voices on reporting...• on 3 january 2018, the companies (amendment) act, 2017 (amendment act,...

TRANSCRIPT

Voices on Reporting

5 July 2018

—

KPMG.com/in

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 2

Welcome

01 Series of knowledge sharing calls

03 Scheduled towards the end of each month

02 Covering current and emerging reporting issues

04 Look out for our Accounting and Auditing Update, IFRS Notes and First Notes publications

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 3

Speaker for the call

AssuranceKPMG in India

Ruchi RastogiPartner

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 4

Agenda

1.Notification of sections of the Companies (Amendment) Act, 2017 and related rules under the Companies Act, 2013

2. Amendments to SEBI Listing Regulations pursuant to Kotak Committee recommendations

3. Ind AS Transition Facilitation Group (ITFG) clarification - Bulletin 15

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 5

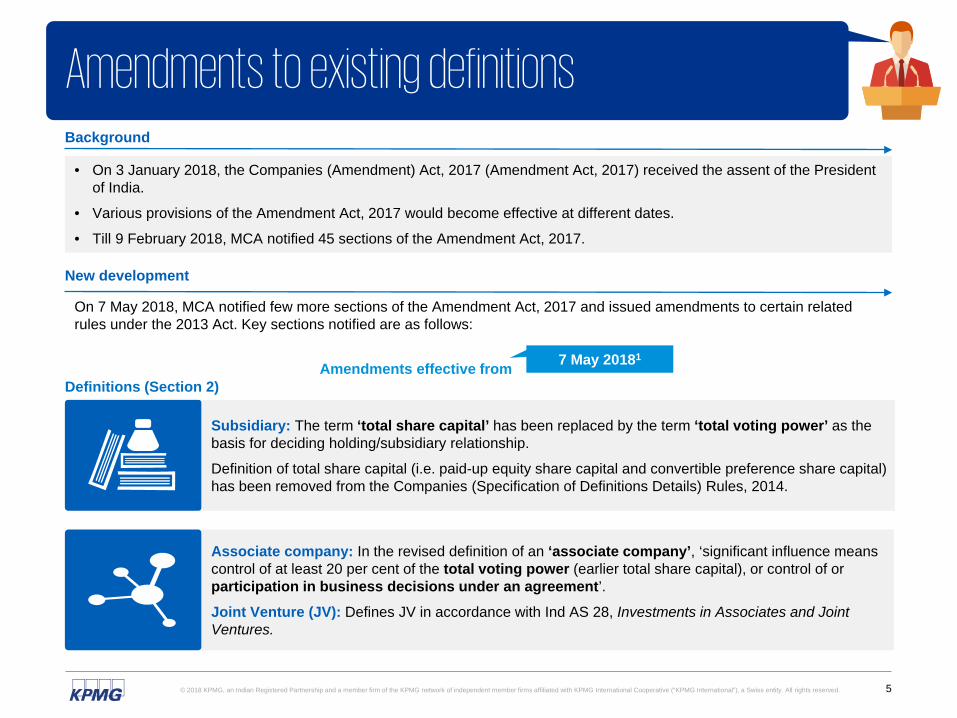

Amendments to existing definitions

Subsidiary: The term ‘total share capital’ has been replaced by the term ‘total voting power’ as the basis for deciding holding/subsidiary relationship.

Definition of total share capital (i.e. paid-up equity share capital and convertible preference share capital) has been removed from the Companies (Specification of Definitions Details) Rules, 2014.

Associate company: In the revised definition of an ‘associate company’, ‘significant influence means control of at least 20 per cent of the total voting power (earlier total share capital), or control of or participation in business decisions under an agreement’.Joint Venture (JV): Defines JV in accordance with Ind AS 28, Investments in Associates and Joint Ventures.

Definitions (Section 2)Amendments effective from 7 May 20181

Background

• On 3 January 2018, the Companies (Amendment) Act, 2017 (Amendment Act, 2017) received the assent of the President of India.

• Various provisions of the Amendment Act, 2017 would become effective at different dates.

• Till 9 February 2018, MCA notified 45 sections of the Amendment Act, 2017.

New development

On 7 May 2018, MCA notified few more sections of the Amendment Act, 2017 and issued amendments to certain related rules under the 2013 Act. Key sections notified are as follows:

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 6

Appointment and qualification of directors

Independent Director (ID) (Section 149)

• Pecuniary relationship does not include:– Remuneration received by an ID

– Any amount from a transaction which does not exceed 10 per cent of an ID’s total income (or such amount as may be prescribed).

• Scope of restriction on a ‘pecuniary relationship or a transaction’ entered by a relative has been made more specific by clearly categorising the types of transactions.

For example, when a relative holds any security/interest in the company, is indebted to the company, etc.

• If a relative of an ID who was an employee during preceding three FYs, then appointment of an ID would not be restricted.

Disqualification of a director (Section 164 and 167)

• In case a person has been appointed as a director of a company in default*, then: – Newly appointed director would not incur the disqualification for a period of six months from

the date of his/her appointment.• In case a director gets disqualified*, then:

– Office of the director would become vacant in all the companies other than the company which is in default.

*Not filed financial statements/annual returns or failed to repay deposits.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 7

Meetings of board and its powers

• The Board of Directors (BoD) of every listed public company and such other class or classes of companies, as may be prescribed should constitute an AC.

• Current requirement to pre-approve all RPTs subject to the approval of the BoD or shareholders as required by Section 188 would continue.

Additionally, AC could give recommendations to the BoD for transactions that are not covered under Section 188, in case it does not approve the transaction.

• A transaction (involving an amount up to INR1 crore) is voidable at the option of the AC if it has been entered without its approval and has not been ratified subsequently by it.

• RPTs between a holding company and its wholly-owned subsidiary that do not require board’s approval under Section 188, would not require approval of the AC.

Audit Committee (AC) (Section 177)

Nomination and Remuneration Committee (NRC) (Section 178)

• The BoD of every listed public company and such other class or classes of companies as may be prescribed, should constitute NRC.

• NRC is required to specify the methodology for the effective evaluation of the performance of the:

– Individual directors– Committees of the board and – BoD.

Such evaluation should be carried out by the board, by the NRC or by an independent external agency. NRC should review its implementation and compliance.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 8

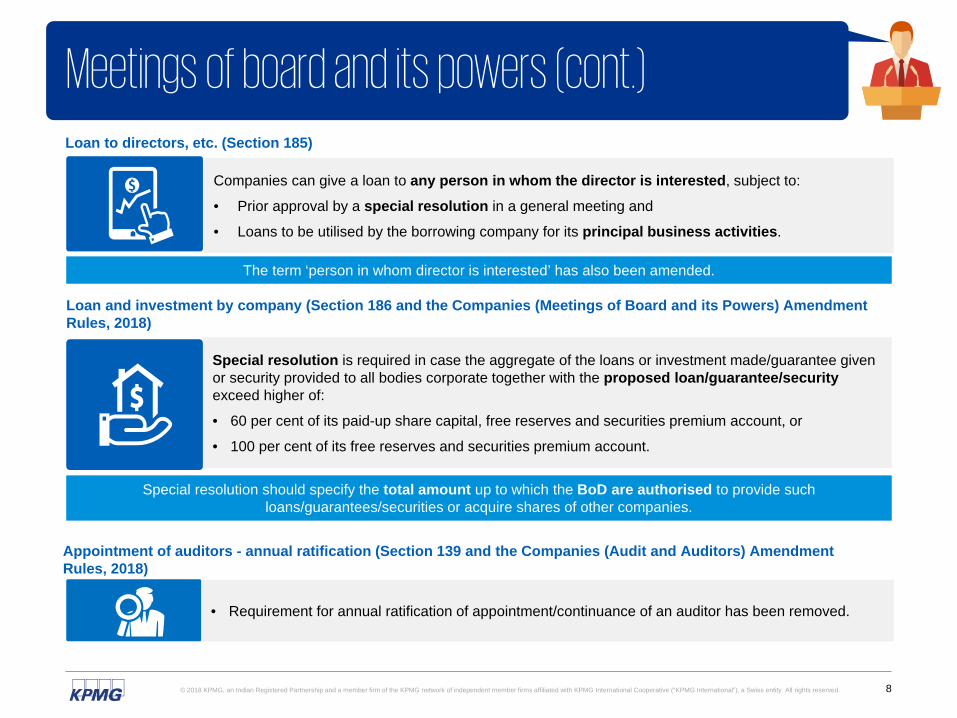

Meetings of board and its powers (cont.)

Companies can give a loan to any person in whom the director is interested, subject to:

• Prior approval by a special resolution in a general meeting and

• Loans to be utilised by the borrowing company for its principal business activities.

Loan to directors, etc. (Section 185)

Loan and investment by company (Section 186 and the Companies (Meetings of Board and its Powers) Amendment Rules, 2018)

The term ‘person in whom director is interested’ has also been amended.

Special resolution is required in case the aggregate of the loans or investment made/guarantee given or security provided to all bodies corporate together with the proposed loan/guarantee/security exceed higher of:

• 60 per cent of its paid-up share capital, free reserves and securities premium account, or

• 100 per cent of its free reserves and securities premium account.

Special resolution should specify the total amount up to which the BoD are authorised to provide such loans/guarantees/securities or acquire shares of other companies.

• Requirement for annual ratification of appointment/continuance of an auditor has been removed.

Appointment of auditors - annual ratification (Section 139 and the Companies (Audit and Auditors) Amendment Rules, 2018)

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 9

Agenda

1.Notification of sections of the Companies (Amendment) Act, 2017 and related rules under the Companies Act, 2013

2.Amendments to SEBI Listing Regulations pursuant to Kotak Committee recommendations

3. Ind AS Transition Facilitation Group (ITFG) clarification - Bulletin 15

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 10

Broad categories of amendments

Monitoring group entities and related parties

Accounting and audit-related matters

Board Committees

Composition and role of the board of

directors

Institution of independent directors

Investor participation

Strong foundation of monitoring and enforcement mechanism

Disclosures and transparency

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 11

Amendments applicable from 10 May 20183

Amendments applicable with immediate effect

Searchable formats of disclosures

• Disclosures on entity’s website: In a user friendly searchable format

• Disclosures to stock exchange: In XBRL format.

Amendments applicable from 9 May 20182

Additional disclosures on board evaluation

• Observations of board evaluation carried out for the year

• Previous year’s observations and actions taken• Proposed actions based on current year observations.

Additional disclosure in the management discussion and analysis section of the annual report

• Entity’s medium-term and long-term strategy based on a time frame as determined by its BoD.

Mandatory

Recommendatory

• Dedicated group governance unit or Governance Committee comprising the members of its BoD

• Strong and effective group governance policy to be formulated.

Mechanisms to monitor multiple unlisted subsidiaries

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 12

Amendments applicable from 1 April 20192

• Mandatory disclosure of consolidated financial results on a quarterly basis

• Limited review/audit of at least 80 per cent of the financial information of the group i.e. consolidated revenue, assets and profits

• Mandatory disclosure of cash flow statement on a half-yearly basis

• Financial results in respect of last quarter could be audited/limited reviewed

• Disclose by way of note, aggregate effect of material adjustments made in the results of the last quarter pertaining to earlier periods.

Accounting and audit related matters

Quarterly financial disclosures

Other significant matters

• Mandatory quantification of audit qualifications, however, an exception has been provided for matters like going concern or sub-judice matters

• Statutory auditor of the listed entity should undertake a limited review of the financial results of all the entities/companies whose accounts are to be consolidated with the listed entity.

Mandatory

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 13

Agenda

1.Notification of sections of the Companies (Amendment) Act, 2017 and related rules under the Companies Act, 2013

2. Amendments to SEBI Listing Regulations pursuant to Kotak Committee recommendations

3. Ind AS Transition Facilitation Group (ITFG) clarification - Bulletin 15

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 14

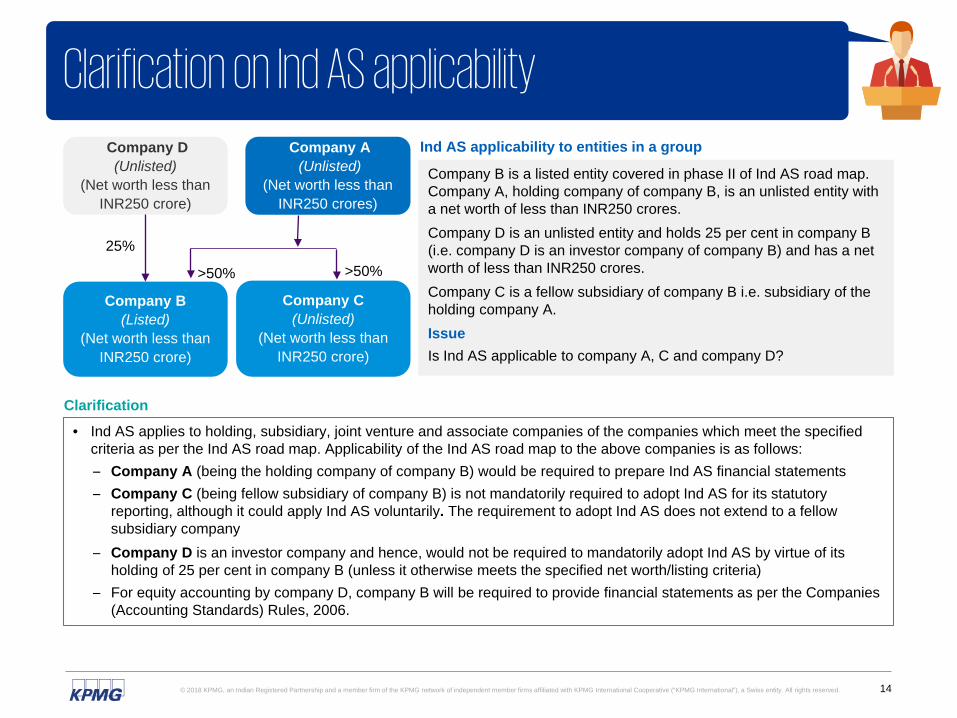

Clarification on Ind AS applicability

Clarification

Company B is a listed entity covered in phase II of Ind AS road map. Company A, holding company of company B, is an unlisted entity with a net worth of less than INR250 crores.Company D is an unlisted entity and holds 25 per cent in company B (i.e. company D is an investor company of company B) and has a net worth of less than INR250 crores. Company C is a fellow subsidiary of company B i.e. subsidiary of the holding company A.IssueIs Ind AS applicable to company A, C and company D?

Company A(Unlisted)

(Net worth less than INR250 crores)

Company B(Listed)

(Net worth less than INR250 crore)

Company C(Unlisted)

(Net worth less than INR250 crore)

Company D(Unlisted)

(Net worth less than INR250 crore)

Ind AS applicability to entities in a group

• Ind AS applies to holding, subsidiary, joint venture and associate companies of the companies which meet the specified criteria as per the Ind AS road map. Applicability of the Ind AS road map to the above companies is as follows:– Company A (being the holding company of company B) would be required to prepare Ind AS financial statements– Company C (being fellow subsidiary of company B) is not mandatorily required to adopt Ind AS for its statutory

reporting, although it could apply Ind AS voluntarily. The requirement to adopt Ind AS does not extend to a fellow subsidiary company

– Company D is an investor company and hence, would not be required to mandatorily adopt Ind AS by virtue of its holding of 25 per cent in company B (unless it otherwise meets the specified net worth/listing criteria)

– For equity accounting by company D, company B will be required to provide financial statements as per the Companies (Accounting Standards) Rules, 2006.

25%

>50% >50%

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 15

Clarifications on financial instruments

MNO Ltd. has an incentive receivable in the form of sales tax refundable from the government, under a scheme of the government on complying with certain stipulated conditions.

There is no formal one-to-one contractual agreement between the government and the company.

Issue

Would such incentives fall under the definition of financial instruments under Ind AS 109, Financial Instruments?

Clarification

• A financial instrument arises as a result of contractual obligation between the parties as per Ind AS 109.• As per Ind AS 32, Financial Instruments: Presentation, a contract need not be in writing and can take various forms.

• In India, although there may not be a one-to-one agreement between the entity and the government with respect to a government incentive scheme, but there is an understanding that on complying the stipulated conditions attached to the scheme, the entity would be granted benefits of the scheme.

• If the entity has complied with the conditions attached to the scheme, then such an incentive (receivable) would meet the definition of a financial instrument and would be accounted for as a financial asset as per Ind AS 109.

Incentive receivable from the government

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 16

Clarifications on financial instruments (cont.)

Can interest free refundable security deposits (such as rent deposits paid to lessor, etc.) given by an entity be required to be discounted as per the principles of Ind AS? If yes, at what rate should these be discounted?

Clarification

• A refundable security deposit is a financial instrument and is classified as a financial asset as per Ind AS 109.

• A financial asset at initial recognition is measured at fair value.

• Where the effect of time value of money is material, refundable security deposits should be discounted and should be shown at their present value at the time of their initial recognition.

• The rate of discounting need to be evaluated based on facts and circumstances taking into account the guidance as per Ind AS 109.

• Deposits which are contractually repayable on demand would be recognised at the transaction price on initial recognition similar to the initial recognition of demand deposit liabilities.

Interest free refundable security deposits

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 17

Application of Ind AS to past business combinations of entities under common control

• Company X is a wholly-owned subsidiary of company Y. Promoters hold 49.95 per cent in company Y as on 31 March 2015.

• Company Y merges with company X on 1 April 2015 and amalgamation was in the nature of purchase as per AS 14, Accounting for Amalgamations.

• Company X is required to adopt Ind AS from FY2017-18. Company X has not opted for the exemption under Ind AS 101, First-time Adoption of Indian Accounting Standards, of not applying Ind AS 103, Business Combinations retrospectively to past business combinations.

Issue

Whether on the transition date, company X is required to apply requirements of Appendix C to Ind AS 103, Business combinations of entities under common control?

Clarification• In this case, assuming that the companies are under common control before and after the amalgamation and company X

has not taken a business combination exemption (for not restating past business combinations), therefore, company X would be required to apply the requirements of Appendix C to Ind AS 103 retrospectively.

Q&A

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 19

Sources

1. MCA notification no. S.O. 1833(E) dated 7 May 2018

2. SEBI notification no. SEBI/LAD-NRO/GN/2018/10 dated 9 May 2018

3. SEBI circular no. SEBI/HO/CFD/CMD/CIR/P/2018/79 dated 10 May 2018

4. ICAI-ITFG clarification bulletin dated 5 April 2018.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20

Glossary

• 2013 Act - The Companies Act, 2013

• Ind AS - Indian Accounting Standards

• SEBI - The Securities and Exchange Board of India

• MCA - The Ministry of Corporate Affairs

• ICAI - The Institute of Chartered Accountants of India

• ITFG - Ind AS Transition Facilitation Group

• BoD - Board of Directors

• RPTs - Related Party Transactions

• AC - Audit Committee

• NRC - Nomination and Remuneration Committee

• ID - Independent Director

• JV - Joint Venture

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 21

Links to previous recordings of VOR

Month Topics LinkMarch 2018(special session) • Ind AS 115 - Sector series 1 Click here

April 2018

• Ind AS 115, Revenue from Contracts with Customers• New/revised Standards on Auditing (SAs)• SEBI accepts some recommendations of the committee report on corporate

governance• Other regulatory updates

Click here

April 2018(special session) • Ind AS 115 - Sector series 2 Click here

May 2018(special session) • Integrated Reporting Click here

May 2018(special session) • SEBI implements Kotak Committee recommendations Click here

June 2018(special session) • ICDS implementation issues Click here

June 2018(special session) • Ind AS implementation for NBFCs Click here

For other archives of VOR calls, visit www.KPMG.com/in

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 22

Coming up next

Our Publications

New issue of:• Accounting and Auditing Update • First Notes• IFRS Notes

Accounting and Auditing Update First Notes

Download from www.kpmg.com/in

IFRS Notes

Thank youKPMG in India contact:

Feedback/queries can be sent to: [email protected]

Ruchi RastogiPartnerAssuranceE-mail: [email protected]

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2018 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

This document is for e-communications only.

kpmg.com/socialmedia