warren buffett stock picks valuation

DESCRIPTION

http://www.oldschoolvalue.comCompilation of warren buffett stock valuations from Old School Value.Valuation and commentary on all 41 stocks of Warren Buffett and Berkshire Hathaway.TRANSCRIPT

Created using zinepal.com. Go online to create your own zines or read what others have already published. 1

Valuation of WarrenBuffett Stock PicksWarren Buffett Stock Picks:Part 1Warren Buffett Stocks: Part 1 | Part 2 | Part 3 | Part 4

With Berkshire Hathaway disclosing their holdings in theirlatest 2nd quarter 13-F, I thought it would be interesting to gothrough each position that is held and calculate the stock valuein hopes of gaining some ideas.

Going through portfolio’s of respected investors is anotherway of generating ideas. Davy Bui of The EnlightenedAmerican does a fine job of tracking and displaying hedge fundholdings of respected investors in an easy to read format.

There are 41 positions in the portfolio of Warren Buffett andBerkshire so I’ll be breaking it up over numerous posts.

Old School Value’s Circle of CompetenceAlthough I’ll try to put a value on each company, exceptfinancials, there are industries that are outside of my circle ofcompetence which I may calculate incorrectly.

E.g. I don’t know much about pharmaceuticals andcommodities and how to look at these businesses as a futuregoing concern which will make it difficult to apply a growthrate that I would be comfortable with compared to others.

Going through the first 10 Stock Ideas

• American Express (AXP) - outside circle of competence

• Bank of America (BAC) - outside circle of competence

• Becton Dickinson & Co (BDX) - Latest addition to theportfolio

• Burlington Northern Santa Fe (BNI)

• CarMax (KMX)

• Coca Cola (KO) - quick analysis

• Comcast Corp (CMCSA)

• Comdisco Holding (CDCO)

• ConocoPhilips (COP)

• Costco (COST) - analysis

(Current stock prices vary due to timing of writing)

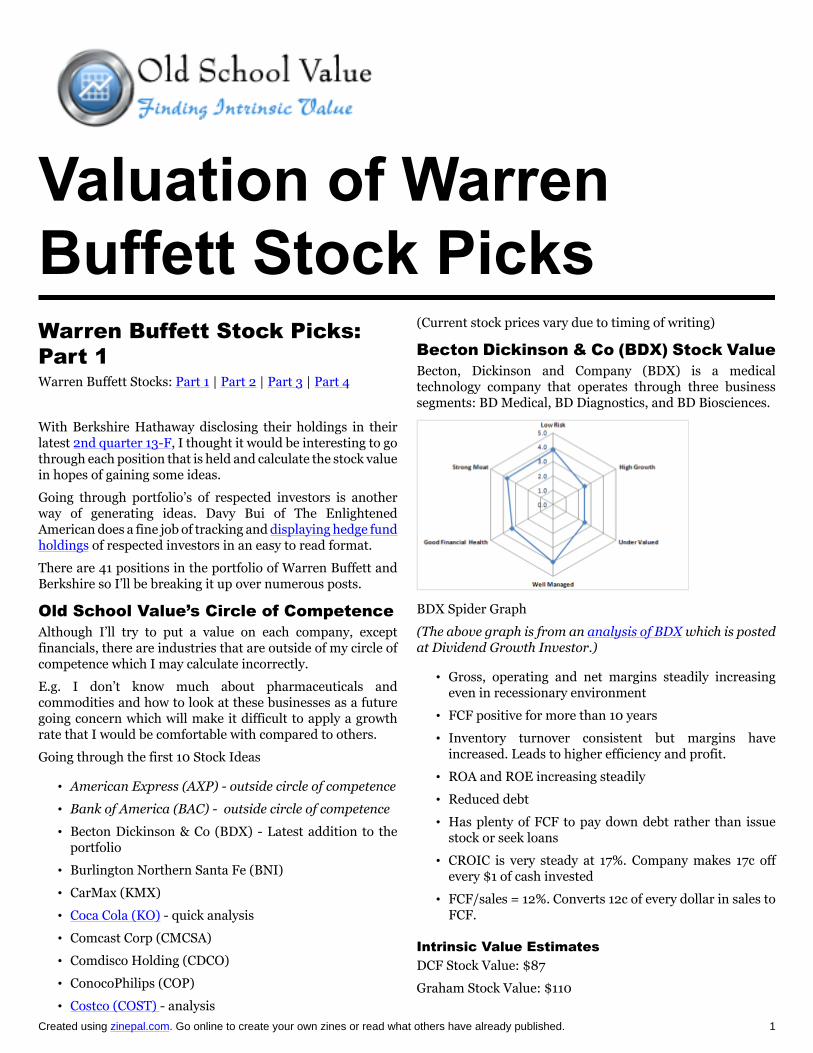

Becton Dickinson & Co (BDX) Stock ValueBecton, Dickinson and Company (BDX) is a medicaltechnology company that operates through three businesssegments: BD Medical, BD Diagnostics, and BD Biosciences.

BDX Spider Graph

(The above graph is from an analysis of BDX which is postedat Dividend Growth Investor.)

• Gross, operating and net margins steadily increasingeven in recessionary environment

• FCF positive for more than 10 years

• Inventory turnover consistent but margins haveincreased. Leads to higher efficiency and profit.

• ROA and ROE increasing steadily

• Reduced debt

• Has plenty of FCF to pay down debt rather than issuestock or seek loans

• CROIC is very steady at 17%. Company makes 17c offevery $1 of cash invested

• FCF/sales = 12%. Converts 12c of every dollar in sales toFCF.

Intrinsic Value EstimatesDCF Stock Value: $87

Graham Stock Value: $110

Created using zinepal.com. Go online to create your own zines or read what others have already published. 2

Competitor and Peer Comparison: $76

BDX Price vs Value Graph

Burlington Northern Santa Fe (BNI) StockValueBurlington Northern Santa Fe is a holding company andengaged primarily in the freight rail transportation business.

• Impressive FCF growth previous 4 years and especiallylast year

• High capex but latest annual result was extraordinary

• lower sales and margins but improved efficiency inreturns and turnover

• CROIC is on the low side at 3%

• Top line growth is also above average at 14%

• Debt to equity ratio is above 200% which isn’tuncommon for capex heavy companies

Intrinsic Value EstimatesDCF Stock Value: $87

Graham Stock Value: $145

Competitor and Peer Comparison: $76

BNI Price vs Value Graph

CarMax (KMX) Stock ValueThe Company is a retailer of used cars.

• Increase in gross margins but decline in operating andnet margin

• Increased cash levels but a huge amount

• Highest accounts receivables to date. Check whether it isdue to non paying customers or more lenient terms.

• No intangibles (as it should be with low to no moatcompanies)

• No long term debt

• Capex a little lower than the upper range

• Latest year cash from operations included higheramount of interest from securities and cash fromreduction inventory

• Inventory turnover at the upper range

• FCF and CROIC close to 0%

Intrinsic Value EstimatesDCF Stock Value: N/A

Graham Stock Value: $11 - $15

Competitor and Peer Comparison: N/A

Can’t seem to get within an acceptable fair value range onCarMax.

Thin margins, cyclical, inconsistent with low returns. Notquite sure how this position fits in. Definitely doesn’t look likea Buffett pick.

Coca Cola (KO) Stock ValueNo introduction needed.

• Price and value have been consistent

• Numbers throughout the past 10 years are excellent

• Previous business spider graph, fair value estimate andautomated KO dcf valuation

Intrinsic Value EstimatesDCF Stock Value: $38 - $44

Graham Stock Value: $61

Competitor and Peer Comparison: Looks fairly valued

KO Price & Value Graph

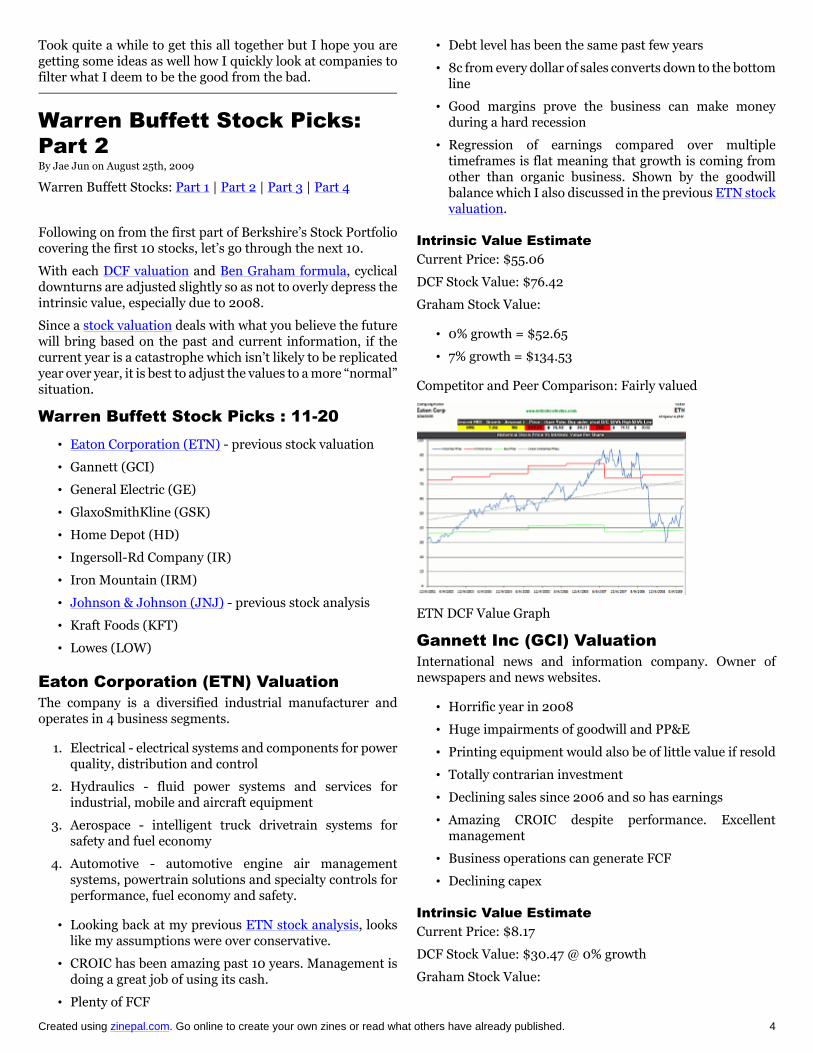

Comcast Corp (CMCSA) Stock ValueComcast Corporation is a provider of cable TV, internet andphone services.

Created using zinepal.com. Go online to create your own zines or read what others have already published. 3

• FCF and CROIC are close. 10.9% and 9.4% respectively.This scenario occurs when a company has maturedwithout much growth to be expected.

• Excellent margins and very stable returns in both the2001 and 2008 recession

• Not over leveraged

• Plenty of FCF to cover debt

• Big decrease in tangible shareholders equity since 2005

• Intangibles more than double in 2007

Intrinsic Value EstimatesDCF Stock Value: N/A

Graham Stock Value: $22

Competitor and Peer Comparison: $12.48

CMCSA Graham Formula

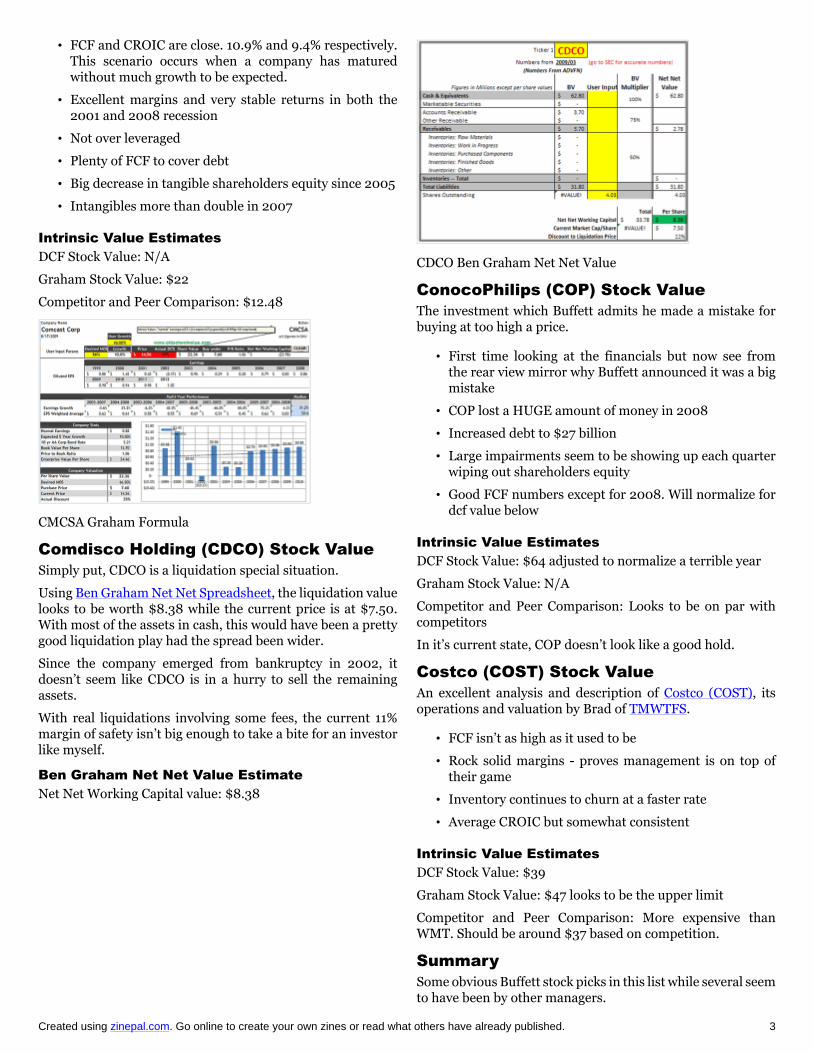

Comdisco Holding (CDCO) Stock ValueSimply put, CDCO is a liquidation special situation.

Using Ben Graham Net Net Spreadsheet, the liquidation valuelooks to be worth $8.38 while the current price is at $7.50.With most of the assets in cash, this would have been a prettygood liquidation play had the spread been wider.

Since the company emerged from bankruptcy in 2002, itdoesn’t seem like CDCO is in a hurry to sell the remainingassets.

With real liquidations involving some fees, the current 11%margin of safety isn’t big enough to take a bite for an investorlike myself.

Ben Graham Net Net Value EstimateNet Net Working Capital value: $8.38

CDCO Ben Graham Net Net Value

ConocoPhilips (COP) Stock ValueThe investment which Buffett admits he made a mistake forbuying at too high a price.

• First time looking at the financials but now see fromthe rear view mirror why Buffett announced it was a bigmistake

• COP lost a HUGE amount of money in 2008

• Increased debt to $27 billion

• Large impairments seem to be showing up each quarterwiping out shareholders equity

• Good FCF numbers except for 2008. Will normalize fordcf value below

Intrinsic Value EstimatesDCF Stock Value: $64 adjusted to normalize a terrible year

Graham Stock Value: N/A

Competitor and Peer Comparison: Looks to be on par withcompetitors

In it’s current state, COP doesn’t look like a good hold.

Costco (COST) Stock ValueAn excellent analysis and description of Costco (COST), itsoperations and valuation by Brad of TMWTFS.

• FCF isn’t as high as it used to be

• Rock solid margins - proves management is on top oftheir game

• Inventory continues to churn at a faster rate

• Average CROIC but somewhat consistent

Intrinsic Value EstimatesDCF Stock Value: $39

Graham Stock Value: $47 looks to be the upper limit

Competitor and Peer Comparison: More expensive thanWMT. Should be around $37 based on competition.

SummarySome obvious Buffett stock picks in this list while several seemto have been by other managers.

Created using zinepal.com. Go online to create your own zines or read what others have already published. 4

Took quite a while to get this all together but I hope you aregetting some ideas as well how I quickly look at companies tofilter what I deem to be the good from the bad.

Warren Buffett Stock Picks:Part 2By Jae Jun on August 25th, 2009

Warren Buffett Stocks: Part 1 | Part 2 | Part 3 | Part 4

Following on from the first part of Berkshire’s Stock Portfoliocovering the first 10 stocks, let’s go through the next 10.

With each DCF valuation and Ben Graham formula, cyclicaldownturns are adjusted slightly so as not to overly depress theintrinsic value, especially due to 2008.

Since a stock valuation deals with what you believe the futurewill bring based on the past and current information, if thecurrent year is a catastrophe which isn’t likely to be replicatedyear over year, it is best to adjust the values to a more “normal”situation.

Warren Buffett Stock Picks : 11-20• Eaton Corporation (ETN) - previous stock valuation

• Gannett (GCI)

• General Electric (GE)

• GlaxoSmithKline (GSK)

• Home Depot (HD)

• Ingersoll-Rd Company (IR)

• Iron Mountain (IRM)

• Johnson & Johnson (JNJ) - previous stock analysis

• Kraft Foods (KFT)

• Lowes (LOW)

Eaton Corporation (ETN) ValuationThe company is a diversified industrial manufacturer andoperates in 4 business segments.

1. Electrical - electrical systems and components for powerquality, distribution and control

2. Hydraulics - fluid power systems and services forindustrial, mobile and aircraft equipment

3. Aerospace - intelligent truck drivetrain systems forsafety and fuel economy

4. Automotive - automotive engine air managementsystems, powertrain solutions and specialty controls forperformance, fuel economy and safety.

• Looking back at my previous ETN stock analysis, lookslike my assumptions were over conservative.

• CROIC has been amazing past 10 years. Management isdoing a great job of using its cash.

• Plenty of FCF

• Debt level has been the same past few years

• 8c from every dollar of sales converts down to the bottomline

• Good margins prove the business can make moneyduring a hard recession

• Regression of earnings compared over multipletimeframes is flat meaning that growth is coming fromother than organic business. Shown by the goodwillbalance which I also discussed in the previous ETN stockvaluation.

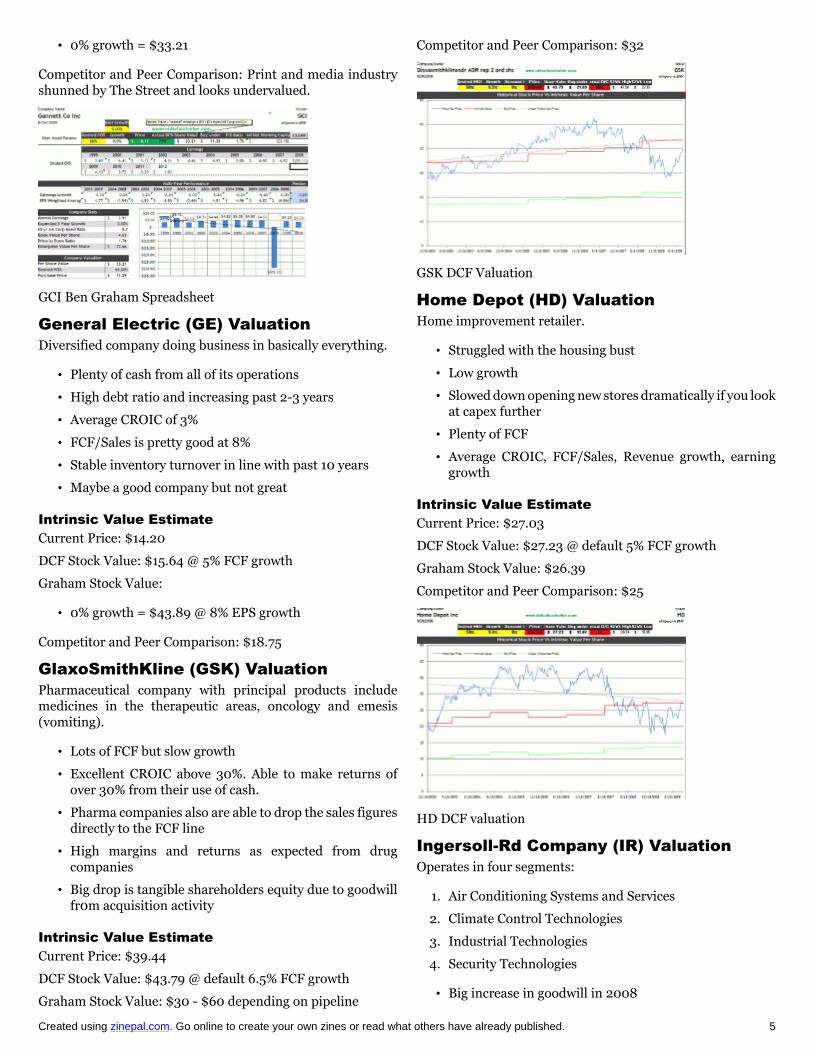

Intrinsic Value EstimateCurrent Price: $55.06

DCF Stock Value: $76.42

Graham Stock Value:

• 0% growth = $52.65

• 7% growth = $134.53

Competitor and Peer Comparison: Fairly valued

ETN DCF Value Graph

Gannett Inc (GCI) ValuationInternational news and information company. Owner ofnewspapers and news websites.

• Horrific year in 2008

• Huge impairments of goodwill and PP&E

• Printing equipment would also be of little value if resold

• Totally contrarian investment

• Declining sales since 2006 and so has earnings

• Amazing CROIC despite performance. Excellentmanagement

• Business operations can generate FCF

• Declining capex

Intrinsic Value EstimateCurrent Price: $8.17

DCF Stock Value: $30.47 @ 0% growth

Graham Stock Value:

Created using zinepal.com. Go online to create your own zines or read what others have already published. 5

• 0% growth = $33.21

Competitor and Peer Comparison: Print and media industryshunned by The Street and looks undervalued.

GCI Ben Graham Spreadsheet

General Electric (GE) ValuationDiversified company doing business in basically everything.

• Plenty of cash from all of its operations

• High debt ratio and increasing past 2-3 years

• Average CROIC of 3%

• FCF/Sales is pretty good at 8%

• Stable inventory turnover in line with past 10 years

• Maybe a good company but not great

Intrinsic Value EstimateCurrent Price: $14.20

DCF Stock Value: $15.64 @ 5% FCF growth

Graham Stock Value:

• 0% growth = $43.89 @ 8% EPS growth

Competitor and Peer Comparison: $18.75

GlaxoSmithKline (GSK) ValuationPharmaceutical company with principal products includemedicines in the therapeutic areas, oncology and emesis(vomiting).

• Lots of FCF but slow growth

• Excellent CROIC above 30%. Able to make returns ofover 30% from their use of cash.

• Pharma companies also are able to drop the sales figuresdirectly to the FCF line

• High margins and returns as expected from drugcompanies

• Big drop is tangible shareholders equity due to goodwillfr0m acquisition activity

Intrinsic Value EstimateCurrent Price: $39.44

DCF Stock Value: $43.79 @ default 6.5% FCF growth

Graham Stock Value: $30 - $60 depending on pipeline

Competitor and Peer Comparison: $32

GSK DCF Valuation

Home Depot (HD) ValuationHome improvement retailer.

• Struggled with the housing bust

• Low growth

• Slowed down opening new stores dramatically if you lookat capex further

• Plenty of FCF

• Average CROIC, FCF/Sales, Revenue growth, earninggrowth

Intrinsic Value EstimateCurrent Price: $27.03

DCF Stock Value: $27.23 @ default 5% FCF growth

Graham Stock Value: $26.39

Competitor and Peer Comparison: $25

HD DCF valuation

Ingersoll-Rd Company (IR) ValuationOperates in four segments:

1. Air Conditioning Systems and Services

2. Climate Control Technologies

3. Industrial Technologies

4. Security Technologies

• Big increase in goodwill in 2008

Created using zinepal.com. Go online to create your own zines or read what others have already published. 6

• FCF positive yet erratic at times. Median of 11% FCFgrowth

• Excellent CROIC. Buffett sure does a good job of pickingeffective management at the helm

• Consistency in ROA and ROE when looking at multipletimeframes

• Revenue growth on the low side

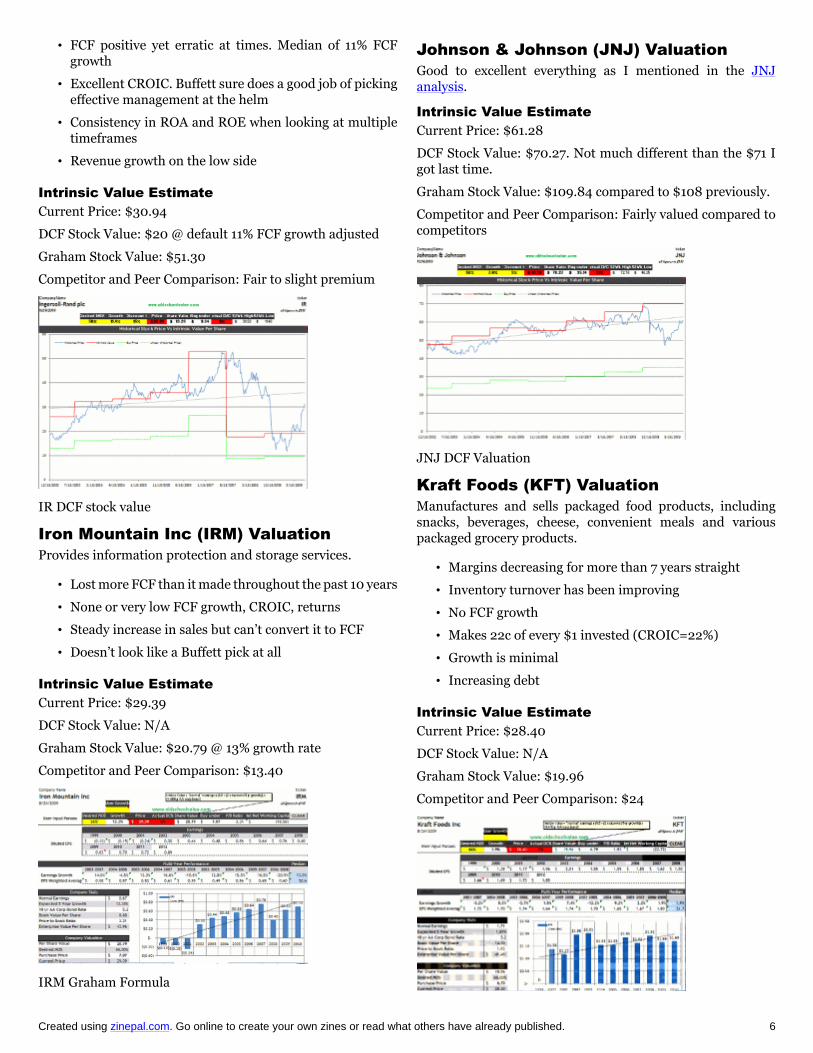

Intrinsic Value EstimateCurrent Price: $30.94

DCF Stock Value: $20 @ default 11% FCF growth adjusted

Graham Stock Value: $51.30

Competitor and Peer Comparison: Fair to slight premium

IR DCF stock value

Iron Mountain Inc (IRM) ValuationProvides information protection and storage services.

• Lost more FCF than it made throughout the past 10 years

• None or very low FCF growth, CROIC, returns

• Steady increase in sales but can’t convert it to FCF

• Doesn’t look like a Buffett pick at all

Intrinsic Value EstimateCurrent Price: $29.39

DCF Stock Value: N/A

Graham Stock Value: $20.79 @ 13% growth rate

Competitor and Peer Comparison: $13.40

IRM Graham Formula

Johnson & Johnson (JNJ) ValuationGood to excellent everything as I mentioned in the JNJanalysis.

Intrinsic Value EstimateCurrent Price: $61.28

DCF Stock Value: $70.27. Not much different than the $71 Igot last time.

Graham Stock Value: $109.84 compared to $108 previously.

Competitor and Peer Comparison: Fairly valued compared tocompetitors

JNJ DCF Valuation

Kraft Foods (KFT) ValuationManufactures and sells packaged food products, includingsnacks, beverages, cheese, convenient meals and variouspackaged grocery products.

• Margins decreasing for more than 7 years straight

• Inventory turnover has been improving

• No FCF growth

• Makes 22c of every $1 invested (CROIC=22%)

• Growth is minimal

• Increasing debt

Intrinsic Value EstimateCurrent Price: $28.40

DCF Stock Value: N/A

Graham Stock Value: $19.96

Competitor and Peer Comparison: $24

Created using zinepal.com. Go online to create your own zines or read what others have already published. 7

Lowe’s (LOW) ValuationAnother home improvement retailer.

Buffett hasn’t backed down from buying the number 1 and2 company in an industry. He doesn’t believe that youshould only buy one company from an industry for portfoliodiversification purposes.

• Better growth opportunity that Home Depot

• Good FCF growth but CROIC is very low at 2%. Betterthan nothing but not effective with utilizing capital.

• Good revenue and earnings growth

• Gross margins increasing to date

• Debt down to average levels

• Tangible book value increasing

• ROE and ROA declining past 2 years

• Sales flat since 2007

• The macro idea that people will continue to repair andimprove houses still doesn’t work well in a recession.

• If I had to choose LOW or HD, I would go for LOW. Orbe like Buffett and get both.

Intrinsic Value EstimateCurrent Price: $20.72

DCF Stock Value: $18.91

Graham Stock Value: $52.66

Competitor and Peer Comparison: $22

Warren Buffett Stock Picks:Part 3By Jae Jun on August 31st, 2009

Warren Buffett Stocks: Part 1 | Part 2 | Part 3 | Part 4

We are now up to the second half of valuing the holdingsof Berkshire Hathaway via the DCF valuation method, BenGraham formula as outlined in the Intelligent Investor, and asimple multiples valuation based on PE, cash flow, sales andother metrics compared to the competition and industry.

Of the 10 companies I go through in this post, I’ll be passingon Moody’s, M&T Bank, Sun Trusts Banks and Torchmark asI do not know how to value financial stocks.

Warren Buffett Stock Holdings : 21-30• M&T Bank Corporation (MTB) - outside circle of

competence

• Moody’s (MCO) - - outside circle of competence

• NRG Energy (NRG)

• Nalco Holding (NLC)

• Nike (NKE)

• Norfolk Southern Corp (NSC)

• Procter & Gamble (PG)

• Sanofi Aventis (SNY)

• Sun Trusts Banks Inc. (STI) - outside circle ofcompetence

• Torchmark Corp (TMK) - outside circle of competence

NRG Energy (NRG)Wholesale power generation company. Owns more than 189active operating generation units at 48 power generationplants.

• Had a big year in 2008

• Big margins increase in 2008 and since 2005

• Increase in short term and long term debt

• Company is able to make money but its returns are onthe low side.

• Mean ROA and CROIC of 2.7% and 5% respectively.Lower than competition

• FCF isn’t consistent.

• Huge increase in capex in 2008

• Large amount of taxes deferred.

• Still converts 12% of sales into FCF

Intrinsic Value EstimateCurrent Price: $27.76

DCF Stock Value: $37.11

Graham Stock Value: $34

Competitor and Peer Comparison: $58

Nalco Holding (NLC)Provider of integrated water treatment applications to preventcorrosion, contamination and the buildup of harmful deposits.

• Needs to improve efficiency. 40+% margins but negativenet income or low single digits at best isn’t good

• Decrease in intangibles suggests bad acquisitions andmistakes by management

• Long term debt is steady

• Been buying back stock

• FCF isn’t reliable. Lots of cash come from “other” income

Created using zinepal.com. Go online to create your own zines or read what others have already published. 8

• Low returns, cash and earnings growth

• Doesn’t look like something Buffett would buy

Intrinsic Value EstimateNumbers aren’t reliable enough for a proper valuation.

Current Price: $17.52

DCF Stock Value: N/A

Graham Stock Value: N/A

Competitor and Peer Comparison: $22

Nike (NKE)Sells athletic footwear, apparel and sports products.

• Great company, leader, innovator, huge moat

• Drop in margins in 2008 but increased inventoryturnover

• Low debt with plenty of cash

• Can pay off debt with FCF easily

• Don’t have to go in detail with numbers. They are justtoo good.

Intrinsic Value EstimateStability and predictability makes it easy to value.

Current Price: $56.18

DCF Stock Value: $65

Graham Stock Value: $77

Competitor and Peer Comparison: fairly valued at $56 (tradesat a premium to competition)

NKE Intrinsic Value Graph

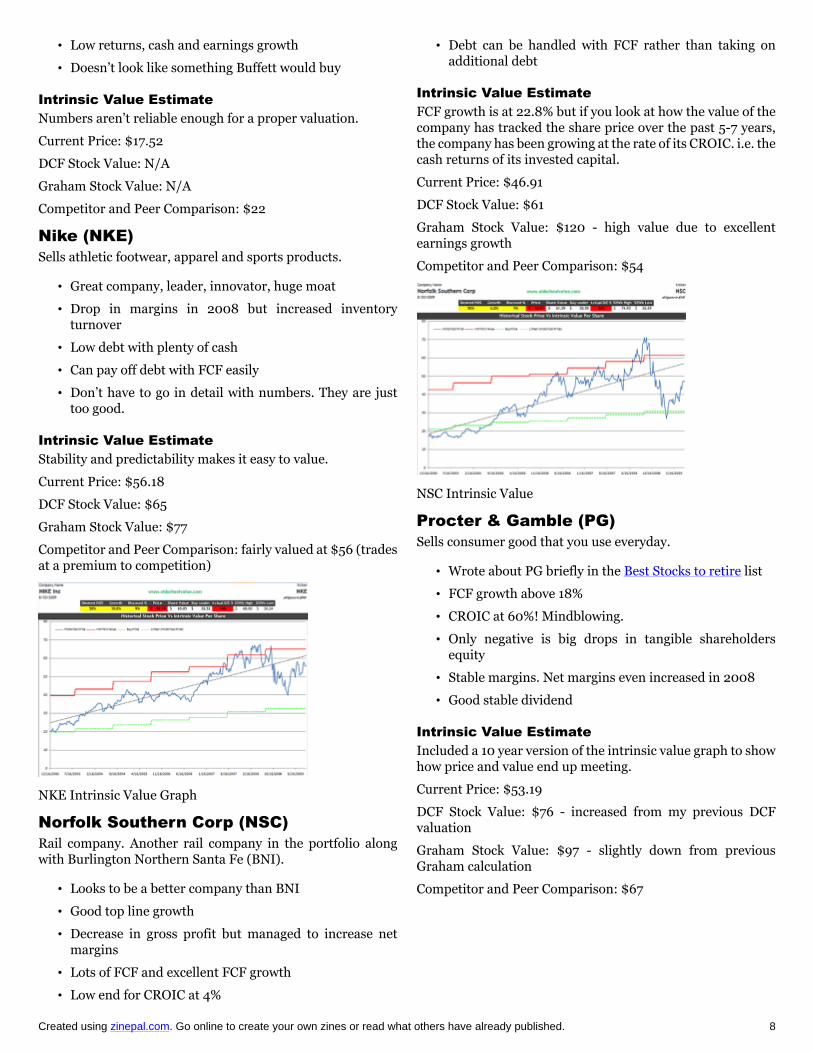

Norfolk Southern Corp (NSC)Rail company. Another rail company in the portfolio alongwith Burlington Northern Santa Fe (BNI).

• Looks to be a better company than BNI

• Good top line growth

• Decrease in gross profit but managed to increase netmargins

• Lots of FCF and excellent FCF growth

• Low end for CROIC at 4%

• Debt can be handled with FCF rather than taking onadditional debt

Intrinsic Value EstimateFCF growth is at 22.8% but if you look at how the value of thecompany has tracked the share price over the past 5-7 years,the company has been growing at the rate of its CROIC. i.e. thecash returns of its invested capital.

Current Price: $46.91

DCF Stock Value: $61

Graham Stock Value: $120 - high value due to excellentearnings growth

Competitor and Peer Comparison: $54

NSC Intrinsic Value

Procter & Gamble (PG)Sells consumer good that you use everyday.

• Wrote about PG briefly in the Best Stocks to retire list

• FCF growth above 18%

• CROIC at 60%! Mindblowing.

• Only negative is big drops in tangible shareholdersequity

• Stable margins. Net margins even increased in 2008

• Good stable dividend

Intrinsic Value EstimateIncluded a 10 year version of the intrinsic value graph to showhow price and value end up meeting.

Current Price: $53.19

DCF Stock Value: $76 - increased from my previous DCFvaluation

Graham Stock Value: $97 - slightly down from previousGraham calculation

Competitor and Peer Comparison: $67

Created using zinepal.com. Go online to create your own zines or read what others have already published. 9

PG Intrinsic Value

Sanofi Aventis (SNY)Pharmaceutical company.

• Stats look good but some metrics are quite erratic

• FCF growth is up and down

• Top line isn’t so consistent

• FCF and earnings growth is relatively low

• Has outstanding returns and converts it to plenty of FCF

• Debt is not an issue

• Maybe MRK or PFE would be better?

Intrinsic Value EstimateNot quite sure about what future products the company hasbut from the current snapshot of the company, I get thefollowing figures.

Current Price: $34.53

DCF Stock Value: $47

Graham Stock Value: $18

Competitor and Peer Comparison: $36

Warren Buffett Stock Picks:Part 4By Jae Jun on September 10th, 2009

Warren Buffett Stocks: Part 1 | Part 2 | Part 3 | Part 4

Up till now, I’ve taken a look at the holdings of Buffett, valuedeach one according to my methods based on free cash flowand DCF valuation, Benjamin Graham’s formula and a simplemultiples method.

In this final section of Buffett’s 2009 stock picks, I’ll gothrough what I know, pass on the usual financials i.e.US Bancorp, Wells Fargo and Wesco Financial, and thensummarize all 41 picks and their valuations again.

Regarding Wesco, I remember vaguely reading in Munger’sbook, Poor Charlie’s Almanack, that he doesn’t expect muchappreciation in the stock. So if Munger says that about his owncompany, then that’s enough for me to believe him and moveon to better value stock opportunities.

Warren Buffett’s Stock Picks: 31-41• U.S. Bancorp (USB) - Outside circle of competence

• USG Corporation (USG)

• Union Pacific Corp (UNP)

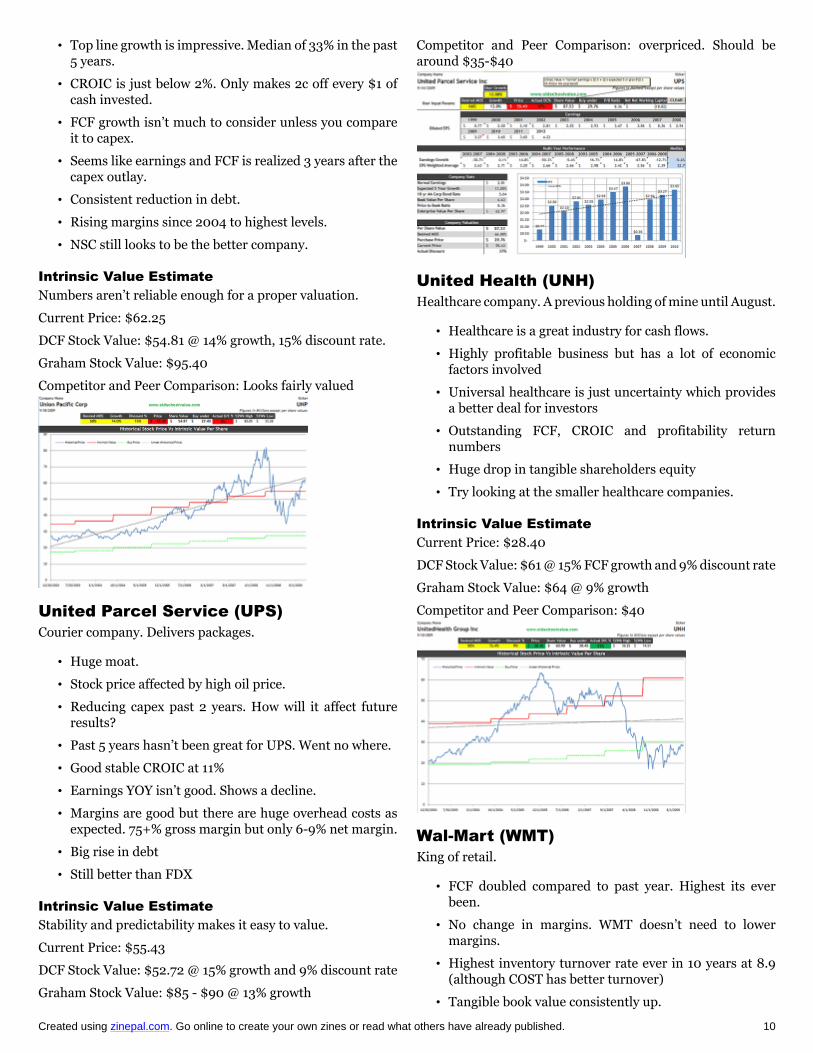

• United Parcel Service (UPS)

• United Health (UNH)

• Wabco Holdings (WBC) - Not enough data

• Wal-Mart (WMT)

• Washington Post (WPO)

• Wells Fargo (WFC) - Outside circle of competence

• Wellpoint (WLP)

• Wesco Financial Corp (WSC) - Outside circle ofcompetence

USG Corporation (USG)Makes and sells building materials.

• Rose with the housing market. Dropped with the housingmarket.

• The capex numbers show in hindsight how USG had highcapex at the peak of the housing bubble.

• Been losing a lot of cold hard cash in the process - FCF

• Tiny gross profits from good revenue

• Turnover back down to 10.9 compared to 12.2 from theprevious year

• Even if I ignore 2008 numbers and imagine looking atthe company in 2006 or 2007, numbers still aren’t great.

Intrinsic Value EstimateCurrent Price: $14.70 No reliable data or numbers to calculateintrinsic value. Only thing I can say with certainty is that thetangible book value is at $14.14. Throw it on the pass pile.

Union Pacific Corp (UNP)Another rail company. Buffett sure likes his train sets.

• Good tangible book value growth. Shows that growth isorganic.

Created using zinepal.com. Go online to create your own zines or read what others have already published. 10

• Top line growth is impressive. Median of 33% in the past5 years.

• CROIC is just below 2%. Only makes 2c off every $1 ofcash invested.

• FCF growth isn’t much to consider unless you compareit to capex.

• Seems like earnings and FCF is realized 3 years after thecapex outlay.

• Consistent reduction in debt.

• Rising margins since 2004 to highest levels.

• NSC still looks to be the better company.

Intrinsic Value EstimateNumbers aren’t reliable enough for a proper valuation.

Current Price: $62.25

DCF Stock Value: $54.81 @ 14% growth, 15% discount rate.

Graham Stock Value: $95.40

Competitor and Peer Comparison: Looks fairly valued

United Parcel Service (UPS)Courier company. Delivers packages.

• Huge moat.

• Stock price affected by high oil price.

• Reducing capex past 2 years. How will it affect futureresults?

• Past 5 years hasn’t been great for UPS. Went no where.

• Good stable CROIC at 11%

• Earnings YOY isn’t good. Shows a decline.

• Margins are good but there are huge overhead costs asexpected. 75+% gross margin but only 6-9% net margin.

• Big rise in debt

• Still better than FDX

Intrinsic Value EstimateStability and predictability makes it easy to value.

Current Price: $55.43

DCF Stock Value: $52.72 @ 15% growth and 9% discount rate

Graham Stock Value: $85 - $90 @ 13% growth

Competitor and Peer Comparison: overpriced. Should bearound $35-$40

United Health (UNH)Healthcare company. A previous holding of mine until August.

• Healthcare is a great industry for cash flows.

• Highly profitable business but has a lot of economicfactors involved

• Universal healthcare is just uncertainty which providesa better deal for investors

• Outstanding FCF, CROIC and profitability returnnumbers

• Huge drop in tangible shareholders equity

• Try looking at the smaller healthcare companies.

Intrinsic Value EstimateCurrent Price: $28.40

DCF Stock Value: $61 @ 15% FCF growth and 9% discount rate

Graham Stock Value: $64 @ 9% growth

Competitor and Peer Comparison: $40

Wal-Mart (WMT)King of retail.

• FCF doubled compared to past year. Highest its everbeen.

• No change in margins. WMT doesn’t need to lowermargins.

• Highest inventory turnover rate ever in 10 years at 8.9(although COST has better turnover)

• Tangible book value consistently up.

Created using zinepal.com. Go online to create your own zines or read what others have already published. 11

• Good top line and bottom line growth.

• Rock solid.

Intrinsic Value EstimateCurrent Price: $51.11

DCF Stock Value: $57 @ 13% growth and 9% discount rate

Graham Stock Value: $70 @ 9% EPS growth

Competitor and Peer Comparison: $60

Washington Post (WPO)Newspaper, media company.

• Media has been one of the worst industries in the pastyear. Especially with everyone believing that newspaperswill become extinct.

• Fiscal 2008 saw a big decline in everything. Sales, profit,cash, book value, ROE, ROA

• Management still used its cash effectively with a CROICof 12.2%

• FCF positive with stable capex.

• Capital expenditures have been steady for 4-5 years now.

• Tells me that most of the current $280mil in capex is dueto maintenance rather than growth.

Intrinsic Value EstimateNot very certain about the growth of the print business so I’llkeep things conservative. Current Price: $435.45 DCF StockValue: Normalized FCF back to a reasonable $200 million asthis is what the company has been able to achieve for the past10 years.

• $293 @ 0% growth and 9% discount rate

• $358 @ 5% growth and 9% discount rate

Graham Stock Value:

• $240 @ 0% growth

• $492 @ 5% growth

Competitor and Peer Comparison: N/A Industry andcompetitors have all fared horribly to be able to provide anyreliable valuation. Seems like GCI is the better pick in termsof value.

Wellpoint (WLP)Healthcare company.

• Again, Buffett likes to buy in pairs.

• Much like UNH. Great cash flow, great numbers.

• By the numbers, I prefer UNH.

• Dependent on macro factors.

Intrinsic Value EstimateCurrent Price: $52.84

DCF Stock Value: $86.91 @ 13% growth and 9% discount rate

Graham Stock Value: $118 @ 10% EPS growth

Competitor and Peer Comparison: $64-$70

Warren Buffett’s Stock Portfolio AnalysisYou view all comments and intrinsic value estimates of all 41stocks in the pdf below.

Warren Buffett Stock Portfolio Analysis and Valuation

DisclosureNo positions in any stock mentioned