venture capital, boards of directors, and the market for

TRANSCRIPT

The Pennsylvania State University

The Graduate School

The Mary Jean and Frank P. Smeal College of Business

VENTURE CAPITAL, BOARDS OF DIRECTORS, AND THE MARKET

FOR CORPORATE CONTROL

A Dissertation in

Business Administration

by

Colin R. Jones

Submitted in Partial Fulfillment

of the Requirements

for the Degree of

Doctor of Philosophy

May 2013

ii

The dissertation of Colin R. Jones was reviewed and approved* by the following:

Chris Muscarella

Professor of Finance

Co-Chair of Committee

Dissertation Co-Advisor

Laura Field

Associate Professor of Finance

Co-Chair of Committee

Dissertation Co-Advisor

David Haushalter

Associate Professor of Finance

N. Edward Coulson

Professor of Economics

William Kracaw

Professor of Finance

Head of the Department of Finance

*Signatures are on file in the Graduate School

iii

ABSTRACT

This dissertation studies the effect of venture capitalists on the decisions of newly-public corporations

after the IPO. I investigate venture capitalists’ role as information conduits in mergers and acquisitions,

specifically, their role while serving on the board of directors of acquiring firms, target firms, or both.

Chapter 1 finds that the information sharing between a VC and a firm’s management results in value-

enhancing acquisitions of VC-backed private targets, especially when the acquirer and target share a

venture capital board member. I also document that this holds true with public targets, which is evidence

in support of the information sharing hypothesis rather than the cheap targets hypothesis. Chapter 2

shows that VC-backed firms are significantly more likely to receive bids and get acquired following their

initial public offering. I also find that they receive higher premiums while the venture capitalist sits on

the board of directors. This seems to come from extracting the negotiation surplus, as the acquirer of VC-

backed targets experiences more pronounced negative announcement returns while the combined

announcement return is on average unaffected. I interpret this as evidence of a wealth transfer from the

acquirer to the target firm. I attribute this to the certification and negotiating abilities of the venture

capitalist serving on the target firm’s board of directors, documenting a further method venture capitalists

can add value to corporations.

iv

TABLE OF CONTENTS

LIST OF TABLES v

LIST OF FIGURES vii

ACKNOWLEDGEMENTS viii

INTRODUCTION 1

CHAPTER 1 - THE INFORMATION ROLE OF VENTURE CAPITALISTS:

HOW VENTURE CAPITALISTS AFFECT THE M&A DECISIONS OF

THEIR PREVIOUS IPOs

3

1.1 INTRODUCTION 3

1.2 BACKGROUND 6

1.3 HYPOTHESES 14

1.4 DATA AND METHODOLOGY 17

1.5 RESULTS 21

1.6 CONCLUSION 28

CHAPTER 2 - THE INFORMATION ROLE OF VENTURE CAPITALISTS

ON BOARDS OF TARGET FIRMS

36

2.1 INTRODUCTION 36

2.2 BACKGROUND 39

2.3 HYPOTHESES 45

2.4 DATA AND METHODOLOGY 47

2.5 RESULTS 50

2.6 CONCLUSION 59

REFERENCES 92

v

LIST OF TABLES

TABLE 1.1: The Effect of Venture Capital Backing on M&A Activity for Recent IPOs

30

TABLE 1.2: Logistic Regression for Likelihood That Target is VC-backed

31

TABLE 1.3: Acquirer CARs in Acquisitions of Private Targets

32

TABLE 1.4: Multivariate Analysis of Acquirer Cumulative Abnormal Announcement

Returns

33

TABLE 1.5: Announcement CARs in Acquisitions of Young VC-backed Public Targets

by Young VC-backed Public Acquirers

34

TABLE 1.6: Multivariate Analysis of Target, Acquirer, and Combined Announcement

Returns in Acquisitions of Young VC-backed Public Targets by Young VC-backed

Public Acquirers

35

TABLE 2.1: IPOs, Venture Capital Backing, and Deal Activity

60

TABLE 2.2: Venture Capital Backing and Deal Activity Through Time

62

TABLE 2.3: Venture Capital Backing and Percentage of Firm Sold in IPO

73

TABLE 2.4a: Venture Capital Backing and Likelihood of an Acquisition Attempt

74

TABLE 2.4b: Venture Capital Backing and Likelihood of Being Acquired

75

TABLE 2.4c: Venture Capital Backing and Likelihood of An Acquisition Attempt

Within 3 years of the IPO

76

TABLE 2.5: IPOs, Venture Capital, and Announcement Returns to Acquisition Targets

in IPO Sample

77

TABLE 2.6a: Acquisition Announcement Returns to Bids on Recent IPOs (VC vs. Non-

VC)

78

TABLE 2.6b: Acquisition Announcement Returns to Completed Acquisitions of Recent

IPOs (VC vs. Non-VC)

79

TABLE 2.6c: Acquisition Announcement Returns to Bids on Recent IPOs (Tech vs.

Non-Tech)

80

TABLE 2.6d: Acquisition Announcement Returns to Completed Acquisitions of Recent

IPOs (Tech vs. Non-Tech)

81

vi

TABLE 2.6e: Acquisition Announcement Returns to Completed Acquisitions of Recent

IPOs (High Tech Only)

82

TABLE 2.6f: Acquisition Announcement Returns to Completed Acquisitions of Recent

IPOs (Non-Tech Only)

83

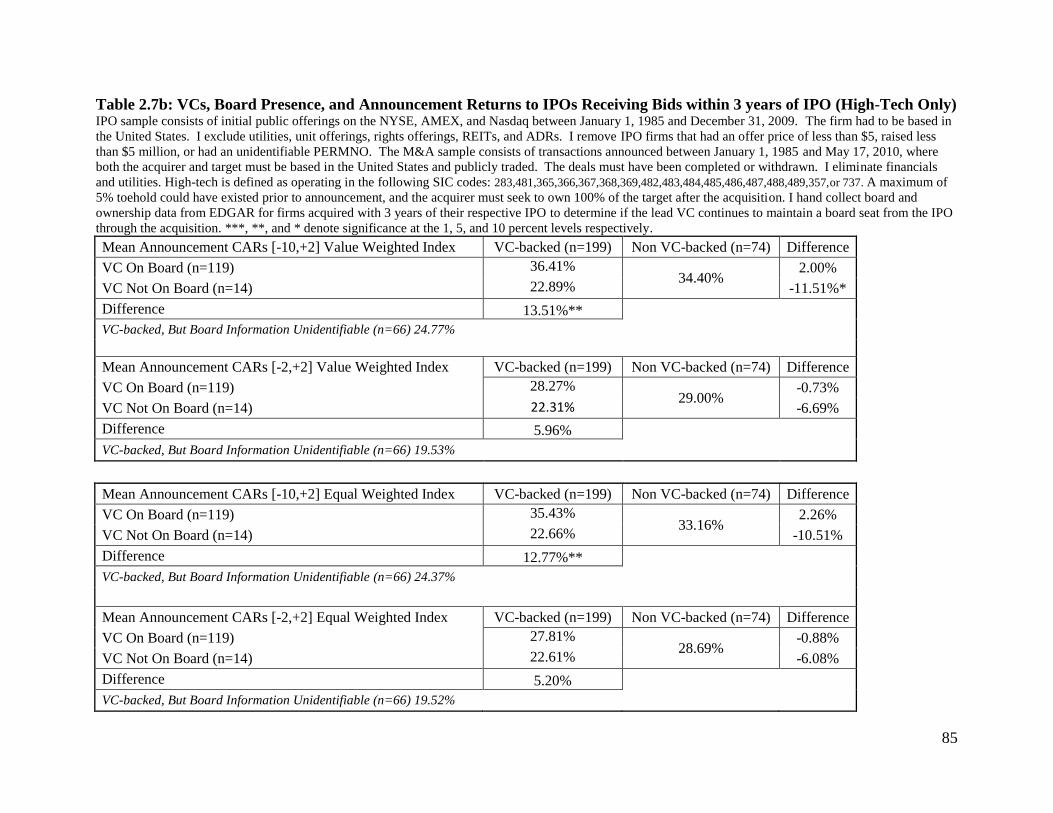

TABLE 2.7a: VCs, Board Presence, and Announcement Returns to IPOs Receiving Bids

within 3 years of IPO

84

TABLE 2.7b: VCs, Board Presence, and Announcement Returns to IPOs Receiving Bids

within 3 years of IPO (High-Tech Only)

85

TABLE 2.7c: VCs, Board Presence, and Announcement Returns to IPOs Receiving Bids

within 3 years of IPO (Non-Tech Only)

86

TABLE 2.8: Target, Acquirer, and Combined Announcement Returns to Bids on Recent

IPOs

87

TABLE 2.9: Summary Statistics of Regression Variables, VC vs. Non-VC

88

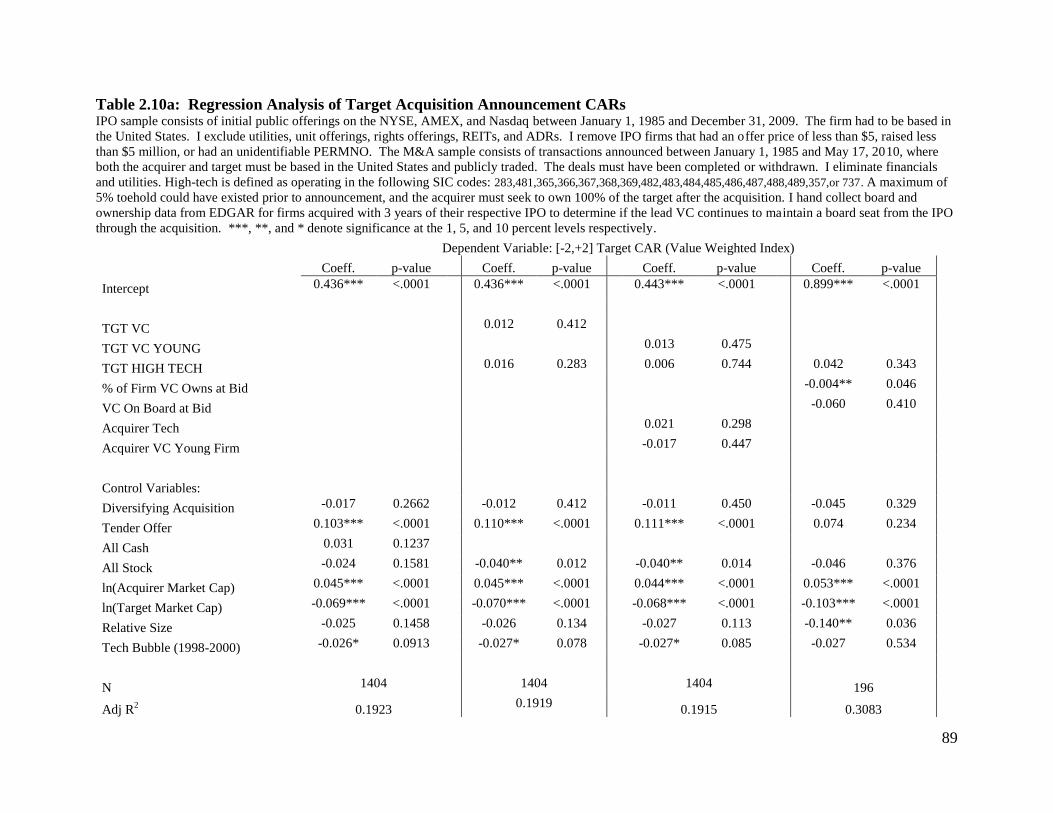

TABLE 2.10a: Regression Analysis of Target Acquisition Announcement CARs

89

TABLE 2.10b: Regression Analysis of Bidder Acquisition Announcement CARs

90

TABLE 2.10c: Regression Analysis of Combined Acquisition Announcement CARs 91

vii

LIST OF FIGURES

FIGURE 2.1: IPOs, Venture Capital Backing, and Acquisition Announcements in Years

Following IPO

64

FIGURE 2.2: Cumulative Total Acquisition Announcements in Years Following IPO

65

FIGURE 2.3: IPOs, Venture Capital Backing, and Acquisitions in Years Following IPO

66

FIGURE 2.4: Cumulative Total Acquisitions in Years Following IPO

67

FIGURE 2.5: Acquisition Announcements on IPO Sample Chronologically

68

FIGURE 2.6: Cumulative Total Bids in Years Following IPO, Technology Firms

69

FIGURE 2.7: Cumulative Total Bids in Years Following IPO, Non-Technology Firms

70

FIGURE 2.8: Cumulative Total Completed Acquisitions in Years Following IPO,

Technology Firms

71

FIGURE 2.9: Cumulative Total Completed Acquisitions in Years Following IPO, Non-

Technology Firms

72

viii

ACKNOWLEDGEMENTS

I’ll start by thanking my incredibly patient advisors, Chris Muscarella and Laura Field,

and committee members, David Haushalter and Ed Coulson. I’d like to acknowledge the Penn

State Smeal College of Business for financial support. I would also like to thank Vladimir

Atanasov, Jean Helwege, Michelle Lowry, Tom Miller, Brad Goldie, and Marco Rossi, as well

as seminar participants at the University of South Carolina, University of Denver, East Carolina

University, the College of William & Mary, and the 2008 FMA meetings for insightful

comments. Special thanks to Spencer Kushner, whose interest in my research at times exceeded

my own, for his research assistance down the stretch.

Whatever it is I’ve done here, I couldn’t have done it without the great group of friends

and colleagues I forged in Happy Valley. From The Threadbare Orchestra to G. Rickey & Co.,

and everything in between, there was nary a dull moment outside of the office. Thanks for

keeping it interesting.

Last but not but least, thanks to my family, for helping me become who I am today.

1

INTRODUCTION

This dissertation studies the effect of venture capitalists on the decisions of newly-public

corporations after the IPO. I investigate venture capitalists’ role as information conduits in

mergers and acquisitions, specifically their role while serving on the board of directors of

acquiring firms, target firms, or both. Chapter 1 studies tightly networked transactions in which

a venture capitalist serves on the board of directors of a recently public firm that acquires a

private target out of the same VC’s portfolio. Chapter 2 examines VC’s effect on the likelihood

of a takeover attempt, the likelihood of takeover completion, and the target, acquirer, and

combined announcement returns to bids (acquisition announcements) on recently public firms.

Given the level of involvement between a venture capitalist and a portfolio firm’s

management, and a VC’s propensity to facilitate collaborations within its network, it is likely

that a VC continues to affect a firm beyond the initial public offering. This could manifest itself

in many ways, including the M&A decisions of management, with a VC facilitating and

encouraging mergers and acquisitions within its network. Chapter 1 seeks determine what role

venture capital firms play in the acquisition decisions of their previous IPOs, and what effect this

has on acquisition announcement returns.

Chapter 1 explores the announcement returns to publicly traded acquirers of venture

capital backed private targets. I find that tightly networked transactions in which a venture

capitalist concurrently sits on the board of both the acquirer and target result in abnormally high

announcement returns. I interpret my findings as evidence that venture capitalists function as

information conduits to alleviate asymmetric information in acquisitions, rather than acting in

their own self-interest at the expense of acquiring firm shareholders. Chapter 1 documents a

further mechanism through which venture capitalists can add value to corporations.

2

It has been well established that venture capitalists are heavily involved with the private firms

in which they invest (Gorman and Sahlman (1989), Gompers (1995), Lerner (1995), Baker and

Gompers (2003)). Less well studied is the role of a venture capitalist after they’ve taken a firm

public. We know that venture capitalists tend to stay on the boards of their companies well after an

IPO (Barry et al. (1990), Gompers (1996)), but we know little about how this affects firm decisions

and firm performance.

Chapter 2 shows that VC-backed firms are significantly more likely to receive bids and

get acquired following their initial public offering. I also find that they receive higher premiums

while the venture capitalist is still on the board of directors. This seems to come from extracting

the negotiation surplus, as the acquirer of VC-backed targets experiences more pronounced

negative announcement returns while the combined announcement return is on average

unaffected. I interpret this as evidence of a wealth transfer from the acquirer to the target firm. I

attribute this to the certification and negotiating abilities of the venture capitalist serving on the

target firm’s board of directors, documenting a further method venture capitalists can add value

to corporations.

I find that venture capitalists continue to affect firm M&A decisions well after the initial

public offering, and that this results in higher returns to firm shareholders. Chapter 1 shows that

the information sharing between a VC and a firm’s management results in value-enhancing

acquisitions of VC-backed private targets. Chapter 2 finds strong evidence that VC involvement

is associated with an increased likelihood of being acquired, and that VC board presence on the

target firm increases the premium paid in acquisition.

3

CHAPTER 1

The Information Role of Venture Capitalists: How Venture Capitalists Affect the M&A

Decisions of Their Previous IPOs

1.1 INTRODUCTION

ON OCTOBER 6, 2006, GOOGLE INC. announced that it would acquire YouTube.com in a

$1.65 billion stock-for-stock transaction. Less than a year earlier, YouTube LLC received its

first and only venture capital round when Sequoia Capital invested $11.5 million in November

2005.1 When the “GooTube” acquisition was completed in November 2006, Sequoia Capital

received 1.07 million shares of Google stock, worth approximately $504 million (a return of

nearly 4300% in a single year). Interestingly, and perhaps not coincidentally, Sequoia Capital

was also a major investor in Google during the search engine’s first and only venture round in

1999. In fact, Sequoia partner Michael Moritz served on the Google board of directors from

May 1999 until his resignation in May 2007.

I suggest that tightly networked transactions like this one are not coincidental, but that the

VC continues to impact the decisions of the newly public firm. Given the level of involvement

between a venture capitalist and a portfolio firm’s management, and a VC’s propensity to

facilitate collaborations within its network, it is likely that a VC continues to affect a firm

beyond a successful public offering2. This could manifest itself in many ways, including the

M&A decisions of management, with a VC facilitating and encouraging mergers and

acquisitions within its network. Specifically, the VC could promote the sale of private targets

from its own portfolio to public acquirers that the VC previously took public. This paper

1 According to Securities Data Company’s VentureXpert database.

2 See Section II of this paper (Background) for an in depth review of the applicable literature.

4

examines the role that venture capital firms play in the acquisition decisions of their previous

IPOs.

I show that public companies that were VC-backed at the IPO [VC-acquirers] are more

likely to acquire VC-backed private targets [VC-targets] in the five years following their IPO. In

a logistic regression for 2,969 acquisitions by firms in my IPO sample, a dummy variable for a

VC-acquirer is positive and significant in determining the likelihood that the target is VC-

backed. This supports the hypothesis that VC-backing at the IPO affects a firm’s M&A activity

following the IPO.

Furthermore, I examine the effect of a venture capitalist’s presence on the announcement

returns of these tightly networked acquisitions. It is possible that the venture capitalist’s role as

an information conduit leads to the identification of profitable acquisitions within its network, ala

Aoki (2000) and Lindsey (2008). In this case, VCs could share valuable information with the

acquiring firm’s management, improving the acquirer’s bidding ability, leading to value-

enhancing acquisitions. On the other hand, it could be that the VC’s propensity to facilitate deals

within its network leads to managerial hubris in the acquiring firm, ala Roll (1986). If acquiring

firm management trusts the VC, management may place too much weight in the information that

is being shared, leading to hubris and overbidding. This would result in value-destructive

acquisitions.

Following a sample of firms that went public between 1996 and 2005, I examine their

acquisitions of private targets within 5 years of the acquirer’s IPO. I identify 188 acquisitions of

VC-backed private targets, 114 involved VCs on both sides, and 34 involving the same VC. I

find mild support for the information sharing hypothesis and strong support against the

managerial hubris hypothesis. Acquisitions in which the same VC backed the acquirer at the

5

IPO and was invested in the private target at the acquisition (SAME_VC transactions)

experience higher cumulative abnormal returns around the acquisition announcement date than

do typical acquisitions of VC-backed private targets by public acquirers. This supports the

information sharing hypothesis.

Masulis and Nahata (2011) also documents the abnormal announcement returns to similar

transactions in the self-dealing portion of their paper, arguing that the positive acquirer

announcement returns are caused by a wealth transfer from the target to the acquirer. They argue

that venture capitalists are selling the target firm “cheap” to the acquirer, resulting in positive

abnormal returns to the acquirer around the acquisition. That is, the acquirer is getting a good

deal on the target due to the self-dealing of the venture capitalist. As the target is a private firm,

we do not observe a market price for the company, so cannot distinguish between my

information sharing hypothesis and their cheap target hypothesis.

However, I distinguish between the information sharing hypothesis and the cheap target

hypothesis by finding acquisitions of VC-backed public targets by VC-backed public acquirers

that had concurrent, overlapping venture capital representation on their respective boards of

directors. While they are few in number, they are quite telling. The highly positive

announcement returns to these transactions disprove the cheap target, or wealth transfer,

hypothesis, and lend strong evidence to the information sharing hypothesis.

I conclude that venture capitalists continue to affect firm M&A decisions well after the

initial public offering, but that this is generally of benefit to acquiring firm shareholders. The

information sharing that occurs between a VC and a firm’s management appears to result in

value-enhancing acquisitions of VC-backed private targets, despite the potential for managerial

6

hubris or self-dealing. This paper documents a further mechanism through which venture

capitalists can add value to corporations.

1.2 BACKGROUND

It is well documented that venture capitalists play a valuable information gathering and

monitoring role for start-up firms, reducing informational asymmetry and agency problems

(Gompers (1995), Lerner (1995), Baker and Gompers (2003)). But in addition to their role as

monitors, existing literature has shown that venture capitalists provide additional value-added

services to the entrepreneurial firm.

Gorman and Sahlman (1989) show that the venture capitalist serves an important role in

fund raising, strategic analysis, management recruitment, and operational planning.

Additionally, they find that the average venture capitalist visits a portfolio company nineteen

times per year, spends 80 hours per year onsite and 30 hours per year on the phone with the

CEO. Sahlman (1990) finds that venture capitalists, while generally not involved in day-to-day

operations, regularly serve on the board of directors. Barry, Muscarella, Peavy, and Vetsuypens

(1990) show that venture capitalists typically control about one-third of the board seats.

Furthermore, the presence of a venture capitalist at an IPO leads to the involvement of

higher quality underwriters and auditors (Barry et al. (1990), Megginson and Weiss (1991)).

Hellman and Puri (2002) examine the differences between venture-backed and non venture-

backed companies and show that the presence of a venture capitalist in a start-up firm leads to a

more professional internal organization (advanced human resource policies, stock option plans,

the hiring of a VP of marketing, etc.). They also find that venture capitalists can play both

7

supportive and controlling roles in the start-up firm, depending on the needs of the particular

firm.

Serving as much more than a monitoring financial intermediary, the venture capitalist

takes on an integral role in the firm during start-up, working to maximize the odds that their

equity investment will lead to a successful exit and superior return. Barry et al. (1990) and

Gompers (1996) show that venture involvement continues long after a firm goes public, where

venture capitalists continue to hold large equity stakes and serve on the board.

In fact, many venture capital firms pride themselves on value-added keiretsu-style

behavior, facilitating strategic alliances among portfolio firms and fostering interaction within

their networks. Lindsey (2008) finds that strategic alliances are more frequent among firms

backed by the same venture capitalist. She also finds that this effect is concentrated in alliances

where high informational asymmetries exist and venture capitalists can utilize their informational

advantage. Venture-backed firms often operate in highly competitive and information-sensitive

industries, where the costs of sharing proprietary information are high. Lindsey (2008) suggests

that venture capitalists can use their information to identify profitable collaborations between

firms, overcoming this hurdle. Furthermore, she shows that these alliances create value for

portfolio firms by increasing the probability of a successful exit (IPO or acquisition).

It is imperative that VCs be able to exit their investments in order to provide liquidity and

returns to their limited partners. This is done either through an initial public offering, an

acquisition, or liquidation. Most prior finance literature focuses on the IPO exit route for venture

capitalists, as it is the most observable. According to Gompers and Lerner (2001), the proportion

of VC-backed IPOs increased from 10% of all IPOs in the 1980s, to 31% in the 1990s, to 56% in

1999, demonstrating the importance of VC-backed firms in the IPO market. Empirical work has

8

shown that VC-backed IPOs experience less underpricing (Barry et al. (1990), Megginson and

Weiss (1991)) and have better long-run performance than non-backed IPOs (Brav and Gompers

(1997)). The authors argue that this is due to the certification role that the venture capitalist

plays in the offering process.

In a Gompers (1995) sample of 794 VC-backed companies, 127 (22.5%) went public,

134 (23.8%) were acquired, 88 (15.6%) were liquidated, and 215 (38.1%) were still privately

held at the end of the sample. In the same sample, Gompers (1995) finds that IPO exits offered

an average return of 59.5% per year (7.1x invested capital in 4.2 years), M&A exits averaged

15.4% per year (1.7x invested capital in 3.7 years), and liquidations lost 80% of their value in 4.1

years. Gompers’ findings demonstrate that while IPOs are a primary source of large returns for

venture capitalists, acquisitions are also an important form of exit, especially in a dry IPO

market. Therefore, venture capitalists may be incentivized to leverage every available tool to

generate exits, including their relationship with the management of a potential acquirer that the

VC previously took public.

“No conflict, no interest” is an old venture capital saying, and this is not the first paper to

address potential conflicts of interest in the venture capital realm. Gompers and Lerner (1999)

address a conflict of interest inherent when an investment bank underwrites an IPO in which its

holds equity through a venture capital subsidiary. The authors find that investors require greater

underpricing for offerings in which the lead underwriter is also a venture investor in the firm.

The authors interpret this as proof of the rational discounting hypothesis, or that investors are

smart enough to anticipate conflicts of interest and compound them into the price at the IPO.

Given the level of involvement between a venture capitalist and a firm’s management,

and a VC’s propensity to facilitate alliances within its network, it is likely that a VC continues to

9

affect a firm beyond the initial public offering. This could manifest itself in many ways,

including the M&A decisions of management, with a VC facilitating and encouraging mergers

and acquisitions within its network. Specifically, the VC could promote the sale of private

targets from its own portfolio to public acquirers that the VC previously took public. The nature

of the VC’s effect on M&A decisions of public firms is an empirical question. This paper seeks

to determine how the VC’s role affects acquiring firm value as measured by acquirer

announcement returns.

The determinants of acquisition announcement returns to publicly-held bidders have been

heavily studied in the financial literature. Earlier event studies show that bidders have no or

slightly negative announcement returns (Jensen and Ruback (1983), Andrade, Mitchell, and

Stafford (2001)). This is generally attributed to managerial hubris, in which acquiring managers

overestimate their ability to run the target (Roll (1986)), or managerial empire building behavior,

in which managers’ personal objectives are inconsistent with maximizing shareholder value

(Jensen (1986), Morck, Schleifer, and Vishny (1990), Harford (1999)). Furthermore, earlier

studies documented that cash deals resulted in better acquirer returns than stock deals (Jensen

and Ruback (1983), Andrade, Mitchell, and Stafford (2001)). This was attributed to the concept

of stock acquisitions as a signal of overvalued acquirer equity (Myer and Majluf (1984), Travlos

(1987)). But more recently, the financial literature has demonstrated the determinants of acquirer

CARs to be much more nuanced.

Chang (1998) and Fuller, Netter and Stegemoller (2002) show that target ownership is an

important factor in predicting acquirer returns, where acquirers of public targets lose 1% on

average but acquirers of private targets gain about 1.5%. Additionally, the method of payment

effect was also shown to depend on target ownership structure. Acquisitions of private targets

10

fair better when financed with equity, which runs counter to public target acquisitions. This is

attributed to the contingency pricing effect, in which target shareholders partially bear the cost of

overpayment when the acquirer pays with stock (Hansen (1987)). Interestingly, Moeller,

Schlingemann, and Stulz (2007) find that the method of payment is irrelevant after controlling

for acquiring firm idiosyncratic volatility. Using the acquirer’s excess stock return volatility as a

proxy for information asymmetry, the authors show that acquirer CARs are negatively related to

idiosyncratic volatility.

Asquith et al. (1983) show that relative deal size is also a determinant of acquirer

announcement returns, where returns are increasing in the ratio of target market capitalization to

bidder market capitalization. Furthermore, Moeller, Schlingemann, and Stulz (2004) find that

acquirer size (as separate from relative size) is an additional determinant of acquirer

announcement returns for both public and private targets, with small acquirers fairing better than

large acquirers on average. The effect of Tobin’s q and the highly correlated market-to-book

ratio of the acquirer is unclear. Lang et al. (1991) and Servaes (1991) find evidence that high-q

bidders have higher announcement returns, but Dong et al. (2006) find the opposite and Moeller

et al. (2004) find no relation at all. This is likely due to sample period differences. It is

generally acknowledged that pre-1990 announcement returns were increasing in acquirer q, but

reversed in the 1990s.

Interestingly, Moeller, Schlingemann, and Stulz (2005) point out that average

announcement returns may be a misleading measure of returns to acquiring firm shareholders.

They find that from 1991-2001, while 3-day announcement cumulative abnormal returns [CARs]

averaged 1.2%, on the whole acquiring firm shareholders lost $216 billion. The authors compare

this to the 1980s, in which acquiring firms’ shareholders averaged 0.6% in CARs but lost only $4

11

billion in acquiring firm value. Most of the losses in their sample came between 1998 and 2001,

where CARs averaged 0.7% but lost $240 billion in acquiring firm value. Specifically, most of

the dollar losses came in 87 large loss deals (defined as an acquiring firm loss of at least $1

billion). The authors find that the acquirer’s in the large loss deals had high Tobin’s q and low

book-to-market ratios, which is consistent with the Jensen (2005) hypothesis that high firm

valuations give managers leeway to make poor acquisitions.

However, only recently have researchers begun to explore the effect of venture capital

involvement on acquisition announcement returns. A related working paper by Gompers and

Xuan (2009) examines the characteristics of public acquirers of private venture-backed

companies, finding that these acquirers are larger, have higher Tobin’s Q, and operate in a

related industry. Their study shows that the market reacts less positively to the announcement of

the acquisition of a venture-backed firm, but that longer-run returns and operating performance

were higher following these acquisitions. The authors attribute the smaller announcement

returns to the view that venture capitalists are strong negotiators or that an adverse selection

problem exists. But nowhere in the paper do they examine whether the public acquirer had been

venture-backed before going public.

A related paper by Masulis and Nahata (2011) studies the acquisition announcement

returns for public acquirers of private targets. The authors find that acquirers of VC-backed

targets experience larger announcement CARs than acquirers of non-backed targets. They

suggest that this is the result of VCs selling their firms cheap due to conflicts of interest between

VCs and other target shareholders (i.e. entrepreneurs, angel investors). However, the paper only

finds support for the self-dealing hypothesis, in which a VC has a concurrent financial stake in

both the acquirer and the target.

12

While at first this paper may appear similar to Masulis and Nahata (2011), my paper has

significant differences and additions. I look at acquisitions by recent IPOs, which allows me to

comment on the effect of VC-backing on post-IPO acquisition behavior. Masulis and Nahata

(2011) look at acquisitions of VC-backed targets by all acquirers, and make no mention of

acquirer VC-backing (with the exception of the self-dealing observations). Masulis and Nahata

(2011) impose a strong filter on their sample of acquisitions, requiring the target size to be at

least 10% of the acquirer size. They do this so that they can get financial data on the target.

Acquirers are not required to disclose target financials unless the target is 10% of the acquirer.

To get an idea of the sample selection, Andrade, Mitchell, and Stafford (2001) find that the

median target size is 11.7% of the acquirer from 1973-1998 and 11.2% from 1990-1998 (a

similar time frame to Masulis and Nahata (2011)). For comparison, the Masulis and Nahata

(2011) sample mean target size is 45% and median 24%. This censors the sample to deals with

high relative target size, which Asquith et al. (1983) shows have higher announcement returns. It

may also censor the sample to high profile deals where witnessing self-dealing is the least likely.

In the Masulis and Nahata (2011) self-dealing section, the authors identify 25

acquisitions in which a VC has a concurrent financial stake in both the acquirer and the target.

This is a dummy variable, so the authors cannot comment on how much of the acquirer or target

the VC owns (in fact, this information is difficult to ascertain). The authors find that these deals

have higher CARs than acquisitions where the VC doesn’t have a stake in the acquirer, and

conclude that it is because the VC (as target representative) isn’t incentivized to negotiate as hard

with the acquirer when holding a concurrent financial stake. However, Masulis and Nahata

(2011) is unable to show if the VC is the lead investor in the target, which could limit the VC’s

effect on negotiations. And again, in such large deals, it is unlikely that the VC would have as

13

much influence over the target’s decisions, making self-dealing less likely. My paper examines

SAME_VC transactions, in which the VC was invested (concurrent or not) in the acquirer and

the target, over a different time period, and offers an alternative explanation (information

sharing) for abnormal announcement returns.

Furthermore, I distinguish between the information sharing hypothesis and the cheap

target hypothesis by finding acquisitions of VC-backed public targets by VC-backed public

acquirers that had concurrent, overlapping venture capital representation on their respective

boards of directors. While they are few in number, they are quite telling. The highly positive

target, acquirer, and combined announcement returns to these transactions disprove the cheap

target, or wealth transfer, hypothesis, and lend strong evidence to the information sharing

hypothesis.

Both Gompers and Xuan (2009) and Masulis and Nahata (2011) explore target venture-

backing as a determinant of acquirer announcement returns. This paper documents that the

effect of this determinant depends on whether the acquirer was also VC-backed at the IPO. I

follow Aoki (2000) and Lindsey (2008) in examining whether the venture capitalist, acting as an

information conduit, can facilitate value-added activities within its network. Specifically, the

venture capitalist may help an acquirer overcome informational asymmetries and alleviate

managerial hubris in bidding on private venture-backed targets.

The lasting effect that venture capitalists have on their previous IPOs requires further

investigation. This paper explores whether public acquirers that were VC-backed at the IPO are

more likely to acquire VC-backed private targets, and how this bias affects acquiring firm

announcement returns. I extend both the M&A literature on acquisitions of private targets by

14

public acquirers and the venture capital literature on the effect of venture capital backing on

post-IPO behavior.

1.3 HYPOTHESES

Do VC-backed IPOs Differ In Their M&A Behavior?

Given the level of involvement between a venture capitalist and a portfolio firm’s

management, and a VC’s propensity to facilitate alliances within its network (Lindsey (2008)), it

is likely that a VC continues to affect a firm beyond the initial public offering. This could

manifest itself in many ways, including the M&A decisions of management, with a VC

facilitating and encouraging mergers and acquisitions within its network. Specifically, the VC

could promote the sale of private targets from its own portfolio to public acquirers that the VC

previously took public. In either case, I would expect to see that acquirers that were VC-backed

at the IPO [VC-acquirers] are more likely to acquire VC-backed private targets [VC-targets].

H1: Acquirers that were VC-backed at the IPO are more likely to acquire VC-

backed private targets, even after accounting for industry and time.

Information Sharing or Managerial Hubris?

Information Sharing: It is possible that the venture capitalist’s informational advantage

leads to the identification of profitable acquisitions within its network, ala Aoki (2000) and

Lindsey (2008). In this case, VCs could share asymmetric information with the acquiring firm’s

management, improving the acquirer’s bidding ability, leading to value-enhancing acquisitions.

Of course, we cannot observe what a target is truly worth. Examining acquirer acquisition

15

announcement returns will reveal whether the market interprets these tightly networked

transactions as information sharing or managerial hubris.

H2: The market believes the venture capitalist’s involvement reduces asymmetric

information and improves the acquirer’s bidding ability. The acquirer would

experience above average abnormal returns over the announcement window.

Managerial Hubris: It could be that the VC’s propensity to facilitate deals within its

network leads to managerial hubris in the acquiring firm, ala Roll (1986). If acquiring firm

management trusts the VC, management may place too much weight in the information that is

being shared, leading to hubris and overbidding. (It is also possible that the VC pressures

acquiring firms to make acquisitions from the VCs network under threat of retribution, but this is

not necessary to explain overbidding by the acquirer.) In either case, we’d expect to see

overbidding by the acquirer which would lead to value-destructive acquisitions.

H2A: The market believes the venture capitalist’s involvement leads to

overbidding for the target. The acquirer would experience below average

abnormal returns over the announcement window.

Differentiating Between Information Sharing and Cheap Target Hypotheses

Of course, as Masulis and Nahata (2011) suggest, above average abnormal announcement

returns could also be interpreted as a result of the venture capitalist selling its targets cheap due

to conflicts of interest with target shareholders. In their self-dealing hypothesis, the venture

capitalist is not incentivized to achieve a high price for its target if it also holds a concurrent

financial stake in the acquiring firm since it would also gain from any positive announcement

16

return to the acquirer. Unfortunately, my paper faces the same data limitations as Masulis and

Nahata (2011), making it difficult to differentiate between these two hypotheses with the private

target sample.

If accurate information on venture capitalist percentage holdings in the acquirer and

target were available, then it would be straight forward to look at the relationship between VC

holdings in the acquirer and acquisition announcement returns. If the cheap targets hypothesis is

correct, then abnormal CARs should be increasing in the VC’s stake in the acquirer. If

information sharing is correct, the VC’s stake shouldn’t matter in determining announcement

returns. It would also be possible to compare concurrent financial stakes (which Masulis and

Nahata (2011) examine) against historical financial acquirer stakes (the VC held a stake at the

IPO, but has since exited the position). If the information sharing hypothesis is correct, these

shouldn’t differ. If the cheap target hypothesis is correct, concurrent-stake acquisitions should

have higher CARs. But for a variety of reasons, including database limitations, reporting

requirements, and the opaque nature of venture capital share distributions, accurate venture

capital holdings could not be ascertained for private targets.

However, I am able distinguish between the information sharing hypothesis and the

cheap target hypothesis by finding acquisitions of VC-backed public targets by VC-backed

public acquirers that had concurrent, overlapping venture capital representation on their

respective boards of directors. While they are few in number, they are quite telling. The highly

positive target, acquirier, and combined announcement returns to these transactions disprove the

cheap target, or wealth transfer, hypothesis, and lend strong evidence to the information sharing

hypothesis.

17

Predictions

Whatever the effect of the venture capitalist on the M&A behavior of their previous

IPOs, I expect that the effect will:

1) Decrease if management changes between IPO and acquisition. During the startup,

the venture capitalist develops a working relationship with the firm’s management. If

management changes, I expect the VC’s influence on management to diminish.

2) Increase if the VC sits on the board at the IPO and the acquisition. I expect that the

VC’s relationship with management is more pronounced by a presence on the board.

3) Decrease with time from IPO. The further the VC is from the close involvement with

management during the startup and IPO, the VC’s influence on management should

decrease.

1.4 DATA AND METHODOLOGY

The initial sample is compiled from SDC’s Global New Issues, Mergers & Acquisitions,

and VentureXpert databases. The IPO sample consists of firms that went public between

January 1, 1996 and December 31, 2005 on the American, Nasdaq, and New York stock

exchanges. It must be the firm’s original public offering and the offering price must be at least

$5. I exclude utilities, financials, unit offerings, rights offerings, REITs, and ADRs. This results

in sample of 2,491 IPOs, of which 1,153 (46.3%) are venture-backed.

The M&A sample consists of completed acquisitions announced between January 1, 1996

and Decemeber 31, 2006 of private targets by public acquirers whose stock is listed on the

American, Nasdaq, and New York stock exchanges. Acquirers and targets must be U.S. based,

the acquisition must be for 100% of the target, and no toe-hold positions exist before the

18

announcement. I exclude all financial acquirers and targets. I then cross-reference the M&A

sample with the IPO sample to determine which acquirers were in the IPO list and, of those,

which were venture-backed. Acquirer stock returns must be available in the CRSP database.

This results in a sample of 2,781 acquisitions of non-VC-backed targets and 188 acquisitions of

VC-backed targets that occurred within 5 years of a firm’s IPO.

I compile a list of venture-backed companies from VentureXpert, and cross-reference that

list with the M&A group to find a sample of venture-backed targets. The venture-backed targets

sample was created by cross-referencing the M&A sample on CUSIP and company name for all

firms in the VentureXpert database of 19,317 portfolio companies. This results in a sample of

188 venture-backed targets. It is clear that these 188 acquisitions are not a comprehensive

sample, but the current depth of the database and my methodology limit my ability to collect a

larger sample. However, there is little reason to think that this sample is biased or

unrepresentative of the population.

From VentureXpert, I gather the names of venture capital firms invested in both the VC-

backed acquirers and VC-backed targets, and hand-check for the presence of overlapping VCs,

which I call SAME_VC transactions. I construct a dummy variable for SAME_VC that equals 1

if there is at least one overlapping VC and 0 if it is a DIFFERENT_VC transaction. The final

sample consists of 34 SAME_VC transactions, 114 DIFFERENT_VC, and 40 acquisitions of

VC-backed targets by acquirers that were not VC-backed at the IPO.

For the 34 SAME_VC acquisitions, I hand-collect from SEC filings whether the CEO

was the same at both the IPO and acquisition. SAME_CEO equals 1 if so and 0 if the CEO

changed. I also check if the VC remained on the board of directors from the IPO through the

19

acquisition. VC_BOARD equals 1 if the VC was on the board at the IPO and the acquisition,

and 0 if not.

From CRSP, I gather the announcement returns for all 2,969 acquisitions. Using a 3-day

window [-1, +1] relative to the announcement date, I use market-adjusted returns using the CRSP

equal-weighted index to define cumulative abnormal returns. Using a market-model or the

CRSP value-weighted index to calculate abnormal returns did not appreciably alter my results.

Later, I Winsorize the CAR data at the 1% and 99% tails to account for the possibility of outliers

biasing the small sample.

High technology companies are defined as those operating in SIC codes 283 (biological

products, genetics, and pharmaceuticals), 357 (computers), 365-369 (electronic equipment), 481

(high-tech communications), 482-489 (communications services), 737 (software services).

As control variables, I gather acquirer size, market-to-book ratio, and idiosyncratic excess

stock return volatility. I define size as shares outstanding multiplied by acquirer stock price the

two days before the acquisition announcement. I define market-to-book ratio as the market value

of equity divided by the book value of equity, where book equity is equal to Total Assets – Total

Liabilities – Preferred Stock + Deferred Taxes + Convertible Debt (Kayhan and Titman (2007)).

I measure idiosyncratic volatility as the standard deviation of the acquirer’s daily stock return

minus the equal weighted market return from 205 days to 6 days prior to the acquisition

announcement (Moeller et al. (2007)).

To analyze acquisitions of public targets, I construct a new sample of recently public

firms that get acquired. This IPO sample consists of initial public offerings on the NYSE,

AMEX, and Nasdaq between January 1, 1985 and December 31, 2009. The firm had to be based

in the United States. I exclude utilities, unit offerings, rights offerings, REITs, and ADRs. I

20

remove IPO firms that had an offer price of less than $5, raised less than $5 million, or had an

unidentifiable PERMNO. The M&A sample consists of transactions announced between

January 1, 1985 and May 17, 2010, where both the acquirer and target must be based in the

United States and publicly traded. The deals must have been completed or withdrawn. I

eliminate financials and utilities. A maximum of 5% toehold could have existed prior to

announcement, and the acquirer must seek to own 100% of the target after the acquisition. I

eliminate observations that had material alternative news around the announcement period.

Merging the samples I find 1,404 acquisition announcements of firms in the IPO sample, and

1,216 completed acquisitions of those firms. I filter for VC-backed acquirers within 5 years of

their IPO making acquisitions of VC-backed targets within 3 years of their IPO, where

overlapping venture capitalists would be most likely, which results in 90 acquisition attempts.

For both bidders and targets, I use a market-adjusted 5-day window [-2,+2] to measure

cumulative abnormal returns [CARs], where the announcement date is day 0. I subtract off the

return to the CRSP value-weighted index over the same period to define cumulative abnormal

returns. All returns data is obtained from CRSP.

∑ ( )

where

21

I also look at market-adjusted 13-day window [-10,+2] to capture any short-term run-up

to the acquisition announcement. For robustness, I run the data with both the CRSP equal- and

value-weighted market indices.

As in Bradley et al (1988) and Mulherin and Boone (2000), combined return (or synergy

return) is defined as the value-weighted CAR of the transaction, where bidder and target values

are their respective market caps 3 trading days prior to the announcement date.

( ) ( ) ( ) ( )

( )

1.5 RESULTS

The Effect of Venture Capital Backing on M&A Activity

Table 1 demonstrates the strong inclination of VC-backed IPOs to acquire VC-backed

private targets in the five years following the IPO. Of the 188 VC-targets in my sample, 148

were acquired by VC-acquirers (78.7%). Of the 2,969 acquisitions in my full sample, VC-

acquirers made 1256 (42.3%) of all acquisitions, of which VC-targets represent 148 (11.8%) of

the acquisitions. This is interesting when compared to the activity of non-VC-backed acquirers,

where VC-targets make up only 2.3% of their acquisitions. A binomial test for the difference in

proportions was strongly significant.

Furthermore, of the 188 observed VC-backed private targets, 34 (18.1%) came from

acquirers that were backed by the same venture capital firm at the IPO. 114 (60.6%) came from

acquirers that were backed by different VC firms, and 40 (21.3%) came from acquirers that were

22

never VC-backed. This indicates that a VC-backed private target is nearly as likely to be

acquired by a firm that was backed by the same VC than any non-backed firm in the IPO sample.

This could of course be due to the VC’s tendency to invest in firms operating in high-tech

SIC codes. High-tech companies should be more likely to acquire high-tech targets, which could

present an omitted variable bias if I don’t control for industry effects. To account for this, I run a

logistic regression which includes control variables to determine the likelihood of acquiring a

VC-target. Table 2 shows a logistic regression where the dependent variable is a dummy that

equals 1 if the target is VC-backed and 0 if not. In addition to the dummy for VC-acquirer, I

include a dummy if the acquirer operates in a high-tech industry and a time variable to capture

any time trends or bubble effects. The VC-acquirer dummy is positive and significant in

determining the likelihood of acquiring a VC-backed private target.

It is clear from this data that VC-backed IPOs disproportionately acquire VC-backed

targets, even after accounting for industry. This is strong support for Hypothesis 1, that VC-

backed acquirers are more likely to acquire VC-backed private targets in the years following

their IPO.

Acquisition Announcement Returns

Table 3 Panel A shows acquirers’ 3-day cumulative abnormal returns for acquisition

announcements. My full sample of 2,969 acquisitions by public acquirers of private targets

appears similar to those in previous studies (Chang (1998), Fuller, Netter, and Stegemoller

(2002)), with a mean acquirer announcement return of 1.3%. But contrary to both Masulis and

Nahata (2011) and Gompers and Xuan (2009), I find that acquirer announcement CARs don’t

23

significantly differ for VC-backed targets than they do for non-VC-backed private targets (2.3%

vs. 1.3% respectively).

However, within the sample of VC-backed targets, SAME_VC transactions experience

larger returns than other acquisitions of VC-backed targets. SAME_VC acquisitions experience

mean returns of 4.7%, compared to 1.6% for DIFFERENT_VC transactions and approximately

0% for acquisitions of VC-targets by non-VC-acquirers. However, mean difference tests fail to

attain acceptable significance, which could be due to the presence of outliers in the small sample.

These results still show mild support for the information sharing hypothesis, and strong support

against the managerial hubris hypothesis.

With a sample of only 34 SAME_VC acquisitions, the results could be strongly affected

by statistical outliers. Panel B reports the results after Winsorizing the CARs data to account for

outliers. Winsorizing at the 1% and 99% tails increases significance in means and mean

differences without drastically altering the absolute values. Here, SAME_VC transactions

significantly outperform acquisitions of VC-targets by non-VC-acquirers (5.6% difference). The

difference between SAME_VC and DIFFERENT_VC acquisitions was 3.2%, but only

significant at the 20% level. This is further support for the information sharing hypothesis, and

strong support against the managerial hubris hypothesis. The information sharing that occurs

between a VC and a firm’s management appears to result in value-enhancing acquisitions of VC-

backed private targets, despite potential managerial hubris.

Segmenting the 34 SAME_VC acquisitions on whether or not management has changed

yields interesting results. For 26 of the 34 acquisitions, the CEO remained the same from the

IPO to the acquisition. Acquisitions where the CEO was different experience average

announcement CARs 4.1% larger than those acquisitions in which the CEO remained the same.

24

This runs counter to my prediction that the effect of the VC would decrease with management

turnover. However, a mean difference test was insignificant. The fact that 26 of the 34

acquisitions involved the same CEO is support for the lasting effect of venture backing on post-

IPO acquisition activity.

Segmenting the 34 SAME_VC acquisitions on whether or not the venture capitalist

served on the board at both the IPO and the acquisition also proves interesting. For 18 of the 34

acquisitions, the venture capitalist remained on the board from the IPO through the acquisition.

These acquisitions had a mean announcement CAR of nearly 7%, significantly different from

zero at the 5% level, but not significantly different from acquisitions in which the VC left the

board before the acquisition. Though lacking significance, this supports my prediction that the

effect of the VC will increase with board presence.

Multivariate Analysis of Acquirer Announcement CARs

Table 4 presents the results of ordinary least squares regressions. The dependent variable

is 3-day [-1, +1] acquirer announcement CARs, measured using market-adjusted returns on the

CRSP equal weighted index (Winsorized at the 1% and 99% tails). The results, though generally

insignificant, still tell a story. If the managerial hubris hypothesis were correct, the SAME_VC

variable would be a negative and significant determinant of acquirer announcement CARs. The

fact that it is positive and fails to significantly load in the regression indicates that I can reject the

managerial hubris hypothesis. This is further support that the market believes venture capitalists

don’t influence their previous successes to make value-destructive acquisitions.

Regression 1 shows that when acquiring a VC-backed private target, public acquirers fair

better if they were VC-backed at the IPO. Regression 2 shows that SAME_VC transactions are

25

likely to fair better, though the coefficient wasn’t strongly significant. In regression 3, I include

variables for management turnover and VC board presence at the acquisition. Interestingly,

these coefficients run against each other. VC board presence at the IPO and the acquisition has a

significantly positive effect on acquisition announcement CARs, while a static CEO has an

insignificantly negative effect. On one hand, this supports my prediction that VC board presence

would facilitate information sharing. On the other, it runs counter to my prediction that a change

in management would hinder information sharing.

Since VCs generally remain on the board for a few years after an IPO before stepping

down, it is possible that the VC board presence is picking up some characteristic of more recent

IPOs. Therefore, all regressions include a control variable that measures the number of years

from the IPO to the acquisition announcement date. This control variable is insignificant, so

from the regressions it is clear that information sharing is strongly facilitated by the VC’s

presence on the board, but not significantly affected by a change in management or the passage

of time. In addition, I include five other control variables in all regressions to account for other

possible determinants of announcement returns: 1) log of acquirer’s market cap at the

acquisition, which should be negatively related to acquirer CARs (Moeller, Schlingemann, and

Stulz (2004)), 2) a dummy variable for acquisitions financed with pure-equity, which should be

positively related to acquirer CARs since my sample is all private targets (Fuller, Netter, and

Stegemoller (2002)), 3) a dummy variable if the acquisition is in a different two-digit SIC code

to account for the possibility of empire building behavior (Morck et al. (1990)), 4) acquirer

idiosyncratic excess stock return volatility to account for information asymmetry, which should

be negatively related (Moeller, Schlingemann, and Stulz (2007)), 5) acquirer market-to-book

ratio as a proxy for Tobin’s Q (Lang et al (1991), Servaes (1991), Dong et al. (2006)). Size is the

26

only control variable to achieve significance at the 10% level. Though most controls lack

significance, in all regressions these controls have the proper sign as predicted by the literature.

Information Sharing Vs. Cheap Targets

Table 5 documents the remarkable returns to SAME_VC acquisitions of public targets by

public acquirers. I identify 90 acquisitions of VC-backed targets within 3 years of their IPO by

VC-backed acquirers within 5 years of their IPO. I searched the IPO and merger documents on

EDGAR to identify overlapping board presence and shareholdings by the same venture capital

firm. While I only have 3 observations of SAME_VC public/public acquisitions, the returns to

these acquisitions lend evidence in favor of the information sharing hypothesis and strongly

against the cheap target hypothesis.

The average 5-day value-weighted announcement return to the target was 50.4%. This is

28.9% higher than the average of similar acquisitions involving different venture capitalists. The

average 5-day value-weighted announcement return to the acquirer was 5.6%, compared to an

average of -4.3% for similar acquisitions with different VCs. The 5-day value-weighted

combined announcement return, a metric more aligned with the overall quality of the business

combination, was 11.7%. This can be compared to the average of -0.6% for similar acquisitions

without an overlapping venture capitalist. Looking at these announcement returns, it is obvious

that the market reacts very well to acquisitions involving firms that share a venture capitalist.

The cheap target hypothesis argues that the positive announcement return to acquirers in

SAME_VC acquisitions is due to the venture capitalist selling the target firm cheap due to the

self-dealing interests of the venture capitalist. This is describing a wealth transfer from target

firm shareholders to acquiring firm shareholders. If this were the case, the acquirer

27

announcement return would be more positive than expected, the target announcement return (a

proxy for the premium paid in acquisition) would be lower than expected, and the combined

announcement return would be no different than expected. However, my data shows that all

three announcement returns are drastically higher than expected, strongly supporting the

information sharing hypothesis rather than the cheap target hypothesis.

Table 6 further documents this effect, laying out multivariate regression results for target,

acquirer, and combined announcement returns. A dummy variable for the presence of

overlapping board representation of the same venture capitalist is positive and significant in

explaining all three announcement returns. This is further evidence for the information sharing

hypothesis.

Discussion of Results

It is clear from my results that the market believes venture capitalists are not leveraging

their relationship with acquiring firm management to encourage overbidding which would result

in value-destructive acquisitions. An obvious question is, why not?

It could be that the venture capitalist’s role in the acquiring firm presents legal

disincentives for acting in their own self-interest. In 18 of the 34 SAME_VC acquisitions, the

VC sat on the board of directors at the IPO and the acquisition. In these instances, the VC is

expected to act in the interest of shareholders. If this were the case, I’d expect to see higher

acquirer announcement CARs for firms in which the VC remains on the board at the acquisition

and is therefore bound not to act self-interested. While I don’t find a significant difference in

means for acquisitions in which the VC remains on the board and those where the VC did not

(7% and 2.3% respectively), I do find that it is significant in my regression at the 10% level. Of

28

course, I predicted that information sharing would also be facilitated by VC presence on the

board, which would also explain this result.

More likely, reputational concerns deter venture capitalists from over-exerting their

influence on management for the VC’s own benefit. Gompers (1996) and Krishnan, Ivanov,

Masulis, and Singh (2010) point out that reputational concerns are important to venture

capitalists, as they repeatedly bring companies public. Reputation affects the VC firm’s ability

to certify companies, raise new funds, and gain access to quality deal flow. Other recent

literature has shown the importance of networks in the venture capitalist industry, providing

further evidence on the importance of reputation (Hochberg, Ljungqvist, and Lu 2007). The

results of my event study indicate that the market believes that venture capitalists avoid selfish

one-time wealth transfers in favor of long-run value maximization through improved reputation

and strong networks.

1.6 CONCLUSION

I find that venture capitalists continue to affect firm M&A decisions well after the initial

public offering, but that this results in higher returns to acquiring firm shareholders. The

information sharing that occurs between a VC and a firm’s management appears to result in

value-enhancing acquisitions of VC-backed private targets, despite the potential for elevated

managerial hubris or self-dealing. I reject the managerial hubris hypothesis that venture

capitalist are using their role as information conduit to encourage overbidding at the expense of

acquiring firm shareholders. I also demonstrate that the information sharing present in the sale

of private targets to public acquirers holds in acquisitions of public targets as well, allowing me

to reject the cheap targets hypothesis. Using this sample of public targets, I reject the cheap

29

targets hypothesis that argues venture capitalists are self-dealing in these transactions selling

target firms cheap as they have an interest in the acquirer as well. This paper demonstrates a

further mechanism through which venture capitalists can add value to corporations.

30

TABLE 1.1

The Effect of Venture Capital Backing on M&A Activity for Recent IPOs Sample is comprised of 2,969 acquisitions from 1996-2006 of private targets by public firms within 5 years of their

IPO. Acquirers must be companies that went public between 1996-2005, listed on the NYSE, Nasdaq, or AMEX,

with an offering price of at least $5, excluding financials and utilities. Within the sample, there are 188 VC-backed

private targets and 2781 non-backed private targets. ***, **, and * denote significantly different from zero at the 1,

5, and 10 percent levels respectively (binomial test for difference in proportions).

PANEL A: FULL SAMPLE (n=2,969)

Private Targets

Public Acquirers VC Backed Non VC Backed

VC Backed At IPO

Acquisitions 148 1108

Row % 11.8% 88.2%

Non VC Backed At IPO

Acquisitions 40 1673

Row % 2.3% 97.7%

Difference 9.5%***

PANEL B: VC-BACKED PRIVATE TARGETS (n=188)

VC-backed Private Targets

Public Acquirers SAME VC DIFF VC

VC Backed At IPO

Acquisitions 34 114

% of n 18.1% 60.6%

Non VC Backed At IPO

Acquisitions 40

% of n 21.3%

PANEL C: AVERAGE YEARS BETWEEN IPO AND ACQUISITION

Public Acquirer

SAME VC DIFF VC NON VC

Mean (years) 1.81 1.68 1.97

Median (years) 1.47 1.22 1.77

n 34 114 40

31

TABLE 1.2

Logistic Regression for Likelihood That Target is VC-backed Sample is comprised of 2,969 acquisitions from 1996-2006 of private targets by public firms within 5 years of their

IPO. Within the sample, there are 188 VC-backed private targets and 2781 non-backed private targets. VC_TGT is

the dependent variable, which equals 1 if the target was VC-backed. VC_AQ equals 1 if the acquirer was VC-

backed at its IPO. TECH_SIC is a dummy if the firm operates in one of the following high-tech SIC codes:

283,481,365,366,367,368,369,482,483,484,485,486,487,488,489,357,or 737. Year is the year in which the acquisition was

announced to capture possible time trends or bubble effects. Acquirers must be companies that went public between

1996-2005, listed on the NYSE, Nasdaq, or AMEX, with an offering price of at least $5, excluding financials and

utilities. ***, **, and * denote significance at the 1, 5, and 10 percent levels respectively.

Logistic Model: VC_TGT = VC_AQ + TECH_SIC + YEAR

Estimate Std Errors Wald Chi-Sq Pr > Chi Sq

Intercept -138.0* 71.953 3.6776 0.0551

VC_AQ 1.1831*** 0.1905 38.5717 <.0001

TECH_SIC 1.7016*** 0.2063 68.041 <.0001

YEAR 0.0668* 0.036 3.4421 0.0636

32

TABLE 1.3

Acquirer CARs in Acquisitions of Private Targets Sample is comprised of 2,969 acquisitions from 1996-2006 of private targets by public firms within 5 years of their

IPO. Acquirers must be companies that went public between 1996-2005, listed on the NYSE, Nasdaq, or AMEX,

with an offering price >$5, excluding financials and utilities. Cumulative abnormal return is calculated using a

market-adjusted returns method subtracting the return on the CRSP equal-weighted index over a 3-day window

[-1,+1] surrounding the announcement date. SAME CEO equals 1 if the CEO was the same at the IPO and

acquisition, 0 if not. VC ON BRD = 1 if the same venture capitalist was on the firm’s board at both the IPO and the

acquisition, 0 if not. In Panel B, sub-sample data is Winsorized as the 1% and 99% tails with a minimum of 1

observation winsorized at each end. ***, **, and * denote significantly different from zero at the 1, 5, and 10

percent levels respectively (two-tailed t test for means, signed rank test for medians).

PANEL A: ACQUIRER ANNOUNCEMENT RETURNS (CAR [-1,+1])

N Mean p-value Median p-value % > 0

FULL SAMPLE 2969 0.013*** <.0001 0.006*** <.0001 55.6%

NON-VC TARGETS 2781 0.013*** <.0001 0.006*** <.0001 55.8%

VC-BACKED TARGETS 188 0.017* 0.08 0.005 0.25 52.7%

NON-VC ACQUIRER 40 -0.008 0.54 -0.008 0.36 45.0%

VC-BACKED ACQUIRER 148 0.023** 0.04 0.009 0.10 54.7%

DIFFERENT VC 114 0.016 0.17 0.005 0.36 52.6%

SAME VC 34 0.047 0.13 0.033* 0.09 61.8%

SAME CEO 26 0.037 0.33 0.022 0.35 57.7%

DIFFERENT CEO 8 0.079 0.11 0.071* 0.08 75.0%

VC ON BOARD 18 0.052 0.21 0.043* 0.03 83.3%

VC NOT ON BOARD 16 0.041 0.40 -0.018 1.00 37.5%

PANEL B: WINSORIZED ACQUIRER ANNOUNCEMENT RETURNS (CAR [-1,+1])

VC-BACKED TARGETS 188 0.016* 0.06 0.005 0.23 52.7%

NON-VC ACQUIRER 40 -0.009 0.44 -0.008 0.35 45.0%

VC-BACKED ACQUIRER 148 0.023** 0.03 0.009* 0.09 54.7%

DIFFERENT VC 114 0.015 0.19 0.005 0.36 52.6%

SAME VC 34 0.048** 0.04 0.033* 0.08 61.8%

SAME CEO 26 0.038 0.15 0.022 0.31 57.7%

DIFFERENT CEO 8 0.079 0.11 0.071* 0.08 75.0%

VC ON BOARD 18 0.070** 0.03 0.043** 0.02 83.3%

VC NOT ON BOARD 16 0.023 0.50 -0.018 1.00 37.5%

PANEL C: MEAN DIFFERENCES Difference p-value

(VC AQ) - (NON VC AQ) 0.031** 0.04

(SAME VC) - (DIFF VC) 0.032 0.18

(SAME VC) - (NON VC AQ) 0.056** 0.03

(DIFF VC) - (NON VC AQ) 0.024 0.14

(DIFF CEO) - (SAME CEO) 0.041 0.44

(VC BOARD) - (VC NOT BOARD) 0.047 0.29

33

TABLE 1.4

Multivariate Analysis of Acquirer Cumulative Abnormal Announcement Returns This table reports ordinary least squares estimates. Sample is comprised of 2,969 acquisitions from 1996-2006 of

private targets by public firms within 5 years of their IPO. Acquirers must be companies that went public between

1996-2005, listed on the NYSE, Nasdaq, or AMEX, with an offering price >$5, excluding financials and utilities.

Cumulative abnormal return is calculated using a market-adjusted returns method subtracting the return on the

CRSP equal-weighted index over a 3-day window [-1,+1] surrounding the announcement date. The dependent

variable is Winsorized at the 1% and 99% tails. ***, **, and * denote significantly different from zero at the 1, 5,

and 10 percent levels respectively (p-values in brackets).

OLS REGRESSIONS

Dependent Variable = CAR [-1, +1]

(1) (2) (3) (4)

VC ACQUIRER 0.041*

[0.09] 0.035

[0.14]

0.036

[0.12]

0.035

[0.14]

SAME VC 0.025

[ 0.27]

0.032

[ 0.47]

VC ON BOARD 0.074*

[0.07]

0.066

[0.11]

SAME CEO -0.030

[0.39]

-0.056

[0.27]

LOG SIZE -0.009**

[0.04]

-0.009*

[ 0.06]

-0.010**

[0.04]

-0.009*

[ 0.06]

M/B RATIO -0.009

[0.79]

-0.008

[0.82]

-0.011

[0.73]

-0.007

[0.84]

ALL STOCK 0.018

[0.35]

0.015

[ 0.45]

0.019

[0.34]

0.018

[0.36]

DIFFERENT SIC 0.010

[ 0.62]

0.009

[ 0.62]

0.010

[0.59]

0.008

[0.66]

VOLATILITY -0.560

[ 0.22]

-0.539

[0.24]

-0.522

[0.26]

-0.543

[0.24]

TIME SINCE IPO 0.007

[ 0.34]

0.006

[ 0.38]

0.006

[ 0.36]

0.006

[0.39]

Adjusted R2 0.010 0.011 0.019 0.016

n 188 188 188 188

INDEPENDENT VARIABLE DEFINITIONS

VC ACQUIRER Equals 1 if the acquirer was VC-backed at its IPO

SAME VC Equals 1 if the acquirer and the target were backed by the same VC firm

SAME CEO Equals 1 if the CEO was the same at the IPO and at the acquisition

VC ON_BOARD Equals 1 if the VC in question was on the board at the IPO and acquisition

TIME SINCE IPO Years from the acquirer's IPO to the announcement date of the acquisition

LOG SIZE Log of acquirer's market capitalization at announcement date

ALL STOCK Equals 1 if the transaction was financed with 100% stock

DIFFERENT SIC Equals 1 if the acquirer and the target operate in different two-digit SIC code

VOLATILITY Std deviation of excess acquirer stock returns from 205 to 6 days prior

M/B RATIO Acquirer’s market value of equity divided by book value of equity

*TECH SIC defined as being in 283,481,365,366,367,368,369,482,483,484,485,486,487,488,489,357,or 737

34

TABLE 1.5

Announcement CARs in Acquisitions of Young VC-backed Public Targets

by Young VC-backed Public Acquirers This table reports target, acquirer, and combined cumulative abnormal announcement returns. Same VC indicates that target and acquirer had concurrent board

representation of the same venture capital firm at their respective IPOs and at the acquisition announcement. DIFF VC indicates that the acquirer and target were

both VC-backed at the IPO, the acquirer was within 5 years of its IPO, and the target was within 3 years of its IPO. Equal (Value) indicates that the CRSP equal

(value) weighted index was used in calculating market adjusted returns. IPO sample consists of initial public offerings on the NYSE, AMEX, and Nasdaq

between January 1, 1985 and December 31, 2009. The firm had to be based in the United States. I exclude utilities, unit offerings, rights offerings, REITs, and

ADRs. I remove IPO firms that had an offer price of less than $5, raised less than $5 million, or had an unidentifiable PERMNO. The M&A sample consists of

transactions announced between January 1, 1985 and May 17, 2010, where both the acquirer and target must be based in the United States and publicly traded.

The deals must have been completed or withdrawn. I eliminate financials and utilities. A maximum of 5% toehold could have existed prior to announcement,

and the acquirer must seek to own 100% of the target after the acquisition. Merging the samples results in 1,404 acquisition announcements of firms in the IPO

sample, and 1,216 completed acquisitions of those firms. Screening for acquirers within 5 years of their IPO making acquisitions of targets within 3 years of their

IPO results in 90 acquisition attempts. ***, **, and * denote significance at the 1, 5, and 10 percent levels respectively.

Mean CARs Same VC (1) Diff VC (2) All Others (3)

(1)-(2) (1)-(3)

Target [-2,+2] CAR (Equal) 50.07% 21.19% 24.41%

28.88%

25.66% ***

Target [-2,+2] CAR (Value) 50.44% 21.52% 24.61%

28.92% *

25.83% ***

Target [-10,+2] CAR (Equal) 71.76% 23.86% 28.83%

47.90% **

42.93% ***

Target [-10,+2] CAR (Value) 74.20% 24.47% 29.43%

49.73% **

44.77% ***

Acquirer [-2,+2] CAR (Equal) 5.21% -4.66% -2.02%

9.87%

7.23% ***

Acquirer [-2,+2] CAR (Value) 5.58% -4.33% -0.33%

9.91%

5.91%

Acquirer [-10,+2] CAR (Equal) 12.18% -4.13% -0.92%

16.31%

13.10% **

Acquirer [-10,+2] CAR (Value) 14.62% -3.51% -0.33%

18.13%

14.95%

Combined CAR (Equal Weighted) 11.32% -0.88% 1.07%

12.20%

10.25% ***

Combined CAR (Value Weighted) 11.69% -0.55% 1.28%

12.24%

10.41% ***

n 3 87 1314

35

TABLE 1.6

Multivariate Analysis of Target, Acquirer, and Combined Announcement Returns in Acquisitions

of Young VC-backed Public Targets by Young VC-backed Public Acquirers This table reports ordinary least squares estimates for acquisitions of targets within three years of their IPO by acquirers within 5 years of their IPO. Same VC

indicates that target and acquirer had concurrent board representation of the same venture capital firm at their respective IPOs and at the acquisition

announcement. DIFF VC indicates that the acquirer and target did not have the same VC concurrently sitting on their board, or the information was not

identifiable on EDGAR. Equal (Value) indicates that the CRSP equal (value) weighted index was used in calculating market adjusted returns. The sample

formation is described in the methodology section. The sample consists of 1,404 acquisition announcements of firms in the IPO sample, and 1,216 completed

acquisitions of those firms. Filtering for VC-backed acquirers within 5 years of their IPO making acquisitions of VC-backed targets within 3 years of their IPO

results in 90 acquisition attempts. Diversifying acquisition equals 1 if the firms operated in different 2-digit SIC codes. Tender offer equals 1 if the bid was a

tender offer. All Stock equals 1 if the offer was a 100% stock offer. ln(Acquirer (Target) Market Cap) is the natural log of the acquirer’s (target’s) share price 3-

days prior to the announcement multiplied by the shares outstanding. Relative size is the target’s market cap divided by the acquirer’s market cap. Tech Bubble

equals 1 is the acquisition was in the years 1998,1999, or 2000. ***, **, and * denote significance at the 1, 5, and 10 percent levels respectively.

Dependent Variable Target [-2,+2] CAR Acquirer [-2,+2] CAR Combined [-2,+2] CAR

Coeff. p-value Coeff. p-value Coeff. p-value

Intercept 0.623 ** 0.020

0.175

0.291

0.360 ** 0.017

Same VC 0.375 ** 0.016

0.176 * 0.069

0.206 ** 0.019

Diversifying Acquisition -0.077 0.289

0.058 0.197

0.045 0.267

Tender Offer 0.175 0.124

-0.143 ** 0.045

-0.112 * 0.081

All Stock 0.062 0.419

-0.045 0.354

-0.029 0.499

ln(Acquirer Market Cap) 0.202 *** <.0001

0.039 0.189

0.000

1.000

ln(Target Market Cap) -0.272 *** <.0001

-0.064 ** 0.037

-0.029

0.295

Relative Size 0.182

0.288

0.137

0.202

-0.014

0.882

Tech Bubble (1998-2000) 0.048

0.411

0.012

0.733

0.002

0.944

N 90

90

90

Adj R-squared 0.464 0.083 0.096

36

CHAPTER 2

The Information Role of Venture Capitalists on Boards of Target Firms

2.1 INTRODUCTION

On February 14, 2002, PayPal Inc. held their initial public offering. Just 144 days later,

on July 8, 2002, eBay Inc. announced that it had entered an agreement to buy PayPal for nearly

$1.5 billion, an 18% premium over the previous day’s closing price, and an 82% premium over

PayPal’s IPO offering price. Prior to PayPal’s IPO, eBay had repeatedly been in negotiations to

buy PayPal. These attempts ultimately failed. At both the time of the IPO and the time of the

acquisition, several venture capitalists sat on PayPal’s board of directors. This leads one to

wonder why PayPal would go through the expensive IPO process just to sell the firm to eBay 4.5

months after the IPO. Zingales (1995) would argue that this is precisely why PayPal went

public, to intentionally create a free-riding shareholder problem with which to extract the surplus

in negotiation. In this context, it would appear that PayPal went public in order to extract a

higher premium in negotiating the later sale of the firm to eBay.