weather issues all over, but… - fats and oils

TRANSCRIPT

MarketingCommunication

October2018AFOAOutlookForum,NYC

StefanVogelGlobalSectorStrategist,Grains&OilseedsHeadofAgriCommodityMarketsResearch

GlobalOutlookonAgriculture

2

Weatherissuesallover,but…

3

WorstdroughtinEUandArgentinain>20years.DroughtinAustralia&issueselsewhere.

Source:Rabobank2018

average

Belowaverage

BaddroughtBaddrough

Baddrough

Slightlyaboveaverage

DespiteWorstdroughtimpactinEU&Argentinain>20years

4

Justimaginewherepriceswouldbeifallcountrieshavearecordcrop…

Source:Bloomberg,Rabobank2018

0

100

200

300

400

500

600

700

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

USD/

tonne

CBOT Wheat CBOT Soybeans +/- 20% of average CBOT Wheat

+/- 20% of average CBOT Soybeans CBOT Corn +/- 20% of average CBOT Corn

TradeWarsonthepoliticalagenda

5

USagricommoditiesheavilyimpactedreliantonexports

6Source:USDA,Rabobank2018

WHEAT

2018WHEATproductionshortfallinEU&Australiaand‘normalized’Russiancrop

8

Changeinproductionvs2017

-25,000

-20,000

-15,000

-10,000

-5,000

0

5,000

1000

t

2018 vs 2017 2019 vs 2017 Source:USDA,Rabobank2018

RussianWheatpricesliftoffagain

9

Russianwheatpricesreflectstrongexportdemand(whichareup20%yoyto15mtforJul-Sep,despitea20%loweryoyexportpotentialof33mtvs40mt)

Source:BSG,Rabobank2018

Biggestbullfactor:PotentialRUSSIANexport

restrictions

GlobalWheatwithlargestdeficitin15years

10

Butwhatwilltheyearafterbring?

Update

-40

-20

0

20

40

60

80

300

350

400

450

500

550

600

650

700

750

800

Mill

ion

tonn

es

Mill

ion

tonn

es

Surplus/Deficit (RHS) Production Total consumption Source:USDA,Rabobank2018

2019WHEATproduction(assumingaverageyields)bringsenough

11

Changeinproductionvs2017.

-25,000

-20,000

-15,000

-10,000

-5,000

0

5,000

1000

t

2018 vs 2017 2019 vs 2017

USwheatpricesforlate2019niceforfarmers,butEUpricesmorerealist!

12

+40%

+20%

Source:Bloomberg,Rabobank2018

13

CORN

Corn:RecordUSyield,butdon’tunderestimatedemand

14

YOYchangeincornfeedingglobally(outsideUS)underestimated!

0

50

100

150

200

250

0

100

200

300

400

500

600

700

USc/

bu

December 2018 Wheat-Corn Spread (RHS) CBOT Corn CBOT Wheat

Record$2/buWheat-Cornspreadtodrivecornfeedingdemandin2018/19

-20

-10

0

10

20

30

40

mlnto

nnes

corn wheat wheat&corn

Source:USDA,Rabobank2018

UScornbalance:Bullsneedyieldshortfallandstronguse,bearslookatASF&recordyield

15

2017/18sawexportsunderestimatedby600mbu!Willhistoryrepeat?Yes,butNO!

Source:USDA,Rabobank2018

SepWASDE bear bull% Change 16/17 17/18 (f) 18/19(f) 18/19(f) 18/19(f) Beginning Stocks 1,737 2,293 2,002 2,140 2,140Yield 174.6 176.6 181.3 183.0 180.0Production 15,148 14,604 14,827 14,964 14,719 Total Supply 16,942 16,937 16,879 17,154 16,909MY Exports 2,294 2,425 2,400 2,400 2,500Feed Consumption 5,470 5,450 5,575 5,400 5,600FSI Consumption 6,885 7,060 7,130 7,130 7,130Ethanol Usage 5,438 5,600 5,625 5,625 5,625 Total Consumption 12,355 12,510 12,705 12,530 12,730 Total Usage 14,649 14,935 15,105 14,930 15,230Ending Stocks 2,293 2,002 1,774 2,224 1,679Stocks/Usage 16% 13% 12% 15% 11%

16

USexports&exportsales50%upYOYsofar

CornexportpotentialfromkeyexportersexclUSatstronglevels

US2019/20cornexportswithastrongstart,butcompetitionwillbestiff

0

20

40

60

80

100

2015/16 2016/17 2017/18 2018/19mlnto

nnes

Ukraine Brazil Argentina othersSource:USDA,Rabobank2018

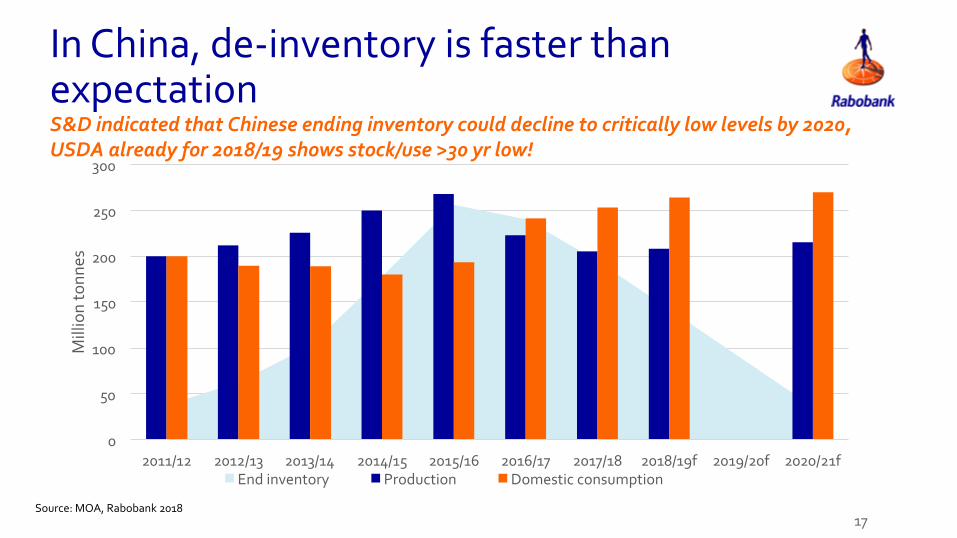

InChina,de-inventoryisfasterthanexpectation

17

S&DindicatedthatChineseendinginventorycoulddeclinetocriticallylowlevelsby2020,USDAalreadyfor2018/19showsstock/use>30yrlow!

0

50

100

150

200

250

300

2011/12 2012/13 2013/14 2014/15 2015/16 2016/17 2017/18 2018/19f 2019/20f 2020/21f

Milliontonn

es

Endinventory Production Domesticconsumption

Source:MOA,Rabobank2018

18

RecordWheat-Cornspreadtodrivecornfeedingdemandin2018/19

UScornandsoybeanpricesheavilydependonexports…Whatiftheydisappoint?!

Source:Bloomberg,Rabobank2018

LowUSexports

Resolvedtradewars

SOYBEANS

USsoybalance:Thedarksideoftradewars:potentially>1bnbuendingstocks

20

ContrarytoCorn,USDAdoesnotunderestimateuse.USsoybeanstockstopotentiallyhitmorethan1bnbu!

Source:USDA,Rabobank2018

SepWASDEOctWASDEtradeissue(Mln acres/Mln bu.) 16/17 17/18 (f) 18/19(f) 18/19(f) 18/19(f) Beginning Stocks 197 302 395 438 438 Yield 52.0 49.1 52.8 52.8 52.8 Production 4,296 4,392 4,693 4,693 4,693 Total Supply 4,515 4,715 5,113 5,156 5,156 MY Exports 2,166 2,130 2,060 2,060 1,950 Crush 1,901 2,055 2,070 2,070 2,055 Domestic Consumption 2,047 2,191 2,208 2,208 2,193 Total Usage 4,214 4,321 4,268 4,268 4,143 Surplus/Deficit 105 93 450 450 576 Ending Stocks 302 395 845 888 1,014 Stocks/Usage 7% 9% 20% 21% 24%

SingledigitUSsoybeanexportstoChinain2018/19?

21

USmightshipsomesoybeanstoArg/Brazilbutrequiresstrongmarketshareinrestofworld

3628

9

46

60

73

6 3 62 2 22 3 30 1 2

0

10

20

30

40

50

60

70

80

2016/17 2017/18 2018/19USA Brazil Argentina Canada Uruguay Others

Source:IEG,Rabobank2018

USsoybeanexportsdilemma…TheUSneedseither100%marketshareoutsideofChinaorpricebackintoChina

22

USsoybeanexportsareasbigasWorldexcl.Chinaimports,requiringtheUStogain~100%marketshareortogetChinabackintothetrademix

Source:USDA,Rabobank2018

PerfectlytimedimplementationofChinesedutiesonUSsoybean

23

ChinaintroduceddutiesinMay,whenanywaynoUSsoybeansgotoChina.But…

-

2,000

4,000

6,000

8,000

10,000

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

mlnto

nnesperm

onth

Min Range avg 2017-18

TotalUSsoybeanexportsstrongerthanusual…supportingprices

24

-

2,000

4,000

6,000

8,000

10,000

12,000

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

mlnto

nnesperm

onth

typicalUSexportstoworld Range avg 2017-18

USgainedmarketshareinimportcountries(exChina)duetopricediscount

HowtoalignUSexportswithworldexclChinaimportpattern?

25Source:USDA,Rabobank2018

Globalmonthlyimportsexcl.Chinaof3mto6mtonnespermontharenotenoughtoabsorbthetypicalhighUSpostharvestexportsinOct-Dec

Tradewar&pricingstructure:…SouthAmericansoybeansatUSD400/t,whileUSsoybeansarewellbelowduetothe25%duty

26

SpreadbetweenBrazilianandUSsoybeanpriceswillprevail,butseasonallywillchange

Source:USDA,Rabobank2018

WavingChineseimports?OrflatteningBrazilianExports?

27

ShowingtheneedtogetmoreSouthAmericansoybeanexportsinespeciallyNov-DectoChina.

Source:USDA,Rabobank2018

-4

-2

0

2

4

6

8

10

12

14

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

milliontonn

es

Braziliantotalexports Arg,Can,Ugytotalexp TotalChineseimports

EarlyharvestedParanasoybeansnotenough!

HowtomeetChina’sDecdemand?Can,Ru,Ukrnotenouth

AlmostsufficientChineseOct-Novcoverage.

TheWorldoutsideoftheUS…canjustaboutmeetChina’sdemand,butonlyifChinaget’s~100%oftheexports

28

Chinaisexpectedtoimport95mtonnes,equivalenttoallsoybeansexportedbycountriesotherthantheUS

Source:USDA,Rabobank2018

75

86 6 3 3 1

Chinaimportpotential,94

0

10

20

30

40

50

60

70

80

90

100

Brazil Argentina Paraguay Canada Uruguay Ukraine Russia

mlnto

nnes

8512

TheOutlookfor2019withSouthAmericancurrenciesunderpressure

29

Productionisbeingincentivisedinmanyproducingcountries…butnotintheUS.

Source:Bloomberg,Rabobank2018

Brazil…4-6%acreageexpansionkeepsproductionaboutunchangedat120mt,butgoodyieldsarerequired!!

30

Exportsmighthit80mtvs76mtincurrentseason,requiringaslowercrush.

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

AreaHarvested Production Exports Crush

1000

tonn

es

2015/16 2016/17 2017/18 2018/19 2018/19alternative

Source:USDA,Rabobank2018

Argentineexporttaxchanges:Soybeansgainincompetitivenessrelativetograins

31

WeakArgentinepesobenefitsexports,whilefarmingcostsareonly55-60%inUSD(fertilizer,seed,…)while40-45%isinARS(labor,fuel,…)

Source:Rabobank2018

GoodnewsforArgentinebiodiesel:EUComdecidednottoreinstateimporttariffsonimportedArgentinebiodiesel(fornow!FurtherInvestigationswilltakeplace)

SouthAmericansoybeanproductioncouldhitanewrecordin2019

32

Closeto200mtofproductionanda12%to17%recoveryfromthisyear!

97115 120 121

5955 38

57

170185

171193

0

50

100

150

200

2015/16 2016/17 2017/18 2018/19

mlnto

nnes

Brazil Argentina Paraguay Bolivia Uruguay

Source:USDA,Rabobank2018

ElNiño–ARealThreatin2018/19?

33

Riskhasbeensomewhatloweredrecently,butstillafactortowatch

Source:AustralianBureauofMeteorology,Bloomberg,NOAA,Rabobank2018

-40

-30

-20

-10

0

10

20

30

SO

I

El Niño threshold La Niña threshold Southern Oscillation Index (SOI) 5-month moving average

Moderate Weak Moderate/Weak

Strong WeakStrong

StrongStrong/Moderate

Previous El Niño

ENSOAlertSystemStatus:ElNiñoWatchEquatorialseasurfacetemperatures(SSTs)arenear-to-aboveaverageacross

mostofthePacificOcean.Thereis~55%chanceofElNiñointheNorthernHemispherefall2018(September-November),increasingto~70%duringwinter2018-19.

PotentialImpactsofaSouthernHemisphereElNiñoEvent

34

Bothunfavourableandfavourableimpactsarepossibleforagricommodities

Source:NOAA,Rabobank2018

AustraliaDrierandwarmer-than-normal

SouthEastAsiaDrierandwarmer-than-normal

IndiaOftenareductionintheintensityoftheIndianMonsoonSouthernUSCanadaandnorthernUScanseemildwinters,whiletheUSsouthernstatescanexpectawetter-than-normalwinter

BrazilWetter-than-normalconditionsareoftenexperiencedacrosssouthernBrazil,whilenorthernBrazilcanexperiencedryness.

USchangeinplantingsfor2019:Lesssoybeans,buthowmuch?

35

Soy/cornpriceratioat2.3forend2018andend2019,callsforsomemorecorn,butnotadramaticcutinsoyacreage,whilemarketactuallyneedsa4-5macrescutinsoybean

1.9

2.1

2.3

2.5

2.7

2.9

3.1

3.3

3.5

3.7

3.9

Dec-12

Feb-13

Apr-13

Jun-13

Aug

-13

Oct-13

Dec-13

Feb-14

Apr-14

Jun-14

Aug

-14

Oct-14

Dec-14

Feb-15

Apr-15

Jun-15

Aug

-15

Oct-15

Dec-15

Feb-16

Apr-16

Jun-16

Aug

-16

Oct-16

Dec-16

Feb-17

Apr-17

Jun-17

Aug

-17

Oct-17

Dec-17

Feb-18

Apr-18

Jun-18

Aug

-18

Oct-18

Dec-18

Feb-19

Apr-19

Jun-19

Aug

-19

Oct-19

soy/corn

moresoy

morecorn

Source:Bloomberg,Rabobank2018

US2019acreagesplit:Lesssoy,moreothers

36

USsoyacreagecutnottoimmediatelymoveallintocorn,iftradewarsstayinplace&SouthAmericancropsaregood,a6macrescutisnoproblematall!!

-8

-6

-4

-2

0

2

4

soybean corn wheat cotton

yoych

ange

inacrea

g(m

acres)

withtarrifs withouttariffs

Source:Rabobank2018

VEGOILS

37

VEGETABLEOILS

Globaloilproductiongrowthexceedstrendinrecentyears(CAGR4.3%)

38

ProductiongrowthCAGR4.3%inpastdecade

Source:USDA,Rabobank2018

39

MalaysianMayandJun2018CPOproduc7onlowestinmanyyears

Indonesiaproduc7onstrong,offse@ngMalaysianshorBall,butithasbeenquitedryposingfutureproduc7onrisk

Palmoilstocksarehighandsoybeanoilisgettingcheaperduetotradewars.

0.8

1

1.2

1.4

1.6

1.8

2

2.2

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun Jul

Aug

Sep

millionsto

nnes

5yrhigh 16/1717/18 5yravg

0

1

2

3

4

5

Jan

Feb

Mar

Apr

May

Jun Jul

Aug

Sep

Oct

Nov

Dec

millon

tonn

es

2016 2017 2018Source:MPOB,Bloomberg,Rabobank2018

India:Slowveg.oilgrowth…duetohighimportduties.Especiallysoyoiluseandsomewhatconsumptionslowed

40

2018/19tobringrisingimportsduetopoorcottonandpeanutcropanddespitesoyrecovery

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

5,000

10,000

15,000

20,000

25,000

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17 2017/18 2018/19

YOYgrow

th(%)

1000

tonn

es

Oil,Palm Oil,Soybean other imports consumptiongrowth(%)

Indiansoycropto

recoverto10mvs8.2mt,butcotton&peanutdown

Source:USDA,Rabobank2018

Chineseveg.oilimportstorecoverin2019,drivenbyreducedsoycrush

41

Importsofpalmoil,soyoilandpartlyotheroilstobenefitfromtradewars

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

2,000

4,000

6,000

8,000

10,000

12,000

1993

/94

1994

/95

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

2011/12

2012

/13

2013/14

2014

/15

2015

/16

2016

/17

2017/18

2018

/19

Source:USDA,Rabobank2018

MarketingCommunication

October2018vegoilsandsoymeal

StefanVogelGlobalSectorStrategist,Grains&OilseedsHeadofAgriCommodityMarketsResearch

10year0utlookforoils&meal

Globalvegetableoilproductionincreased3.5Xinlast25years,withpalmrising5X.

43

Willthisproductionrallycontinueinthenextdecade?

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

SoutheastAsia

EastAsia SouthAmerica

EuropeanUnion-28

NorthAmerica

FormerSovietUnion

-12

otherAsia Africa other

1993/94 1998/99 2003/04 2008/09 2013/14 2018/19

Soy

Mal & Ind Palm

Rape & sun & soy

Soy

China soy

Source:USDA,Rabobank2018

50

55

60

65

70

75

80

85

90

2012 2013 2014 2015 2016 2017 2018f 2019f 2020f 2021f 2022f 2023f 2024f 2025f 2026f 2027f 2028f 2029f 2030f

mill

ion

tonn

es

Global production high case Global production base case Global production low case Global production better-seed case

Global palm oil production increases on the back of increasing South-East Asian production

Global palm oil production decreases due to decreasing South-East Asian production, a result of replanting and old oil palm trees

Improving global palm oil production situation, as oil palm trees which were planted in Indonesia and Malaysia from 2018 to 2023 reach their young mature and mature stages

Low global palm oil price environment

Neutral to already slightly bullish price environment Bullish price environment

Global palm oil consumption is required to increase more than ‘long-term’ consumption. Thus, low palm oil prices are needed

Global palm oil consumption will have to decline from previous years, as global production decreases

Global palm oil consumption will decrease more than ‘long-term’ consumption in order to adjust for global palm oil supply availability

Other vegetable oils will fill the difference between palm oil base-case consumption and ‘long-term’ consumption

ThedecreaseinSouth-EastAsianpalmoilproductionpost-2021willresultinabullishpalmoilpriceenvironment

Source:UnitedNations,ChineseMinistryofAgriculture,IndonesianDirectorateGeneralofEstateCropsMPOB,USDA,Rabobank2018AgriCommodityMarketsResearch

ChinaSoybeandemandgrowthslowing,evenifthetradewarswouldberesolved

45

+75m tonnes

+45m tonnes

Source:USDA,Rabobank2018

EURapeseedproductionmaxedout,soyontherise

46

AnalmostflatoutlookforEUrapeseedproctioninnext10years

Source:USDA,Rabobank2018

Consumptiongrowthbyregion&keydrivers

47Source:USDA,Rabobank2018

Food 9m & industrial 12m t

food

China food

Food +4.5m & industrial+11m t

Food +5m & industrial+5m t

Food +4m & industrial+7m t

India food

India’simportgrowthsofvegetableoilstoslowto25mtfor35mtconsumption

48

Palmoiltoposethebiggestabsoluteincrease,buttoloosesharestosoy&sun

Sources:USDA,Rabobank2018

Africa:Importstoriseby1/3rdthrough2030from9mtto12mt

49

Thegapbetweenvegetableoilconsumptionandproductioniswidening,2010-2030f

Source:Rabobank2018

RisingAfricanVegetableOilImportsinNextDecade

50Source:Rabobank2018

Globalsoymealuseroseby75mt…or~50%inthepastdecade

51

Howmuchwilltheglobalsoymealdemandriseinthenextdecade?

Source:USDA,FAO,Rabobank2018

Globalmeat&aquaculturegrowth…isslowinginnextdecade(+56mtvs+84mt)

52

Adding56mtofmeatproductionor+15%in10years

Source:USDA,FAO,Rabobank2018

Globalmeat&aquaculturegrowth…isslowinginnextdecade(+56mtvs+84mt)

53

Representinga1/3rdslowergrowthcomparedtopreviousdecade

Source:USDA,FAO,Rabobank2018

Globalmeat&aquaculturegrowth…isslowinginnextdecade(+56mtvs+84mt)

54

Poultryforecasttogrowth55%lessinnextdecade,porkandaquaculture26%less

Source:USDA,FAO,Rabobank2018

Globalsoymealusetorisebyonly50-55mt…or~22%inthenextdecade

55

Howmuchwilltheglobalsoymealdemandriseinthenextdecade?

Source:USDA,FAO,Rabobank2018

287

Futureexportsofsoymealtogrow…atsimilarlevelasinthepastDespiteadeclineofglobalsoymealconsumptiongrowth

56

Changeofglobalsoymealuse2006/08-2016/18vs2016/18-2026/28

Source:USDA,FAO,Rabobank2018

57

UScrushtobenefitfromdomesticmealuse

USSoybeans…despitetheChinasetback,long-termproductionisexpectedtorise

Source:USDA,Rabobank2018

0

10

20

30

40

50

0

40

80

120

160

200

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

2011/12

2012

/13

2013/14

2014

/15

2015

/16

2016

/17

2017/18e

2018

/19f

2019

/20f

2020

/21f

2021

/22f

2022

/23f

2023

/24f

2024

/25f

2025

/26f

2026

/27f

2027/28f

mhec

tares

mto

nnes

Production(LHS) Area(RHS)

Braziliansoybeanproduction…isexpectedtoreach157mtonnesplantedin45.5mhectaresin2027/28

58

Brazil'ssoybeanproductionandacreageforecast,2000/01-2027/28f

Source:USDA,Rabobank2018

0

6

12

18

24

0

20

40

60

8020

00/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

2011/12

2012

/13

2013/14

2014

/15

2015

/16

2016

/17

2017/18e

2018

/19f

2019

/20f

2020

/21f

2021

/22f

2022

/23f

2023

/24f

2024

/25f

2025

/26f

2026

/27f

2027/28f

mhec

tares

mto

nnes

Production(LHS) Area(RHS)

Argentinesoybeanproduction…isexpectedtoreach68mtonnesplantedin22mhectaresin2027/28

59

Argentina'ssoybeanproductionandacreageforecast,2000/01-2027/28f

Source:USDA,Rabobank2018

TheWildcards:India

60

Risingdomesticmealdemandturnsthecountrysoonintoanetimportereitherofsoybeansorofsoymeal

Source:USDA,Rabobank2018

6161

ThisdocumentismeantexclusivelyforyouanddoesnotcarryanyrightofpublicationordisclosureotherthantoCoöperatieveRabobankU.A.(“Rabobank”),registeredinAmsterdam.Neitherthisdocumentnoranyofitscontentsmaybedistributed,reproduced,orusedforanyotherpurposewithoutthepriorwrittenconsentofRabobank.Theinformationinthisdocumentreflectsprevailingmarketconditionsandourjudgementasofthisdate,allofwhichmaybesubjecttochange.Thisdocumentisbasedonpublicinformation.Theinformationandopinionscontainedinthisdocumenthavebeencompiledorderivedfromsourcesbelievedtobereliable;however,Rabobankdoesnotguaranteethecorrectnessorcompletenessofthisdocument,anddoesnotacceptanyliabilityinthisrespect.Theinformationandopinionscontainedinthisdocumentareindicativeandfordiscussionpurposesonly.Norightsmaybederivedfromanypotentialoffers,transactions,commercialideas,etceteracontainedinthisdocument.Thisdocumentdoesnotconstituteanoffer,invitation,orrecommendation.Thisdocumentshallnotformthebasisof,orcannotberelieduponinconnectionwith,anycontractorcommitmentwhatsoever.Theinformationinthisdocumentisnotintended,andmaynotbeunderstood,asanadvice(including,withoutlimitation,anadvicewithinthemeaningofarticle1:1andarticle4:23oftheDutchFinancialSupervisionAct).ThisdocumentisgovernedbyDutchlaw.ThecompetentcourtinAmsterdam,theNetherlandshasexclusivejurisdictiontosettleanydisputewhichmayariseoutof,orinconnectionwith,thisdocumentand/oranydiscussionsornegotiationsbasedonit.ThisreporthasbeenpublishedinlinewithRabobank’slong-termcommitmenttointernationalfoodandagribusiness.ItisoneofaseriesofpublicationsundertakenbytheglobaldepartmentofRaboResearchFood&Agribusiness.©2018-AllRightsReserved.

Rabobank Food and Agribusiness Research & Advisory Stefan Vogel

Head of Agri Commodity Markets Research Global Sector Strategist Grains & Oilseeds

Telephone +44 (0) 20 7664 9523 Email [email protected]

Contacts:

London office Thames Court

One Queenhithe

London EC4V 3RL United Kingdom

62Source:USDA,FAO,Rabobank2018

Additionalsoymealdemandbycountryfrom2006/08to2016/18(mlnt)

Wherehappenedthegrowth…anddidcrushingatoriginordestinationrisemost?

Regionswithsoymealusedeclineoverpastdecade(ttl-5.6mtonnes)

Wildcards:AlternativeMeat

63

Ifittasteslikemeatandlookslikemeat,itmightnotbemeat…

Veggiemealswon’tkillyourfeedbusiness…butwillslowthefuturegrowth

64

Despitestrongconsumptiongrowthofalternativeproteins,volumesareforecasttostaybelow1%ofmeatproductionvolumes,2016-2022

Source:Rabobank2018

• Keydriversin2019forglobalvegoiltradeflows• • Vegoilsuppliesinglobalmarketsarelikelytoremainhighin2018/19;IndonesianCPOproductionmorethancompensatingforslightlylowery-o-yMalaysianproduction,USisexpectingrecordhighsoybeancrop;andlocallyinIndia,thankstodecentmonsoon,domesticoilseedandvegoilsuppliesarelikelytoremainbettery-o-y.

• Tradewarandcrudeoilarelikelytocontinuedictatingtheglobalvegoilpricesincomingseason.AnyupsurgeinbrentcrudepricescouldtriggerhigherCPOconsumption;orMPOBpalmpricinghastogodownfromcurrentlevelstotriggerdemandrecovery(butwithcurrentpricing,lowscopeforfurtherpricedrop).