vic campbell senior vice president milton johnson svp and controller mark kimbrough vp, investor...

TRANSCRIPT

Vic CampbellSenior Vice President

Milton JohnsonSVP and Controller

Mark KimbroughVP, Investor Relations

Banc of America – May 2004

2

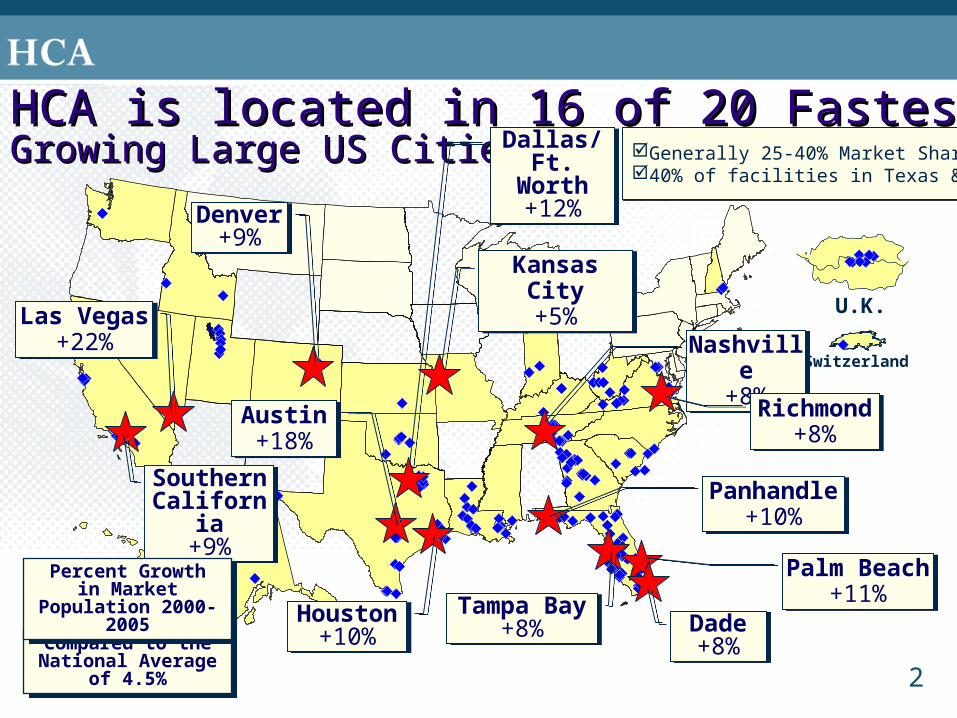

HCA is located in 16 of 20 Fastest HCA is located in 16 of 20 Fastest Growing Large US CitiesGrowing Large US Cities

Switzerland

U.K.

%%

%

%%%

Compared to the National Average of

4.5%

Compared to the National Average of

4.5%

Las Vegas+22%

Las Vegas+22%

Southern California

+9%

Southern California

+9%

Denver+9%

Denver+9%

Dade+8%

Dade+8%

Nashville+8%

Nashville+8%

Panhandle+10%

Panhandle+10%

Tampa Bay+8%

Tampa Bay+8%

Dallas/Ft. Worth+12%

Dallas/Ft. Worth+12%

Austin+18%

Austin+18%

Richmond+8%

Richmond+8%

Palm Beach+11%

Palm Beach+11%

Houston+10%

Houston+10%

Kansas City+5%

Kansas City+5%

Percent Growth in Market Population

2000-2005

Percent Growth in Market Population

2000-2005

Generally 25-40% Market Share40% of facilities in Texas & Florida

Generally 25-40% Market Share40% of facilities in Texas & Florida

3

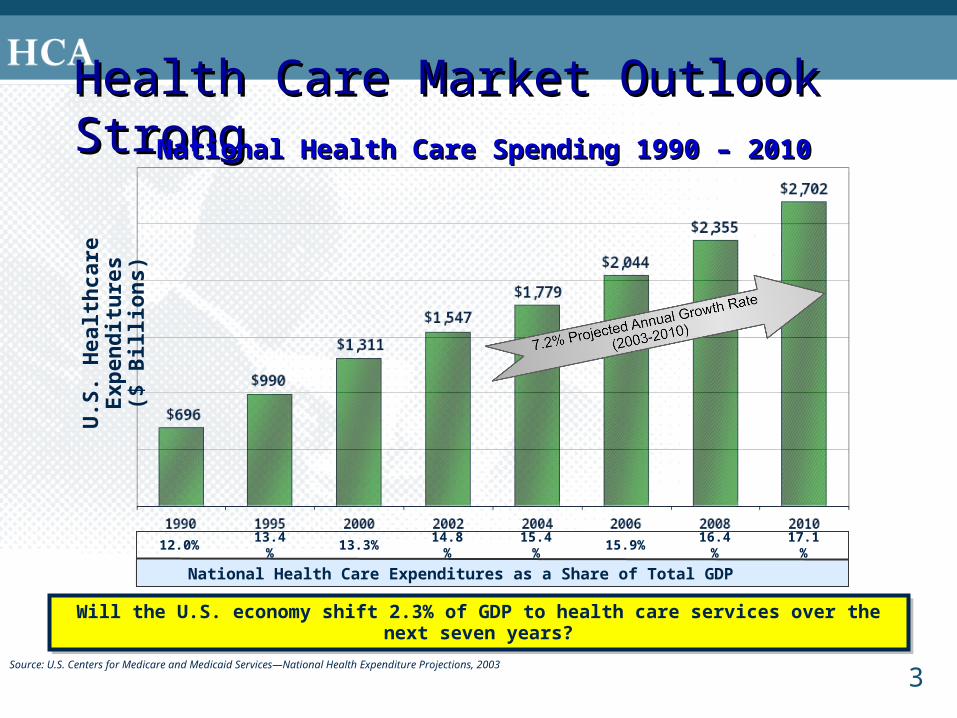

Health Care Market Outlook StrongHealth Care Market Outlook StrongU

.S. H

ealt

hca

re E

xpen

dit

ure

s($

Bill

ion

s)

National Health Care Spending 1990 – 2010National Health Care Spending 1990 – 2010

National Health Care Expenditures as a Share of Total GDP

12.0%13.4%

13.3% 14.8% 15.4% 15.9% 16.4% 17.1%

Source: U.S. Centers for Medicare and Medicaid Services—National Health Expenditure Projections, 2003

Will the U.S. economy shift 2.3% of GDP to health care services over the next seven years?Will the U.S. economy shift 2.3% of GDP to health care services over the next seven years?

4

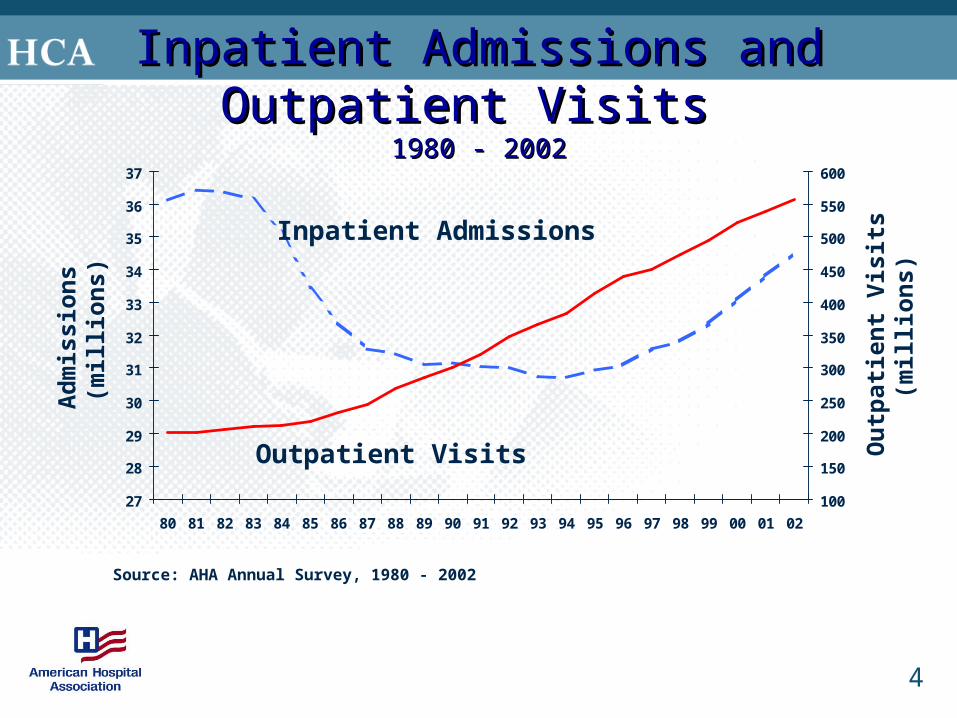

Source: AHA Annual Survey, 1980 - 2002

27

28

29

30

31

32

33

34

35

36

37

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02

100

150

200

250

300

350

400

450

500

550

600

Outpatient Visits

Inpatient Admissions

Ad

mis

sio

ns

(mil

lio

ns)

Ou

tpat

ien

t V

isit

s (m

illi

on

s)

Inpatient Admissions and Outpatient Visits Inpatient Admissions and Outpatient Visits 1980 - 20021980 - 2002

5

-1.0%

1.0%

3.0%

5.0%

7.0%

1Q 00 2Q 00 3Q 00 4Q 00 1Q 01 2Q 01 3Q 01 4Q 01 1Q 02 2Q 02 3Q 02 4Q 02 1Q 03 2Q03 3Q03 4Q03 1Q04

Admissions Rolling 12 mo. Avg

HCA Admission Trends 2001 to 1Q 2004HCA Admission Trends 2001 to 1Q 2004Same FacilitySame Facility

6.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

HCAMarket

Competitors

15.4%

HCA Growing Medicare Market Share

Growth in Medicare Admissions 1998-2001

HCA Growing Medicare Market Share

Growth in Medicare Admissions 1998-2001

6

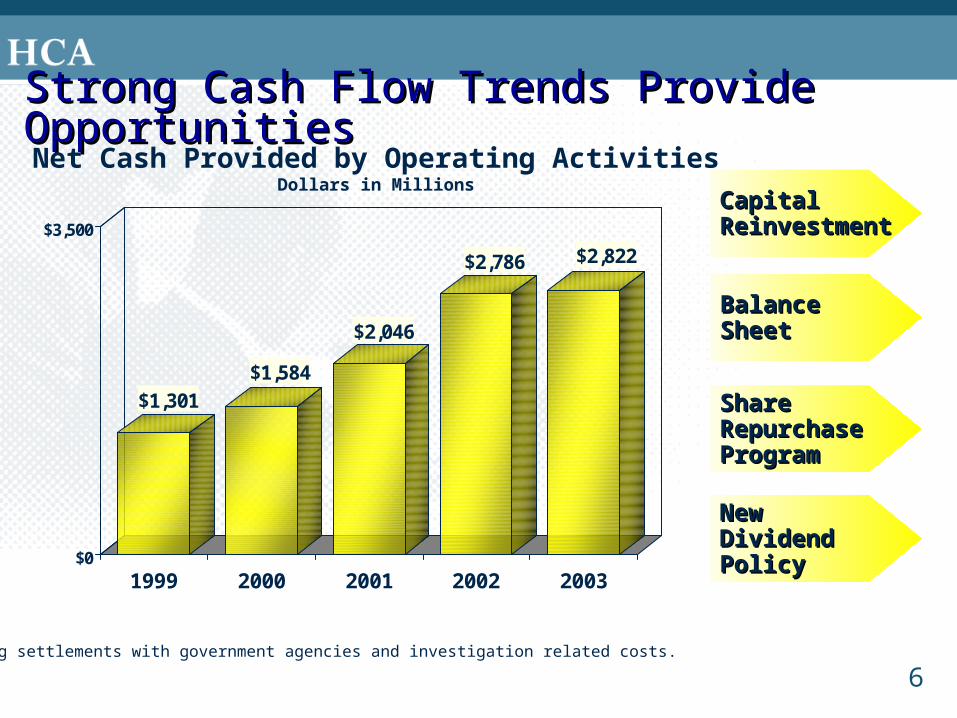

Strong Cash Flow Trends Provide OpportunitiesStrong Cash Flow Trends Provide Opportunities

$1,301

$1,584

$2,046

$2,786 $2,822

$0

$3,500

1999 2000 2001 2002 2003

Net Cash Provided by Operating ActivitiesDollars in Millions

Excluding settlements with government agencies and investigation related costs.

New New Dividend PolicyDividend Policy

Share Share Repurchase Repurchase ProgramProgram

Capital Capital ReinvestmentReinvestment

BalanceBalanceSheetSheet

7

HCA Capital ExpendituresHCA Capital Expenditures

$0.0

$0.5

$1.0

$1.5

$2.0

2000 2001 2002 2003 2004E

Billions 2000

$1.22001

$1.42002

$1.72003

$1.82004E

$1.8

Land & Improvements

14%/$565M

Surgery/Special Units

22%/$870M

Beds14%/$550M

New Facilities10%/$395M

New & Expanded Services

18%/$740M

Replacement Facilities3%/$98M

ER & Outpatient Services19%/$720

1,565 New Beds

54 Facilities with Surgery and/or ICU/CCU expansions

Four New Facilities 378 Beds

Open Heart, ImagingCardiology, Oncology, etc.

37 ERExpansions

37 ERExpansionsDistribution of

Capital Dollars

2002-2005 and Beyond

Distribution of Capital Dollars

2002-2005 and Beyond

New Denver FacilityNew Denver Facility

NewHospitals

Expansions

Routine

PatientSafety

Infra-

structure

8

$7.3 Billion$7.3 Billion

244 Million Shares244 Million Shares

38% of outstanding 38% of outstanding sharesshares

Average Price: Average Price: $30.03$30.03

Opportunities Of Having Strong Cash FlowOpportunities Of Having Strong Cash FlowShare Share repurchase repurchase programprogram

$1.3B: 37.9M Shares1997

1998

1999

2000

2001

20032002

YTD 20041

1: 2004 purchases through 5-6-04 2: Includes other activities affecting share balance (stock option exercises, restricted grants, and ESPP activity).

$33.59/share$22.68/share

$930M: 41M Shares

$1.4B: 55.6M Shares $24.61/share$1.3B: 43.5M Shares $28.65/share$706M: 19.2M Shares$706M: 19.2M Shares $36.88/share$1.1B: 31.1M Shares $35.76/share

$422M: 10.0M Shares$42.19/share

650M Shares 12/31/96

465M Shares2 4/30/04

$282M: 6.2M Shares$45.53/share

9

The Genesis of the Bad Debt/Charity Care The Genesis of the Bad Debt/Charity Care IssueIssue

22.222.2%%

23.523.5%%

21.221.2%%

22.222.2%%

17.017.0%%

19.219.2%%

29.729.7%%

23.523.5%%

15.115.1%% 15.415.4%%

19.719.7%%

16.716.7%%20.320.3%%15.415.4%%

19.319.3%%15.915.9%%

16.416.4%%

NationalAverage:15.2% 1

NationalAverage:15.2% 1

18.118.1%%

>20% Uninsured

15-20% Uninsured

<15% Uninsured

25.625.6%%

14.6%

22.822.8%%

HCA is in 14 of the 20 highest uninsured states, with 72% of its hospitals in those states

HCA is in 14 of the 20 highest uninsured states, with 72% of its hospitals in those states

HCAHCAWeightedAverage:22.6% 2

HCAHCAWeightedAverage:22.6% 2

1: U.S. Census Bureau “Health Insurance Coverage in the United States: 2002”.2: Kaiser Commission: Health Ins. Coverage of Nonelderly Adults 2001-2002.

13.1%13.1%

10

A prudent financial strategy that provides for a strong A prudent financial strategy that provides for a strong balance sheet and return of cash to shareholders through balance sheet and return of cash to shareholders through

share repurchase and/or dividendsshare repurchase and/or dividends

Excellent Investment OpportunitiesExcellent Investment Opportunities

Strong Cash FlowsStrong Cash Flows

Excellent Long-Term Earnings Growth OutlookExcellent Long-Term Earnings Growth Outlook

Great AssetsGreat Assets

In Summary We Have….In Summary We Have….