videsh sanchar nigam limited: growth opportunities for the ... · 1 videsh sanchar nigam limited:...

TRANSCRIPT

1

Videsh Sanchar Nigam Limited: Growth Opportunities for the FutureI

This case presents the situation faced by N. Srinath (Director Operations) who finds himself in the

unenviable position of trying to steer an erstwhile public sector monopoly unit to acquire a new culture,

develop business processes and systems, evolve new businesses and models, integrate a new acquisition, and

achieve profitability in the face of loss of monopoly status and declining profits and share price. An

international acquisition opportunity for VSNL is posing a strategic dilemma for Srinath about whether to

pursue growth despite poor current performance, or consolidate first? Readers are expected to develop

recommendations for shaping the strategy of VSNL.

The top management team of Tata – one of the oldest Indian business conglomerates, acquired Videsh Sanchar Nigam Ltd (VSNL) and was reviewing the performance of the company in June 2005, ahead of the annual Analyst Meet. Until three years ago, VSNL was a Government of India (GoI) owned monopoly incumbent International Long Distance (ILD) service provider with the usual monopoly inheritance of high tariffs and indifferent customer service. The monopoly in Internet Services until 1998 and ILD Services until 2002 had ensured that VSNL was a highly profitable enterprise. This had been a driver for the Tatas to acquire VSNL. With WTO imposed stipulations, VSNL had lost its monopoly, first over the Internet business and then in ILD. The emergence of private players and consequent decrease in tariffs affected the business of VSNL. Revenues declined by more than 52 per cent over a span of three years, 2001-02 to 2004-05 (Exhibits 1a-d for financial data). The share price too had dropped within this period.

For N. Srinath, Director (Operations), the biggest concern was why VSNL had not been as successful as he had envisaged? Had VSNL managed to create synergies with other existing telecom entities within the Tata group? Had the Tata Group made a mistake with the VSNL acquisition? He also had to reverse the downward trend in VSNL’s business. VSNL had recently made some ambitious moves into international markets, including the acquisition of Tyco Global Network (TGN) announced in November 2004. Another international acquisition opportunity, Teleglobe International, was currently on the radar, and it was now time to take a decision on that acquisition. Should they proceed with the Teleglobe acquisition and spend more money with an eye on international growth or should they try to consolidate their position in the existing business areas and investments first? Global ILD Business In the decade of 1995-2005, the global ILD business had witnessed an exponential rise in international call volume from 109.8 billion minutes in 1999 to 258.4 billion minutes in 2005, i.e. a

I Prepared by Rekha Jain and Abhishek Mishra. Research support provided by Pratibha Tripathi and Nishil Bali is gratefully acknowledged. Teaching material of the Indian Institute of Management Ahmedabad is prepared as a basis for class discussion. Cases are not designed to present illustrations of either correct or incorrect handling of administrative problems. Copyright © 2010 by the Indian Institute of Management Ahmedabad.

2

CAGR of 13.4 per cent between 2001-2005 (Exhibit 2). The rise had been propelled by regulatory and technological changes, which had transformed a market dominated by monopoly national carriers into a highly competitive market. After the opening of the ILD sector in several countries in 1990’s, the number of licensed international carriers grew to 4,000 in 2002 from just 600 in 1997. The world's largest ILD carriers included AT&T, MCI WorldCom, Sprint, Deutsche Telekom, France Telecom, Teleglobe and iBasis. The market share of new carriers increased largely at the cost of incumbent monopoly operators. The reason for the decline in the share of incumbent operators was fuelled by a combination of falling call prices, regulatory intervention, and declining margins in the voice business. Market

3

The global revenues from international voice business declined marginally even though there had been extensive growth of voice traffic during 1999-2005 (Exhibit 3). This was due to afall in the average calling price, which outpaced traffic growth. The consequences were disastrous for many long distance carriers. For example, while AT&T’s outgoing traffic from the U.S. grew 28 per cent between 2002 and 2004, revenues from this traffic plunged from Rs 240.5 billion to Rs 144.5 billion during this period. Technology Changes in technology had transformed the ILD business in a substantive way. Most players moved towards digital mode of transmission via optic-fiber and terrestrial cables to increase bandwidth. In addition, reducing optic-fiber capacity prices lowered the cost of transporting a call. For example, the average U.S. carrier call termination cost went down from Rs 34.59 per minute in 1991 to Rs 6.56 per minute in 2001. Similarly, Voice over Internet Protocol (VoIPII) traffic began to have an appreciable impact on international call volumes since 19991 (Exhibit 4 shows growth in VoIP volumes between 2002 and2004). Most VoIP traffic was carried by iBasis and Internet Telephony Exchange Carrier (ITXC). Another significant chunk was contributed by traditional Public Switched Telephone Network (PSTN) operators who had migrated to VoIP.

New technology such as DWDMIII (that allowed multiplication in capacity using optical signals) revolutionized fiber optics in the 1990s. Consequently, the number of undersea cable systems grew over the years, particularly in intra-Asia-Pacific and trans-Pacific regions. Between 1998 and 2000, new submarine cables increased trans-Pacific bandwidth from nearly 14 Gbps to 244 Gbps. The submarine cable market, which was led by AT&T, British Telecom and Verizon was flooded with a number of cables like Columbus-3, Yellow/Atlantic Crossing-2 (AC-2), TAT-14, Apollo etc (Exhibit 5).

International telecom services also made extensive use of satellite technology. International Telecommunications Satellite Organization (INTELSAT- the world’s first ever satellite launched in1967) and the International Maritime Satellite OrganizationIV (INMARSAT – founded in 1979), were two satellite consortia established by national telecommunications administrations for the purpose of owning and operating satellite communication systems. When INTELSAT began to accumulate losses because of management failures and the increasing market share of fiber-optic cables, this intergovernmental satellite consortium was privatized. Iridium, Globalstar and ICO (ICO Global Communications (Holdings) Limited) were private satellite systems.

II VoIP networks convert the voice or data that is being transmitted into ‘packets’ by breaking the communication stream into smaller units and embedding these with origin and destination addresses. Packets allow for better utilization of the transmission channel, as these can be multiplexed, unlike a normal voice transmission (circuit switched) in which the entire channel is reserved for the communication. Another advantage is that the VoIP network can be used for transmitting multimedia and data content. III DWDM refers to Dense Wavelength Division Multiplexing. Wavelength-division multiplexing (WDM) is a technology which multiplexes multiple optical carrier signals on a single optical fiber by using different wavelengths (colors) of laser light to carry different signals. This allows for a multiplication in capacity, in addition to enabling bidirectional communications over one strand of fiber. http://en.wikipedia.org/wiki/Wavelength-division_multiplexing (10: 50 a.m. April 5, 2010). IV INMARSAT was later named International Mobile Satellite Organisation.

4

New Services Players like Global Crossing, Interoute, Level 3, Telia, and TyCom that initially supplied only wholesale bandwidth started moving to new services due to over-saturation in the infrastructure market. These services included collocation (renting of physical space on a service provider's premises), IP transit (sale of wholesale Internet bandwidth to Internet service providers and content providers on a per megabit per second per month basis), ‘Last Mile’ facilities (the final leg of delivering connectivity from a communications provider to a customer), and content distribution(a system of computers containing copies of data, placed at various points in a network to maximize bandwidth for access to the data from clients throughout the network). This move marked their transition to a total solution provider from an infrastructure provider only. Pricing The global ILD business also changed as a consequence of regulatory changes in accounting rates. (The prices and charges for international calls governed by international accounting rate system consisted of three main components. The collection rate, which was the rate charged by an operator to its customers. The accounting rate was the rate agreed between the originating country and the destination country and the settlement rate, which was the proportion of the accounting rate that determines the actual payment between countries. Under arrangement made between operators of two countries for traffic between them, operators at each end negotiated a multiplication factor known as an accounting rate. The accounting rate was calculated using net traffic flowing between them in a given period, say a quarter, and multiplied this by half of the accounting rate, a factor known as the settlement rate. Exhibit 6 gives a pictorial representation of how ILD revenues were shared among operators2). Falling prices of telecommunication services lowered settlement rates for countries that received more calls. The imbalance between inbound and outbound calls increased over the years due to which the net settlement payments grew larger. In an effort to drive settlement rates closer to the cost of the call (which was falling in domestic markets), and to address the need of international carriers from paying inappropriately high rates to foreign companies, the Federal Communication Commission (FCC) - the U.S. telecommunication regulator, came out with a benchmark policy to reduce above-cost settlement rates paid by U.S. carriers to foreign carriers for termination of their international traffic. As a result, U.S. carriers’ per minute settlement outpayment in 2000 was almost 50 per cent less than that in 1997. Plummeting international bandwidth costs and decreases in both settlement rates and interconnection charges enabled many carriers to send traffic at lower costs. Telecom Regulation in India

A paradigm shift in GoI policy took place in early 1990’s when telecommunications sector was opened to private sector. Apart from privatizing basic telephone services, the National Telecom Policy (NTP-1994) introduced a number of value added services through private operators, such as cellular mobile telephones, radio paging, e-mail, Internet, etc. Within the NTP-1994 framework, two cellular operators (both private) and two fixed line operators (one being the government

5

incumbent) were introduced in each circleVwith an option of Department of Telecom (DoT) becoming the third cellular operator. In 1997, the Telecommunications Regulatory Authority of India (TRAI) was established by GoI to regulate the telecommunications sector. New Telecom Policy (NTP-1999)

The growth of the telecom sector took off when NTP-1999 was implemented, which allowed existing private cellular and fixed-line operators to migrate from a very high fixed annual license-fee to a one-time entry fee plus revenue sharing. This expectedly led to improvement in project viability for most basic and cellular service projects in which operators had earlier bid very high license fees. However, in return for this concession, the GoI removed restrictions on the number of companies operating in a service area or on the number of licenses that could be awarded to a bidder across different geographical areas. This attracted MNC’s, Indian conglomerates and other entrants. In August 2000, NLD was opened for private sector followed by the ILD market, which deregulated the NLD, ILD and Internet telephony sectors. On 1st October 2000, DoT - the erstwhile incumbent in national and local telecom space (other than Mahanagar Telephone Nigam Limited (MTNL), which was the telephone services provider in Delhi and Mumbai) was corporatized and became Bharat Sanchar Nigam Limited (BSNL). Both BSNL and MTNL were given the third cellular license in 2001. Subsequently, a fourth cellular operator was introduced in 2001. Fixed line operators were allowed to provide Wireless-in-Local-Loop (WLL3) services, which was later modified to WLL-limited mobility as license holders were permitted to offer limited mobility, usually within the boundaries of a town. Internet Telephony and its Deregulation

From 1stApril,2002, GoI permitted Internet Service Providers (ISPs) to offer restricted Internet Telephony services, i.e. primarily for international outbound calls. As of 31st March 2004, DoT had permitted 121 ISPs to provide Internet Telephony services and 43 of them started operations by March 2005. Though Internet Telephony accounted for a small portion of total revenue for ISP’s (0.5 per cent in 2002), its share in total ILD segment was likely to grow as it allowed for a more efficient, lower-cost means of transmitting voice, data and video on a single, converged network. After opening up of VoIP, foreign players such as AT&T, BT, Cable and Wireless, PCCW (a leading communication provider from Hong Kong), Sprint, and WorldCom entered the market with newer technologies. Among the Indian ISPs, BSNL and MTNL shared a major portion of the total ISP market. De-monopolization and Compensation

In order to accelerate its commitments to WTO, GoI brought forward termination of VSNL’s ILD monopoly from 2004 to 2002. To offset the likely loss, GoI announced a compensation package. It consisted of grant of an NLD license with waiver of entry fee and license fee for a period of 5 years commencing from 1st April 2001, net of taxes. A Category ‘A’ (all India) ISP license was also given as a part of this package. GoI agreed to provide additional compensation, if found necessary based

V Circle refers to an administrative boundary usually co-terminus with a state boundary and is categorized as A, B or C depending on its estimated revenue potential

6

on a detailed review in the future. Later, in January 2002, after providing an assurance of ILD traffic from BSNL and MTNL, GoI unilaterally wrote to VSNL stating that the above dispensation was granted as the full and final settlement of every claim against advancing the ILD de-monopolization of VSNL by two years4. Unified Access Service License (UASL)

In 2003, GoI introduced Unified Access Service License (UASL), which permitted migration of basic and WLL (LM) to full mobility (state level), enabling players to participate in telecom access services in a single circle with a single authorization using any technology. Some companies opted to migrate to full mobility; e.g. Reliance Infocom and Tata Teleservices Limited (TTSL) that earlier had WLL (LM) licenses opted for UASL. Bharti Televentures and some other cellular operators also opted for UASL as they saw flexibility in service provision at no additional cost. The Indian telecommunication network with over 110 million connections as of 31st March 2005 became the fifth largest in the world and the second largest among the emerging economies of Asia5. The total subscriber base, which was grew at nearly 20 percent in year 2002-03, had jumped to an average growth rate of more than 40 per cent in year 2003-04. Tele-density improved from under 4 percent as of 31st March 2001 to 11.32 per cent as of 31st March 2005, against a targeted tele-density of 15 percent by 2010 (as envisaged in NTP-1999). The growth of Indian telecom sector was cellular driven and accelerated by GoI’s policies, and the contribution of both public and private sector telecom firms. Broadband

7

The Internet subscriber base increased from 3.0 million as of 31st March 2001 to 5.3 million as of 31st March 2005. This was after GoI allowed provisioning of Internet services by private operators and the opening of the international gateway market. Revenue from Internet services also grew by 41 per cent to touch Rs 15,730 million by 31st March 2005 over a span of four years (Exhibit 7 (a & b)). The growth in Internet subscribers in India, however, had been slower in comparison to growth in mobiles (only 1.3 million internet subscribers6 were added in 2004-05 compared to the 52.2 million mobile subscribers in the same year), largely due to limited PC penetration and the inability of service providers to supply good quality connectivity at most locations (Exhibit 8). Unlike in several other countries, GoI had chosen not to do local loop unbundling (LLU); therefore the existing telephony (copper) network could only be used by BSNL/MTNL for providing DSLVI broadband services. Private operators that wanted to provide broadband services had to rollout their own fixed-line or wireless networks. Broadband growth could be accelerated due to developments in broadband wireless technologies as well as the recent focus of some service providers on bundled services. The bundled services package included wireless, broadband Internet connectivity, VoIP telephone service, commercial network monitoring and custom video, as well as other traditional ISP services. The Players

VSNL was the GoI owned incumbent international telecom service provider, while BSNL and MTNL were GoI owned incumbent fixed line operators. BSNL was also the incumbent national long distance operator and had recently obtained an ILD license. As a consequence of the liberalized regime of NTP-1999 and the move towards UASL, a number of private players emerged in all segments - mobile, NLD and ILD. A comparative account of their services, market share in terms of revenue and subscribers shows that this sector witnessed growth in all segments after deregulation (see Exhibit 9a for details of revenue contributed by different segments of Indian Telecom Sector and percent market share of different players over the years; Exhibit 9b gives additional details on important players in the industry).

The three types of players in telecom services were7: • State owned companies (BSNL and MTNL). • Private Indian owned companies (Reliance, Tata Teleservices). • Companies with varying amounts of foreign investment (Hutchison-Essar, Bharti Tele-

Ventures, Escotel, Idea Cellular, BPL Mobile, Spice Communications). Context and Approaches to Growth The unprecedented growth of wireless services followed the realization among telecom companies that to grow and prosper, they must expand at the bottom i.e. make phones more affordable. Mobile phones, for instance, fast moved from a class service to mass service driven by

VI Digital Subscriber Line - a family of technologies that provides digital data transmission over a local telephone

network

8

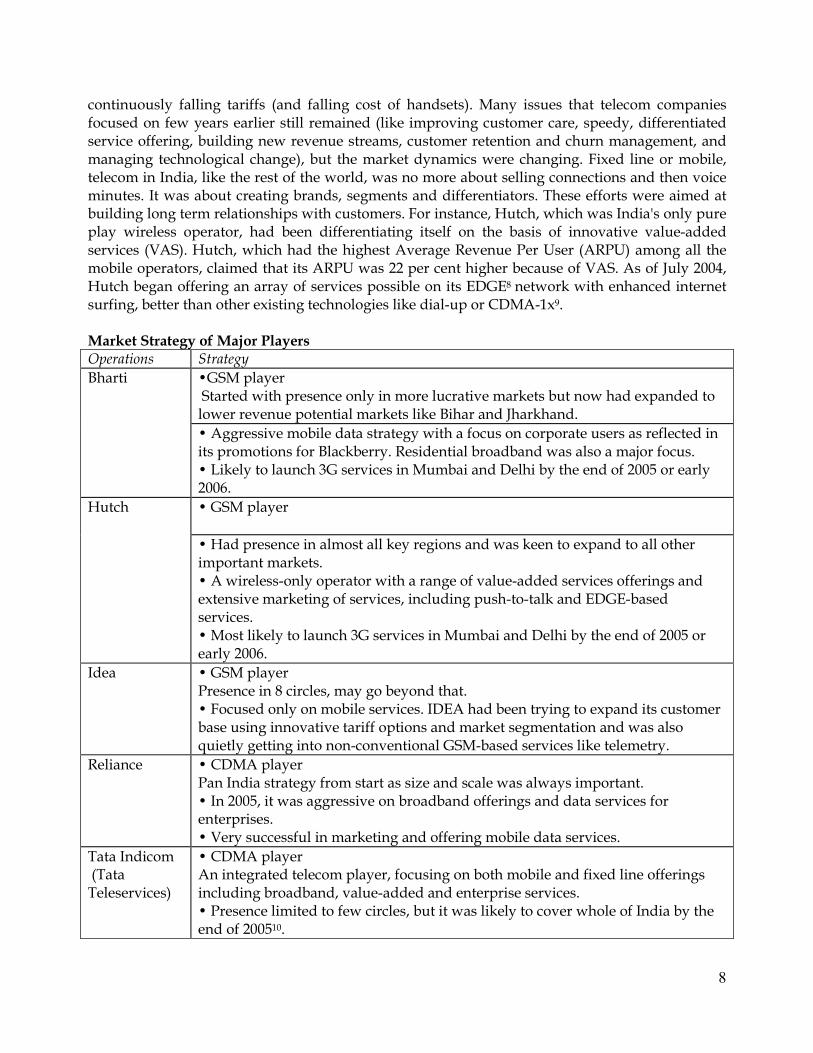

continuously falling tariffs (and falling cost of handsets). Many issues that telecom companies focused on few years earlier still remained (like improving customer care, speedy, differentiated service offering, building new revenue streams, customer retention and churn management, and managing technological change), but the market dynamics were changing. Fixed line or mobile, telecom in India, like the rest of the world, was no more about selling connections and then voice minutes. It was about creating brands, segments and differentiators. These efforts were aimed at building long term relationships with customers. For instance, Hutch, which was India's only pure play wireless operator, had been differentiating itself on the basis of innovative value-added services (VAS). Hutch, which had the highest Average Revenue Per User (ARPU) among all the mobile operators, claimed that its ARPU was 22 per cent higher because of VAS. As of July 2004, Hutch began offering an array of services possible on its EDGE8 network with enhanced internet surfing, better than other existing technologies like dial-up or CDMA-1x9. Market Strategy of Major Players Operations Strategy

Bharti •GSM player Started with presence only in more lucrative markets but now had expanded to lower revenue potential markets like Bihar and Jharkhand.

• Aggressive mobile data strategy with a focus on corporate users as reflected in its promotions for Blackberry. Residential broadband was also a major focus. • Likely to launch 3G services in Mumbai and Delhi by the end of 2005 or early 2006.

Hutch • GSM player

• Had presence in almost all key regions and was keen to expand to all other important markets. • A wireless-only operator with a range of value-added services offerings and extensive marketing of services, including push-to-talk and EDGE-based services. • Most likely to launch 3G services in Mumbai and Delhi by the end of 2005 or early 2006.

Idea • GSM player Presence in 8 circles, may go beyond that. • Focused only on mobile services. IDEA had been trying to expand its customer base using innovative tariff options and market segmentation and was also quietly getting into non-conventional GSM-based services like telemetry.

Reliance • CDMA player Pan India strategy from start as size and scale was always important. • In 2005, it was aggressive on broadband offerings and data services for enterprises. • Very successful in marketing and offering mobile data services.

Tata Indicom (Tata Teleservices)

• CDMA player An integrated telecom player, focusing on both mobile and fixed line offerings including broadband, value-added and enterprise services. • Presence limited to few circles, but it was likely to cover whole of India by the end of 200510.

9

BSNL • Largely GSM player

• Largest telecom operator both in terms of subscribers and revenues (as of March 2005).

• Low-profile marketing strategy partly owing to inherent limitations of being a government-owned organization. • Had ambitious plans for coming years. The company appeared to have global ambitions as well, and could soon seriously consider acquiring businesses abroad11.

Videsh Sanchar Nigam Limited (VSNL)

On 1st April 1986, VSNL, a GoI owned corporation with a monopoly on international telecommunications, was created as the successor to Overseas Communications Service(s)12 (OCS). In initial years, VSNL’s core business was providing international switched telecom service (telephones, telex, telegraph, and bureau fax) to approximately 237 territories worldwide. It had access to both national and global markets. VSNL pioneered the Internet in India in 1996. In addition, it also offered data and value added services that included International Leased Lines (ILL), INMARSAT (a constellation of geo-stationary satellites designed to extend phone, fax and data communications all over the world), International Private Leased Circuits (IPLC) access, Electronic Data Interchange, Managed Data Network Services (MDNS), Television/Video Uplinking, Program Transmission Services, Frame Relay Services and e-mail Services. Having been a government organization, VSNL was an equity holder in INTELSAT (5.42 per cent) and INMARSAT (2.02 per cent). It had ownership interests and access to capacity in undersea cables interconnecting the South Asia region, as well as those linking the region with Europe, North America and Asia/Pacific (Exhibit 10). VSNL also had ownership interests in various undersea cables that did not land in India, but provided connections between various locations. In 1997, VSNL became the first Indian public sector undertaking to issue Global Depository Receipts (GDRs) when it issued 37.80 million GDRs. In 1999, when many of the Indian companies stayed away from accessing international capital markets, VSNL made a successful second GDR issue (20 million GDRs) by way of divestment by the government. VSNL made the debut in the US capital market by listing its American Depository Receipts (ADRs) on New York Stock Exchange on 15 August 2000. The ADR was listed on NYSE at $11 indicating a premium of 40 per cent over domestic price13. VSNL and Tata’s Other Telecom Undertakings On 13th February 2002, VSNL ceased to be a public sector undertaking when GoI, which owned 52.9 per cent of VSNL’s equity, divested14 a 25 per cent stake to the Tata Group as a strategic partner along with the right to manage VSNL. The Tata group was a leading player in several industries and businesses in India, notably steel, information technology services, commercial vehicles, tea, salt, watches, hotels, etc15. Tata Group’s telecom foray began as Tata Cellular Limited in the Andhra Pradesh circle under the cellular license. Tata Cellular merged with Birla AT&T Limited to create a three-way joint venture

10

between the Birlas, Tatas and AT&T, called Birla Tata AT&T Limited, since renamed as Idea Cellular in 2004 (refer Exhibit 9b for equity ownership and details about IDEA). Tata Teleservices Ltd. (TTSL) was another Tata venture, initially in a partnership with Bell Canada that acquired the Basic Services license in Andhra Pradesh in 1997 and offered services under the Tata Indicom brand name. Subsequent to amendments in basic services, and licensing and migration to UASL, TTSL obtained licenses in Delhi, Gujarat, Karnataka and Tamil Nadu. TTSL also acquired controlling stake in Hughes Tele.net, a Basic Services operator in Maharashtra (including Mumbai and Goa) circle. Hughes Tele was subsequently renamed as Tata Teleservices (Maharashtra) Limited (TTML). Later, by divesting stake in the Andhra Pradesh circle, Tata became a CDMA player in all its service areas. The logic behind Tata Group’s investment in VSNL was driven by the latter’s monopoly leadership position in the ILD sector as well as its strong, debt-free balance sheet. There was also the additional attraction of assured traffic from BSNL and MTNL, which had the largest base of subscribers and outgoing ILD traffic. As mentioned before, in January 2002, as part of the compensation package, the GoI had directed MTNL and BSNL to route their ILD calls for a period of two years through VSNL at market rates. Later, in the same month, GoI sent another letter to VSNL stating that the above dispensation was granted as the full and final settlement of every claim against advancing the ILD de-monopolization of VSNL by two years. The TTSL Controversy In 2002 the VSNL board under Tata management decided to invest Rs 12,000 million from VSNL to TTSL. The Tata’s justified the decision as being part of the effort to extend VSNL’s activities to the basic services customer. The investment was to be made over 3-4 years for a 20-26 per cent stake in TTSL. TTSL was planning projects worth Rs 82,470 million over the next four years with equity amounting to Rs 43,250 million. Out of this, the Tata group had to invest Rs 25,520 million, VSNL was to put in Rs 12,000 million and Rs 5,730 million were to come in from non-Tata sources. The Union Communications Minister objected to the decision as VSNL was a GoI company and in his opinion, could not justify putting “public money” in any private firm. The criticism was also because VSNL was to acquire a 25 per cent stake in TTSL whereas the Tatas had gained 25 per cent equity share in VSNL by investing an amount only marginally higher than 12,000 million, which practically meant that the valuation of VSNL was similar to that of Tata Teleservices, a much smaller company and still in its formative stages16. After some deliberations between the Ministry and VSNL, the VSNL board set-up a committee to decide the quantum and valuation of the proposed investment. The committee decided to go ahead with the investment but with equal participation of all shareholders. While sources in the DoT saw this to be a provision for the sub-committee to identify more attractive investment opportunities for VSNL other than TTSL, sources in the Tata group indicated that this clause pertained to additional investment opportunities that meant that the initial proposal of investing in TTSL would remain unaltered.

11

VSNL’s ILD Business In 2001, the ILD business of India amounted to 16.6% of the total revenue arising from telecom services. It contributed to 90 per cent of VSNL’s revenue. In 2000-01, VSNL carried 2.6 billion minutes of international traffic, which was less than 2% of the global traffic of 156.2 billion minutes. According to VSNL's Ninth plan (April 1997 to March 2002), it aimed to invest Rs 50 billion, which would be funded through cash flows from operations and through its share of the net proceeds of the Global Depository Receipts (GDRs) offering, which were issued in March 1997 and had raised Rs19.6 billion17. During the period of VSNL’s monopoly, VSNL and BSNL/MTNL shared the revenues generated from subscribers in India for outgoing international calls as well as the revenues from settlement payments on incoming international calls terminating on the domestic network. VSNL did not have any direct relationships with the customers; it dealt with BSNL and MTNL on the Indian end and international carriers on the foreign end. A major chunk of its revenues went to the carriers, mainly BSNL as interconnect costs. Though the total ILD minutes from India were increasing, there was an imbalance in the ratio of inbound calls to outbound calls. The ratio of inbound calls to outbound calls in India was 4:1 in 2001. The reason being that India's outgoing call rates to most other countries were higher in terms of relative costs. The lower purchasing power of India versus those in other countries aggravated the imbalance between the countries to which it predominantly connected (U.S., Europe and Gulf) so that inbound calls were more than outbound calls. Therefore, VSNL was the recipient of net settlement payments (nearly 13 per cent of ILD revenue). But after the FCC benchmark policy of 1997, there was a continuous fall in accounting rate and settlement payment. For example, the accounting rate of U.S. carriers with VSNL came down from Rs 12.50/minute in 2001 to Rs 8.50/minute in 2002. As a result, overall revenues began to decline despite a strong rise in international call volumes (Exhibit 11). Over the years TRAI also reduced ILD tariff rebalancing exercise. For example, a call from India to the US in 2005 was Rs 12.00 per minute whereas in 2002 it cost Rs 49.20 per minute. The progressive fall in tariffs led to a squeeze on margins during 2002-03 - a decline of 6% over the previous financial year. Competition in the ILD Sector The policy framework for ILD license provided for a fixed one-time entry fee of Rs 250 million and a performance bank guarantee of Rs 250 million, which would be released as soon as rollout obligations were met. In addition, ILD service providers were required to pay an annual license fee including Universal Service Obligation (USO) levy, which was 15 per cent of the Adjusted Gross Revenue (AGR). Three new Indian telecom sector players: Data Access, Bharti Telesonic, and Reliance Infocom entered the market in July 2002. BSNL also obtained an ILD license, but operated its (limited) services through an infrastructure sharing arrangement with VSNL. With prices falling, ILD service providers started offering high capacity bandwidth like DS3 (also called T3 - a high capacity circuit), data services and launched international operations. Data Access, a joint venture between Spa Enterprises, India and PCCW, Hong Kong was very aggressive in cutting ILD rates; a lot of its traffic was through VoIP18.

12

Bharti became the first private company to own an undersea cable in India. The 3,200 km i2i cable network gave Bharti an opportunity to sidestep its dependency on foreign firms and VSNL for bandwidth. Bharti also announced an investment of Rs 1,751 million in the SEA-ME-WE-4 cable consortium along with VSNL, a project that was to be completed by the end of 200519. Reliance Infocom installed Points of Presence (PoPs) in New York and Los Angeles and secured international connectivity using undersea cable bandwidth of FLAG, a 65,000 km global submarine cable network that it acquired in late 2003. Thus, the market shares of the four ILD players during the period 2002-05 underwent a significant change (Exhibit 12). Market Demand A study by iLocus20 on VoIP in India highlighted that VoIP could account for up to 61 per cent of ILD traffic by year 2007 (Exhibit 13). Many ISPs were moving towards Asynchronous Transfer Mode (ATM) switches, which were not only low-cost but would also provide fully-integrated digital networks and allowed better transmission of voice and broadband data traffic. To reduce inter and intra-office communication costs, provisioning of newer flexible connectivity media like Virtual Private Networks (VPN) came into focus for all players. IDC India expected the Indian VPN services and equipment market to grow to Rs 12.7 billion in 2005 from Rs 1.6 billion in 2001.

Performance of VSNL

VSNL faced falling market share in its core business of ILD, decreasing profits, and increasing competition. VSNL not only had to deal with concerns arising from its transformation from a government-owned company to a private enterprise, but also needed to devise a strategy to grapple with the changing market scenario. The divestment process, which caused a lot of euphoria and high expectations about VSNL did not translate into financial results (Exhibits 1a-d). Change in Business Proposition To compete and survive in the changed market scenario, VSNL felt that it needed to diversify its offerings. The Director of Finance elaborated on this need, “If you look at any incumbent that was privatized, either in the U.S. or Europe, they usually had a combination of the access business and the long distance business. As the long distance businesses became more competitive and the overall value came to shrink, most of them moved into mobile. So mobile became the growth vehicle for all the incumbent telecoms over a period of time.” VSNL could not start mobile services because of the GoI’s rule that any company with a holding of 10 per cent in another company in the same circle could not get a mobile license. Because both the major shareholders of VSNL, Tata’s and GoI, had other mobile ventures (TTSL and BSNL, respectively), VSNL could not get a mobile license. Therefore, it launched other new services such as NLD competing with established players like Bharti Tele Ventures, Reliance and BSNL. In-house Restructuring After acquisition, VSNL needed a drastic restructuring in terms of business, financing, and human resource as market conditions were changing rapidly and top management felt that the existing

13

organisational structure would not allow VSNL to respond optimally. It had the technical knowledge but not the commercial skills. VSNL needed to restructure and diversify at the same time while generating revenues and profits. The company decided to focus on the enterprise business and step-up domestic operations. A joint team from VSNL and the Tata Group was involved in restructuring parts of the business, especially personnel. Following the diversification strategy, initiatives on enterprise business, and tapping of domestic market had to be stepped up. According to N. Srinath, “Our initial objectives were to protect our market position in the ILD business, get the NLD business launched as soon as possible, and work on making the operations of the company more market/customer focused and efficient. Multiple task forces, focusing on business priorities, were set up to achieve these objectives. Over time the priorities changed and evolved as projects were completed21.” Extensive steps for cost cutting and profit enhancement were taken in every department. In sales and marketing, the company restructured both the headquarters and its regional organizations and established a centralized 24/7 call centre for enterprise data customers and two other call centers for retail and broadband customers. Under quality management, it implemented the Tata Business Excellence Model (TBEM) - a framework for practicing business excellence pioneered by the Tata group. In 2004, it became the first telecom service provider globally to achieve the TL 9000 (Quality Management System). VSNL introduced a continuous improvement system, trained a number of auditors in different quality systems and created VizNet, a real time CRM system to gather data on customer transactions. VSNL adopted a strong performance based culture and reduced the total number of employees from 3,148 to 1,786 through a Voluntary Retirement Scheme (VRS). Employees over 40 years of age or over 10 years service were eligible for VRS. Simultaneously, the company inducted over 500 full time employees plus over 1,000 people (on contract) to get a mix of employees of desired disciplines and levels. It conducted specialized sales training, and managerial and leadership programs at its Tata Management Training Center (TMTC) to improve skills of its employees. Low return assets were pruned to generate funds for investment in new offerings. Major savings were achieved in bandwidth charges by optimizing capacity utilization through re-grooming cables, surrendering excess bandwidth, closing costly microwave links and identifying lower-cost suppliers. Various assets, notably earth station equipment, were re-deployed for maximum utilization. The company sold its entire holding in INMARSAT for Rs 941 million and INTELSAT for Rs 5,000 million. Revenue Assurance processes that monitored the entire chain from the point of service provisioning right up to billing were established in 2003 to proactively prevent leakages. Market and Product Structure

VSNL diversified into three main areas: Physical capacity expansion, Enterprise services, and International business. It also intended to strengthen its position in the market for value added services, particularly data services, by offering services like VPN, Co-location, Managed Data Network Services (MDNS) based on Internet data centers, and application support services. It continued its emphasis on the international switched telecom services and other VAS – such as IPLC, Internet telephony, ILL, Internet dial-up access, e-mail services and the transmission of television signal. New products and services such as corporate Internet telephony, VoIP, and bandwidth on demand were introduced to serve the needs of corporate customers. VSNL

14

integrated its retail offerings under a single package that included Internet access, net telephony and email to its customers (Exhibit 14). Physical Capacity Building Although VSNL continued to have the largest market share of ILD revenues, its share was declining (46.6 per cent during 2004-05 compared to 67.4 per cent during 2003-04). During 2004, VSNL launched VoIP for incoming voice termination, and concluded traffic agreements with ten new international carriers that used this technology. During the year 2004-05, VSNL’s overseas PoPs in New York, Los Angeles and London became operational. In 2005, following negotiations with BSNL (after BSNL got an ILD license), VSNL started carrying the outgoing ILD traffic of BSNL under a wholesale carriage agreement at an agreed cost per minute of traffic handled (Rs 2.20 per minute to the UK, US and Canada22). The agreement was effective until 31st October 2005. VSNL also launched outbound calling cards in April 2004, accessed through a toll-free number. However, these cards could be used only from phones within the TTSL's network because other local service providers blocked calls from their network to the VSNL’s toll-free number. In February 2005, TRAI mandated VSNL to stop selling outbound calling cards as it was not permitted under its license. VSNL approached the Telecom Disputes Settlement and Appellate Tribunal (TDSAT) challenging the TRAI order23. NLD Services In September 2002, with a view to cover the NLD licensed area with a fiber optic backbone, VSNL committed to rollout its network by establishing PoPs in 322 Long Distance Charging Areas24 (LCDA) across the country in a phased manner. By January 2004, it established its PoPs in 109 cities using optical-fiber cable/satellite media. In April 2004, it signed a right to use agreement for 15 years with Bharti Infotel Limited for 23,000-route kilometers capacity on Bharti’s existing advanced fiber optic network in India. This agreement was for approximately Rs 5,000 million. After this, it had about 36,000 kms of NLD network running across the country. VSNL had revenue sharing agreements with many basic service and cellular mobile service operators and telecom public sector companies i.e. BSNL and MTNL to carry NLD traffic to and from their networks. By March 2005, NLD services accounted for a significant component of VSNL’s voice services, and volumes in this segment increased from 240 million minutes in 2003-04 to 1.5 billion minutes in 2004-05. The reduction in tariff by TRAI contributed to a substantial increase in call volumes. The revenue due to NLD services also witnessed a hike from Rs 60 million to Rs 2,301 million. Internet-related Services As a part of category ‘A’ license, VSNL extended Internet access to 22 cities and planned to extend it to more cities. Although GoI allowed private ISPs to set up their own gateways, over 90 of them (from nearly 183 ISPs 25) continued to choose VSNL’s gateway services. Keeping a particular focus on the corporate segment, VSNL provided new services: VPN, Voice-mail, numerous broadband applications and an enterprise communication system called ALICE, besides providing ILLs to 1,512 customers as of 31st March 2002. In December 2003, VSNL launched an enhanced integrated

15

retail Internet offering combining multiple services like Internet access, net telephony and value added services. In 2004 it launched Wi-Fi or Wireless Fidelity for Internet access at Bangalore. In March 2004, as a step towards strengthening and consolidating its presence in the Internet and broadband space, VSNL took over the narrowband and broadband businesses of Dishnet’s ISP division26 for a consideration of Rs 2.7 billion. Dishnet was a prominent dial-up and broadband services provider with customers across 38 cities and 200 towns in India. This acquisition gave VSNL access to a vast base of over 600 owned and franchised cybercafés of Dishnet. In June 2004, VSNL launched limited broadband services using metro Ethernet technology for data transfer at high speeds. Ethernet cabling provided end-users capacity of up to 10/100 Mbps (data speed of 10 MBPs for older computers and 100 MBPs for new ones), resulting in shorter access times for voice, video and Internet. Further, to boost its broadband strategy, it invested Rs 1,751 million in the SEA-ME-WE 4 cable. VSNL, in consortium with 11 other international telecommunication carriers, decided to invest in the cable project, which would connect 12 countries: Bangladesh, Egypt, France, India, Indonesia, Italy, Malaysia, Pakistan, Saudi Arabia, Singapore, Sri Lanka and the United Arab Emirates. The 20,000 km cable would be designed to have an 8.1 terabit capacity and would be built using the DWDM technology. VSNL intended to leverage its extensive VoIP infrastructure and ILD expertise to offer high quality Internet telephony as a complement to its ILD business. In March 2003, it commissioned VoIP equipment at Mumbai and Ernakulam to tap increasing market opportunities. It also planned to invest Rs 9.6 million to expand the advanced VoIP gateways to other places such as New Delhi and Jallandhar in 2003-04 and to have strategic tie-ups with global players for this segment. Corporate offerings would provide value-added customized solutions for companies that operated from multiple locations.

The Metropolitan Area Network (MAN) was the basic infrastructure required to offer broadband services. Since VSNL launched broadband services in India, it announced to roll out MAN in 10 major cities of India as of March 2005. It spent Rs 3.9 billion in 2002-03 on infrastructure including cables, NLD switches and its optical fiber link, and a data center at Vashi in Mumbai27.

VSNL also started commissioning Asynchronous Transfer Mode (ATM) network to integrate and allocate bandwidth for voice, data and broadband traffic. The initial investment in ATM expansion was Rs 360 million for the year 2002-03 and Rs 202 million for 2003-04. The ATM backbone of 155 to 620 Mbps would allow for the use of state-of-the-art multimedia applications for distance learning and other research activities. A number of universities and those connected to ERNET also intended to experiment with high-speed links to this ATM backbone28.

Enterprise Business

The enterprise data market (comprising services for corporate data transmission) was expected to grow at a range of 30-40 percent CAGR, while the corporate voice market was likely to grow at about 3-5 percent in revenue terms. (The lower growth in voice revenues was driven by the relatively inelastic demand of the corporate voice market, and because of sharply falling unit revenue29). Enterprise customers were increasingly looking for a single partner that could offer them both IT and telecom solutions30. Recognizing the high potential of this business, VSNL

16

started offering a range of data services across the country since 2002. It focused initially on the top 500 large enterprise customers and then set up a channel team to concentrate on the SME market. Investments in new services yielded results as reflected in the transformation of the revenue mix. VSNL planned to exploit existing synergies with other Tata group companies (such as Tata Consultancy Services) and was getting into managing integrated services such as hardware, software, networks and applications offering end-to-end solutions to its customers. Integrated service providers such as Reliance, Bharti, and BSNL were the main competitors for Tata’s in the Enterprise services segment. Sify and HECL had also begun offering partial services in the enterprise segment. Each of the major service providers had started to offer similar services such as end-to-end connectivity, bundled IP addresses, leased lines, wide choice of bandwidths, SLA based services, choice of interface (G.703, V.35 or Ethernet) and customized wireless solutions. The key issues that the enterprise services market faced are summarized below31: - Connectivity services as business proposition: Connectivity services were being looked at as a

business proposition and not merely as telecom pieces, prompting top management to be involved in these decisions. With more people getting involved, sales and negotiating cycles became longer. The increase in deal sizes and sales cycles, led corporates to become very choosy about their 'partners' as they wanted to opt for one who could deliver as per their requirement and not what the partners were carrying in their kitty. Corporate users were now looking at a lot of issues like fault management, business-continuity management, service-level management, and lifecycle management before finalizing their service provider.

- Competition to cooperation: With technologies, applications, and geographies increasing for

enterprise users, the complexity of the network was also increasing and there was a need for partners, system integrators, and managed service providers who could work along with service providers to see that all functions ran smoothly. The service provider had to pick up the contract, outsource bits and pieces, and see how efficiently it could be managed in terms of time and cost. Service providers would also have to focus on educating corporate customers on a regular basis on the new technology options in the market.

- Service level agreements (SLAs): With competition becoming aggressive, enterprise users were

looking for service providers who could provide SLAs with network uptime of nearly 100% and also provide redundancies. Enterprises were also looking at service providers for network and bandwidth optimization. Communications infrastructure in India was unreliable; therefore enterprise users opted for three levels of redundancies to ensure that their links remained stable. This increased network complexity as well as cost for enterprise users.

- Business intelligence: The financial reporting cycles for enterprises had shifted from monthly to

weekly to daily and now to online. Enterprises were looking at network management facilities that could offer all requisite tools so that optimization could happen at all levels and that could manage facilities remotely. Using network performance management tools and reports, enterprise users were also interested in knowing what kind of applications were creating problems, where the bandwidth was being choked and where was there a need for additional bandwidth.

17

- Shift from Time Division Multiplexing32 (TDM) to Internet Providers (IP): Enterprise users were opting for IP-based technologies as they provided flexibility and increased reliability. In majority of cases, it also led to lower total cost of ownership. So, the move was towards IP-EPABXVII, IP-VPNVIII, and MPLSIX based IP-VPN, IP-SANX, and VoIP solutions. On the IP front, enterprises moved from the pilot stage and were now looking more on the deployment aspect. But the real challenge was how to maintain legacy applications or services and migrate to new technologies at the same time.

- Security: With increased reliance on networks and increasing number of applications, security

became critical for enterprises. Security had to be implemented at different levels to make the environment secure. Some service providers were implementing security operating centers (SOC), which would be connected to the network operating center. This would help in remote security management of the network and provide security and management at the same time.

To further support the enterprise business, VSNL formed a specialized sales and marketing team in 2003 called the Tata Indicom Enterprise Business Unit (TIEBU) with TTSL, TTML and Tata Internet Services Limited. TIEBU provided specialized sales and marketing coverage to major Indian corporate accounts, offering integrated voice and data solutions under the Tata Indicom brand. TIEBU had a special focus on six industry verticals with specialized needs: IT, IT enabled services, media and entertainment, government services, industrial and distribution, and banking, financial Services and insurance (BFSI). In 2003-04, TIEBU achieved Rs 5,000 million from the booked incremental orders, which added revenue of Rs. 3,450 million to VSNL from enterprise segment33. TIEBU's Solutions team adopted TIEBU Telecom Consulting Methodology (TTCM), which involved small and large businesses at all levels.

For the future, TIEBU adopted a three-fold strategy to address the growing telecom data needs of industries. Firstly, it focused on added value by offering managed data and voice services, providing better value for their money. Secondly, with a view to meet the future bandwidth needs of these industries, the group committed itself to increasing the bandwidth availability in the country. Lastly, the group planned to offer customized telecom solutions for these industries to enable them to optimize the utilization of their telecom infrastructure.

Investments in New International Businesses

In the post-acquisition scenario, VSNL planned to expand its domestic and global business. (Exhibit 15 shows major projects in hand). It established VSNL International (VSNLI) in 2004 for governing the international operations. VSNLI focused on capitalizing its long-standing relationships with about 90 international carriers by offering them flexible solutions (see Exhibit 16 for VSNLI’s position in wholesale market and composition of its gross margin segment). During

VII Electronic Private Automatic Branch Exchange (EPABX) more commonly called just PBX (private branch

exchange). VIII

A Virtual private network (VPN) links two computers through an underlying local or wide-area network, while encapsulating the data and keeping it private. IX Multiprotocol Label Switching (MPLS) is a mechanism in high-performance telecommunications

networks, which directs and carries data from one network node to the next. X Storage area network (SAN) is an architecture to attach remote computer storage devices to servers in such a way that the devices appear as locally attached to the operating system.

18

2004-05, it implemented IP-based solutions for faster connectivity with overseas carriers, and improved its IP network by upgrading IP gateways to increase the number of carriers that could interconnect to VSNL. It also focused sharply on realizing old dues and recovered about Rs 1.2 billion in past debts from overseas carriers. The Director of Finance emphasized the need of expanding international business for future growth: “If you look at the way business was in 2001-02, we were at Rs 70,890 million, out of which ILD business contributed almost 90 per cent. Things have changed now. So the biggest challenge is how do you chop the capex and how do you clean up and bring more revenue. The enterprise business was growing, but there were major tariff pressures. Retail was slightly up from Rs 70-80 crore in the year 2002-03. Revenues were not coming from ILD and even from NLD business so we started looking for opportunities to go into international market. We tested our appetite for international business through a very small deal in the U.S. in 2003.” International Expansion / Operations In July 2003 VSNL took over assets and network of US-based Gemplex, a global provider of business-networking services, and IP-VPN services. Gemplex was a Virginia-based business networking service provider, which was founded in 2000. The acquisition of Gemplex would enable VSNL to offer voice and data services through the existing IP-VPN network. It planned to sell and service domestic and global clients over this network. “The IP-VPN market in India is still in a ‘nascent stage’, but will grow to touch around Rs 400 crore in the next three to four years” said N Srinath while announcing the acquisition34. VSNL began significant forays into the international markets. It formed a joint venture with regional partners in Nepal to form United Telecom Limited. It also began operations in the U.S. by establishing a subsidiary - VSNL America Inc. in 2003 and set-up VSNL Singapore Private Limited (VSPL) as headquarters for its international expansion. VSNL continued to explore further opportunities abroad in telecom markets that were deregulating and opening up. It had also recently formed VSNL UK Ltd., a subsidiary of VSNL America Inc., purchased as a shell company, to provide telecom and value added services to the UK and European markets. VSNL Hong Kong Ltd., a subsidiary of VSNL Singapore Pte. Ltd. was formed in July 2004 to provide telecom and value added services in that region 35 . A description of VSNL’s international initiatives and activities is presented in Exhibit 17.

Asset Build-up After acquisition, VSNL invested in a combination of submarine cables and microwave systems, which provided seamless, high quality connectivity and a strong platform in the field of international voice, data communications and value added services. In November 2003, VSNL began setting up a 3,100 km submarine cable system between Chennai and Singapore. VSNL completed the construction of this cable in September 2004, which became commercially operational in March 2005. The state-of-the-art system was VSNL’s first self-owned undersea cable with an estimated life of 25 years and an initial capacity of 320 Gbps that could ultimately be scaled up to 5.1 terabits/sec. On completion, this cable would extend VSNL’s bandwidth infrastructure significantly, and along with VSNL’s NLD backbone would enable it to offer service at reasonable tariff to customers in India and abroad36.

19

International Business Group (IBG)

To drive its geographical expansion, VSNL set up an International Business Group (IBG) on 1st April 2004, headquartered in Singapore. In view of promoting VSNL’s offerings, such as the new Tata Indicom Cable (TIC), to both enterprise and carrier customers who required connectivity to India, IBG would leverage the establishment of IP-based data and voice services in select countries. It would enable VSNL to provide extended relationship support to Indian and international enterprise customers. VSNL needed a major international pipeline to stay price competitive with vertically integrated rivals like Bharti and Reliance Infocom in the domestic market. After the construction of Tata Indicom Cable, VSNL felt the need to expand its global network. Tyco Global Network (TGN)

Tyco International Ltd. was a diversified business conglomerate involved in four core business segments: Electronics for telecommunications (undersea fiber optic systems), fire and security services, healthcare, and specialty products. In 2000, TyCom (Tyco’s 86 per cent owned telecommunications subsidiary) commenced Tyco Global Network (TGN), which was world’s largest, fastest and technologically advanced independent open-access undersea fiber optic telecommunications network, linking more than 80 per cent of the world’s population. It mainly consisted of Tyco Trans-Pacific, Tyco Trans-America, Tyco Trans-Atlantic, Tyco Western-Europe and Tyco Northern-Europe. It spanned more than 60,000 kms and connected 3 continents (Exhibit 18). Expecting high bandwidth demand, Tyco invested heavily in TGN - a Rs. 145 billion ($ 3.3 billion) project. Simultaneously, other rivals like 360network, Global Crossing and Level3 launched new submarine cables. The result was a glut of fiber optic capacity resulting in declining prices and reduced anticipated future cash flows. The glut at that particular time affected the build-out of TGN. In 2001, TGN had a 26.6 per cent decrease in revenue over 2000. The operating margins increased due to project completions, certain reduced accruals due to lower profitability levels, and various contractual settlements. 360networks was already in bankruptcy, and Global Crossing was weighed down by Rs 262.7 billion in debt and became profitless. In 2002, TGN recorded a loss of over Rs 131.3 billion, with an impairment charge of over one half of Rs 44 billion. In 2003, on completing the construction of TGN with an operating loss of Rs 5,035 million, Tyco started a divestiture and restructuring program. Tyco was facing continuous losses (see Exhibit 19 for financial details of Tyco and balance sheet information for the TGN business held for sale) and decided to stop investing in submarine cable business. The annual report 2003 puts it in perspective: “In addition to selling the TGN, we are also starting a broader divestiture program designed to increase the focus on our core operations by exiting certain operations that do not meet our criteria for strategic fit or financial returns. We are estimating that the potential proceeds (excluding operating loss from the TGN of $115 million) could be at least $ 400 million (Rs 17,600 million) once the program is completed.XI If we dispose of these businesses, we may not fully recover their recorded book values.” Tyco decided to sell-off TGN for Rs 9,695 million (Exhibit 20). For VSNL, this acquisition could be beneficial, as it felt there was profit to be made in the hyper-competitive subsea market at this price (there was about 90 per cent decline in submarine cable price) and increased bandwidth. If

XI The conversion rate taken is: 1 US$ = Rs. 44

20

the deal was finalized, experts reckoned that it would make it easier for telecom players to offer a range of services - especially broadband and international voice services at far lower prices. Besides the cable systems, the acquiring company would also gain real estate in international locations through associated landing stations and data centers. Therefore Reliance and VSNL both were keen to get this deal. According to an industry analyst37, "They are both (VSNL and Reliance) trying to be the king of bandwidth. (The National Association for Software and Service Companies (NASSCOM) estimated that India's bandwidth usage was only 8.5 Gbps in comparison to China, which had an usage of 80 Gbps bandwidth). Reliance is worried that VSNL already owns too much bandwidth through SeMeWe2 and 3 (a South-east Asia-Middle East-West Europe cable system, in which VSNL has a stake) and VSNL is worried that the combination of Flag Telecom and TGN will give Reliance too much power.” Given that bandwidth prices had been falling across the world due to a supply glut, how much sense did it make to buy a submarine cable network? The sub-sea link being sold by TGN was described by an analyst as a "disaster sale" as it was an ailing submarine cable business. The buyer of TGN would have to grapple with the problem of very low TransAtlantic prices. The operating and maintenance costs of an undersea network would enhance expenses. The buyer would also have to deal with formidable competitors like Global Crossing, Alcatel and Qwest. Teleglobe

Teleglobe (Teleglobe International Holdings Ltd. (TLGB) or Teleglobe) originated in 1950 as an offshoot of the Canadian Overseas Telecommunications Corporation (COTC), which later became Teleglobe Inc. Until the deregulation of the Canadian telecommunications market in October 1998, Teleglobe Inc. was the monopoly ILD service provider in Canada. The elimination of monopoly allowed service providers to route international calls through competing networks, including those serving the U.S38. Teleglobe had a vast infrastructure consisting of undersea fiber cables (Cantat-3, Canus-1, Tat-9, and Tpc-4), satellite investments and leased fiber, which interconnected it operations in 28 other countries. It was the third largest network in the world after AT&T and MCI WorldCom. Teleglobe had over 250 direct and bilateral relations with voice carriers, ownership in over 100 subsea and terrestrial cable systems, directly connecting over 90 countries to North America and was one of the largest providers of satellite capacity connecting the Internet. In 1987, the Government of Canada privatized Teleglobe Inc., which sold its 23 per cent share to Bell Canada Enterprises (BCE) in 1998. In 2000, BCE acquired Teleglobe. In 2001, BCE spent approximately Rs 78.8 billion to build Teleglobe’s Globe System network, an integrated voice and data network. The privatization affected Teleglobe: “The wholesale nature of Teleglobe's business made it especially vulnerable when deregulation came to the Canadian telephone industry. The company had no direct ties with end users, no name recognition and no brand equity. When Teleglobe managers realized that the company's monopoly on international traffic to and from Canada was about to end, they realized that they had to develop new lines of business quickly to replace the business they would lose39.” Teleglobe faced stiff competition from international alliances (AT&T, MCI, IDT Corporation, Sprint, Global Crossing, Level 3, and NTT/Verio) and consolidations among telecommunication companies resulting from the global trend of privatization, competition and deregulation. The increased competition resulted in a general decline in revenue of Teleglobe (see Exhibit 20 for selected financial details of Teleglobe). The net income started declining in 1998. Teleglobe

21

revenues in the second quarter of 2003 were US$594.6 million, down 17 per cent from the same period last year. The company lost $87.7 million in the quarter, compared to a net gain of $25.9 million a year ago. About half of the decline resulted from falling revenues at multi-level marketing subsidiary Excel Communications. New owner BCE said it would close Teleglobe's Montreal head office and eliminate about 850 jobs worldwide that year40. In April 2002, developments in the Canadian telecommunications industry, continuing losses at Teleglobe and substantial ongoing capital expenditure requirements related to the build-out of the Globe System platform caused BCE to withdraw all financial support from Teleglobe. The company was restructured and renamed as Teleglobe International Holdings Ltd. Following a split from BCE, Teleglobe became victim to overcapacity and lower demand in the telecom market, which pushed it into bankruptcy in 2002. Teleglobe emerged from bankruptcy in May 2003 when Cerberus, a private equity firm, for Rs. 6,820 million, brought its core voice and data assets out of bankruptcy protection. In December 2003, Teleglobe acquired 100 per cent ownership of ITXC (Internet Telephony Exchange Carrier), a US based wholesale provider of VoIP. This acquisition was supposed to increase the declining gross margins of both companies41. However, Teleglobe again reported a net loss of Rs 941.4 million for 2004. Under pricing pressures, scale and investment requirement, Teleglobe preferred to grow organically and was looking at the fast growing emerging economies. Indian telecom market growing at a scorching pace could be an interesting play. The assets and experience of employees of Teleglobe made the offer very attractive for Indian bidders (Reliance, Bharti and VSNL). The acquisition of Teleglobe was expected to cost around Rs 10,500 million. But even at this price the winning bidder was poised to become a global player in wholesale voice, bandwidth and enterprise data services as it would enable a global reach to over 240 countries.

22

The Future

Srinath knew that the company was facing a new era of competition and to survive it the company had to face a new set of challenges. As VSNL looked to transform itself into a consumer-friendly global company, it had to ensure that it had the right skills and focus in business development. From an organizational point of view, the restructuring of VSNL was simply a first step towards a more efficient and responsive organization, but was it sufficient considering the competition at the national and international levels? Srinath knew he had to evaluate these issues in the context of VSNL’s total business, which included national and international voice, data and enterprise solution. Under the current circumstances of declining revenue and profit, would it not be right to consolidate rather than to expand by investing through acquisition of international companies like Tyco and Teleglobe? Would they really add value or merely prove to be an expense? 1 Source: Executive Summary 2000-05, Telegeography Research http://www.telegeography.com/ee/free_resources/pdf/tg05_exec_sum.pdf (2: 30 p.m. on Dec 02, 2009) 2 http://www.telegeography.com/ee/supplemental_files/pdf_file=tg02_exec_sum.pdf (2: 30 p.m. on Dec 02, 2009) 3 WLL (LM) is a system that connects subscribers to the PSTN (Public Switched Telephone Network) using radio signals as a substitute for copper for all or part of the connection between the subscriber and the switch. In India it was introduced by Basic Service operators including Reliance and Tata Tele Services Limited. 4 Source: http://www.indianexpress.com/ie/daily/20000907/ibu07052.html (2: 00 p.m. April 5, 2010) 5 Source: DoT Annual Report 2004-05, pp: 5 6 Source: http://www.indiastat.com/table/telecommunication/28/internet/143/395675/data.aspx (2:20 p.m. on April 05, 2010) 7 Source: http://www.iimcal.ac.in/community/consclub/reports/telecom.pdf (2: 30 p.m. on Dec 07, 2009) 8 http://www.rediff.com/money/2004/jul/28edge.htm (3:00 p.m. on April 2010) 9 Source: http://voicendata.ciol.com/content/top_stories/105020801.asp (12: 50 p.m. on Dec 07, 2009) 10 Source: http://voicendata.ciol.com/content/top_stories/105020801.asp (12: 50 p.m. on Dec 07, 2009) 11 Source: http://voicendata.ciol.com/content/vNd100/2005/2005a/105070621.asp (2:20 p.m. on April 05, 2010) 12 OCS was an erstwhile department under the DoT and predecessor of VSNL 13 Source: http://www.expressindia.com/news/ie/daily/20000817/ibu17021.html (2: 00 p.m. on Dec 03, 2009) 14 Through a public auction; Reliance was the other unsuccessful bidder 15 More details about the Tata Group available at www.tata.com 16 Source: http://www.thehindu.com/2002/06/11/stories/2002061101842000.htm (1:40 p.m. on Dec 08, 2009) 17 Source: sec.edgar-online.com/2003/09/29/0001145549-03-001242/Section8.asp (2: 00 p.m. on Dec 01, 2009) 18 Data Access ran into financial trouble when it had to defer its IPO in 2004 and had to practically suspend operations by the end of 2004 19 Source: Bharti Tele-venture Press Release, 29th March 2004 20 Source: http://www.convergenceplus.com/jun03%20india%20telecom %2002.html 21 N. Srinath, in an interview with Christabelle Noronha www.tatamail.com/our_commitment/employee_relations/articles/20030526_the_integrated_approach.htm (10:00 a.m. on Feb 02, 2008) 22 Source: http://archives.infotech.indiatimes.com/News/VSNL-not-to-cut-rates-for-carrying-BSNLs-ILD-traffic/articleshow/msid-573740,curpg-2.cms (11: 50 a.m. on April 22, 2010) 23 Source: http://www.thehindubusinessline.com/2006/05/27/stories/2006052702830400.htm (2: 00 p.m. on Dec 01, 2009) 24 Long distance charging area (LDCA) means one of the several areas into which the country is divided and declared as such for the purpose of charging for trunk calls which generally is co-terminus with Secondary Switching Area. 25 http://www.indiaonestop.com/ISPS.htm#ISPs (2: 15 p.m. on April 06, 2010) 26 Dishnet, belonging to the Sterling Infotech Group, had been one of the pioneers in the Digital Subscriber Line (DSL) Broadband access technology in India, making DSL available across leading cities in India. DSL is a technology to provide high-speed, always-on broadband Internet access to customers through transmission of data signals even over standard copper telephone lines. Dishnet has played a major role in contributing significantly in enhancing Internet penetration and Broadband Internet in India

23

27 An intermediate form of network in terms of geography is a Metropolitan Area Network (MAN) http://www.erg.abdn.ac.uk/users/gorry/course/intro-pages/man.html (10:30 p.m. on Dec 30, 2009) 28 Source: http://idrinfo.idrc.ca/Archive/114638/pany_inst_version/in1.htm (7:40 p.m. on Dec 8, 2009) 29 Source: http://www.convergenceplus.com/dec04%20expert%20view%2002.html (5: 30 on April 6, 2010) 30 Source: http://www.tata.com/media/interviews/inside.aspx?artid=1XvlEK2GH6A= (7:00 p.m. on Dec 8, 2009) 31 Source: http://voicendata.ciol.com/content/goldbook/goldbook05/105030401.asp (5:00 p.m. on April 6, 2010) 32 Time Division Multiplexing (TDM) circuits have been the backbone of communications over the past several decades. These circuits which provide reliable and low-delay services for voice, data and video transport, are migrating towards Internet Protocol (IP) based packet switched networks. The primary reason for the migration of these circuits is to reduce the cost of transport and management by having a converged network for all services. 33 Source: http://www.tataindicomebu. com/news/show.asp?f=20040412-milestone 34 Source: www.tata.com/vsnl/media/20030702.htm 35 Source: VSNL eighteenth annual report 2004 36 Specifications: Landing Points: Chennai, India and Changi, Singapore; City POP: Chennai, India; Global Switch: Tai Seng Avenue, Singapore; Cable Length: 3,175 kms; Number of Fiber Pairs: 8; System Capacity: 5.12 Terabits per Second; Initial Capacity: 320 Giga bits per second; Branching Units: 4 37 Source: http://www.businessworld.in/content/view/1436/1494/ (10:30 p.m. on Dec 30, 2009) 38 Source: http://strategis.ic.gc.ca/epic/site/smt-gst.nsf/en/sf06287e.html (10:30 p.m. on Dec 30, 2009) 39 Source: http://telephonyonline.com/mag/telecom_new_old_carrier/ (10:30 p.m. on Dec 30, 2009) 40 Source: Angus TeleManagement's bulletin – Telecom Update 14th August 2000 41 Source: VoIP Newsletter, December 2003