users of financial statements what you look for in the...

TRANSCRIPT

INT / INC - 1

Users of Financial Statements

What you look for in the statements depends on your objectives

• Equity investment: profitability, risk, cash generating ability

• Merger and acquisition: profitability, risk, price to pay, impact on financial

statements.

• Credit extension/Customer health: short-term vs. long-term, ability to pay interest &

-principal, liquidity.

• Supplier health (supplier of key raw material, supplier's quality, JIT): cash

generating ability, profitability.

• Employer health (employees, unions): long-term viability & ability to meet pension

liabilities, profitability, risk.

• Internal operation analysis: analysis of business segments performance, cost,

profit, budgeting, and business strategy.

• Antitrust regulations: monopoly power (profitability, market share), cost of capital,

justifying merger through "failing company doctrine" disregarding monopoly

consideration.

• Competitors analysis: profitability, profit margins, market share (aids in pricing,

product mix).

• Audit tests: going concern judgements by auditors.

• Legal judgement: fraudulent conveyance.

Concentrate on investors and creditors

(Covers most users).

INT / INC - 2

Financial statements (the reports produced by the financial accounting system), in theory, aim at providing information useful for these two groups, while limiting the

information available for competitors.

What information is considered useful to investors and creditors? 1 Information that helps in predicting future cash flows. Investors are primarily

interested in valuing firms. 2 Information relating to a firm’s risk characteristics - liquidity, solvency 3 Information that may serve as an observable on which contracts are written. Two simple examples:

Example 1: Corporate lending contracts typically contain certain restrictions on the borrowing party in order to reduce its risk of default. These restrictions are typically based on accounting variables such as debt-equity, ratios and working capital. Example 2: Managers' compensation is tied to firm performance that is often measured by reported earnings.

Does this however hold true in practice?

INT / INC - 3

The Adversarial Nature of Financial Reporting

Corporations and Management have substantial incentives to exploit the fact that

accounting principles are neither fixed nor precise as to be open to only one

interpretation. (e.g., SEC requires companies to disclose information if it is material

but does not define materiality with great precision.) The simple fact that preparers

of financial statements spend time contemplating issues such as the accounting

methods to be used (e.g., LIFO or FIFO), what is to be disclosed, the timing of the

disclosure, etc., indicates that they believe that their choice makes a difference.

The incentives to exploit the nature of financial reporting are twofold:

1. As part of the fiduciary duty to shareholders:

A corporation exists for the benefit of its shareholders, not for the purpose of

educating the public about its financial condition. Bearing in mind this fiduciary

responsibility, corporate managers may ask themselves whether they are acting

responsibly if they do not take advantage of legal opportunities to maximize

shareholder’s wealth.

2. For self-serving reasons as management compensation and perhaps their

job itself is tied to financial results These reasons lead to the following conclusion on the part of management:

THE BEST KIND OF FINANCIAL STATEMENT IS THE ONE THAT RESULTS IN THE HIGHEST POSSIBLE

PRICE FOR ITS STOCK AND/OR

PERSONAL COMPENSATION

FASB and SEC prohibit companies from going too far in this direction, but once

managers accept the premise that financial statements are instruments for

INT / INC - 4

maximizing shareholders’ wealth, they will realize the benefits by preparing the

statements so as to:

1. lower cost of capital (risk) 2. create higher "earnings" expectations 3. downplay "real' and contingent liabilities

INT / INC - 5

Accounting Definitions of Income - Review A major problem in measuring firm performance for a specific accounting period arises in situations where a transaction is started in one period but will be completed in a future period.

Two approaches to determine the timing of earnings recognition exist:

Cash basis of accounting

Accrual basis of accounting

The difference between these two methods is in the time when they

consider a transaction as completed, namely, when they recognize earnings. (i.e., the question is when revenues and/or expenses are reported (i.e.,

recognized) in the income statement.). Over the life of the firm, income and cash flows converge. They differ only as to timing of recognition. Accounting concept of income: Purpose →→→→ Informational →→→→ Future Cash Flows

Question: If purpose of accounting is to forecast future cash flows why not just provide cash flows or cash basis income. Answer: Accrual accounting “better” forecaster of future cash flows:

• e.g. spend $10 to purchase asset which is sold for $12 on account What is better forecast of profitability ($10) or $2?

INT / INC - 6

The accounting definition of income and the economic definition of earnings [and/or the definition(s) relevant to the analyst] are not always equivalent. Some examples of theoretical definitions of income are presented below. These definitions although useful as normative principles, are often difficult to operationalize and are not equivalent a priori to the accounting definition of income.

THEORETICAL INCOME CONCEPTS Economic earnings is net cash flow plus the change in market value of the

firm’s assets.

Sustainable earnings refers to the level of income that can be maintained in the future given the firm’s stock of capital investment (e.g., fixed assets and inventory).

Permanent earnings is used by analysts for valuation purposes. It is the

amount that can be normally earned given the firm’s assets and equals the

market value of those assets times the firm’s required rate of return. It is the

base to which a multiple is applied to arrive at a “fair price.”

Consider previous example but after purchasing asset for $10, its cost

increases to $11 --- Mark-up continues at 20%. Selling Price ______

Accounting Earnings ________ Economic Earnings _______

Sustainable Earnings _______ Permanent Earnings _______

INT / INC - 7

1. Accrual Basis Two characteristics:

Recognizes revenues when following conditions satisfied: 1. Goods and services substantially provided; 2. Cash collectibility reasonably assured.

These conditions are typically met when goods are delivered or services are rendered. Expense recognition is governed by the matching principle:

• costs incurred in the process of generating revenues are reported as expenses in the period when the revenues are recognized.

Various modifications/implications in the process:

• Costs incurred that cannot be associated specific revenue streams (e.g., administrative expense) are treated as an expense of the period. • To reflect the fact that some portion of sales on credit will eventually prove uncollectible we adjust downward by the amount expected to be lost (an allowance for bad debt). • The matching principle also suggests that long lived assets should be expensed during the whole period they generate income. We get this result through depreciation charges.

Opening Balance Sheet Cash 100 Common Stock 100 Purchase Inventory Cash 90 Inventory 10 Common Stock 100

100 Equity 100 Sell for $12 on account Cash 90 Gain 2 A / R 12 Common Stock 100 102 Equity 102

INT / INC - 8

2. Cash basis Revenues (from selling goods or rendering services) are recognized in the

period when cash is received from customers.

Expenses (for merchandise, insurance, salaries and even the acquisition of

long-lived assets) are reported in the period they are actually made.

Opening Balance Sheet Cash 100 Common Stock 100 Purchase Inventory Cash 90 Loss (10) Common Stock 100 Equity 90 Sell for $12 on account Cash 90 Loss (10) Common Stock 100 Equity 90

INT / INC - 9

Disadvantages of the cash basis: • The costs of generating income are not adequately matched with

revenues.

• The cash basis postpones unnecessarily the time when revenues are

recognized.

Typical users of the cash basis: professional people (e.g., lawyers, and

accountants) and individuals (employees).

Disadvantages of the accrual basis: Serious problems with accrual accounting is that its periodic income numbers

reflect

• the results of some but not all of a firm’s real economic events • also choices (manipulation) of and/or changes in accounting methods and

estimates made by management

IMPORTANT IMPLICATION OF ACCRUAL MEASURE OF INCOME

Balance Sheet amounts are function of income policy choice. Cash collected after sale → Accounts receivable Cash outlay prior to expense recognition: → Inventory, PP&E

Income = Cash Flow +/- Accrual

Accrual →→→→ Balance Sheet

Thus assets/liabilities on balance sheet may not reflect “reality” but rather are accounting constructs:

INT / INC - 10

We illustrate by considering first exceptions to the general case (i.e. when revenue is recognized at time of delivery.) Some types of businesses deserve special attention because the nature of the transactions in which they are involved are particularly problematic from the income determination standpoint, and therefore these businesses get special accounting treatment.

Accounting for long-term contractors Characterization of long-term contractors:

• The business cycle spans several years. • A contract exists in advance; so selling price and payment terms

are known.

While one may like to recognize earnings as soon as possible, it cannot be done at the time the contract is signed as the service is not yet rendered.

Completed Contract Method Under the completed contract method revenues and expenses are

recognized when the service is completed.

Percentage of Completion Method. If it is possible to accurately estimate1 the results of the transaction at the time

the contract is signed, one recognizes earnings during the project as work is

rendered, using the percentage of completion method.

Under this method, one recognizes a portion (e.g., using engineering

estimates) of the total project price as revenues (and expense) for the period,

based on the degree of completion of the work during that period.

1 If there exists uncertainty about the outcome of the project, it is recommended to use the completed contract method.

INT / INC - 11

Example: Assumptions: Project -3 year life Cash disbursements measure progress. Year 1 2 3 Total Cash Receipts 1,000 1,000 1,000 3,000 Disbursements 900 600 300 1,800 ∆ cash 100 400 700 1,200 ∆ cash cumul 100 500 1,200

INCOME STATEMENT Completed Contract Year 1 2 3 Total Revenues Expenses Income Income Cumul

Percentage of Completion Year 1 2 3 Total Revenues Expenses Income Income Cumul

BALANCE SHEET Completed Contract Year 1 2 3 Cash Inventory Current Assets Advances (CL) Retained Earnings Liability & Equity Percentage of Completion Year 1 2 3 Cash Accounts Receivable2 Current Assets Retained Earnings Liability & Equity

2 May be called Inventory: Work in Process at Contract Price and may be reported at times net of advances

INT / INC - 12

Differences between Methods: Both Income Statement and Balance Sheet

• Profitability

• Current Assets

• Working Capital

• Total Assets

• Equity

Note: Percentage of Completion

-- shows profitability trends earlier These differences are critical when comparing the size, profitability, return on assets, and return on equity ratios for European/Japanese (using completed contracts) construction companies with their US competitors (using percentage-of-completion).

INT / INC - 13

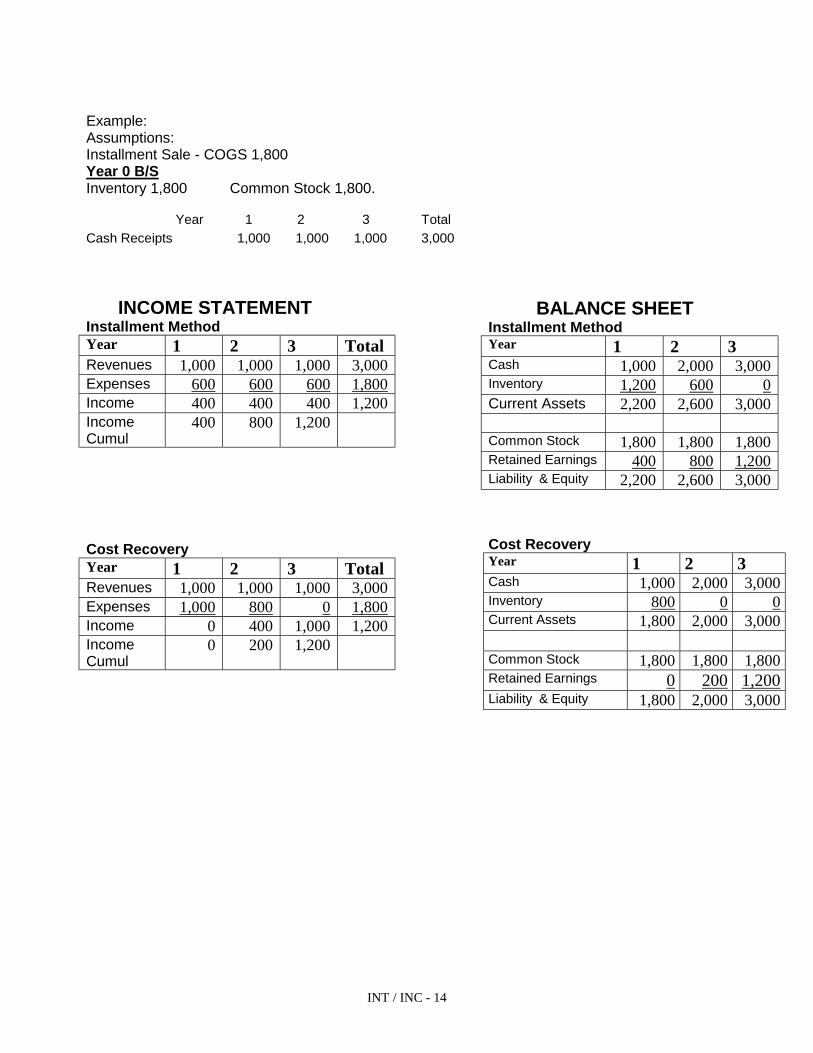

Accounting where cash collection is uncertain Two methods are in use:

Installment method: Revenues are recognized as parts of the selling price are collected in cash; e.g., $100 selling price, $60 cost price, 5 installments, each period will recognize $20 revenues and $12 costs.

Cost-Recovery First Method: Revenues and costs are equal in each period until all costs are recovered. Using the example: in the first 3 periods the profit is 0, in each of the fourth and fifth periods, $20 profit is recognized.

INT / INC - 14

Example: Assumptions: Installment Sale - COGS 1,800 Year 0 B/S Inventory 1,800 Common Stock 1,800. Year 1 2 3 Total Cash Receipts 1,000 1,000 1,000 3,000

INCOME STATEMENT Installment Method Year 1 2 3 Total Revenues 1,000 1,000 1,000 3,000 Expenses 600 600 600 1,800 Income 400 400 400 1,200 Income Cumul

400 800 1,200

Cost Recovery Year 1 2 3 Total Revenues 1,000 1,000 1,000 3,000 Expenses 1,000 800 0 1,800 Income 0 400 1,000 1,200 Income Cumul

0 200 1,200

BALANCE SHEET Installment Method Year 1 2 3 Cash 1,000 2,000 3,000 Inventory 1,200 600 0 Current Assets 2,200 2,600 3,000 Common Stock 1,800 1,800 1,800 Retained Earnings 400 800 1,200 Liability & Equity 2,200 2,600 3,000 Cost Recovery Year 1 2 3 Cash 1,000 2,000 3,000 Inventory 800 0 0 Current Assets 1,800 2,000 3,000 Common Stock 1,800 1,800 1,800 Retained Earnings 0 200 1,200 Liability & Equity 1,800 2,000 3,000

INT / INC - 15

It follows that the income numbers as well as balance sheet numbers

should be carefully examined before inferences are made. Thus,

financial statement analysis is a two step procedure:

Step 1. Examine carefully the reported numbers in financial statements and make adjustments in cases they are distorted (depart from economic reality). The reported numbers may be distorted either because managers manipulate them or because of limitations underlying GAAP. Step 2. Use the adjusted numbers for analytic purposes:

e.g. valuation / credit analysis.

INT / INC - 16

Recurring versus Nonrecurring income

Company has one asset - original cost $1,000 Asset generates annual income of $100. Cost of capital = 10%. Value of firm: 100/.1 = $1,000 Scenario 1:

Annual income increases to $120 -

Value of firm = $120/.1 = $1,200

Scenario 2: Firms sells asset for $1,150; replaces it with one costing $1,000 Income this year = $250 (i.e. annual income of $100 + gain on sale $150)

Value of firm = ?

INT / INC - 17

Traditional Format Sales 12,000 Affiliate Income 1,000 13,000 COGS (7,900) SG&A (3,600) Asset Sales 1,400 Restructuring (400) Interest (1,500) (12,000) EBT 1,000 Taxes (@ 40%) 400 Net Income 600

Suggested Format Sales 12,000 COGS (7,900) Gross Profit 4,100 SG&A (3,600) Operating Income 500 Affiliate Income 1,000 Recurring Income 1,500 Interest (1,500) Pretax Income from Continuing Operations

0

Taxes N/A Asset Sales 1,400 Restructuring (400) EBIT 1,000 Taxes (@ 40%) 400 Net Income 600

INT / INC - 18

2-11. [Revenue and expense recognition: Pricing season tickers—The Toronto Raptors, courtesy of Professor I. Krinsky] The Toronto Raptors, a 1995 NBA expansion team, announced an elaborate season-ticket plan with a ticket price and vantage point to satisfy almost every need. Ticket prices range from $85 per game for 45 games--plus a one-time license fee of $8,750—for the best seats, to $10 per game—plus a one-rime license fee of $750—for the cheapest seats; the team has eight ticket prices.

The license fee, used for the first time by a sports team in Canada, entitles the holder to a de facto lease on the seat. The license holder retains the right to buy the accompanying ticket and may sell that right to anyone at a mutually agreed on price.

A. Discuss how the Toronto Raptors should recognize revenue from ticket sales and the license fee under this system.

B. Discuss how a corporation that purchases Toronto Raptors

tickets and gives them to its customers should recognize the license fee.

C. As an analyst, how would you incorporate

• The licensing fee • Season-ticket sales

in your estimation of the Raptors’ expected earnings?

INT / INC - 19

2-14 (Recurring and Nonrecurring income - Courtesy of Professor M.

Schiff) It is often argued by analysts that it is important to focus on

ongoing recurring income and ignore nonrecurring charges. Exhibit 2P-

3 is adapted from AT&T’s 1995 annual report. The exhibit reports the

company’s sales and operating income (Earnings Before interest and

Taxes) for the 11-year period 1985-1995. Information about the

company’s restructuring charges and other writedowns are also

provided in the exhibit.

(a) What would AT&T’s operating income have been without the

nonrecurring charges? (b) Compare the trend in AT&T’s reported operating income with the

adjusted numbers computed in (a) and with sales. (Graphical analysis may be useful here)

(c) Which set of operating income numbers do you feel is most relevant in analyzing AT&T. What adjustments or other information would you need?

EXHIBIT 2P-3 AT&T Revenues and Operating income (1985-1995) All Data in Billions of $

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 Results of Operations Total Revenues 63.2 62.0 60.7 62.1 61.6 63.2 64.5 66.6 69.4 75.1 79.6 Operating Income (Loss) 3.6 1.0 4.1 (2.5) 4.8 5.4 1.4 6.5 6.5 7.9 1.2

1986 DATA REFLECT $3.2 BILLION OF PRETAX CHARGES FOR BUSINESS RESTRUCTURING, AND ACCOUNTING CHANGE AND OTHER ITEMS. I988 DATA REFLECT A $6.7 BILLION PRETAX CHARGE DUE TO ACCELERATED DIGITIZATION OF THE LONG DISTANCE NETWORK 1991 DATA REFLECT $4.5 BILLION OF PRETAX BUSINESS RESTRUCTURING AND OTHER CHARGES. 1993 DATA REFLECT $0.5 BILUON OF PRETAX BUSINESS RESTRUCTURING AND OTHER CHARGES. 1995 DATA REFLECT $7.8 BILLION OF PRETAX BUSINESS RESTRUCTURING AND OTHER CHARGES. Source: Adapted from 1995 Annual Report

INT / INC - 20

INT / INC - 21

INT / INC - 22

INT / INC - 23

Thousand Trails - I Revenue and Expense Recognition Thousand Trails owned and operated private membership resort

campgrounds (preserves) in the United States arid Canada. Membership

allowed a member’s family an unlimited number of visits to any of the

company’s present or proposed campgrounds for an initial membership fee and

annual dues. Memberships could be used over the lifetime of the member and

passed on to heirs (transfer limited to one generation). They did not convey

ownership interest in the company or its preserves. The company was not

contractually obligated to provide additional campgrounds or to provide

additional facilities at existing sites. The company, however, did promise (and

planned) to develop and operate additional sites.

In addition to membership sales, the company earned income from (1)

interest on installment receivables generated by membership sales and (2)

annual dues paid by existing members. Membership sales, however, were by

far the primary source (approximately two-thirds) of Thousand Trails’ income

Thousand Trails’ net income increased almost fourfold (from $3.3 million

to $12 million) in the period 1981 to 1983. Most of the increase was attributable

to the high growth rate of membership sales, which increased by 40% in each

of the years 1982 and 1983. Income from membership sales increased almost

three times over the same period.

Revenue Recognition by Thousand Trails -

Thousand Trails’ revenue recognition footnote states The Company sells memberships for cash or on installment contracts.

Revenues are recorded in full upon execution of membership agreements.

Installment sales require a down payment of at least 10% of the sales price.

All marketing costs and an allowance for estimated contract collection losses

(based on historical loss occurrence rates) are recorded currently.

INT / INC - 24

The footnote indicates that revenue was recognized in full for both cash

and installment sales as long as a down payment of 10% was received. Other

footnotes indicate that installment sales had terms of 24 to 84 months with an

average term of 61 months.

Expense Recognition by Thousand Trails

Thousand Trails incurred two types of expenditures in generating sales

of memberships: (1) marketing costs and (2) preserve development costs.

Marketing costs were charged to expense as incurred. Preserve development

costs were treated as stated in the revenue recognition footnote:

Operating preserve land and improvement costs, including the estimated costs

to complete preserves in accordance with the Company ‘s development plans,

are aggregated by geographical region and recorded as a cost of membership

sales based upon the ratio of actual memberships sold within each region to

the total memberships planned by the Company to be available for sale within

the region

For expense recognition, Thousand Trails used a percentage-of-

completion method and allocated (actual and planned) costs to expenses

based upon the portion of actual to planned sales. With respect to actual and

planned sales the company stated that

As of December 31, 1983, the Company had 51,000 members which

represented approximately one-third of the total planned memberships for sale

on its 36 operating preserves

INT / INC - 25

INT / INC - 26