video consumption in 2020 - diva-portal.org827417/fulltext01.pdf · based on consumers’...

TRANSCRIPT

DEGREE PROJECT, IN , SECOND LEVELMEDIATECHNOLOGYSTOCKHOLM, SWEDEN 2015

Video consumption in 2020A STUDY ON CONSUMER BEHAVIOUR ANDCONSUMER MOTIVES

CIM NORDLING, [email protected]

KTH ROYAL INSTITUTE OF TECHNOLOGY

COMPUTER SCIENCE AND COMMUNICATION (CSC)

VIDEO KONSUMTION 2020

En studie över konsumtionsbeteende och motiven bakom tv-tittande SAMMANFATTNING Tv-branschen har gått från en tid då traditionella medier hade ett större inflytande över konsumenternas beteende. Konsumenterna tar allt större kontroll över sin konsumtion av rörlig bild, vilket ställer nya krav på medieindustrin. Genom att förstå varför konsumenter vänder sig till rörlig bild i olika tittarsituationer kan medieaktörer erbjuda en förbättrad tittarupplevelse. I denna studie undersöks hur konsumenternas beteende kan komma att utvecklas fram till 2020. Studien består av två delar; dels en analys av konsumentdrivkrafter identifierade av tidigare forskning, och dels en kvalitativ studie baserad på expertintervjuer. I studien fastställdes tre tittarsituationer; socialt tittande, engagerat tittande och bakgrundstittande. Situationer sattes i relation till de identifierade trenderna inom områdena; teknik, konsumentbeteende och nya affärsidéer. Resultatet av studien tyder på att linjär tv fortfarande kommer vara en stor del av videokonsumtionen 2020, samtidigt som användningen av Over-the-top-tjänster (OTT) förväntas öka. Linjär tv torde användas mer för slötittande och live-evenemang, medan VOD väntas användas för att uppfylla personliga behov. Konsumentbeteende förväntas utvecklas mest i den sociala tittarsituationen, eftersom bilden av socialt tittande vidgas och de förväntade tekniska framstegen sannolikt kommer att få oss att känna närvaro både över tid och rum. Engagerat tittande torde också förändras, om fem år antas binge watch, alltså titta på flera avsnitt av samma serie i rad, vara allt vanligare. Till skillnad från de andra tittarsituationerna, tyder resultatet på att bakgrundstittande inte kommer att förändras lika mycket, främst på grund av att beteendet är djupt rotat i linjär tv. Nyckelord TV konsumtion, Tittarbeteende, Need states, Uses and gratification, VOD, Linjär tv, OTT

Video consumption in 2020 A study on consumer behaviour and consumer

motives

Cim Nordling KTH Royal institute of technology

Computer Science and Communication (CSC) Stockholm, Sweden

ABSTRACT The television industry is evolving from an environment where traditional media had a greater influence over the consumer behaviour. Consumers are taking control over their video consumption, which places new demands on the media industry. By understanding consumer motives and viewing situations, media actors can provide an enhanced viewing experience. This thesis studies how consumer behaviour can evolve until 2020. The study consists of two parts; firstly the identification of viewing motives identified by previous research and secondly a qualitative study based on expert interviews. The study concluded three viewing situations; social viewing, engaged viewing and background viewing. The viewing situations were put in relation to the identified trends in the areas; technology, consumer behaviour and new business concepts. The main findings state that broadcasted linear television ought to be an evident part of video consumption in 2020, while the usage of Over-the-top (OTT) services are expected to increase. Broadcasted television is likely to be used more for background viewing and for live events, while Video-on-demand (VOD) is assumed to approach a role as a customizable service that satisfies personal needs. The consumer behaviour is believed to evolve the most in the social viewing situation. For the reason that the definition of social television is extending and the technological advancement is likely to make us feel connected both over space and time. Another aspect that is presumed to change is the engaged viewing, where consumers ought to be more likely to binge watch, which is when you watch multiple episode of the same show in a row. Unlike the other situations, the background viewing behaviour is not assumed to change fundamentally, mainly because the behaviour is deeply rooted in linear television. Keywords TV consumption, Viewing behaviour, Need states, Uses and gratification, VOD, Linear TV, OTT

1. INTRODUCTION The television landscape has changed; online alternatives have become an evident part of our media consumption and are closing up on traditional channels [1]. Digital revolution is not only changing the TV landscape it is also a driving force behind consumer behavior. Statistics show that broadcasted television is decreasing in viewing time; during 2014 it declined with 4% while the viewing time via Internet increased with 21% [2]. Consumers are given more choices and the possibility to pick and mix a personalized range of TV and video services. Similar to the trend we have seen within the music industry, TV and video services are becoming unbundled, in the sense that consumers can choose services separate and decide how they would like to pay from a wide range of subscription and transaction models [3]. Consumers are expected to quickly adapt to new services and products, while becoming more active users. Therefore when designing new video services, it is important to understand how consumers use television, in order to make the digital transition easier [4].

Today video consumption occurs in a wide range of environments, on multiple platforms and via different devices. Video can be anything from a short clip on YouTube, or video on demand to traditional scheduled TV shows. The device used to access the video content can be a static television or a mobile device like a tablet or a laptop. The technology development has brought new business opportunities and changed the fundamental habits of video consumption. The diversity of the multiple viewing situations lead to significant different contextual factors, that affect the consumers’ choice of device and content. In the next five years we will see a remarkable change as the traditional television services, like terrestrial, satellite and cable services, continue to meet new Internet and mobile media platforms. Indications are that we have seen the beginning of this journey and now we can expect behavioural changes among the mass as well [5]. Predicting the exact future is close to impossible, but this thesis will try to create a vision of how the television

industry could appear in the future, by looking at the viewing situation today combined with current trends. 1.1 Purpose and problem definition The future of the television industry is essential for multiple actors; one of them is Nepa1, a research company that operates in several fields including the media industry. Nepa provides entertainment companies with customer insights through analytics. This thesis has been done in collaboration with and with supervision from Nepa. Given the larger effect by the consumers on the media industry, the users’ motives behind choosing certain content or channels are of high relevance. By understanding the contextual factors of viewing situations, TV-providers and video delivery systems can enhance the experience when watching video. Therefore the main focus of this thesis has been to investigate how consumers will watch video in 2020. The underlying objectives were (1) to identify different viewing situations based on consumers’ motivation for watching video and pinpointing the underlying internal needs that drives the media consumption and (2) to identify what trends are relevant when approaching the future consumer behaviour. This has given the problem definition: How will the viewing behaviour of video appear in 2020? • Which are the underlying drivers behind the choice of

platform and content today? • What trends are relevant for the development within

the TV industry during the five following years? • How will the trends affect the future consumer

behaviour? 1 http://www.nepa.com

1.2 Delimitations The thesis is focused on the Swedish consumers and the Swedish media market. Advertising aspects will not be considered to a larger extent since the focus is on the consumers’ perspective. The main concern will be legal services and therefore illegal alternatives such as illegal downloading and streaming, will not be taken into account.

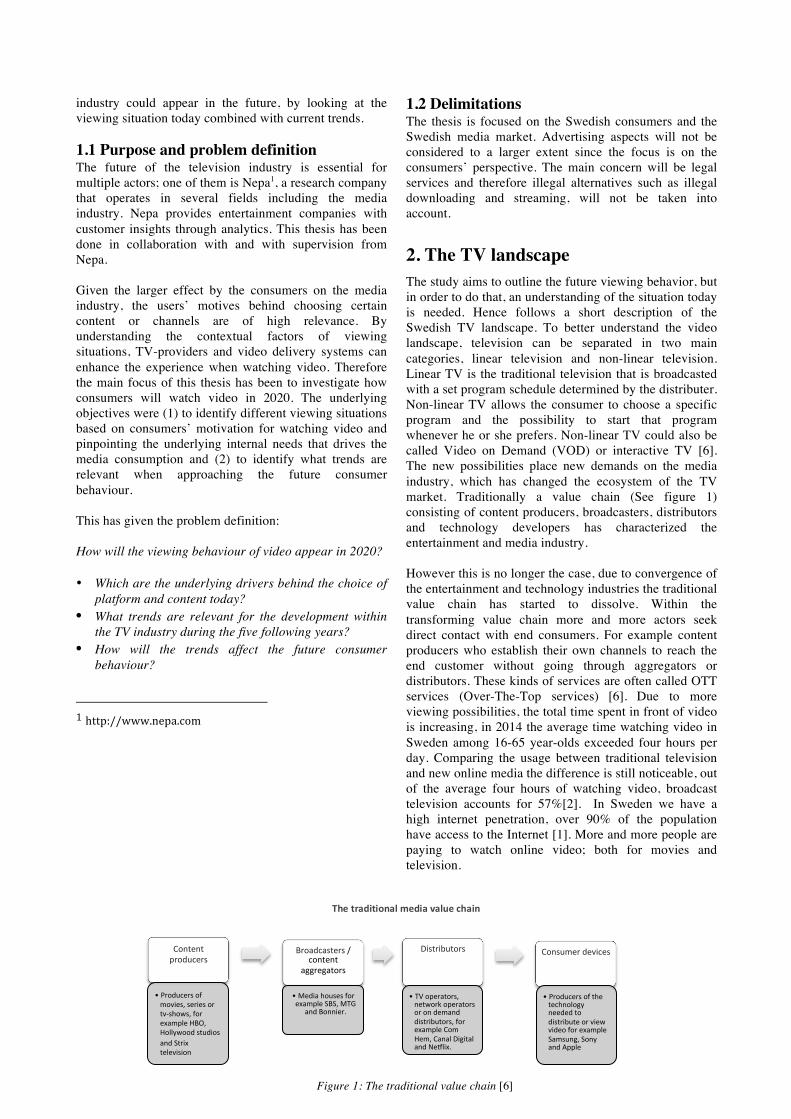

2. The TV landscape The study aims to outline the future viewing behavior, but in order to do that, an understanding of the situation today is needed. Hence follows a short description of the Swedish TV landscape. To better understand the video landscape, television can be separated in two main categories, linear television and non-linear television. Linear TV is the traditional television that is broadcasted with a set program schedule determined by the distributer. Non-linear TV allows the consumer to choose a specific program and the possibility to start that program whenever he or she prefers. Non-linear TV could also be called Video on Demand (VOD) or interactive TV [6]. The new possibilities place new demands on the media industry, which has changed the ecosystem of the TV market. Traditionally a value chain (See figure 1) consisting of content producers, broadcasters, distributors and technology developers has characterized the entertainment and media industry. However this is no longer the case, due to convergence of the entertainment and technology industries the traditional value chain has started to dissolve. Within the transforming value chain more and more actors seek direct contact with end consumers. For example content producers who establish their own channels to reach the end customer without going through aggregators or distributors. These kinds of services are often called OTT services (Over-The-Top services) [6]. Due to more viewing possibilities, the total time spent in front of video is increasing, in 2014 the average time watching video in Sweden among 16-65 year-olds exceeded four hours per day. Comparing the usage between traditional television and new online media the difference is still noticeable, out of the average four hours of watching video, broadcast television accounts for 57%[2]. In Sweden we have a high internet penetration, over 90% of the population have access to the Internet [1]. More and more people are paying to watch online video; both for movies and television.

Content producers

• Producers of movies, series or tv-‐shows, for example HBO, Hollywood studios and Strix television

Broadcasters / content

aggregators

• Media houses for example SBS, MTG

and Bonnier.

Distributors

• TV operators, network operators or on demand distributors, for example Com Hem, Canal Digital and NeJlix.

Consumer devices

• Producers of the technology needed to distribute or view video for example Samsung, Sony and Apple

The traditional media value chain

Figure 1: The traditional value chain [6]

In Sweden 14 % of the Internet users have a subscription to a video on demand service (SVOD) [1]. It also exist more media devices than ever, in an average Swedish home there are seven media devices [2]. A total of 45% of the population has access to a smartphone, a computer and a tablet (See figure 2); only 10% of the people do not have access to neither of the devices. A high Internet usage in combination with a widespread diffusion of devices has resulted in OTT services gaining a big audience. In the end of 2014 nearly 2,5 million people had access to a SVOD service in their home [7] which meant that streaming services reached 71% of the Swedish population each month (See figure 3).

3. METHOD This study consists of two parts. The first part; a review of literature based on studies containing the uses and gratification-theory, the goal was to identify frequently observed consumer motivations. By analysing gratifications and need states (See figure 4) in relation to the following parameters, explained in 4.1 and 4.2, common viewing situations have been identified.

• Context; is the consumer sharing the experience or watching solitary?

• Content selection; What type of content is chosen? • Temporal context; Is the video consumed on a

special occasion or is it everyday viewing? • Consumption device; Which devices and services

are most commonly used?

A lot of studies have been done on user situations, where similar situations have been found. The identified viewing situations in this study do not provide a fully extensive view, but rather an overall picture that includes the majority of the user motivations [8].

The second part of the study and the main focus of the thesis was a qualitative study based on expert interviews. To be able to identify trends within the media industry, it proved more valuable to make an interview study with industry experts rather than consumers. Data source triangulation was used to gain a more comprehensive understanding of the media industry and to understand the drivers and barriers for each actor. The reason for this was mainly to get a deeper understanding of difficulties and opportunities within the media market [9]. The interview participants were chosen to cover actors from different parts of the value chain as well as advisory companies within the media area. In total 8 interviews were carried out from: TV-providers and VOD services, technology providers, broadcasting companies and media strategy companies. (See Table 1) The interviews were semi-structured in depth interviews [10]. All the interviews were done in Swedish and the results and quotes has been translated to English.

Before conducting the interviews, questions were iteratively defined and sent to the participants in advance in order for them to understand the aim of the interview. The questions were based on findings from the literature review. Basically the same open-ended questions were used through all interviews, however questions differed in some extent depending on in which area the company operated. The interviews were, all but one, carried out face-to-face and ranged in the length of 35-70 minutes. The last interview were done by telephone and lasted about 60 minutes. The data was collected via transcriptions of audio recordings from the interviews. The material was sorted and analysed to identify trends on the market and in consumer behaviour. The identified trends were then compared in order to determine which trends were the most important, i.e. which trends will have an impact on consumer behaviour. The trends were categorized and then analysed in relation to the identified viewing situations. The interview questions, translated into English, can be found in Appendix 2.

45%

25%

5% 1% 1%

13% 10%

Computer, smartphone and tablet

Computer and

smartphone

Computer and tablet

Smartphone and tablet

Only smartphone

Only computer

Neither

Access to computer, smartphone and tablet

Figure 2: Population with access to each device [1]

Streaming reach among the Swedish population (15 to 74 years-‐old)

Per month: 71%

Per week: 60%

Per day: 35%

Figure 3: Streaming reach among the population [35]

Table 1. Conducted expert interviews

4. EXISTING RESEARCH ON MEDIA BEHAVIOUR To fully understand how consumer behaviour can evolve during the coming years a here follows a presentation of theories used to determine consumers’ motives behind watching television, and a description on current user behaviour. 4.1 Consumer motivations One approach to why people watch television is the “uses and gratifications”-theory, which is a widely used framework that studies consumer behaviour and motives behind using media [4],[11],[12]. The theory suggests that choices made when watching television are motivated by the desire to satisfy a series of needs [13]. The uses and gratification perspective assumes that consumers are active users that make goal-oriented choices [14], therefore the choice of content and platform will be based on the objective to fulfil the desired gratification. The uses and gratification-theory has been the subject for various studies, most of them have found three to six gratifications that consumers seek when watching television. Similar to other research, McQuail [15], [16] argues that the gratifications are: Surveillance, Personal identity, Integration and social interaction, Diversion. (See Appendix 1 for more examples)

Even though the uses and gratifications approach is widely used it is not without some criticism. Firstly, the assumption that the consumer always makes active and goal-oriented choices has been criticised, especially regarding traditional media which is less selective and is assumed to trigger more habitual watching patterns [4]. Secondly, research argues that it is not enough to only look at the individual factors when determining consumer motivation. The uses and gratification approach ignores structural and contextual factors such as cultural specifics, audience availability, and access [4]. Some studies argues that choice of medium and platform are mostly depending on contextual factors while choice of content often is associated with individual factors, see for example [17].

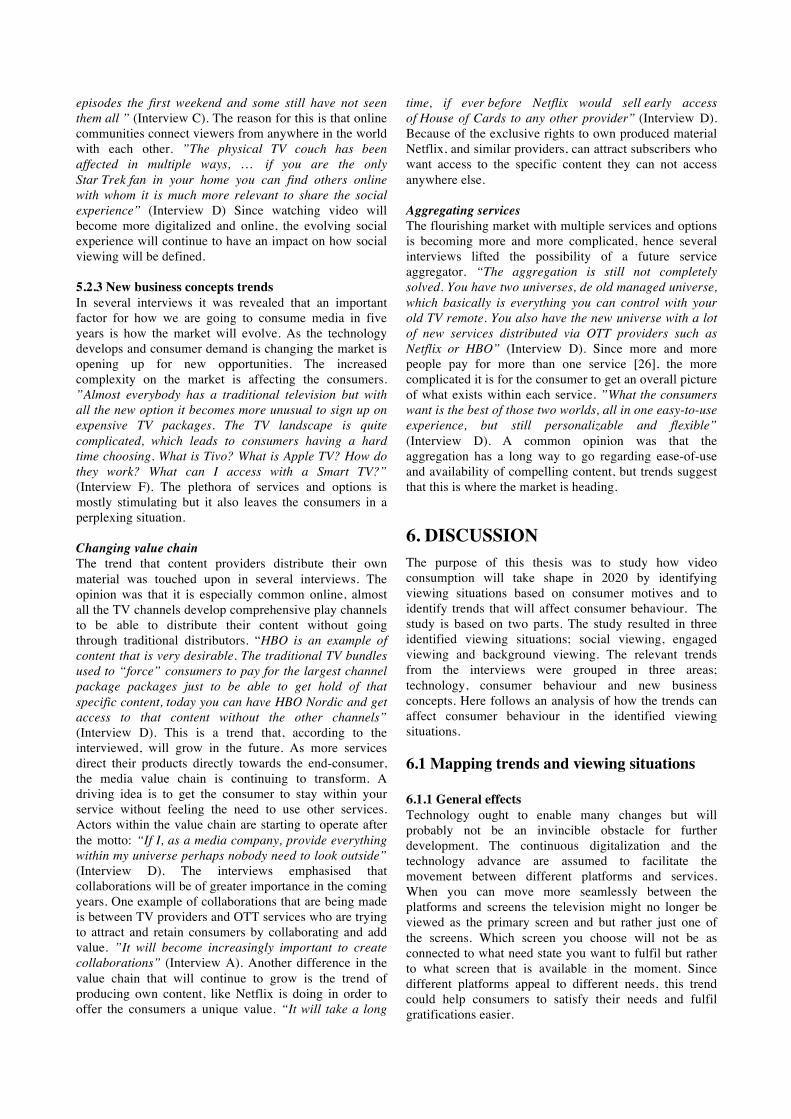

A more recent approach, that accounts the criticism of the uses and gratification perspective, is the theory about television need states (See figure 4). Each state is not only shaped by the motive behind watching video, but also by context as well as the choice of device and content. The six need states disclose a variety of viewing motives that could be used to describe different viewing situations.

The need state Indulge is about satisfying the need for “me-time” and give in to pleasures, it is the time when you watch your ���favourite content and really devour in what you enjoy watching the most. Escape could be described as the need to leave everyday-life, when you want to immerse into another place or time. The consumer could use the content as a portal to “escape” from the reality. The state Experience is the desire of a fun and enjoyable occasion, which could be shared with family or friends. Unwind is defined by the need of de-stressing after a day of hard work or deferring the pressures in life. By watching television the consumers can relax and clear their minds. Comfort is about the everyday rituals, for example it could be shared family time in front of the TV while having dinner or when seeking comfort in togetherness. Connect is the need to feel a sense of connection to society, to time or to a place. It is often characterized by live-based content that connect the consumer with people outside the living room.

Operation area Position Interview

TV operator

Market Analysis and Research

A

TV operator

Product and Business

development

B

Broadcasting company

Program director for interactive

content

C

Network, technology and service provider

Media strategy

D

VOD Service CEO E VOD Service CEO F

Business development and

strategy Analyst

G

Media measuring company CEO H

The six need states of television

Figure 4: Chart of the six need states of television, adapted from [22]

4.2 Consumer habits VOD services and OTT solutions have made the viewership more flexible and personalized [6]. Consumers demand larger control over their media consumption, which promotes the free choice within the TV landscape. Consumers want unrestricted access anywhere, any time and on any device [3]. With a multitude of devices and multiple viewing occasions the time spent watching video is more fragmented than ever. Even though multiple devices are used, consumers’ attitude has shifted from accessing a device to accessing content no matter device. The mind-set has changed from “What is on right now” to “What do I feel like watching right now” [18]. Even though smartphones and tablets have extended our viewing behaviour throughout the day, most of the viewing is still done from the home. The largest viewing occasion is at home during prime time, approximately between 7pm-11pm [19]. It is also the situation when the consumer is most focused and engaged with the content. Most of the video is consumed on the TV screen (See figure 5) [20]. However, consumers have adopted a second screen behaviour, meaning that they use their phone, computer or tablet while watching television. 36% of the time spent in front of a traditional TV set is spent doing other activities like browsing, looking at the TV schedule or using social media on another screen (See figure 6) [21]. Viewing occasions can be split up into everyday viewing and special occasion viewing. Everyday viewing tends to be non-live television while special occasion viewing tends to be more live content and event based watching. Content can also be divided into two parts; premium content such as your favourite TV shows and secondary content for example old movies. In a study by Ericsson [23], VOD is present in each of the four quadrants in the two-dimensional space defined by content type and viewing type (See figure 7).

The study done by Thinkbox research [22] claims that personal needs are better satisfied by VOD services; especially the states indulge and escape. However VOD seems to be less suitable for social needs like experience and connect, mainly because the traditional TV is more equipped to satisfy those needs. When people watch television to unwind or for comfort, they more often chose to watch it on the TV screen [19].

31%

17% 17%

48%

0%

10%

20%

30%

40%

50%

60%

2013

2014

Figure 6: Second screen behaviour [21]

Percentage of the viewers who use other devices while watching television

Average time spent watching video on each device per week

Figures 5: Most used device, adapted from [23]

The role of different content types and content services

Figure 7: Map over content and viewing occasions, adapted from [23]

5. RESULT

5.1 Identified viewing situations The following section is mainly based on the review of previous research and existing statistics of television viewing. By analysing the television need states in relation to the Swedish TV landscape and current consumer habits, the following viewing situations have been identified. 5.1.1 Social viewing Refers to a social viewing situation with the purpose of connecting with others and feel a sense of belonging. The situation is characterized by the longing for connection to society, to a place or to people around you. The viewing often occurs in company with others, such as family and friends, based on the desire of a shared experience. Both in the sense of being together and in the sense of discussing the content with others, the viewer feel like a part of a group or community. The situation mainly consists of special occasion viewing and can be categorized as primetime watching. The content watched is either premium or secondary. If the need is to feel connected to others the choice of content is very important, typically it is premium content such as live events, sports, or primetime shows. The content often has a live feeling connected to it, such as competition shows. It is often watched at a set time through broadcasted television, since this reinforces the feeling of connection to people outside the living room. If the aim is to socialize with the people in the same room, the choice of content is still important but not as crucial as in the previous scenario. It could be secondary content, such as a movie, since the most important is to share the experience and have quality time with the people in the room. The device chosen in both scenarios is generally the big TV screen, since it is easier to share with others and gives the viewers a better social experience. 5.1.2 Engaged viewing A viewing situation customized after your preferences. The aim is to treat yourself with your personal favourites and satisfy the need for “me-time”. It can work as an escape from reality, in order to leave your everyday life and stop thinking about difficult or uncomfortable situations in your real life. This situation is about cuddling up in front of your favourite program and just enjoying the moment. The situation is often characterized by solitary viewing, because the content watched may be your personal favourite or not appropriate for the whole family to watch. People who share the same interest could share this situation together, but the focus is still to indulge and empathizes with the content. The situation is characterized by premium content and special occasion viewing, the situation occurs when the consumer have time and are often watched on demand. The content is highly engaging and is something the consumer really enjoys watching.

The content could be watched on the big TV screen, on a tablet or computer from the bed before going to sleep, depending on the context and access to devices. This type of engaged viewing often occurs during the later part of the evening. 5.1.3 Background viewing The situation is a routine viewing situation with the goal to de-stress and to defer the pressures in life. The consumption is habitual and used to feel comfort and relaxed as well as to get your mind of things. The choice of content and device is not as important. What characterizes this situation is simplicity and routine, therefore it is common to watch secondary content or the content that is broadcasted at the moment. Since the consumer is not as engaged in the content, it is not a must to watch the entire program. The situation often occurs during the early part of the evening and is a way to pass time when getting home from work or school and to reload before making dinner or doing chores. 5.2 Identified trends Based on the expert interviews the study found three main areas that will have an impact on how consumer behaviour will evolve during the next five years. The identified trends are therefore categorized by these three main areas; technology, consumer trends and new business concepts. The relevant trends have been identified based on frequency in the interviews and potential affect on consumer behaviour. 5.2.1 Technology trends According to Ng [24] technology is a central part of the media industry; therefore the technology development is an evident part when forecasting how the consumer behaviour could change. Technology was also a recurring subject during the interviews, here follows a couple of relevant technology trends that were identified on top on the continued digitalization. Extended flexibility One of the trends that was brought up in several interviews, was free choice and flexibility, this trend is believed to continue to evolve and have a great effect on consumer behaviour. Two important technology aspects that were raised was the possibility to place shift and time shift. The option to control at what time to consume specific content is called time shift while place shift allows you to access content stored on one device from another place through a different device [23]. Both place shift and time shift is frequently used when watching VOD today and this study shows that it is assumed to become even more common in the future. This could allow consumers to move easier between new digital media platforms and traditional linear television. ”To the consumers VOD and broadcasted television will blend together, it is becoming more of a technology issue. The easier the platforms and solutions become the more the audience can move seamlessly between different distribution channels”(Interview C).

The increasing movement over space and time can be summarized by the acronym AWATAD – Anywhere, Any Time, Any Device. AWATAD is a term that has been used within the television industry for a couple of years [25]. In several of the interviews it was highlighted that it has been considered an advantage to offer the consumers AWATAD. However, it is becoming more of an expectation and demand from the consumers rather than a competitive edge. “… As soon as some new device or platform appears the consumer expects us to exist there as well” (Interview F). It was also brought up that AWATAD is a trend that is expected to continuously affect the consumer behaviour and evolve to be a standard functionality among all the media actors – from TV providers to VOD services. ”People are getting used to the free choice when consuming media, and you as a media company are expected to deliver that” (Interview G). A barrier to the demand to exist on all platforms that was highlighted was the cost issue, today it is costly and time consuming to exist everywhere since all platforms requires different applications. According to the experts this is expected to change. “In the future I think it will be more generic how to develop applications, today you need to develop different apps for each platform, which is quite demanding” (Interview F). An expected technology trend is therefore the standardization of application programming within the TV industry. Content discovery tools Another trend frequently brought up regarding technology was the management of content. Regarding content the common opinion was that it ought to be one of the most important factors that steer consumer behaviour. The interviews also stated that the available selection of content will increase. As the amount of content and services increases the technology needs to adapt and create new smarter ways to find the right content at the right time. ”When talking about content we can’t only look at the physical available content, we also need to think of what we perceive as accessible, since it’s the content we believe to be accessible that direct our consumption” (Interview H). This is supported by a report from Ericsson where they state that enhanced search tools with more personalized recommendations will come in the near future. ”As the volume of TV and video material increases, smart and personal recommendations from social networks are becoming an important source for discovering and exploring new content. [3]” The interviews also showed that existing solutions are not sufficient and that they have to advance within the coming years. On claim is that it is far from as efficient to search for video content, as it is for text-based content. If search functions and discovery tools do not advance, it could be complicated to find the content you are looking for as the amount of content increases. ”If any actor could launch a search engine that could guide us among motion pictures as well as within text based content it would make a lot of video content seem more available” (Interview H). The interviews also suggest that technology will develop to give better and more

personalized recommendations, both at the right time and the right type of content for each situation. “It will happen more frequently that your TV or your device recommend what you could watch based on what you have watched before, say for example that I watch news every evening around seven, then my TV could show me all the possible news programs when I turn on the TV around that time” (Interview A). According to the experts this is a trend that will affect how we consume video. 5.2.2 Consumer behaviour trends As mentioned earlier, we have entered a new era in television; not only in regards to technology but also the way we approach media has changed. The consumers have embraced the new watching possibilities, which have resulted in increased average time spent in front of video. ”Earlier we were bound to use the computer or television, now it is more flexible and it is easy to bring the video with you. When we get a little better Internet connection we can truly watch video unlimited” (Interview A). Here follows the identified trends within consumer behaviour. Embrace of the digitalization From the interviews, a frequently identified trend regarding consumer behaviour was the adaptation to digital services. Consumers probably will continue to embrace the digitalization and all the new possibilities it brings. How we consume media will proceed to change, the trend shown in the statistics about the TV year 2014 from MMS [2], stated that linear television decreased in watching time with 4% and online television increased by 21% - and this is just the beginning. “We are moving towards a time when all key content will exist on multiple platforms, satellite, terrestrial, cable TV and all the digital solutions” (Interview B). This could give the consumers even more freedom to freely chose content, viewing situations and payment models. ”The winners of the development is the consumers, it’s they who benefits from the changes” (Interview H). The choices are within the consumers’ power, from the pick and mix-behaviour, a content chasing habit is starting to emerge, especially when it comes to VOD services. Consumers chose the service that satisfy their needs right now and switch service if they would like to see something that they can not access from their existing service. “The consumers are starting to chase content, not many services requires you to sign up during a specific time, what is happening is rather that the consumer signs up for HBO one month to watch Game of thrones and the next month he or she signs up for Netflix in order to watch House of cards. What we are seeing is the consumers changing to a transaction behaviour” (Interview F). On the other hand, a couple of barriers that is slowing down this transition were identified in the interviews. The most significant one were the fact that people are habit creatures; it takes some time to accept new technology and change behaviour. ”People want to test new things but they are rooted in their habits which delays the digital

shift”(Interview H). The interviews suggest that people adapt to technology and new services at different pace, but technology keeps evolving. “I don’t see any technology barriers that we will not solve, the obstacle rather is the consumers’ ability to embrace the technology development” (Interview E). However we have seen signs that the mass is starting to change viewing behaviour as well. According to the interview D, the reason that the industry is opening up to the mainstream mass, is that the technology as well as the services have matured. The technology will become more accessible and appealing to a larger audience. Even the late adopters are becoming advanced users and now when the mass is adopting we can expect the transformation to go fast. “We have definitive leaved the early adopters phase, it is not only the people with technology interest that buys movies digitally, we have reached pretty far in to the bend shape curve” (Interview E). According to the interviewed experts, the mass adoption to the digital viewing behaviour will have an impact at the media measurements the coming years. “The average time spent watching television will continue to increase since not everybody is using the new platforms yet” (Interview B). Another topic that was emphasized in the interviews was the generation issue. Media consumption and media habits are linked to generational aspects. ”Television viewing is based on personal choices, some people watch broadcasted television and others watch television online, it is partially a generation issue. It is related to the habit of using different platforms and the habit of being able to make your own choices” (Interview C). The reason that was accentuated was the fact that younger people have grown up with another mind-set and a habit of using technology. The younger generations are going to set new standards on how we think of motion pictures. “Adolescents and young people are much more mobile in their consumption behaviour and they have shorter span of attention” (Interview G). The fact that younger people are more frequent users of VOD and online video services is also confirmed by the statistics from the MMS study [2]. Social television A consequence of the digitalization that was raised in several interviews was the change of social aspects. The emerging behaviour, such as second screen and binge watching, make us question the traditional TV sofa. ”What does it mean to watch together? When we are sitting together in the sofa but watching different content on different screens? Or watching the same content at the same time but from different locations? (Interview H). The common view was that the TV sofa will continue to be a meeting point in the home, but what is changing is where the attention is directed. A family can be gathered in the sofa in front of the TV but where the attention is directed can be scattered. The amount of screens competing for your attention has increased and according to a study from Sifo [21] the attention directed towards the traditional TV screen is shrinking. It is not that common to watch more than one video at the same time

since watching video requires high focus. It is much more common to do other things while consuming TV i.e. play games, answer mails or use social media. Second screen behaviour is taking up a larger portion of our viewing time (See figure 6), 36% out of the time spent watching traditional TV is spent in front of more than one screen [21]. “People do a lot when watching television, like surf the web, browse through a magazine or have dinner” (Interview A). The second screen behaviour was discussed in several interviews. The conclusion was that the behaviour amplifies the view that a device just is a screen that enables the possibility to watch the content that you want. ”We are starting to think of the TV as a screen, a big but dumb screen that provides a good experience that is easily shared with others, we do not associate the screen with a specific content in the same extent as before” (Interview D). The different screens are used in different situations and different purposes. ”It is not always one screen that is better than the other, the consumer is directing their attention towards the screen with the right content to satisfy their needs in that moment” (Interview H). All interviewed indicated that the preferred screen still is going to be the big traditional TV screen, especially if you are going to watch something with others or if the content requires high quality, for example an action movie, live events or sports. ”If you are at home and you are going to watch something for a while I believe that you as a consumer prefer the bigger screen with the best quality and the best sound” (Interview A). The fact that the TV screen will continue to have a central part in our lives in five years was widely recognized among the interviews. ”The traditional television has a great social capacity but it is changing, I do not believe it will fade out entirely. Certain content like live broadcasted programs or specific movies will still gather the whole family around the TV” (Interview D). However a shared view was that it is not always possible to use the big screen, it could be because someone else uses it or that you want to watch something when you go to bed. “… Nowadays we solve it by taking our own device and sit down wherever in the home or on the couch with other family members but with headphones” (Interview D). It was not only the social aspect within the same location that was raised during the interviews, but also the concept of binge watching. When content providers like Netflix release all the episodes of one season at once it encourage consumers to binge watch. Naturally this results in some people watching the whole season at once and some people watching one episode every other week. This opens up for a shared experience over space, the possibility to watch a series at the same pace as other people without being in the same place. Thanks to the Internet, a shared experience can be created within a group of people without them actually knowing each other. ”The window for a shared TV experience is widen over time … during two weeks House of cards season three was a shared experience amongst the viewers even though some people watched all the

episodes the first weekend and some still have not seen them all ” (Interview C). The reason for this is that online communities connect viewers from anywhere in the world with each other. ”The physical TV couch has been affected in multiple ways, … if you are the only Star Trek fan in your home you can find others online with whom it is much more relevant to share the social experience” (Interview D) Since watching video will become more digitalized and online, the evolving social experience will continue to have an impact on how social viewing will be defined. 5.2.3 New business concepts trends In several interviews it was revealed that an important factor for how we are going to consume media in five years is how the market will evolve. As the technology develops and consumer demand is changing the market is opening up for new opportunities. The increased complexity on the market is affecting the consumers. ”Almost everybody has a traditional television but with all the new option it becomes more unusual to sign up on expensive TV packages. The TV landscape is quite complicated, which leads to consumers having a hard time choosing. What is Tivo? What is Apple TV? How do they work? What can I access with a Smart TV?” (Interview F). The plethora of services and options is mostly stimulating but it also leaves the consumers in a perplexing situation. Changing value chain The trend that content providers distribute their own material was touched upon in several interviews. The opinion was that it is especially common online, almost all the TV channels develop comprehensive play channels to be able to distribute their content without going through traditional distributors. “HBO is an example of content that is very desirable. The traditional TV bundles used to “force” consumers to pay for the largest channel package packages just to be able to get hold of that specific content, today you can have HBO Nordic and get access to that content without the other channels” (Interview D). This is a trend that, according to the interviewed, will grow in the future. As more services direct their products directly towards the end-consumer, the media value chain is continuing to transform. A driving idea is to get the consumer to stay within your service without feeling the need to use other services. Actors within the value chain are starting to operate after the motto: “If I, as a media company, provide everything within my universe perhaps nobody need to look outside” (Interview D). The interviews emphasised that collaborations will be of greater importance in the coming years. One example of collaborations that are being made is between TV providers and OTT services who are trying to attract and retain consumers by collaborating and add value. ”It will become increasingly important to create collaborations” (Interview A). Another difference in the value chain that will continue to grow is the trend of producing own content, like Netflix is doing in order to offer the consumers a unique value. “It will take a long

time, if ever before Netflix would sell early access of House of Cards to any other provider” (Interview D). Because of the exclusive rights to own produced material Netflix, and similar providers, can attract subscribers who want access to the specific content they can not access anywhere else. Aggregating services The flourishing market with multiple services and options is becoming more and more complicated, hence several interviews lifted the possibility of a future service aggregator. “The aggregation is still not completely solved. You have two universes, de old managed universe, which basically is everything you can control with your old TV remote. You also have the new universe with a lot of new services distributed via OTT providers such as Netflix or HBO” (Interview D). Since more and more people pay for more than one service [26], the more complicated it is for the consumer to get an overall picture of what exists within each service. ”What the consumers want is the best of those two worlds, all in one easy-to-use experience, but still personalizable and flexible” (Interview D). A common opinion was that the aggregation has a long way to go regarding ease-of-use and availability of compelling content, but trends suggest that this is where the market is heading. 6. DISCUSSION The purpose of this thesis was to study how video consumption will take shape in 2020 by identifying viewing situations based on consumer motives and to identify trends that will affect consumer behaviour. The study is based on two parts. The study resulted in three identified viewing situations; social viewing, engaged viewing and background viewing. The relevant trends from the interviews were grouped in three areas; technology, consumer behaviour and new business concepts. Here follows an analysis of how the trends can affect consumer behaviour in the identified viewing situations.

6.1 Mapping trends and viewing situations 6.1.1 General effects Technology ought to enable many changes but will probably not be an invincible obstacle for further development. The continuous digitalization and the technology advance are assumed to facilitate the movement between different platforms and services. When you can move more seamlessly between the platforms and screens the television might no longer be viewed as the primary screen and but rather just one of the screens. Which screen you choose will not be as connected to what need state you want to fulfil but rather to what screen that is available in the moment. Since different platforms appeal to different needs, this trend could help consumers to satisfy their needs and fulfil gratifications easier.

If people in a larger extent start to chase content, it will probably result in less loyal customers. According to the interviewed experts, if a media company does not keep up with the advancement in terms of technology, content or price points, the consumers will seek alternative services. Consumers are taking larger control over their media consumption; they want to consume video on their own terms. Forcing restrictions, such as regional access or technological limitations, could also lead to a risk of consumers switching services. It could be difficult to be an omni-platform that provides everything from great TV shows to the latest movies and news programs without aggregating other companies’ material. If an aggregator is successfully created it could give consumers a better overview over their services and existing content. An aggregator could also ensure easy access to all your services from one entry-point. The aggregator could be a base for hybrid viewing, a platform with a single interface that seamlessly integrates linear, catch-up and VOD. If all the content you had access to would be gathered in one platform, it would make the content seem more available. Other trends that could have the same impact are a more precise search functions and better content discovery tools. More tailored recommendations, that combine previous consumption patterns with situational aspects could lead to the consumer perceiving the available content more relevant and fitting for each situation and need. 6.1.2 Social viewing The extended TV sofa ought to help customers connect over distance and time in a larger extent, the social aspect, will not be limited to the same space. The definition of viewing together will, according to this study, expand to include various situations; such as consumers connecting through online platforms like social media and two friends watching a series at the same pace but not in the same space. As the viewing landscape becomes more fragmented, social experiences connected to the program could make people feel like a part of something larger than their living room couch. Via multiscreen storytelling, companies can engage consumers on all platforms and devices, and make people feel more included and connected to each other. One example of that could be a football game; when watching a match, you can bet against other people, look at the after talk, and even re-play the same game on your game console after the match is over. On several of these additional platforms, you have the possibility to connect with other people, either friends or people you do not know. The social viewing will probably become more like an event with storylines tied together. Another thing that affects the social perspective is when people gather in the same space but use different devices. A family could gather together in the sofa, but instead of everybody watching the same program their attention is directed towards different content. The content they engage in could be video while others engage in social media or play games. They still keep each other company

and fulfil the social gratification, while using different screens. When content discovery tools become more intelligent, they can also include a social aspect, where users can share and take part of others favourites, no matter platform. Social recommendations can make you feel more connected to friends both in the sense that you are watching the same content but also because it make ground for conversation. This study suggests that you will be able to share a social experience and feel connected to friends or even celebrities who share their personal favourites. 6.1.3 Engaged viewing More personalized experiences and tailored recommendations are especially important when coming to the state of indulgence or escapism. When seeking to satisfy these gratifications it is all about “me-time” and therefore especially important to view your personal favourites. One aspect of this is that TV and video subscriptions are assumed to evolve and focus more on the individual, by going from household-based accounts to individual-based accounts. This will help consumers organize and keep track of their personal favourites. The multiscreen trend, ought to facilitate the personal viewing situations, it could make the “me-time” more accessible no matter the situation, when all content exists on all platforms. The larger amount of content and the growing trend to binge watch could lead to people being more selective when choosing what to watch. A consequence could be that people follow fewer TV shows but really devour in their favourite show, watching multiple episodes back-to-back. This will probably prolong the engaged viewing sessions. 6.1.4 Background viewing The viewing behaviour with the motive of relaxing or routine viewing is assumed to persist fairly similar as today. The reason for this is that linear television is well equipped to satisfy the need of casual and passive viewing. People understand what types of programs that are broadcasted during a specific time on different channels. This is one of the reasons why linear TV excels to meet the needs when the goal is to unwind when coming home from work. If the advanced search and content discovery tools can bring the same simplicity to VOD platforms, it would give consumers an alternative source to satisfy the same need state. Some people do not want to pick and choose and if they are not in the mood for the shows broadcasted, VOD could generate a playlist from their favourite VOD shows. Better content recommendations could eliminate the browsing process and make VOD to a convenient platform for this viewing situation. This could lead to consumers who seek a relaxing video experience firstly rely on recommendation engines rather than relying on broadcasted program blocks. But even if VOD services advance to better gratify background viewing, people are set in their habits

hence it will probably take time until the behaviour is fully embraced. 6.2 Choice of method As mentioned in the beginning of this paper the exact future is impossible to determine. There are a lot of actors within the television industry and there are many different views of how the future will take shape. The chosen method aims to gather an overall picture by compiling the distinctive approaches to get a picture of what the video consumption can look like in 2020. Since the future is uncertain, interviewing other actors could have lead to a slightly different result. However, the final trends did reappear in several interviews and were singled out on frequency, therefore would a change in interviewed companies probably not vary the result in a large extent. One aspect regarding the execution of the method that has to be considered is the choice of interviewees. Eight companies were interviewed within the areas; TV-providers and VOD services, Technology providers, Broadcasting companies and media strategy companies. The spread of companies helped to gather different perspectives but was unfavourable in the sense that the result within each area was not generalizable for the whole market. Another aspect is that the interviews only were conducted with one person from each company, the trends could have been more thoroughly investigated, if several persons within the same organization were interviewed. However, the information gathered was sufficient enough to get reliable trends. Eight interviews resulted in a good amount of data and the discussed trends were recurring in many of the interviews. The potential effect the trends can have on each viewing situation was interpreted by the writer, if someone else would have done the analysis the material might have been interpreted differently. Nonetheless, several of the expected effects can be identified in literature [3] [27] [28], which to some extent ensures the relevance. The purpose to investigate how viewing behaviour could appear in 2020 has been accomplished, nevertheless there are several more perspectives that were not included in this thesis and could be subject for further research. 6.3 Future research To further verify the result of this thesis, a study that confirms the identified viewing situations could be of interest. This study has not included the consumers, who are of high interest, thus it would be interesting to do a qualitative and a quantitative study with consumers, to determine their viewing habits and make the results generalizable. In this thesis the legislation and other restrictions were not considered, but during the interviews it was repeatedly brought up as an important factor of how the TV industry will change. Therefor it would be essential to research how media legislation is developing and how it affects the industry.

7. CONCLUSION In the thesis it has been examined how consumer behaviour could evolve until 2020. The result showed that broadcasted linear television probably will continue to remain an important part of video consumption even though the usage of OTT services ought to increase. Broadcasted television is expected to be used for background viewing and for live events in a larger extent than today, while VOD is assumed to approach a role as a customizable service that satisfy personal needs. The consumer behaviour will probably evolve the most in the social viewing situation, the reason for that is firstly because the definition of social television is extending. Secondly, because the technology advance will help us feel connected both over space and time. Another aspect that is expected to be an important factor in 2020 is the engaged viewing behaviour. People ought to be more prone to binge watch their favourite shows, which could make the engaged viewing a larger part of their total video consumption. The viewing behaviour in the background viewing situation, will probably not change fundamentally in the next five years. Mainly since it is a routine behaviour that is deeply rooted in linear television. Another reason is the importance of simplicity; the background viewing situation is characterized by few choices and ease-of-use. Even if VOD services could evolve to better satisfy the need to unwind and relax, people are habit creatures and it would take time until the mass have adopted this behaviour. Many of the identified trends are likely to evolve in the predicted direction, even so there are several unforeseeable uncertainties, that could alter the future of consumer behaviour.

8. REFERENCES

[1] O. Findahl, “Svenskarna och Internet,” 2014. [Online]. Available: https://www.iis.se/docs/SOI2014.pdf. [Accessed: 15-Mar-2015].

[2] MMS, “TV-året 2014,” 2015. [Online]. Available: http://www.mms.se/wp-content/uploads/_dokument/presentationer/akademi/2015-02-05_MMS_TV-aret_2014.pdf. [Accessed: 17-Mar-2015].

[3] O. Anebygd, “Changing habits - challenge the media industry,” Ericsson Business Review, 2014. [Online]. Available: http://www.ericsson.com/res/thecompany/docs/publications/business-review/2014/screen-test-changing-habits-challenge-the-media-industry.pdf. [Accessed: 02-Mar-2015].

[4] J. Livaditi, K. Vassilopoulou, C. Lougos, and K. Chorianopoulos, “Needs and gratifications for interactive TV implications for designers,” 36th Annu. Hawaii Int. Conf. Syst. Sci. 2003. Proc., 2003.

[5] Ericsson, “Media Vision 2020 - A vision of the Television Future,” 2014. [Online]. Available: http://www.ericsson.com/televisionary/static/pdf/MediaVision-Brochure-RevA.pdf. [Accessed: 03-Mar-2015].

[6] Ernst & Young, “TV-marknaden i Sverige,” 2009. [Online]. Available: http://www.kkv.se/upload/Filer/Trycksaker/Rapporter/rap_2009-4_ernst-young.pdf. [Accessed: 08-Feb-2015].

[7] MMS, “MMS SVOD-topp Q4 2014: Netflix ökade med 600 000 personer jämfört med förra året,” 2015. [Online]. Available: http://www.mms.se/2015/02/05/mms-svod-topp-q4-2014-netflix-okade-med-600-000-personer-jamfort-med-forra-aret/. [Accessed: 18-Mar-2015].

[8] K. Mercer, A. May, and V. Mitchel, “Designing for video: Investigating the contextual cues within viewing situations,” Pers. Ubiquitous Comput., vol. 18, no. 3, pp. 723–735, 2014.

[9] V. a Thurmond, “The point of triangulation.,” J. Nurs. Scholarsh., vol. 33, no. 3, pp. 253–258, 2001.

[10] Y. Rogers, H. Sharp, and J. Preece, Interaction design: beyond human-computer interaction. John Wiley & Sons, 2011.

[11] A. M. Rubin, “Television uses and gratifications: The interactions of viewing patterns and motivations,” J. Broadcast., vol. 27, no. 1, pp. 37–51, 1983.

[12] P. Palmgren, L. A. Wenner, and J. Rayburn, “Relations between gratifications sought and obtained - A Study of Television News,” Communic. Res., vol. 7, no. 2, pp. 161–192, 1980.

[13] C. A. Lin, “Standpoint: Looking back: The contribution of Blumler and Katz’s uses of mass communication to communication research,” J. Broadcast. Electron. Media, vol. 40, no. 4, pp. 574–581, 1996.

[14] E. Katz, J. G. Blumler, and M. Gurevitch, “American Association for Public Opinion Research,” vol. 37, no. 4, pp. 509–523, 1973.

[15] D. McQuail, J. Blumler, and J. Brown, The television audience: A revised perspective. London: Sociology of Mass Communication., 1972.

[16] D. McQuail, Mass Communication Theory, 6th ed. London: SAGE, 2010.

[17] R. Cooper and T. Tang, “Predicting Audience Exposure to Television in Today’s Media Environment: An Empirical Integration of Active-Audience and Structural Theories,” J. Broadcast. Electron. Media, vol. 53, no. 3, pp. 400–418, 2009.

[18] E. Consumerlab, “TV & Video - Consumer Trends,” 2011. [Online]. Available: http://www.ericsson.com/news/111014_consumerlab_244188808_c?query=tv+habits. [Accessed: 05-Feb-2015].

[19] MMS, “Ordbok,” 2013. [Online]. Available: http://www.mms.se/start/vara-tjanster/ordbok/. [Accessed: 06-May-2015].

[20] E. Consumerlab, “TV and Media - Identifying the needs of tomorrow’s video consumers,” 2013. [Online]. Available: http://www.ericsson.com/res/docs/2013/consumerlab/tv-and-media-consumerlab2013.pdf. [Accessed: 03-Feb-2015].

[21] J. Bjur, “SECOND SCREEN & HYBRID VIEWING,” 2014. [Online]. Available: http://www.tv-nyheterna.se/upload/termin/pdf/pres181.pdf. [Accessed: 18-Mar-2015].

[22] Thinkbox, “Screen Life : TV in Demand,” 2013. [Online]. Available: http://www.thinkbox.tv/research/screen-life-tv-in-demand-summary/. [Accessed: 05-Feb-2015].

[23] E. Consumerlab, “TV and Media - Changing consumer needs are creating a new media landscape,” 2014. [Online]. Available: http://www.ericsson.com/res/docs/2014/consumerlab/tv-media-2014-ericsson-consumerlab.pdf. [Accessed: 05-Feb-2015].

[24] S. Ng, “A brief history of entertainment technologies,” Proc. IEEE, vol. 100, no. SPL CONTENT, pp. 1386–1390, 2012.

[25] Ericsson, “Growing the digital economy The Market Supply failure of lawful digital content,” 2011. [Online]. Available: http://digital.org.au/sites/digital.org.au/files/2_ Rene_ADA March 9 2012 Ericsson_Rene.pdf. [Accessed: 12-Mar-2015].

[26] Mediavision, “Hushållen betalar allt mer för streamingtjänster via internet,” 2014. [Online]. Available: http://www.mediavision.se/wp-content/uploads/2014/12/Pressrelease-december-2014-SV3.pdf. [Accessed: 16-Mar-2015].

[27] EY, “Future of Television,” 2013. [Online]. Available: http://www.ey.com/Publication/vwLUAssets/EY_6_trends_that_will_change_the_TV_industry/$FILE/EY-6-trends-that-will-change-the-TV-industry.pdf. [Accessed: 14-Mar-2015].

[28] G. Gimpel, “Five pressing issues shaping the future of TV & video,” 2013. [Online]. Available: http://ebusiness.mit.edu/research/papers/2013.05_Gimpel_Five Pressing Issues Shaping the Future of TV Video.pdf. [Accessed: 03-Feb-2015].

[29] B. S. Greenberg, “Gratifications of television viewing and their correlates for British children,” uses mass Commun. Curr. Perspect. gratifications Res., vol. 3, pp. 71–92, 1974.

[30] A. M. Rubin, “Television uses and gratifications: The interactions of viewing patterns and motivations,” J. Broadcast. Electron. Media, vol. 27, no. 1, pp. 37–51, 1983.

[31] W. Schramm, Television in the lives of our children. Stanford University Press, 1961.

[32] B. Lee and R. S. Lee, “How and why people watch TV: Implications for the future of interactive television,” J. Advert. Res., vol. 35, no. 6, pp. 9–18, 1995.

[33] J. Lull, “The social uses of television,” Hum. Commun. Res., vol. 6, no. 3, pp. 197–209, 1980.

[34] E. Katz, H. Haas, and M. Gurevitch, “On the Use of the Mass Media for Important things,” Am. Sociol. Rev., vol. 38, no. 2, pp. 164–181, 1973.

[35] Mediavision, “Svensk streamingmarknad miljardindustri under 2014,” 2014. [Online]. Available: http://www.mediavision.se/wp-content/uploads/2014/05/Pressrelease-Svensk-streamingmarknad-201405051.pdf. [Accessed: 16-Mar-2015].

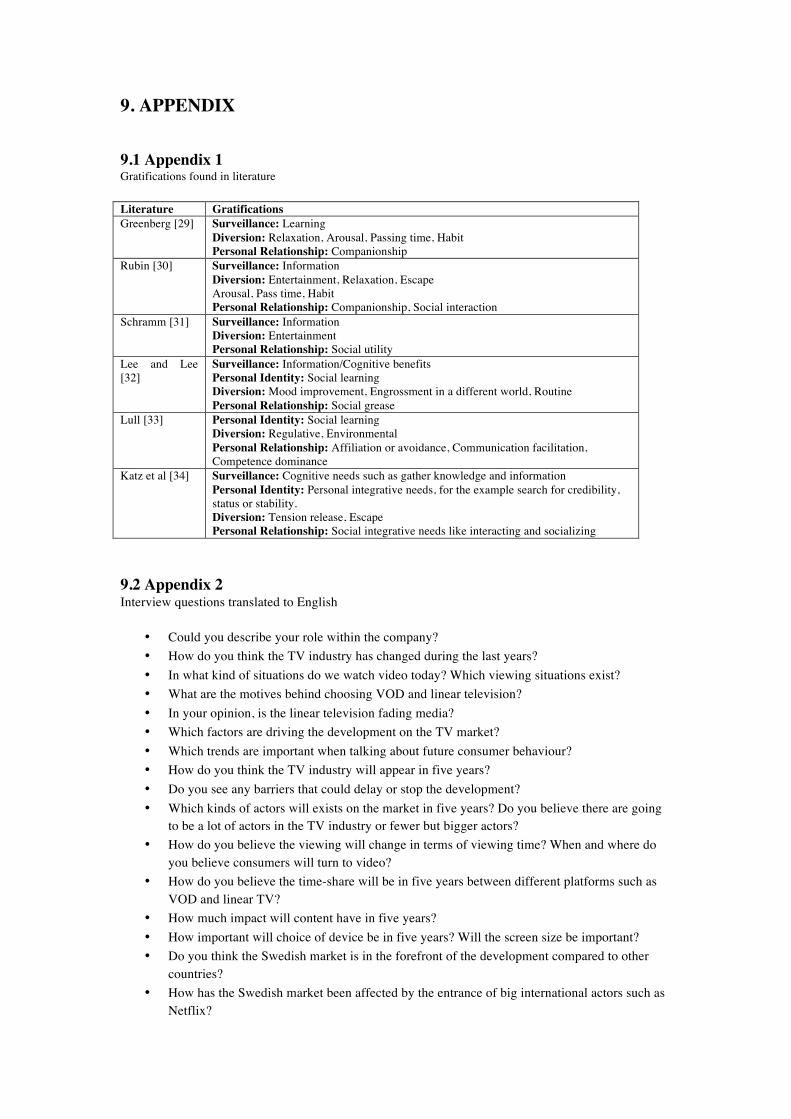

9. APPENDIX 9.1 Appendix 1 Gratifications found in literature Literature Gratifications Greenberg [29] Surveillance: Learning

Diversion: Relaxation, Arousal, Passing time, Habit Personal Relationship: Companionship

Rubin [30] Surveillance: Information Diversion: Entertainment, Relaxation, Escape Arousal, Pass time, Habit Personal Relationship: Companionship, Social interaction

Schramm [31] Surveillance: Information Diversion: Entertainment Personal Relationship: Social utility

Lee and Lee [32]

Surveillance: Information/Cognitive benefits Personal Identity: Social learning Diversion: Mood improvement, Engrossment in a different world, Routine Personal Relationship: Social grease

Lull [33] Personal Identity: Social learning Diversion: Regulative, Environmental Personal Relationship: Affiliation or avoidance, Communication facilitation, Competence dominance

Katz et al [34] Surveillance: Cognitive needs such as gather knowledge and information Personal Identity: Personal integrative needs, for the example search for credibility, status or stability. Diversion: Tension release, Escape Personal Relationship: Social integrative needs like interacting and socializing

9.2 Appendix 2 Interview questions translated to English

• Could you describe your role within the company? • How do you think the TV industry has changed during the last years? • In what kind of situations do we watch video today? Which viewing situations exist? • What are the motives behind choosing VOD and linear television? • In your opinion, is the linear television fading media? • Which factors are driving the development on the TV market? • Which trends are important when talking about future consumer behaviour? • How do you think the TV industry will appear in five years? • Do you see any barriers that could delay or stop the development? • Which kinds of actors will exists on the market in five years? Do you believe there are going

to be a lot of actors in the TV industry or fewer but bigger actors? • How do you believe the viewing will change in terms of viewing time? When and where do

you believe consumers will turn to video? • How do you believe the time-share will be in five years between different platforms such as

VOD and linear TV? • How much impact will content have in five years? • How important will choice of device be in five years? Will the screen size be important? • Do you think the Swedish market is in the forefront of the development compared to other

countries? • How has the Swedish market been affected by the entrance of big international actors such as

Netflix?

www.kth.se