vellekoop

DESCRIPTION

ujTRANSCRIPT

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Path-Dependent Dividendsand the American Put Option

M.H. Vellekoop1 J.W. Nieuwenhuis2

1Department of Applied MathematicsUniversity of Twente

2Department of Economics and Business AdministrationUniversity of Groningen

Numerical Methods in Finance, Paris 2009

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Outline

1 Problem FormulationStandard Black-Scholes-Merton ModelIncluding DividendsAssumptions

2 Main TheoremEarly Exercise Premium with DividendsCalculating the Optimal Exercise Boundary

3 Numerical ResultsKnock Out Dividend ModelProportional Cash Dividend ModelFixed Cash Dividend Model

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Standard Black-Scholes-Merton ModelIncluding DividendsAssumptions

Standard Equity Model

Consider the standard Black-Scholes-Merton model for stock and bond prices

dSt = rStdt + σStdWt

dBt = rBtdt

for time period t ∈ [0, T ] with

S0, B0, r , σ given strictly positive constants and

W a one-dimensional Brownian Motion on the filtered probability space(Ω,F , (Ft)t∈[0,T ], Q).

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Standard Black-Scholes-Merton ModelIncluding DividendsAssumptions

American and European Put Options

Let AP and EP denote the American and European Put price processes forthe maturity T and a strike K > 0:

EPt = EQ[ BtBT

(K − ST )+ | Ft ]def= E(t , St)

APt = ess supτ∈T[t,T ]

EQ[ BtBτ

(K − Sτ )+ | Ft ]def= A(t , St)

where T[t,T ] is the set of all stopping times with values in [t , T ].Optimal stopping problem for American Put has the solution

τ∗ = infu ≥ t : A(u, Su) = (K − Su)+ = infu ≥ t : Su ≤ S∗u

where S∗ denotes what is called the optimal exercise boundary.

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Standard Black-Scholes-Merton ModelIncluding DividendsAssumptions

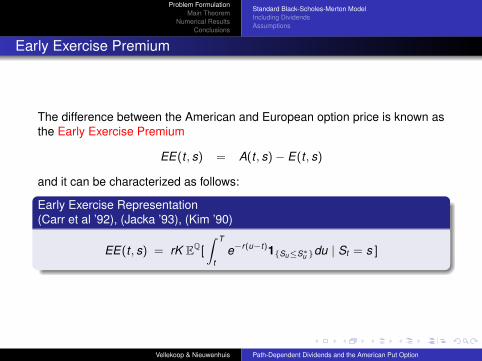

Early Exercise Premium

The difference between the American and European option price is known asthe Early Exercise Premium

EE(t , s) = A(t , s)− E(t , s)

and it can be characterized as follows:

Early Exercise Representation(Carr et al ’92), (Jacka ’93), (Kim ’90)

EE(t , s) = rK EQ[

∫ T

te−r(u−t)1Su≤S∗u du | St = s ]

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Standard Black-Scholes-Merton ModelIncluding DividendsAssumptions

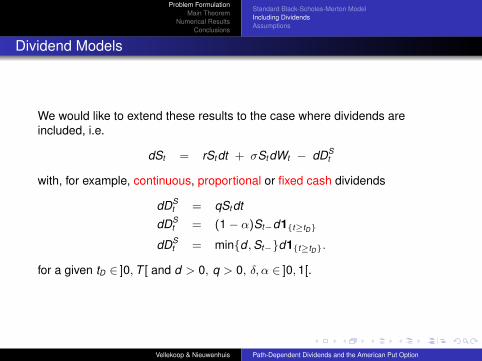

Dividend Models

We would like to extend these results to the case where dividends areincluded, i.e.

dSt = rStdt + σStdWt − dDSt

with, for example, continuous, proportional or fixed cash dividends

dDSt = qStdt

dDSt = (1− α)St−d1t≥tD

dDSt = mind , St−d1t≥tD.

for a given tD ∈ ]0, T [ and d > 0, q > 0, δ, α ∈ ]0, 1[.

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Standard Black-Scholes-Merton ModelIncluding DividendsAssumptions

Path-Dependent Dividend

Here, we focus on ’knock-out’ version of proportional dividends:

dDSt = (1− α)St−1 min

u∈[0,td ]Su ≥ δS0

d1t≥td

This models the fact that the company which issued the stock will only paydividends if the stock price has not fallen below the level δS0 before thedividend date.

This obviously makes the dividend path-dependent.

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Standard Black-Scholes-Merton ModelIncluding DividendsAssumptions

Path-Dependent Dividend

European Put option with knockout dividends can be priced in closed form:

Lemma

For general α ∈ ]0, 1] and mt ≥ δS0 we have that the European put optionprice E(t , St) with strike K and maturity T equals, for all t ∈ [0, T ],

PK ,T (t , St) + 1t<td Ke−r(T−t)(

htd ,T (δS0, K ) − Lβt htd ,T ( St

Lt, K

L2t))

−1t<td e−r(T−t)(

Htd ,T (δS0, K ) − L2+βt Htd ,T ( St

Lt, K

L2t))

with Lt = δS0St

, β = 2rσ−2 − 1 and

Ht1,t2(x1, x2) = αEQ[St2 1St2

≤x2α

, St1>x1

| Ft ]

− EQ[St2 1St2≤x2, St1

>x1| Ft ]

ht1,t2(x1, x2) = Q(St1 > x1, x2 < St2 ≤x2α| Ft )

where S is the asset process with zero dividends.

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Standard Black-Scholes-Merton ModelIncluding DividendsAssumptions

Dividend Model Assumptions

In more general setup, we assume1 S is an adapted càdlàg semimartingale, Markov, and distribution of St

has a density for all t2 DS is an adapted, increasing càdlàg semimartingale, continuous in all

but countable number of time points3 S/B +

∫dDS/B is a Q-martingale, and the functions

x → EQ[Φ(Su) | St = x ], x → EQ[

∫ u

tdDS

v /Bv | St = x ]

are increasing for all 0 ≤ t < u ≤ T and for all increasing functionsΦ : R → R.

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Standard Black-Scholes-Merton ModelIncluding DividendsAssumptions

Dividend Model Assumptions

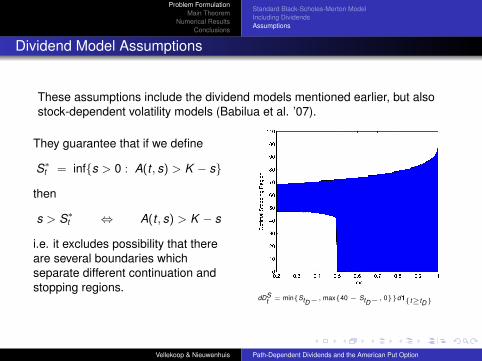

These assumptions include the dividend models mentioned earlier, but alsostock-dependent volatility models (Babilua et al. ’07).

They guarantee that if we define

S∗t = infs > 0 : A(t , s) > K − s

then

s > S∗t ⇔ A(t , s) > K − s

i.e. it excludes possibility that thereare several boundaries whichseparate different continuation andstopping regions.

dDSt = minStD−

, max40 − StD−, 0d1t≥tD

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Early Exercise Premium with DividendsCalculating the Optimal Exercise Boundary

Early Exercise Premium with Dividends

For stock price models with dividends, the early exercise premium can becharacterized as follows:

Theorem (Early Exercise Representation including Dividends)

Under the assumptions stated above, and the additional assumption that theoptimal exercise boundary S∗ is continuous apart from at most a countablenumber of points, the American and European Put price processes satisfy

APt − EPt = −Bt EQ[

∫ T

t1Su−≤S∗u ∧∆Su=0(d( K

Bu) +

dDSu

Bu) | Ft ].

Continuity of optimal exercise boundary is subject of ongoing research, incollaboration with CERMICS.

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Early Exercise Premium with DividendsCalculating the Optimal Exercise Boundary

Part I

First prove that s → A(t , s) is Lipschitz continuous, uniformly over t

Apply Meyer-Ito formula for convex mappings to the processX = (AP − K + S)/B.

Use the fact that AP/B, as Snell envelope of upper semicontinuousprocess, is a continuous positive supermartingale, and

that S∗t is continuous apart from a countable number of points,

to show that the local time of X in zero equals zero.

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Early Exercise Premium with DividendsCalculating the Optimal Exercise Boundary

Part II

Since S/B +∫

dDS/B is a Q-martingale, it turns out that the remainingtechnical point is to prove that∫ t

01Su−>S∗u d( APu

Bu)

is also a martingale under Q.

We do this by extending earlier defined methods (El Karoui ’79, Karatzas& Shreve ’88, Jacka ’93) for optimal stopping problems, exploiting thefact that we may show that we should never stop in points where S isdiscontinuous.

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Early Exercise Premium with DividendsCalculating the Optimal Exercise Boundary

Integral equation for Optimal Exercise Boundary

Inserting s = S∗t as initial condition at time t gives

Corollary

Under the assumptions of the previous theorem, the optimal exerciseboundary satisfies

K − S∗t =

E(t , S∗t )− Bt EQ[

∫ T

t1Su−≤S∗u ∧∆Su=0(d( K

Bu) +

dDSu

Bu) | St = S∗t ].

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Knock Out Dividend ModelProportional Cash Dividend ModelFixed Cash Dividend Model

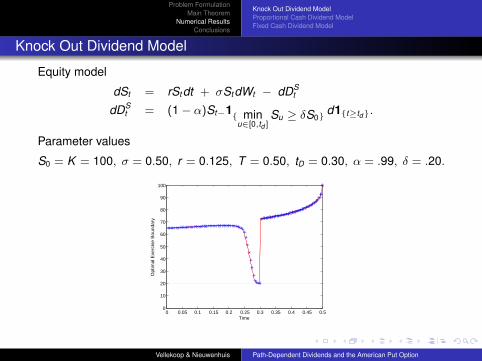

Knock Out Dividend Model

Equity model

dSt = rStdt + σStdWt − dDSt

dDSt = (1− α)St−1 min

u∈[0,td ]Su ≥ δS0

d1t≥td.

Parameter values

S0 = K = 100, σ = 0.50, r = 0.125, T = 0.50, tD = 0.30, α = .99, δ = .20.

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.4 0.45 0.50

10

20

30

40

50

60

70

80

90

100

Time

Opt

imal

Exe

rcis

e B

ound

ary

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Knock Out Dividend ModelProportional Cash Dividend ModelFixed Cash Dividend Model

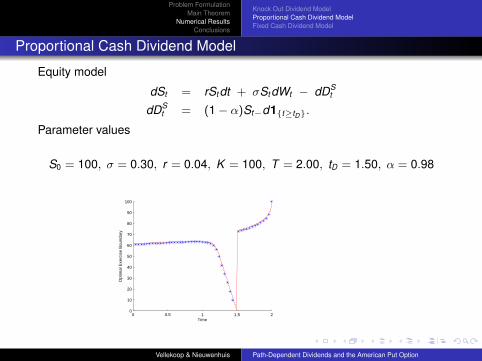

Proportional Cash Dividend Model

Equity model

dSt = rStdt + σStdWt − dDSt

dDSt = (1− α)St−d1t≥tD.

Parameter values

S0 = 100, σ = 0.30, r = 0.04, K = 100, T = 2.00, tD = 1.50, α = 0.98

0 0.5 1 1.5 20

10

20

30

40

50

60

70

80

90

100

Time

Opt

imal

Exe

rcis

e B

ound

ary

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Knock Out Dividend ModelProportional Cash Dividend ModelFixed Cash Dividend Model

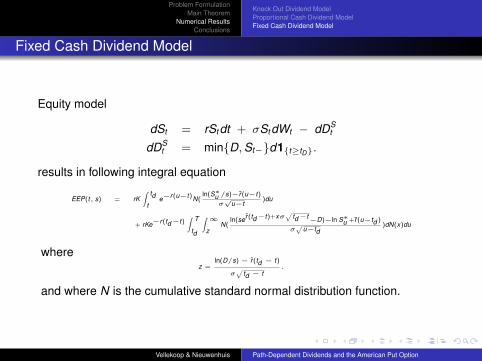

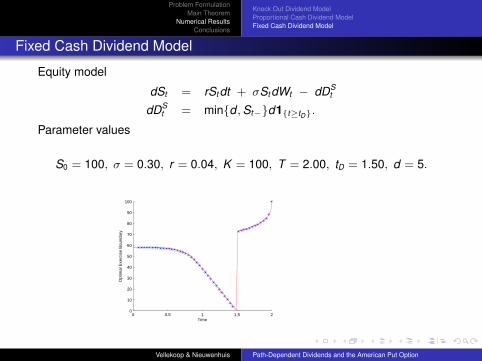

Fixed Cash Dividend Model

Equity model

dSt = rStdt + σStdWt − dDSt

dDSt = minD, St−d1t≥tD.

results in following integral equation

EEP(t, s) = rK∫ td

te−r(u−t)N(

ln(S∗u /s)−r(u−t)σ√

u−t)du

+ rKe−r(td−t)∫ T

td

∫ ∞z

N(ln(ser(td−t)+xσ

√td−t−D)−ln S∗u +r(u−td )

σ√

u−td)dN(x)du

wherez =

ln(D/s) − r(td − t)

σ√

td − t.

and where N is the cumulative standard normal distribution function.

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Knock Out Dividend ModelProportional Cash Dividend ModelFixed Cash Dividend Model

Fixed Cash Dividend Model

Equity model

dSt = rStdt + σStdWt − dDSt

dDSt = mind , St−d1t≥tD.

Parameter values

S0 = 100, σ = 0.30, r = 0.04, K = 100, T = 2.00, tD = 1.50, d = 5.

0 0.5 1 1.5 20

10

20

30

40

50

60

70

80

90

100

Time

Opt

imal

Exe

rcis

e B

ound

ary

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Problem FormulationMain Theorem

Numerical ResultsConclusions

Conclusions

We extended the early exercise representation formula to a rathergeneral model for stocks with ’knock-out’ dividends.

However, we need to assume that the optimal exercise boundary iscontinuous apart from a countable number of points in time.

Establishing how to prove this a priori is known to be hard, and is thesubject of ongoing research.

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Appendix References

References I

P. Babilua, I. Bokuchava, B. Dochviri, and M. Shashiashvili.The American put option in a one-dimensional diffusion model withlevel-dependent volatility.Stochastics, 79:5–25, 2007.

P. Carr, R. Jarrow, and R. Myneni.Alternative characterizations of American puts.Mathematical Finance, 2:87–106, 1992.

N. El Karoui.Les aspects probabilistes du contrôle stochastique, Lecture Notes inMathematics 876.Springer-Verlag, Berlin, 1981.

S.D. Jacka.Local times, optimal stopping and semimartingales.Annals of Probability, 21:329–339, 1993.

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option

university-logo

Appendix References

References II

S. Kallast and A. Kivinukk.Pricing and hedging American options using approximations by Kimintegral equations.European Finance Review, 7:361–383, 2003.

I.J. Kim.The analytical valuation of American options.Review of Financial Studies, 3:547–472, 1990.

G. Peskir.On the American option problem.Mathematical Finance, 15:169–181, 2005.

Vellekoop & Nieuwenhuis Path-Dependent Dividends and the American Put Option