veterans in business forum may 3, 2013 health care reform—next steps presented by: terry k....

TRANSCRIPT

VETERANS IN BUSINESS FORUM

MAY 3, 2013

HEALTH CARE REFORM—NEXT STEPS

Presented by: Terry K. Headley

Past President – NationalAssociation of Insurance &

Financial Advisors

Affordable Care Act

March 23, 2010President Barack Obama signed

the Patient Protection & Affordable Care Act into law

March 30, 2010 Amendments were signed into

law

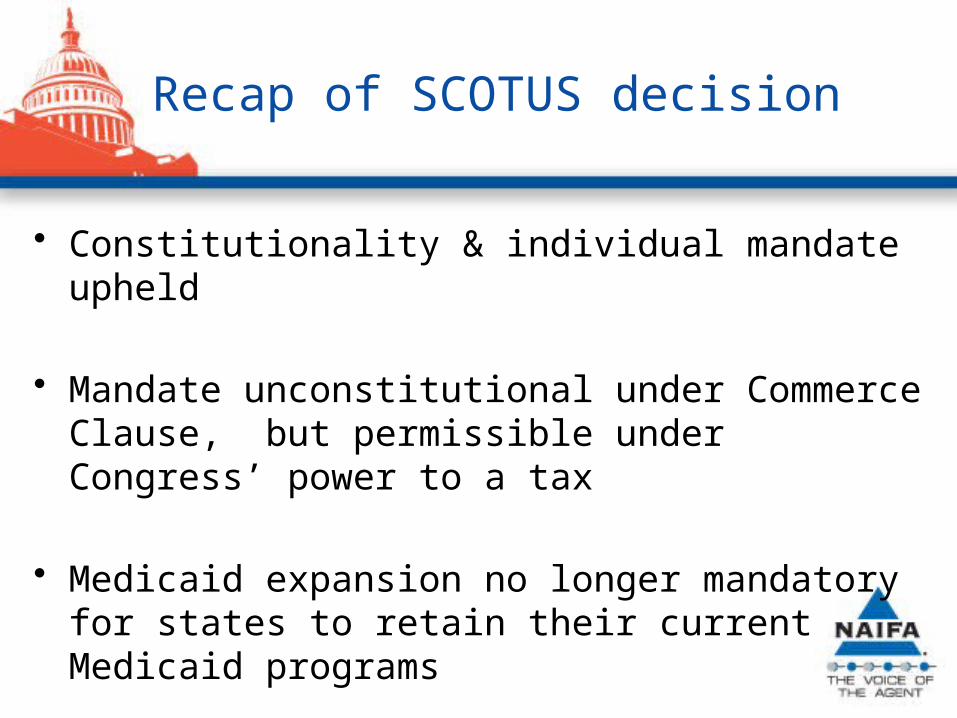

Recap of SCOTUS decision

• Constitutionality & individual mandate upheld

• Mandate unconstitutional under Commerce Clause, but permissible under Congress’ power to a tax

• Medicaid expansion no longer mandatory for states to retain their current Medicaid programs

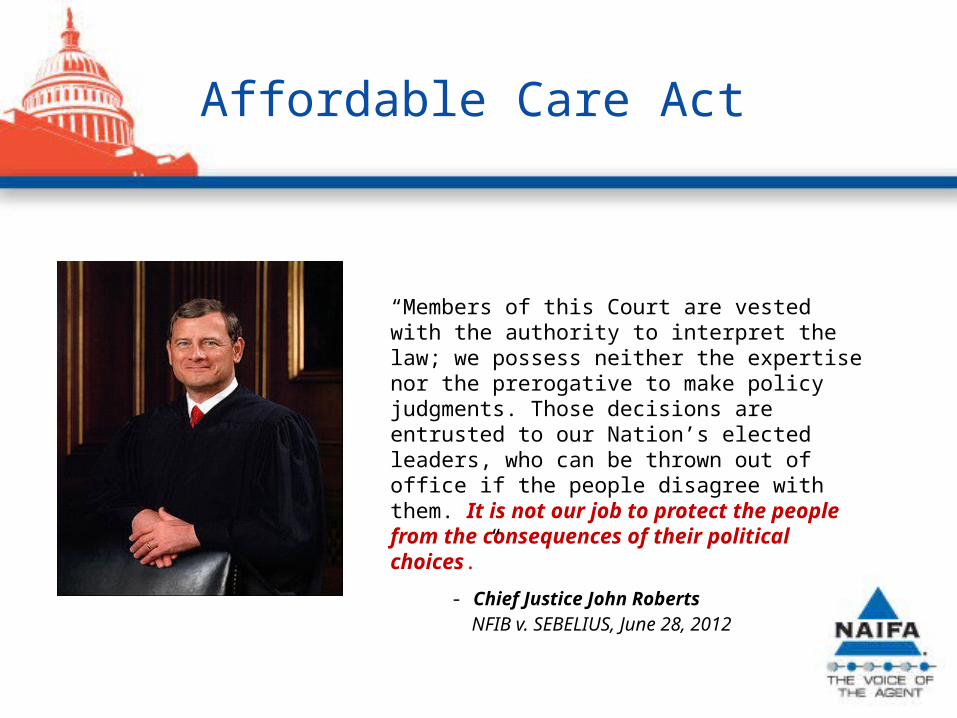

Affordable Care Act

“Members of this Court are vested with the authority to interpret the law; we possess neither the expertise nor the prerogative to make policy judgments. Those decisions are entrusted to our Nation’s elected leaders, who can be thrown out of office if the people disagree with them. It is not our job to protect the people from the consequences of their political choices.”

- Chief Justice John Roberts NFIB v. SEBELIUS, June 28, 2012

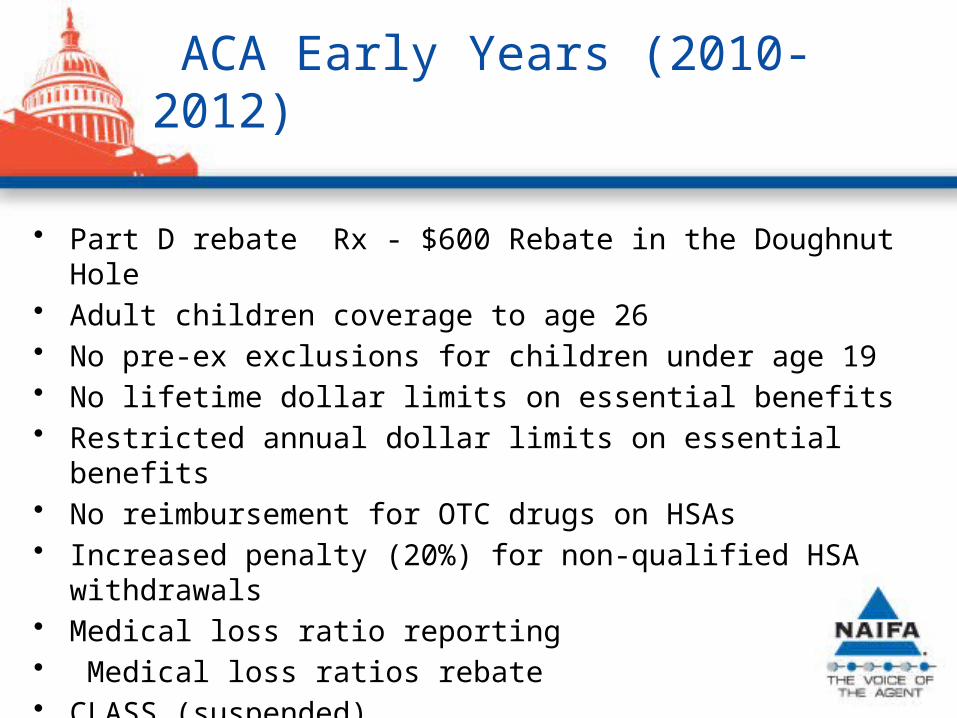

ACA Early Years (2010-2012)

• Part D rebate Rx - $600 Rebate in the Doughnut Hole• Adult children coverage to age 26 • No pre-ex exclusions for children under age 19 • No lifetime dollar limits on essential benefits • Restricted annual dollar limits on essential benefits • No reimbursement for OTC drugs on HSAs • Increased penalty (20%) for non-qualified HSA

withdrawals• Medical loss ratio reporting • Medical loss ratios rebate • CLASS (suspended)

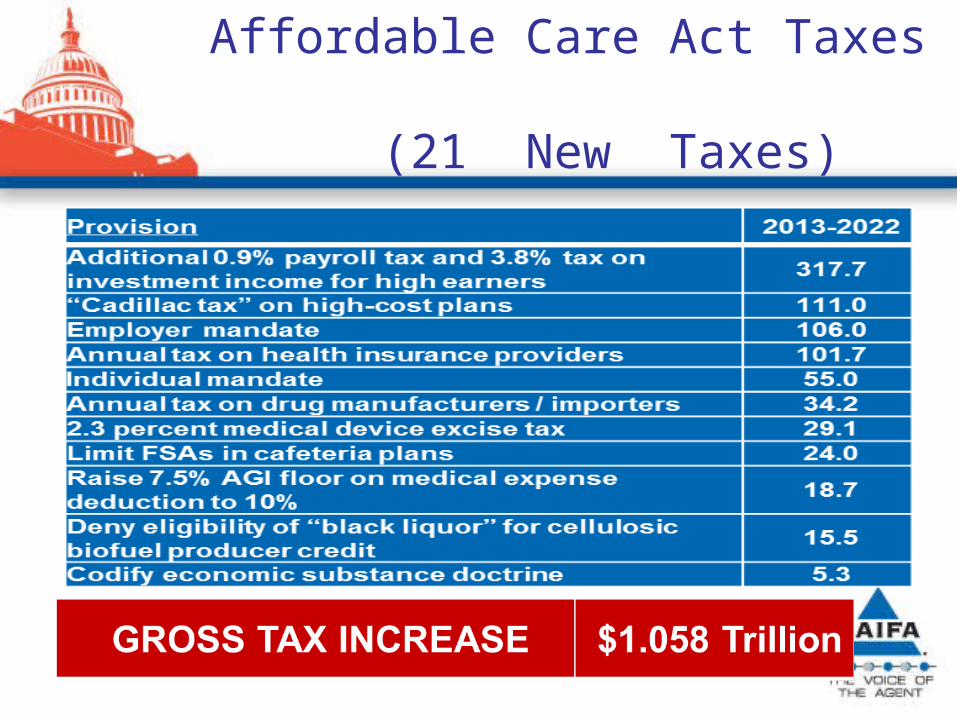

Affordable Care Act Taxes (21 New Taxes)

Affordable Care Act Taxes

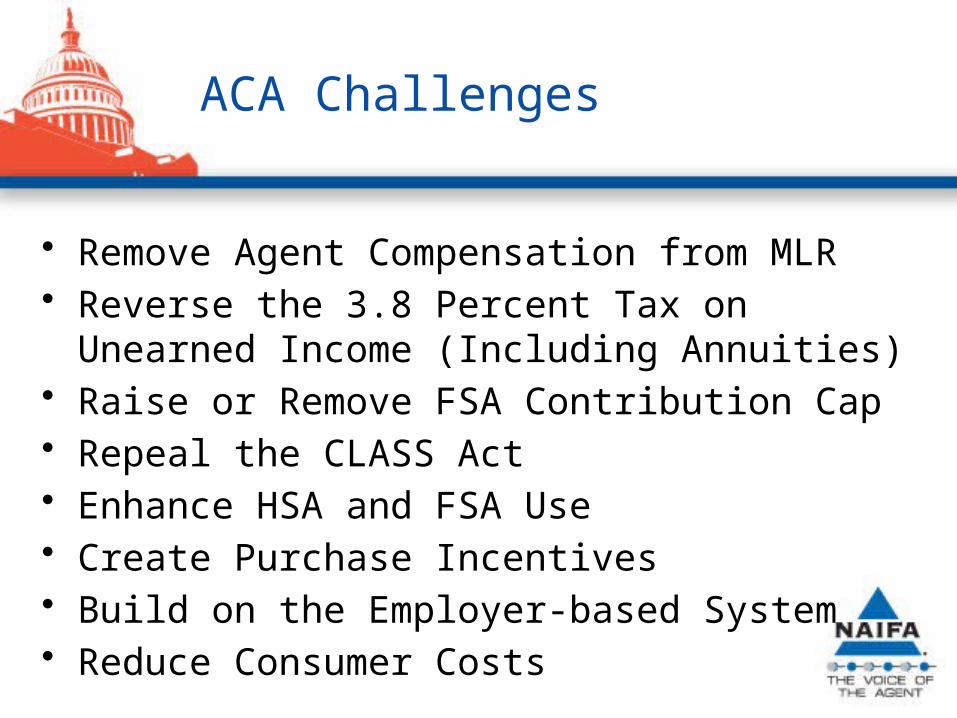

ACA Challenges

• Remove Agent Compensation from MLR • Reverse the 3.8 Percent Tax on Unearned

Income (Including Annuities) • Raise or Remove FSA Contribution Cap• Repeal the CLASS Act • Enhance HSA and FSA Use• Create Purchase Incentives • Build on the Employer-based System • Reduce Consumer Costs

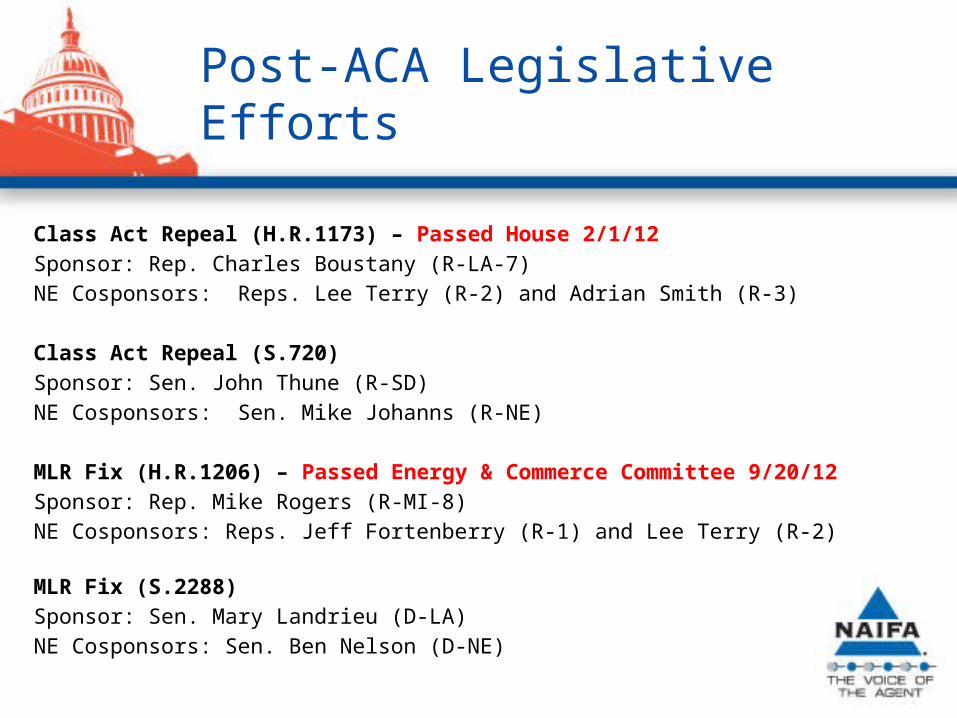

Post-ACA Legislative Efforts

Class Act Repeal (H.R.1173) – Passed House 2/1/12Sponsor: Rep. Charles Boustany (R-LA-7)NE Cosponsors: Reps. Lee Terry (R-2) and Adrian Smith (R-3)

Class Act Repeal (S.720)Sponsor: Sen. John Thune (R-SD)NE Cosponsors: Sen. Mike Johanns (R-NE)

MLR Fix (H.R.1206) – Passed Energy & Commerce Committee 9/20/12Sponsor: Rep. Mike Rogers (R-MI-8)NE Cosponsors: Reps. Jeff Fortenberry (R-1) and Lee Terry (R-2)

MLR Fix (S.2288)Sponsor: Sen. Mary Landrieu (D-LA)NE Cosponsors: Sen. Ben Nelson (D-NE)

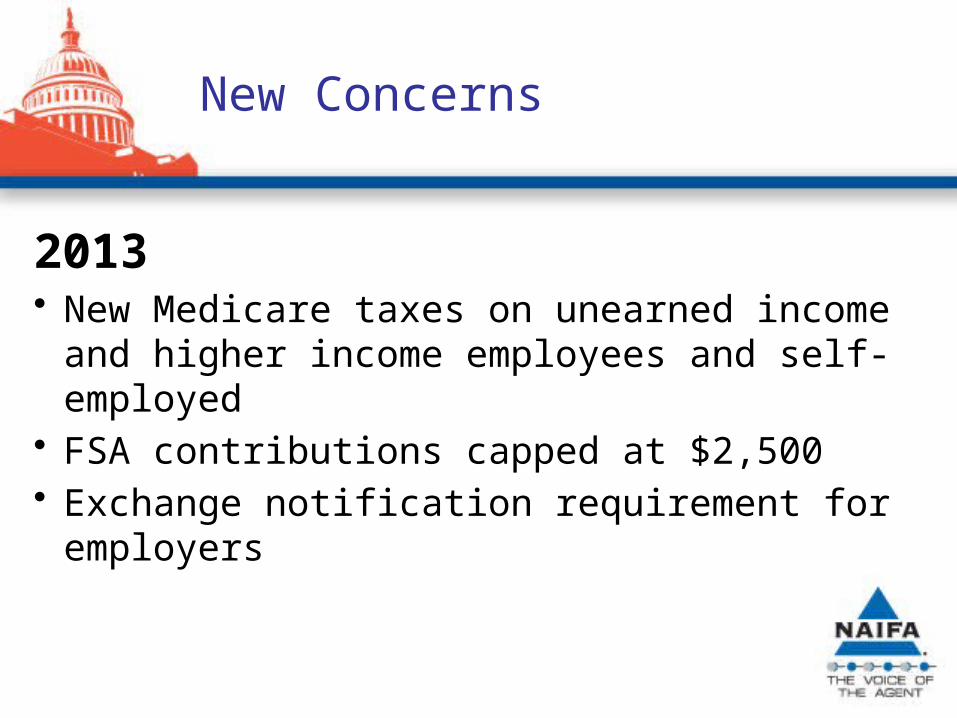

New Concerns

2013 • New Medicare taxes on unearned income and

higher income employees and self-employed• FSA contributions capped at $2,500• Exchange notification requirement for

employers

ACA’s Big Year - 2014

• Individual Mandate• Health Insurance Exchanges• Employer Mandate• Individual market guaranteed issue• Elimination of preexisting condition look-back and

exclusionary periods• Subsides available for qualified individuals

purchasing individual coverage through the exchanges

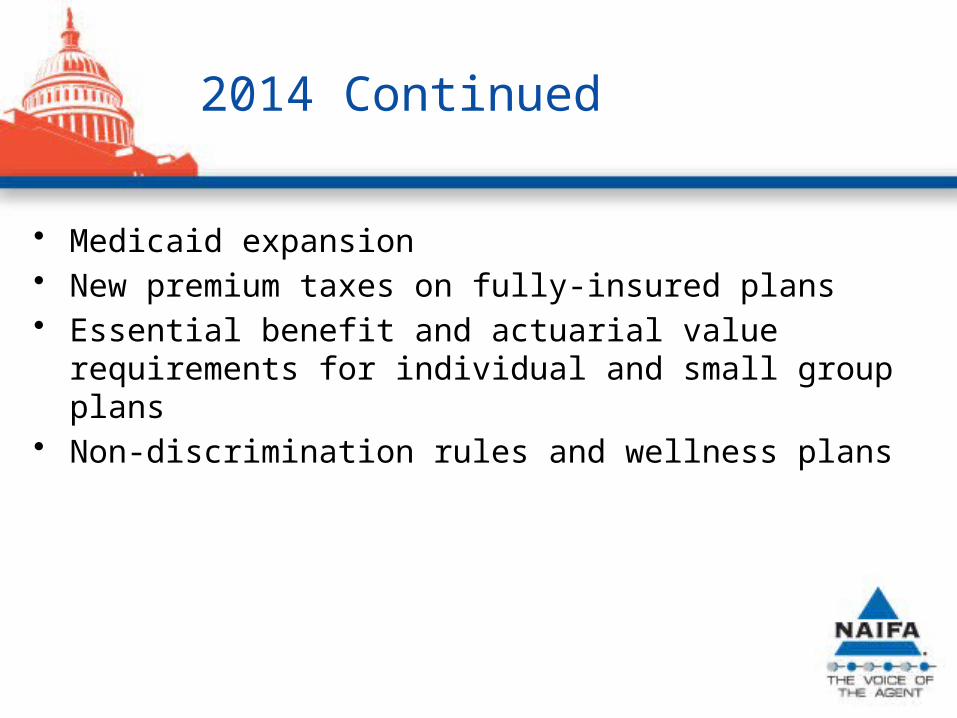

2014 Continued

• Medicaid expansion• New premium taxes on fully-insured plans• Essential benefit and actuarial value requirements

for individual and small group plans• Non-discrimination rules and wellness plans

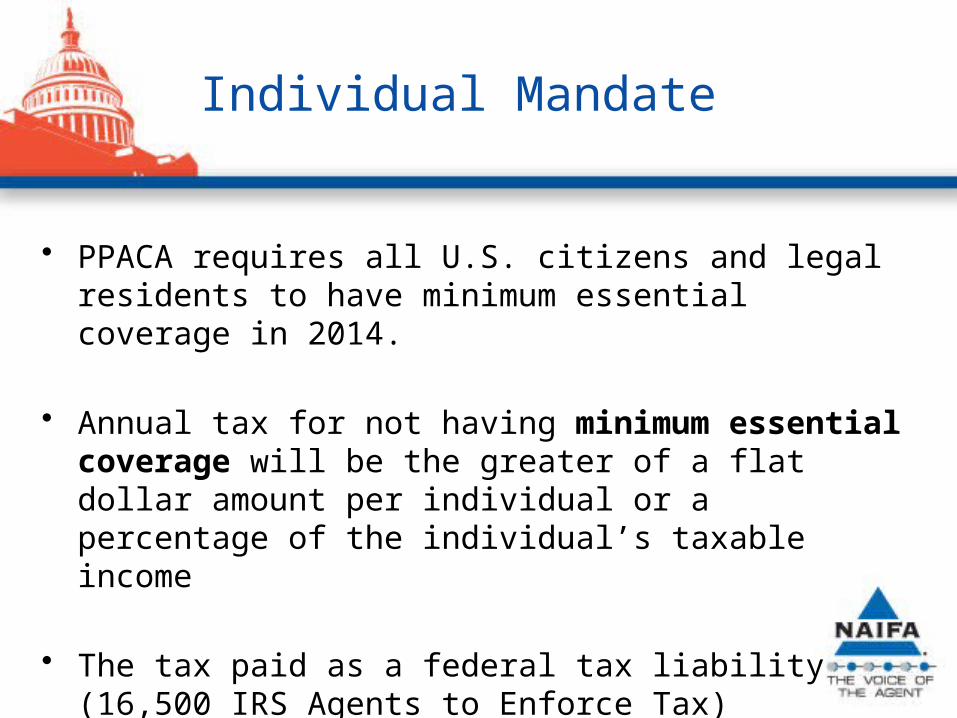

Individual Mandate

• PPACA requires all U.S. citizens and legal residents to have minimum essential coverage in 2014.

• Annual tax for not having minimum essential coverage will be the greater of a flat dollar amount per individual or a percentage of the individual’s taxable income

• The tax paid as a federal tax liability (16,500 IRS Agents to Enforce Tax)

New Premium Tax Credit

• Tax credit available to individuals and families with incomes between 100% and 400% of the federal poverty level

• CBO estimates average credit $5,000 per year

• Credit is generally the difference between the “benchmark plan” (silver level) premium and the taxpayer's “expected contribution”

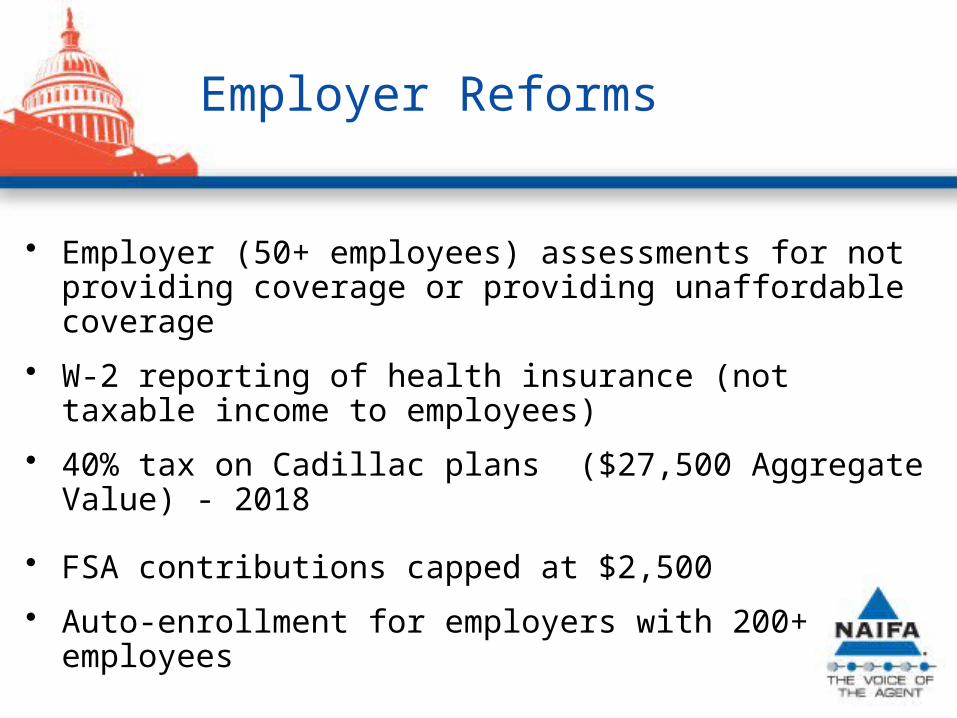

Employer Reforms

• Employer (50+ employees) assessments for not providing coverage or providing unaffordable coverage

• W-2 reporting of health insurance (not taxable income to employees)

• 40% tax on Cadillac plans ($27,500 Aggregate Value) - 2018

• FSA contributions capped at $2,500

• Auto-enrollment for employers with 200+ employees

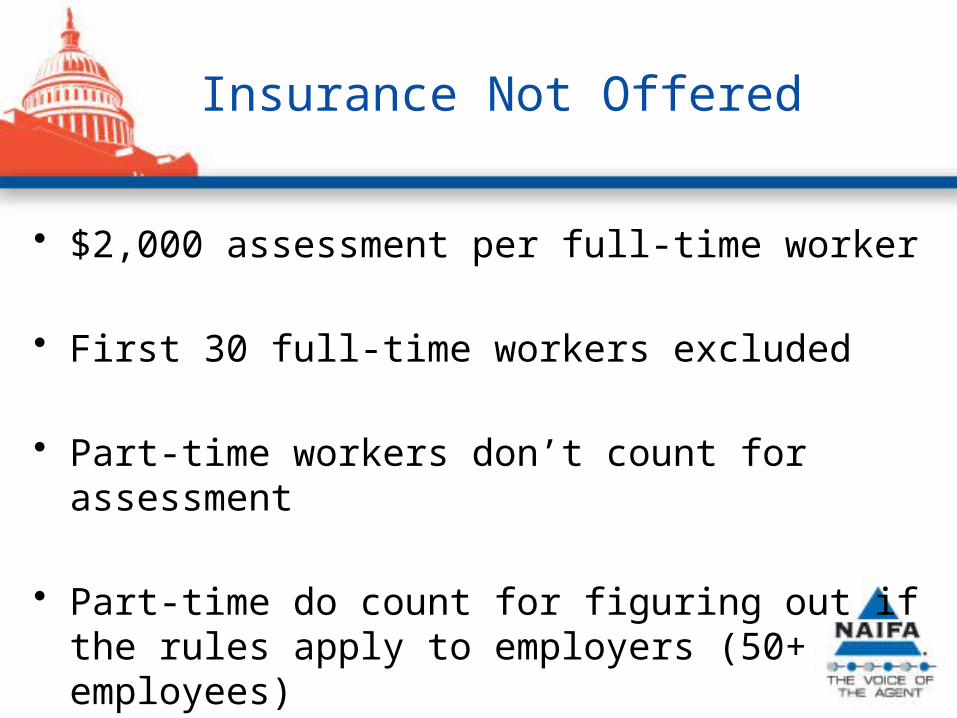

Insurance Not Offered

• $2,000 assessment per full-time worker

• First 30 full-time workers excluded

• Part-time workers don’t count for assessment

• Part-time do count for figuring out if the rules apply to employers (50+ employees)

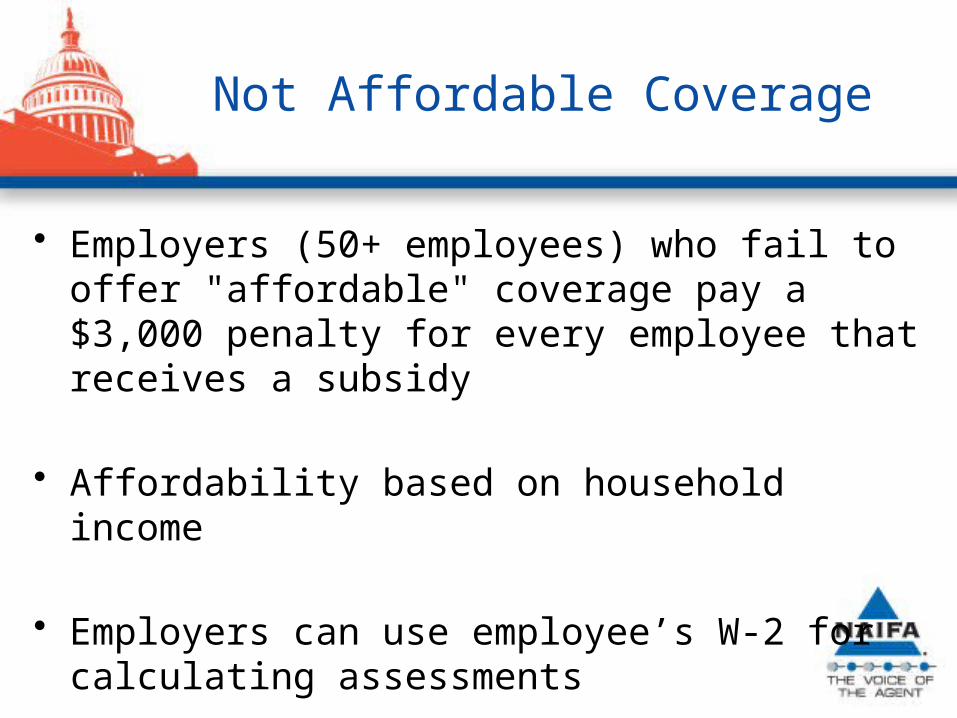

Not Affordable Coverage

• Employers (50+ employees) who fail to offer "affordable" coverage pay a $3,000 penalty for every employee that receives a subsidy

• Affordability based on household income

• Employers can use employee’s W-2 for calculating assessments

Federal Subsidies

• Federal subsidies for low-income individuals buying coverage through state exchanges

• Employer obligation to pay an assessment is contingent on a worker qualifying for a federal subsidy

• Will subsidies exist in federal facilitated exchange?

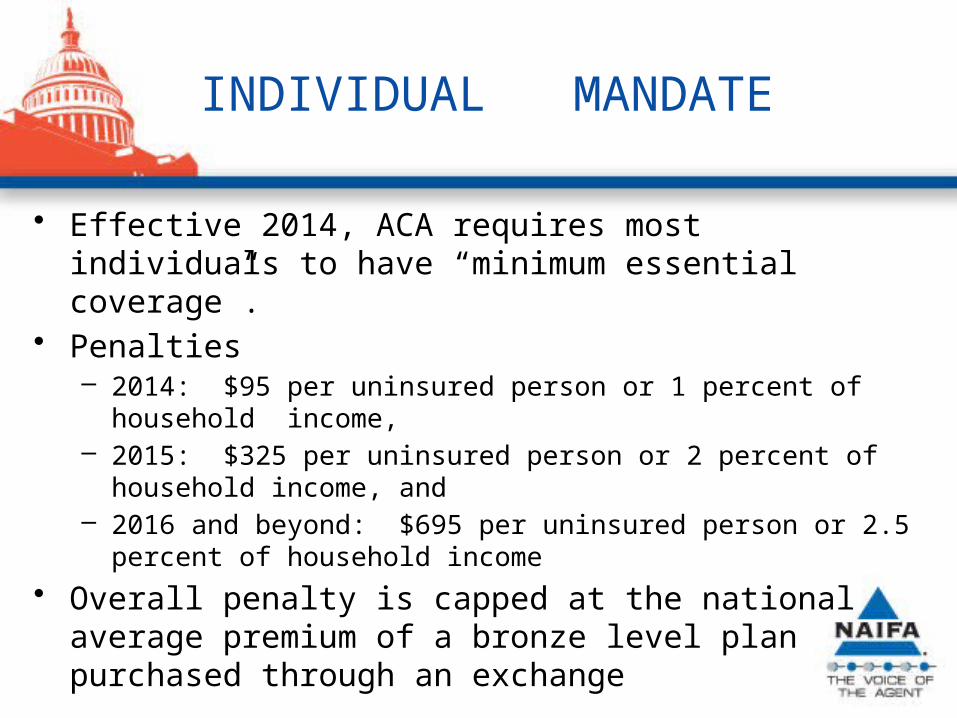

INDIVIDUAL MANDATE

• Effective 2014, ACA requires most individuals to have “minimum essential coverage”.

• Penalties– 2014: $95 per uninsured person or 1 percent of household

income,– 2015: $325 per uninsured person or 2 percent of household

income, and– 2016 and beyond: $695 per uninsured person or 2.5

percent of household income• Overall penalty is capped at the national average

premium of a bronze level plan purchased through an exchange

EMPLOYER SHARE RESPONSIBILITY

General Rules

• Today: Employer can refuse to offer coverage without any federal penalty

• January 1, 2014: Large employers are not required to provide health insurance, but tax applies if full-time employee receives federally-subsidized exchange coverage.– No explicit exclusion for government, church or non-profit

employers• Tax depends on whether “minimum essential

coverage’ was offered to full-time employees (& their dependents – Kids – Adopted & Foster)

Employer “Pay or Play”

• Step 1: Understand the rules• If employer has 50-full-time employees or more (30+

hours/week or 130 hours/month) and offers no coverage, the penalty is $2,000 per employee per year ($166.67 per month) if any employee receives a subsidy in the exchange, minus the first 30 employees.– Part-time employees calculated by taking the

hours worked by a part-time employees in a month divided by 120.

– Seasonal employees not counted if working less than 120 days a calendar year.

Determining Number of Employees

• Step 2: Are you an applicable large employer?

• A large employer is one who employed an average of 50 full-time Equivalent Employees on business days during the preceding calendar year.

• Again, takes into account part-time Employees as “full-time Equivalents”.

Calculating Part-Time Employees

• Only for purposes of determining if “Pay or Play’ applies – do not have to offer coverage to part-time employees

• Hours worked in month divided by120 + FTEs• Example

– A restaurant has 20 part-time employees who all work 24 hours per week or 96 hours per moth.

– These 20 part-time employees would be counted as 16 full-time employees.

– 20 part-time employees “x” 96 hours worked in a month = 1920 divided by 120 hours = 16 full time equivalents.

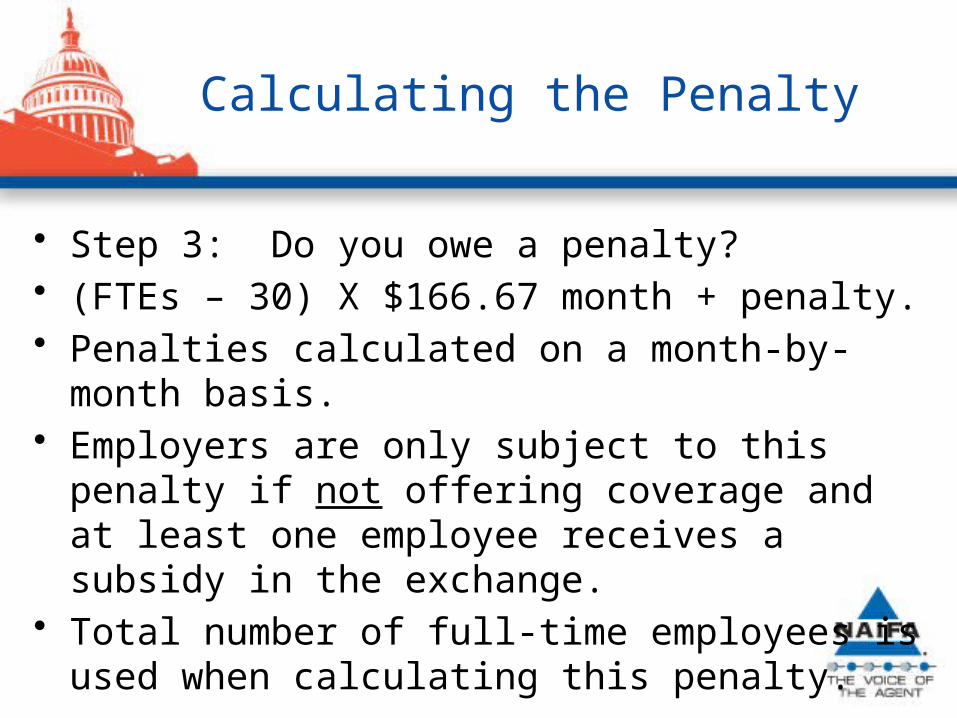

Calculating the Penalty

• Step 3: Do you owe a penalty?• (FTEs – 30) X $166.67 month + penalty.• Penalties calculated on a month-by-month

basis.• Employers are only subject to this penalty if

not offering coverage and at least one employee receives a subsidy in the exchange.

• Total number of full-time employees is used when calculating this penalty.

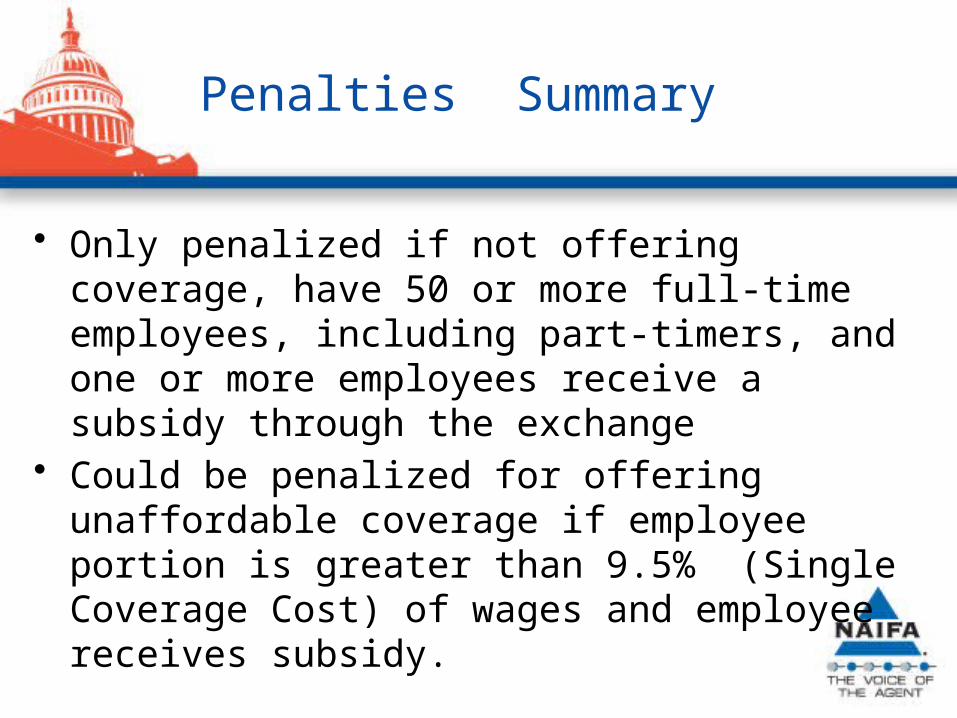

Penalties Summary

• Only penalized if not offering coverage, have 50 or more full-time employees, including part-timers, and one or more employees receive a subsidy through the exchange

• Could be penalized for offering unaffordable coverage if employee portion is greater than 9.5% (Single Coverage Cost) of wages and employee receives subsidy.

Essential Health Benefits

• HHS has not issued formal regulations on the essential health benefits

• States tasked with identifying their own benchmarks plans on which to base essential health benefits

State EHB Benchmark Plans

Nebraska has proposed a benchmark planhttp://www.doi.ne.gov/healthcarereform/exchange/EHB/EHB_letter.pdf

State Exchanges

• On January 1, 2014, states are required to establish health care exchanges.

• If the state fails to establish the exchange, the federal government will step in and run the state exchange.

• Nebraska has opted for Federally-Run

Exchange.

Medicaid Expansion

• Medicaid Expansion creates a new Medicaid group - Newly Eligible Individuals age 19-64 who:– Have income below 133% FPL (138% with a

standard 5% of income disregard)

Annual Fee on Health Insurance Plans

• PPACA will impose a fee on all health insurers based on their market share of net premiums written, which will be effective beginning in 2014.– The fee will not apply to self-insured plans and

federal, state, or other government entities.

• This fee is projected to raise about $60 billion over a 10-year period

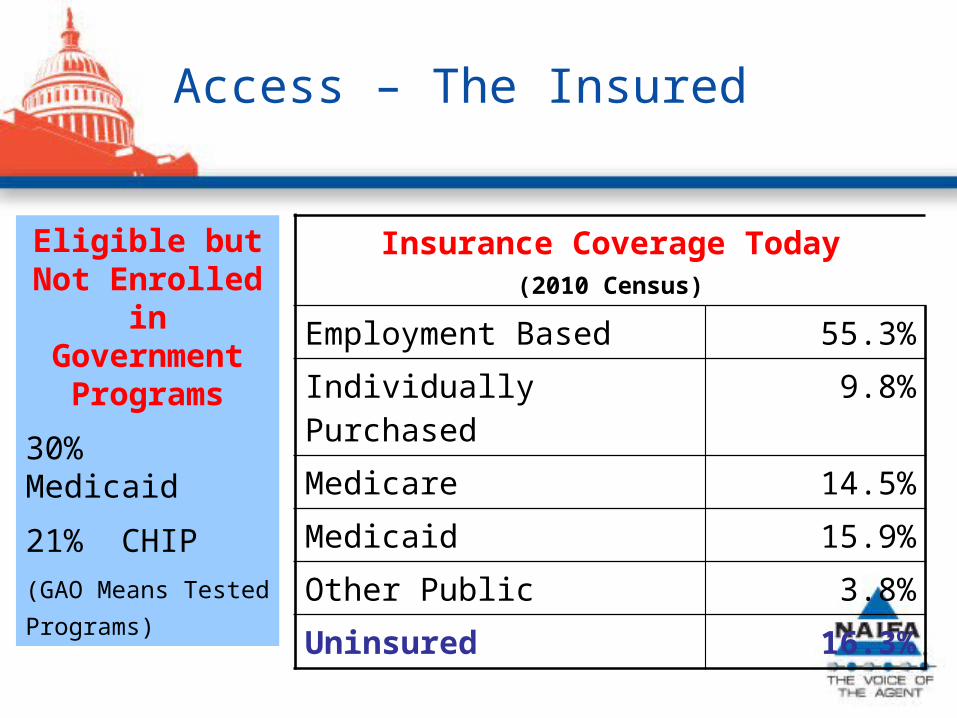

Access – The Insured

Insurance Coverage Today(2010 Census)

Employment Based 55.3%

Individually Purchased 9.8%

Medicare 14.5%

Medicaid 15.9%

Other Public 3.8%

Uninsured 16.3%

Eligible but Not Enrolled in

Government Programs

30% Medicaid

21% CHIP

(GAO Means Tested

Programs)

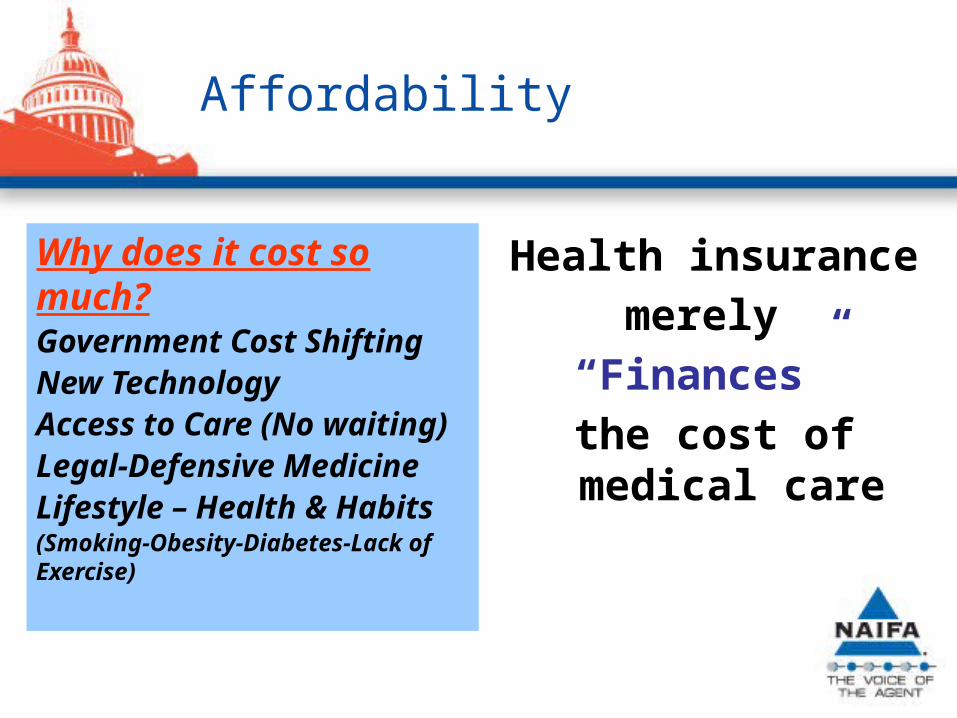

Affordability

Health insurance merely

“Finances” the cost of medical care

Why does it cost so much?Government Cost ShiftingNew TechnologyAccess to Care (No waiting)Legal-Defensive MedicineLifestyle – Health & Habits(Smoking-Obesity-Diabetes-Lack of Exercise)

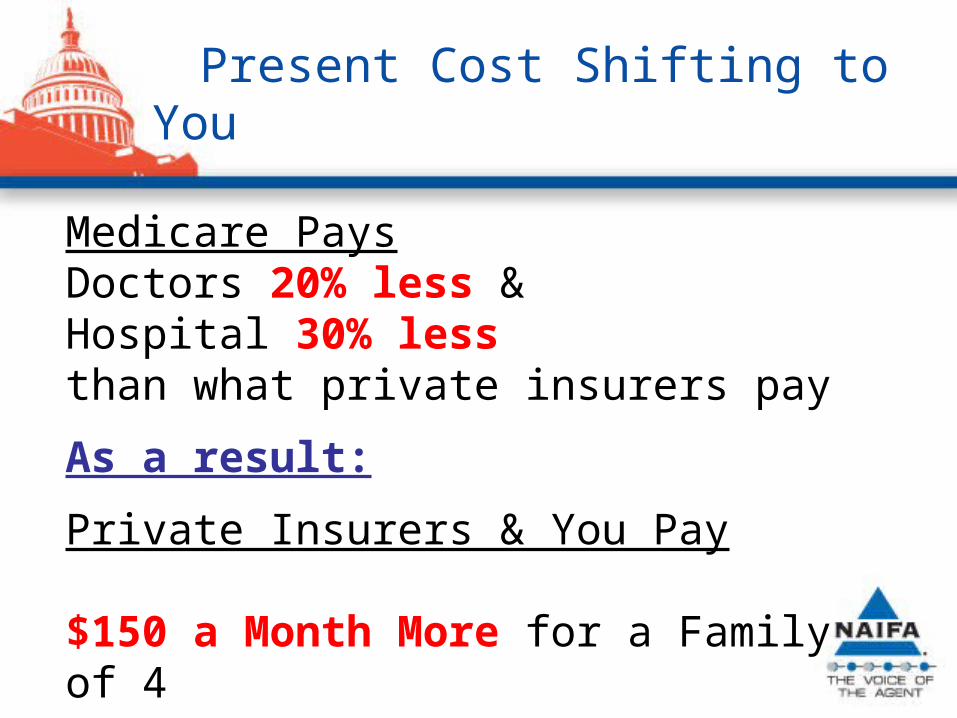

Present Cost Shifting to You

Medicare PaysDoctors 20% less &Hospital 30% less than what private insurers pay

As a result:

Private Insurers & You Pay $150 a Month More for a Family of 4

Source: Milliman 2008

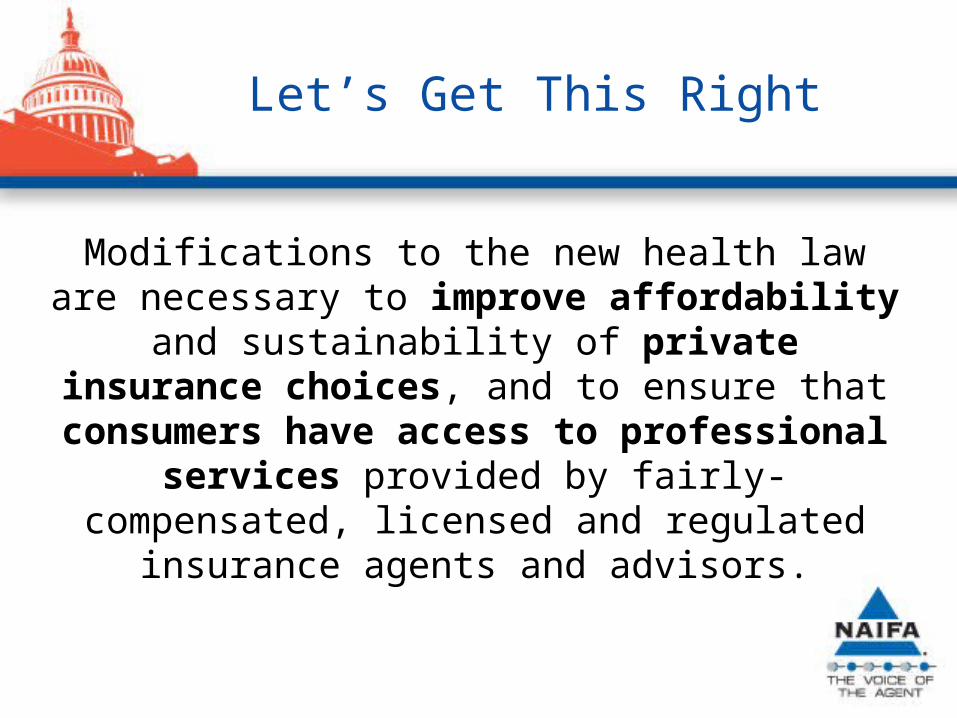

Let’s Get This Right

Modifications to the new health law are necessary to improve affordability and

sustainability of private insurance choices, and to ensure that consumers have access to professional services provided by fairly-compensated, licensed

and regulated insurance agents and advisors.

Small Employer Responsibilities

• Allocating Medical Loss Ratio Rebate

• Withholding Medicare (FICA) Tax

• Administering FSA Contribution Cap

• High-value Health Insurance Tax

• Calculating & Reporting to IRS “high value” health insurance

QUESTIONS ???