 25% don't know.

62%

Importance of telecommunications services to companies’ business strategies

Source: all 2018 respondents.

27%11%

Highly critical Critical Not critical

58%

Telecommunications sector evolving at a rate that is conducive to innovation

Source: all 2018 respondents.

17%

25%

Yes No Don’t know

Satisfaction levels with telecommunications services

Source: all 2018 respondents.

Very satisfied Satisfied Indifferent

Less satisfied Dissatisfied

17% 62% 12% 8% 1%

16% 58% 15% 9% 3%

11% 52% 30% 3%3%

Fixed broadbrand

Mobile telephony

Fixed telephony

EY’s bolt-on surveys: sectors in depth

Over the last few years, EY’s attractiveness bolt-on surveys have sparked considerable interest, as entities and institutions wish to gain insights from EY by asking a range of questions that are relevant to certain sectors. The objective is to use this unique opportunity to ask specific cohorts particular questions, in order to gauge the perceptions of investors and the business community. Entities that participated in this part of EY's Malta Attractiveness Survey 2018 include the Malta Communications Authority (MCA); Malta Industrial Parks (MIP); the MGA; the Malta Freeport Corporation Ltd. (MFC) and the Malta Investment Management Company Limited (MIMCOL).

EY's Malta Attractiveness Survey 201836

Start-ups rising Sixty-two percent of investors believe that Malta is an attractive start-up location. When asked which sector is the most attractive for start-ups, respondents indicated that it is the iGaming sector. The businesses that should be targeted by a business accelerator include FinTech, digital business and iGaming. The top three support measures needed to create a sustainable start-up ecosystem include financial — tax incentives (67%), financial – grants (50%) and fast-track visas for tech employees (non-EU nationals) (50%).

Source: all 2017–18 respondents.

62%Yes

10%No

28%Don’t know

–2%

–4%

+7%

Malta remains an attractive start-up location

of investors believe that Malta is an attractivestart-up location.62%

Source: all 2018 respondents.Note: respondents could select no more than three responses. Total number of mentions: 301.

Sectors to be targeted by business accelerators

48%FinTech

29%Digital business

29%iGaming

20%Big data and artificial intelligence

17%Renewable energy

17%Software

17%E-tourism and travel tech

11%Biotech and pharma

Source: all 2018 respondents.

The attractive sectors for start-ups

57%

18%

10%

40%

16%

10%

26%

16%

9%

iGaming

Digital media and games

Maritime

FinTech

Aviation

Biotechand pharma

Digital business

Software

Big data and artificial intelligence

EY's Malta Attractiveness Survey 2018

www.ey.com/attractiveness

37

Malta as an international logistics hub Malta’s strategic location, in the heart of the Mediterranean, is perfectly suited to create a competitive regional trade and logistics hub.

When asked whether Malta would be considered as a distribution hub in a free trade zone environment, 18% of all survey respondents replied positively. Seven percent showed interest in setting up in a common user facility managed by a public-private partnership.

Malta as an international logistics hub

Malta as a distribution center or hub

18%

18%

63%

Malta as a distribution center or hub in a

special economic zone

15%

17%

69%

Malta as a third-party logistics provider

12%

19%

69%

Setting up in a common user facility that is managed by a

public-private partnership

7%

21%

72%

Source: all 2018 respondents.

Yes No Not applicable

Source: all 2018 respondents.Note: respondents could choose more than one area. Total number of mentions: 446.

Financial − tax incentives

67%

Financial − grants

50%

Fast-track visas for tech employees (non-EU nationals)

50%

Facilities and premises

44%

Residency visasfor entrepreneurs (non-EU nationals)

38%

Introduction of skill sets for new economy at schools

36%

Networking opportunities

35%

Support measures needed to create a sustainable start-up ecosystem

EY's Malta Attractiveness Survey 201838

iGaming for the futureiGaming investors in Malta believe the regulatory developments that will have the biggest impact on their business include the New Regulatory Framework, followed by the Fourth AML Directive. Survey respondents also believe that taxation, General Data Protection Regulation (GDPR), transparency, blockchain, responsible gaming initiatives, and licensing should be priority policy actions. Moreover, it is believed that international cooperation and bilateral relations with other countries should be fostered and strengthened further for the overall benefit of the gaming sector.

Industrial AgeWithin the "Future" section of this report, 13% of investors highlighted that their expansion plans are hindered by space limitations. Sixty-five percent of MIP tenants believe that the best solution to offset Malta’s lack of space is to build multistory industrial parks.

Source: all 2018 iGaming and gaming respondents.

Regulatory developments with the biggest impact in the next three years

New regulatoryframework

1

Fourth AML Directive

2GDPR

365%

Building multistory industrial parks

Source: all 2018 respondents.

13%

22%

Yes No Don’t know

of MIP tenants believe that the best solution to offset Malta’s lack of space is to build multistory industrial parks.65%

EY's Malta Attractiveness Survey 2018 39

www.ey.com/attractiveness

4

Methodology

Full-time employees: Malta

More than 100

Between 50 and 100

Between 10 and 50

Less than 10

20%

17%

29%

34%

Full-time employees: global

More than 100

Between 50 and 100

Between 10 and 50

Less than 10

52%

12%

21%

15%

Source: all 2018 survey respondents.

Size of Maltese companies in terms of revenue

Less than €1m24%

Between€1m and €2m

14%

33% Between€2m and €12m

12% Between €12m and €35m

5% More than €150m

Between €35m and €150m

11%

Percentage of revenue exported

0%1%–10%11%–25%26%–50%51%–75%76%–100%

39%

10%

8%

34%

4%5%

Asia

North America

South America

Middle East

Europe

Africa

Worldwide

Key target markets

A total of 115 current FDI companies or investors responded to EY’s e-survey, conducted between March and May 2018. The respondents’ cohort profile was very similar to that of previous EY surveys, reflecting a range of sectors and sizes. This creates the opportunity to compare results over time, whenever possible.

79%

24%

17%

14%14%

9%

4%

EY's Malta Attractiveness Survey 2018 41

www.ey.com/attractiveness

Publications

The Malta Alternative Investment FundsThe Alternative Investment Fund Managers Directive has introduced a pan-European regulated branded investment fund that targets professional and sophisticated investors, which enefits from mar eting provisions that had previously only been available to UCITS funds. The Malta Alternative Investment Funds: a technical guide provides an in-depth analysis of the regulations governing the formation and operation of these type of fund structures in alta, and how they fit within the scope of the directive.

http://www.ey.com/Publication/vwLUAssets/EY_-_The_Malta_Alternative_Investment_Funds/$FILE/ey-the-malta-alternative-investor-funds.pdf

EY’s Europe Attractiveness Survey 2018 EY’s Europe Attractiveness Survey has been tracking these investment decisions since 2000. This year, it reveals an infle ion in the pace of inflows, influenced y four powerful undercurrents of change. e thin these are true game changers because, sweeping in from different directions, they are rewriting the European rulebook on cross-border investment.

https://www.ey.com/Publication/vwLUAssets/ey-attractiveness-survey-europe-june-2018/$FILE/EY-Attractiveness-Survey-Europe-June-2018-Game-changers.pdf

The Malta Alternative Investment Fund ManagerThe Alternative Investment Fund Managers Directive has introduced new concepts and regulations to the wealth and asset management industry. The Malta Alternative Investment Fund Manager: a technical guide seeks to provide clarity to the myriad of regulations that have been introduced by this directive, how it has impacted the Malta asset manager regime, and the regulations governing the formation and operation of asset managers in Malta.

http://www.ey.com/Publication/vwLUAssets/EY_-_The_Malta_Alternative_Investment_Fund_Manager/$FILE/ey-the-malta-alternative-investor-fund-manager.pdf

Beyond this economic horizon At EY Malta's Attractiveness Event 2015, we brought forward a number of proposals, which were subsequently discussed at length with many private and public stakeholders in each sector. They covered commodity trading, logistics, FinTech, Asian e-commerce and turning regular immigrants from a challenge into an opportunity.

https://www.ey.com/Publication/vwLUAssets/ey-beyond-this-economic-horizon/$FILE/ey-beyond-this-economic-horizon.pdf

EY's Malta Attractiveness Survey 201842

Securitization: the Malta propositionEmerging as an international domicile of choice for securitization vehicles, Malta provides several highly credited services that have generated significant growth within their respective mar ets in alta. everal advantageous elements include:

• Tax neutrality, meaning that there is no additional tax burden at any level of securitization

• ualifications and nowledge of wor force

• Flexible regulatory environments that can adapt to the needs of structures

• Accessibility and responsiveness of the tax and supervisory authorities

• Expertise and cost competitiveness of locally based service providers

• The ability to outsource, to the extent possible, both within the domicile and cross-border

http://www.ey.com/Publication/vwLUAssets/EY-securitization-the-malta-proposition-2016/$FILE/EY-securitization-the-malta-proposition-2016.pdf

The Malta UCITS Investment FundsThe greatest enefit of the T rand is the high level protection it offers to investors and its mar eta ility. The Malta UCITS Investment Funds: a technical guide provides an introduction to the UCITS brand and how it fits within the scope of the T irective. t also provides an overview of alta as a center for these types of investment funds, and a summary of the regulations governing the formation and operation of UCITS investment funds in Malta.

https://www.ey.com/Publication/vwLUAssets/ey-the-malta-ucits-investment-funds/$FILE/ey-the-malta-ucits-investment-funds.pdf

The Malta Professional Investor FundsThe Malta Professional Investor Funds: a technical guide provides an introduction to one of Malta’s primary investment fund structures. The success of the structure can e udged on its regulatory efficiency and fle i ility, which is e tremely eneficial, especially for start up funds esta lishing themselves in an E urisdiction. Our technical guide provides an introduction to the formation, operation and regulation of such investment fund structures and e plains how this structure would fit within the scope of the lternative nvestment und anagers Directive.

http://www.ey.com/Publication/vwLUAssets/ey-the-malta-professional-investor-funds/$FILE/ey-the-malta-professional-investor-funds.pdf

EY economic seriesThe Economic Advisory Team at EY Malta conducts economic research and studies on various economic areas. In connection with this year’s EY economic series event, the team has conducted a study on the Maltese property market.

The study analyzes the latest trends in the market, particularly developments related to property prices by locality. The market has been characterized by rapidly rising property prices, which have shown an average annual growth rate of 4.5% over the last 15 years. The research also provides insights on factors driving the property market and their effect on the sustainability of this market. Factors such as end-user affordability, vacant property, regulation and government initiatives are analyzed in the research study. With the use of property listing data, it was possible to obtain insights on the property market by region and locality, with diverse trends and characteristics being observed across localities.

For further information, contact: [email protected].

EY's Malta Attractiveness Survey 2018 43

www.ey.com/attractiveness

HighlightsEY Malta's AnnualAttractivenessEvent25 October 2017

60+speakers

250companies

delegates1,000

EY mem er firms in alta

About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital mar ets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY member firms in MaltaEY mem er firms in alta form part of the E E area and ring together 98 EY country practices. No other big four organization has achieved this level of integration on such a scale, with such scope. e are the first professional services organization to bring a borderless approach to the emerging markets of the Commonwealth of Independent States, India, the Middle East, Africa and the established markets of Europe.

EY has been operating in Malta since the late 1990s. The member firms have een growing rapidly and now employ more than people locally. We provide assistance to a wide range of clients, from private individuals and entrepreneurial businesses to major public companies and large multinationals. We help them to anticipate, define and deal with issues that are critical to their success.

Effectively, EY mem er firms in alta have four service lines — Assurance, Tax, Transaction Advisory Services and Advisory — comprising 19 business units, each with its own head. Our newly esta lished anaged ervices hu supports the financial services industry in meeting regulatory and reporting requirements. The Managed Services Team in Malta works closely with our Managed Services delivery centers in the UK to provide support to global financial institutions.

Assurance

• Asset Management

• Banking

• Industrial and Commercial

• Insurance

Tax

• International Tax Services

• Accounting, Compliance and Reporting

• Business Tax Compliance

Transaction Advisory Services

• Mergers and Acquisitions

• Project Finance and Infrastructure

• Transaction Support Services

• Valuation, Business Modeling and Economic Advisory

Advisory

• Asset Management Advisory

• Banking Advisory

• EU Advisory

• Financial Crime Advisory

• Insurance Advisory

• Internal Audit

• IT Risk and Assurance

• Risk Advisory

Managed Services

The EY Managed Services hub supports a number of activities, including regulatory remediation and compliance. Managed Services offers a way to handle mandatory business processes efficiently, while using sophisticated management information tools, highly skilled and experienced resources, improved processing environment and enhanced controls. EY Managed

ervices is certified.

EY's Malta Attractiveness Survey 201846

ContactSimon L Barberi Director, EY Malta Tel: +356 2134 2134 [email protected]

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2018 EYGM Limited. All Rights Reserved.

EYG no. 011698-18Gbl ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

The views of third parties set out in this publication are not necessarily the views of the global EY organization or its member firms. Moreover, they should be seen in the context of the time they were made.

ey.com

EY | Assurance | Tax | Transactions | Advisory