vanguard financial education series | estate … financial education series® | estate planning how...

TRANSCRIPT

V a n g u a r d F i n a n c i a l E d u c a t i o n S E r i E S® | E S t a t E p l a n n i n g

How to create an estate plan that will help your family

People don’t like to think about their own demise. Perhaps that’s why most Americans lack a will.

Yet the absence of clear direction about who should inherit your money and possessions—or even who should raise your children—could cause no end of heartache for your family.

A well-made estate plan would be a wonderful gift to the people who love and depend on you.

Identify your goals

A well-made estate plan addresses both personal and financial issues for your family.

Personal Financial

Make your health-care preferences clear should you be unable to communicate.

Provide for the support of a surviving spouse, children, or partner.

Organize your affairs to make the transition easier on your survivors.

Distribute family heirlooms and valuable assets according to your wishes.

Name the guardian whom you wish to raise your minor children.

Minimize the taxes and expenses associated with the distribution of your assets.

Maintain your privacy by avoiding probate, the court-supervised distribution of an estate.

Provide for the orderly transition of a business, such as a family farm.

Estate planning > 3

To begin, identify what you hope to achieve. These objectives will help steer the estate-planning process.

Do you want to make sure your spouse and children can maintain their current standard of living? Often that means analyzing your life insurance coverage.

Do you want to leave an inheritance to your children from a previous marriage while also supporting your current spouse? In that case, you may need a trust to balance everyone’s interests.

Do you want to avoid estate taxes? Then you may need a gifting strategy to reduce the value of your estate.

Common goals of estate planning What are your goals?

Provide for a spouse. 1.

Support minor children. 2.

Provide for a special-needs family member. 3.

Avoid probate. 4.

Pass on a family business. 5.

Help with grandchildren’s education. 6.

Pass on a vacation home. 7.

Make a charitable bequest. 8.

4 < Financial Education Series

Have your will made

A will is a legally enforceable document that expresses your wishes for the distribution of your assets. Requirements vary by state, but in general a will must be:

• In writing (handwritten or typed), except under exceptional circumstances.

• Signed by the person whose will it is.

• Witnessed by two (or, in some states, three) people who saw the will signed.

To be sure that your estate plan meets the needs of your family and will be legally enforceable, you should seek legal advice.

Consulting an estate attorney is especially important if you or your family has a large estate or owns a small business, has a special-needs child, or has children from a prior marriage. If you already have a will, review it to make sure it is current. Important life events, such as a birth, marriage, adoption, or divorce may mean your will needs revision.

If you don’t have a lawyer, ask friends to recommend one or get a referral from your local bar association.

If you die without a will, legally assets would be divided according to the formula established by the laws of your state.

Your state may require that your property be divided among your spouse, parents, and children. If your children are minors, their share might have to be supervised by a court-appointed guardian until they reach adulthood.

It’s far better that you control the disposition of your assets. If you do not have a will, don’t put off creating one. Put it on your must-do list.

Estate planning > 5

Name an executor, guardian, and trustee

Identify the people who will have important responsibilities under your will. Typically these will include:

• an executor. This person will handle the settling of your estate, from cataloging your assets, paying your final bills, filing an estate-tax return, to distributing your property as you instructed.

• a guardian. If you have minor children or adult family members who require supervision, you’ll name this person to raise them or take care of their affairs.

• a trustee. If, under your will, you create a trust for tax planning purposes, or because a benefi-ciary needs professional money management, or for any other reason, this person or institution would manage and distribute the assets of the trust according to the terms of the trust.

Look for people whose competence and integrity you can rely on. An executor can be a longtime trusted friend, a grown child, or a financial institution that has an estate or trust department.

Because an executor has many details to attend to, it would be easier if you chose someone who lives nearby rather than someone who would have to travel a long distance to get the work done.

If you name a guardian for your minor children, make sure you’re comfortable with his or her parenting style.

Your trustee should be someone who has the skill to manage assets and also be sensitive to the needs of the trust beneficiary. A trust may have a long life, so the trustee should be available to serve in this capacity potentially for many years.

Make sure the people you choose are willing to serve in the capacity you’ve identified. These roles can entail a good deal of time and effort for which they may not be paid.

Finally, consider naming successors to each of the persons you choose, just in case any of your first choices cannot carry out the duties of executor, guardian, or trustee.

6 < Financial Education Series

Review your beneficiaries

The money in your employer-sponsored retirement plan will go to whomever you named as you beneficiary. You may have made your beneficiary designation during your first week at work. It’s important to check your selections again when you draw up your estate plan to make sure the beneficiaries you named are still appropriate.

You should be able to check whom you’ve named by logging on to your account at vanguard.com, calling Vanguard at 800‑523‑1188, or contacting your benefits office.

Having the wrong beneficiary named can be a costly mistake, as this hypothetical example shows: Beverly divorced John in 1997. John never remarried and willed his entire estate to his brother Fred. But John never removed Beverly as the beneficiary of his 401(k) account. When John died, Beverly inherited John’s retirement account. The beneficiary form, not his will, determined who received his 401(k) account.

Other assets that pass by contract to whomever you’ve named as your beneficiary include IRAs, life insurance contracts, and annuities. It’s a good practice to review these accounts periodically to make sure you still have the right beneficiaries named.

See how your property is titled

When you’re planning your estate, it’s important to understand how you own each asset today. That’s because the way your assets pass can depend on several factors, including the type of asset, how the asset is titled, and federal and state law.

Examine the deed to your home. If you own it alone, it would pass by the terms of your will. But if you own it jointly, it might pass automatically by title to your co-owner (in the case of joint tenants with rights of survivorship) or to the person you name in your will (in the case of tenants in common).

Example: In his will, Joe left his share of a family vacation cabin to his son Jared. But he failed to examine how the cabin was titled. Joe owned the cabin in joint tenancy with his brother Bill. Under joint tenancy rules, Joe’s ownership passed automatically to Bill. The title superseded Joe’s will. Jared will not inherit a share in the cabin from his father.

In addition to your house deed, examine how your car and checking, savings, and investment accounts are titled. Be prepared to discuss all this with your attorney as part of the estate planning process.

Finally, if you keep vital papers in a safe deposit box, see who can access it in your absence. You may want your spouse or executor to be able to open it without a court order.

8 < Financial Education Series

Will your estate be taxed?

Your executor will have to value your estate and file a tax return.

Everything you own will be counted in the value of your estate, including life insurance payouts, your home, retirement plan accounts, automobiles, IRAs, and personal possessions.

Under federal estate-tax law, in 2013 you can pass $5.25 million tax-free to your heirs. Married

couples can pass on as much as $10.5 million if both use their federal estate tax exemptions. These exemption amounts will automatically increase annually by the rate of inflation.

Furthermore, your estate won’t be taxed on assets that pass to your spouse, regardless of value, if your spouse is a U.S. citizen. The amount you can pass estate tax-free to a spouse who is not a U.S. citizen is limited.

Federal estate, gift, and generation-skipping tax exemptions for 2013

Federal estate-tax exemption $5.25 million

Generation-skipping tax exemption* $5.25 million

Gift-tax exemption** $5.25 million

Maximum tax rate for estate, generation-skipping, and gift taxes combined 40%

*Wealthy families once avoided paying estate tax twice on the same asset by leaving property to grandchildren rather than children. To close this loophole, the federal government created the generation-skipping tax. This tax is imposed at the highest federal tax rate in addition to any estate or gift tax owed on assets left or given to children.

**The federal government taxes gifts of property between people whether the giver is alive (the gift tax) or dead (the estate tax). The tax rate is progressive, meaning that the higher the amount of the gift, the higher the tax rate.

Estate planning > 9

Estimate the value of your estate

Use the “Your assets” table on the next page to estimate the total value of your assets.

Your taxable estate consists of the value of everything you own, minus your debts and final expenses.

List the fair market value of all your assets, remembering that the fair market value often differs from the purchase price. You can find the value of most investments online. To find the value of your residence, see how much comparable properties in your neighborhood have sold for recently.

If it appears that the taxable value of your estate could exceed the estate tax exemption, tell your lawyer. He or she can build tax-reduction strategies into your estate plan. For example, you might reduce the value of your estate by making annual tax-free gifts of up to $14,000 to each of your children, or by paying for your grandchildren’s educations.

Another common way to reduce estate taxes is to have property pass to a trust designed to take full advantage of the federal estate tax exemption. These are commonly called bypass or credit shelter trusts. These types of trusts can provide for a spouse and other beneficiaries while avoiding federal estate tax on the assets passing in the trust.

Note: The state where you live may tax your estate, inheritances, or both. Your lawyer should be familiar with your state’s laws.

10 < Financial Education Series

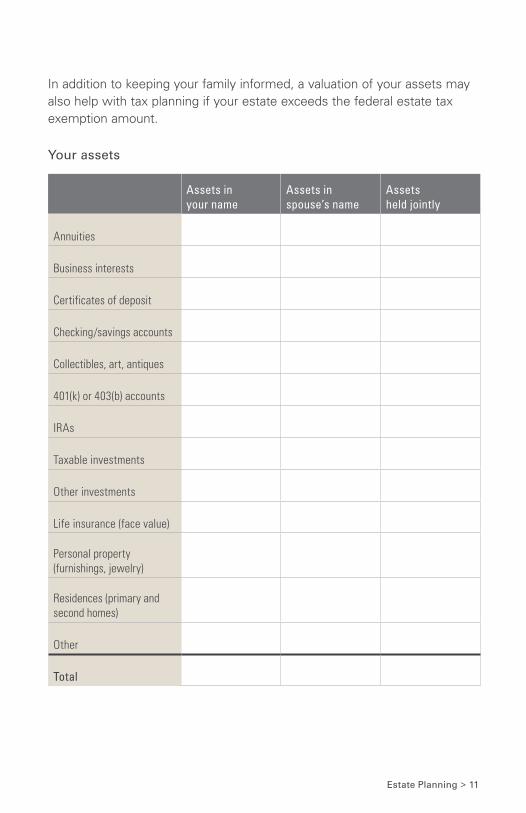

In addition to keeping your family informed, a valuation of your assets may also help with tax planning if your estate exceeds the federal estate tax exemption amount.

Your assets

Assets in your name

Assets in spouse’s name

Assets held jointly

Annuities

Business interests

Certificates of deposit

Checking/savings accounts

Collectibles, art, antiques

401(k) or 403(b) accounts

IRAs

Taxable investments

Other investments

Life insurance (face value)

Personal property (furnishings, jewelry)

Residences (primary and second homes)

Other

Total

Estate planning > 11

Make your health care wishes known

You can make your medical-care wishes known by preparing an advance medical directive consisting of a living will and a durable power of attorney for health care.

A living will is a document that spells out the health care interventions you do or do not want administered should you become unable to make

your wishes known. Hospitals frequently ask adult patients to fill out a living will upon admission.

You should also consider creating a durable power of attorney for health care. This legal document also makes your health care wishes known, but unlike a living will, appoints someone to make medical decisions on your behalf if you cannot make your wishes known.

12 < Financial Education Series

This person does not have to be a lawyer. A spouse or other close family member whom you trust implicitly to honor your wishes would be a good choice.

durable power of attorney

In a similar vein, you can appoint someone to look after your assets should you become too ill to take care of your affairs. A durable power of attorney for property is a legal document that authorizes someone of your choosing to manage your financial affairs if you become incapacitated.

An agent’s authority to act on your behalf ends at your death. Think carefully about whom you give this power to as it gives him or her the right to control your property. Again, someone you trust to honor your wishes would make a good choice for this role.

Consider providing a copy of your advance medical directive to your primary physician so it can be kept with your medical records.

Estate planning > 13

Your action plan

We’ve broken estate planning down into seven steps. As you finish each task, record the date it was completed. Aim to finish the list within six months.

You don’t have to follow this list in order. For example, you could review your beneficiary designations today.

The best advice is to work through your estate plan one step at a time. Try not to give up halfway through. Remember, your family is depending on you.

Although there is no substitute for working with qualified legal counsel, you can find additional tools and information at vanguard.com/planyourestate.

Identify your goals (pages 3–4).

Have your will made (page 5).

Name an executor, guardian, or trustee (page 6).

Review your beneficiary designations (page 7).

See how your property is titled (page 8).

Estimate the value of your estate (visit vanguard.com/estateassets).

Make your health care wishes known (pages 12–13).

Organize your important papers (visit vanguard.com/estatedocuments).

Create a list of your important contacts (visit vanguard.com/estatecontacts).

14 < Financial Education Series

© 2013 The Vanguard Group Inc. All rights reserved.

BBBBFZWM 032013

Connect with Vanguard®

retirementplans.vanguard.com > 800-523-1188

institutional investor group

P.O. Box 2900 Valley Forge, PA 19482-2900