vce accounting - specifications and sample€¦ · examination specifications overall conditions...

TRANSCRIPT

VCE Accounting 2013–2016Written examination

Examination specifications

Overall conditionsThe examination will be sat at a time and date to be set annually by the Victorian Curriculum and Assessment Authority. VCAA examination rules will apply. Details of these rules are published annually in the VCE and VCAL Administrative Handbook.There will be 15 minutes reading time and 2 hours writing time.The examination will be marked by a panel appointed by the VCAA.The examination will contribute 50 per cent to the Study Score.

ContentThe VCE Accounting Study Design 2013–2016 is the document for the development of the examination. The study design includes the Characteristics of the Study (pages 12–16). Questions will be based on the key knowledge and key skills that underpin the outcomes in Units 3 and 4. Students will be required to apply the knowledge and skills of the accounting processes undertaken in Units 3 and 4.Students will not be required to use information and communications technology (ICT) in the examination.Students will not be required to undertake calculations relating to financial indicators in the examination; however, the underpinning knowledge, interpretation and analysis associated with these indicators are examinable.Students will not be required to prepare graphical representations in the examination; however, the explanation and interpretation of graphical representations are examinable.

FormatThe examination will consist of a series of short answer and extended response questions. These may include a variety of item types, including scenarios, questions with multiple parts, short answer questions and extended response questions. All questions in the examination will be compulsory.The total marks for the examination will be 100.The examination will be in the form of a question book and an answer book.

Approved materials and equipment• normal stationery requirements (pens, pencils, highlighters, erasers, sharpeners and rulers)• one scientific calculator

AdviceDuring the 2013–2016 accreditation period for the VCE Accounting Study Design, examinations will be prepared according to the examination specifications above. The examination will assess a representative sample of the key knowledge and key skills from Unit 3 and Unit 4.

© VICTORIAN CURRICULUM AND ASSESSMENT AUTHORITY 2012

July 2012

The accreditation period for VCE Accounting has been extended to 31 December 2018.

VCE Acounting (Specifications and sample) – July 2012 2

The following sample examination is intended to demonstrate the format and type of questions that teachers and students can expect on the end-of-year Accounting examination. Teachers and students should be aware of the Characteristics of the Study, including accounting principles and qualitative characteristics, as described on pages 12–16 of the study design.The VCAA does not publish answers for sample examinations.The following documents should be referred to in relation to the VCE Accounting examination.• VCE Accounting Study Design 2013–2016• VCE Accounting Assessment Handbook 2013–2016• VCAA Bulletin VCE, VCAL and VETIt is recommended that students write in pencil when answering questions that involve calculations.

S A M P L E

ACCOUNTINGWritten examination

Day Date Reading time: *.** ** to *.** ** (15 minutes) Writing time: *.** ** to *.** ** (2 hours)

QUESTION BOOK

Structure of bookNumber of questions

Number of questions to be answered

Number of marks

11 11 100

• Studentsarepermittedtobringintotheexaminationroom:pens,pencils,highlighters,erasers,sharpeners,rulersandonescientificcalculator.

• StudentsareNOTpermittedtobringintotheexaminationroom:blanksheetsofpaperand/orwhiteoutliquid/tape.

Materials supplied• Questionbookof10pages.• Answerbookof17pages.

Instructions• Writeyourstudent numberinthespaceprovidedonthefrontpageoftheanswerbook.• Answerallquestionsintheanswerbook.

• AllwrittenresponsesmustbeinEnglish.

At the end of the examination• Youmaykeepthisquestionbook.

Students are NOT permitted to bring mobile phones and/or any other unauthorised electronic devices into the examination room.

©VICTORIANCURRICULUMANDASSESSMENTAUTHORITY2012

July2012

Victorian Certificate of Education Year

ACCNTEXAMQB(SAMPLE) 2 July2012

Question 3–continued

Question 1 (2 marks)Define theterm ‘doubleentryaccountingsystem’.

Question 2 (11 marks)MarkBrownownsandoperatesMark’sMegaMovers.HehasprovidedhisaccountantwiththefollowinggraphdisplayingdetailsofhisNon-CurrentAssets.Hepurchasedthemallon1July2009.

Historical Cost

Depreciation – 2009–10

Depreciation – 2010–11

Depreciation – 2011–12

Depreciation – 2012–13

Accumulated Depreciation – 30 June 2013

Construction Equipment

ComputerEquipment

Tools and Equipment

Fixtures andFittings

45 000

40 000

35 000

30 000

25 000

20 000

15 000

10 000

5 000

0

a. Usingthegraph,identifyandjustifytheselectionofthedepreciationmethodusedforthe• ConstructionEquipment• FixturesandFittings.

4marks

b. GiventhattheConstructionEquipmentwasdepreciatedusingarateof30%perannum,calculateandshowhowtheConstructionEquipmentwouldbereportedintheBalanceSheetasat30June2013.

3marks

c. Markstated‘wecanchangemethodsofdepreciationnextyearifwewantto’.Usinganaccountingprincipleandaqualitativecharacteristic,explainwhetherthiswouldbeadvisable.

4marks

Question 3 (15 marks)CourtneyHaylesistheownerofHaylesHomeEntertainment,abusinessthatsellshomeentertainmentproducts.At1June2013thebusinesshadthefollowingdebtors.

$JSimon 880MAvis 2200 3080

July2012 3 ACCNTEXAMQB(SAMPLE)

TURN OVER

ExtractsoftheCashReceiptsJournalandSalesJournalforJune2013areprovidedbelow.

Cash Receipts Journal

Date 2013

Details Rec. No.

Bank Disc. Exp.

Debtors Control

Cost of Sales

Sales Sundries GST

1June Sales 234 1320 800 1200 120

3June JSimon 235 792 88 880

9June GSTClearing 236 3600 3600

14June Sales 237 1650 1 000 1500 150

16June SSlater 238 594 66 660

21June MAvis 239 1 000 1 000

28June Sales 240 1320 800 1200 120

Totals to date 10 276 154 2 540 2 600 3 900 3 600 390

Sales Journal

Date 2013

Debtor Invoice Number

Cost of Sales

Sales GST Debtors Control

4June SSlater 123 400 600 60 660

10June JSimon 124 600 900 90 990

19June SSlater 125 300 450 45 495

22June JSimon 126 200 300 30 330

Totals to date 1 500 2 250 225 2 475

Additional information• On30June,Courtneytransferred$10000fromherpersonalbankaccounttothebusinessbank

account(asnotedontheBankStatement).• On30June,thebusinesswasadvisedthattheamountoutstandingforDebtor–MAvis,shouldbe

writtenoff(Memo5).• On30June,JSimonreturnedthegoodshehadpurchasedon22June,becausetheywerefaulty

(CN538).

a. Recordtheadditionalinformationintheappropriatejournals.Totalthejournalswhereappropriate. Narrationsarenotrequired.

5marks

b. CompletetheDebtorsSubsidiaryLedgerforDebtor–JSimonasitwouldappearafteralljournalshavebeenpostedforJune2013.

Youarerequiredtobalancetheaccount.4marks

c. Manybusinessesusecontrolaccountsandsubsidiaryledgersintheiraccountingsystems. Discussthebenefitsandlimitationsofusingcontrolaccountsandsubsidiaryledgers.

6marks

ACCNTEXAMQB(SAMPLE) 4 July2012

Question 4 –continued

Question 4 (19 marks)ChrisLaurenceownsandoperatesChrisso’sFitnessWarehouse,asmallbusinesssellingavarietyoffitnessequipment.Featuresofthebusiness’saccountingsystemincludethefollowing.• Thebusinesssellstocustomersonbothacashandcreditbasis.Creditisofferedtoreliablecustomersat

credittermsof5/14,n/30.TheperpetualmethodofstockrecordingandtheFIFOcostassignmentmethodareused.

• Stockismarkedupatarateof50%.• Thebusinesspreparesfinancialreportsattheendofeachmonth.Chrishasrecordedalltransactionsintotherelevantjournals.Asummaryoftheseisprovided.

Cash Payments Journal (summary)

Date 2013

Details Chq. No.

Bank Disc. Rev.

Creditors Control

Stock Control

Wages Sundries GST

30June Totalstodate 34200 1300 27000 4 000 3000 1 000 500

Sales Journal (summary)

Date 2013

Debtor Invoice Number

Cost of Sales

Sales GST Debtors Control

30June Totalstodate 30000 45000 4500 49500

Purchases Journal (summary)

Date 2013

Creditor Invoice Number

Stock Control

GST Creditors Control

30June Totalstodate 29000 2900 31900

Cash Receipts Journal (summary)

Date 2013

Details Rec. No.

Bank Disc. Exp.

Debtors Control

Cost of Sales

Sales Sundries GST

30June Totalstodate 39300 700 18000 12000 20000 – 2000

Attheendofthereportingperiod,Chrisrealisedthatthefollowingdocumentshadnotbeenrecorded.

CFWInvoice CFW234 Date: 19 June 2013

Charge to: Rob’s Gym

Sale: 2 ZX7 Treadmills

Amount GST Invoice

$4200 $420 $4620

Terms: 5/14, n/30

CFWMemo 9

Date: 27 June 2013

Instruction: 1 ZX7 Treadmill, at a cost of $1500, was used at a recent fitness expo and will now be used solely for advertising purposes.

CFWReceipt 105

Date: 28 June 2013

Details: Received payment in full from Rob’s Gym for invoice CFW234.

July2012 5 ACCNTEXAMQB(SAMPLE)

TURN OVER

a. ExplainwhatismeantbytheFIFOcostassignmentmethod.2marks

b. Update andtotaltherelevantjournalswiththeinformationcontainedintheabovedocuments. Narrationsarenotrequired.

5marks

c. ExplainwhythestockreferredtoinMemo9shouldbetreatedasanexpense.2marks

FollowingaphysicalcountoftheModelZX7Treadmillsat30June2013,Chrispreparedthefollowingmemo.

CFW

Memo 10

Date: 30 June 2013

Details: A physical stocktake showed 1 ZX7 Treadmill on hand.

ChrisprovidedthefollowingStockCardfortheZX7Treadmill.

Stock Item: ZX7 Treadmill Supplier: TreadiesLocation: E4 Cost Assignment Method: FIFO

Date 2013

Details IN OUT BALANCE

Qty Cost Total Qty Cost Total Qty Cost Total

1June Balance 8 1300 10 400

8June Inv.CFW230 4 1300 5200 4 1300 5200

12June Rec.103 3 1300 3900 1 1300 1300

18June Inv.ZX42 4 1500 6000 14

13001500

13006000

d. CompletetheStockCardforZX7Treadmillswithallrelevanttransactionsuptoandincluding 30June2013.

3marks

e. PreparetheGeneralJournalentrytorecordthenecessaryadjustingentryforstockat30June2013. Anarrationisrequired.

3marks

f. Calculate theAdjustedGrossProfitonthesaleofZX7TreadmillsforthemonthofJune2013.4marks

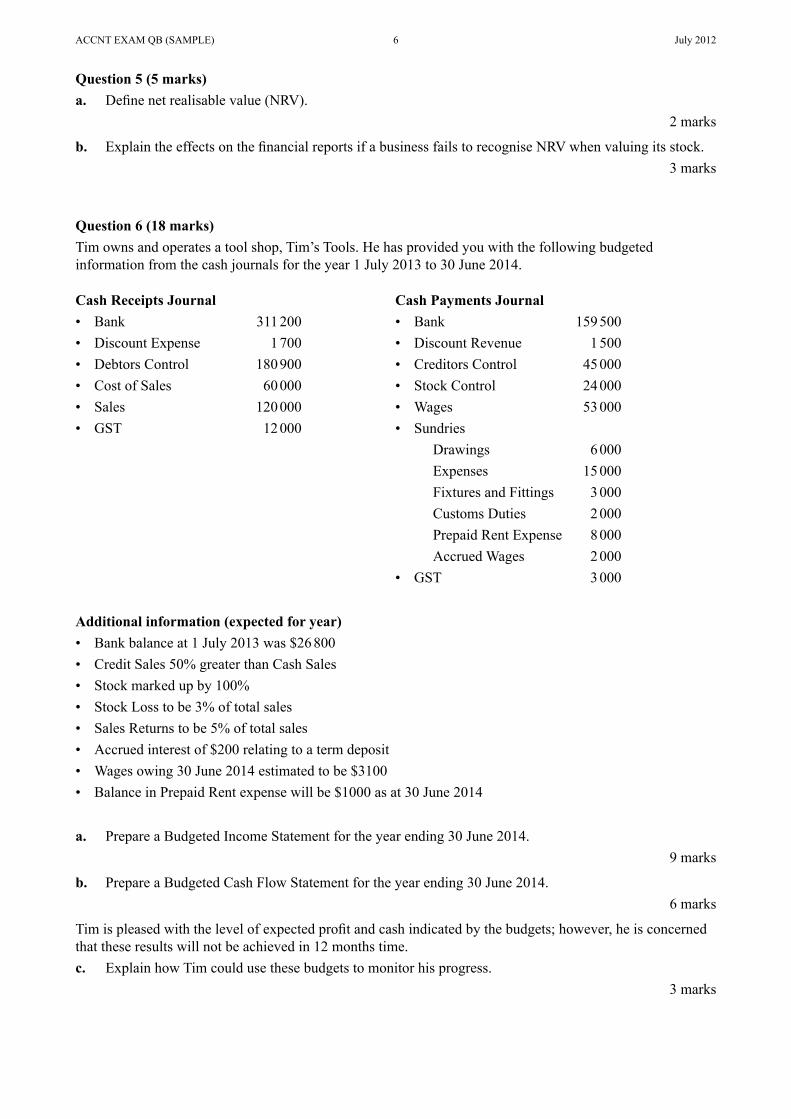

ACCNTEXAMQB(SAMPLE) 6 July2012

Question 5 (5 marks)a. Definenetrealisablevalue(NRV).

2marks

b. ExplaintheeffectsonthefinancialreportsifabusinessfailstorecogniseNRVwhenvaluingitsstock.3marks

Question 6 (18 marks)Timownsandoperatesatoolshop,Tim’sTools.Hehasprovidedyouwiththefollowingbudgetedinformationfromthecashjournalsfortheyear1July2013to30June2014.

Cash Receipts Journal• Bank 311200• DiscountExpense 1700• DebtorsControl 180900• CostofSales 60000• Sales 120000• GST 12000

Cash Payments Journal• Bank 159500• DiscountRevenue 1500• CreditorsControl 45000• StockControl 24000• Wages 53000• Sundries Drawings 6000 Expenses 15000 FixturesandFittings 3000 CustomsDuties 2000 PrepaidRentExpense 8000 AccruedWages 2000• GST 3000

Additional information (expected for year)• Bankbalanceat1July2013was$26800• CreditSales50%greaterthanCashSales• Stockmarkedupby100%• StockLosstobe3%oftotalsales• SalesReturnstobe5%oftotalsales• Accruedinterestof$200relatingtoatermdeposit• Wagesowing30June2014estimatedtobe$3100• BalanceinPrepaidRentexpensewillbe$1000asat30June2014

a. PrepareaBudgetedIncomeStatementfortheyearending30June2014.9marks

b. PrepareaBudgetedCashFlowStatementfortheyearending30June2014.6marks

Timispleasedwiththelevelofexpectedprofitandcashindicatedbythebudgets;however,heisconcernedthattheseresultswillnotbeachievedin12monthstime.c. ExplainhowTimcouldusethesebudgetstomonitorhisprogress.

3marks

July2012 7 ACCNTEXAMQB(SAMPLE)

TURN OVER

Question 7 (4 marks)Abusinessownerhasstated,‘IamnotsureIwanttomakeaprofitthisyear.LastyearImadealossbutmybankbalanceincreasedby$8900despitehavingnonewloansorcapitalcontributions’.Explain,givingtwoexamples,howthiscouldoccur.

Question 8 (8 marks)On1October2013,GenDomesticstradedinitsolddeliveryvanforanewdeliveryvanfromClubMotors.Theolddeliveryvanwaspurchasedatthebeginningof2007for$28000andhadacarryingvalueat 1October2013of$3500.Detailsofthepurchaseandtrade-inforthenewdeliveryvanaredocumentedintheinvoicebelow.

Club MotorsDate 1October2013Invoice no. 79Sold to GenDomesticsDESCRIPTION $

DeliveryVan 42000plusGST 4200 46200Lesstrade-in 2000

TOTAL PRICE 44200Terms: Net 30 days

a. ShowhowthefollowingaccountswillappearintheGeneralLedgerafterallentrieshavebeenposted.• DeliveryVan• AccumulatedDepreciation–DeliveryVan• DisposalofDeliveryVan

Youarenotrequiredtobalancetheaccounts.6marks

b. Explain,usingtheinformationfromGenDomestics,whytheprofitorlossondisposalofthevanoccurred.

2marks

ACCNTEXAMQB(SAMPLE) 8 July2012

Question 9 (6 marks)Abusinessownerisconcernedthatherbusiness’scashflowandliquidityaredeteriorating,soheraccountanthasprovidedsomeinformationregardingthebusiness’sshort-termfinancialposition.

Indicator 2010 2011 2012

WorkingCapitalRatio 2.15:1 2.25:1 2.79:1

QuickAssetRatio 1.42:1 1.05:1 0.79:1

CreditorsTurnover 17days 16days 15days

StockTurnover 58days 79days 98days

DebtorsTurnover 47days 44days 42days

Thebusiness’scredittermshavebeen2/14,n/30since2009.Suppliers’credittermsarealln/30.a. ExplainhowitispossiblethattheWorkingCapitalRatiotrendisfavourablewhiletheQuickAsset

Ratiotrendisunfavourable.2marks

b. Suggesttwotypesofinformation,otherthanfinancialindicators,thatcouldbeusefultothebusinessownerinanalysingtheperformanceofherbusiness.

2marks

c. Statetwostrategies,excludingadditionaladvertising,thatthebusinessownercouldimplementtoimprovetheStockTurnover(thatis,reduceStockTurnoverdays)withoutaffectingtheGrossProfitmargin.

2marks

July2012 9 ACCNTEXAMQB(SAMPLE)

TURN OVER

Question 10 (8 marks)BelindaBrowncommencedbusinesson1January2013underthenameofBubbleBaths.HeraccountantprovidedthefollowingPre-adjustmentTrialBalanceat30June2013.

Bubble Baths Pre-adjustment Trial Balance as at 30 June 2013

Account Debit Credit

Capital 26800

CashatBank 12360

CostofSales 76000

CreditorsControl 63000

DebtorsControl 34000

DiscountExpense 480

DiscountRevenue 800

Drawings 32800

FreightInward 1 000

GSTClearing 20

InterestExpense 2400

Loan 42000

PrepaidAdvertisingExpense 1800

PrepaidSalesRevenue 1 000

Sales 152000

ShopFittings 2000

StockControl 77500

Vehicle 46000

WagesExpense 24000

297 980 297 980

Theaccountantnotedthefollowing.• ThePrepaidAdvertisingExpenserelatestosixadvertisements(onepermonthforsixmonths)in‘Beautiful

Bathrooms’magazine,commencingJune2013.• Wagesincurredforthesix-monthperiodare$25000.• PrepaidSalesRevenuerepresentsadepositonacustom-madebath,whichwasdeliveredtothecustomer

on30June2013.

a. PrepareGeneralJournalentriestorecordtheseadjustmentsat30June2013. Narrationsarenotrequired.

6marks

b. ExplaintherelationshipbetweentheGoingConcernprincipleandtheneedforbalancedayadjustments.2marks

ACCNTEXAMQB(SAMPLE) 10 July2012

Question 11 (4 marks)BucklesandBeltshasprovidedthefollowinginformation,whichwasextractedfromtheCashFlowStatementVarianceReportforthemonthended31October2013.

Budgeted Actual Variance Fav/Unfav

CashSaleofVehicle 6000 7500 1500 F

ReceiptsfromDebtors 95000 90000 5000 U

Loan (9000) (8000) 1 000 F

Interest 300 375 75 U

a. Referringtotheextractabove,statewhethertheinterestisacashinfloworcashoutflow. Explainyouranswer.

2marks

b. ExplainhowBucklesandBeltscouldusetheinformationcontainedintheextractfromtheCashFlowStatementVarianceReport.

2marks

END OF QUESTION BOOK

Instructions

• Aquestionbookisprovidedwiththisanswerbook.• Answerallquestionsinthespacesprovidedinthisbook.• Writeyourstudent numberinthespaceprovidedaboveonthispage.• RefertoInstructionsonthefrontcoverofthequestionbook.

Students are NOT permitted to bring mobile phones and/or any other unauthorised electronic devices into the examination room.

©VICTORIANCURRICULUMANDASSESSMENTAUTHORITY2012

July2012

ACCOUNTINGWritten examination

Day Date Reading time: *.** ** to *.** ** (15 minutes) Writing time: *.** ** to *.** ** (2 hours)

ANSWER BOOK

SUPERVISOR TO ATTACH PROCESSING LABEL HERE

Figures

Words

STUDENT NUMBER Letter

Victorian Certificate of Education Year

ACCNTEXAMAB(SAMPLE) 2 July2012

This page is blank

July2012 3 ACCNTEXAMAB(SAMPLE)

Question 2–continuedTURN OVER

Question 1 (2 marks)

Definition

Question 2 (11 marks)a. 4marks

Construction Equipment Method of depreciation

Fixtures and Fittings Method of depreciation

Justification

b. 3marks

Calculation

Mark’s Mega Movers Balance Sheet (extract) as at 30 June 2013

Non-Current Assets $ $

ACCNTEXAMAB(SAMPLE) 4 July2012

Question 3–continued

c. 4marks

Explanation

Question 3 (15 marks)a. 5marksCash Receipts Journal

Date 2013

Details Rec. No.

Bank Disc. Exp.

Debtors Control

Cost of Sales

Sales Sundries GST

1June Sales 234 1320 800 1200 120

3June JSimon 235 792 88 880

9June GSTClearing 236 3600 3600

14June Sales 237 1650 1000 1500 150

16June SSlater 238 594 66 660

21June MAvis 239 1000 1000

28June Sales 240 1320 800 1200 120

Totals to date 10 276 154 2 540 2 600 3 900 3 600 390

July2012 5 ACCNTEXAMAB(SAMPLE)

Question 3–continuedTURN OVER

Sales Journal

Date 2013

Debtor Invoice Number

Cost of Sales

Sales GST Debtors Control

4June SSlater 123 400 600 60 660

10June JSimon 124 600 900 90 990

19June SSlater 125 300 450 45 495

22June JSimon 126 200 300 30 330

Totals to date 1 500 2 250 225 2 475

General Journal

Date 2013

Details General Ledger Subsidiary Ledger

Debit Credit Debit Credit

ACCNTEXAMAB(SAMPLE) 6 July2012

b. 4marksDebtor – J Simon

Date 2013

Cross-reference Amount Date 2013

Cross-reference Amount

c. 6marks

Discussion

July2012 7 ACCNTEXAMAB(SAMPLE)

Question 4–continuedTURN OVER

Question 4 (19 marks)a. 2marks

Explanation

b. 5marksCash Payments Journal (summary)

Date2013

Details Chq. No.

Bank Disc. Rev.

Creditors Control

Stock Control

Wages Sundries GST

30June Totalstodate 34200 1300 27000 4000 3000 1000 500

Sales Journal (summary)Date 2013

Debtor Invoice Number

Cost of Sales

Sales GST Debtors Control

30June Totalstodate 30000 45000 4500 49500

Purchases Journal (summary)Date 2013

Creditor Invoice Number

Stock Control

GST Creditors Control

30June Totalstodate 29000 2900 31900

ACCNTEXAMAB(SAMPLE) 8 July2012

Question 4–continued

Cash Receipts Journal (summary)Date 2013

Details Rec. No.

Bank Disc. Exp.

Debtors Control

Cost of Sales

Sales Sundries GST

30June Totalstodate 39300 700 18000 12000 20000 – 2000

General JournalDate2013

Details General Ledger Subsidiary LedgerDebit Credit Debit Credit

c. 2marks

Explanation

July2012 9 ACCNTEXAMAB(SAMPLE)

TURN OVER

d. 3marks

Stock Item: ZX7 Treadmill Supplier: TreadiesLocation: E4 Cost Assignment Method: FIFO

Date 2013

Details IN OUT BALANCE

Qty Cost Total Qty Cost Total Qty Cost Total

1June Balance 8 1300 10400

8June Inv.CFW230 4 1300 5200 4 1300 5200

12June Rec.103 3 1300 3900 1 1300 1300

18June Inv.ZX42 4 1500 6000 14

13001500

13006000

e. 3marksGeneral Journal

Date 2013

Details General Ledger Subsidiary Ledger

Debit Credit Debit Credit

f. 4marks

Calculation

Adjusted Gross Profit $

ACCNTEXAMAB(SAMPLE) 10 July2012

Question 5 (5 marks)a. 2marks

Definition

b. 3marks

Explanation

July2012 11 ACCNTEXAMAB(SAMPLE)

Question 6–continuedTURN OVER

Question 6 (18 marks)a. 9marks

Tim’s ToolsBudgeted Income Statement for the year ending 30 June 2014

$ $

ACCNTEXAMAB(SAMPLE) 12 July2012

b. 6marksTim’s Tools

Budgeted Cash Flow Statement for the year ending 30 June 2014

$ $

Question 6–continued

July2012 13 ACCNTEXAMAB(SAMPLE)

TURN OVER

c. 3marks

Explanation

Question 7 (4 marks)

Explanation

ACCNTEXAMAB(SAMPLE) 14 July2012

Question 8 (8 marks)a. 6marks

Delivery Van

Date 2013

Cross-reference Amount Date 2013

Cross-reference Amount

Accumulated Depreciation – Delivery Van

Date 2013

Cross-reference Amount Date 2013

Cross-reference Amount

Disposal of Delivery Van

Date 2013

Cross-reference Amount Date 2013

Cross-reference Amount

b. 2marks

Explanation

July2012 15 ACCNTEXAMAB(SAMPLE)

TURN OVER

Question 9 (6 marks)a. 2marks

Explanation

b. 2marks

Other information 1

Other information 2

c. 2marks

Strategy 1

Strategy 2

ACCNTEXAMAB(SAMPLE) 16 July2012

Question 10 (8 marks)a. 6marksGeneral Journal

Date 2013

Particulars General Ledger Subsidiary Ledger

Debit $

Credit $

Debit $

Credit $

b. 2marks

Explanation

July2012 17 ACCNTEXAMAB(SAMPLE)

Question 11 (4 marks)a. 2marks

Cash Inflow or Cash Outflow

Explanation

b. 2marks

Explanation

END OF ANSWER BOOK