using binaries-to-trade-direction

TRANSCRIPT

Using Binaries for Short Term Directional Trading

Using Binaries for Short Term Directional Trading, June 2013 Page 2 of 9North American Derivatives Exchange, Inc. is subject to U.S. regulatory oversight by the CFTC.

USing BinarieS for ShorT Term DirecTional TraDingBinaries can be used to take an intra-day directional view on underlying markets, allowing the trader to go long or short in a market for a fraction of the margin necessary when trading more conventional contracts.

And the usual benefits of Binaries apply – a trader’s risk is strictly capped without the danger of being stopped out by a temporary adverse move.

This presentation shows you how to use Binaries, either singly or strategically combined, to tailor your exposure to an underlying market.

As an example, let’s look at Nadex’s “US 500” Binaries, which settle based on an expiration value calculated by reference to the CME® E-mini® S&P 500® Futures†.

In this hypothetical example, the CME E-mini S&P 500 Futures for March are trading at 1252.00. The recent price action of these futures, as seen in the graph below, leads you to believe that the market has just broken through some short term resistance at the 1250.00 level. You believe that over the next couple of hours a market rally of a further 5-10 points is significantly more likely than a drop back below 1250.

1250

1252

12pm 1pm 2pm

Possible resistance level

Current level

Possible short term break out

Consider the ladder of end-of-day (expiration at 4:15pm ET) US 500 Binary contracts typically available on Nadex:

Contract Bid Offer

Daily US 500 (Mar) > 1268 - 2

Daily US 500 (Mar) > 1265 - 2.1

Daily US 500 (Mar) > 1262 - 2.8

Daily US 500 (Mar) > 1259 3 6

Daily US 500 (Mar) > 1256 15 18

Daily US 500 (Mar) > 1253 38.3 42.3

Daily US 500 (Mar) > 1250 66.9 70.4

Daily US 500 (Mar) > 1247 87.3 90.3

Daily US 500 (Mar) > 1244 96.2 98.9

Daily US 500 (Mar) > 1241 97.6 -

Daily US 500 (Mar) > 1238 98 -

Daily US 500 (Mar) > 1235 98 -

2 hours to expiration, futures trading at 1252.0

These prices can be viewed as consensus probabilities generated by Nadex market participants. So, for instance, the generality of Nadex traders perceive only a 15-18% chance of the US 500 settlement being higher than 1256 at the end of the day. And they believe that the probability of the market holding above 1250 at the end of the day is between 66.9% and 70.4%.

Futures, options, and swaps trading involves risk and may not be appropriate for all investors. Any trading decisions that you may make are solely your responsibility. The trading activity and other information presented herein are for informational purposes only. The contents hereof are not an offer, or a solicitation of an offer, to buy or sell any particular financial instrument offered on Nadex.

†S&P 500 is a registered mark of the McGraw-Hill Companies, Inc. CME and E-mini are registered marks of the Chicago Mercantile Exchange Inc. Nadex is not affiliated with these organizations and neither they nor their affiliates sponsor or endorse Nadex or its products in any way.

Using Binaries for Short Term Directional Trading, June 2013 Page 3 of 9North American Derivatives Exchange, Inc. is subject to U.S. regulatory oversight by the CFTC.

If you believe in a 5 point rally by the end of the day, to approximately 1257, a strategy you could use is to buy the “>1256” contract at 18. For each contract purchased you would be risking $18 to potentially make a profit of $82.

If you perceive the potential for a rally of around 10 points you could buy the “>1259” contract at 6. In this case, for each contract purchased, you would be risking $6 to potentially make $94. Or you might even buy the “>1262”, risking $2.80 to potentially make a profit of $97.20.

Taking a less bullish view, if you believe the market will simply hold above the key 1250 level, you could buy the “>1250” contract at 70.4, risking $70.40 to potentially make a profit of $29.60.

Contract Bid Offer

Daily US 500 (Mar) > 1268 - 2

Daily US 500 (Mar) > 1265 - 2.1

Daily US 500 (Mar) > 1262 - 2.8

Daily US 500 (Mar) > 1259 3 6

Daily US 500 (Mar) > 1256 15 18

Daily US 500 (Mar) > 1253 38.3 42.3

Daily US 500 (Mar) > 1250 66.9 70.4

Daily US 500 (Mar) > 1247 87.3 90.3

Daily US 500 (Mar) > 1244 96.2 98.9

Daily US 500 (Mar) > 1241 97.6 -

Daily US 500 (Mar) > 1238 98 -

Daily US 500 (Mar) > 1235 98 -

2 hours to expiration, futures trading at 1252.0

The following slides show the kinds of P&L profile you can generate with these and other strategies.

long 5 loTS of “>1256” @ 18

-200

-100

0

100

200

300

400

500

1247 1250 1253 1256 1259 1262 1265

Current market (= 1252)

Potential profit on 5 lot position (= $410 )

Potential loss on 5 lot position (= $90 )

Collateral required to enact this intraday binary strategy: $90

In this strategy, going long the “>1256” contract, you would be backing the underlying market to be more than 4 points higher by the end of day. The consensus of other Nadex participants is that this is only 15-18% likely.

Assuming you hold the position until expiration, each contract purchased would risk $18 to potentially make $82 (you buy at 18, and final settlement must be either 0 or 100). In this example 5 lots are being traded, so your maximum possible loss (and total required collateral) is 5 x 18 = $90.

Note that you do not have to hold the position until expiration – you might choose to exit early if the market moves up a few points in the short term and you do not believe the rally will be sustained. The price at which you could exit under these circumstances will depend on the precise size of the rally and the amount of time still remaining until expiration, as these two factors will shape the new probability that the “>1256” outcome will occur.

Example does not include fees and commissions, which may vary by broker. Example assumes all positions are entered into by trading at the available offer price rather than working orders at a more favorable level.

Back a strong (approx 10 pt) rally by buying one of these contracts – very small risk, very large potential reward for an outcome the market believes is very unlikely

Back any kind of rally, and still profit even if there is a small fall, by buying this contract – large risk, small potential reward for an outcome the market believes is somewhat likely

Back a moderate (approx 5 pt) rally by buying this contract – small risk, large potential reward for an outcome the market believes is pretty unlikely

Contract Bid Offer

Daily US 500 (Mar) > 1268 - 2

Daily US 500 (Mar) > 1265 - 2.1

Daily US 500 (Mar) > 1262 - 2.8

Daily US 500 (Mar) > 1259 3 6

Daily US 500 (Mar) > 1256 15 18 Buy 5

Daily US 500 (Mar) > 1253 38.3 42.3

Daily US 500 (Mar) > 1250 66.9 70.4

Daily US 500 (Mar) > 1247 87.3 90.3

Daily US 500 (Mar) > 1244 96.2 98.9

Daily US 500 (Mar) > 1241 97.6 -

Daily US 500 (Mar) > 1238 98 -

Daily US 500 (Mar) > 1235 98 -

2 hours to expiration, futures trading at 1252.0

Using Binaries for Short Term Directional Trading, June 2013 Page 4 of 9North American Derivatives Exchange, Inc. is subject to U.S. regulatory oversight by the CFTC.

long 5 loTS of “>1253” @ 42.3

-300

-200

-100

0

100

200

300

400

1247 1250 1253 1256 1259 1262 1265

Current market (= 1252)

Potential profit on 5 lot position (= $288.50 )

Potential loss on 5 lot position (= $211.50 )

Collateral required to enact this intraday binary strategy: $211.5

This strategy, going long the “>1253” contract, backs the underlying market to be more than just 1 point higher by the end of day. This is a less bullish view than the previous strategy and the consensus of nadex participants is that the outcome is more probable, at a likelihood of 38.3-42.3%.

Because success is more likely, your risk/reward ratio is less favorable than in the previous example. assuming you hold the position until expiration, each contract purchased would risk $42.30 to potentially make a profit of $57.70 (you buy at 42.3, and final settlement must be either 0 or 100). In this example 5 lots are being traded, so your maximum possible loss (and total required collateral) is 5 x 42.3 = $211.50.

Once again, though, you are not tied in to risking the whole $211.50 by waiting until expiration. If you feel the position is not working out (or if it is going right and you want to take an early profit) you can place an order to exit early. Provided your order is placed at a level which is attractive to other participants, you can close out your exposure to cap a loss or lock in a profit.

long 5 loTS of “>1259” @ 6

This is an example of an extremely bullish strategy, backing the market to be more than 7 points higher at the end of the day by going long the “>1259” contract. The consensus of Nadex participants is that the outcome is very improbable, at a likelihood of just 3-6%.

Because success is considered so unlikely by other participants, your risk/reward ratio is far more favorable than in either of the previous examples. Assuming you hold the position until expiration, each contract purchased would risk $6 to potentially make a profit of $94 (you buy at 6, and final settlement must be either 0 or 100). In this example 5 lots are being traded, so your maximum possible loss (and total required collateral) is 5 x 6 = $30.

A full payout in this example is, by definition, extremely unlikely. But note that a short term rally of a few points may, depending on precise timing and magnitude, lift the consensus bid above 6 and allow an opportunity to take a profit on the strategy, even if the final goal of a 7 point rally is never achieved.

Contract Bid Offer

Daily US 500 (Mar) > 1268 - 2

Daily US 500 (Mar) > 1265 - 2.1

Daily US 500 (Mar) > 1262 - 2.8

Daily US 500 (Mar) > 1259 3 6

Daily US 500 (Mar) > 1256 15 18

Daily US 500 (Mar) > 1253 38.3 42.3 Buy 5

Daily US 500 (Mar) > 1250 66.9 70.4

Daily US 500 (Mar) > 1247 87.3 90.3

Daily US 500 (Mar) > 1244 96.2 98.9

Daily US 500 (Mar) > 1241 97.6 -

Daily US 500 (Mar) > 1238 98 -

Daily US 500 (Mar) > 1235 98 -

2 hours to expiration, futures trading at 1252.0

Contract Bid Offer

Daily US 500 (Mar) > 1268 - 2

Daily US 500 (Mar) > 1265 - 2.1

Daily US 500 (Mar) > 1262 - 2.8

Daily US 500 (Mar) > 1259 3 6 Buy 5

Daily US 500 (Mar) > 1256 15 18

Daily US 500 (Mar) > 1253 38.3 42.3

Daily US 500 (Mar) > 1250 66.9 70.4

Daily US 500 (Mar) > 1247 87.3 90.3

Daily US 500 (Mar) > 1244 96.2 98.9

Daily US 500 (Mar) > 1241 97.6 -

Daily US 500 (Mar) > 1238 98 -

Daily US 500 (Mar) > 1235 98 -

2 hours to expiration, futures trading at 1252.0

Example does not include fees and commissions, which may vary by broker. Example assumes all positions are entered into by trading at the available offer price rather than working orders at a more favorable level.

-100

0

100

200

300

400

500

1247 1250 1253 1256 1259 1262 1265

Current market (= 1252)

Potential profit on 5 lot position (= $470 )

Potential loss on 5 lot position (= $30 )

Collateral required to enact this intraday binary strategy: $30

Using Binaries for Short Term Directional Trading, June 2013 Page 5 of 9North American Derivatives Exchange, Inc. is subject to U.S. regulatory oversight by the CFTC.

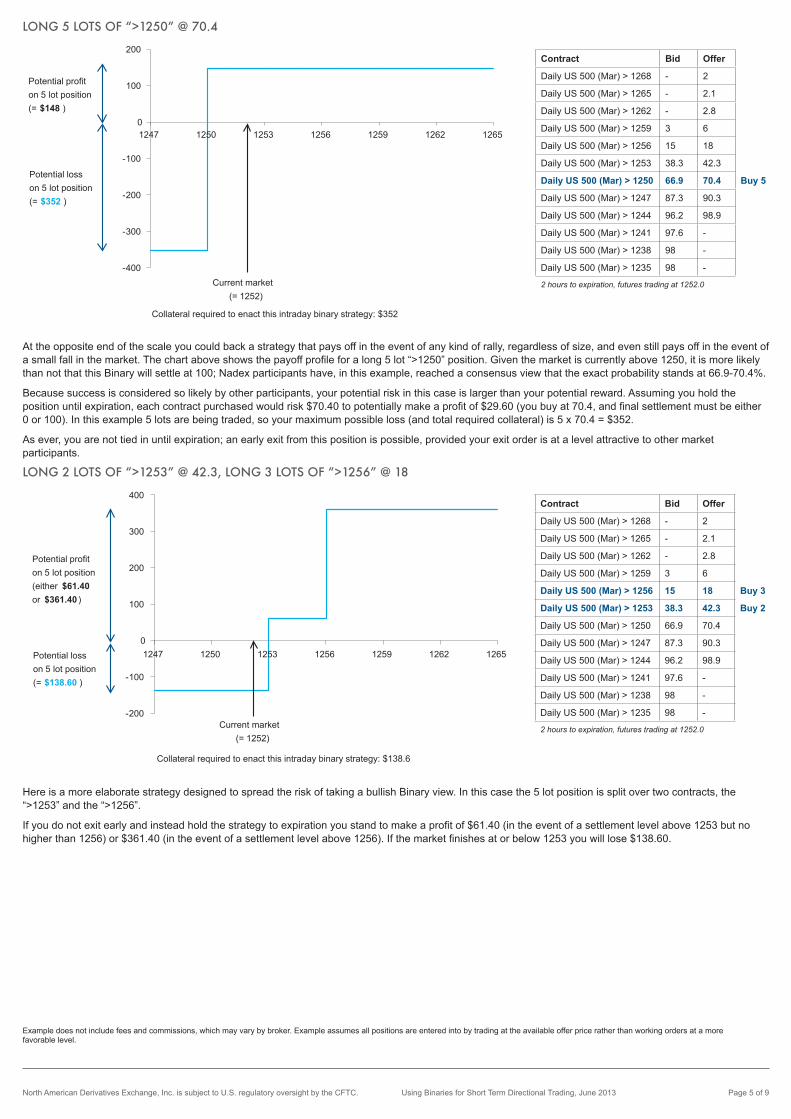

LOng 5 LOts Of “>1250” @ 70.4

-400

-300

-200

-100

0

100

200

1247 1250 1253 1256 1259 1262 1265

Current market (= 1252)

Potential profit on 5 lot position (= $148 )

Potential loss on 5 lot position (= $352 )

Collateral required to enact this intraday binary strategy: $352

At the opposite end of the scale you could back a strategy that pays off in the event of any kind of rally, regardless of size, and even still pays off in the event of a small fall in the market. The chart above shows the payoff profile for a long 5 lot “>1250” position. Given the market is currently above 1250, it is more likely than not that this Binary will settle at 100; Nadex participants have, in this example, reached a consensus view that the exact probability stands at 66.9-70.4%.

Because success is considered so likely by other participants, your potential risk in this case is larger than your potential reward. Assuming you hold the position until expiration, each contract purchased would risk $70.40 to potentially make a profit of $29.60 (you buy at 70.4, and final settlement must be either 0 or 100). In this example 5 lots are being traded, so your maximum possible loss (and total required collateral) is 5 x 70.4 = $352.

As ever, you are not tied in until expiration; an early exit from this position is possible, provided your exit order is at a level attractive to other market participants.

long 2 loTS of “>1253” @ 42.3, long 3 loTS of “>1256” @ 18

-200

-100

0

100

200

300

400

1247 1250 1253 1256 1259 1262 1265

Current market (= 1252)

Potential profit on 5 lot position (either $61.40 or $361.40 )

Potential loss on 5 lot position (= $138.60 )

Collateral required to enact this intraday binary strategy: $138.6

Here is a more elaborate strategy designed to spread the risk of taking a bullish Binary view. In this case the 5 lot position is split over two contracts, the “>1253” and the “>1256”.

If you do not exit early and instead hold the strategy to expiration you stand to make a profit of $61.40 (in the event of a settlement level above 1253 but no higher than 1256) or $361.40 (in the event of a settlement level above 1256). If the market finishes at or below 1253 you will lose $138.60.

Contract Bid Offer

Daily US 500 (Mar) > 1268 - 2

Daily US 500 (Mar) > 1265 - 2.1

Daily US 500 (Mar) > 1262 - 2.8

Daily US 500 (Mar) > 1259 3 6

Daily US 500 (Mar) > 1256 15 18

Daily US 500 (Mar) > 1253 38.3 42.3

Daily US 500 (Mar) > 1250 66.9 70.4 Buy 5

Daily US 500 (Mar) > 1247 87.3 90.3

Daily US 500 (Mar) > 1244 96.2 98.9

Daily US 500 (Mar) > 1241 97.6 -

Daily US 500 (Mar) > 1238 98 -

Daily US 500 (Mar) > 1235 98 -

2 hours to expiration, futures trading at 1252.0

Example does not include fees and commissions, which may vary by broker. Example assumes all positions are entered into by trading at the available offer price rather than working orders at a more favorable level.

Contract Bid Offer

Daily US 500 (Mar) > 1268 - 2

Daily US 500 (Mar) > 1265 - 2.1

Daily US 500 (Mar) > 1262 - 2.8

Daily US 500 (Mar) > 1259 3 6

Daily US 500 (Mar) > 1256 15 18 Buy 3

Daily US 500 (Mar) > 1253 38.3 42.3 Buy 2

Daily US 500 (Mar) > 1250 66.9 70.4

Daily US 500 (Mar) > 1247 87.3 90.3

Daily US 500 (Mar) > 1244 96.2 98.9

Daily US 500 (Mar) > 1241 97.6 -

Daily US 500 (Mar) > 1238 98 -

Daily US 500 (Mar) > 1235 98 -

2 hours to expiration, futures trading at 1252.0

Using Binaries for Short Term Directional Trading, June 2013 Page 6 of 9North American Derivatives Exchange, Inc. is subject to U.S. regulatory oversight by the CFTC.

long 1 loT of “>1253” @ 42.3, long 1 loT of “>1256” @ 18, long 3 loTS of “>1259”” @ 6

-200

-100

0

100

200

300

400

500

1247 1250 1253 1256 1259 1262 1265

Current market (= 1252)

Potential profit on 5 lot position (either $21.70 or $121.70 or $421.70 )

Potential loss on 5 lot position (= $78.30 )

Collateral required to enact this intraday binary strategy: $78.3

Here is an example of a 3 contract strategy designed to ratchet up a payout in the event of a large rally. In this case the 5 lot position is split over three contracts, the “>1253”, the “>1256” and the “>1259”.

Here your maximum risk, should you choose to hold the position until expiration, is capped at $78.30. A settlement level above 1253 will result in a profit of either $21.70, $121.70 or $421.70, depending on just how strong the market is by the end of the day.

You can also use Binaries in conjunction with conventional futures contracts. The final few examples look at the effect of going long of a single lot of the CME E-mini S&P 500 Futures, while providing temporary protection against a sudden adverse move by shorting some US 500 Nadex Binaries.

1250

1252

12pm 1pm 2pm

Possible resistance level

Current level

Possible short term break out

Contract Bid Offer

Daily US 500 (Mar) > 1268 - 2

Daily US 500 (Mar) > 1265 - 2.1

Daily US 500 (Mar) > 1262 - 2.8

Daily US 500 (Mar) > 1259 3 6

Daily US 500 (Mar) > 1256 15 18

Daily US 500 (Mar) > 1253 38.3 42.3

Daily US 500 (Mar) > 1250 66.9 70.4 If you go long of the CME E-mini S&P 500 Futures, selling some of these Binaries can provide protection against an unexpected short term drop in the market

Daily US 500 (Mar) > 1247 87.3 90.3

Daily US 500 (Mar) > 1244 96.2 98.9

Daily US 500 (Mar) > 1241 97.6 -

Daily US 500 (Mar) > 1238 98 -

Daily US 500 (Mar) > 1235 98 -

2 hours to expiration, futures trading at 1252.0

Contract Bid Offer

Daily US 500 (Mar) > 1268 - 2

Daily US 500 (Mar) > 1265 - 2.1

Daily US 500 (Mar) > 1262 - 2.8

Daily US 500 (Mar) > 1259 3 6 Buy 3

Daily US 500 (Mar) > 1256 15 18 Buy 1

Daily US 500 (Mar) > 1253 38.3 42.3 Buy 1

Daily US 500 (Mar) > 1250 66.9 70.4

Daily US 500 (Mar) > 1247 87.3 90.3

Daily US 500 (Mar) > 1244 96.2 98.9

Daily US 500 (Mar) > 1241 97.6 -

Daily US 500 (Mar) > 1238 98 -

Daily US 500 (Mar) > 1235 98 -

2 hours to expiration, futures trading at 1252.0

Example does not include fees and commissions, which may vary by broker. Example assumes all positions are entered into by trading at the available offer price rather than working orders at a more favorable level.

Using Binaries for Short Term Directional Trading, June 2013 Page 7 of 9North American Derivatives Exchange, Inc. is subject to U.S. regulatory oversight by the CFTC.

shOrt 5 LOts Of “>1250” @ 66.9, LOng 1 LOt CME E-MInI s&P 500 futurEs @ 1252

-200

-100

0

100

200

300

400

1238 1241 1244 1247 1250 1253 1256

-800

-600

-400

-200

0

200

400

1238 1241 1244 1247 1250 1253 1256

Strategy boosts futures P&L by $334.50 in this region

Strategy reduces futures P&L by $165.50 in this region

Standalone Binary P&L

Standalone Futures P&L

Net Strategy P&L

Current market (= 1252)

A short position in the “>1250”, taken out at a price of 66.9, means that for each contract you stand to make $66.90 for a risk of $33.10.

Going short of 5 lots, in conjunction with a long position of 1 lot in the futures, results in boosting your P&L by $334.50 in the event of a settlement at or below 1250. This comes at the cost of reducing your P&L by $165.50 in the event of a settlement above 1250.

Example does not include fees and commissions, which may vary by broker. Example assumes all Binary positions are entered into by trading at the available bid price rather than working orders at a more favorable level. Payout profiles assume futures position is closed out at a level identical to the Nadex-calculated US 500 Expiration Value.

Contract Bid Offer

Daily US 500 (Mar) > 1268 - 2

Daily US 500 (Mar) > 1265 - 2.1

Daily US 500 (Mar) > 1262 - 2.8

Daily US 500 (Mar) > 1259 3 6

Daily US 500 (Mar) > 1256 15 18

Daily US 500 (Mar) > 1253 38.3 42.3

Daily US 500 (Mar) > 1250 66.9 70.4 Sell 5 (and buy 1 lot of futures)

Daily US 500 (Mar) > 1247 87.3 90.3

Daily US 500 (Mar) > 1244 96.2 98.9

Daily US 500 (Mar) > 1241 97.6 -

Daily US 500 (Mar) > 1238 98 -

Daily US 500 (Mar) > 1235 98 -

2 hours to expiration, futures trading at 1252.0

Using Binaries for Short Term Directional Trading, June 2013 Page 8 of 9North American Derivatives Exchange, Inc. is subject to U.S. regulatory oversight by the CFTC.

shOrt 5 LOts Of “>1247” @ 87.3, LOng 1 LOt CME E-MInI s&P 500 futurEs @ 1252

-100

0

100

200

300

400

500

1238 1241 1244 1247 1250 1253 1256

-800

-600

-400

-200

0

200

400

600

1238 1241 1244 1247 1250 1253 1256

Strategy boosts futures P&L by $436.50 in this region

Strategy reduces futures P&L by $63.50 in this region

Standalone Binary P&L

Standalone Futures P&L

Net Strategy P&L

Current market (= 1252)

Cheaper (but less comprehensive) protection can be engineered by taking a short position in the “>1247” at a price of 87.30, leaving you with a per-contract potential profit of $87.30 and a maximum possible per-contract loss of $12.70.

Going short of 5 lots, in conjunction with a long position of 1 lot in the futures, results in boosting your P&L by $436.50 in the event of a settlement at or below 1247. This comes at the cost of reducing your P&L by $63.50 in the event of a settlement above 1247.

Contract Bid Offer

Daily US 500 (Mar) > 1268 - 2

Daily US 500 (Mar) > 1265 - 2.1

Daily US 500 (Mar) > 1262 - 2.8

Daily US 500 (Mar) > 1259 3 6

Daily US 500 (Mar) > 1256 15 18

Daily US 500 (Mar) > 1253 38.3 42.3

Daily US 500 (Mar) > 1250 66.9 70.4

Sell 5 (and buy 1 lot of futures)

Daily US 500 (Mar) > 1247 87.3 90.3

Daily US 500 (Mar) > 1244 96.2 98.9

Daily US 500 (Mar) > 1241 97.6 -

Daily US 500 (Mar) > 1238 98 -

Daily US 500 (Mar) > 1235 98 -

2 hours to expiration, futures trading at 1252.0

Example does not include fees and commissions, which may vary by broker. Example assumes all Binary positions are entered into by trading at the available bid price rather than working orders at a more favorable level. Payout profiles assume futures position is closed out at a level identical to the Nadex-calculated US 500 Expiration Value.

Using Binaries for Short Term Directional Trading, June 2013 Page 9 of 9North American Derivatives Exchange, Inc. is subject to U.S. regulatory oversight by the CFTC.

North American Derivatives Exchange, Inc.311 South Wacker Drive • Suite 2675 • Chicago, IL 60606Phone: 312-884-0100 • Fax: 312-884-0940 • Email: [email protected]

shOrt 1 LOt Of “>1250” @ 66.9, shOrt 2 LOts Of “>1247” @ 87.3, shOrt 2 LOts Of “>1244” @ 96.2, LOng 1 LOt CME E-MInI s&P 500 futurEs @ 1252

-100

0

100

200

300

400

500

1238 1241 1244 1247 1250 1253 1256

-800

-600

-400

-200

0

200

400

600

1238 1241 1244 1247 1250 1253 1256

Strategy boosts futures P&L by either $33.90 or $233.90 or $433.90 in this region

Strategy reduces futures P&L by $66.10 in this region

Standalone Binary P&L

Standalone Futures P&L

Net Strategy P&L

Current market (= 1252)

Again, many more elaborate strategies are possible. In this one the 5 lot position has been split between 3 contracts, giving extensive downside protection to your long E-Mini position, at the cost of reducing P&L by $66.10 in the event that all the Binaries settle in the money.

range of markeTSWe offer contracts on:

Equity Indices: US 500, Wall Street 30, US Tech 100, US SmallCap 2000, Germany 30, Japan 225, FTSE 100®

Spot FX: EUR/USD, USD/JPY, GBP/USD, USD/CHF, USD/CAD, AUD/USD, GBPJPY, EURJPY

Energies: Crude Oil, Natural Gas

Metals: Gold, Silver, Copper

Agriculturals: Corn, Soybeans

Economic Events: Initial Jobless Claims, Fed Funds, ECB Rate, Nonfarm Payrolls, Unemployment Rate

Example does not include fees and commissions, which may vary by broker. Example assumes all Binary positions are entered into by trading at the available bid price rather than working orders at a more favorable level. Payout profiles assume futures position is closed out at a level identical to the Nadex-calculated US 500 Expiration Value.

Futures, options, and swaps trading involves risk and may not be appropriate for all investors. Any trading decisions that you may make are solely your responsibility. The information presented herein is for informational purposes only. The contents hereof are not an offer, or a solicitation of an offer, to buy or sell any particular financial instrument offered on Nadex.

Contract Bid Offer

Daily US 500 (Mar) > 1268 - 2

Daily US 500 (Mar) > 1265 - 2.1

Daily US 500 (Mar) > 1262 - 2.8

Daily US 500 (Mar) > 1259 3 6

Daily US 500 (Mar) > 1256 15 18

Daily US 500 (Mar) > 1253 38.3 42.3

Daily US 500 (Mar) > 1250 66.9 70.4 Sell 1

Sell 2

Sell 2 (and buy 1 lot of futures)

Daily US 500 (Mar) > 1247 87.3 90.3

Daily US 500 (Mar) > 1244 96.2 98.9

Daily US 500 (Mar) > 1241 97.6 -

Daily US 500 (Mar) > 1238 98 -

Daily US 500 (Mar) > 1235 98 -

2 hours to expiration, futures trading at 1252.0