variable pay and collective bargaining in british retail ... · variable pay and collective...

TRANSCRIPT

1

Variable pay and collective bargaining in British retail

banking

James Arrowsmith* and Paul Marginson** * Department of Management (Albany). Massey University, New Zealand ** Industrial Relations Research Unit, University of Warwick, UK Word count = 8,912 text (11,181 total) Corresponding author: Prof. Jim Arrowsmith Department of Management (Albany) Massey University Private Bag 102 904 North Shore Mail Centre Auckland, New Zealand

2

Variable pay and collective bargaining in British retail

banking

Abstract

The growth of variable pay schemes (VPS) appears to threaten collective approaches to

pay determination, which are based on standardization and centralization. This article

utilizes case study research to analyze the still little-known relationship between

collective bargaining and VPS. It focuses on the retail banking sector, where trade union

representation and collective bargaining remain relatively robust. The research identifies

an emergent process whereby the growth of bonus schemes has both supplanted

collective profit-share and permitted greater standardization of merit-pay awards. Unions

have therefore achieved some success in terms of limiting variation in base pay, at the

same time as the overall purchase of collective bargaining on employee earnings has

diminished. The factors contributing to this development are explained.

1. Introduction

A striking finding of the 2004 Workplace Employment Relations Survey (WERS) is the

growth of variable forms of pay. Half of all British private-sector workplaces with five or

more employees now have collective forms of variable pay (including share schemes,

profit-related pay and group-based payment schemes), covering 62% of employees; just

over a third have individual payments by results, extending to 43% of employees; and

3

16% use appraisal-based merit pay schemes which cover 26% of workers (Bryson and

Freeman, 2008: 3, 24). The 1998-2004 panel dataset recorded an increase from 20% to

32% in the use of such schemes in continuing workplaces (with ten or more employees),

‘suggesting that there has been a substantial increase in the use of performance-related

pay schemes since 1998’ (Kersley, et al, 2006: 191).

This growth has occurred in the context of a long-term decline in collective bargaining,

which now embraces only 14% of private-sector workplaces with ten or more employees

(Kersley et al, 2006: 182). It has also been suggested that even where collective

bargaining remains, much of it may be ritualistic and with limited impact on pay

outcomes (Forth and Millward, 2002). Seemingly, then, the growth of variable pay may

be related to the weakening of trade-unions and collective bargaining, and the assertion of

management control over pay systems, as implied in the literature. Pay flexibility and the

link to performance is usually a defining feature of human resource management (HRM)

models in which the role of trade unions is limited (Guest, 1987; Tyson, 2002). The same

applies to the so-called ‘new pay’ literature, where variable pay is seen as an important

part of an organization’s human resource strategy with little acknowledgement of any

trade union role (Lawler, 1995; Schuster and Zingheim, 1996).

Variable payments systems (VPS) are distinguished from traditional time-based or

service-related pay schemes in that they incorporate criteria linked to employee

performance. This can be at the level of the individual, work team, workplace, or

organization as a whole. Localized schemes tend to be concerned with employee

incentivization, whereas organization-wide arrangements have broader objectives to do

with recruitment, retention and employee ‘engagement’ or ‘reward’. There are three

4

broad types of VPS: incentive-based schemes and bonuses; merit pay; and organizational

arrangements such as profit- and equity-share schemes. The conceptual basis for

incentive pay arrangements is principal-agent theory. Agency models identify incentive

pay as an important means to ensure that employees focus on the achievement of

managerially-defined indicators (Prendergast, 1999). Incentive-based schemes are thus

designed to stimulate and focus greater effort and performance against targets; to have

significant effects they need to be tightly specified, and localized, to provide a clear line-

of-sight between employee inputs and pay outcomes (Lawler, 1981). The main forms of

incentive pay comprise piece-work and payments-by-results (PBR) schemes in which pay

is formulaically linked to output and/or productivity measures.

The problems of incentive payments schemes are long established. Though Marx

observed in volume one of Capital (1967: 556) that piecework ‘is the form of wages most

in harmony with the capitalist mode of production’ because it divided workers,

intensified work and made it easier to reduce pay, at the same time it was complex to

administer, gave workers a degree of control over production and provoked ‘constant

battles between capitalist and labour’. These problems become more acute as the

proportion of pay accounted for by VPS increases, since most workers are naturally more

risk-averse than those at the top of the organizational hierarchy (Burke and Hsieh, 2006).

Incentive pay can also foster a perversely narrow and short-term focus, and undermine

workforce cooperation (Bryson, et al, 2008).

Other forms of VPS are thus less directly concerned with incentives. Profit-related

schemes and employee share-ownership programmes (ESOPs), which entitle employees

to a share of an organization’s financial success, are commonly referred to as ‘financial

5

participation’ (Poutsma, 2006). Payments vary from year to year but they are less

immediately related to the performance of individual employees and work groups,

especially in larger organizations where they are more common (Kersley, et al, 2006:

191-2). The objectives of such schemes are often loosely specified in terms of promoting

organizational culture, employee retention and the ‘engagement’ of employees with

business objectives (Bryson and Freeman, 2007). They are forms of variable ‘reward’

designed to demonstrate organizational recognition of the contribution of employees to

past performance and to maintain their ongoing loyalty and motivation. They are most

effective when introduced alongside wider changes to work organization, especially

practices associated with ‘high performance working’ and employee involvement

(Sengupta, 2008).

Under ‘merit pay’ or ‘performance-related pay’ (PRP) schemes, a part of employee

earnings is decided by supervisory assessment. Merit pay schemes have traditionally been

used for managerial and white-collar occupations where simple ‘objective’ targets are too

crude to capture individuals’ contribution. Their use brings various problems, including

complexity of measurement criteria and management time involved (Kessler and Purcell,

1992). Larger organizations tend to formalize the assessment process through

performance management systems involving managerial appraisal against a range of

goals that may be input, output or behaviourally related. An overall rating can be used to

decide the level of merit pay. The payment can take the form of a bonus or be used to

determine the increase that will be applied to base pay, thereby substituting for across-

the-board settlements linked to seniority or the cost of living. Merit pay is variable in the

6

double sense that it differs from year to year, based on employee performance, and it

varies horizontally as workers receive different bonus or pay awards.

Variable pay represents a response to the ‘managerial dilemma’ of indeterminacy in the

employment relationship and the problem of employee motivation. Employment

contracts cannot specify what labour must be performed under all eventualities, and

workers retain a degree of control over the exercise of their labour power. By linking pay

to performance, employers introduce what Flanders (1974) termed a ‘managerial

function’ to pay, as part of the repertoire of inducements and sanctions designed to

motivate and control workers; it is distinguished from the ‘market function’ of pay, which

relates to recruitment and retention (though this may also be a consideration in the

application of VPS to high performers). To this end, modern payments systems

increasingly utilize a combination of VPS schemes to variously incentivize and reward

workers (Bryson, et al, 2008).

In contrast to employers, trade unions generally prefer standardized and centralized

approaches to pay (Metcalf, et al, 2001). This reflects an ideological egalitarianism, based

on principles of solidarity and non-discrimination, and practical considerations to do with

minimizing the transaction costs associated with multiple forms and levels of pay setting.

Unions therefore seek to define pay rates collectively, by job classifications and seniority,

and link pay reviews to standard benchmarks such as inflation and the ‘going rate’.

However, they are not necessarily averse to VPS where it comes on top of base pay and

offers a means to share in organizational success. This pragmatic accommodation also

reflects equity considerations, which inform employee attitudes. According to equity

theory, employees judge the fairness of a pay scheme in terms of how pay relates to their

7

own effort inputs and by comparing this to the inputs and outputs of other employees

(Adams, 1965). The implication is that employees may perceive VPS as potentially fairer

than standardized pay systems, providing they are procedurally robust and deliver an

acceptable level and distribution of returns.

If the implications of VPS for collective bargaining seem unfavourable in principle, they

are less clear-cut in practice. There is little evidence that employers followed purposeful

strategies of ‘union substitution’ through VPS (Wood and Bryson, 2008), although some

employers did de-recognize trade unions in such circumstances (Heery, 1997). More

generally, the decentralization and individualization of pay-setting weakens the

institutional role of trade unions because it fragments arrangements for pay determination

and enhances the scope for unilateral managerial decision making (Walsh, 1993). It can

also weaken the relationship between trade unions and their members since the growth of

pay outside the boundaries of traditional regulation by collective bargaining reduces the

scope of union influence over employee earnings (Heery, 2000). The use of merit-pay

awards as the means to implement the collectively-agreed base pay settlement also

introduces an element of individualization that obscures the contribution of collective

bargaining to employee pay (Kessler and Purcell, 1995). Furthermore, the application of

different forms of pay, or the implementation of pay at the level of the individual or small

groups, might fragment the interests of union members and make collective action harder

to achieve (Hyman, 1997).

Yet, union involvement in VPS potentially offers management the benefits of ‘voice’,

facilitating problem-solving by identifying employee concerns, and ‘legitimacy’ by

reassuring employees of the ‘fairness’ of the schemes (Bowey and Thorpe, 1986; Kessler,

8

2001). It can also help ensure schemes are well managed. As one study concluded,

‘employee involvement in pay system design and implementation is critical to ensuring

acceptance and effectiveness’ (Cox, 2000: 372). Much depends on the scheme under

consideration. Profit-related pay, for example, tends to be less problematic for unions as

it is not normally individualized or linked to incentivization (Pendleton, 1997). Both

profit-related pay and ESOPs tend to be more likely to be found in workplaces that

recognize trade unions, which is not the case for incentive systems such as PBR (Bryson,

et al, 2008: 19). Also crucial is the general state of industrial relations, with parties in

‘higher trust’ workplaces more likely to pursue a cooperative approach over VPS

(Dalton, 1998).

Empirically, Heery’s (2000) assessment that little is known about the actual relationship

between VPS and pay bargaining in unionized firms continues to hold true. The industrial

relations of variable pay has largely been examined in public sector settings (e.g.

Marsden, 2004a). The objective of the present study was therefore to explore, through

detailed and comparative case-study analysis, the forms and goals of VPS pursued by

employers, and trade union responses, in private-sector firms.i The principal research

questions concerned how far, in what ways and under what conditions VPS might

undermine or reconfigure collective bargaining; equally, how might VPS itself be

mediated by collective bargaining? The focus here is the non-managerial workforce in

retail banking, which is one of the leading sectors in usage of VPS and also has a higher-

than-average coverage of collective bargaining.

The rationale for the choice of sector is elaborated in the next section, followed by a

summary of the research design and methods. The results section is subdivided into three

9

parts to respectively examine company use of merit pay, performance bonuses and profit-

share, including reference to trade union views and the role of collective bargaining. This

is followed by a discussion of the industrial relations of VPS and the conclusion.

2 Context

Retail banking represents an insightful sector with which to research the relationship

between collective bargaining and VPS. At the onset of the research, banks and building

societies directly employed around 543,000 people in the UK, making it one of the

largest private sectors. It was also one of the most unionized, with trade union density at

30.5% and collective bargaining coverage extending to 38.1%, compared to 16.6% and

19.6% respectively for the private sector as a whole.ii Each form of VPS was also

extensively used. According to survey data from Industrial Relations Services (IRS), four

out of five banks used a merit approach to determine employee pay increases in 2004,

compared to 68% in 1997 (Dennis, 2004). Bonuses were also common. According to the

LFS (2004), 56% of employees in the sector were in receipt of individual bonuses; a

quarter group or team bonuses; 3% sales or commission-based bonus; and 16% another

form of bonus. The Annual Survey of Hours & Earnings (ASHE) states that overall,

bonuses accounted for 10.5% of employee earnings in 2004.

The significance of VPS reflects the transformation of banking services following

deregulation in the late 1980s (Storey, 1995). The 1986 Building Societies Act enabled

banks to diversify into mortgage lending and insurance services, and building societies to

offer unsecured loans, credit cards and current accounts. This contributed to an

intensification of competition and a series of mergers and acquisitions which accelerated

10

after most of the large building societies followed Abbey National’s de-mutualization in

1989. A subsequent rationalization of branch networks was also precipitated by the

introduction of new technologies such as automatic-teller machines, photo-scanning and

digitization which enabled the restructuring of back-office work into dedicated

administration centres. The growth of ‘remote’ banking via the telephone and internet

also led to increasing employment in call centres. Despite the high profitability of the

sector until recent years (the ‘big five’ banks collectively posted profits of £33 billion in

2006), cost-cutting measures became an increasing feature of efforts to improve cost-

income ratios given constraints on organic growth. The restructuring of employment in

the branches involved the redesign of jobs to emphasise customer service and the selling

of a widening portfolio of financial products. Pay systems changed to reflect this, shifting

from standardized and incremental arrangements designed to reward staff retention and

experience to schemes geared to incentivize individual and team performance.

This process of organizational change identifies banking as a prime case of the

purposeful application of HRM initiatives such as performance management and

employee flexibility (Flannery, et al, 1996; Storey et al, 1997). Yet, collective bargaining

remains extensive, and is used in each of the case study companies. The growth of VPS

in a unionized context is something largely unanticipated by the HRM and reward

literature (see e.g. Hendry et al, 2000), if not new to industrial relations research (see e.g.

Daniel and Millward, 1983). It poses two key questions. First, does collective bargaining

regulate VPS, or at least some of its forms? Second, and conversely, does VPS

undermine collective bargaining? To make such an assessment requires data on pay

11

schemes, and also a qualitaive perspective of management objectives and trade union

response.

3 Design and Methods

The comparative case study approach has been described as ‘crucial’ to understanding

developments in pay (Kessler, 1994: 123). This is because the process of comparing and

contrasting developments in organizations within a sector enables a more systematic

analysis of the contingencies that might generate similar or different outcomes. Such

‘contextualized comparison’ has a strong heritage in industrial relations research and

underpins the methodology of ‘critical realism’ (Edwards, 2006). This approach seeks to

combine the rigour of systematic enquiry with sensitivity to context and social processes.

The present study was not driven by hypotheses testing; nor was it solely concerned with

actors’ perceptions of the phenomena under consideration. The objective was to identify

the major themes and developments in variable pay, and the relationship to the

established institutions of industrial relations, in an exploratory but structured way.

The research was based on a common research instrument in order to maximize the

potential for comparative analysis. It commenced in 2005 with sector-level interviews

with the British Bankers’ Association and national trade union officials in order to

provide a broad context to trends and developments in payments systems. This data,

together with a review of the literature, informed the semi-structured interview schedules

produced for managerial and trade union respondents. These focused on industrial

relations arrangements and pay systems, with quantitative data also collected through a

questionnaire. The case-study fieldwork was undertaken from the end of 2005 until early

12

2007. Six organizations were studied, comprising three clearing banks of different size,

two building societies (also of different size) and one direct bank operation. Between

three and six interviews were conducted for each case, according to company size and

complexity of pay schemes, including HR managers, remuneration specialists, trade

union officials and lay representatives as appropriate. These interviews were transcribed

and followed up by telephone and email to clarify data. Six case study documents were

produced to a common template, which also drew on published and internal documents.

The companies are briefly described in table 1. Each of the case-study organizations

conducts centralized negotiations that determine pay arrangements across all branches. A

single union or staff association is recognized in four of the companies, and separate but

parallel bargaining rounds are conducted in the two multi-union cases.

- Table 1 about here -

4 Results

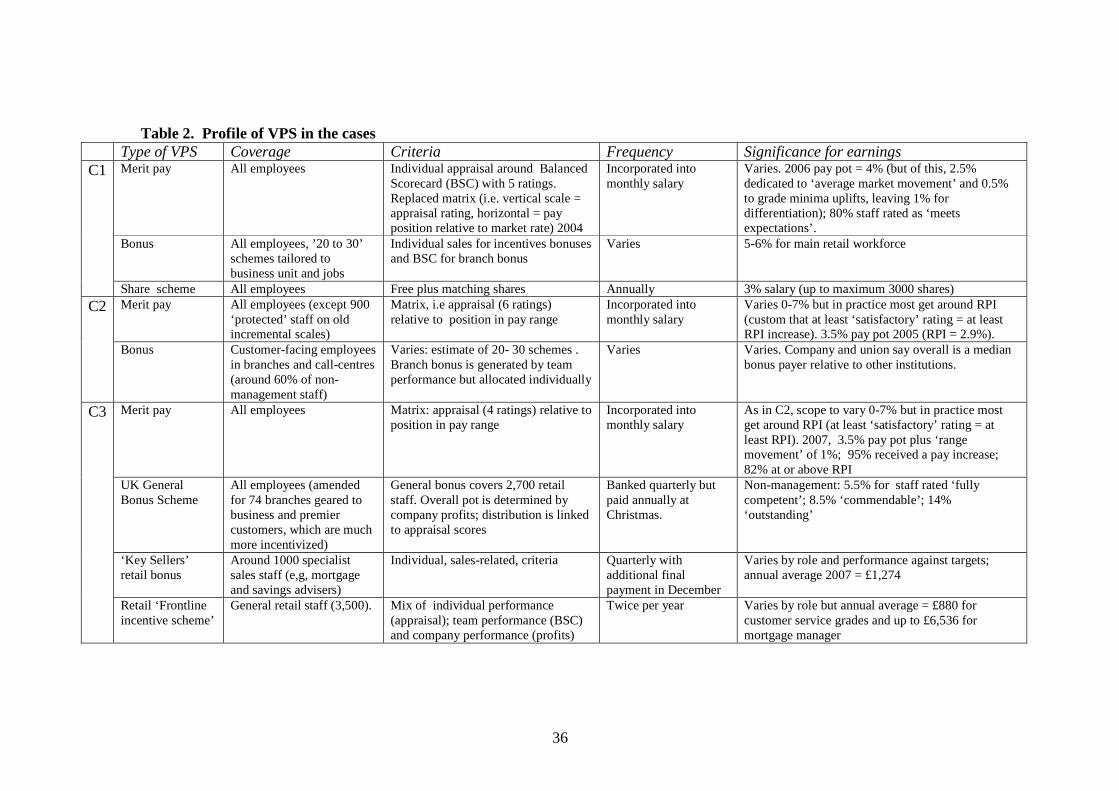

Of our six cases, all but the direct bank operate a merit pay scheme, in which the total

amount available for distribution (usually called the ‘pay pot’) conventionally follows an

‘inflation plus’ formula. Table 2 also shows that all six companies utilize various forms

of performance bonuses, which are more significant than merit pay in terms of earnings.

Financial participation is less common, though the large building society (BS1) bases its

corporate bonus on profits and the large commercial bank (C1) operates an employee

share ownership scheme. The form and rationales for each type of VPS are considered in

turn, with attention given to the main features of schemes, management rationales for

13

utilizing them, union responses and priorities and the extent of any consultation or

negotiation.

- Table 2 about here –

Merit pay

A merit pay approach was used to implement the basic pay award in all but one of the

cases. The direct bank (DB) chose to standardize base pay increases, though with some

scope for progression in base pay through individuals’ skills attainment. DB’s rationale

was that performance was rewarded through the bonus system, which utilized employee

appraisal scores to moderate the payments involved (see later). Elsewhere, annual pay

increases are determined under merit schemes, based on managerial appraisal, although

these take various forms and have been subject to change. In C1, for example, the

original scheme was designed to fully decentralize pay-setting to local managers in order

to better tailor pay to local circumstances and to ‘push accountability down the line’

(senior HR manager). Managers were provided with their own ‘pay pots’ and encouraged

to make their own assessment of how to distribute them. However, managers felt this

involved more work for them, and could be corrosive of teamwork, so they tended to

spread pay awards evenly. Others saw the decentralization of pay-setting as an

opportunity to reduce overall costs, mainly by recruiting at the lowest point on the scales,

which led to pay inequities and recruitment and retention difficulties. As a result, the

scope for managerial discretion was reformed by the introduction of three sets of pay

scales in 2004 for new employees and staff judged as either capable or high performers.

14

In contrast, the other four firms proceeded more cautiously by introducing centralized

matrix systems in which the allocation of the pay award is determined both by position in

the pay scale and performance as assessed by management appraisal. Basically, higher

performers who are lower paid would receive higher proportionate increases than those

perfoming similarly who had progressed further up the scales.

The growth of merit pay in retail banking began in the early 1990s following the

termination of multi-employer collective bargaining. Under the sector agreements,

incremental pay schemes had provided service-related increases in addition to the general

pay increase until individuals reached the top of their scale. Our interviewees included

long-serving, senior employer and trade union officials who had been involved in

negotiations to replace incremental progression. According to employer respondents, the

demise of incremental pay reflected increased competition and changing job requirements

which brought a renewed emphasis on performance. At first, even with pay determination

at company level, the large banks continued to maintain incremental pay scales ‘which

weren’t a million miles away from the other clearing banks’ (senior manager,

Compensation, C1). However, across-the-board increments increasingly came to be seen

as incongruous. It was argued that it was unjust that people should be paid more simply

for having been in the job longer. Indeed, some managers said that their company used

equal pay arguments in favour of merit pay, as male workers disproportionately benefited

from seniority pay scales because of uninterrupted service. More significant was that

employment stability resulted in employers retaining high numbers of long-service staff

who were seen as less likely to have the newly-desired sales skills yet because of

incremental scales were felt to be paid over ‘market rate’.

15

Union representatives argued that employers were also concerned to introduce merit pay

for ideological and cost reasons. The discourse of merit pay was concerned with

‘reshaping employee attitudes’ towards task flexibility and promoting a sales culture, and

to ‘substitute the language of the market for the collectivist cost of living’ (TU1 general

secretary, C1). In the larger banks, which tended to pay above-average rates, the use of

market rates enabled them to gradually move ‘from a system that paid at the upper

quartile to the median of the market’. For their part, all the banks denied that cost-cutting

was a rationale for the shift to merit pay, though they acknowledged that it could be an

effect of ‘moving from generally speaking an industry that paid highly, high base pay, to

pay levels that reflect the more general employment market’ (Compensation and Benefits

Manager, C1). With pay scales based on market rates, progression beyond the median

became a product of individual performance. At the same time, however, bonuses had

grown; employers argued that pay expenditure had not been reduced but redirected over

time (‘to introduce high levels of bonus you can only do it by taking away basic salary,

and that’s a slow progress’, Compensation and Benefits Manager, C1). Finally,

benchmarking may also have played a part (‘There’s often an element of ‘we have to do

it that way because that’s how everyone else does it’’ , National union official, BS2).

Union agreement to the introduction of merit pay was explained by officials in both

positive and negative terms. For example, the TU2 official in C2 said that their members

gave up incremental progression in favour of a performance pay matrix in 1995 following

merger with a building society. The rationale was that the new scheme’s broader job

grades and pay scales would enable better progression for lower-paid staff, particularly

good performers, whilst the consolidation of the value of the increments with the cost-of-

16

living rise would ensure acceptable increases for those at the higher end of the scales.

Also relevant was a context of redundancies, which were managed by ‘voluntary’

meansiii :

‘How it was partly put to us was that ‘if you don’t accept this who knows what

the future will be?’ So people say there was a gun to our head when we accepted

it’.

In the event, union representatives said that the value of the increments effectively

disappeared over time and no replacement funds were made available to fund the matrix.

The pay pot was instead linked to inflation, which was stable at low rates.

Union concerns about VPS are often at their highest for merit pay as this affects base

rather than ‘on top’ pay. Merit pay was widely seen by union respondents as potentially

divisive and exposing employees to uncertainty. There were practical reservations too

over the mechanism for setting and assessing performance goals, and the scope for

subjectivity (and thereby favouritism and discrimination) in managerial appraisal. All of

which is contrary to the instinctive union view of fairness as ‘everyone treated equally’

(branch official, DB). However, the banks’ pay data indicated that actual differentiation

within the schemes was minimal in practice, save for the relatively few employees judged

as exceptional or less than competent. Partly, this reflects the well-documented

difficulties of appraisal schemes to do with lukewarm managerial enthusiasm and

problems in measuring performance (Kessler and Purcell, 1992). Central tendency in

managerial ratings combined with pay pots kept low by the link to inflation left little

practical scope for differentiation. For example, C2 agreed a pay pot in 2005 of 3.5%, to

be implemented individually in a range from zero (ratings five and six) to 7% (rating

17

one). However, nearly 90% of employees were rated between 2 and the ‘satisfactory’

rating of 4; for these employees, pay varied only from 3.1% for lower rated workers who

were high in the pay scale, to 3.9% for higher performers on lower rates. Overall pay

dispersion is, as a result, very low.

This relative standardization of merit pay served to address trade union concerns over

basic-pay differentiation, which translated into two main priorities. First, to ensure

transparency and consistency in the appraisal process by regulating, and essentially

limiting, the scope of managerial discretion. As the TU2 National Official for C1 put it,

the key concern is:

‘ to place more regulations around how individual pay is determined. That’s the

greatest philosophical divide between us and management. Ideally the company

would like the branch manager to decide pay. Our job, because the members want

this, is to reduce the discretion of local managers. Insofar as there are battle lines

this is one – clawing back control’.

Second, in terms of outcomes, ‘the guiding principle is that nobody gets less than

inflation’ (TU3 General Secretary, C2). More realistically, the goal is that those staff

rated as satisfactory should receive an inflation-matching increase, whatever their

position in the pay scale. Union concerns over the use of matrix formulae became more

pronounced from the turn of the decade as increasing numbers of higher-paid staff

received pay increases less than inflation, including those rated as good performers,

because they were assessed as over ‘market rate’. This provoked an industrial dispute at

C1 in 2005, resolved by adopting the practice (used elsewhere) of additional non-

consolidated payments to such staff. In contrast, in C2, C3 and BS2, it became customary

18

that anyone rated as satisfactory or above would receive a minimum increase of RPI and

this continued to hold despite rising levels of inflation. As one senior manager explained,

‘From a union side it always gets down to what percentage of the overall

population are going to get at least RPI .... And the clinching factor usually in the

union discussions is how high we can make that. If you are not into the seventy

per cents we are not going to get a deal... certainly up to 75% or so and then we

know we are talking and we can perhaps be reaching an agreement. But that’s –

it’s a big point for them’ (Head of HR/ IR, C3).

In practice, therefore, there is full information and consultation around the apparatus of

merit pay (appraisal scheme, matrix formula, market pay data, progression schemes etc)

in all five companies. There is also some form of collective bargaining over the allocation

as well as the generation of the pay pot in all except C1. Indeed, there is more scope for

negotiation concerning allocation within the matrix than for the overall size of the pay

pot. In each of the company cases a de facto RPI-plus mechanism operates to set the pay

pot, usually a percentage point above inflation depending on business results, which is

determined by the business and finance functions. Hence, the largest union in C1

complained that the overall pay framework is ‘top heavy and driven by the chief

executive’, with the pay pot ‘delivered like Moses and the tablets of stone’. This was

echoed by the union in BS2, where budgeting for the pay pot was said to be ‘done behind

closed doors’ and the union was pressing for greater involvement in order to help ‘set the

priorities and focus of employee spend’. With the generation of the pay pot to a large

degree beyond the control of HR or IR managers, the focus of actual negotiations centred

on the distribution of pay within the matrix arrangements.

19

As democratic organizations, unions are routinely mandated to pursue standardized pay

settlements. The question is begged, however, why employers continue to maintain merit-

pay systems that hardly discriminate between staff. Employers have essentially

abandoned any pretence that merit increases have any incentive affect because of the

relatively small scale and consolidated nature of the payments:

‘ I don’t think it acts as an incentive for people to actually work any harder than

they would have done normally. I think if anything, when the people who worked

very hard and got good ratings get their (small) pay award, it actually acts as a

disincentive’. (Employee Relations Manager, C2)

‘We wouldn’t call the merit pay ‘variable pay’ - bonuses are variable pay as that

is money at risk’. (Compensation and Benefits Manager, C1)

Yet none of the companies abandoned their merit pay schemes. This is partly due to an

awareness that circumstances could change. Some managers suggested that rising

inflation might effect paybill redistribution by releasing larger sums for the purposes of

differentiation, though unions would continue to press for cost-of-living increases for

most staff. There was also an incentive effect for the relatively small number of high-

achieving and under-performing employees, which might also serve a wider symbolic

purpose. More generally, it was argued that merit pay helped underpin the process of

performance management, i.e. getting employees to focus on desired objectives and

encouraging managers to better communicate and coach their staff. It is felt that appraisal

is taken more seriously by both managers and staff if there is some implication for pay,

however small, of the rating:

20

‘The difficulty that we have culturally is that we need managers to take ownership

for their people and their people decisions. So that is one of the drivers for us to

[retain merit pay]” (Head of Reward, C3).

Bonuses were seen as the more effective incentivization tools, and there was even some

sympathy for union arguments against differentiation in basic pay:

“where everybody is doing the same kind of job you really should all be given a

similar amount of money..., you get the right level of pay for doing the job that

you do, whereas the bonus should recognize [superior] individual performance”.

(Head of Reward, C3)

In practice, the growing panoply of bonus schemes meant that there was less reliance on

merit pay as a means of incentive or reward.

Performance bonuses

All the companies use bonuses to a significant degree, often in multiple forms as Table 2

shows, and these are generally significant for employee earnings. The most common

form is a team-based scheme where the overall ‘pot’ is linked to branch performance,

with some scope for individual variation by using appraisal scores. The building society

schemes tend to use more aggregate performance criteria than the commercial banks. In

addition, specialist sales staff such as mortgage, savings or pensions advisers usually

receive individual sales commission. These bonuses are intended to incentivize

employees ‘to leverage performance beyond target, beyond what you would reasonably

expect’’ (Senior Rewards Manager, BS1). The retention of high-performing employees

21

was also cited as a rationale for bonuses. In DB, higher performance bonuses were

introduced for experienced staff due to tightening labour markets. However managers

reported tension between the retention objective and the performance objective, as targets

became more ‘stretching’.

Bonuses are more variable than merit pay as they are linked to specific criteria that can be

readily adjusted and controlled. These are partly formulaic, linked to product sales or

service targets, but appraisal scores may also feature as part of a broader ‘balanced

scorecard’ approach.iv Bonuses are also attractive to firms on cost grounds; unlike merit-

pay awards, they do not add to fixed costs as they are not consolidated into salaries, and

they may be to some extent self-generated when linked to targets such as sales growth.

Indeed, the idea that bonuses may pay for themselves was referred to by union officials as

a reason why they do not necessarily see them as a threat to basic pay.

Business managers are normally responsible for the design of bonus schemes as they are

closely linked to sales and service priorities. Line-management ownership was reported

as presenting problems for HR and the unions:

‘(A bonus) tends to pitch up in HR for approval the day before it’s going to be sort

of launched. So it comes to us, we send it straight on to the union who complain

they haven’t had time to look at it and review it… We don’t have very much central

debate or negotiation around bonus schemes if at all [and union involvement is] a

source of contention on a regular basis’ (Employee Relations Manager, C2)

However a number of managers said that the HR function has become more closely

involved, partly due to problems of coherence and manageability, but also because of a

22

changed regulatory environment which means that schemes have to be more multi-

faceted than in the past.v

Bonus arrangements in the six companies were almost universally outside the scope of

collective bargaining. This is partly for historical reasons. Most bonuses traditionally paid

only small sums and negotiations with the unions focused on basic pay claims. The union

full-time official in C2 explained that when the main bonus scheme was first introduced

in 1995, the union as well as management was keen to keep it separate from collective

bargaining, partly because of a suspicion it could be used to manipulate bargaining over

base pay:

‘[We said] we are not prepared to talk to you about the bonus, we negotiate an

annual cost-of-living rise, so however generous you say you’ve been on that, it’s

irrelevant.’

When bonuses began to increase managers were keen to maintain control as they were

seen as vital to the new performance culture of the banks:

‘ [they are] business tools [to] turn on or off the tap of business into a particular

product or area…our position on bonus schemes is very much that they are

discretionary benefits that are subject to change or are subject to being withdrawn’

(Employee Relations Manager, C2).

This was echoed by the Head of Rewards in BS1, who said ‘You would never ever give

away the negotiating rights on a discretionary item’. Unions may be consulted about the

framework of the major schemes but, as C3’s Head of HR/ IR put it,

23

‘We debate the issue but it’s done as a consult rather than a negotiation. And

certainly when we come to the quantum of the bonus, that is ‘announced’.’

Thus, at the same time as pay dispersion in merit pay schemes became flatter, bonus

payments grew rapidly to support changes to the product mix and underscore new job

requirements. This strategy was succinctly expressed by the Head of Rewards at C3:

‘ the balance that we are trying to get to as an organization, like a lot of

others, is that fixed becomes fixed, and tightly controlled, and variable starts

to increase’.

The growth of bonuses means that an increasingly significant proportion of employee

earnings are determined without direct union involvement. Furthermore, where bonus

payments are high, they can now constrain what collective bargaining can deliver on

around basic pay. For example, after the 2006 pay settlement at BS2, the union’s

communication to members stated that:

‘The society is aware that the union has accepted the revised [base pay] offer

reluctantly, fully aware of the lack of room to deliver anything better because of

already decided bonus arrangements.’

The Head of HR/ IR at C3 confirmed that pay expectations were framed by the main

bonus payment that immediately followed announcement of business results:

‘when we are negotiating, yeah, it informs dialogue … [the Rewards] team can be

working with management about what the bonuses will mean and it often comes

out during the salary negotiations what the bonuses are… if they are quite high

they [employees] will say that’s marvelous - so you don’t get so big a salary

24

settlement. And if it comes in low or they feel it’s low they [the union] will say you

will have to give more towards the salary settlement (or) do something else on the

[union] agenda because the bonuses are crap.’

Responding to the growth in bonuses is therefore problematic for trade unions. They want

members to be able to achieve higher incomes, but they are also aware that bonuses

introduce risk and uncertainty into employee earnings. Being both variable and target-

driven, bonuses can also contribute to work intensification and stress. Yet even though

their significance has increased, there is no union demand for bonuses to be subject to

collective bargaining. Unions are wary to be seen as too closely involved in schemes

designed to ‘stretch’ employees and vary earnings across the workforce and over time. As

the BS1 union general secretary put it,

‘ if it is good the company will claim the benefit anyway but if it is bad the

members would say why did you agree to this?! It’s a no-win for the union’.

Instead, unions emphasise their involvement in terms of monitoring, ‘to make sure that

the bonus schemes are fair and that targets are achievable’ (General Secretary, TU3, C2).

However this is difficult since schemes can be highly localized and subject to rapid

change, particularly in the larger organizations (‘it is difficult to keep track of them… I’d

not be surprised if there are other bonuses that we don’t know about’; National Official,

C1). A large part of their role is thus essentially reactive, raising and supporting

employee grievances. In 2005, for example, TU1 raised a collective grievance about new

bonus targets in C2’s call centre. The company responded quickly by agreeing to revisit

the whole performance management structure. The appraisal process was suspended

25

while union concerns were investigated, and many individual scores were upwardly

revised.

This potential for conflict means that in practice unions are consulted about the design of

the major bonus schemes. Managers in C1 agreed that a degree of informal bargaining

regularly occurs over the design and review of some schemes as part of a ‘problem

solving’ or, as a DB manager had it, ‘audience positioning’ process. There are also

isolated instances of formal negotiations where incentive pay contributes a particularly

high proportion of employee earnings (e.g. for 5000 sales staff in C1) or where changes

to longstanding schemes were thought easier to manage by collective rather than

individual agreement (BS1). Overall, though, there was little appetite for more formal

arrangements from either parties.

Profit-related schemes and ESOPs

Profitability was high at all six companies at the time of the research (table 1). Yet

conventional profit-share arrangements were not commonly used. In two cases, C1

and C2, profit-share schemes were abandoned following the government’s phasing-

out of tax benefits and replaced with employee share ownership arrangements.vi This

remains a significant form of reward in C1, with employees receiving 3% of basic

salary by way of free shares up to a set maximum in 2005. In C2, shares were also

allocated according to the performance of the business, averaging around 5% of

salary, but in 2003 the free share award was capped at around £650 as an offset

against mounting pension costs. The unions agreed to this to protect the final salary

scheme, but in 2004 the company said it would halve the value of the offering in

26

order to provide a further pension injection, then announced the termination of the

share scheme in 2005. The unions said that this decision was made unilaterally but as

it was a non-contractual benefit they had little real say (other than to unsuccessfully

demand a group-wide profit-related bonus in the 2006 pay claim in response).

The two other banks in a position to offer employee share schemes (building societies

cannot because they are mutually owned) have somewhat different arrangements. DB

is unusual in that the scheme is not open to all employees (a normal requirement to

attract tax breaks); rather, eligibility depends on length of service and employee

performance. The scheme therefore acts as a retention and motivation tool. Around

15% of employees are in the scheme and may receive shares worth between 10-30%

of salary. In C3 the parent company’s share-save scheme was introduced in 2000.

This was greeted with enthusiasm by the union because it was seen as resembling a

profit-share initiative. However, subsidiary-level management demonstrated little

interest in the scheme, and payouts were low (with none in 2004). Managers concede

that this left ‘a very bad taste in the mouth’ of employees. However, the Head of

Rewards said that financial participation schemes did not fit the C3’s philosophy of

‘meritocracy’:

‘ It’s meritocracy so the variable pay piece is about what you deliver as opposed

to what the organization as a whole delivers ... obviously the profit share is ‘you

get it regardless of how you perform’’.

The union national officer confirmed that

‘They are really focusing on the [individual] bonuses… in creating this great

meritocracy that they are talking about’

27

The two building societies also have no conventional form of profit-share but they do

have corporate bonuses linked to company financial performance. The available pot for

the bonus in BS2 is determined by company profits and distributed according to team and

individual performance. Most employees receive double-digit payments, as a percentage

of salary, in the course of the year. In BS1, the bonus is paid as a lump sum each June. It

was partly introduced to offer something resembling the ESOP benefits available to

employees of banks and the de-mutualizing building societies; or, ‘because in the

marketplace other people do it’ (Senior Rewards Manager). BS1 also sees the bonus as

useful to help managers and staff understand its key business priorities. It is based on four

performance measures at the company level: cost; profit; market share of savings and

mortgage; and non-mortgage and savings income. All but those staff rated as poor

performers (400 of around 16,000) receive it as a standard percentage of salary (12.8% in

2005). Otherwise there is no link to individual performance, as current thinking is that

introducing this would undermine the performance management system by over-focusing

on appraisal ratings.

Overall, BS1 is the only organization with a scheme providing a standardized payment

linked to company profit or performance, whilst the other large employer, C1, is the only

one with a standardized, workforce-wide share-save scheme. Other companies (C3, DB,

BS2) use a link to company profits as the basis for generating the overall spend for

bonuses but these are implemented according to individual or branch performance. The

notion of profit-share as a collective return to labour, which found some resonance with

unions, is secondary to other, more incentive-oriented, forms of VPS.

28

5 The industrial relations contingencies of VPS in banking

The growth of VPS has occurred in a context of transformation in banking service

provision and bank reorganization. Yet industrial disputes have been rare. This is in large

part because the banks could afford a managed approach to change to avoid damaging

their brand through labour disputes.vii Though there are differences in industrial relations

between the companies, which we briefly explore below, all but one of the six companies

has avoided major pay disputes in recent years.

The exception is C1 which has two competing unions, with the largest marketing itself on

the basis of its independence or, as management would have it, adverserialism.

According to a senior HR manager,

‘pay is used as a propaganda tool as a potential recruiting device… so we haven’t

had the ownership and advocacy role played by the unions which might be found

elsewhere’.

As indicated above, the dispute was caused by the company’s initial refusal to grant a pay

rise in 2005 to up to 10,000 staff above ‘market rate’. TU1 balloted for industrial action

short of a strike, and TU2 balloted members on whether they want to reject the

company’s pay offer. Industrial action was avoided by the provision of an additional

consolidated award to affected staff who were high performers. TU2 accepted this; the

larger TU1 did not reach agreement but took no further action following a participation

rate of only 22% in its ballot. This apparent lack of agitation might be indicative of

interest differences in the membership. Most employees were unaffected by the ‘zero pay

award’ and those that were already received higher basic pay. Differences of interest

29

were also evident in C2, where half the membership of TU1 has ‘protected’ terms and

conditions, i.e. retain the incremental system, as they were in employment at the time of

acquisition in 1990. The other half receives merit pay. The union said it is difficult for

them to serve and represent both groups at the same time as they have different concerns

about performance management and pay.

Considerations of technology, ownership and key personalities help account for

differences in industrial relations and payments systems elsewhere. Concerning

technology, the direct bank has eschewed merit pay in favour of incentive bonus

arrangements partly because its form of work organization lends itself to target-setting

and technical forms of monitoring and control (Edwards, 1979). This more readily

accommodates bonus schemes as well as undermining the ‘performance management’

case for merit pay. The significance of ownership is clearly seen in the case of the two

building societies. These operate in competitive markets but senior management does not

have the same short-term pressures for results associated with ownership by external

shareholders. Furthermore, the societies advertise their mutual status as offering a more

‘caring’ ethos both in terms of customer service and internally to staff. Neither company

had implemented any redundancy programmes, and BS1 used employee satisfaction data

and its good industrial relations record as part of a campaign to secure the Sunday Times

‘best employer to work for’ award. Pay settlements in this company had been above

average for seven successive years, and voluntary staff turnover was some 6 percentage

points lower than the sector average. The senior rewards manager summarized the

approach thus,

30

‘We don’t sit there [in negotiations] and say ‘this is it, take it or leave it otherwise

we shut 50 branches’… [and] we probably over-reward under performers and

under-reward high performers. However, the upside of that is very satisfied

people, a very stable workforce and historically a very good business

performance…The difference is being mutual which is a hell of a thing. That

means we are driven by a value set, for our customers and our staff’.

At BS2, the full-time union official described the society’s overall approach as

‘paternalism’, and said that the company had continued to fully involve the union even

when membership dropped to a low level under his predecessor. The HR Director said

that:

‘We have a very good relationship with the trade union and try and work with

them in everything we do. We do take the relationship very seriously and they

sense that…We want people to see us as a fair organization and an organization

they can trust, which is part our whole ethos as a building society... Trade union

concerns are taken on board – if the union thinks it’s not fair there is a chance

that the staff will, or soon will, so it is important to be transparent.’

The relevance of ownership also comes through at C3, which has an overseas parent.

Rationalization was a significant contextual factor in the UK operation, including the

threat of disposal, which happened with the company’s Irish operations in 2005. The

union feels that being part of a foreign-owned international group intensifies the effect of

‘shareholder pressure’ as the bank has to continually demonstrate its relevance to the

portfolio of the wider group. It particularly feared the sale of the bank, which was

actively considered by the parent company in order to relieve financial problems caused

31

by a trading scandal that led to the departure of the group chief executive in early 2004.

His replacement, however, was appointed from C3 and was committed to maintaining it

within the group, based on the strategy of restructuring. Here, the sometimes significant

importance to industrial relations of personalities and personal relations is revealed. Both

the new group chief executive and his replacement as chief executive of C3 have

building-society backgrounds. The former had at one time been a branch official of the

staff association; as an executive of one of the ‘big five’ banks he later developed a

‘partnership agreement’ with its union. On moving abroad to the parent company of C3,

he refused overtures by its government to support what were seen as anti-union labour

law reforms and instead signed national and global agreements with the company’s

unions. Thus industrial relations have actually improved in C3 over the last few years

even during the rationalization process:

‘They are used to working in partnership with the union… it’s actually very good

for us because the old managers were always quite anti-union” (National Officer).

Thus, industrial relations in the six banks have been generally constructive, though with

differences according to ownership, business models and management style, multi-

unionism and differing interests amongst members. Management was generally able and

willing to meet most union concerns over base pay, partly because they could afford to,

and also because they wish to avoid disputes. (The case of C1 also suggests that union

capacity to mobilize the membership is not unproblematic.) Consistent with this,

management strategy over pay has been ‘adaptive’ or ‘emergent’ (Mintzberg and Waters,

1985). The growth of bonus schemes meant that employers’ initial goals over merit pay

32

increasingly were addressed through other forms of VPS, which permitted them greater

space to address trade union concerns over variation in base pay.

6 Conclusions

The relationship between joint regulation and new forms of variable pay in banking is a

complex story of hybridization. Unions have managed to reframe negotiations around the

modalities of merit pay. Originally, employers had intended that pay negotiations be

confined to the size of the overall ‘pay pot’, granting local managers greater discretion

over implementation based on individualized performance criteria. Merit pay thus

presented particular challenges to trade unions as it subverted the collectivist notions

underpinning pay bargaining. Unions increasingly extended their influence to regulate the

actual distribution of pay so that it became more standardized as a result, yet this was

achieved at limited cost to management. First, it became apparent that the scope for

individual pay dispersion in merit pay schemes was limited in practice due to a

combination of small pay pots, which continued to be defined by inflation rather than by

‘ability to pay’, and by well-known practical problems such as central tendency in

managerial appraisal. Second, meeting union demands over an inflation-based floor for

all but ‘poor performers’ also made sense where management wanted to avoid

demotivating staff in a context of tight labour markets and work intensification. Third,

bonuses became the principal means to motivate and control staff through pay. By

utilizing a combination of team and individual performance measures, they also became

increasingly sophisticated. Merit pay schemes have not been abandoned, partly because

there is still a direct incentive effect for exceptionally strong or poor performers, and

33

partly for symbolic reasons, in stressing to employees and line managers the importance

of the wider performance management systems of which it is a part. A link to pay, even if

small, helps to underscore line management responsibilities for employee appraisal,

communication, goal-setting, and coaching (Lawler, 1981; Armstrong and Baron, 2005).

From a managerial point of view, bonus payments are now strongly embedded as

performance tools under unilateral control. Bonus payments also helped contain fixed

wage growth at a time when profits were high. Yet from a trade union perspective, there

is little real appetite for joint regulation of bonus schemes. Not only is it practically

difficult to maintain involvement in bonuses where they are highly localized and prone to

change; it also exposes them to the risk of negative association. Unions continue to

closely monitor the procedural equity of the schemes and raise employee concerns and

grievances (which itself can serve a useful function for management). In substantive

terms their main focus continues to concern basic, pensionable pay and its relation to the

‘cost of living’. Here they have been relatively successful, maintaining modest real wage

growth for the majority of members, most of whom also benefit from significant bonus

payments. This has happened at a time when unions have been defensive in the face of

restructuring pressures, even if job reductions have been managed on a ‘voluntary’ basis.

Both sides, then, are not unhappy with the emergence of a situation whereby collective

bargaining has developed a tighter regulation of merit pay, but where it also retains a

weak capacity to regulate bonuses.

The findings demonstrate that even in a sector which has undergone radical restructuring,

the assertion of management prerogative can proceed without abandoning collective

regulation (Brown, et al, 2000; Deery and Mitchell, 1999). Instead, collective regulation

34

has been reconfigured, and the boundary between the collectively-bargained and

unilaterally-determined elements of earnings redrawn. It is individual, appraisal-based

merit pay, which amongst the different forms of VPS is the one to which unions have

exhibited the greatest antagonism (Heery, 2000), where unions have been successful in

asserting collective regulatory control. This reflects both the emergent nature of

management strategy, where apparent concessions over merit pay came to be made in a

wider context of increasing discretion over earnings, and the continuing priority unions

place on securing acceptable increases in real base pay for members. Contrary to some

expectations (e.g. Marsden, 2004b), the ‘common rule’ and not just ‘procedural justice’

remains at the heart of trade union approaches to negotiating pay. The unions maintained

a focus on merit pay as it affected base pay, pensions and relativities; management could

use and refine bonus schemes to incentivise performance ‘on top’ of basic pay without

necessarily disturbing the consistency of established pay grades and rates. The

implication of variable pay for collective bargaining is, therefore, itself variable; trade

unions have largely been successful in defending their core terrain at the same time as a

growing area of pay regulation lies beyond its scope.

Acknowledgements

Thanks to Alex Bryson and the anonymous referees for useful suggestions and comments, and to Molly Gray who conducted the fieldwork in DB and part of C2. The participation of the companies and individuals is also gratefully acknowledged. The research was funded by the ESRC (award RES-000-23-0453).

35

Table 1. The case-study companies

Name Ownership Market, economic performance Employment characteristics

Industrial relations

C1 UK ‘high street bank’; some limited overseas operations.

Pre-tax profits > £4.2bn but ‘voluntary’ job losses due to branch rationalization, outsourcing of processing and offshoring of call centres. Cost- income ratio (CIR), %, 50.8 (2006; 52.8 2005).

Total employment c. 70,000; Retail 35,000 (FTE) in >2000 branches.

Two rival unions (independent union, TU1, and TU2) reflecting merger history. TU1 dominant in membership terms. Overall density c. 75%. Dual bargaining process.

C2 Ex-mutual that subsequently acquired a privatized bank.

Operating profit: £548 m 2005. Branch rationalization strategy. CIR 53.0 (2006; 55.2 2005).

Total employment c. 9000; >250 branches employ 5,500 staff

2 separate (national) bargaining units, with 3 unions (TU1, in acquired bank; mainly managerial TU2, also in acquisition; former staff association, TU3, based in branches and call centres). Overall density 50%.

C3 Subsidiary of large foreign group.

UK profits £360m, up following investment and rationalization strategy. (Group profits around £2.9bn). CIR 62.9 (2006; 68.2 2004)

c. 9000 in around 400 branches

One union. Density c.55%. Single bargaining unit for UK retail (terms and conditions now harmonized from two separate banks)

DB Subsidiary of large UK group.

No recent data; profit was £33m 2001, estimated at £100m 2006). Group profits £11.7bn 2006, CIR 51.0.

3,400 in two sites (2,500 and 900);

One union. Density < 50%. Single bargaining unit covering subsidiary but different pay rates for the two sites

BS1 Large mutual. Profits around £500m. CIR 58.7 2006 (64.1 2004).

>16,000, with c. 10,000 in 680 branches

One union, ex-staff association. Density c. 75%. Single bargaining unit.

BS2 Medium-size/ regional mutual.

Profit £56.6m 2005, up 8.8% on 2004. (No CIR data)

> 1200, including 550 in 49 branches

One union. Low membership but rising with renewed recruitment campaign. Single bargaining unit.

36

Table 2. Profile of VPS in the cases Type of VPS Coverage Criteria Frequency Significance for earnings

Merit pay All employees Individual appraisal around Balanced Scorecard (BSC) with 5 ratings. Replaced matrix (i.e. vertical scale = appraisal rating, horizontal = pay position relative to market rate) 2004

Incorporated into monthly salary

Varies. 2006 pay pot = 4% (but of this, 2.5% dedicated to ‘average market movement’ and 0.5% to grade minima uplifts, leaving 1% for differentiation); 80% staff rated as ‘meets expectations’.

Bonus All employees, ’20 to 30’ schemes tailored to business unit and jobs

Individual sales for incentives bonuses and BSC for branch bonus

Varies 5-6% for main retail workforce

C1

Share scheme All employees Free plus matching shares Annually 3% salary (up to maximum 3000 shares) Merit pay All employees (except 900

‘protected’ staff on old incremental scales)

Matrix, i.e appraisal (6 ratings) relative to position in pay range

Incorporated into monthly salary

Varies 0-7% but in practice most get around RPI (custom that at least ‘satisfactory’ rating = at least RPI increase). 3.5% pay pot 2005 (RPI = 2.9%).

C2

Bonus Customer-facing employees in branches and call-centres (around 60% of non-management staff)

Varies: estimate of 20- 30 schemes . Branch bonus is generated by team performance but allocated individually

Varies Varies. Company and union say overall is a median bonus payer relative to other institutions.

Merit pay All employees Matrix: appraisal (4 ratings) relative to position in pay range

Incorporated into monthly salary

As in C2, scope to vary 0-7% but in practice most get around RPI (at least ‘satisfactory’ rating = at least RPI). 2007, 3.5% pay pot plus ‘range movement’ of 1%; 95% received a pay increase; 82% at or above RPI

UK General Bonus Scheme

All employees (amended for 74 branches geared to business and premier customers, which are much more incentivized)

General bonus covers 2,700 retail staff. Overall pot is determined by company profits; distribution is linked to appraisal scores

Banked quarterly but paid annually at Christmas.

Non-management: 5.5% for staff rated ‘fully competent’; 8.5% ‘commendable’; 14% ‘outstanding’

‘Key Sellers’ retail bonus

Around 1000 specialist sales staff (e,g, mortgage and savings advisers)

Individual, sales-related, criteria Quarterly with additional final payment in December

Varies by role and performance against targets; annual average 2007 = £1,274

C3

Retail ‘Frontline incentive scheme’

General retail staff (3,500). Mix of individual performance (appraisal); team performance (BSC) and company performance (profits)

Twice per year Varies by role but annual average = £880 for customer service grades and up to £6,536 for mortgage manager

37

Table 2 continued

Annual Bonus All employees Standard ‘target award’ linked to company performance is adjusted according to individual appraisal ( 9 ratings computed to an overall score between 0 and 2)

Annual 2005: role levels 1 to 7 = 6.3% multiplied by ‘personal performance factor’ (PPF); level 8-10 = 7.9% x PPF. Range = 0% to 25.5%, average = 14%. Scheme revised 2006 to increase importance of PPF (e.g. difference between a 1.0 and 1.2 PPF score became£800 from £300), and low performers excluded from payments.

Incentive Bonus.

Sales and customer service staff in levels 3-4 (1,700)

Criteria determined by local departments; paid in vouchers.

Monthly or quarterly

Varies but average 5-10%

DB

Share scheme Managers and employees with 3 years experience deemed to have scarce skills; 15% of employees receive

Linked to skills development and individual performance (appraisal)

Annually Between 10-20% salary

Merit pay All employees Individual appraisal (4 ratings) Incorporated into monthly salary

Paybill increase of 5.79% of which 3.83% for base pay (1.77% for salary progression of lower paid and 0.19% for some allowances): 2005 pay award, according to appraisal rating, was 3.5% (74% staff), 5.25% (23%) or 8% (1.3%)

Corporate bonus

All employees 4 company performance measures (cost, profit, market-share, income).

Annually Paid as flat percentage of salary; 2005 = 12.8%. Those rated as low performers (around 400) receive no payment.

Retail bonus Branch staff (9,500) 16 team targets Quarterly Varies; average £50 per quarter. Paid in vouchers

BS1

Incentive bonuses

Retail sales specialists (1000) Individual targets (formula of sales, service, administration)

Monthly (with part annual)

Highly variable: 20-100+%, annual average = £7,000

Merit pay All employees (1,200) Appraisal (BSC), 6 ratings Incorporated into monthly salary

3% pay pot in 2006 but employees with at least ‘good’ rating (i.e. 95%) received at least 2.5%

‘Performance Incentive Pay Schemes’ (PIPs)

Branch staff and 150 call centre employees

Team (branch) performance, but distribution also reflects individual performance (more so for sellers after 2005).

Quarterly Sellers (mortgage and savings advisers) range 0-7%, on target = 3.5% per quarter (i.e. 14% p.a.); other branch staff 0-5% range with 2.5% ‘on-target’ earnings (i.e. 10% p.a.). Quarterly maxima 10% for sellers and 5% general staff.

BS2

Head office bonus

Head office staff (668) Linked to business targets (mortgage offers; net retail receipts; regulated sales commissions; other income)

Quarterly. Varies; generally slightly lower than branch PIPs payouts.

38

References

Adams, J. S. (1965). ‘Inequity in social exchange’, in L. Berkowitz (ed.) Advances in Experimental social Psychology, 2. NY: Academic Press.

Armstrong, M. and Baron, A. (2005). Managing Performance: Performance Management in Action. London: CIPD,

Arrowsmith, J. (2005) ‘Job losses and strike threats hit banking sector’, EIRO. URL: http://www.eurofound.europa.eu/eiro/2005/05/feature/uk0505106f.htm.

Arrowsmith, J., Nicholaisen, H., Bechter, B. and Nonell, R. (2008). ‘The management of variable pay in banking: forms and rationale in four European countries’, Bulletin of Comparative Labour Relations, 67: 201-40.

Bowey, A. and Thorpe, R. (1986). Payment Systems and Productivity. New York: St. Martins.

Brown, W., Deakin, S., Nash, D., Oxenbridge, S. (2000). ‘The Employment Contract: From Collective Procedures to Individual Rights’, British Journal of Industrial Relations 38: 611–629.

Bryson, A. and Freeman, R. (2007). ‘Doing the right thing? Does fair share capitalism improve workplace performance?’. Employment Relations Research Series no. 81, London: DTI.

Bryson, A. and Freeman, R. (2008). ‘How does shared capitalism affect economic performance in the UK?’, Working Paper 14235. Cambridge, MA: National Bureau of Economic Research.

Bryson, A., Pendleton, A. and Whitfield, K. (2008). ‘The changing use of contingent pay at the modern British workplace’, Discussion Paper no. 319, National Institute of Economic and Social Research.

Burke, L. A. and Hsieh, C. (2006). ‘Optimizing fixed and variable compensation costs for employee productivity’, International Journal of Productivity and Performance Management, 55: 155-162.

Cox, A. (2000). The importance of employee participation in determining pay system effectiveness International Journal of Management Reviews, 2: 357-375.

Dalton, G. (1998). ‘Shattering the myth that alternative rewards won’t work with unions’, Compensation and Benefits Review, 30: 38-45.

Daniel, W. and Millward, N. (1983). Workplace Industrial Relations in Britain. London: Heinemann.

Deery S. and Mitchell R., (eds.), Employment Relations: Individualisation and Union Exclusion. Sydney: Federation Press.

Dennis, S. (2004). 'Pay in finance banking on brighter prospects', IRS Employment Review. 804. 32-35.

39

Druker, J. (2000). ‘Wages systems’, in J. Druker and G. White (eds.) Reward Management, London: Routledge.

Edwards, P. (2006). ‘Industrial relations and critical realism: IR’s tacit contribution’, Warwick Papers in Industrial Relations, no. 80

Edwards, R. (1979). Contested Terrain: The Transformation of the Workplace in the Twentieth Century. London: Heinemann.

Flanders, A. (1975). Management and Unions: The Theory and Reform of Industrial Relations. London: Faber and Faber

Flannery, T. P., Hofrichter, D. A. and Platten, P. E. (1996). People, Performance and Pay: Dynamic Compensation for Changing Organizations. New York: Free Press.

Forth, J. and Millward, N. (2002). ‘Pay settlements in Britain’, NIESR Discussion Paper 173. London: National Institute of Economic and Social Research.

Guest, D. (1987), ‘Human resource management and industrial relations’, Journal of Management Studies, 24: 503-21.

Heery, E. (1997). ‘Performance-related pay and trade union de-recognition’, Employee Relations, 19: 208-221.

Heery, E. (2000). ‘Trade unions and the management of reward’ in J Druker and G White (eds.). Reward Management. London: Routledge.

Hendry, C., Woodward, S., Bradly, P. and Perkins, S. (2000). ‘Performance and reward: Cleaning out the stables’, Human Resource Management Journal, 10: 46-62.

Hyman, R. 1997. ‘The future of employee representation’, British Journal of Industrial Relations, 35: 309–336.

Kaplan, R. and Norton, D. (1996). The Balanced Scorecard: Translating Strategy into Action. Boston: Harvard Business School Press

Kersley B., Alpin C., Forth J., Bryson A., Bewley H., Dix G. and Oxenbridge S. (2006). Inside the Workplace. London: Routledge.

Kessler, I. (1994). ‘Reward systems’, in J. Storey (ed.) Human Resource Management - A Critical Text. London: Routledge

Kessler, I. (2001). ‘Reward Choices’, in J. Storey (ed.) Human Resource Management - A Critical Text (2nd edition). London: Thomson. 206-223.

Kessler, I. and Purcell J., (1992). ‘Performance related pay: objectives and application’. Human Resource Management Journal. 2: 16-33.

Kessler, I. and Purcell, J. (1995). ‘Individualism and collectivism in theory and practice: Management style and the design of pay systems’, in P. Edwards (ed.), Industrial Relations. Oxford: Blackwell.

Lawler, E. (1981). Pay and Organization Development. Reading MA: Addison-Wesley.

Lawler, E. (1995). ‘The New Pay: A Strategic Approach’, Compensation Benefits Review; July-August. 14-22

40

Marginson, P., Arrowsmith, J. and Gray, M. (2008). ‘Undermining or Reframing Collective Bargaining? Variable Pay in Two Sectors Compared’, Human Resource Management Journal, 18: 327-46

Marsden, D. (2004a). ‘The role of performance related pay in renegotiating the ‘effort bargain’: The case of the British public service’. Industrial and Labor Relations Review 57: 350-370.

Marsden, D. (2004b). ‘Unions and procedural justice: An alternative to the common rule', CEP working paper 0613, LSE.

Marx, K. (1967). Capital, volume 1. New York: International Press.

Metcalf, D., Hansen, K. and Charlwood, A. (2001). ‘Unions and the sword of justice: unions and pay systems, pay inequality, pay discrimination and low pay’, National Institute Economic Review; 176: 61-75

Mintzberg, H. and Waters, J. (1985). ‘Of strategies, deliberate and emergent’, Strategic Management Journal, 3: 257-272.

Pendleton, A. (1997). ‘Characteristics of workplaces with financial participation: evidence from the Workplace Industrial Relations Survey’, Industrial Relations Journal, 28: 103-119

Poutsma, E. (2006). Employee Share Ownership and Profit-sharing in the European Union. European Industrial Relations Observatory. http://www.eurofound.europa.eu/pubdocs/2001/56/en/1/ef0156en.pdf

Prendergast, C. (1999). ‘The Provision of Incentives in Firms’, Journal of Economic Literature, 37: 7-63.

Schuster, J. R. and Zingheim, P. K. (1996). The New Pay: Linking Employee and Organizational Performance. San Francisco: Jossey-Bass.

Sengupta, S. (2008). ‘The impact of employee-share-ownership schemes on performance in unionised and non-unionised workplaces’, Industrial Relations Journal, 39: 170-90.

Storey, J. (1995). ‘Employment policies and practices in UK clearing banks: An overview’, Human Resource Management Journal, 5: 24-43.

Tyson, S. (2002) ‘The Changing Nature of Human Resource Management’, in F. Analoui (ed.) The Changing Patterns of Human Resource Management. Aldershot: Ashgate

Walsh, J. (1993). 'Internalisation versus decentralisation: An analysis of recent developments in pay bargaining', British Journal of Industrial Relations, 31: 409-432.

Wood, S. J. and Bryson, A. (2008). ‘The rise of high-involvement management in Britain’, NIESR Discussion Paper no, 321. London: National Institute for Economic and Social Research.

i The comparative element also involved UK sector comparisons, i.e. mechanical engineering, which was co-ordinated by Marginson, as well as banking, co-ordinated by Arrowsmith (see e.g. Marginson et al, 2008). Cross-national comparison was also conducted via coordinated projects in Austria, Norway and Spain (see e.g. Arrowsmith et al, 2008).

41