verisk insurance solutions | iso air worldwide xactware © 2015 verisk analytics, inc. all rights...

TRANSCRIPT

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

Avoiding Fraud at the Point of Sale

Bill Ayscue, Sr. Product Manager, Verisk UnderwritingJohn Petricelli, VP Product Management, Verisk Underwriting

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

2

Agenda• Fraud – The issue and costs• What to do?-Traditional approach-Perimeter defense

• Fraud correlation• Loss ratio correlation• Other findings• Conclusions

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

3

Cost of Fraud

US$80 billion (entire industry)1

3

9% - 18% of auto claim payments (C$769M to C$1.56 billion)2

C$116 to C$236 per year per family2

US$64 billion (P&C) industry3

US$15.4 billion in lost auto premium4

10% of P&C claims, US$13.2 billion in personal auto5

1. Coalition Against Insurance Fraud (http://www.insurancefraud.org/the-impact-of-insurance-fraud.htm)2. Insurance Bureau of Canada / BAC. (http://www.fin.gov.on.ca/en/autoinsurance/submissions/Fraud_Task_Force_Submission.ATTACH.170812.FINAL.pdf)3. FBI (http://www.insurance-research.org/sites/default/files/downloads/IRC_Fraud_NR.pdf)4. Aite Study(http://www.aitegroup.com/report/escalating-war-insurance-fraud-pc-carriers-and-fraudsters-their-games)5. QPC (http://www.verisk.com/underwriting/resources/qpc%20rating%20error%20report%202010_final.pdf6. SNL 2012 P&C Underwriting Analysis

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

4

Recent headlines“Insurance Fraud: A $40 billion battle” (Chicago Tribune, 5/3/2013)

“Feds allege $279 million auto insurance fraud scheme in New York” (NBC News, 2/29/2012)

“Two North Texas women sentenced to federal prison for bilking auto insurance companies” (Dallas News, 11/27/2012)

“19 Fraudsters Nabbed As Florida PIP Reform Takes Hold” (PropertyCasualty360, 1/4/2013)

“Durham Group accused of staging car crashes for cash” (WRAL.com, 5/31/2013)

“Vandling man charged with insurance fraud” (The Scranton Times – Tribune, 2/25/2014)

Minn. Man Charged In Auto Insurance Fraud (insurancenewsnet.com, 10/1/2013)

Claims and Coverage: Lawyers key in fight against motor vehicle insurance fraud (Law Times, 10/5/2015)

“Canadian auto personal accident benefits loss ratio highest since 2010” (Canadian Underwriter, 9/24/2015)

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

5

Loss ratio is increasing…

4TH 1ST 2ND 3RD 4TH 1ST 2ND 3RD 4TH 1ST 2ND 3RD 4TH 1ST 2ND 3RD 4TH10 11 11 11 11 12 12 12 12 13 13 13 13 14 14 14 14

0.500

0.550

0.600

0.650

0.700

0.750

0.800

0.850

0.900

Liability

Phys Dam

Combined

Linear (Combined)

Lo

ss

Ra

tio

Source: ISO Fast Track

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

6

As rates and costs increase…

Source: BLS.gov

Jan 2010

Feb 2010

Mar 2010

Apr 2010

May 2010

Jun 2010

Jul 2010

Aug 2010

Sep 2010

Oct 2010

Nov 2010

Dec 2010

Jan 2011

Feb 2011

Mar 2011

Apr 2011

May 2011

Jun 2011

Jul 2011

Aug 2011

Sep 2011

Oct 2011

Nov 2011

Dec 2011

Jan 2012

Feb 2012

Mar 2012

Apr 2012

May 2012

Jun 2012

Jul 2012

Aug 2012

Sep 2012

Oct 2012

Nov 2012

Dec 2012

Jan 2013

Feb 2013

Mar 2013

Apr 2013

May 2013

Jun 2013

Jul 2013

Aug 2013

Sep 2013

Oct 2013

Nov 2013

Dec 2013

Jan 2014

Feb 2014

Mar 2014

Apr 2014

May 2014

Jun 2014

Jul 2014

Aug 2014

Sep 2014

Oct 2014

Nov 2014

Dec 2014

1

1.05

1.1

1.15

1.2

1.25

PPI

CPI

PP

I/C

PI. J

an

20

10

= 1

.00

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

7

And questionable claims increase…

20082009

20102011

20122013

1.00

1.20

1.40

1.60

1.80

Index Exposures Index Claims Index QC Linear (Index QC)

Ind

ex:

20

08

= 1

.0

Sources: Index Exposures and Claims: ISO Fast Track; Questionable Claims: NICB Questionable Claims Report

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

8

What to do?• Most antifraud efforts target the claim.• Traditional approach is to address fraud at the point of claim; too late, cost of litigation is often more than settling the claim.

• Statutes require some claims to be paid regardless.

• The desire: identify the fraudulent claim as early as possible.

• Almost 90% use technology to assist with fraud detection; less than half use it outside claims.

• Is there a way to predict fraud at the point of sale?

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

9

Identify fraud at the point of sale

By validating the information on the application, can we predict:1.A consumer’s propensity to commit fraud

at point of sale prior to bind (hard fraud)?

2.A consumer’s propensity to exaggerate a claim (severity) and/or report nuisance claims (frequency) (soft fraud)?

3.A consumer’s premium avoidance due to the purposeful misrepresentation of characteristics (soft fraud)?

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

10

FrameworkFraud is pervasive throughout all aspects of insurance. Carriers need an integrated multifactor framework designed to quantify and predict both hard and soft fraud:

1.Identity • Verify consumers’ identity. Are they who they say

they are, or have they assumed an alternative identity?

2.Location/territory– Is the asset located where the consumer indicated it

is? What’s the proximity to external risks/hazards?

3.Exposure(s)– Are consumers representing the risk adequately or

have they masked/omitted characteristics that could affect rating?

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

11

Framework (continued)

4.Asset use• Does the consumer use the asset per the terms of

the policy?

5.Asset ownership– Is the consumer the owner or otherwise authorized

to insure the property?

6.Rating variable validation– Did the consumer represent the characteristics and

condition of the asset correctly?

7.Miscellaneous– Other verifications that do not fit into any of the

other six categories; condition and restrictions fall into this category.

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

12

Study methodology

• Analyzed 3+ million policies ($2.64 billion earned premium)

• 1.84 million associated claims ($2.54 billion losses)

• 1,160,626 policies had no claims (38% of policies)

• 920,438 policies had non-suspicious claims (50% of claims)

• 892,034 policies had suspicious claims (48.5% of claims)

• 26,982 flagged as known fraud(1.5% of claims)

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

13

Study methodology• We analyzed policyholder applications to

see which exceptions had the highest correlation with known fraud claims.

• Used 7-factor framework approach.

• We performed a loss ratio analysis. • Examined frequency, severity, and

premium leakage/rate evasion.

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

14

High exception rate predicts known fraud claims

• The 20% of policies with the most exceptions are 5x more likely to have a known fraud claim.

• Policies with a fraud trigger on the application (2.8%) are 16 times more likely to have a known fraud claim.

• Conversely, the 20% of policies with the fewest exceptions are 60% less likely to have a known fraud claim.

Best 20% Mid 60% Worst 20%0%

20%

40%

60%

80%

% Policies % Claims

% Suspect Claims % Known Fraud

% o

f to

tal p

olic

ies

Fraud Trigger0%

20%

40%

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

15

Fraud triggersWithin the 7-factor framework, we have 2 major types of

exceptions:

Application information cannot be confirmed.

Could be due to fraud, but could also be the result of a transitory lifestyle.

Application information is negatively confirmed.

Reflects information that is intentionally excluded or misrepresented (e.g., I “forgot about” my 16-year-old child).

Fraud triggers are the negative exceptions most highly correlated with known fraud claims.

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

16

High exception rate also predicts loss ratio

• In addition to predicting fraudulent claims, high incidence of application misrepresentation correlated to higher loss ratios.

• Studies of more recent data continue to show this relationship.

Best 2

0%

Mid

60%

Wor

st 20

%

Highe

st Exc

eptio

n Gro

up50%

70%

90%

110%

130%

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

17

Findings from recent studies

0%

100%

200%

300%

400%

0%

20%

40%

60%

80%

68.1%

2.1% 2.9% 1.4% 0.4% 0.8% 0.4%

1.0

1.6 1.6 1.61.8

2.5

2.9

% PIFLR Relativity

LR

re

lativ

ity

% P

IF

More recent studies show correlations between types of exceptions and loss ratio:

• 0–1 exception group is base loss ratio.

• Identity and branded title have a 60% loss ratio relativity.

• Combination of address, ownership, and branded title has the highest LR relativity.

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

18

Other interesting correlations

Individual triggers with high loss ratios

• Phone number = paging service

• Vehicle registration state ≠ policy state

Foreign driver’s license

• FDLs tend to have favorable performance, unless (pretenders) attempting to hide a valid state DL.

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

19

Conclusion

Once an insurer issues a policy and a loss occurs, avoiding a fraudulent claim is extremely difficult and expensive.

Insurers should use available data and technology to screen policies for fraud and misrepresentation early in the process, with minimal impact on production.

A “perimeter defense” is the most effective strategy. Keep fraudsters from infiltrating your book.

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

Recent Studies

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

21

Need for change• Millennial demographic not as concerned

with price as older consumers; want easy and fair;

– Not into vehicles like Baby Boomers– Migrating to cities, leverage “shared”

vehicles, many people using the same vehicle– Into Uber, Lyft, Zipcar (as users and

providers)

• Insurers who present the most accurate/fair quote early in the process will win.

• Sale of insurance needs to be like every other online transaction: short, minimal input, easy to close, and high quality.

• Verification must be behind the scenes and transparent to the customer.

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

22

And the winner is…

• Can simplify consumer’s interaction and dramatically reduce the time to acquisition to 1 minute or less

• Can figure out how to break out of the current “household” paradigm and define the household and thus the risk

• Finds alternative ways to consume information and underwriting reports

– Current information providers are not helping; they have defined when and how consumer reports are purchased

– Consuming the same underwriting reports earlier in the acquisition lifecycle will lead to more expense

The carrier that:

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

23

And the winner is…

The serviceprovider that:

• Can apply population-specific advanced analytics at point of sale

• Will assess and adjust the information being provided before transmission to the insurer (quality is key)

• Invents new ways to format and deliver underwriting reports early in the quoting process without dramatically increasing an insurer’s expense

• Will work with and help the insurer determine when enough is enough; not all consumers will require the same level of information and scrutiny

• The result is lower acquisition cost per unit

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

24

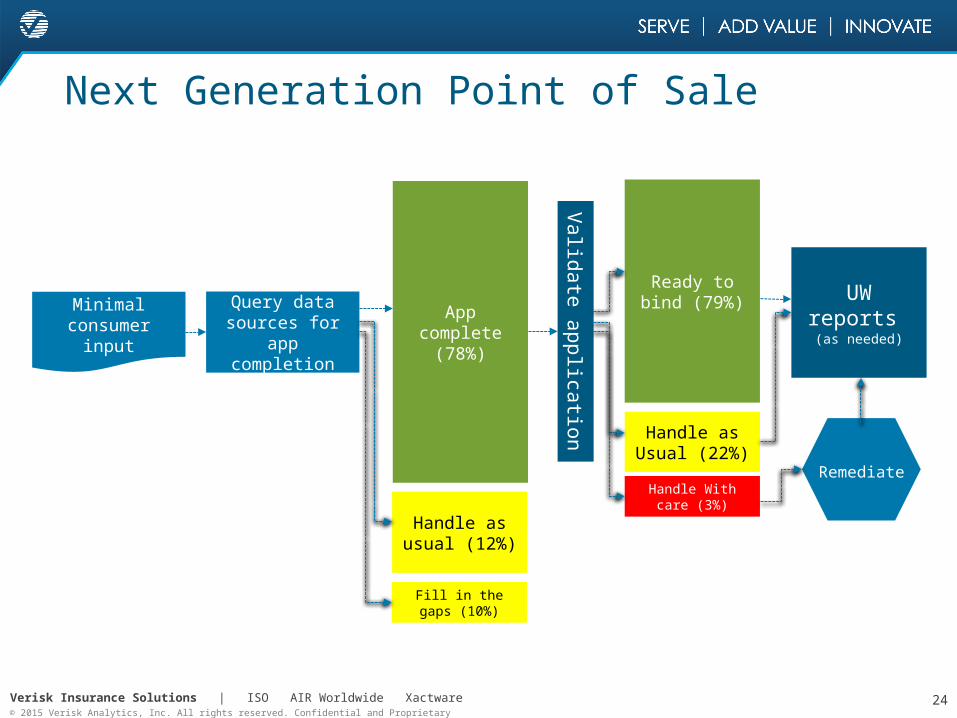

Next Generation Point of Sale

Minimal consumer

input

Query data sources for app

completion

App complete

(78%)

Ready to bind (79%)

Handle as Usual (22%)

Handle With care (3%)

Fill in the gaps (10%)

Handle as usual (12%)

Valid

ate

applica

tion

Remediate

UW reports (as needed)

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

25

Findings• Initial analysis showed that 78% of applications

could be completed using independent data sources with minimal customer input.

– The resulting applications were validated using secondary sources.

– Over 50% of the applications were fully validated; nearly double what we see in applications completed by consumers or using standard application prefill approaches.

• 12% had minimal exceptions

– 2.5% of applications contained significant variations; current processes result in two to three times as many “high-risk” applications.

• Financial outcomes– Historical analysis shows that policies with

minimal exceptions (62% above) perform 52% better than those “high-risk” policies with significant variances .

– The distribution shift alone yields a loss ratio improvement before any remediation.

Verisk Insurance Solutions | ISO AIR Worldwide Xactware© 2015 Verisk Analytics, Inc. All rights reserved. Confidential and Proprietary

26

Questions / Discussion