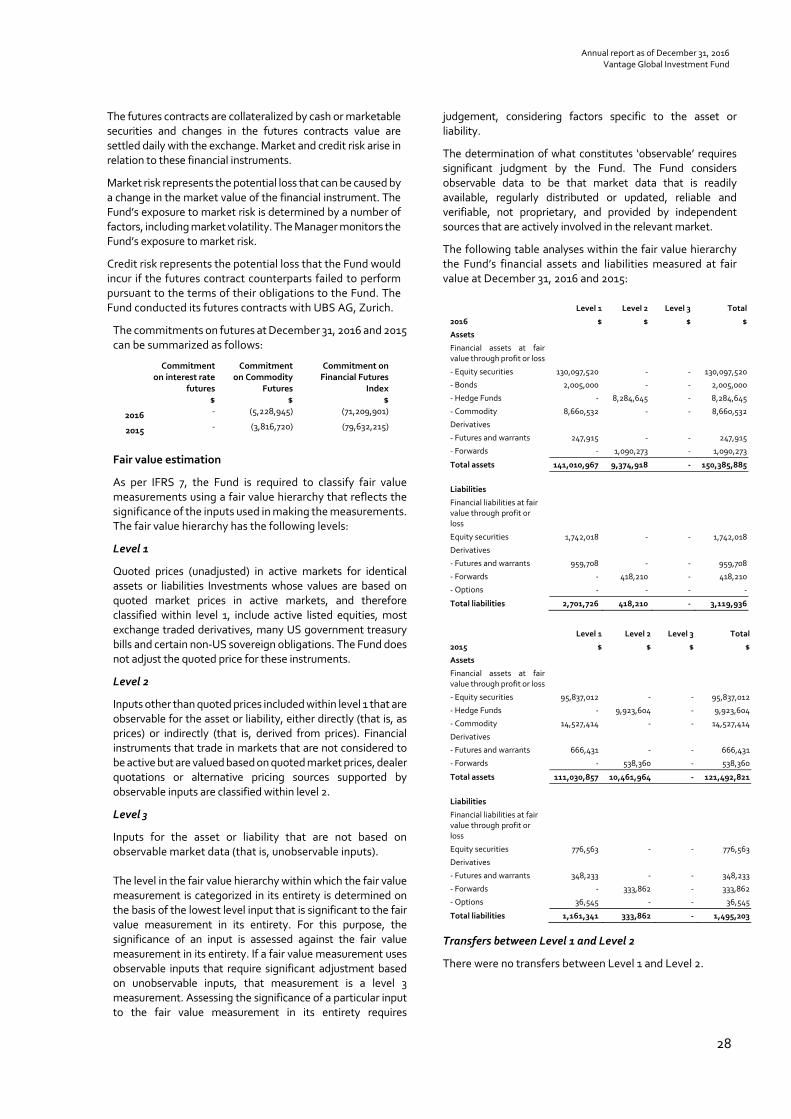

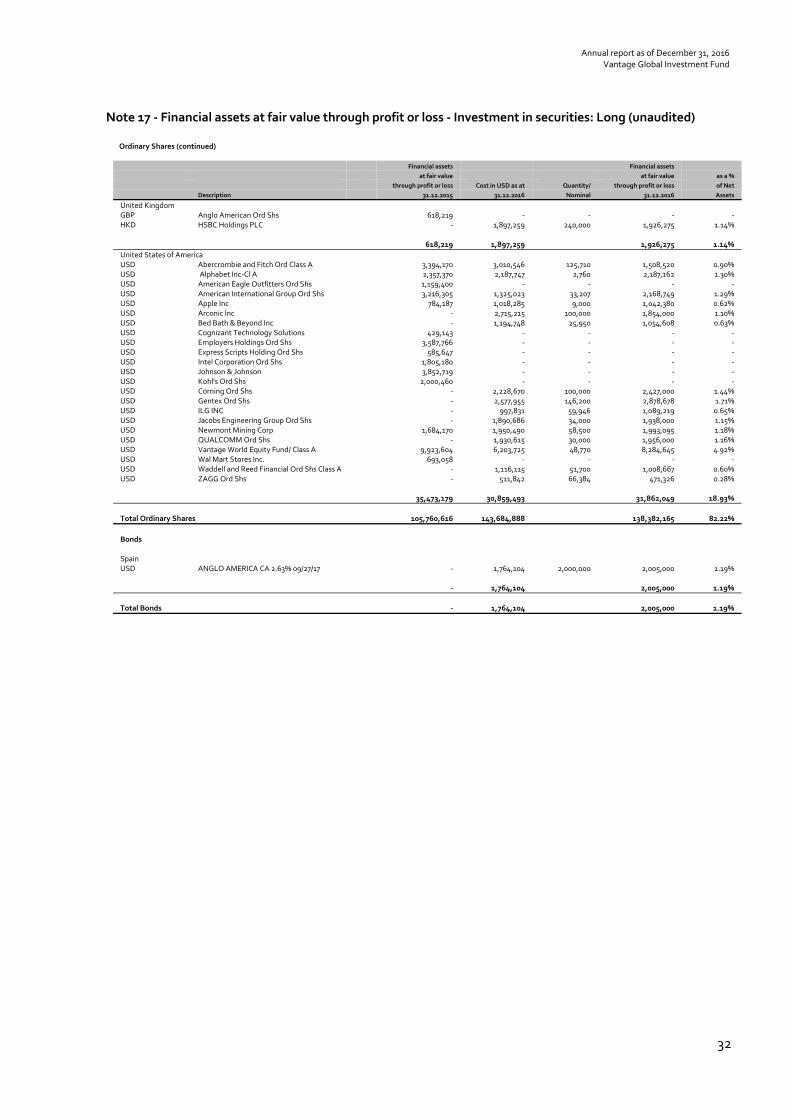

vantage · 2019. 1. 3. · 4 vantage global investment fund annual report to 31 december 2016...

TRANSCRIPT

ANNUAL REPORT

31 December 2016

GLOBAL INVESTMENT FUND

VANTAGE

Annual report as of December 31, 2016 Contents

Executives and Other Information 3 Directors’ Report 4‐5 Manager’s Report 6‐15 Independent Auditor's Report 16‐17

Audited Financial Statements of Vantage Global Investment Fund 18‐20

Notes to the Financial Statements 21‐36

The Portfolio Movements can be obtained from the registered office of the Fund or from the Administrator.

3

Executives and Other Information Annual report as of December 31, 2016

Vantage Global Investment Fund

Directors Custodians and Prime Brokers Andrew B. Veglio di Castelletto UBS AG (London) Christopher D. Corrigan 1 Finsbury Avenue Richard Davidson London EC2M 2PP United Kingdom Investment Manager UBS AG (Zurich) Vantage Investment Management Limited Bahnhofstrasse 45 2nd Floor, Block B, Ruisseau Créole 8001 Zürich Black River, Mauritius Switzerland Independent Auditors of the Fund Administrator and Banker BDO MUFG Alternative Fund Services (Cayman) Limited P.O. Box 31118 P.O. Box 852 GT 2nd Floor – Building 3 227 Elgin Avenue Governors Square George Town 23 Lime Tree Bay Avenue Grand Cayman, KY1‐1103 Grand Cayman KY1‐1205 Cayman Islands Cayman Islands Investment Advisor Registered Office Vantage Investment Advisory Limited MUFG Alternative Fund Services (Cayman) Limited 43 Brook Street P.O. Box 852 GT London W1K 4HJ 227 Elgin Avenue United Kingdom George Town Grand Cayman KY1‐1103 Cayman Islands Legal Counsel Walkers Walker House George Town Grand Cayman KY1‐9001 Cayman Islands

4

VANTAGE GLOBAL INVESTMENT FUND

ANNUAL REPORT to 31 December 2016

DIRECTOR’S REPORT Dear Member, Your Fund’s Net Asset Value gained 1% over the year, under performing its Investment Benchmark which rose 3.2% over the period and the 8.2% return of the world’s equity markets as represented by the MSCI World Index (MSWI), all measured in US dollars. The Risk Free Rate lost 2.0% over the year measured in US dollars as the US dollar strengthened against most other major currencies. Your Fund’s under performance versus the MSWI over the final quarter was due to renewed weakness in gold and gold shares, retained as a hedge against monetary instability, and the sharp appreciation of the US equity market post the November 8 election victory of Donald Trump, where your Fund held no net exposure after hedging. Your Fund’s significant overweight in the US dollar, averaging over 70% of its net assets over the year, contributed to its out performance of the Risk Free Rate. Subsequent to year-end your Fund has recovered some of its fourth quarter underperformance, rising 3.7% in US dollars versus the 2.4% gain in its Investment Benchmark. Global equity markets have experienced a roller coaster ride over the past eighteen months. Equity markets entered 2016 on a continuing weakening trend – the MSWI lost some 18% measured in US dollars from its May 2015 peak to its February 2016 lows. This equity slump reflected concerns about the US Federal Reserve’s move to normalise monetary policy and the collapse in global commodity prices provoked by these concerns, as well as by the slowing Chinese economy. With the Fed signalling a very cautious approach to raising interest rates, and the Chinese authorities encouraging faster credit growth and hence a domestic recovery, equity markets rallied progressively from their February lows. They quickly recovered sharp initial losses from the unexpected UK Brexit vote end June and the election of Donald J Trump as President of the USA early November. Total return funds had a tough time managing this volatility with many experiencing negative returns in 2016. Global bond markets appreciated sharply to generational peaks around mid 2016, and have subsequently been selling off, as fear of global deflation gradually shifted, along with higher commodity prices and recovering global economies, to views that global reflation is likely underway. With concerns that monetary policy makers will be slow to react to rising inflationary pressures, the prices of inflation protected bonds surged. It certainly appears that an inflection point has been reached in the 35 year old bull market in developed economy government bonds. The US dollar initially weakened against a trade weighted basket of currencies after its sharp appreciation in 2015, then gathered momentum in the final quarter to end the year broadly unchanged but on a strengthening trend. The UK pound was the weakest major currency, losing some 17% against the US dollar post the British referendum vote to exit the European Union.

At time of writing global equity markets continue on a rallying trend, with US equity market indices at all time highs. The markets have taken President Trump’s promises to cut US corporate taxes and regulation and to massively increase US infrastructure spending, as well as his appointments of several financial industry insiders to his Administration, as significant positives. They have chosen to ignore the risks associated with the many inconsistencies and ‘alternative facts’ in his pronouncements, the impact of his trade unilateralism and protectionism on global and US economic growth, and the geo-political impact of his abrasive foreign policy positions and his America First myopia. We discuss at length our take on the Trump phenomena in the Manager’s report. Suffice to state that we don’t believe his tenure of this most influential of global posts bodes well for the USA’s economic and geo-political standing in an increasingly fractured global order. Your Fund ended the year with a 95% gross exposure to global equities, and a 51% net exposure after hedging. The US dollar exposure ended the year at 75%, with a 5% exposure to gold bullion and a 7% exposure to the now undervalued UK pound. We remain grateful for your support as we continue to seek to add value for your Fund.

Andrew Veglio di Castelletto 27 January 2017

5

VANTAGE GLOBAL INVESTMENT FUND

ANNUAL REPORT to 31 December 2016

VANTAGE GLOBAL AND BENCHMARKS IN US$ 5/1/17

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 1650

100

150

200

250

300

350

VANTAGE FUND

MSCI WORLD INDEX

RISK FREE BENCHMARK

VANTAGE BENCHMARK

Source: DATASTREAM

The Performance of the Vantage Global Investment Fund and its Comparative Indices since 2001 is presented below:

PERFORMANCE OF VANTAGE GLOBAL AND COMPARATIVE INDICES TO 30 DECEMBER 2016

% Returns In US$

% Returns In Currency Benchmark (3)

Returns over the Preceding: Quarter(1)

Year to Date (2)

Since Incept. (9)

Quarter

Year to Date

Since Incept.

Vantage Global (2.3) 1.0 348.5 2.1 3.2 395.1

Fund’s Benchmark (4) (1.2) 3.2 149.2 3.3 5.5 175.0

MSWI (5) 2.0 8.2 282.1 6.6 10.5 321.7

Risk Free (6) (4.2) (2.0) 40.0 0.0 0.2 54.5

Value Added Risk Free (7) 2.1 3.0 220.4 2.1 3.0 220.4

V.A. Investment Benchmark (8) (1.1) (2.2) 80.0 (1.1) (2.2) 80.0

Key to Performance Table

1. Quarterly returns are presented from the last trading NAV of the previous calendar quarter; 2. Current year returns are presented from the last NAV of the previous calendar year; 3. The Currency Benchmark is defined as 40% US dollar, 20% Euro, 10% Yen, 10% UK pound, 10% Singapore

dollar, 5% Swiss franc, 2.5% Canada dollar, 2.5% Australia dollar as from 1st Jan 2011. 4. The Fund’s Investment Benchmark is defined as the average of the returns of the MSWI and of Risk Free

securities, i.e. 50% MSWI plus 50% Risk Free. 5. MSWI is defined as the MSCI World Index including income. 6. Risk Free is defined as the return generated from investing in 6 month Government Securities, in the

weightings of the Currency Benchmark. 7. Value Added Risk Free is defined as the net return earned by the Fund over the period after deducting all

expenses and Fees including the Manager’s Performance Fee (the “Net Return”), and after deducting the return that would have been derived from investing all the Net Assets of the Fund in Risk Free securities.

8. Value Added Investment Benchmark is defined as the net return earned by the Fund after deducting the return that would have been derived from investing all the Net Assets of the Fund in the Fund’s Investment Benchmark.

9. Inception of the Fund was on 1st January 1996.

6

VANTAGE GLOBAL INVESTMENT FUND

ANNUAL REPORT to 31 December 2016

REGIONAL EQUITY INDICES IN US$ - REBASED TO 100 5/1/17

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC80

85

90

95

100

105

110

115

120

USA

EUROPE

JAPAN

ASIA

Source: DATASTREAM

MANAGER’S REPORT

Equities and Economies Over the year to December 2016 the MSCI World Index including income (MSWI) increased by 8.2% measured in the US dollar and 9.6% in local currencies. The table below shows the regional equity market returns over the year to 30th December 2016: Equity Market Local Currency

Return US Dollar Return Weighting in

World Index World Index 9.6 8.2 100% United States 11.6 11.6 60% Europe 8.3 1.0 23% Japan -0.4 2.7 9% Asia Pacific Ex Japan 6.4 5.8 1% Others 10.6 9.4 7%

The chart below shows the evolution of the regional equity markets measured in US dollars over the course of 2016:

After falling sharply in January and early February to a low on the MSWI of down 13%YTD, the markets rallied to broadly break even by mid year, and then continued to gain into year end. The US equity market was again the best performing major market, gaining 11.6% for the year, with more than half of that gain coming after the Nov 8th election of Donald J Trump as President of the USA. Up until that stage it did look as if equity markets were tracing out a topping pattern with September 2016 highs. However subsequent equity market strength has invalidated that view, and most equity markets appear now to be in renewed bull markets. Supporting the US equity market is a gradual recovery in overall US corporate earnings as the energy and commodity related falls of 2015 wash out, as well as the still very accommodative monetary policies deployed by the US Fed.

7

VANTAGE GLOBAL INVESTMENT FUND

ANNUAL REPORT to 31 December 2016

While the fourth quarter 2016 US GDP growth numbers just announced came in softer than expected at 1.9% annualised, a resurgence in US consumer confidence and US small business optimism surveys to 15 year highs, combined with strong increases in forward looking surveys for manufacturing, for orders, and for imports and exports, all point to renewed strength in the US economy into early/mid 2017. With few signs of a US economic recession in sight, and expectations that President Trump will cut US corporate taxes, deregulate the US economy, and greatly increase fiscal spending on infrastructure, the US equity market has found renewed confidence and looks to be moving higher. We are firmly of the view that the election of Donald Trump to the Presidency of the world’s dominant military and economic power will foster neither US nor global economy prosperity, much less geopolitical stability. The post WW II global economic and political consensus has been eroding for some time (in our view the 1999 NATO bombing of Belgrade in support of the separatist KLA in Kosovo, a millennium old province of independent Serbia, without supporting UN authorisation and operating outside of NATO’s defensive charter, marked a start of a breakdown in the international order). The USA’s relative economic dominance is inevitably diminishing due to the shift in economic power to Asia, and principally to China. We believe that the Trump phenomena will accelerate rather than arrest this trend. We fully understand the frustrations of Middle America at the perceived East Coast bias towards globalisation, unfettered free trade, and monetary largesse. Major US corporations have for decades boosted their profits by relocating production and investment to low cost countries. These corporate investment decisions hollowed out many US industrial communities while contributing to the creation of significant and sustainable overseas competitors through the technology transfer requirements imposed by these low cost countries, particularly China. US industrial workers have borne the brunt of globalisation policies that have overwhelmingly benefited ‘East Coast’ elites and Wall Street mavens. President Trump’s success in connecting with this large community, who feel marginalized and ignored by Washington’s career politicians and the ‘special interests’ they represent, and whose confidence in the future has been shaken by serial redundancies, long term unemployment, mid life retraining requirements and falling real wages, has been the foundation of his success. He has also successfully plugged into the growing view that political correctness has reached absurd levels and that support for minorities, particularly of recent immigrant and refugee populations, has taken precedence over, and even been at the expense of, the interests of long term US citizens. His projection of himself as a successful self made business man, is seen by his supporters as key to him upholding basic American values of free enterprise and free choice, individual responsibility, and national pride, which they believe to have been severely eroded under two terms of President Obama’s Administration. We get all that and empathise with some of it – although we should note that under President Obama the USA had experienced the longest period of unbroken job creation for 40 years, that the current headline US unemployment rate of 4.7%is the lowest since 2000 and second lowest over those 40 years, and that the US equity market’s ratings are near their highest ever, after enjoying one of the longest bull runs on record. It is ironic that Donald Trump has been elected ‘to fix the carnage’ just as real wages for Middle America start to rise sharply, as the US economy nears fill employment, and as the US equity market reaches record levels. The problem is that in Donald Trump the US has elected a President with a history replete with failed enterprises, broken promises, unpaid creditors, and disenchanted customers.

8

VANTAGE GLOBAL INVESTMENT FUND

ANNUAL REPORT to 31 December 2016

They now have a President whose world views often seem so simplistic that he feels able and indeed impelled to convey them via 144 letter Twitter outbursts, a man who has scant regard for fact or truth, who is braggadacious beyond compare (except perhaps for a select few African potentates), whose grasp of economics appears almost non-existent, who seems disinclined to take advice or even seek input from the expert staff available in the US public administration, who doubles down on any opposition, denigrating and belittling those who offer any criticism of his often bizarre behaviour and policy pronouncements. One of the basic tenets of Vantage’s investment philosophy is that good companies tend to remain good companies over time, despite short term market or cyclical factors, and that lousy companies tend, over time to revert to type. We have over the years sometimes not followed this principle (witness the investment in gold shares when we thought the global fiat monetary system might collapse under the unparalleled abuses visited on it by Central Banks post 2008). We have always, over time, lived to regret deviations from this tenet, and are committed never to stray down that path again.

We view Mr Trump in much the same light. His track record is one of personal success at the expense of his creditors, his customers, and in the one listed company he ran, (and into the ground at that), of his shareholders. He has not created any major operating businesses, and most of the operating businesses he established have failed. He has personally prospered out of being long US real estate, and by being bailed out periodically by the US Federal Reserve’s extreme monetary largesse. His statements that he is going to ‘Make America Great Again’, ‘Win so much Americans will get tired of Winning’, ‘Put America First instead of Last’ etc. are beguiling to those who feel that the nation’s and their personal relative positions have been slipping for decades. However, beyond a potential short term fillip, none of his policies, if enacted, appear likely to create more US jobs, enhance America’s long term global standing and influence, or increase its national and domestic security. To the contrary some of his pronouncements, if carried through, will bring the US into direct economic conflict with many of its major trading partners (or adversaries as he views them), and potentially militarily too.

On the campaigning stump President Trump appeared to view most issues as a simple zero sum game. In order to win somebody else had to get screwed (we guess that may well be his leitmotif). Hopes that the responsibility of Office and access to a well informed staff would attenuate his more extreme views appear, certainly on early evidence, to be misplaced. Rather than seek outside counsel, President Trump has surrounded himself in his Administration with campaign supporters who hold similar views. Witness the worrying appointment of Stephen Brannon, Chairman of the ‘Alt-Right’ Breitbart News and CEO of Trump’s election campaign, as Chief Strategist and Senior Counsellor to the President, and to the US National Security Council (NSC), while dropping the permanent attendance of the Director of National Intelligence and or the Joint Chief of Staff of the US military! Also the appointment of his son-in-law Jared Kushner as Senior White House Advisor (he who will successfully forge a Palestinian/Israeli peace accord according the President Trump!)

Most of Trump’s trade or industrial policies appear to us profoundly short sighted. Take for example his trumpeted success in creating 700 auto jobs in Michigan by pressurising Ford to abandon a $1.6bn half way completed plant in Mexico by threatening to impose a 20% trade tariff on car imports from Mexico. Ford will now write off a major investment which would have lowered its cost of production, improved its ability to supply the Mexican domestic market, and benefited North American component suppliers as well as US consumers. Instead Ford will create a paltry number of jobs in an area with rising labour costs as full employment and a skills shortage starts to bite.

9

VANTAGE GLOBAL INVESTMENT FUND

ANNUAL REPORT to 31 December 2016

Despite the overwhelming evidence that command economies fail, and that political interference in the functioning of markets bears a heavy economic cost, Mr Trump thinks he is in a better position than the Ford directors on deciding where to allocate their capital. Let’s say he is successful in this drive, and the US auto industry abandons in some measure its lower cost overseas production facilities and returns production to the US. Will that make US cars better, more reliable or more affordable? And if the price of US cars and other imported goods goes up, what happens to interest rates? And if US interest rates go up (US consumers buy cars overwhelmingly on credit), what will happen to demand for these more costly US manufactured cars. And if demand for US manufactured cars falls (from the near record current levels of around 17 million vehicles per year), what happens to those US auto jobs and the jobs of N.A. auto component suppliers?

Economic nuances appear lost on President Trump and his Alt-Right advisors, just as the nuances of removing militarily the principal secular leader in the Middle East on bogus WMD charges, at a time of rising Islamic fundamentalism, were lost on President George W. Bush and his Neo-Con advisors. It is profoundly ironic that President Trump claims that he foresaw the problems that would arise from the US invasion of Iraq (against which millions marched in Europe and around the world), while appearing to be blundering into equally misguided attack on global trading partners, including withdrawing from the Trans Pacific Partnership (TPP) trade deal, at a time when China is moving to occupy the policy gap left by American disengagement. Unlike President Trump, we wrote in your Fund’s 2002 reports and elsewhere about the likely dysfunctional outcome of destabilizing Iraq. We are equally clear that President Trump’s campaign promises to renegotiate or scrap most multilateral trade deals between the US and its trading partners, to coerce US Industrial companies to relocate their manufacturing back home and slap tariffs on imports from countries with trade surpluses with the US, will damage the US and global economies to the extent they are enacted.

There have been attempts to liken President Trump’s election to that of President Reagan, a President initially ridiculed by much of the establishment as a Californian bumpkin with little grasp of economics and no experience of Congress, and who turned out to be one of the most successful two term US Presidents and one of the most loved to boot. We couldn’t disagree more. President Reagan was a two term serving Governor of California before election. He was a great communicator and a prodigious delegator. He was pro-free trade and pro immigration into the US. He focussed on a few major areas of policy, articulated them clearly and simply, and built alliances across party lines and internationally to help achieve his policy objectives. His message was usually inspirational and often uplifting. Donald Trump’s message is one of current US despair and carnage, even at a time of remarkable US stability and prosperity. His speeches, far from uplifting, are angry tirades against his perceived personal injustices or threats to US economic and national interests, none of which are supported by fact. Donald Trump is no Ronald Reagan - in many ways he is his antithesis!

We have written at length about President Trump because we think that his election, without a popular mandate, and after attempts to influence the election outcome by President Putin’s Russia, will prove a defining moment in US political and economic history. The most unpopular US President to take office in the modern era, President Trump’s first week in office confirms that he will likely continue to polarise US society, antagonize important geo-political allies and diminish the US’s international standing. His world view that the US has somehow come off second best in most major negotiations since the 1960’s is at odds with the general perception that the US has generally set the framework for, and prospered from, the post WW II geopolitical, trade and financial order. We could go on and on, but Members will be aware of all of the above, and more, from the general coverage of President Trump’s election and of his Administration.

10

VANTAGE GLOBAL INVESTMENT FUND

ANNUAL REPORT to 31 December 2016

After an eight year US equity bull market, one of the longest on record, and with the US equity market trading near its peak levels relative to normalised earnings of 26X (excluding to 1999/2000 bubble) we expect that the current US equity market euphoria will give way to caution and then angst moving into 2018. We understand the drivers for short term continued US equity price appreciation. However we think the US equity market’s positive initial response to President Trump’s election will, over time, give way to concern about the impact of his policy choices on US inflation and US interest rates, on global trade and US corporate earnings, on US equity risk premia and hence on US equity prices. We see little sign that the Republican controlled Congress is willing, or indeed yet feels politically able, to moderate Trump’s excesses. In summary we think that President Trump’s Administration will damage the US economy and severely challenge to the US’s pre-eminent global position over time. It does appear that European economies are finally recovering from their 2008 slump, helped by the globally competitive Euro exchange rate and by the extreme monetary accommodation of the ECB, currently adding some Euro 80bn per month (falling to E60Bn per month in April) to the Euro area monetary base. Higher long term European interest rates are lifting the cloud under which European financials have languished. One such European financial company in which your Fund has a position is the Italian insurer Generali. The chart below shows Generali’s share price (light blue) relative to its fundamentals over the past 30 years:

Shares in Assicurazioni Generali, along with many other European financials, appear significantly undervalued and offer attractive long term return potential. Recently Generali has been subject to takeover speculation, but our investment case is independent of its attractiveness as a takeover candidate in an industry ripe for consolidation. Your Fund ended the year with a 95% gross exposure and a 51% net exposure to global equities, the highest such exposures for years. Your Fund has subsequent to quarter end increased its exposure to European stocks, such that its gross equity exposure is now at it maximum 100%. We continue to find good value in Asian equity markets. We think that the move from economically defensive stocks into cyclical stocks has a way to run, and this move should benefit your Fund. After another disappointing year, wherein your Fund lagged its Investment Benchmark although at least added value relative to Risk Free, it is encouraging to note that your Fund, despite its low risk characteristics, is ahead of all of its benchmarks year to date.

Assicurazioni Generali

NAV PS

Dividends PS*20

Sales PS

EPS*10

11

VANTAGE GLOBAL INVESTMENT FUND

ANNUAL REPORT to 31 December 2016

Fixed Interest The chart below shows the evolution of the prices of long-term Government Bond futures over the past 3 years:

After falling to all time lows in September 2016, based on lingering concerns about global deflation, and on continued aggressive Central Bank bond purchasing in Europe and Japan, the yields on government bonds have started to push higher (bond prices have started to fall). US 30 year treasury bond interest rates touched a low of 2.1% back in July 2016 – they are currently close to 3.2%. UK 20 year GILT rates have nearly doubled from the absurdly low 1.1% reached in August 2016, on BOE buying post the Brexit vote to offset the deflationary impact they foresaw from Britain’s withdrawal from the EU. It seems clear to us that inflation, in both the US and the UK is heading higher, and that monetary policy in both countries will lag this push up in prices. Hence we think it appropriate that government bond prices are falling, and expect that the 30 year bull market in government bonds has peaked. European long-term interest rates are rising as signs of economic recovery take hold, European inflation starts rising, and the ECB signals it intends scaling back on monthly government bond purchases. Even Japanese long-term interest rates appear to have bottomed in July at negative 30 bps for 10 year JGB’s, on concerns of the Bank of Japan about the damage negative long term interest rates were causing to the Japanese long term insurance and the savings and pensions industries. While fixed interest is not a core focus of your Fund, we will from time to time seek to augment its returns, when interest rates appear anomalous as they do now, by investing in or selling short government bonds and/or their derivatives. We think that government bond yields reached absurdly low levels in Q3 2016. Your Fund has a 6% short position across the spectrum of long-term government bond futures

12

VANTAGE GLOBAL INVESTMENT FUND

ANNUAL REPORT to 31 December 2016

Currencies

The chart below shows the evolution of the US dollar’s exchange rate against the Euro, the UK pound, the Japanese yen and the Chinese yuan, all rebased to 100 on 1 January 2014:

Since January 2014, the US dollar has appreciated by a quarter against the Euro and the UK pound, and by close to 10% against the Japanese yen and the Chinese yuan. Over the course of 2016 the UK pound fell 17%, the Chinese yuan 6% and the Euro 4% against the US dollar, while the Japanese yen gained 3%. Against its broad trade weighted index the US dollar gained 2% over the year, more than recovering its 6% losses between January and April 2016. The chart below shows the USD per GBP exchange rate and the Vantage and OECD measures of the Purchasing Power Parity between the two currencies:

The UK pound appears some 12 to 15% undervalued against the US dollar. We think the outlook for the UK’s trading position is more favourable than the consensus post Brexit appears to be, and have recently increased your Fund’s exposure to the UK pound to the 10% neutral position in its Currency Benchmark (CB). Your Fund’s 75% exposure to the US dollar is significantly over weight relative to a 40% CB neutral position. We think that the US Fed will be more aggressive in raising interest rates this year, both to counter the impact of increased fiscal spending at a time when the US economy is nearing full employment, and because US inflation looks like accelerating, especially should President Trump impose import tariffs.

Deviation of USD/GBP from OECD PPP

Deviation of USD/GBP from Vantage PPP

Vantage PPP

USD per GBP

OECD PPP

USD per GBP and measures of their PPP

13

VANTAGE GLOBAL INVESTMENT FUND

ANNUAL REPORT to 31 December 2016

INVESTMENTS, HEDGES, AND NET ASSETS AT 30 DECEMBER 2016

Percent Portfolio Holdings Number Market Value 94.6% SHARES HELD LONG

$ 159,225,172

22.6% North America $ 38,038,995 1.8% Gentex 146,200 $ 3,023,416 1.5% Honda Motors ADR 83,300 $ 2,553,978 1.5% Corning 100,000 $ 2,446,000 1.4% Carnival 46,107 $ 2,435,372

16.4% Investments less than 1.4%

$ 27,580,229

47.4% Japan and Pacific Rim $ 79,780,900 2.6% Mitsubishi Heavy Ind 938,000 $ 4,350,644 2.3% Japan Petroleum 169,000 $ 3,871,341 2.1% Mitsubishi UFJ Finl.gp 559,600 $ 3,556,167 2.1% Mediatek 517,000 $ 3,465,384 1.3% Investments less than 2.1% 280,000 $ 2,172,534

24.6% Europe, UK and other EMEA $ 41,405,277 1.9% Brown Gp 1,305,329 $ 3,281,014 1.8% Lukoil 51,162 $ 2,951,024 1.3% Supergroup 111,509 $ 2,269,749 1.3% Tesco 894,227 $ 2,264,214

18.2% Investments less than 1.3%

$ 30,639,276

(1.0%) SHARES SOLD SHORT ($ 1,683,141)

(1.0%) Exxon Mobil (19,300) ($ 1,734,877)

EXPOSURE

(0.6%) STOCK MARKET HEDGES ($ 927,630) (42.9%)

0.1% S&P Futures (242) $ 220,845 (15.7%)

(0.1%) Hang Seng Futures (100) ($ 194,726) (8.2%)

(0.2%) Nikkei Futures (119) ($ 329,834) (5.6%)

(0.2%) Other Stock Index Futures

($ 403,070) (13.4%)

(0.0%) COMMODITY ($ 37,380) 2.0%

(0.0%) Platinum Futures 74 ($ 37,380) 2.0%

1.2% BONDS $ 1,999,000 1.2%

1.2% Anglo American Capital 2012 5/8% 27/09/2017 2.000.000 $ 1,999,000 1.2%

(0.0%) BOND FUTURES

($ 62,247) (4.9%)

(0.0%) BTP Italy Bond Futures (20) ($ 27,553) (1.6%)

(0.0%) JGB Bond Futures (14) ($ 2,395) (1.0%)

(0.0%) Other Bond Futures

($ 32,299) (2.3%)

5.8% CASH AND EQUIVALENTS $ 9,738,115 5.2% Gold Bullion 7,518 $ 8,760,791 5.1%

0.6% Cash, and Margin Deposits Net of Provisions

$ 977,324

100.0% NET ASSET VALUE $ 168,314,135.00

Net Asset Value per Share $ 448.50

Number of Shares in Issue 375,284

14

VANTAGE GLOBAL INVESTMENT FUND

ANNUAL REPORT to 31 December 2016

EXPOSURES TO INVESTMENTS AND HEDGES AT 30 DECEMBER 2016

EQUITY EXPOSURE

Investments by Country

Long Exposure (%)

Short Exposure %

Investment Hedges (%)

Net Exposure (%)

Weight in MSWI (%)

U.S.A 22 (1) (16) 5 60 Canada 1 - 0 1 4 North America 23 (1) (16) 6 64 United Kingdom 10 - (5) 5 7 Germany 3 - 0 3 3 Ireland 1 - 0 1 Other Europe 4 - 0 4 13 Europe 19 - (5) 14 23 Japan 16 - (6) 10 9 Taiwan 9 - (4) 5 Hong Kong 8 - (8) 0 1 China 6 - (4) 2 South Korea 4 - (1) 2 South Africa 4 - 0 4 Other 8 - 0 8 3 Asia Pacific and Other 38 - (17) 21 4 TOTAL EQUITIES 95 (1) (43) 51 100

CURRENCY EXPOSURE

Currencies by Country Investment Exposure %

Currency Hedges %

Net Exposure % Weight in Currency

Benchmark % Gold 5 5 - US Dollar 22 50 72 40 Hong Kong Dollar 8 (4) 4 US Dollar Block 30 45 75 Canadian Dollar 1 (1) 0 2.5 GBP 10 (3) 7 10 Euro 5 (5) 0 20 Swiss Franc 1 (1) 0 5 Other Europe 3 (2) 1 Europe 9 (8) 1 Japanese Yen 16 (12) 4 10 China Yuan 6 (3) 3 Singapore Dollar 1 0 1 10 Australian Dollar 2 (3) (1) 2.5 Other 22 (17) 5 Asia Pacific and Other 30 (22) 8 TOTAL 100 0 100 100

(Please note that numbers may not add up to totals due to rounding)

15

VANTAGE GLOBAL INVESTMENT FUND

ANNUAL REPORT to 31 December 2016

APPOINTMENTS Directors of the Fund :

Web Site :

Andrew B. Veglio di Castelletto www.vantagefunds.com Richard Davidson (to 31 Dec 2016) Christopher D. Corrigan Ian Lambert (from 1 Jan 2017)

Custodians : Investment Manager : UBS AG (London) Vantage Investment Management Ltd. 1 Finsbury Avenue, London EC2M 2PP

2nd Floor, Block B, Ruisseau Creole, Black River, 90625 Mauritius

Tel: + 44 20 7567 8000 Tel : +230 483 4767 Fax: + 44 20 7568 7024 UBS AG (Zurich) Bahnhofstrasse 45, 8001 Zurich Tel: + 41 44 234 1111 Fax: + 41 44 237 6094 Administrator and Registered Office : MUFG Alternative Fund Services (Cayman) Ltd. P.O. Box 852 GT, George Town, Grand Cayman Cayman Islands Tel: + 1 345 914 1000 Fax: + 1 345 914 4060 Legal Advisors : Walkers Walker House, George Town, Grand Cayman Cayman Islands

Fax : +230 483 8585 Investment Advisor : Vantage Investment Advisory Ltd. 43, Brook Street, London W1K 4HJ United Kingdom Tel : +44 20 7629 4224 Auditors : BDO (Cayman) P.O. Box 31118 2nd Floor, Building 3, Governors Square 23 Lime Tree Bay Avenue Grand Cayman, Cayman Islands Tel: + 1 345 943 8800 Fax: + 1 345 943 8801

Tel : +1 345 949 0100 Fax : +1 345 949 7886

Definitions The MSWI denotes the MSCI World Index including income. The Currency Benchmark denotes the Currency Benchmark mix as defined by the Directors in the Prospectus dated 6

January 2011. The Investment Benchmark denotes the Investment Benchmark as defined by the Directors in the Prospectus dated 6

January 2011. The Net Equity Exposure to a particular region is the sum of all the Fund’s equity investments in that region, less any

equity hedges including delta adjusted option positions entered into in that region. The Net Currency Exposure to a particular currency or currency block is the sum of all the Fund’s investments and cash

denominated in that currency or currency block, less any currency hedges including delta adjusted option positions entered into in that currency or currency block.

The Bid and Offer Prices and Net Asset Value of the Fund are calculated each week as of the close of business on Wednesday by the Administrator, MUFG Alternative Fund Services (Cayman) Ltd., and are available via the internet on www.vantagefunds.com.

BDO Cayman Ltd., a Cayman Islands company, is a member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms.

16

Tel: +1 (345) 943-8800 Fax: +1 (345) 943-8801 Email: [email protected] www.bdo.ky

PO Box 31118 2nd Floor – Building 3 Governors Square 23 Lime Tree Bay Avenue Grand Cayman KY1-1205 Cayman Islands

Independent Auditor’s Report

To the Board of Directors of Vantage Global Investment Fund Grand Cayman, Cayman Islands

Opinion

We have audited the financial statements of Vantage Global Investment Fund (the “Fund”), which comprise the statement of financial position as of December 31, 2016, and the statement of comprehensive income, statement of changes in net assets attributable to holders of redeemable participating shares and statement of cash flows for the year then ended, and the notes to the financial statements, including a summary of significant accounting policies.

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Fund as of December 31, 2016, and its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards (“IFRSs”).

Basis for Opinion

We conducted our audit in accordance with International Standards on Auditing (“ISAs”). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Fund in accordance with the International Ethics Standards Board for Accountants’ Code of Ethics for Professional Accountants (“IESBA Code”), and we have fulfilled our ethical responsibilities in accordance with the IESBA Code. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Responsibilities of the Directors for the Financial Statements

The directors are responsible for the preparation and fair presentation of the financial statements in accordance with IFRSs, and for such internal control as the directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, the directors are responsible for assessing the Fund’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Fund or to cease operations, or has no realistic alternative but to do so.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

17

Independent Auditor’s Report (continued)

Auditor’s Responsibilities for the Audit of the Financial Statements (continued)

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

• Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Fund’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Fund to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Other Information

The directors are responsible for the other information presented with the financial statements. The other information comprises the information included in the directors’ report, but does not include the financial statements and our auditor’s report thereon.

Our opinion on the financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Other Matter

This report has been prepared for and only for the Vantage Global Investment Fund and its directors in accordance with the terms of our engagement letter dated November 8, 2016 and for no other purpose. To the fullest extent permitted by law, we do not accept or assume any liability or duty of care for any other purpose or to any other person to whom this report is shown or into whose hands it may come save where expressly agreed by our prior consent in writing.

June 28, 2017

Annual report as of December 31, 2016 Vantage Global Investment Fund

The notes on pages 21 to 36 are an integral part of the financial statements.

18

Statement of Financial Position as at December 31

Note 2016 2015 $ $ Assets Current Assets Financial assets at fair value through profit or loss 150,385,885 121,492,821 (Cost: $154,976,803) (2015: $138,050,391) Loans and receivables Cash and deposit accounts 12,675,006 90,475,584 Margin accounts 7,548,380 16,637,889 Receivable on securities sales 1,132,557 247,483 Receivable on dividends 179,909 ‐ Interest receivable 13,708 ‐ Other assets and prepaid expenses 7,371 6,883 Total Assets 171,942,816 228,860,660 Equity

Founder shares 14 100 100 Total Equity 100 100 Liabilities Current Liabilities

Financial liabilities at fair value through profit or loss 3,119,936 1,495,203 (Proceeds: $1,458,056) (2015: $5,354,686) Financial liabilities measured at amortised cost Payable on securities purchased ‐ 2,302,419 Payable on redemptions 214,497 711,579 Fees payable 6 294,247 415,781 Total Liabilities 3,628,680 4,924,982

Net assets attributable to holders of Fund’s shares 168,314,036 223,935,578 Total Equity and Liabilities 171,942,816 228,860,660

Key Figures

2016 2015 Fund’s shares outstanding 375,284.88 504,178.93 Net asset value per Fund’s share in USD 448.50 444.16 Net assets attributable to holders of Fund’s shares 168,314,036 223,935,578

APPROVED ON BEHALF OF THE BOARD

Annual report as of December 31, 2016 Vantage Global Investment Fund

The notes on pages 21 to 36 are an integral part of the financial statements.

19

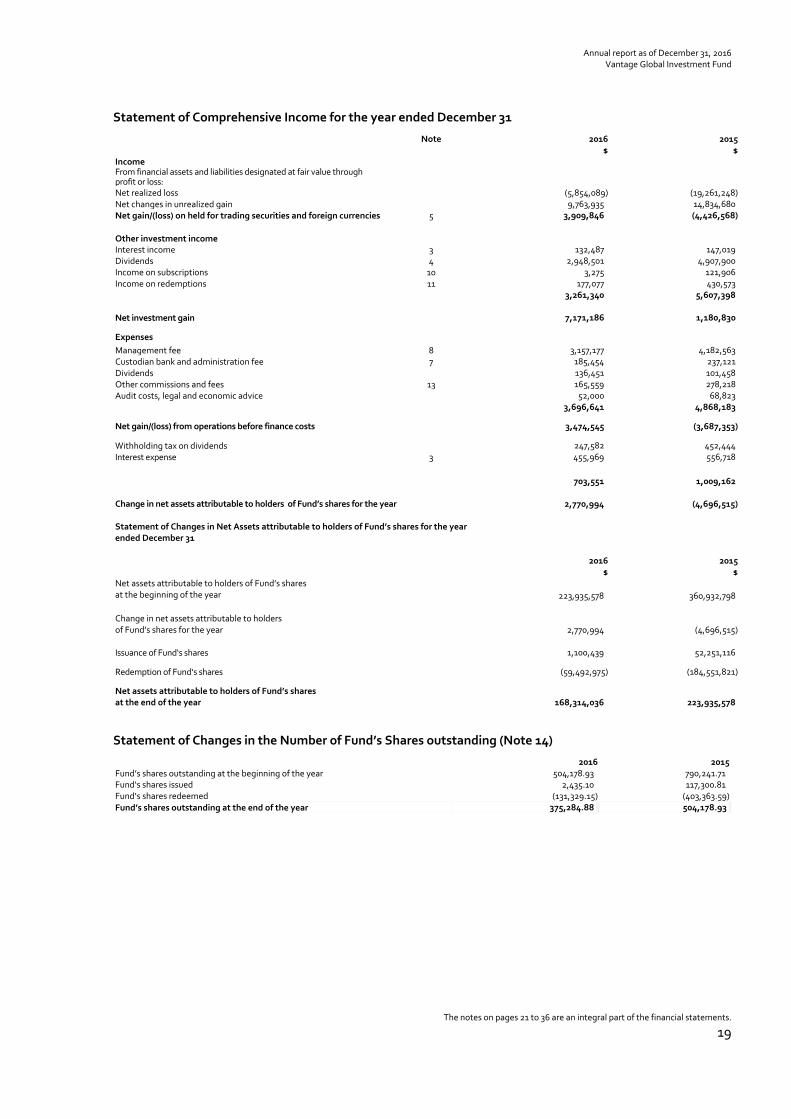

Statement of Comprehensive Income for the year ended December 31

Note 2016 2015 $ $

Income From financial assets and liabilities designated at fair value through profit or loss:

Net realized loss (5,854,089) (19,261,248) Net changes in unrealized gain 9,763,935 14,834,680 Net gain/(loss) on held for trading securities and foreign currencies 5 3,909,846 (4,426,568) Other investment income Interest income 3 132,487 147,019 Dividends 4 2,948,501 4,907,900 Income on subscriptions 10 3,275 121,906 Income on redemptions 11 177,077 430,573

3,261,340 5,607,398

Net investment gain 7,171,186 1,180,830

Expenses

Management fee 8 3,157,177 4,182,563 Custodian bank and administration fee 7 185,454 237,121 Dividends 136,451 101,458 Other commissions and fees 13 165,559 278,218 Audit costs, legal and economic advice 52,000 68,823 3,696,641 4,868,183

Net gain/(loss) from operations before finance costs 3,474,545 (3,687,353)

Withholding tax on dividends 247,582 452,444 Interest expense 3 455,969 556,718 703,551 1,009,162 Change in net assets attributable to holders of Fund’s shares for the year 2,770,994 (4,696,515) Statement of Changes in Net Assets attributable to holders of Fund’s shares for the year ended December 31 2016 2015

$ $ Net assets attributable to holders of Fund’s shares at the beginning of the year

223,935,578 360,932,798

Change in net assets attributable to holders of Fund’s shares for the year

2,770,994 (4,696,515)

Issuance of Fund‘s shares 1,100,439 52,251,116

Redemption of Fund‘s shares (59,492,975) (184,551,821)

Net assets attributable to holders of Fund’s shares at the end of the year

168,314,036 223,935,578

Statement of Changes in the Number of Fund’s Shares outstanding (Note 14)

2016 2015 Fund’s shares outstanding at the beginning of the year 504,178.93 790,241.71 Fund‘s shares issued 2,435.10 117,300.81 Fund‘s shares redeemed (131,329.15) (403,363.59) Fund’s shares outstanding at the end of the year 375,284.88 504,178.93

Annual report as of December 31, 2016 Vantage Global Investment Fund

The notes on pages 21 to 36 are an integral part of the financial statements.

20

Statement of Cash Flows for the year ended December 31

2016 2015 $ $ Cash Flows from Operating Activities Interest received 118,779 147,019 Dividends received 2,768,493 4,417,816 Interest paid (455,969) (556,718) Dividends paid (136,451) (103,522) Other income received 180,352 552,479 Payment of operating expenses (3,682,212) (5,009,038) Net payments from securities sold and purchased (20,939,372) 158,089,358 Realized gain on investments and options (4,696,830) (5,283,613) Realized loss on futures, forward foreign exchange contracts and foreign currency translation

(1,157,259) (13,977,635)

Net cash (used in)/ provided by operating activities (28,000,469) 138,276,146

Cash Flows from Financing Activities Proceeds from Fund’s shares issued 1,100,439 51,563,447 Payments for Fund’s shares redeemed (59,990,057) (184,183,112) Net cash used in financing activities (58,889,618) (132,619,665) Net (decrease)/ increase in cash and cash equivalents (86,890,087) 5,656,481 Cash and cash equivalents

Beginning of the year 107,113,473 101,456,992

End of the year 20,223,386 107,113,473

Notes to the Financial Statements

Annual report as of December 31, 2016 Vantage Global Investment Fund

21

Note 1 ‐ General

Vantage Global Investment Fund (the “Fund”) was incorporated on October 2, 1995 as an exempted company under the Companies Law (revised) of the Cayman Islands, and is regulated under The Mutual Funds Law (revised) of the Cayman Islands, as amended from time to time. The Fund’s registered office is located at MUFG Alternative Fund Services (Cayman) Ltd, P.O. Box 852 GT, 227 Elgin Avenue, George Town, Grand Cayman KY1‐1103, Cayman Islands.

The Fund is a single fund managed by Vantage Investment Management Limited (the “Manager”) which invests the assets of the Fund in a focused portfolio of shares, currencies and portfolio hedges.

MUFG Alternative Fund Services (Cayman) Limited serves as the administrator (the "Administrator") to the Fund. Note 2 ‐ Summary of significant accounting policies

The principal accounting policies applied in the preparation of these financial statements are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated.

a) Basis of preparation

The Fund's financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) issued by International Accounting Standards Board (“IASB”). The financial statements have been prepared under the historical‐cost convention, as modified by the revaluation of the financial assets and financial liabilities held at fair value through profit or loss.

Standards, amendments and interpretations that are effective from 1 January 2016 and beyond:

(i) Standards and amendments to existing standards effective 1 January 2016 There are no standards, interpretations or amendments to existing standards that are effective for the first time for the financial year beginning 1 January 2016 that have had a material impact on the Fund. (ii) New standards, amendments and interpretations effective after 1 January 2016 and have not been early adopted At the date of authorization of the financial statements there were a number of other Standards and Interpretations which were in issue but not yet effective. Management anticipates that the adoption of these Standards and Interpretations in future periods will have no material impact on the financial statements of the Fund.

b) Accounting currency

The accounting records as well as the financial statements of the Fund are kept in the United States (“US”) dollars. US dollar (“$”) is the functional and reporting currency of the Fund as subscriptions and redemptions are performed in US dollars.

c) Use of estimates

The preparation of financial statements in accordance with IFRS requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the year. Actual results could differ from those estimates and assumptions. d) Valuation principles

The Fund’s value is calculated each week, based on the valuation of its underlying assets and liabilities pertaining as of the close of business on each Wednesday or at such other time as the Administrator with the approval of the Directors shall determine (termed the “Valuation Day”). All subscriptions and redemptions are based on the Fund’s Net Asset Value per Share, determined by the Administrator at values pertaining as of the close of business on the Valuation Day. The Fund’s value is calculated by the Administrator on the first Business Day in the Cayman Islands after the Valuation Day (termed the “Calculation Day”). The Net Asset Value per Share is expressed in US dollars and is determined by dividing the net assets of the Fund by the number of Shares in issue on the Valuation Day, excluding any subscriptions or redemptions scheduled for that Valuation Day. The net assets of the Fund comprise the principal aggregate of all the investments owned or contracted to be purchased by the Fund at their closing prices in their markets as of the Valuation day, plus any cash, bills, accrued interest, or other property of any kind as defined from time to time by the Directors, from which are deducted the management, custodial and administrative expenses, the value of any investments contracted to be sold, the aggregate amount of any borrowings, any interest or other charges, or other liabilities of any kind as defined from time to time by the Directors.

e) Financial instruments

I. Classification The Fund classifies its investments in debt and equity securities, underlying fund and derivatives as financial assets and liabilities at fair value through profit or loss. Financial assets that are classified as loans and receivables include cash and deposit accounts, margin accounts, receivable on securities sales and receivable on dividends. Financial liabilities measured at amortized cost include fees payable, payable on securities purchases, payable on redemptions and payable on dividends.

Annual report as of December 31, 2016 Vantage Global Investment Fund

22

II. Recognition, derecognition and initial measurement

The Fund recognizes financial assets or liabilities on the date it commits to purchase or sell the instrument. From this date, any gains and losses arising from changes in fair value of the assets or liabilities are recognized in the statement of comprehensive income. Financial instruments categorized at fair value through profit or losses are recognized initially at cost. For financial assets acquired, cost is the fair value of the consideration given, while for the financial liabilities, cost is the fair value of the consideration received. Transaction costs for such instruments are recognized directly in the statement of comprehensive income. Financial assets classified as loans and receivables are recognized on the day that they are transferred to the Fund at fair value plus transaction costs that are directly attributable to their acquisition or issue.

Financial assets are derecognized when the rights to receive cash flows from the investments have expired or the Fund has transferred substantially all risks and rewards of ownership.

Financial liabilities, other than those as at fair value through the profit or loss, are recognized initially at fair value plus transaction costs that are directly attributable to their acquisition or issue. Financial liabilities arising from the Fund’s shares are carried at the redemption amount representing the investors’ right to a residual interest in the Fund’s assets. Financial liabilities are not recognized unless one of the parties has performed.

A financial liability is derecognized when the obligation specified in the contract is discharged, cancelled or expired.

III. Subsequent measurement

Subsequent to initial recognition, the Fund measures all financial instruments classified at fair value through profit or loss at fair value with changes in the fair value recognized in the statement of comprehensive income. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The fair value of financial assets and liabilities traded in active markets (such as publicly traded derivatives and trading securities) are based on quoted market prices at the close of trading on the reporting date. Prior to 1 January 2013, the quoted market price used for financial assets held by the Fund was the current bid price; the quoted market price for financial liabilities was the current asking price. The Fund adopted IFRS 13, ‘Fair value measurement’, from 1 January 2013; it changed its fair valuation input to utilise the last traded market price for both financial assets and financial liabilities where the last traded price falls within the bid‐ask spread. Financial assets classified as loans and receivables, and financial liabilities other than those as at fair value through the profit or loss, are measured at amortized cost.

IV. Unrealized gains and losses on subsequent measurement

Unrealized gains and losses arising from a change in the fair value of trading instruments during the year are recognized in the statement of comprehensive income.

In the case of any security which is listed or dealt in on more than one stock exchange, the Directors determine the stock exchange whose quotations shall be used in the determination of the value of such security.

In the case of any security for which no price quotations are available, the value thereof is determined from time to time in such manner as the Directors from time to time determine.

f) Conversion of foreign currencies

Foreign currency transactions are translated to US dollars at the foreign exchange rate ruling at the date of the transaction. Foreign currency assets and liabilities are translated to US dollars at the foreign exchange rate ruling at the statement of financial position date.

Foreign currency exchange differences arising from translation are included in the statement of comprehensive income.

Foreign currency exchange differences relating to financial assets and liabilities are included in the statement of comprehensive income within net gains from financial assets and liabilities.

g) Valuation of forward foreign exchange contracts

As part of the Fund’s investment strategy, the Fund enters into certain financial instruments including forward foreign exchange contracts. These forward foreign exchange contracts are initially recognized at fair value and subsequently re‐measured at their fair value.

The fair value of forward foreign exchange contracts is based upon the settlement prices from the recognized and regulated markets, with the resulting unrealized gain/(loss) recorded in the statement of comprehensive income.

Fair value estimates are made at a specific point in time, based on the market conditions and information about the financial instrument. These estimates are subjective in nature and involve uncertainties and matters of significant judgement. Hence, changes in assumptions could significantly affect the estimates.

Annual report as of December 31, 2016 Vantage Global Investment Fund

23

At December 31, 2016, the Fund was committed to the following amounts as a result of outstanding forward foreign exchange contracts:

Sold Currency Bought Currency Maturity

Date

Unrealized gain/(loss)

$

AUD1,830,195 USD1,361,692 03.31.2017 45,334

AUD3,900,370 USD2,886,957 03.31.2017 81,635

CAD900,000 USD687,053 03.31.2017 16,722

CHF1,633,513 EUR1,521,233 03.31.2017 (4,873)

CNH18,651,179 USD2,654,203 03.31.2017 39,196

CNH31,880,671 USD4,527,171 03.31.2017 57,311

CNY10,984,000 USD1,600,000 01,23.2017 34,056

USD3,170,728 DKK22,027,558 03.31.2017 (38,415)

DKK28,650,055 USD4,096,875 03.31.2017 22,844

EUR839,195 USD892,567 03.31.2017 5,803

EUR5,029,594 USD5,300,000 03.31.2017 (14,686)

NOK8,091,000 EUR941,741 03.31.2017 (27)

USD10,478,377 GBP8,291,141 03.31.2017 (223,521)

HKD98,899,870 USD12,740,020 03.31.2017 (14,835)

USD1,198,805 HKD9,300,000 03.31.2017 592

JPY280,000,000 USD2,542,448 03.31.2017 137,350

JPY2,093,687,162 USD18,169,305 03.31.2017 185,299

KRW4,165,619,313 USD3,562,993 03.31.2017 113,234

KRW1,322,504,061 USD1,131,181 06.30.2017 35,032

USD1,110,000 KRW1,322,504,061 06.30.2017 (13,851)

SGD1,240,549 USD863,653 03.31.2017 6,567

USD2,101,998 SGD3,008,793 03.31.2017 (23,245)

TWD476,531,289 USD15,012,062 03.31.2017 309,298

ZAR101,046,469 USD7,189,345 03.31.2017 (42,931)

ZAR26,658,183 USD1,866,200 03.31.2017 (41,826)

At December 31, 2015, the Fund was committed to the following amounts as a result of outstanding forward foreign exchange contracts:

Sold Currency Bought Currency Maturity

Date

Unrealized gain/(loss)

$

USD2,230,000 CNY14,706,119 08.18.2016 (44,994)

USD3,299,491 KRW3,903,627,750 03.30.2016 16,409

USD1,200,000 MYR5,211,840 03.30.2016 7,104

USD570,441 SEK4,948,793 03.30.2016 17,374

USD2,300,000 SGD3,256,487 03.03.2016 (9,080)

USD2,300,000 SGD3,256,904 03.03.2016 (8,787)

USD2,300,000 TWD75,508,972 03.03.2016 (14,247)

USD2,400,000 TWD78,912,000 03.30.2016 (10,981)

USD1,000,000 ZAR15,158,335 03.03.2016 (31,712)

CAD900,000 USD646,113 06.30.2016 (4,699)

CNH12,564,858 USD1,900,000 11.28.2016 45,842

CNH31,880,671 USD4,816,607 03.30.2016 24,627

CNH6,086,321 USD900,000 11.28.2016 1,860

CNY14,671,677 USD2,230,000 08.18.2016 50,111

CNY34,442 USD5,117 08.18.2016 ‐

DKK4,245,877 USD621,289 03.30.2016 1,627

EUR2,098,246 USD2,300,000 06.30.2016 8,559

EUR11,100,000 USD12,130,746 06.30.2016 8,717

GBP1,070,793 USD1,600,000 03.30.2016 21,842

JPY1,530,000,000 USD12,692,777 06.30.2016 (105,453)

JPY133,719,850 USD1,100,000 03.30.2016 (15,009)

KRW1,063,312,380 USD900,000 03.30.2016 (3,221)

KRW15,988,801,674 USD13,520,042 03.30.2016 (61,494)

KRW2,728,175,360 USD2,300,000 03.30.2016 (17,423)

MYR5,211,810 USD1,202,263 03.30.2016 (4,834)

SGD1,774,970 USD1,250,000 03.03.2016 1,319

SGD1,771,108 USD1,250,000 03.03.2016 4,036

SGD1,657,352 USD1,170,000 03.03.2016 4,063

SGD1,309,961 USD924,409 03.30.2016 3,592

TWD405,140,779 USD12,383,946 03.30.2016 118,522

TWD75,864,240 USD2,300,000 03.30.2016 3,250

TWD59,526,000 USD1,800,000 03.03.2016 (1,928)

ZAR9,274,936 USD630,665 03.30.2016 41,007

ZAR15,139,100 USD1,000,000 03.30.2016 37,525

ZAR13,693,707 USD900,000 03.30.2016 29,416

ZAR15,158,335 USD989,036 03.03.2016 20,749

ZAR47,283,045 USD3,069,414 03.30.2016 63,372

ZAR7,747,698 USD500,000 03.30.2016 7,437

h) Valuation of financial futures contracts

Derivative financial instruments including financial futures contracts are initially recognized in the statement of financial position at fair value and subsequently re‐measured at their fair value. Fair values are obtained from quoted market prices. All financial futures contracts are carried in current assets when amounts are receivable by the Fund and in current liabilities when amounts are payable by the Fund. Changes in fair values of financial futures contracts are included in the statement of comprehensive income.

Realized profits and losses are determined following the FIFO‐Method (First In First Out). i) Dividend and interest income

Dividend income from financial assets at fair value through profit or loss is recognized in the statement of comprehensive income within dividend income when the Fund’s right to receive payment is established.

Interest income is recognized in the statement of comprehensive income for all interest bearing instruments using the effective yield method. Interest income may include coupons earned on fixed income investment and trading securities and accrued discount on treasury bonds, commercial papers, floating rate notes and other discounted instruments.

j) Cash and cash equivalents

Cash comprises cash on hand and demand deposits. Cash equivalents are short term, highly liquid investments with maturities of three months or less when purchased.

For the purpose of the statement of cash flows, cash and cash equivalents includes cash and deposit accounts and margin accounts.

k) Margin accounts and receivable on securities sales

This account represents cash positions held with the broker as margin to carry its exchange traded future contracts’ transactions. These cash positions and/or securities held by the broker serve as collateral for any amounts due to broker. The Fund is subject to credit risk if the broker is unable to repay both initial and maintenance margin balances due in their custody. The cash balances and/or securities also serve as collateral for potential defaults of the Fund. l) Fees and commission expense

Fees and commission expense are recognized in the profit or loss as the related services are performed.

m) Taxation

Under current legislation in the Cayman Islands there is no income, estate, corporate, capital gain or other taxes payable by the Fund.

The Fund may be subject to foreign withholding tax on certain interest, dividends and capital gains.

Annual report as of December 31, 2016 Vantage Global Investment Fund

24

n) Offsetting financial instruments

Financial assets and liabilities are offset and the net amount reported in the statement of financial position where the Fund currently has a legally enforceable right to set‐off the recognised amounts and there is an intention to settle on a net basis or realise the asset and settle the liability simultaneously. Note 3 ‐ Interest income and expenses

Interest income and expense arises from:

2016 2015 $ $

Interest income for financial assets that are at fair value through profit or loss and at amortized cost 132,487 147,019

Total interest income 132,487 147,019

Interest expense for financial liabilities that are at fair value through profit or loss and at amortized cost 455,969 556,718

Total interest expense 455,969 556,718

Note 4 ‐ Dividend income

2016 2015 $ $ Designated at fair value through profit or loss upon initial recognition

‐ Equity securities 2,948,501 4,907,900

Total dividend income 2,948,501 4,907,900

Note 5 ‐ Net gain/(loss) on held for trading securities and foreign currencies

Net gain on held for trading securities and foreign currencies can be summarized as follows:

2016 $

2015 $

Realized loss on securities (4,696,830) (12,685,455) Realized loss on currencies (1,157,259) (6,575,793)

Net realized loss (5,854,089) (19,261,248)

Net change in unrealized gain on securities 5,977,723 9,424,947 Net change in unrealized gain on currencies 3,786,212 5,409,733

Net change in unrealized gain 9,763,935 14,834,680

Net gain (loss) on held for trading securities and foreign currencies 3,909,846 (4,426,568)

Note 6 ‐ Fees payable

The detail of fees payable is as follows:

2016 2015

$ $

Management fees 220,502 342,227 Administration fees 38,245 42,054 Audit fee 31,500 31,500 Other fees 4,000 ‐

TOTAL 294,247 415,781

Note 7 ‐ Administrator's fee

The Administrator receives their fees on the basis of eight basis points (0.08%) per annum of the weekly average net assets of the Fund.

Note 8 ‐ Manager’s and Performance fee

The Manager’s fee is designed to align the interest of the Manager and those of investors in the Fund, who seek returns exceeding those attainable from investing in risk free securities without exposing their investment to the volatility normally associated with investing in global equities. The Manager’s Fee is determined by the Administrator each week on the Calculation Day and charged to the Fund. It consists of: ‐ a base fee of 1.5% per annum of the weekly net asset value; ‐ a Performance fee of 15% of the incremental value added. The incremental value added is determined as of each valuation day as follows: The value added return is calculated for the period since the prior valuation day as the difference between the return of the Fund’s shares after deducting all expenses other than the Performance fee, and the return of the risk free securities in the currency benchmark mix. The cumulative value added return is calculated as the accumulation of the weekly value added returns since the inception of the Fund. The incremental value added return is calculated as the ratio difference between the cumulative value added return on the current valuation day and the cumulative value added return at which the last Performance Fee was charged within the previous 52‐week period. The incremental value added is calculated as the incremental value added return multiplied by the net asset value of the Fund after all subscriptions and redemptions on the prior valuation day. The incremental value added is taken as zero if the incremental value added return is negative.

Note 9 ‐ Dividend distribution policy

The Fund does not anticipate paying dividends, other than if required to do so in order to maintain the Reporting Fund Status designated by United Kingdom HM Revenue & Customs (“UK HMRC”) or a similarly advantageous tax classification in another jurisdiction important to the Fund’s shareholders. Absent such a requirement, the Fund will retain all dividends, interest and other income derived from its assets, and this will be reflected in the Net Asset Value of the Fund.

For the year ended December 31, 2016, the Fund did not declare dividends (2015: $Nil).

Annual report as of December 31, 2016 Vantage Global Investment Fund

25

Note 10 ‐ Income on subscriptions

The income from subscriptions corresponds to the difference between the issue price and the net asset value per share. The issue price is rounded up to the next monetary unit. The transaction cost which is determined with reference to the underlying investment portfolio is currently set at 0.3% of the net asset value per share.

Note 11 ‐ Income on redemptions

The income from redemptions corresponds to the difference between the redemption price and the net asset value per share. The redemption price is rounded up to the next monetary unit. The transaction cost which is determined with reference to the underlying investment portfolio is currently set at 0.3% of the net asset value per share.

Note 12 ‐ Risks associated with the investments and financial instruments held by the Fund

Associated risks: The Fund’s investment activities expose it to the various types of risk which are associated with the financial instruments and markets in which it invests. The following summary is not intended to be a comprehensive summary of all risks and investors should refer to the prospectus for a more detailed discussion of the risks inherent in investing in the Fund.

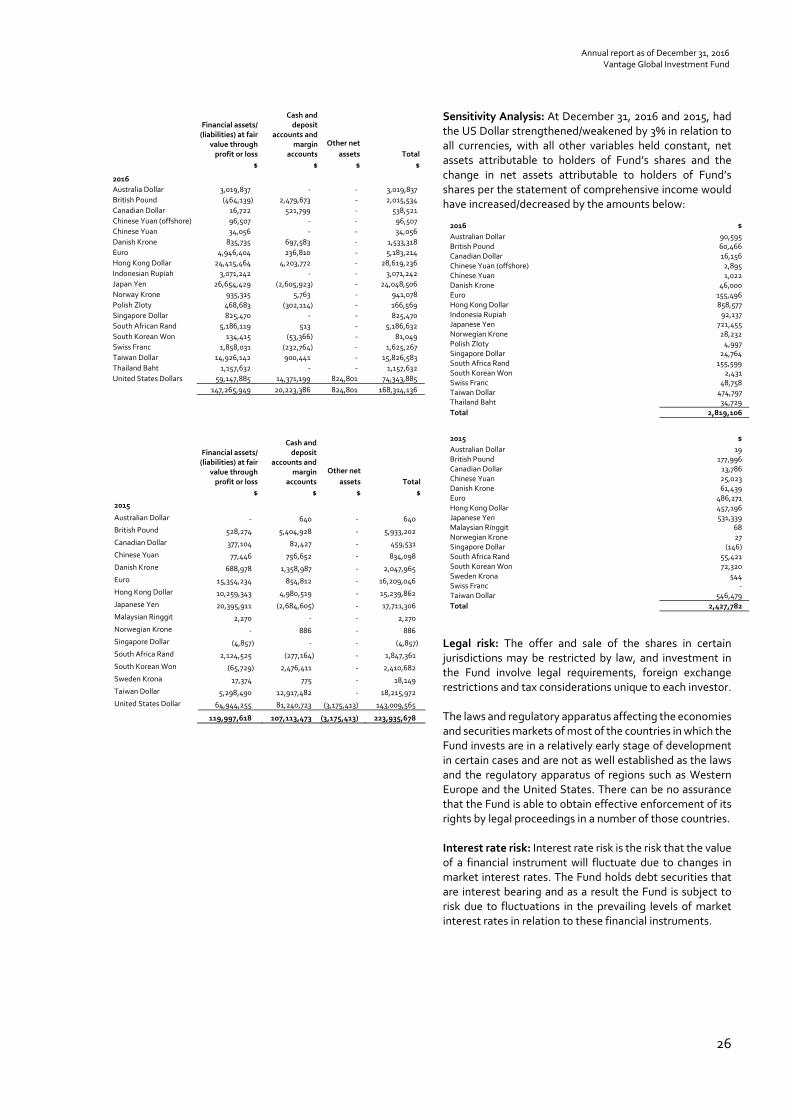

Currency and exchange risk: Currency exposures significantly influence global investment returns. Traditionally, investment managers consider the forecast combined return of an equity in its local currency, and the return of that currency relative to a Fund’s base currency, when evaluating an investment in an equity. The Manager does not follow this traditional approach, but rather selects equities with forecast real returns in their local currencies considerably in excess of the real returns generally forecast for global equities. Should the Manager believe the future value of the associated currencies to be vulnerable, they are then hedged into currencies whose future values are expected to strengthen. Very often attractive equity investment opportunities are available in countries with vulnerable currencies. Hence the Fund’s currency deployment will frequently differ significantly from its deployment of equities by country. In attempting to meet the needs of disparate global investors who have differing domestic or reference currencies, and who recognize the need to generate returns not solely in their domestic currencies, but rather in a mix of the rest of the World’s currencies, the Directors have defined a Currency Benchmark. The weightings of the constituent currencies in this Currency Benchmark approximate the proportion of global trade made up by the countries in each currency block. These weightings may be altered from time to time by the Directors to reflect large shifts in the relative sizes of each currency block’s significance in the MS World Index (MSWI) and in global trade.

The weightings of each currency block in the Currency Benchmark are as follows:

US Dollar 40%

Euro 20%

UK pound 10%

Japanese Yen 10%

Singapore dollar 10%

Swiss Franc 5%

Canadian dollar 2.5%

Australian dollar 2.5%

The Currency Benchmark represents a “neutral currency position” for the Fund. The Fund’s currency deployment will deviate from this “neutral currency position” to the extent that the Manager actively chooses to overweight or underweight certain currencies and/or currency blocks. If the Manager is neutral on the relative attractiveness of all currencies, the Fund’s currency deployment will be in‐line with the weightings in the Currency Benchmark. It follows that the Fund’s performance is most appropriately measured in terms of return and risk in Currency Benchmark units, and not in US dollars. The Manager may seek to hedge against a decline in the value of the Fund’s investments resulting from currency devaluations or fluctuations but only when suitable hedging instruments are available on a timely basis and on acceptable terms. There is no assurance that any hedging transactions engaged in by the Fund will be successful in protecting against currency devaluations or fluctuations. The Fund is valued in US dollar and fluctuates in accordance with changes in the foreign exchange rates between the US dollar and other relevant currencies. Shareholders’ investments in the Fund and cash distributions from the Fund are made in US dollars, and currency conversions are required prior to the Fund making portfolio investments and distributing any income and realization proceeds from the Fund investments. There can be no assurance that fluctuations in exchange rates do not have an adverse effect on the net asset value, on the funds available for investment after conversion of the US dollar proceeds of the Placing or on the distributions received by shareholders in US dollars after conversion of the income and realization proceeds from the Fund’s investments (which are not necessarily denominated in US dollars).

Annual report as of December 31, 2016 Vantage Global Investment Fund

26

Financial assets/ (liabilities) at fair

value through profit or loss

$

Cash and deposit

accounts and margin

accounts

$

Other net

assets

$

Total

$

2016

Australia Dollar 3,019,837 ‐ ‐ 3,019,837

British Pound (464,139) 2,479,673 ‐ 2,015,534

Canadian Dollar 16,722 521,799 ‐ 538,521

Chinese Yuan (offshore) 96,507 ‐ ‐ 96,507

Chinese Yuan 34,056 ‐ ‐ 34,056

Danish Krone 835,735 697,583 ‐ 1,533,318

Euro 4,946,404 236,810 ‐ 5,183,214

Hong Kong Dollar 24,415,464 4,203,772 ‐ 28,619,236

Indonesian Rupiah 3,071,242 ‐ ‐ 3,071,242

Japan Yen 26,654,429 (2,605,923) ‐ 24,048,506

Norway Krone 935,315 5,763 ‐ 941,078

Polish Zloty 468,683 (302,114) ‐ 166,569

Singapore Dollar 825,470 ‐ ‐ 825,470

South African Rand 5,186,119 513 ‐ 5,186,632

South Korean Won 134,415 (53,366) ‐ 81,049

Swiss Franc 1,858,031 (232,764) ‐ 1,625,267

Taiwan Dollar 14,926,142 900,441 ‐ 15,826,583

Thailand Baht 1,157,632 ‐ ‐ 1,157,632

United States Dollars 59,147,885 14,371,199 824,801 74,343,885

147,265,949 20,223,386 824,801 168,314,136

Financial assets/ (liabilities) at fair

value through profit or loss

$

Cash and deposit

accounts and margin

accounts

$

Other net

assets

$

Total

$

2015

Australian Dollar ‐ 640 ‐ 640

British Pound 528,274 5,404,928 ‐ 5,933,202

Canadian Dollar 377,104 82,427 ‐ 459,531

Chinese Yuan 77,446 756,652 ‐ 834,098

Danish Krone 688,978 1,358,987 ‐ 2,047,965

Euro 15,354,234 854,812 ‐ 16,209,046

Hong Kong Dollar 10,259,343 4,980,519 ‐ 15,239,862

Japanese Yen 20,395,911 (2,684,605) ‐ 17,711,306

Malaysian Ringgit 2,270 ‐ ‐ 2,270

Norwegian Krone ‐ 886 ‐ 886

Singapore Dollar (4,857) ‐ ‐ (4,857)

South Africa Rand 2,124,525 (277,164) ‐ 1,847,361

South Korean Won (65,729) 2,476,411 ‐ 2,410,682

Sweden Krona 17,374 775 ‐ 18,149

Taiwan Dollar 5,298,490 12,917,482 ‐ 18,215,972

United States Dollar 64,944,255 81,240,723 (3,175,413) 143,009,565

119,997,618 107,113,473 (3,175,413) 223,935,678

Sensitivity Analysis: At December 31, 2016 and 2015, had the US Dollar strengthened/weakened by 3% in relation to all currencies, with all other variables held constant, net assets attributable to holders of Fund’s shares and the change in net assets attributable to holders of Fund’s shares per the statement of comprehensive income would have increased/decreased by the amounts below:

2016 $

Australian Dollar 90,595 British Pound 60,466 Canadian Dollar 16,156 Chinese Yuan (offshore) 2,895 Chinese Yuan 1,022 Danish Krone 46,000 Euro 155,496 Hong Kong Dollar 858,577 Indonesia Rupiah 92,137 Japanese Yen 721,455 Norwegian Krone 28,232 Polish Zloty 4,997 Singapore Dollar 24,764 South Africa Rand 155,599 South Korean Won 2,431 Swiss Franc 48,758 Taiwan Dollar 474,797 Thailand Baht 34,729

Total 2,819,106

2015 $

Australian Dollar 19 British Pound 177,996 Canadian Dollar 13,786 Chinese Yuan 25,023 Danish Krone 61,439 Euro 486,271 Hong Kong Dollar 457,196 Japanese Yen 531,339 Malaysian Ringgit 68 Norwegian Krone 27 Singapore Dollar (146) South Africa Rand 55,421 South Korean Won 72,320 Sweden Krona 544 Swiss Franc ‐ Taiwan Dollar 546,479

Total 2,427,782

Legal risk: The offer and sale of the shares in certain jurisdictions may be restricted by law, and investment in the Fund involve legal requirements, foreign exchange restrictions and tax considerations unique to each investor. The laws and regulatory apparatus affecting the economies and securities markets of most of the countries in which the Fund invests are in a relatively early stage of development in certain cases and are not as well established as the laws and the regulatory apparatus of regions such as Western Europe and the United States. There can be no assurance that the Fund is able to obtain effective enforcement of its rights by legal proceedings in a number of those countries. Interest rate risk: Interest rate risk is the risk that the value of a financial instrument will fluctuate due to changes in market interest rates. The Fund holds debt securities that are interest bearing and as a result the Fund is subject to risk due to fluctuations in the prevailing levels of market interest rates in relation to these financial instruments.

Annual report as of December 31, 2016 Vantage Global Investment Fund

27

The following table details the Funds exposure to interest rate risk:

2016 Less than

1 year More than

1year Non‐interest

bearing Total

$ $ $ $

Assets

Financial assets at fair value through profit or loss ‐ ‐ 150,385,885 150,385,885 Cash and deposit accounts 12,675,006 ‐ ‐ 12,675,006

Margin accounts 7,548,380 ‐ ‐ 7,548,380 Receivable on securities sales ‐ ‐ 1,132,557 1,132,557

Receivable on dividends ‐ ‐ 179,909 179,909

Interest receivable ‐ ‐ 13,708 13,708 Other assets and prepaid expenses ‐ ‐ 7,371 7,371

Total assets 20,223,386 ‐ 151,719,430 171,942,816

Liabilities

Financial liabilities at fair value through profit or loss ‐ ‐ (3,119,936) (3,119,936)

Payable on redemptions ‐ ‐ (214,497) (214,497)