valuations: what is happening and does it matter?

TRANSCRIPT

Valuations: What is happening, and does it

matter?Talia Goldberg & Jeremy Levine (Feb 2015)

2

For the Amusement Park Goers

3

For the Newtonian Physicists

4

For the Park Goers

ENTREPRENEURS

5

Quantitative Easing Means Easy Money

“So have you sent a note of thanks yet to Ben Bernanke and Janet Yellen? For all of your hard work and delightful intelligence, they arguably have had as much to do with your fund's success as you have.”

– Dan Primack (2/19/2015)

6

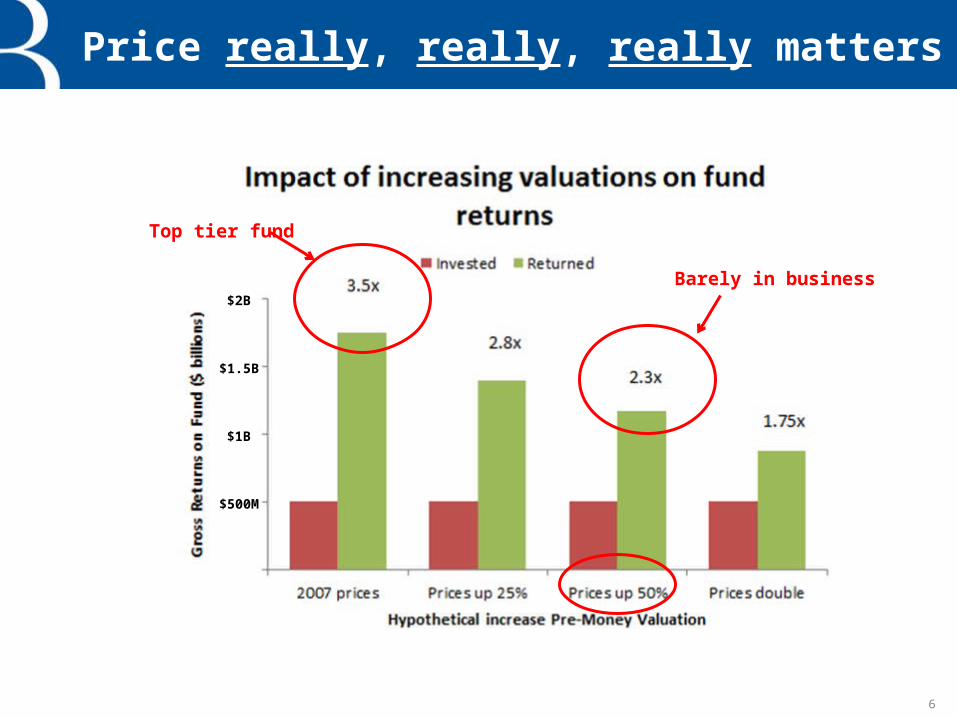

Price really, really, really matters

Top tier fund

Barely in business

$500M

$1B

$1.5B

$2B

7

What Did We Do?

• Looked at 4 public market segments relevant to most of our investing:1. Software as a Service2. Marketplaces3. Consumer Internet 4. E-Commerce

• Collected monthly valuation multiple and growth data for each company from 1999 (or first year of public listing) through February 2015

• Sanitized the data1. Excluded companies with negative EBITDA from all

charts with EBITDA multiples (only in the period of negative EBITDA)

2. Each sub segment has a minimum sample size of 5 companies

3. LTM EBITDA excludes stock based compensation expense

8

We are nowhere close to bubble madness (phew!)

-

20.0x

40.0x

60.0x

80.0x

100.0x

120.0x

140.0x

-

100.0x

200.0x

300.0x

400.0x

500.0x

600.0x

700.0x

1/25

/199

9

1/25

/200

0

1/25

/200

1

1/25

/200

2

1/25

/200

3

1/25

/200

4

1/25

/200

5

1/25

/200

6

1/25

/200

7

1/25

/200

8

1/25

/200

9

1/25

/201

0

1/25

/201

1

1/25

/201

2

1/25

/201

3

1/25

/201

4

1/25

/201

5

Med

ian

Reve

nue

mul

tiple

Med

ian

EBIT

DA

mul

tiple

Consumer Internet Multiples

EBITDA multiple Revenue Multiple

Consumer Internet public valuation multiples have held steady for 5 – 10 years.

Let’s zoom in:

SaasMarketplacesConsumerEcommerce

9

Maybe a slight uptick in last 24 months

-

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

35.0x

Med

ian

mul

tiple

Consumer Internet Multiples

EBITDA multiples Revenue Multiples

Recent increase in EBITDA multiples is probably driven by newish batch of hyper-revenue growth IPOs.

SaasMarketplacesConsumerEcommerce

10

Growth clearly drives multiples

Be wary of massive multiple re-rating when growth dips below ~30%

-

5.0x

10.0x

15.0x

20.0x

25.0x

-40% -20% 0% 20% 40% 60% 80% 100% 120%

LTM

reve

nue

mul

tiple

2014 revenue growth

Growth Rate vs. Revenue Multiples

Multiple compression begins at ~30%

SaasMarketplacesConsumerEcommerce

11

$10 billion is the new $1 billion

Current public companies

>$10B market cap

Private companies with at least $10B valuation

SaasMarketplacesConsumerEcommerce

In ~20 years, we got 10 US public Internet companies with > $10bn market caps, and we have 5 new private ones in 5

years.

12

E-commerce businesses aren’t worth much

-

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

18.0x

20.0x Ecommerce EBITDA Multiple

-

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x Ecommerce Revenue Multiple

*Data set includes traditional ecommerce, does not include ecommerce marketplace businesses

Many VC’s are paying 3-5x revenues for companies that are worth 1x in the public markets.

SaasMarketplacesConsumerEcommerce

13

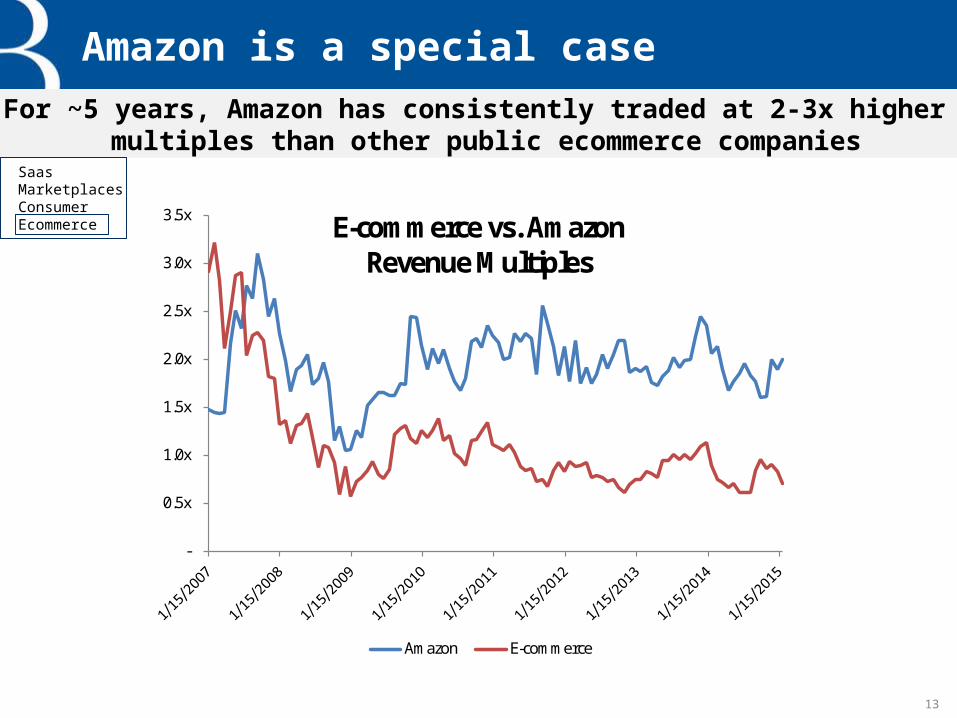

Amazon is a special case

-

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x E-commerce vs. AmazonRevenue Multiples

Amazon E-commerce

For ~5 years, Amazon has consistently traded at 2-3x higher multiples than other public ecommerce companies

SaasMarketplacesConsumerEcommerce

14

Marketplace models are highly valued

Valuation multiples are robust, but public markets have calmed down recently – much more so than private markets.

-

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

9.0x

10.0x E-commerce vs. MarketplaceRevenue Multiples

Marketplace E-commerce

SaasMarketplacesConsumerEcommerce

15

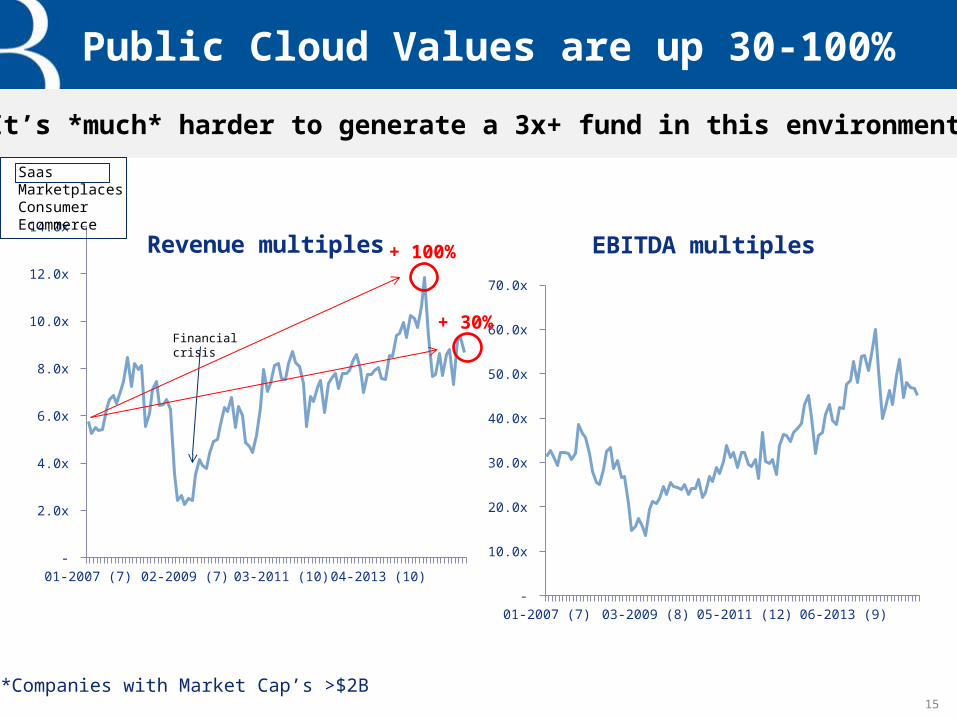

Public Cloud Values are up 30-100%

It’s *much* harder to generate a 3x+ fund in this environment

01-2007 (7) 09-2008 (7)05-2010 (10)02-2012 (9)10-2013 (11)-

10.0x

20.0x

30.0x

40.0x

50.0x

60.0x

70.0x

EBITDA multiples

01-2007 (7) 09-2008 (7)05-2010 (10)02-2012 (9)10-2013 (11)-

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x Revenue multiples

*Companies with Market Cap’s >$2B

Financial crisis

SaasMarketplacesConsumerEcommerce

+ 100%

+ 30%

16

It’s not a tech-wide issue, it’s just our sectors

While SaaS valuations have soared, their legacy counterparts are stable with much less rich valuations

*Data set: SAP, Oracle, Adobe, Microsoft, HP, Cisco

-

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x "Legacy" revenue multiple

-

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x "Legacy" EBITDA multiple

SaasMarketplacesConsumerEcommerce

17

SaaS investing was more fun in 2007!It’s easier to make money betting ahead of the curve. It’s

much harder when everyone agrees with you.

-

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x SaaS vs. "Legacy" software revenue multiples

SaaS Legacy

SaasMarketplacesConsumerEcommerce

“The interesting thing about cloud computing is that we’ve redefined cloud computing to include everything that we already do. ... The computer industry is the only industry that is more fashion-driven than women’s fashion. Maybe I’m an idiot, but I have no idea what anyone is talking about. What is it? It’s complete gibberish. It’s insane. When is this idiocy going to stop?"-- Larry Ellison, Sept 2008