weeks topic bank reconciliation accounting … · • bank column of the crj with the credit side...

TRANSCRIPT

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 1

GRADE 12 SUBJECT

ACCOUNTING WEEKS TOPIC Bank Reconciliat ion

THIS LESSON: WEEK DATE LESSON NR. 1 of 7

LESSON SUMMARY FOR: DATE STARTED:

88D8EDWW DATE COMPLETED:

5 CHBFSGHVJCSHJ

LESSON OBJECTIVES

At the end of this lesson, learners must be able to:

• Define the term ‘Reconciliation’ • Explain what is being reconciled when a Bank Reconciliation is done.

TEACHER ACTIVITIES LEARNER

ACTIVITIES TIMING

RESOURCES NEEDED

1 1.1 1.2 1.3

Pre-knowledge CRJ: Receipting and depositing of cash. CPJ: Issuing of cheques as an instruction to the bank to honour payment. Bank Account: A control account for money received and money paid

Answer questions / Discussions

1.

Transparency

of a CRJ, CPJ

and a Bank

Statement.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 2

TEACHER ACTIVITIES LEARNER

ACTIVITIES TIMING

RESOURCES NEEDED

2 2.1

2.2

2.3

Introduction Establish with learners that the provisional closing balance on the Bank Account in the General Ledger must be equal to the balance reflected on the Bank Statement. However, this is not the case. Therefore, there is a need for reconciliation. Establish the general meaning of Reconciliation to be a process of bringing into two things into agreement with each other. [Make reference to the notes provided]

Answer questions / Discussions

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 3

TEACHER ACTIVITIES

LEARNER ACTIVITIES

TIMING RESOURCES NEEDED

3

3.1

3.2

3.3

3.4

Main Body [Lesson Presentation] Discuss the relevant previous knowledge [provided in the notes] from point 1 to

point 3.4.

Use the question and answer approach so that learners are kept engaged at all

times.

Allow learners to ask questions. However, you may defer questions to a later stage

if the question is not relevant at this stage of the lesson. This will assist in

remaining focused and not swaying away from the lesson.

When mediating this part of the procedure, place emphasis on the following

aspects:

• The effect on the Bank Account when receipts are recorded in the CRJ.

• The effect on the Bank Account when payments are recorded in the CPJ.

• The CRJ represents the Debit side of the Bank Account.

• The CPJ represents the Credit side of the Bank Account.

• The double entries made in the books of the business as against the entry

made on the Bank Statement.

• The effect of a debit entry on the Bank Account and a credit entry on the

Activities:

Worksheet,

text book

chalkboard /

transparency

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 4

3.5

Bank Statement. [Increasing or decreasing]

• The effect of a credit entry on the Bank Account and a debit entry on the

Bank Statement. [Increasing or decreasing]

• Favourable and unfavourable Bank balances.

• Favourable and unfavourable Bank Statement balances.

Establish at the end of the presentation that there is a need for reconciling the

balance on the Bank Account with the balance on the Bank Statement.

TEACHER

ACTIVITIES

LEARNER ACTIVITIES

TIMING

RESOURCES NEEDED

4 4.1

Conclusion The educator must summarise his lesson preferably on a transparency and spend approximately ten minutes consolidating the lesson.

Worksheet, text book chalkboard / transparency

Name of Teacher____________________________ HOD:_________________________________

Sign: ____________________________________ Sign:__________________________________

Date:______________________________________ Date: _________________________________

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 5

GRADE 12 SUBJECT

ACCOUNTING WEEKS TOPIC Bank reconciliation

THIS LESSON: WEEK DATE LESSON NR. 2 of 7

LESSON SUMMARY FOR: DATE

STARTED: 88D8EDWW

DATE

COMPLETED: 5 CHBFSGHVJCSHJ

LESSON OBJECTIVES

At the end of this lesson, learners must be able to:

• Outline the procedure followed to do Bank Reconciliation.

TEACHER ACTIVITIES LEARNER

ACTIVITIES TIMING

RESOURCES NEEDED

1 1.1

Pre-knowledge Continuation from Lesson 1.

Answer questions / Discussions

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 6

TEACHER ACTIVITIES LEARNER

ACTIVITIES TIMING

RESOURCES NEEDED

2

2.1

Introduction Spend approximately ten minutes recapping lesson 1. This must be done through the medium of questioning.

Answer questions / Discussions / Selected activity completed on a transparency.

1.

Transparency

of a CRJ, CPJ

and a Bank

Statement.

TEACHER ACTIVITIES

LEARNER ACTIVITIES

TIMING RESOURCES NEEDED

3

3.1

3.2

3.2.1

Main Body [Lesson Presentation] Discuss Integration of Internal Control over Cash by explaining to learners that

the business needs to ascertain whether all the entries that were made in the CRJ

and CPJ appear on the Bank Statement. This can only be done by means of comparisons.

Discuss 4.1 in the notes provided.

Focus on determining the items / amounts that are causing differences by

comparing the following:

Activities:

1 A text book

example

should be

used illustrate

and make the

discussion

more

meaningful.

Worksheet,

text book

chalkboard /

transparency

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 7

3.2.2

3.2.3

• Bank column of the CRJ with the Credit Side of the Bank Statement to

ascertain whether all the Deposits have been captured by the business and

the bank.

• Bank column of the CPJ with the Debit Side of the Bank Statement to

ascertain whether Cheques issued have been presented for payment and

also to ascertain whether other items as listed in the notes have been

captured by the business and the bank.

• Explain, with the aid of a transparency of a Salaries Journal, the need to

compare the Salaries Journal with the Bank Statement.

Explain to learners that in the following month the Bank Statement must first be

compared with the Bank Reconciliation Statement of the previous month to

ascertain whether the differences of the previous month appear on the bank

statement of the current month.

Explain to learners that the items causing the difference in balances between the

Bank Account and the Bank Statement must be recorded so that the balances

would agree. This process is called Bank Reconciling.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 8

TEACHER ACTIVITIES

LEARNER ACTIVITIES

TIMING RESOURCES NEEDED

4 4.1

Conclusion The educator must summarise his lesson preferably on a transparency and spend approximately ten minutes consolidating the lesson.

Worksheet, text book chalkboard / transparency

Name of Teacher____________________________ HOD:_________________________________

Sign: ____________________________________ Sign:__________________________________

Date:______________________________________ Date: _________________________________

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 9

GRADE 12 SUBJECT

ACCOUNTING WEEKS TOPIC Bank Reconciliat ion

THIS LESSON: WEEK DATE LESSON NR. 3 of 7

LESSON SUMMARY FOR: DATE

STARTED: 88D8EDWW

DATE

COMPLETED: 5 CHBFSGHVJCSHJ

LESSON OBJECTIVES

At the end of this lesson, learners must be able to:

• Identify specific items in the CRJ that could cause differences. • Identify specific items in the CPJ that could cause differences. • Identify specific items on the Credit Side of the Bank Statement that could cause differences. • Identify specific items on the Debit Side of the Bank Statement that could cause differences. • State specifically where the items must be recorded in each of the above cases.

TEACHER ACTIVITIES LEARNER

ACTIVITIES TIMING

RESOURCES NEEDED

1 1.1

Pre-knowledge Follow-up from lesson 2.

Answer questions / Discussions

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 10

TEACHER ACTIVITIES

LEARNER

ACTIVITIES TIMING

RESOURCES

NEEDED

2 2.1

Introduction A brief revision of the comparisons done in lesson 2.

Answer questions / Discussions

1.

Transparency

of a CRJ, CPJ

and a Bank

Statement.

TEACHER ACTIVITIES

LEARNER ACTIVITIES

TIMING RESOURCES NEEDED

3

3.1

3.2

3.2.1

Main Body [Lesson Preparation] Question learners on the items that cause differences as listed in the notes from 4.2 to 4.7. In each case learners must be prompted to indicate where the item in question will be recorded. Special attention must be given to the recording of the following: Direct deposits / EFT’s / deposits made by the business that were not captured by the business.

Activities:

Worksheet, text book chalkboard / transparency

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 11

3.2.2

3.2.3

3.2.3

3.2.4

3.2.5

3.2.6

3.2.7

Stop Payments. Bank Charges and Interest on Overdraft. Stop Orders and Debit Orders. PDC’s issued and payable in the current financial year. PDC’s issued and payable in the next financial year. Errors on the Cash Journals. Errors on the Bank Statement.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 12

TEACHER ACTIVITIES

LEARNER ACTIVITIES

TIMING RESOURCES NEEDED

4 4.1

Conclusion Spend ten minutes consolidating the lesson.

Worksheet, text book chalkboard / transparency

Name of Teacher____________________________ HOD:_________________________________

Sign: ____________________________________ Sign:__________________________________

Date:______________________________________ Date: _________________________________

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 13

GRADE 12 SUBJECT

ACCOUNTING WEEKS TOPIC Bank Reconciliat ion

THIS LESSON: WEEK DATE LESSON NR. 4 of 7

LESSON SUMMARY FOR: DATE STARTED:

88D8EDWW DATE COMPLETED:

5 CHBFSGHVJCSHJ

LESSON OBJECTIVES

At the end of this lesson, learners must be able to:

• Explain what a Bank Reconciliation Statement is. • Prepare Bank Reconciliation Statements using two columns. • Prepare Bank Reconciliation Statements using one column.

TEACHER ACTIVITIES LEARNER

ACTIVITIES TIMING

RESOURCES NEEDED

1 1.1

Pre-knowledge From Lesson 3

Answer questions / Discussions

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 14

TEACHER ACTIVITIES LEARNER

ACTIVITIES TIMING

RESOURCES NEEDED

2 2.1

Introduction Spend ten minutes recapping Lesson 3.

Answer questions / Discussions

TEACHER ACTIVITIES

LEARNER ACTIVITIES

TIMING RESOURCES NEEDED

3

3.1

3.2

3.3

Main Body [Lesson Preparation] Through questioning establish that any errors or omissions in the Cash Journals would have to be rectified or included by the business. Through questioning establish that any errors or omissions on the Bank Statement would have to be rectified or included by the bank as the business does not have any control over the Bank Statement. Therefore, the business is only in a position of keeping a record of the discrepancies. This information is shown in the Bank Reconciliation Statement. During the reconciliation process its anticipated that the two balances would be brought into agreement with each other, viz. Bank Account and Bank Statement balances.

Activities: Learners must complete the remaining activities.

Worksheet, text book chalkboard / transparency

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 15

3.4

3.5

Hence, the Bank Reconciliation Statement will commence with the balance as per closing balance of the Bank Statement. This means that the Bank Reconciliation Statement is a continuation of the Bank Statement. It must be pointed out to learners that entries recorded in the Bank Reconciliation Statement are recorded from the Bank’s point of view. These entries must not be construed as being completed on the Bank Statement. Therefore, the bank statement of the following month must be compared with the previous month’s Bank Reconciliation Statement in order to ascertain that the discrepancies in the form of errors or omissions have been corrected or included on the Bank Statement of the current month.

TEACHER

ACTIVITIES

LEARNER ACTIVITIES

TIMING RESOURCES NEEDED

4 4.1

Refer to Activity Bank Reconciliation Statements Demonstrate the preparation of the Bank Reconciliation Statement using a debit and a credit column. Then redo the same activity using a single column.

Worksheet, text book chalkboard / transparency

Name of Teacher____________________________ HOD:_________________________________

Sign: ____________________________________ Sign:__________________________________

Date:______________________________________ Date: _________________________________

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 16

GRADE 12 SUBJECT

ACCOUNTING WEEKS TOPIC Bank Reconciliat ion

THIS LESSON: WEEK DATE LESSON NR. 5 of 7

LESSON SUMMARY FOR: DATE STARTED:

88D8EDWW DATE COMPLETED:

5 CHBFSGHVJCSHJ

LESSON OBJECTIVES

At the end of this lesson, learners must be able to:

• Record supplementary entries from the Bank Statement into the Cash Journals. • Prepare the Bank Reconciliation Statement. • Prepare the Bank Account.

TEACHER ACTIVITIES

LEARNER

ACTIVITIES TIMING

RESOURCES

NEEDED

1 1.1

Pre-knowledge Lesson 3.

Answer questions / Discussions

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 17

TEACHER ACTIVITIES LEARNER

ACTIVITIES TIMING

RESOURCES NEEDED

2 2.1

Introduction Recap Lesson 3 and 4

Answer questions / Discussions

TEACHER ACTIVITIES

LEARNER ACTIVITIES

TIMING RESOURCES NEEDED

3

3.1

3.2

3.2.1

3.2.2

Main Body [Lesson Presentation] Learners must complete an activity with the guidance of the teacher. Learners must identify the discrepancies and indicate where they would record these. [Use the Question and answer approach] Compare the Bank statement with the previous month’s Bank Reconciliat ion Statement: Guide learners to commence the reconciliation process by checking that the discrepancies noted in the previous month appear in the current month. Items viz, outstanding cheques, that still do not appear in the current month’s Bank Statement must be recorded in the Bank Reconciliation Statement. Stale cheques must be cancelled by making the entry in the CRJ. The same details must be used as when the entry was made in the CPJ.

Activities:

Worksheet, text book chalkboard / transparency

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 18

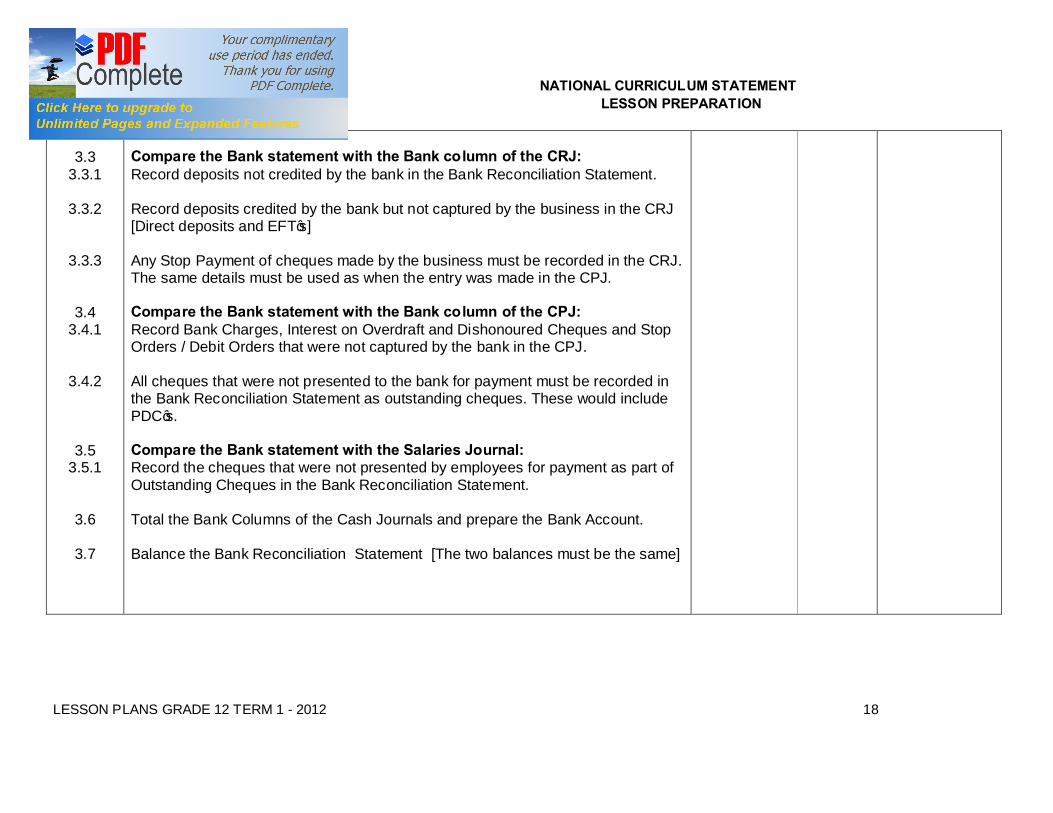

3.3

3.3.1

3.3.2

3.3.3

3.4 3.4.1

3.4.2

3.5 3.5.1

3.6

3.7

Compare the Bank statement with the Bank column of the CRJ: Record deposits not credited by the bank in the Bank Reconciliation Statement. Record deposits credited by the bank but not captured by the business in the CRJ [Direct deposits and EFT’s] Any Stop Payment of cheques made by the business must be recorded in the CRJ. The same details must be used as when the entry was made in the CPJ. Compare the Bank statement with the Bank column of the CPJ: Record Bank Charges, Interest on Overdraft and Dishonoured Cheques and Stop Orders / Debit Orders that were not captured by the bank in the CPJ. All cheques that were not presented to the bank for payment must be recorded in the Bank Reconciliation Statement as outstanding cheques. These would include PDC’s. Compare the Bank statement with the Salaries Journal: Record the cheques that were not presented by employees for payment as part of Outstanding Cheques in the Bank Reconciliation Statement. Total the Bank Columns of the Cash Journals and prepare the Bank Account. Balance the Bank Reconciliation Statement [The two balances must be the same]

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 19

TEACHER ACTIVITIES

LEARNER ACTIVITIES

TIMING RESOURCES NEEDED

4

4.1

Conclusion Draw to the attention of the learners that the Balance as per Bank account in the Bank Reconciliation Statement could be sourced as the opening balance of the Bank Account for the following month.

Worksheet, text book chalkboard / transparency

Name of Teacher____________________________ HOD:_________________________________

Sign: ____________________________________ Sign:__________________________________

Date:______________________________________ Date: _________________________________

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 20

GRADE 12 SUBJECT

ACCOUNTING WEEKS TOPIC Bank Reconciliat ion

THIS LESSON: WEEK DATE LESSON NR. 6 of

LESSON SUMMARY FOR: DATE STARTED:

88D8EDWW DATE COMPLETED:

5 CHBFSGHVJCSHJ

LESSON OBJECTIVES

At the end of this lesson, learners must be able to:

• The ways in which Bank Reconciliation assists as an Internal Control Process over cash

TEACHER ACTIVITIES LEARNER

ACTIVITIES TIMING

RESOURCES NEEDED

1 1.1

Pre-knowledge That Internal Control is a process that assists in safeguarding the assets of the business.

Answer questions / Discussions

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 21

TEACHER ACTIVITIES LEARNER

ACTIVITIES TIMING

RESOURCES NEEDED

2 2.1

Introduction Cash in a business is classified as an asset and must, therefore, be safeguarded. Bank Reconciliation is one form of an Internal Control Process that assists in safeguarding cash from being stolen.

Answer questions / Discussions

TEACHER ACTIVITIES

LEARNER ACTIVITIES

TIMING RESOURCES NEEDED

3

3.1 3.2 3.3

3.4 3.5

3.6

3.7

Main body [Presentation Clarify that Bank Reconciliat ion is an Internal Control Process over cash that assists in ensuring the following: That all entries are properly recorded in the CRJ and CPJ. [Free of errors] That monies received are deposited promptly. [On a daily basis] The business is kept informed about outstanding cheques and outstanding deposits. It is a way of detecting fraud. It assists in controlling cash so that the business does not go into an overdraft unnecessarily or exceed its overdraft facility. Keeps a track of cheque deposits so that the necessary steps can be taken to recover monies from debtors whose cheques have been dishonoured / returned unpaid. Question learners on additional control measures needed in larger businesses. Consider the following responses:

• Supervisors checking the cash received from cashiers and issuing receipts.

Activities:

Worksheet, text book chalkboard / transparency

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 22

• Accountant checks the cash he receives from the cashiers. • The Internal auditor checks that the cash received is: ¶ according to the Cash Register Tapes ¶ properly receipted and recorded in the CRJ ¶ deposited the following day.

TEACHER

ACTIVITIES

LEARNER ACTIVITIES

TIMING RESOURCES NEEDED

4

4.1

Conclusion Spend approximately five minutes consolidating the lesson.

Worksheet, text book chalkboard / transparency

Name of Teacher____________________________ HOD:_________________________________

Sign: ____________________________________ Sign:__________________________________

Date:______________________________________ Date: _________________________________

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 23

GRADE 12 SUBJECT

ACCOUNTING WEEKS TOPIC Bank Reconciliat ion

THIS LESSON: WEEK DATE LESSON NR. 7 of

LESSON SUMMARY FOR: DATE

STARTED: 88D8EDWW

DATE

COMPLETED: 5 CHBFSGHVJCSHJ

LESSON OBJECTIVES

At the end of this lesson, learners must be able to:

• Adjust figures for Bank and Creditors’ Control in respect of PDC’s issued in the current financial year but payable in the next financial year.

TEACHER ACTIVITIES LEARNER

ACTIVITIES TIMING

RESOURCES NEEDED

1 1.1 1.2 1.3

Pre-knowledge CPJ Bank Account Creditors’ Control

Answer questions / Discussions

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 24

TEACHER ACTIVITIES LEARNER

ACTIVITIES TIMING

RESOURCES NEEDED

2 2.1

2.2

2.3

Introduction Reporting on financial statements must not only be accurate, but it must also not be misleading to the reader of the financial statements. PDC’s issued but payable in the next financial year are recorded in the CPJ and posted to the Bank and Creditors’ Control Account. Hence, these two accounts are reduced [or adjusted] without the money actually having been paid. Therefore, the figures would be misleading to the reader of the financial statements. Consequently, the balances on these two accounts would have to be adjusted in order to provide accurate reporting to the reader of the financial statements.

Answer questions / Discussions

TEACHER ACTIVITIES

LEARNER ACTIVITIES

TIMING RESOURCES NEEDED

3

3.1

3.2

Main body [Presentation In recording information on the financial statements in respect of PDC’s issued and payable in the next financial year, the Bank Account and the Creditors’ Control Account would have to be adjusted for purposes of accurate reporting. Note that only an adjustment is made to the figures in the financial statements. No adjustment is made to the ledger account. Therefore, there is no double entry for this adjustment. Adjustment to the Creditors’ Control Account Add the value of the PDC’s issued and payable in the next financial to the balance on the Creditors’ Control Account at the end of the year. Reflect the adjusted balance in the financial statements. [Note: Trade and other Payables]

Activities:

Worksheet, text book chalkboard / transparency

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 25

3.3

3.3.1

3.3.2

3.3.3

There are three different situations that can arise in respect of the Bank Account and in each case the adjustment would differ. Bank Account has a favourable at the end of the year. Add the value of the PDC’s issued and payable in the next financial to the balance on the Bank Account at the end of the year. Reflect the adjusted Creditors’ Control balance in the financial statements. [Note: Cash and Cash Equivalents] Bank Account has an unfavourable balance that is greater than the value of the PDC’s issued and payable in the next financial year. Subtract the value of the PDC’s from the unfavourable Bank balance. The Bank Account will now have a lesser unfavourable [credit] balance. Reflect the adjusted Bank balance in the financial statements. [Note: Trade and other Payables] Bank Account has an unfavourable balance that is lesser than the value of the PDC’s issued and payable in the next financial year. Subtract the value of the unfavourable Bank balance from the value of the PDC’s issued. The Bank Account will now have a favourable [debit] balance. Reflect the adjusted Bank balance in the financial statements. [Note: Cash and Cash Equivalents]

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 26

TEACHER ACTIVITIES

LEARNER ACTIVITIES

TIMING RESOURCES NEEDED

4

4.1

Conclusion Spend approximately ten minutes consolidating the lesson through the medium of T-accounts.

Worksheet, text book chalkboard / transparency

Name of Teacher____________________________ HOD:_________________________________

Sign: ____________________________________ Sign:__________________________________

Date:______________________________________ Date: _________________________________

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 27

PROCEDURE FOR BANK RECONCILIATION 1. Bring about an understanding of the term “reconciliation” from the learners

own understanding

Q. Why is it necessary to reconcile two people?

• Due to differences • Therefore, sorting these differences and bringing each into

agreement with the other means RECONCILING. 2. Bank Reconciliation:

Q. What must be brought into agreement with what?

Relevant previous knowledge

2.1

Money received Recorded in the CRJ Bank Account is Debited

Therefore, the CRJ represent the Debit side of the of the Bank Account

2.2

Money Paid Recorded in the CPJ Bank Account is Credited

Therefore, the CPJ represent the Credit side of the of the Bank Account

2.3 Go back to 2.1 – consolidate and continue

Q. What does the Bank (financial institution) do to our account when we deposit

money into our bank account?

A Credit

Why?

A Because they now owe us (business) the money and therefore, they regard us as their liability

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 28

\

• When depositing Money

The Business

Debit Bank Account Asset Increases

The Bank Credit Bank Statement

Liability Increases

Therefore, entries are recorded in opposite

2.4 Go back to 2.2 – consolidate and continue

Q. What does the bank do to our account when we issue cheques to make payments?

A. Debit

Why?

Because they owe us money and by paying out our money they owe us

less, thus their liability towards us decreases

• When issuing cheques OR making any form of payment via the bank

The Business

Credit Bank Account Asset Decreases

The Bank Debit Bank Statement Liability Decreases

Therefore, entries are recorded in opposite. 2.5 Favourable and unfavourable Bank Balances purely from the

business point of view.

Bank Account Debit FAVOURABLE Bank Statement Credit

Bank Account Credit UNFAVOURABLE Bank Statement Debit

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 29

3. Deductions from the above

3.1

As we debit Bank Account The bank Credits our bank statement

As we Credit Bank Account

The bank Debits our bank statement

3.2 Therefore, we expert that the balance on the bank account should be the same as the balance on the bank statement.

3.3 But the balances are not the same!

3.4 Because there are differences / discrepancies.

3.5 We have to reconcile the balance of the bank account with the balance on the bank statement

4. PROCEDURE FOR BANK RECONCILIATION:

4.1 Determine the items / amounts that are causing the difference by comparing the

following:

• Bank column of the CRJ, with the Cr. side of the bank statement • Bank column of the CPJ, with the Dr side of the bank statement • Salaries journal with the bank statement • Previous bank reconciliation statement with the current month bank

statement. NOTE THE SEQUENCE FOR THE NEXT MONTH CHANGES.

What are the items that are causing the difference?

4.2 > Bank charges

> Interest on overdraft

> Stop orders / debit orders (differentiate) note 1

> Unpaid cheques

4.3. > Interest on current account

> Direct deposit

4.4 > Deposits in the CRJ not credited by bank

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 30

4.5 > Cheques issued and not recorded in the CPJ but not presented

to the bank for payment – including PDC issued (NOTE 2)

4.6 > Stop payments (NOTE 1)

5. Use the logical Approach

5.1 Who should make the entries firs (the business or bank)

5.2 Entries missing in the CRJ and CPJ will be recorded from the point of the business.

5.3 Entries missing on the bank statement will be shown on the bank reconciliation statement from the point of view of the bank

5.4 NOTE: The bank Reconciliation Statement is a continuation of the bank Bank Statement

5.5 Through questioning, learners must be made to understand that the CRJ and the CPJ is finally totalled after the bank statement arrives, and reconciliation is done

Q. What are provisional totals?

5.6 How do PDC issued affect the bank and creditors control in the financial statements

NOTES 1. STOP ORDERS AND DEBIT ORDERS

Ø They are both instructions to the bank TO PAY •STOP ORDER Ø Instruction to the bank to pay a specific amount to a person/

business on a specific date for a specific period •DEBIT ORDERS Ø Instruction to the bank via the payee to pay a certain sum of

money to the payee on a monthly basis. Note that the amount can differ from time to time

2. STOP PAYMENT.

Instruction to the bank NOT TO PAY a cheque that has already been issued.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 31

3. RECORDING THE INFORMATION ON THE FINANCIAL STATEMENTS

Adjust Creditors’ Control and Bank Balances as a result of PDC’s issued and payable in the next financial year.

• CREDITORS’ CONTROL Ø Add the value of PDC’s issued and payable in the next financial

year to the bank account balance • BANK ACCOUNT HAS AN UNFAVOURABLE BALANCE THAT IS

GREATER THAN THE VALUE OF PDC’S ISSUED AND PAYABLE IN THE NEXT FINANCIAL YEAR Ø Subtract the value of the PDC’s from the unfavourable bank balance

and bank account will now have a lesser unfavourable balance [Cr] • BANK ACCOUNT HAS AN UNFAVOURABLE BALANCE THAT IS

LESSER THAN THE VALUE OF PDC’S ISSUED AND PAYABLE IN THE NEXT FINANCIAL YEAR Ø Subtract the value of the PDC’s from the unfavourable bank balance

and bank account will now have favourable balance [Dr]

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 32

GRADE 12

WEEK:

LESSON:

DEBTORS TRANSACTIONS AND DEBTORS ACCOUNTS

WORKSHEET 1

JOURNALS

• When customers or other enterprise buy goods on credit from our enterprise, the transaction is recorded in the Debtors Journal (DJ)

• Any sales returns are recorded in the Debtors Allowance Journal (DAJ)

• Payments received from debtors are recorded in the Cash Receipt Journal (CRJ)

• Errors that are corrected, interest charged on overdue accounts and transfers between debtors and creditors accounts are recorded through entries in the General Journal (GJ)

DEBTORS CONTROL ACCOUNT: FORMAT Dr DEBTORS CONTROL ACCOUNT Cr

Date Day Details fol Amount Date Day Details fol amount

2011 Apr

1 Balance b/d xxxx 2011 Apr.

30 Bank and discount allowed

CRJ xxxx

30 Sales DJ xxxx Debtors allowances

DAJ xxxx

Bank (R/D) CPJ xxxx Journal credits GJ xxxx

Petty cash PCJ xxxx Balance c/d xxxx

Journal debits GJ xxx

x xxx

Balance b/d xxxx

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 33

• The balance brought down on the debit side is the net balance which is the

debit balances minus any credit balances that were obtained from the debtors ledger.

• Credit balances occur when debtors overpay, or when discounts are granted after an account has been settled, or when incorrect entry is made in the account.

2. DEBTORS LEDGER

• Businesses that buy and sell on credit keep a debtors ledger which contains an individual account of each debtor.

• A record of all transactions of the debtor is shown in the Debtors Ledger. • The Debtors Ledger contains the opening balance, invoices issued to him

for stock sold to him on credit, returns, allowances, payments made by him (debtor) and discounts allowed to him

• A copy of this account is sent to the debtor at the end of the month. These accounts are presented are presented in “three column’ format instead of the conventional “T-form’ account as this is generally easy for the debtor to read and understand

DEBTORS LEDGER: FORMAT

Date Details fol Debit (+) Credit (-) Balance

2011 April

01 Account rendered b/d xxx

05 Invoice DJ xxx xxx

O7 Dishonoured cheque CPJ xxx xxx

09 Petty cash voucher PCJ xxx xxx

12 Journal voucher (interest received, discount cancelled, asset disposal, transfer of correction)

GJ

xxx

xxx

17 Receipt CRJ xxx xxx

Receipt (discount allowed) CRJ xxx xxx

21 Credit note DAJ xxx xxx

25 Journal voucher GJ xxx xxx

The following transactions resulted in the entry being made on the debit side of debtor’s accounts:

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 34

DEBTORS ACCOUNTS NO TRANSACTIONS JOURNAL

1 Sold inventory to debtor on credit. Debtor therefore owes business more money

DJ

2 A cheque previously received from a debtor in payment of his account was dishonoured by bank. The payment must therefore be cancelled.

CPJ

3 Payment made from petty cash on behalf of a debtor. An example of this could be pay the transport of goods on behalf of a debtor, who will then owe the money to the business.

PCJ

4

Charged a debtor interest on overdue account (interest received)

Cancelled a discount on a dishonoured cheque

Sold asset on credit

Transferred credit balance of a debtor to his/her account in the creditors ledger

The correction of errors made on a debtor’s account during th month

GJ

The following transactions resulted in the entry being made on the credit side of debtor’s accounts: DEBTORS ACCOUNTS NO TRANSACTIONS JOURNAL

5 Received money and cheques from debtors in part payment or in settlement of accounts and allowed them discounts for prompt payment.

CRJ

6

Debtors returned goods to our store or requested allowances on goods previously sold to them.

DAJ

7

Wrote off a debtor’s account as uncollectable or bad debt

Transferred the debit balance of a debtor to his/her account in the creditors ledger

The correction of errors made on a debtors account during the month.

GJ

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 35

DEBTORS LIST

• Debtors list is prepared at the end of each month. • The list serves as a summary of all the debtors and the balances owing • The total of the debtors list must agree with balance on the debtors control

accounts • Control accounts are drawn up from the totals obtained from the relevant

subsidiary journals. • Should the owner of the business need to know what an individual debtor

owes him he would look at the Debtors Ledger • If he needs to know what the total amount owing by all his debtors, he will

look at the Debtors Control account.

For control purposes: • The control account should always be in balance with the debtors list. • In many instances they are not be in balance. The personnel responsible will

have to investigate the reasons, and reasons could be: ü Errors in posting ü Wrong amounts entered when posting ü Transactions that had not been processed ü The error/omission may impact on the relevant control; the list or

both the control account and the list.

DEBTORS RECONCILIATION: • Transaction takes place • Transactions are recorded on source documents • Information on source documents is entered into Journals

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 36

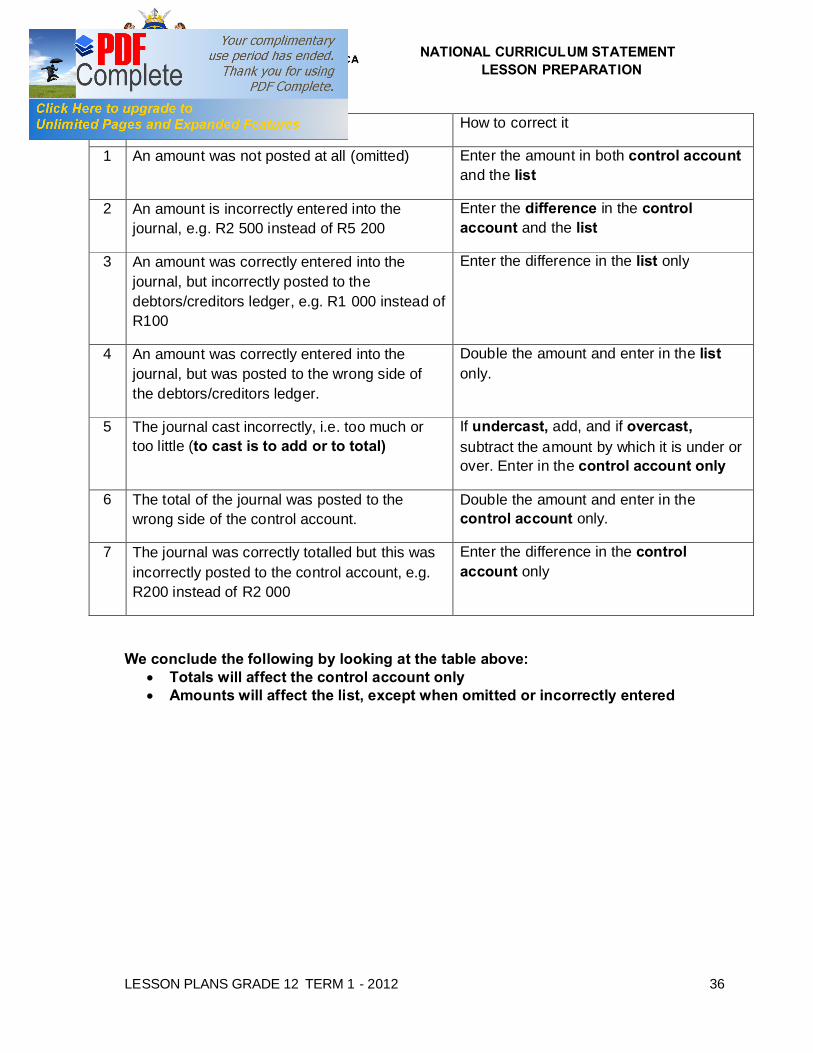

The following errors may occur; No. Possible mistake How to correct it

1 An amount was not posted at all (omitted) Enter the amount in both control account and the list

2 An amount is incorrectly entered into the journal, e.g. R2 500 instead of R5 200

Enter the difference in the control account and the list

3 An amount was correctly entered into the journal, but incorrectly posted to the debtors/creditors ledger, e.g. R1 000 instead of R100

Enter the difference in the list only

4 An amount was correctly entered into the journal, but was posted to the wrong side of the debtors/creditors ledger.

Double the amount and enter in the list only.

5 The journal cast incorrectly, i.e. too much or too little (to cast is to add or to total)

If undercast, add, and if overcast, subtract the amount by which it is under or over. Enter in the control account only

6 The total of the journal was posted to the wrong side of the control account.

Double the amount and enter in the control account only.

7 The journal was correctly totalled but this was incorrectly posted to the control account, e.g. R200 instead of R2 000

Enter the difference in the control account only

We conclude the following by looking at the table above:

• Totals will affect the control account only • Amounts will affect the list, except when omitted or incorrectly entered

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 37

Activity 1 A. Draw up the formats of the following:

• Debtors control and Debtors ledger Accounts B. You asked a junior debtors clerk to draw up the debtors control account below. When he presented it to you, you noticed that it was incorrect. i. Correct the account as it should appear in the books on 31 march 2010 ii. Explain the control account to the debtors clerk by using the following table headings: Transaction that led to the entry being made

Source document Subsidiary Journal

Hint: start with debit entries, and then do the credit entries.

Dr Debtors Control Account Cr

2010 Mar

1 balance b/d 15 100 2010 Mar

31 Bank (payment received only)

CRJ 31 274

31 Sales DJ 29 960 Discount allowed CRJ 1 746

Debtors allowances

DAJ 1 442 Bank (dishonoured cheque)

CPJ 750

Discount cancelled

GJ 45 Interest on overdue account

GJ 70

Bad debts GJ 278 Balance c/d 12 985

46 825 46 825

May 1 Balance b/d 12 985

• Learners will use their Accounting books to do the activities

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 38

Activity 2.

The information below was taken from the books of J & M Biltong Stores for May 2010

Draw up the Debtors Control account in the General ledger and balance it at the end of the month.

Information:

1. The following balances appeared , amongst others, in the books on 1 may 2010 Amounts owing by debtors 31 200

Amounts owing to debtors 330

2. The following information was extracted from the journals for May 2010: • Total cost price of goods sold on credit at a mark-up of 80% on cost, R14 200 • Total cost price of goods sold for cash at a mark-up of 60% on cost, R22 660. • 10% of all goods sold on credit to debtors were returned. • Money and cheques received from debtors , R25 480. • Discounts allowed to debtors, R1 363. • Bad debts recovered, R270. • Total of the debtors column in the Petty cash Journal, R68. • Cheques previously received from debtors dishonoured by the bank, R1 520. • The credit amount of R330 owed to M. Smith on 1 may was refunded to her by

issuing a cheque to her. • The following general Journal entries must be considered:

ü Discount of 5% was allowed on behalf of the dishonoured cheque. ü 10% of the amount owed by debtors as on 1 may is still outstanding and

interest must be charged at 5% p.a. for May. ü A debtor who owed R900 was declared insolvent, a final dividend of 60c in

the rand was received and recorded. The remainder of his debt must be written off.

ü The account of a creditor, Robert Suppliers, with a debit balance of R490, must be transferred to his account in the Debtors Ledger.

ü An old biltong oven was sold to a staff member for R350 on credit.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 39

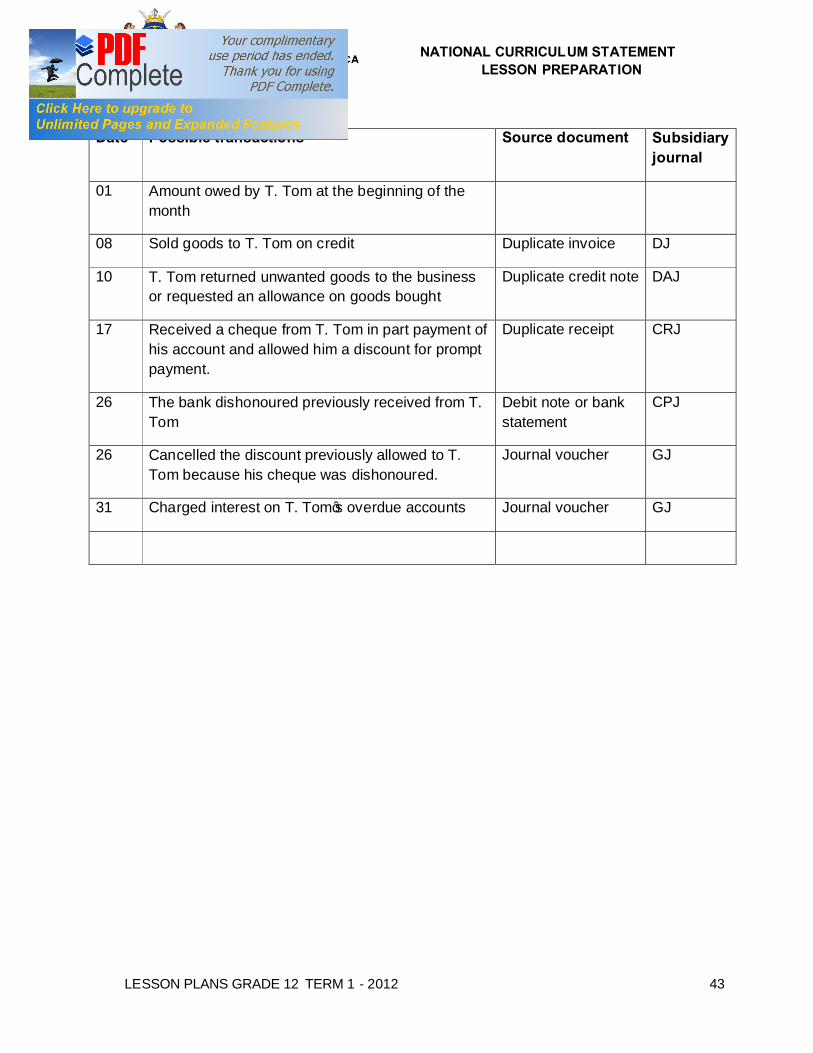

Activity 3 The account of T. Tom, a debtor in the books of Alegre Traders, appeared in the Debtors Ledger during May 2010. Analyse each of the entries on the table below Date Possible transaction Source document Subsidiary journal

Debtors ledger of Alegree Traders T. Tom

Date Details fol Debit Credit Balance

2010 may

1 Account rendered b/d 3 100

8 ......163 6 830 9 930

10 ......87 260 9 670

17 .....202 1 425 8 245

.....202 75 8 170

26 Cheque not cashed 1 425 9 595

Journal (..... .) 75 9 670

31 Penalty for late payment 93 9 763

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 40

MODEL ANSWERS

ACTIVITY 1

A.

DEBTORS CONTROL ACCOUNT: FORMAT Dr DEBTORS CONTROL ACCOUNT Cr

Date Day Details fol Amount Date Day Details fol amount

2011 Apr

1 Balance b/d xxxx 2011 Apr.

30 Bank and discount allowed

CRJ xxxx

30 Sales DJ xxxx Debtors allowances DAJ xxxx

Bank (R/D) CPJ xxxx Journal credits GJ xxxx

Petty cash PCJ xxxx Balance c/d xxxx

Journal debits GJ xxx

x xxx

Balance b/d xxxx

DEBTORS LEDGER: FORMAT Date Details fol Debit (+) Credit (-) Balance

2011 April 01 Account rendered b/d xxx

05 Invoice DJ xxx xxx

O7 Dishonoured cheque CPJ xxx xxx

09 Petty cash voucher PCJ xxx xxx

12 Journal voucher (interest received, discount cancelled, asset disposal, transfer of correction)

GJ

xxx

xxx

17 Receipt CRJ xxx xxx

Receipt (discount allowed) CRJ xxx xxx

21 Credit note DAJ xxx xxx

25 Journal voucher GJ xxx xxx

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 41

B

Corrections to the Debtors Control Account

Dr Debtors Control Account Cr

2010 Mar

1 Balance b/d 15 100 2010 Mar

31 Bank and discount allowed (31 274+1 746)

CRJ 31 274

31 Sales DJ 29 960 Debtors allowances

DAJ 1 442

Bank (dishonoured cheque)

CPJ 750 Bad debts GJ 278

Discount cancelled (70+45)

GJ 115 Balance c/d 11 185

45 925 45 925

Apr 1 Balance b/d 11 185

ANALYSIS OF TRANSACTIONS:

Transactions that led to the entry Source Document Subsidiary Journal

Amount owed by debtors at the beginning of the month

n/a n/a

Sold goods to debtors on credit Duplicate invoice DJ

The bank dishonoured cheque previ ously received from a debtor

Debit note or bank statement CPJ

Cancelled the discount previously allowed because the debtors was dishonoured

Journal voucher GJ

Charged interest on debtors’ overdue account Journal voucher GJ

Received money and cheques from debtors in part payment or in settlement of their accounts and allowed them discounts for prompt payment.

Duplicate receipts CRJ

Debtors returned unwanted goods or requested an allowance on goods bought.

Duplicate credit note DAJ

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 42

Wrote off a debtor’s account as uncollectable/irrecoverable

Journal voucher GJ

Balance owed by debtors at the end of the month - -

ACTIVITY 2

General Ledger of J & M Biltong

Dr Debtors Control Account Cr

2010 May

1 Balance

(31 200 – 330)

b/d 30 870 2010 Mar

31 Bank and discount allowed

(25 480+1 363)

CRJ 26 843

31 Sales DJ 25 560 Debtors allowances

DAJ 2 556

Bank (dishonoured cheque)

CPJ 1 520 Journal credits GJ 360

Bank refund CPJ 330 Balance c/d 29 482

Petty cash PCJ 68

Journal debits (40+13+490+350)

GJ 893

59 241 59 241

Jun 1 Balance b/d 29 482

• Sales: 14 200 x 180/100 = 25 560

Debtors allowances: 25 560 x 10/100 = 2 556

General Journal: 1 520/2 = 760 x 100/95 = 800

800 – 760 = 40 discount cancelled

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 43

ACTIVITY 3:

Date Possible transactions Source document Subsidiary journal

01 Amount owed by T. Tom at the beginning of the month

08 Sold goods to T. Tom on credit Duplicate invoice DJ

10 T. Tom returned unwanted goods to the business or requested an allowance on goods bought

Duplicate credit note DAJ

17 Received a cheque from T. Tom in part payment of his account and allowed him a discount for prompt payment.

Duplicate receipt CRJ

26 The bank dishonoured previously received from T. Tom

Debit note or bank statement

CPJ

26 Cancelled the discount previously allowed to T. Tom because his cheque was dishonoured.

Journal voucher GJ

31 Charged interest on T. Tom’s overdue accounts Journal voucher GJ

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 44

NOTES: DEBTORS/CREDITORS RECONCILIATIONS

CONTROL ACCOUNTS AND DEBTORS/ CREDITORS LIST

1. Debtors and Creditors accounts are continually updated as transactions take place. During the month, the recording procedure is as follows:

• Debtors transaction takes place • Transactions are recorded on source documents • Information on source documents is entered into Journals

DEBTORS/CREDITORS LIST

• Debtors/Creditors list is prepared at the end of each month. • The list serves as a summary of all the debtors/creditors and the balances

owing • The total of the debtors/creditors list must agree with balance on the

debtors/creditors control accounts • Control accounts are drawn up from the totals obtained from the relevant

subsidiary journals. • Should the owner of the business need to know what an individual debtor

owes him he would look at the Debtors Ledger • If he needs to know what the total amount owing by all his debtors, he will

look at the Debtors Control account.

For control purposes: • At the end of the month the balance of the control accounts must agree with

the totals of the Debtors/Creditors list • If they do not agree, someone has made a mistake. The mistakes must be

found before the statements are sent to debtors/ cheques sent to creditors to ensure that:

1. Debtors do not get upset because the account they receive is always wrong, they might think of taking their business somewhere else

2. We do not overpay our Creditors 3. We earn the correct discount by paying the correct amount promptly

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 45

The following errors may occur;

No. Possible mistake How to correct it

1 An amount was not posted at all (omitted) Enter the amount in both control account and the list

2 An amount is incorrectly entered into the journal, e.g. R2 500 instead of R5 200

Enter the difference in the control account and the list

3 An amount was correctly entered into the journal, but incorrectly posted to the debtors/creditors ledger, e.g. R1 000 instead of R100

Enter the difference in the list only

4 An amount was correctly entered into the journal, but was posted to the wrong side of the debtors/creditors ledger.

Double the amount and enter in the list only.

5 The journal cast incorrectly, i.e. too much or too little (to cast is to add or to total)

If undercast, add, and if overcast, subtract the amount by which it is under or over. Enter in the control account only

6 The total of the journal was posted to the wrong side of the control account.

Double the amount and enter in the control account only.

7 The journal was correctly totalled but this was incorrectly posted to the control account, e.g. R200 instead of R2 000

Enter the difference in the control account only

We conclude the following by looking at the table above: • Totals will affect the control account only • Amounts will affect the list, except when omitted or incorrectly entered

ACTIVITY 4 INDIVIDUAL WORK

The debtors Control account and Debtors List below were prepared by the newly appointed bookkeeper of Lotti Stores. You have noticed a number of errors and omissions .

Required:

1. Prepare a corrected Debtors control account 2. Prepare a corrected Debtors List on July 2010

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 46

Information:

General Ledger of Lotti Stores

Balance Sheet Accounts Section

Dr Debtors Control Account Cr

2010 July

1 Balance b/d 11 916 2010 July

31 Bank CRJ 28 654

31 Sales DJ 45 190 Discount allowed

CRJ 1 762

Bank CPJ 5 678 Debtors allowances

DAJ 2 308

Sundry accounts GJ 1 200 Sundry accounts

GJ 974

Balance c/d 29 986

63 684 63 684

Aug 1 Balance b/d 29 986

Debtors List

Debit Credit

G. Dwyer 14 069

A. Hendricks 9 861

M. Malinga 3 455

G. Docrat 2 687

E. Ebenza 5 438

32 823 32 823

Errors and omissions:

1. G. Docrat’s account of R2 687 was written off during May 2010. He was traced and the amount owing by him was recovered. However, the amount the amount was wrongly recorded in the debtors Control column of the CRJ during July 2010.

2. The total of the sales column in the Debtors journal was overstated by R250 while the total of the Debtors allowances column in the DAJ was understated by R80.

3. M. Malinga returned goods to the value of R110 but the bookkeeper incorrectly treated this as a credit sale and posted accordingly.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 47

4. Stock was sold on credit to A. Hendriks for R1 681. This was entered correctly in the journal, but was posted to his account as R1 861.

5. A cheque for R779 which was received from G. Dwyer had been dishonoured. A 5% discount had been allowed to him.

6. On 1 July 2010, E. Ebenza submitted a cheque for R4 000. This cheque was dated 7 July 2010. the cheque was deposited on the 9th, but was not recorded.

ACTIVITY 5:

Blue Traders sells 80% of their fashion wear on credit. their credit terms are strictly 30 days.

Study the information given below and answer the following questions:

5.1 Explain what action the bookkeeper should have taken when he discovered a difference of R6 800 in the reconciliation statements. Discuss at least two actions

5.2 Calculate the correct balance owing by the following debtors:

• D. Ben • A. Dish • J. Song

5.3 Calculate the opening balance in the debtors control account on 1 June 2010

Information:

Blue Traders

Reconciliation of the debtors control account to the debtors list on 31 May 2010:

R

Balance as per debtors control account 62 800

Balance as per debtors ledger 56 000

T. Tom 12 000

D Ben 9 000

C. Gordon 17 000

A. Dish 11 000

J. Song ?

Difference 6 800

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 48

Additional Information:

The following errors were discovered and must be corrected:

1. Goods sold on credit to A. Dish for R2 600 were correctly recorded in the in the debtors Journal but incorrectly posted as R6 200 to A. Dish’s account in the debtors ledger.

2. No entry has been made for a cheque of R6 000 which was returned by the bank due to insufficient funds. The cheque was originally received from D. Ben in settlement of a debt of R6 400.

3. The DAJ has been undercast by R5 600 4. An invoice issued to D. Ben for R2 400 has been posted to the wrong side of

her account

ACTIVITY 4:

General Ledger of Lotti Stores

Balance Sheet Accounts Section

Dr Debtors Control Account Cr

2010 July

1 Balance b/d 11 616 2010 July

31 Bank [6] CRJ 32 654

31 Sales [2] DJ 44 940 Discount allowed

CRJ 1 762

Bank [5] CPJ 6 457 Debtors allowances [3]

DAJ 2 308

Sundry accounts [1]

GJ 4 038 Sundry accounts [4]

GJ 1 084

Balance c/d 29 243

67 051 67 051

Aug 1 Balance b/d 29 243

\Calculations:

[1] = 1 200 + 2 687 + 110 + 41

[2] = 45 190 – 250

[3] = 2 228 + 80 = 2 388

[4] = 974 + 110

[5] = 5 678 + 779

[6] = 28 654 + 4 000

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 49

Debtors List on 31 July

Debit

G. Dwyer [14 069 + 779 + 41] 14 889

A. Hendricks [9 861 – 180] 9 681

M. Malinga [3 455 – 110 – 110] 3 235

G. Docrat [-2 687 + 2 687 0

E. Ebenza [5 438 – 4 000] 1 438

29 243

Note to teacher:

1. Since the amount was entered in the Debtors Control column of the CRJ, Docrst’s account was credited. This should not have been the case as his account was previously written off. furthermore a credit in his account indicates that Lotti Stores owes him R2 687. Correction of error ü A journal entry is required: Debtors control/ G. Docrat [+] is debited and bad

debts recovered account [+] is credited. bank is not affected – all monies received should recorded in CRJ and this was done, but the amount was entered in the Debtors Control account. it should have been recorded in the Sundry account column and reflected as Bad debts recovered.

2. sales is overstated by R250 therefore sales must decrease by R250. Debtors Allowances is understated by R80 therefore debtors Allowances must increase by R80. 3. Since this transaction was treated as a sale, debtors control/M. Malinga [+] was debited and sales account [+] was credited. Correction of error: ü A journal entry: Dr Sales [-]; Cr Debtors control/M. Malinga [-] ü Another journal entry is required to record the return: Dr Debtors Allowances

[+]; Cr Debtors Control/M. Malinga [-]

4. No journal entry is required as the amount was correctly recorded in the journal. Debtors control account is not affected, but the personal account of A. Hendriks was debited with R180 (1 861 – 1 681) extra. Correction of error: Subtract R180 in A. Hendrik’s account in the Debtors Ledger.

5. When the cheque was received:

Bank was debited and Debtors control/G. Dwyer was credited [-]

Discount Allowed was debited [+] and Debtors control/G. Dwyer was credited [-]

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 50

Correction of error:

ü Dr. Debtors Control/G. Dwyer [+] R779 ü Cr. Bank [-] R779 ü Dr Debtors control/G. Dwyer [+] R41 ü Cr Discount allowed [-] R41

calculation of the discount: 779 x 5/95 = R41

ACTIVITY 5:

5.1 The following should be checked;

• Entries in the Journals • additions • posting

5.2

D. Ben (9 000 + 6 400) 15 400

A. Dish (11 000 - 3 600) 7 400

J. Song (7 000 +2 400 + 2 400) 11 800

5.3 Debtors control balance on 1 June 2010:

Balance = R62 800 + 6 400 – 5 600 = R63 600

BUSINESS ETHICS

You should already know from what you have learned in grade 10 and 11 that most Professional Businesses operate according to an ethical code.

The ethics of a business set the standard according to which the employees in a business should conduct themselves.

1. All members of the business should follow the principles of ethics and professional behaviour, which include, amongst others:

• integrity • objectivity • professional competence and proper care • confidentiality • human rights and honesty

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 51

2. The ethic code also indicate how the business should deal with third parties, e.g. creditors, debtors, department of Labour and SARS

3. The has the responsibility towards the community, and the ethic code ensures that this is adhered to.

Summary: Business Ethics

Ethics is a system of values and behaviour that results in honesty, transparency and good business practice

there are many examples of unethical behaviour amongst office workers, such as cashiers, bookkeepers, accountants, lawyers and so on where money has been stolen from the business for personal use

This type of crime is called “White Collar Crime” and has become a serious problem for business owners.

Accountability:

Accountability means to be held responsible for your behaviour by the business or shareholders. A professional community expert’s behaviour in accordance with good practice and integrity.

Accountability therefore means to be responsible, within a given period of time, for the execution of certain tasks, and that the outcomes will be comparable with expectations. this means that an individual is responsible for the protection of assets and financial information of a business, and will be accountable should he or she abuses these.

Transparency:

It means making the truth available to others. The criteria for ensuring total transparency involve the following:

• Accounting transparency is based on the use of true, accurate, and complete information for recording in the accounting records.

• Each employee must cooperate fully so that events can be entered in the accounting records in full detail and on time.

• For each transaction supporting proof (source documents) should be supplied. • Each entry must reflect exactly whatever is indicated in the source document • An employee who becomes aware of any form of misconduct or neglect with

regards to the accounting records must report this to management . • Transparency should play a role in preventing financial fraud: Only by means of

transparency will it be possible to detect and prevent fraud and financial scandal.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 52

INTERNAL CONTROL

Internal control is the action taken by the business to ensure that the business fulfils its aims and goals

Types of control:

• Preventative: to prevent unwanted incidents, e.g. an alarm to prevent theft or break-ins.

• Detective: to detect the cause of unwanted incidents, e.g. the disappearance of stock – better control over stock.

• Affirmative/Correctional: to correct or set right unwanted incidents – better control over stock.

• Indicative: this a positive action to prevent unwanted incidents, e.g. “ no smoking” signs to protect the work place against fire.

internal control measures are essential in all businesses to ensure that employees are able to commit these crimes easily. Ethical behaviour is more difficult to enforce as it stems from personal values and attitudes.

Internal control over Cash:

Each business needs an effective internal control system for cash, as this could very easily be mismanaged. In smaller businesses, the owner or manager is able to have control over all cash transactions. In bigger businesses, however, it is impossible for one person to take control of this and control measures should therefore be put in place.

Cash control should adhere to the following requirements:

• People who receive, pay out o r handle cash should not be in control of the bookkeeping function as well. This prevents a person who misuses cash from hiding it by making a false entry.

• Keeping records of cash receipts must be of such a nature that the cash that has been received can be controlled against an independent daily record. This can be done by all cash receipts on source document, namely receipts, cash invoices and cash register rolls.

• All cash received must be banked daily and no payments should be made by means of this cash received. This ensures the safety of cash and bank deposits can serve as a control for cash received.

• All payments, except petty cash payments must be done by cheque. Cheques should be co-signed and verified by an authorised document that serves as a proof of payment.

• Cash verification must be done. this means that the amount of the actual cash at hand must be compared with the source documents.

• the cash receipt and the cash payment must be compared with the bank statement.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 53

• Payments from the petty cash must be limited to one person, and must be verified by a petty cash slip as a source document.

Internal credit control:

Debtors:

The following are internal control measures for keeping sufficient control over debtors:

• The business should have a properly formulated credit policy in place and the credit worthiness of clients must be determined before credit is allowed.

• All credit sales must be properly recorded on pre-numbered invoice and initialled by the sales person.

• The balance of the Debtors Control account must be reconciled on a monthly basis with the list of debtors in the debtors ledger.

• An age analysis of outstanding debts should be compiled. • Clients must be notified of outstanding amounts on regular basis and the terms of

payments. Writing off bad debts and other adjustments of debtors accounts must be properly authorised.

Creditors:

The following are internal control measures for keeping sufficient control over creditors:

• Goods received, must be controlled by means of the invoices of the creditors received.

• Duties must be separated – different people should be responsible for purchasing and receiving goods.

• The person responsible for the purchase of goods, should not be responsible for bookkeeping/ recording as well. In this way the recording of fictitious payments to creditors is avoided.

• The balance of the creditors control account must be reconciled with the list of creditors from the Credi tors Ledger on a monthly basis.

• Accounts payable should be paid as early as possible without incurring interest on the accounts, thus affecting the credit worthiness of the business.

THE DIFFERENCE BETWEEN AUDITING AND ACCOUNT ING:

Broadly, accounting is the writing up of the books and preparation of financial statements, while auditing involves the vouching or checking of the income and expenditure and the verification of the assets and liabilities in order to enable the auditor to compile a report.

Normally, an audit can only commence when the accounting work has been completed.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 54

ACTIVITY 1: In your groups, brainstorm examples of unethical conduct in your everyday life. ACTIVITY 2: Compile a list of other types of fraud, dishonesty or immoral conduct that might be encountered in a business. Draw columns as shown in the example below and list the offence as well as the stakeholders who will be affected by the offence in each case. Present your completed list to the class for discussion

No. Offence Stakeholder affected

.g.

Price fixing or overcharging customers

customers

1

2

3

4

5

6

7

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 55

ACTIVITY 3:

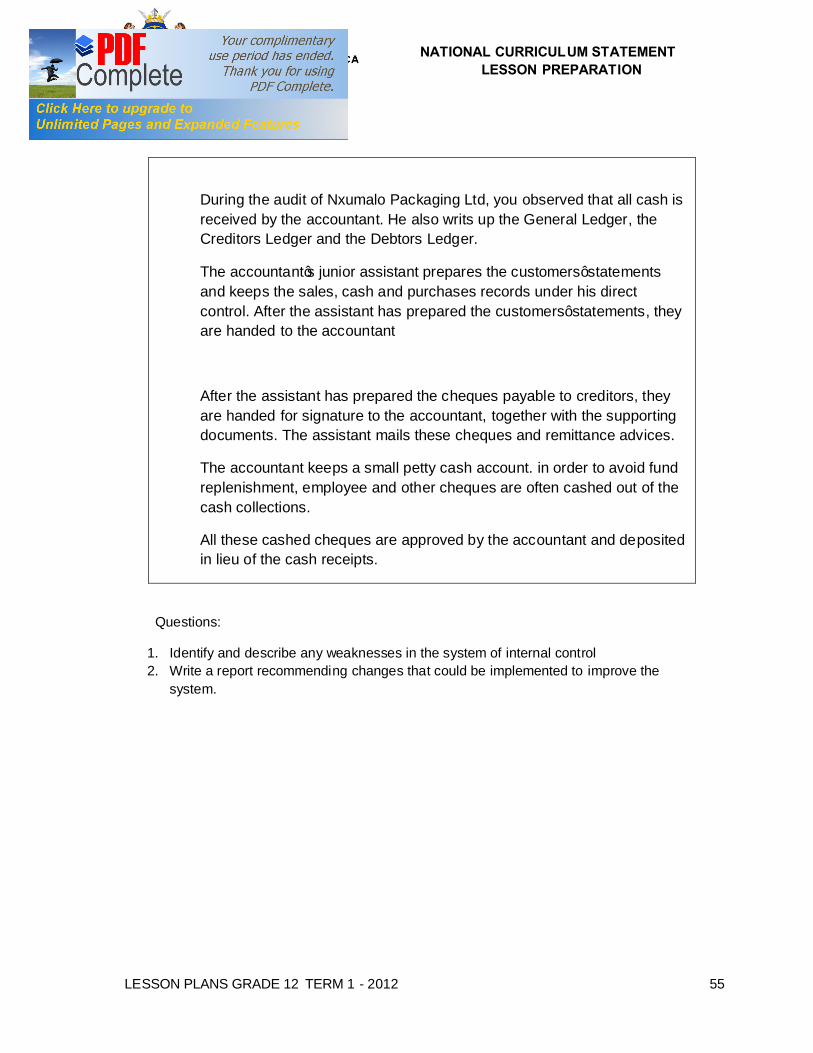

CASE STUDY 1:

During the audit of Nxumalo Packaging Ltd, you observed that all cash is received by the accountant. He also writs up the General Ledger, the Creditors Ledger and the Debtors Ledger.

The accountant’s junior assistant prepares the customers’ statements and keeps the sales, cash and purchases records under his direct control. After the assistant has prepared the customers’ statements, they are handed to the accountant

After the assistant has prepared the cheques payable to creditors, they are handed for signature to the accountant, together with the supporting documents. The assistant mails these cheques and remittance advices.

The accountant keeps a small petty cash account. in order to avoid fund replenishment, employee and other cheques are often cashed out of the cash collections.

All these cashed cheques are approved by the accountant and deposited in lieu of the cash receipts.

Questions:

1. Identify and describe any weaknesses in the system of internal control 2. Write a report recommending changes that could be implemented to improve the

system.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 56

ACTIVITY 4:

CASE STUDY 2;

The duties of the bookkeeper of W Picks Ltd included the writing up and reconciling of the Cash Receipt and Cash payment Journals and the opening of the mail.

Before commencing the audit, you are advised by the financial controller that the bookkeeper has been cashing her personal cheques out of the cash sales.

He established that, when one of her cheques was returned to the company marked R/D, she did not reflect in the CPJ, but included it as an item in the bank reconciliation, namely “R/D cheques”

1. Write down the steps you would take to establish whether or not this was an isolated case

2. Recommend measures to prevent similar occurrences in the future.

ACTIVITY 5: SCENARIO: Refer to each case below and indicate:

• The implication of each case • How each case should be dealt with.

No. Scenario Implication Action to be taken

1

The owner insist that all customers who pay him by cheque, make the cheque a “cash cheque” i.e. the word Cash is entered and not his name. Further more customers must not cash their cheques.

2

A deposit made by some other person appears on the bank statement of the trader

3

Reconciliation is not done on monthly basis. it is actually done when the boss requests an updated bank balance.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 57

4

Debtors who give bad cheques are threatened with legal action.

5

The owner keeps large amounts of business money at home.

6

A cheque for a large amount issued to a creditor has been outstanding in the bank reconciliation statement for 4 months.

7

A foreign debit order in favour of an unknown insurance company appears on the bank statement of the trader.

8

A customer paid his account on time, but his account does not reflect the payment. he produces the cancelled cheque as proof of payment.

9

At month-end, the cashier does not deposit all the cash on hand. He retains a certain amount. He deposit this amount on the 3rd or 4th day of the next month.

10 The total cash takings for a day do not coincide with the amount shown on the deposit slip.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 58

MODEL ANSWERS: ACTIVITY 1: Unethical conduct in everyday life;

• Copying home/class work • Copying in a test or examination • Plagiarism (this includes using information from the internet without

referencing it) • infringing on copyright laws (this includes copying CDs, DVDs and

downloading music from internet) • You could also discuss the effect of technology on modern

behaviour. ACTIVITY 2: Discuss each offence identified by the learner and allow them to provide examples for the offences they listed.

No. Offence Stakeholder affected

e.g.

Price fixing or overcharging customers

customers

1

Theft

Owners and /or employees

2

Bribery

Competitors

3

Environmental abuse

Community

4

Racism

Employees and customers

5

Sexual harassment

Employees/ employer

6

Misuse of business assets

Employees/ employer

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 59

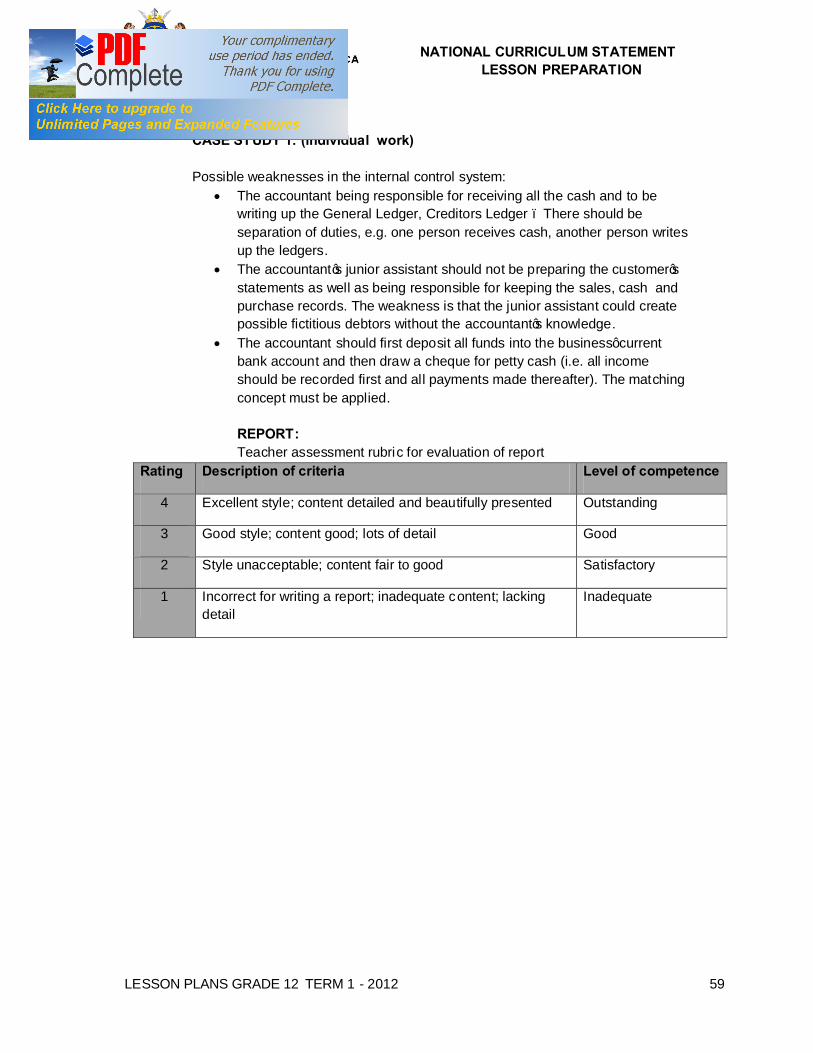

ACTIVITY 3: CASE STUDY 1: (individual work) Possible weaknesses in the internal control system:

• The accountant being responsible for receiving all the cash and to be writing up the General Ledger, Creditors Ledger – There should be separation of duties, e.g. one person receives cash, another person writes up the ledgers.

• The accountant’s junior assistant should not be preparing the customer’s statements as well as being responsible for keeping the sales, cash and purchase records. The weakness is that the junior assistant could create possible fictitious debtors without the accountant’s knowledge.

• The accountant should first deposit all funds into the business’ current bank account and then draw a cheque for petty cash (i.e. all income should be recorded first and all payments made thereafter). The matching concept must be applied. REPORT: Teacher assessment rubric for evaluation of report

Rating Description of criteria Level of competence

4 Excellent style; content detailed and beautifully presented Outstanding

3 Good style; content good; lots of detail Good

2 Style unacceptable; content fair to good Satisfactory

1 Incorrect for writing a report; inadequate content; lacking detail

Inadequate

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 60

ACTIVITY 4 CASE STUDY 2: (group work)

Possible steps the auditor will take:

• The auditor may check that all cash sales according to the cash register rolls (source document) have been written up in the deposit book and banked. When drawing a sample, the auditor will look for large sums of cash according to the cash register roll. (i.e. he will look for material amounts.)

• The auditor has to check all the cheques returned marked as R/D. • the auditor should also carry out random bank reconciliation, and scrutinise the other

months’ bank statements for any amounts that indicate that they are returned cheques

Accept all reasonable/logical answers, learners’ answers will vary.

ACTIVITY 5.

No. Scenario Implication Action to be taken

1

The owner insist that all customers who pay him by cheque, make the cheque a “cash cheque” i.e. the word Cash is entered and not his name. Further more customers must not cash their cheques.

The cheque can be cashed by anyone. The cheque does not have to be deposited into a bank account, it can be cashed over the counter. It seems that the owner does not want the payment to be reflected on the bank statement. It is likely that the owner does not keep a proper set of books as he does not want the payment to be processed in the normal way via his cheque account

The owner should be advised on the dangers of accepting cash cheques – they can be easily cashed by the wrong person. in order to ensure payment, he can insist that his customers pay him electronically – safer and more convenient. he may also insist on bank guaranteed cheques.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 61

2

A deposit made by some other person appears on the bank statement of the trader

The bank has made an error

He should inform the bank immediately, he should not keep quite as the error will be detected by the bank, and furthermore the person who made the deposit will investigate as the deposit most likely does not appear on his bank statement.

3

Reconciliation is not done on monthly basis. it is actually done when the boss requests an updated bank balance.

The books are not updated with entries in the bank statement, e.g. fees, debit orders, dishonoured cheques e.t.c.

The bookkeeper needs to be reminded of the importance of bank reconciliation as an important tool for internal control. The boss should ensure that this is done at least once a month.

4

Debtors who give bad cheques are threatened with legal action.

Legal actions entail legal costs which are charged to the customer’s bill.he debtor is charged a penalty fee by his bank.

The threat of legal action ensures that debtors have sufficient funds in their accounts when making cheque payments.

Legal action is a drastic step – it should be used only as a last resort. defaulters should be approached and some arrangements be made to recover the money. the defaulter is the customer of the business and his business is still needed. Careful screening of debtors is necessary.

5

The owner keeps large amounts of business money at home.

Unsafe practice – money is safer in a bank than at home

He should organize his banking times so that he does not have large amount of cash at any given time. he may invest in a safe at his home. Carrying large sums of money home is definitely not advisable.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 62

6

A cheque for a large amount issued to a creditor has been outstanding in the bank reconciliation statement for 4 months.

The creditor may have lost the cheque. He may have forgotten about the cheque. The creditor may have relocated or his business may have closed down.

Contact the creditor and enquire about the cheque. It may be necessary to write out new cheque

7

A foreign debit order in favour of an unknown insurance company appears on the bank statement of the trader.

The trader’s bank balance decreases with this debit order. It could be some type of scam organise by crime syndicate to siphon off money from people’s accounts.

He will need to if the debit order was authorised by any of the staff members. he must contact his bank immediately and arrange for the debit order instruction to be cancelled. if need be the police may have to be contacted

8

A customer paid his account on time, but his account does not reflect the payment. he produces the cancelled cheque as proof of payment.

The payment may not have been recorded in his account.

Investigate – check the receipt book and match with the deposit book, if correct the trader will have to apologise to the customer. The person responsible for posting must be reprimanded

9

At month-end, the cashier does not deposit all the cash on hand. He retains a certain amount. He deposit this amount on the 3rd or 4th day of the next month.

The cashier is withholding cash and using it for his own purposes. cash deposits are being understated.

An explanation would be required of the cashier. His actions amounts to fraud and he could be liable for prosecution

10 The total cash takings for a day do not coincide with the amount shown on the deposit slip.

As above As above

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 63

GRADE 12 SUBJECT

ACCOUNTING WEEKS TOPIC Age Analysis

THIS LESSON: WEEK DATE LESSON NR. 1 of 3

LESSON SUMMARY FOR: DATE STARTED:

88D8EDWW DATE COMPLETED:

5 CHBFSGHVJCSHJ

LESSON OBJECTIVES

At the end of this lesson, learners must be able to:

• Explain the need for preparing a Debtors’ Age Analysis.

TEACHER ACTIVITIES LEARNER

ACTIVITIES TIMING

RESOURCES NEEDED

1 1.1 1.2

Pre-knowledge Debtors’ Control Account. Statements of accounts sent to debtors.

Answer questions / Discussions

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 64

TEACHER ACTIVITIES LEARNER

ACTIVITIES TIMING

RESOURCES NEEDED

2

2.1

2.2

2.3

Introduction This aspect of the lesson must be considered to be important to the section on age analysis and should take the form of an interactive discussion between the teacher and the learners. Question learners on the purpose of preparing a Debtors’ Control Account.

• The balance on the control account represents the total amount due by all debtors appearing in the Debtors’ ledger.

• The balance can be verified with the total Debtors’ List. Question learners on the information that appears on the Statement of Account.

• Focus on the age analysis, the credit terms and credit limit, and discuss concerns.

Question learners on the need for preparing a Debtors’ Age Analysis.

• Highlight the fact that this information is crucial to the business as it informs the business on whether the debtor is paying on time or not.

Answer questions / Discussions

1.Transparenc

y with Debtors’

Control and

Debtors’ List.

2.

Transparency

of a statement

of account.

NATIONAL CURRICULUM STATEMENT LESSON PREPARATION

LESSON PLANS GRADE 12 TERM 1 - 2012 65

TEACHER ACTIVITIES

LEARNER ACTIVITIES

TIMING RESOURCES NEEDED

3

3.1

3.2

3.2.1

3.2.2

3.2.3