usability factors in digital music distribution services and their

TRANSCRIPT

Joakim Landegren 780119-0070

Tutor: Roger Wallis Examiner: Nils Enlund

Usability Factors in Digital Music Distribution Services and Their Relationships with Established

and New Value Chains in the Music Industry

- A Study on Online Distribution Models Used by the Music Industry Today and Identifying of Important Factors for a Successful Service

A Master’s Thesis in Media Technology and Graphic Arts Department of Numerical Analysis and Computer Science

Royal Institute of Technology 17-04-2003

Joakim Landegren 780119-0070

Handledare: Roger Wallis Examinator: Nils Enlund

Användbarhetsfaktorer för digitala musikdistributionstjänster och deras relation till

etablerade och nya värdekedjor inom musikindustrin

- En studie av online-distributionsmodeller, identifiering av viktiga faktorer för en attraktiv tjänst samt konsumenters, musikskapares och

industrins intressen

Ett examensarbete i Medieteknik och Grafisk produktion Institutionen för Numerisk Analys och Datalogi

Kungliga Tekniska Högskolan, Stockholm 2003-04-17

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

Abstract The findings in this report are the results of an evaluation of the available digital music distribution services over a longer period, and an analysis the underlying rules, mechanisms, theories and opinions within the music industry to find what factors are essential for a commercially successful service.

The music industry has now acknowledged digital music distribution services as a new channel, but there is still no successful commercial service today. Commercial services are competing with Peer-to-Peer services that offer a wide diversity of music at a minimal cost for consumers. So there is a great need for the industry to find a commercial alternative that consumers will accept.

A number of factors important for a successful service have been identified. These include a relevant music selection, availability virtually as conveniently as unprotected files. They also include usability in the form of a good search tool and logical categorisation as well as an efficient revenue control utilising alternative revenue channels. Other important factors are copyright rules that need to be revised to become more globally coherent. The industry also needs to develop a working copy protection system that does not impose too many limitations for consumers without losing the ability to generate revenue for content owners. New pricing models are needed for consumers to accept payments for music files, and subscriptions. Eventually an indirect payment method seems to be the best solution.

Digital music distribution promotes diversity in music genres and services, and ventures with superstars will be riskier and less lucrative in an uncontrolled music environment. There are a limited number of different customer groups, and services should focus on groups interested in a more diverse market offering. At the moment only P2P services offer such diversity.

Up to now, music industry strategy towards file sharing and services such as Napster and Kazaa has been counterproductive. The notion that downloading is free (and therefore involves consumers stealing from artists and record companies) is far from correct. The annual estimated spend by consumers on downloading, in the form of feeds to telecom firms and Internet Service Providers far exceeds estimates of the record industry’s net annual revenue (income - costs).

When adapting from the current physical value chain, based on sales of CDs, to one including digital music distribution there are redundant steps. Restructuring and streamlining of the value chain is necessary in the new environment. There is also the possibility to tap informa-tion from various stages of the physical value chain and take advantage of it to create new revenue sources.

Disintermediation of steps in the physical value chain can benefit creators by bringing more independence from the industry and by creating new possibilities for distribution of their music, although this is dependent on how established the artist is. New artists will still need third parties, but need not necessarily be as dependent on the industry as today.

Landegren, J. and Liu, P. Användbarhetsfaktorer för digitala musikdistributionstjänster och deras relation till etablerade och nya värdekedjor inom musikindustrin Joakim Landegren

Användbarhetsfaktorer för digitala musikdistributionstjänster och deras relation till etablerade och nya värdekedjor inom musikindustrin

Sammanfattning Resultaten från detta arbete kommer från utvärderingar av de nuvarande tjänsterna för musik-distribution gentemot konsumenter över en längre period och också en analys av underliggan-de regler, mekanismer, teorier och åsikter inom musikindustrin för att fastställa vilka faktorer som är nödvändiga för en kommersiellt framgångsrik tjänst.

Musikindustrin har erkänt digital musikdistribution som en ny kanal men ingen av deras kommersiella satsningar har hittills varit framgångsrika. De kommersiella tjänsterna konkur-rerar med P2P-tjänster som erbjuder musik till synes gratis. Där av finns det ett stort behov hos industrin att hitta ett kommersiellt fungerande alternativ som konsumenterna kan accep-tera.

Ett antal viktiga faktorer för en kommersiell tjänst har identifierats och dessa inkluderar ett relevant utbud av musik, en tillgänglighet jämförbar med den för oskyddade filer. De inklude-rar också användarvänlighet i form av goda sökmöjligheter och logisk kategorisering samt en effektiv intäktskontroll med hjälp av alternativa intäktskällor. Andra viktiga faktorer är upp-hovsrättsregler som måste ses över och synkroniseras globalt samtidigt som det bör utvecklas ett fungerande kopieringsskydd som inte inskränker användares rättigheter men ändå har möjlighet att generera intäkter för innehållsägarna. Ny prissättning behövs för att användare ska acceptera att betala för musikfiler och prenumerationer. Eventuellt kan indirekt betalning vara den bästa modellen att genomföra dessa betalningar.

Digital musikdistribution främjar mångfald inom både musikgenrer och tjänster och sats-ningar på superstjärnor kommer inte att löna sig lika bra på en mindre kontrollerad musik-marknad. Det finns ett begränsat antal konsumentgrupperingar och tjänsterna borde fokusera på den grupp som är intresserad av ett mer varierat musikutbud och erbjuda dem ett attraktivt utbud.

Fram tills nu har musikindustrins strategi gentemot fildelningstjänster, som Napster och Kazaa, varit att motverka dem. Uppfattningen om att nerladdning av musik är gratis (som då innebär att konsumenter stjäl från artister och skivbolag) är långt ifrån riktig. En uppskattning av konsumenternas årliga trafikavgifter till tele- och Internetbolag visar att det vida överstiger skivindustrins uppskattade nettointäkter.

När man gör om den nuvarande fysiska värdekedjan som är baserad på CD-försäljning till en som inkluderar digital musikdistribution blir en del steg överflödiga och därför krävs en omarbetning och optimering av värdekedjan i den nya miljön. Det finns också en möjlighet att utnyttja information från de olika stegen i den fysiska värdekedjan för att skapa nya intäkts-källor.

Borttagning av mellansteg (disintermediation) i den fysiska värdekedjan medför ett större oberoende från industrin för musikskapare och nya möjligheter för musikskaparna att sprida sin musik, även om möjligheterna beror på hur etablerad artisten är. Nya artister behöver fort-farande en tredje part, men inte nödvändigtvis i den utsträckning som idag.

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

Acknowledgements Foremost, I would like to thank my tutor Roger Wallis for all invaluable help with providing contacts with important people in the business and also for all information sources I would not have been able to acquire myself.

This report would have looked completely different (in a negative way) without the coopera-tion and support from my friend and colleague Patrick Liu. It has been great to have the opportunity to try ideas and get opinions from another person with a similar degree of knowl-edge on the subject, not to mention how much less enjoyable the writing process would have been.

I would also like to thank the people at Svensk Musik who let me and Patrick use one of their rooms to install an office in the first stage of the thesis.

Other people I would like to thank for being helpful during the course of this thesis are Thomas Stenmo for lending me the IFPI report and the sushi bar Dosanko for keeping our stomachs full during the writing process.

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

Table of Contents

1 REPORT STRUCTURAL DETAILS AND IMPORTANT DEFINITIONS ____ 1 1.1 Chapter Overview ........................................................................................................ 1

1.2 Division of the Report .................................................................................................. 2

1.3 Weaknesses in the Report............................................................................................ 2

1.4 Important Definitions .................................................................................................. 3

2 BACKGROUND ___________________________________________ 4 2.1 History of Digital Distribution of Music .................................................................... 4

2.2 Digital Distribution of Music Today........................................................................... 4

2.3 Events in the Music Industry during the Course of the Thesis................................ 5

3 PROBLEM DEFINITION_____________________________________ 6

4 RESTRICTIONS___________________________________________ 7

5 TARGET GROUP __________________________________________ 8

6 THEORIES_______________________________________________ 9 6.1 Copyrights and Revenue Flows in the Music Business............................................. 9

6.1.1 Copyrights 9 6.1.2 Music Publishers 10 6.1.3 Revenue Flow 11

6.2 Intellectual Property Rights ...................................................................................... 11 6.2.1 History of Laws and Agreements 11 6.2.2 Digital Rights Management on Music Files 14

6.3 Economics of the Internet.......................................................................................... 14 6.3.1 Network Effects 15 6.3.2 Economies of Scale 15 6.3.3 Winner-Take-All 15 6.3.4 Lock-In 16 6.3.5 EMH – Electronic Market Hypothesis 17

6.4 Value Chain ................................................................................................................ 19 6.4.1 The Physical Value Chain 19 6.4.2 The Virtual Value Chain 20 6.4.3 The Value Matrix 21

7 METHODS ______________________________________________ 22 7.1 Evaluation of Services................................................................................................ 22

7.1.1 Selection Models 22 7.1.2 Classification Matrices 23

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

7.1.3 Evaluation Methodology 25 7.1.4 Evaluation Factors 25 7.1.5 Music Bill of Rights 25

7.2 Interviews.................................................................................................................... 26 7.2.1 Service Providers 26 7.2.2 Interest Organisations 26

7.3 External Reports, Surveys and Statistics ................................................................. 26 7.3.1 Internet Connection and Digital Music Usage Statistics and Surveys 26 7.3.2 Music Sales Figures 27

7.4 Keeping Up to Date with the MP3 News and Web Log.......................................... 27

8 FINDINGS______________________________________________ 28 8.1 Evaluated Services Findings...................................................................................... 28

8.1.1 Selected Services 28 8.1.2 Briefly Investigated Services 29 8.1.3 Overall Impressions of Pay Services 29 8.1.4 Overall Impressions of P2P and Non-Licensed Services 30 8.1.5 Differences between Licensed Services and Non-Licensed Services 30 8.1.6 Interesting Observations during Evaluation of Services 31

8.2 Interview Findings...................................................................................................... 31 8.2.1 Interviewed Services 31 8.2.2 Interest Organisations 31

8.3 External Reports, Surveys and Statistics Findings ................................................. 32 8.3.1 Telecoms’ Revenues Compared to Record Companies’ Annual Profit 32 8.3.2 Trends for Single Sales versus Album sales 37 8.3.3 Other Sales Trends 37

8.4 Study of Important Factors for a Commercial Service .......................................... 38 8.4.1 Music Selection Control 38 8.4.2 Selection Difficulties 38 8.4.3 Copy Protection, Digital Rights Management and Other Limitations 38 8.4.4 Customer Groupings 39 8.4.5 Value vs. Fee 39 8.4.6 Extra Value 40 8.4.7 Offered Selection 40 8.4.8 Revenue Control 40

9 DISCUSSION ___________________________________________ 42 9.1 Discussion of Important Factors For a Commercial Service ................................. 42

9.1.1 Music Selection Control 42 9.1.2 Value vs. Fee and Pay-Models 42 9.1.3 Copy Protection and Copyright on the Internet 46 9.1.4 Revenue Control 48

9.2 Music Industry Interests............................................................................................ 49

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

9.2.1 Current Issues Facing the Music Industry 49 9.2.2 New Possibilities in a Digital Environment 51 9.2.3 Digital Distribution Effects on the Current Value Chain 51

9.3 Bringing Together the Industry’s, Consumers’ and Creators’ Interests.............. 53 9.3.1 Conflicts 53 9.3.2 Common Interests and Possible Solutions 53 9.3.3 Connecting the classification matrices 54

10 CONCLUSIONS __________________________________________ 56

11 RECOMMENDED CONTINUED WORK _________________________ 58

12 REFERENCES ___________________________________________ 59 12.1 Literature................................................................................................................ 59

12.2 Seminars.................................................................................................................. 60

12.3 Interviews................................................................................................................ 61

12.4 Web References...................................................................................................... 61

13 APPENDICES____________________________________________ 65 13.1 Appendix I – Summary of Industry Interviews .................................................. 65

13.2 Appendix II – Summary of Interest Organisation Interviews........................... 66

13.3 Appendix III – Interview with Musicnet ............................................................. 69

13.4 Appendix IV – Interview with OD2 ..................................................................... 71

13.5 Appendix V – Interview with Morpheus ............................................................. 73

13.6 Appendix VI – Interview with Niklas Zennström............................................... 75

13.7 Appendix VII – Questions to Alan Morris (Sharman Networks)...................... 77

13.8 Appendix VIII – Kazaa Bundle Acceptance........................................................ 78

13.9 Appendix IX – Interview with IFPI ..................................................................... 80

13.10 Appendix X – Second Interview with IFPI Sweden............................................ 81

13.11 Appendix XI – Interview with SAMI................................................................... 82

13.12 Appendix XII – Interview with STIM/NCB Internet group.............................. 83

13.13 Appendix XIII – Evaluation of Musicnet............................................................. 85

13.14 Appendix XIV – Evaluation of Pressplay ............................................................ 89

1

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

1 Report Structural Details and Important Definitions

1.1 Chapter Overview Chapter 1: Report Structural Details and Important Definitions - This structural overview is meant to give brief descriptions of all chapters and clarify the structural design and correla-tions between them.

Chapter 2: Background - The introductory background covers a brief description on certain events that preceded this thesis and created the basis of some of the problems this report is trying to solve. It also gives a short summary of today’s situation with commercial services competing with Peer-to-Peer (P2P) services for the same consumers.

Chapter 3: Problem Definition – The problem definition describes what problems the record industry face and formulate the main questions to be answered by this report.

Chapter 4: Restrictions – Restrictions include all the restrictions made when choosing services to evaluate.

Chapter 5: Target Group – It explains what kind of readers the thesis is aimed at and what basic knowledge is needed for a good understanding of the material.

Chapter 6: Theories – The theories chapter include some theories that are of importance for an understanding of both the economic and commercial factors that are valid for digital distribu-tion of music. This includes an explanation of copyrights, intellectual property rights, economics of the Internet and the value chain concept.

Chapter 7: Methods – Methods gives an overview of how the evaluations and interviews of different services, creators and organisations were performed and what other research material has been used in the thesis.

Chapter 8: Findings – The findings have been structured into four subchapters where the first three have correspondent subchapters in the methods chapter. The methods chapter describes how the findings are achieved, and the findings chapter consequently displays what findings are achieved. From these findings several factors of importance for a commercial service are obtained and then presented in the fourth subchapter.

Chapter 9: Discussion – In the first subchapter of the discussion all the retrieved factors from the findings are discussed in accordance with theories from the theories chapter and other observations from the research. The subsequent subchapter gives a summary on the industry’s view of an attractive service, and in the last subchapter I try to bring these views together with the consumers’ and creators’ viewpoint presented in Liu’s report1 and find common interests and complications for all three parties.

Chapter 10: Conclusions – Conclusions presents the results and conclusions of this thesis.

1 LIU, P. “Usability Factors in Digital Distribution Services for Music - A Study of Online Distribution Services Today, Identification of Important Factors for an Attractive Service, the Interests of Consumers and Music Creators”

2

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

Chapter 11: Recommended Continued Work – Recommendations include suggestions of possible subsequent work in the same area of interest as this thesis.

Chapter 12: References – Here all references from literature, interviews and web sites used will be collected.

Chapter 13: Appendices – The appendices will include complete transcripts of interviews and some outsourced evaluations of Pressplay and Musicnet.

1.2 Division of the Report This report is closely related to Patrick Liu’s thesis2 since we have performed the research together and achieved the same findings. From these findings we have treated the information differently and achieved different results and conclusions depending whether we look at it from the consumers’, creators’ or the industry’s interests.

Because of the above mentioned fact many chapters are common for both reports. Below are all chapters that are unique for this report. Remaining chapters are also included in Liu’s report.

6.1.2-6.1.3; 6.3; 7.2.1; 8.2.1; 8.4.1-8.4.2; 8.4.8; 9.1.1; 9.1.4; 9.2; 13.1; 13.3-13.5; 13.7-13.8

The theory chapter (chapter 6) has a clear separation of what subchapters have been written by whom while the methods, findings, discussions and conclusions chapters (chapters 7-10) are written in cooperation. Subchapters 6.1.2-6.1.3; 6.3-6.4 are written by Joakim Landegren, and subchapters 6.1.1 and 6.2 are written by Patrick Liu.

The intention is to bring together all material in one report later including all three players’ different views for a more complete picture of the problems involved.

Since most research and literature studies have been made together with Patrick Liu this report often refers to the author as “we”. This definition includes both me and Patrick since we have cooperated in acquiring and extracting the information.

1.3 Weaknesses in the Report Unfortunately, representatives from several of the services have been disinclined to partici-pate in interviews, and other contacts that did participate have been very restrictive with their answers to highlight themselves and not leak any negative information. We have chosen not to rely much on these interviews since their impartiality and relevance can be questioned. Most information of interest was omitted in the answers.

Another complication is that the music business currently experiences lots of changes on almost a daily basis and some events mentioned in this report might be inaccurate at the time of reading because of this fact.

Information concerning the music industry has been acquired from a large number of different sources. Same figures from various sources vary and we have chosen the information source we believe is the most reliable in consultation with our tutor Roger Wallis. 2 LIU, P. “Usability Factors in Digital Distribution Services for Music - A Study of Online Distribution Services Today, Identification of Important Factors for an Attractive Service, the Interests of Consumers and Music Creators”

3

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

Because of limited resources (funds and time) user downloading behaviour figures have been taken from other companies’ studies and are not always exactly accurate for the desired purpose. A user survey could have revealed more accurate figures for the study on telecoms’ revenues made in chapter 8.3.1, but to get any statistically relevant information the number of users included would require a lot more resources than what was available.

1.4 Important Definitions There are a few terms used in the thesis that might need to be clearly defined since they are words often used in media but the meaning of the words is often very broad.

Free music – P2P file sharing is often claimed to be “free” but as shown later on in the report this is a false statement. There are very many revenue sources from P2P but not to the record companies, and consumers do not pay directly for the downloaded music but indirectly through other channels such as Internet Service Providers (ISPs).

Illegal – P2P services are often called “illegal“, but they are not illegal until convicted by a court. The definition of who carries the responsibility for illicit downloading has yet to be made.

Legal – The term “legal service“ is mentioned at several occasions in the thesis and it refers to a service run by the major labels or at least including licensed material from them.

Piracy – Piracy is a word frequently used especially in connection with statements from the recording industry. This term is not used in this thesis, other than in quotations, since we believe there is a considerable difference between a technology-loving teenager and an illegal CD-copying factory producing thousands of illegal copies to sell on the black market. Thus the term piracy should be applied on the organised illegal CD manufacturing for a commercial purpose and not to P2P.

There are some terms mentioned that have the same meaning. User and consumer are both commonly used in the thesis and refer to exactly the same group of people, i.e. the people consuming music. Creator, composer and songwriter are also synonyms for the originator of the musical works. In reality these terms refer to originators of music from different genres but that difference is of no importance in this thesis. An artist or performer also included in the definition of creator when speaking about creators’ interests but not when dealing with copyrights and revenues. In that context artists are subject to other legislation and rules.

Mainstream – Mainstream music is popular music that is on different hit lists and top-ten-charts and can be found in nearly all music retail stores.

Telecoms – This definition includes both telephone companies and ISPs and is often used in conjunction with revenues from P2P downloading. In that context telecoms include both the players providing the physical network and the companies responsible for Internet traffic in the network.

Digital distribution – The term digital distribution is often used in the thesis and is actually referring to digital online distribution since we only deal with services operating over the Internet.

4

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

2 Background

2.1 History of Digital Distribution of Music The idea of digitally distributed music on the Internet was started by Jeff Patterson and Rob Lord with the Internet Underground Music Archive (IUMA), using the proprietary audio compression format MP3. The idea was picked up by others and distribution via other websites and ftp-sites began appearing3. It was nothing big, and for many years the music industry did not care much about the websites. A few established bands picked up on the idea (Grateful Dead among them), and even more underground bands caught on the idea. A few tried commercial efforts, but nothing really came out of it. Some key persons went to the big record companies with proposals, but no one actually acted on it. The music industry did not seem very interested at all, until they were forced to look into this new uncharted area.

The digital distribution system that startled the music industry was Napster, having something between 40 and 70 million users trading music in MP3 format. The estimation of the number of users varies very much depending on the source. But no matter what the exact number was, it was a significant number of users swapping files. File-swapping created a massive value in itself, both by teaching consumers new ways of appropriating music, and generating massive traffic for telecoms.

The industry reacted negatively, and attacked Napster by legal means. Established artists were split between the parties, and the Recording Industry Association of America (RIAA) has since had their hands full. After a few years Napster was finally closed down. Shortly after Napster was closed down a flood of new decentralised networks arose, most notable Gnutella and Fasttrack and all Peer-to-Peer clients together today, such as Kazaa, are building net-works larger than Napster ever was. At a certain point the industry realised they had to counter the P2P networks with their own services, and the majors developed new digital distribution services.

2.2 Digital Distribution of Music Today Today there are numerous P2P networks and even more clients. Some have been around for very long, in the current context and others emerge and fade away rather quickly. Users adopt and change new ways of trading files relatively quickly. The P2P networks are huge and it is possible to find virtually everything from movies, music and computer software to books in these networks. All can be downloaded for free, apart from the cost of being online. The downloaded material and the connections are not always reliable, but a lot of consumers apparently think it is worth the effort.

There are few large legal services today, and all of them are centralised. Pressplay and MusicNet are the ventures of the five major record companies. Rhapsody is another service that provides a large selection of music from the major companies. There have been very few services offering music from the majors, but the number is now increasing. All of the above services use a subscription model for providing the music, with the addition of buying additional separate tracks and albums for burning.

3 ALDERMAN, J. Sonic boom – Napster, MP3, and the new pioneers of music

5

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

Most other services provide independent or underground music. MP3.com is an exception that also offers some larger artists, but only single tracks for marketing.

Internet radio stations have also caught the industry’s attention, since most of them are independent stations broadcast by individuals without a license. Most are not commercial stations, but still do not have the industry’s consent to broadcast.

2.3 Events in the Music Industry during the Course of the Thesis The music industry is moving very fast, and during the course of this work a lot of the condi-tions on the music market have changed. For example Pressplay, MusicNet and Rhapsody all have made great progress in increasing the size of their music selection and what is allowed in the agreements for downloading. Below are headlines in chronological order of a few P2P-related events from the last six months:

- October15th 2002: Songspy is closed down after a lawsuit.

- November 1st 2002: Court orders Madster to implement filtering technologies.

- November 6th 2002: BMG and EMI independently plan to only have copy-protected CDs in the future.

- November 8th 2002: New disc format announced with built-in copy protection.

- December 3rd 2002: Madster told to pull the plug.

- December 11th 2002: Canadian government subsidizes DRM, and decides to intro-duce a levy on CD media.

- December 14th 2002: Record companies pay for inflated prices. They were uncovered earlier that they have had a cartel to force higher prices on CD. They were convicted in court and have to pay back to buyers and/or donate huge sums to charity.

- December 23rd 2002: New Danish law prohibits music copying to MP3 format.

- January 3rd 2003: European copyrights expiring on recording from 1950’s. That means anyone can publish old recordings without having to ask for permission from the composer first.

- January 17th 2003: Apple silences iTunes P2P software.

- January 17th 2003: IFPI employee describes P2P sabotage activities. The industry is exposed trying to sabotage P2P networks with various methods.

- January 18th 2003: Rosen want to impose a type of fee on Internet Service Providers (ISP).

- January 18th 2003: Microsoft introduces CD copy protection ‘fix’. MS offers a new type of copy protection method that the industry finds quite attractive.

- January 22nd 2003: Rosen will step down as head of RIAA.

- January 31st 2002: EC proposes new antipiracy rules. The new rules are aiming at illegal copying for commercial purposes, and tones down the copying of individuals.

6

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

3 Problem Definition The music industry today finds itself increasingly worried by the increasing number of Peer-to-Peer (P2P) users. Millions of people download music without any direct revenues for record companies or content owners. There have been efforts from the industry to compete with the P2P services but no commercial service has been very popular among consumers so far.

There have also been attempts to stop P2P downloading but we believe that it is impossible to stop these activities completely. The industry must find a way to live alongside P2P and exploit its possibilities instead of its disadvantages.

That leads to the two main questions for this thesis:

What factors are of importance for a commercial service that appeal to all parties involved (consumers, creators and the industry)?

How can economic efficiency be maximised for both music creators and the music industry in a digital environment?

7

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

4 Restrictions In order to limit the scope of this thesis to a reasonable level, several restrictions listed below have been made.

• This thesis only deals with services specialised in distribution of music. Studies of Peer-to-Peer services will be limited to those functions related to music files.

• The evaluated services all have a target group consisting of ordinary music consumers. In some cases, for example OD2, the service itself is focused on other businesses, such as Internet portals, but the actual end users of the service are the consumers visiting the portal.

• The service evaluations are based on minor case studies of a selected sample of services that have been selected according to certain criteria described in the Methods section below.

• The sample of services is restricted to those whose distribution occurs over the Internet. The distribution occurs by transfers of files or as a digital transport stream (i.e. real audio streaming). No services providing mainly distribution by tangible products (CDs) are studied.

8

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

5 Target Group This thesis is mainly of interest for people at record labels or new distribution services that need distilled and evaluated information of the recent changes in the market compiled and reviewed in one report. It is also aimed toward university students at Media Technology and Graphic Arts at the Royal Institute of Technology, or students with a special interest in digital distribution. Many terms and abbreviations used are implied that the reader understands and is well familiar with.

9

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

6 Theories The theories below are needed to get a deeper understanding of how users behave and how business optimisation works in a digital environment.

6.1 Copyrights and Revenue Flows in the Music Business Below is a short explanation of the copyrights and revenue flows in the music business today.

6.1.1 Copyrights Publishing Rights Each time a songwriter creates a new piece a publishing right is created, representing the composer’s ownership of the music. Any subsequent use or exploitation of the piece requires a payment to the owner of these rights. The publishing rights must not be owned by the actual composer but can be sold and transferred to a new owner. Publishers often design contracts so that artists or composers must give up shares on their publishing rights when signing the contract. In exchange they get money in advance for past, present or future material.

Mechanical Royalties Whenever a song is reproduced by a mechanical device you have to pay a mechanical royalty. Even though this term’s validity is somewhat diminished with introduction of digital equip-ment it still refers to royalties for reproduction of songs reproduced on devices sold on a unit basis. This includes CDs, audiocassettes, audio greeting cards etc. File downloads is a special case where the rules and tariffs still are under development according to Maria Wande at STIM4. Today they have divided the royalties for file downloads into one mechanical royalty part when the first reference file is created, and one performance part where every subsequent download is treated as an Internet performance and hence performance tariffs apply5.

Synchronisation License Synchronisation licenses are used when songs are used together with a visual image. Music publishers issue synchronisation to for example TV advertisers, motion picture companies, video manufacturers and CD-ROM companies. Usually about 50% of the net proceeds are paid back to the songwriter.

Transcription License Because radio is not a visual medium synchronisation licenses do not apply. For songs used in radio commercials there are instead transcription licenses that correspond to synchronisation licenses.

Public Performance Royalty An exclusive right of the copyright owner is to authorise public performances of the copy-righted work. Thus radio and television broadcasters must acquire licenses from interest organisations such as STIM in Sweden and ASCAP in the USA. Performance rights organi-sations like those then collect incomes on behalf of the songwriters when songs are publicly

4 Interview with Maria Wande, STIM (Appendix XII) 5 Interview with Tobias Eltell, SAMI (Appendix XI)

10

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

broadcast. Even though publishers do not collect any income from performance rights they are still entitled to a big share of the income from those organisations.

Exploitation of Rights Rights can be divided in several components for a more lucrative exploitation of the rights. A possible division is shown in Figure 1 below. A more concrete example is a local distributor in Germany that can be assigned the rights to distribute the CD and cassette version of a certain track for a five-year period in the German market.

International Agreements To simplify licensing of music internation-ally, and on the Internet as a global net-work, the Santiago agreement was estab-lished during the CISAC Congress 2000. In short it means that the collecting society in each country is the licensor for all music licensed in their respective countries. Licenses granted to content providers are then global on a non-exclusive basis, and the applied tariff is the one used in the country where the material is published. The revenues are then distributed between each country’s collection societies.

6.1.2 Music Publishers Music publishers’ role in the past was to

publish sheets of music from a composer6. Publishers have a less important role today but continue to perform several functions in the music business, such as administering copyrights, licensing songs to record companies and collecting royalties for the composers.

Publishers may also help promising artists to record demos and assist in the process of acquiring a record deal. In return they most often get shares of the mechanical royalties or public performance royalties.

Foreign countries often have different laws on music distribution and licensing and hence another role of the publisher is to enter into agreements with foreign publishers to collect mechanical royalties in that particular region. Publishers often have their own network within different countries and can much easier than the artist strike a profitable deal with the local publishers.

6 KORN, A. http://www.alankorn.com/articles/publishing_1.html

Figure 1. Exploitation of rights

Territory

Medium

Time

11

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

6.1.3 Revenue Flow In order to better understand the current revenue system a visualisation might help. Figure 2 shows a map7 of the revenue generation before Internet made its impact, thus excluding revenues from digital distribution.

6.2 Intellectual Property Rights The relevance of Intellectual Property Rights (IPR) in this report is to briefly cover how pricing and copy protection of music in digital format works. IPR is a fairly wide term including musical work amongst others, and it is of use when looking into licensing issues, pricing and protection of the files.

6.2.1 History of Laws and Agreements Most experts agree that legislation has had difficulties keeping up with the development of technology. A few years back legislation was far behind technology, but the last few years much work has been done, not least international agreements that apply to digital distribution. A problem that now arises is to enforce the new laws, and the public is slow in adapting new laws, especially when law enforcement on the Internet is virtually impossible8. One reason for this is that the public is not informed about the specific rules that apply to music on the Internet. Laws on itself will not help much. They have to be enforced by some sort of tools, such as DRM technology. Below is some history of the laws and agreements that are today. Most of it began in the US, and the US has also experienced the most radical changes, far more extreme than the international treaties.

The first IPR organisation is the 1967 World Intellectual Property Organisation (WIPO) that administers, amongst other agreements, the 1886 Berne Convention. In 1991 a major revision

7 KLIMIS, G.M. March. Disintermediation and Re-intermediation In the Music Business – the Effect of Multimedia Technologies and E-commerce 8 Interview with Maria Wande, STIM (Appendix XII)

Sales of tangibles to wholesailers

and retailers

Radio, TV performance

Music used in films or TV

commercials

Recorded music used by licensees

or record clubs

Music publishing “the song”

Recorded music “the recording”

Royalty

Mechanical license

Synchronisation license License

Royalty

Performance rights

Royalty Royalty

Sales

Revenue

Figure 2. Revenue generation in the music industry before digital distribution

12

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

was planned, but its negotiations failed for several years until 1996 when a treaty was agreed on, the 1996 WIPO Treaty, which directly addressed digital information.

The US The US had in 1992 introduced the Audio Home Recording Act to adhere to the Berne Convention. The Audio Home Recording Act requires levies on recordable media, and tech-nology in media to prevent serial copying (Serial Copy Management System). It has since been successful in implementation only on DAT tapes, which in turn never became very wide spread. The Act was brought up when MP3 players began to sell (the Diamond Rio case), and also in the case of CD burners. It has not yet been very effective. The Diamond Rio player won the case, with the argument that the device does not directly copy music, but data from a computer and thus they are considered parts of computers. Though, after the case Diamond freely agreed to cooperate in development of new protections.9

The US did not allow public performances in sound recordings, unlike most other European countries. That caused a problem when streaming on the Internet was considered perform-ances and not reproduction, so it was solved with the Digital Performance Right in Sound Recordings Act in 1995.

The EU The EU has since 1994 had the Rolling Action Plan (RAP) where copyright is but one of several issues addressed. When making a transfer from traditional physical media to the Internet it involves new actors that have no experience in copyright issues, such as Internet Service Providers (ISP) that are addressed by the RAP. There are a number of directives in the EU that already applies to digital distribution, although they were not created for these purposes.

The Rental and Lending Directive in 1992 provides a legal framework for cross-border trans-missions in a digital environment. The Term Directive in 1993 and Database Directive in 1996 also provide protection for phonogram producers and on-line databases. Most executive work is done in the member states, though.

In 1997 the draft Copyright Directive was presented. Compared to the US these rules were more general and open for interpretation. One of the most central issues was liability. After some reworking some rules for liability were made and the main points of it were setting different levels of liability depending on how the service providers stored the data. Intermedi-ary providers could not be liable. Cachers would need to send out notices to users and remove illegal data. Lastly, hosts need to actively find and remove illegal data. There still needs to be some clarification of how to define for example “caching” and “storing”. Another problem in the EU is that all member states have their own rules, and are not always willing to change in favour of the directives from the EU.

The enforcement part of the Copyright Directive was presented through the 1998 Green Paper on Combating Counterfeiting and Piracy in the Single Market. The same year the Condition Access Directive was adopted, which resembles the DMCA (Digital Millennium

9 MIDEM 2000. Legal and Commercial Effects of Digitisation on the Music Industry: Snapshot of Current US Legislation, Midem 2000

13

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

Copyright Act, see below) rule of circumvention of copy protection, but is not equally specific.

Just recently the European Commission has proposed a new rule for intellectual property right enforcement that does not impose sanctions against individuals downloading music for non-commercial purposes. They only focus on copyright infringements for commercial purposes. P2P services would fall under the latter case because of advertisements in the clients.

1996 WIPO Treaty The first initiative that directly addressed digital information (in the US) was the National Information Infrastructure Task Force by the Clinton administration. Roughly explained it wanted to protect and control all information on the Internet on economic grounds, which sounded very good to the industry. It also addressed the issue of digital transmissions claiming to be performances. One much criticised rule was the new chapter that would prohibit any device that in any way, direct or indirect, would facilitate copying of any material. It was criticised because it would include anything ranging from encryption tech-nologies to sealed envelopes, and also all transitory storing such as the random access memory (RAM) and cache in computers. The US wanted to extend the later NII White Paper to an international treaty, which they brought forth in the 1996 WIPO Treaty. It ended up with a compromise - a quite unspecific formulation open for interpretation and free for the parties to implement: “…provide adequate legal protection and effective legal remedies against the circumvention of effective technological measures that are used by authors in connection with the exercise of their rights inter this Treaty or the Berne Convention and that restricts acts, in respect of the their works, which are not authorised by the authors concerned or permitted by law.”

1998 Digital Millennium Copyright Act However, the US went on making their own bill, the Digital Millennium Copyright Act that followed the previous White Paper more closely since the 1996 WIPO Treaty only provided minimum requirements. The problem here is that legislation only applies in the US. The DMCA has been strongly criticised, not least for the fair use issue (discussed later). The DMCA is now under revision.

Secure Digital Music Initiative When portable MP3 players were introduced, the RIAA set new rules that would apply to this group of players and the Secure Digital Music Initiative (SDMI) was born in 1999. The purpose was to develop specifications for secure digital distribution of music, and enable new legitimate business models in electronic music distribution. It also meant to improve dialogue between interested industries such as the music, IT and consumer electronics industry to name a few.10 The standards were going to be open, optional and interoperable between all partici-pants.

The SDMI has been working well so far. Very quickly they set up and implemented the so called Phase 1. Practically Phase 1 meant that all devices had a certain degree of copy protec-tion enabling reception of any file, including pirated, but not file transfers from the device. Phase 2 meant to fully use copy protection on new music with a copy protection flag, but it still allows illegal files. In practice, it has had a minor impact on the market. The Secure 10 MIDEM 2000, Infringement of Rights in Sound Recordings in the Online World and IFPI

14

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

Digital format has for example had fairly successful penetration amongst consumers but is hardly any effective copy protection since most consumers are trading unprotected files.

Internet Radio Royalty Rates The main legislation for Internet radio has been done in the US (as most other Internet legis-lation). During spring 2002 the CARP and Library of Congress set new webcasting royalty rates, by recommendations from RIAA. The new rules were very unfortunate and would bankrupt most small Internet radio stations because of set rates. A lot of work has been done since, amongst them the Internet Radio Fairness Act, and just recently the Small Webcaster Settlement Act, that sets a royalty rate based on percentage of revenues that is fairer to small webcasters. So far the legislation for Internet radio seems to be going toward a more reason-able state.

6.2.2 Digital Rights Management on Music Files Digital Rights Management (DRM) is an overall name for technology systems for protecting digital material, such as books and music. All majors’ services are using some kind of DRM, and different companies develop different technologies, incompatible with each other. Examples of companies offering DRM-protected music are Microsoft, LiquidAudio and Real.

A DRM protected file is encrypted and registered in a database, and is independent of where it is used. Every usage of the file sends a license check through an online database query and if the use is authorised the file will work, otherwise it is useless. Encryptions have been hacked, but continuous updates of the licenses are supposed to counter hacking attempts. DRM also enables tracking of file source, owner, contents and more.

The DRM system limits the music files in several ways. Firstly there is a time limit on every piece of music. For example the license is only valid as long as there is a subscription. When the subscription has ended, the next time the license is updated the music will stop working. Secondly the files are limited in media (sound carriers). For example they mostly only work on the computer where the files are downloaded, although moving to other computers is possible. And they cannot be moved to other portable players or burned to CD unless an additional fee is paid. Read more about limitation of copyrighted material in chapter 6.1.1.

6.3 Economics of the Internet Chapter 6.3.1 through 6.3.4 all include theories for economics of the Internet described by Liebowitz11. He states that the principle of value creation on the Internet is merely a lowering of the cost of transmitting information. That is in fact all Internet does, not saying that it is not an immense advancement in scientific evolution. But Liebowitz also emphasizes that infor-mation transmission does not change the laws of economics and that the laws described below still are valid on the Internet.

11 LIEBOWITZ, S. Re-thinking the network economy: the true forces that drive the digital marketplace

15

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

6.3.1 Network Effects “A network effect is present when a product becomes more useful to consumers in proportion to the number of people using it.”12 A telephone, for example, is useless unless there are other telephones to communicate with and thus telephones display network effects. There are other less obvious so-called virtual networks such as all the users of WordPerfect13. If the cost of a single copy of WordPerfect increases accordingly with the number of total users then Word-Perfect would be said to embody network effects.

Network effects definitely exist but their effect is often overestimated and the results of this overestimation can be quite fatal. There are plenty of examples of this during the early stages of Internet where companies raced and spent enormous amounts of money to be first with establishing a huge network of customers since the theory of network effects yields a higher profit for a bigger network. For this business model to succeed you must ensure a lock-in of the customers as described below. The burst of the IT bubble shows that this is in fact not the way markets have worked.

6.3.2 Economies of Scale The theory of economies of scale implies a decrease of average costs with an increase in number of sales and size of the company. Almost all manufacturing shows some economies of scale. But at some point there are other components of the production costs that replace the economies of scale and raise the average costs as output increases. Computer software is a very good example of a product that exhibits economies of scale. The cost of developing the software is high and fixed since it is independent of the number of copies sold. The duplica-tion and shipping costs are close to zero and will thus lower the average costs the more copies are sold. Economies of scale and network effects both have very similar impacts and profit a company with a large customer base, but economies of scale are frequently going to be more significant of the two, according to Liebowitz.

6.3.3 Winner-Take-All As mentioned above, the theories on network effects and economies of scale both benefit large companies in favour of small ones. In a scenario based only on these theories there would naturally evolve a single competitor taking hold of the market as a result of its economic advantages. This was referred to as increasing returns (of scale) and was usually thought to lead to winner-take-all results, especially since economic theories often tend to view products from different vendors as identical.

Increasing returns, however, was incompatible with the observation that most industries consist of far more than a single dominant company. It was also incompatible with one of the fundamental assumptions in economists’ basic model of competition pointing out the ideal of having many competitors in a market. Liebowitz means that a winner-take-all situation might be the outcome when large companies benefit from cost advantages that small companies do not, but it does not have to be the outcome. One important factor is the actual differences between products that appeal to different groups of customers. 12 LIEBOWITZ, S. Re-thinking the network economy: the true forces that drive the digital marketplace 13 A word processor application by Corel.

16

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

Another factor that is thought to contribute to winner-take-all results is instant scalability, meaning the ability of a company to instantly change its products to meet market demand. This is the case when the production process involves non-specific inputs. Once again computer software serves as a good example because it requires machinery for duplicating CDs but these machines are the same independently of the software copied to the CD. The same machine that copies Microsoft Office can instantly switch to copy Microsoft Windows instead.

6.3.4 Lock-In In a market where the winner-take-all theory is applicable there is the possibility of a rapidly changing leadership whenever a better product enters the market, but lock-in implies that the winner not only takes hold of the market, but also keep doing so even though more attractive options are available for the customers. The reason for this is mainly due to network effects that help creating a winner-take-all situation and then support the winner by creating coordi-nation difficulties as described under strong lock-in below.

Compatibility is a key word when dealing with lock-in concepts. When consumers make their choice of what brand to buy they have already made several calculations (consciously or not) whether the new product is worth buying or switching to and in network markets they also have to consider the strength of the new network. An example is consumers choosing between BETA and VHS in the 1980s. For them it might be very important to choose a VCR with the most common format the video store keeps in stock to get a good selection of movies to choose from.

Lock-in costs can be separated in two types. First there are costs for familiarising and relearning old habits when switching product. This also includes being able to use your old work with the new product and could be said to be the cost of being compatible with one’s self according to Liebowitz. The other costs originate from an eventual loss of compatibility with others. If all your colleagues use Microsoft Word, for example, it is more difficult to exchange documents if you switch to WordPerfect.

The two factors, being compatible with others and being compatible with one’s self, are fundamental to Liebowitz distinction between strong and weak lock-in. Unlike the weak form of lock-in, the strong form supports the concept of first-mover-wins where the first company on the market will be able to stand ground against all competitors (even a better product) because of the consumers’ reluctance to switch.

Strong Lock-In Strong lock-in exists when a switch to a superior product is not adopted even though self-compatibility issues can be overcome by the superiority of the product. The reason for the consumer not switching in such a case is the fear of losing compatibility with others. What is most important if strong lock-in exists, as said by Liebowitz, is to get hold of a majority of the consumers first, even though the costs are very high, since the competitors will have difficul-ties in getting the consumers to switch to their product irrespective of its eventual superiority.

Except compatibility it is also a question about the consumer’s assumption of other peoples’ continued use of the product. It is actually the expectation of the network size that matters. The actual market shares are irrelevant if the consumers believe that the product will do well. Otherwise products such as the telephone never would have been if no one had believed that this was a product that people would buy.

17

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

Weak Lock-In If a company produces a product that is superior to the incumbent but not superior enough to make up for the self-compatibility costs of switching to the new product you can say that the consumers are weakly locked-in to the incumbent. Unlike strong lock-in, the weak lock-in concept has nothing to do with network effects or economies of scale.

There are many different examples of weak lock-in, e.g. you do not want to buy a new computer a few months after buying your last one even though the new computer is slightly better. This example together with lots of others offers some protection for the incumbents.

Liebowitz mentions one final difference between the two forms of lock-in. It is economically efficient with weak lock-in because learning costs are real and weakly locked in consumers will switch product but not until the new product is sufficiently better to make it economically beneficial to do so. Strong lock-in on the other hand, will make the consumers stick to the old product unless all other consumers switch product as well. If that was the case all would be better of even after switching costs were included.

6.3.5 EMH – Electronic Market Hypothesis In his PhD14 Klimis refers to the Electronic Market Hypothesis (EMH), first introduced by Malone, Yates and Benjamin in 1987. It offers a theory that can be used as a base for predicting scope and evolution of electronic markets.

There are some important definitions to make to clarify the hypothesis. First there is the use of the terms production costs and coordination costs. Production costs include costs from all the physical or other primary processes necessary for creating and distributing the goods or services being produced, and coordination costs result from all the information processing necessary to coordinate the machines and people working with the primary processes.

Two other important terms are markets and hierarchies that are the two mechanisms of economic transaction coordination. Both represent two ends of a continuum of relationships that can evolve from a computer-mediated environment. The polarisation between these two coordination mechanisms can be observed in

Table 1. Hierarchical coordination means that a single authority such as a company manager controls the value chain activities, and thus product and service attributes are set by managerial decisions rather from open market selection. Hierarchical control supports long-term relationships in favour of quick and impulsive transactions. Markets, on the other hand, work on a transaction-to-transaction basis and the flow of goods and services through the value chain is coordinated by a decentralised price system. Assuming a situation with perfect market information, buyers make their purchases from the seller that offer the most attractive combination of price, quality and other attributes.

As seen in

Table 1, markets maximise the search costs since there are a multitude of products offered from different vendors to search through when looking for a product of choice. A hierarchy

14 KLIMIS, G.M. March. Disintermediation and Re-intermediation In the Music Business – the Effect of Multimedia Technologies and E-commerce

18

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

gives the buyer only one choice of product and thus minimises the search costs but it is not necessarily the best or cheapest product available.

Coordination through markets Coordination through hierarchiesNo of vendors Maximum OneSearch costs Maximum MinimumBuyer's choice Wide Limited

Table 1. The Two Coordination Mechanisms

Malone et al.15 summarise relative costs for markets and hierarchies in Table 2 below. They mean that the production costs in the physical domain fall and coordination costs rise with an increasing number of competitors for a hierarchy.

Organisational form Production costs Coordination costsMarkets Low HighHierarchies High Low Table 2. Relative Costs for Markets and Hierarchies

From this table you can assume that lower coordination costs in a market would make the markets prevail as an economically efficient organisational form, or similarly that lower production costs for hierarchical organisation would make hierarchies prevail. The EMH predicts that since Information Technology and Internet lowers coordination costs by making information flows very fast and efficient this will result in an overall shift from use of hierarchies to markets as the basis of economic activity. Klimis also refers to Rayport and Sviokla16 who predict such a large effect of computer mediated transactions that eventually a disruption of many activities in the current value chain is due.

Three characteristics that Klimis distinguish as vital for a lowering of the transaction costs already apply to the electronic market and they are:

1. There are always alternative suppliers and buyers

2. Information is freely available

3. Opportunism due to bounded rationality is prevented

Two other factors that affect and encourage market transactions are low asset specificity and low complexity of product. By low asset specificity and low complexity Malone et al.17 means a product that is not specifically made to suit a certain target group or a product whose content is very easily understood, i.e. a wide range of people can use it. Music is a very good example of such a product.

15 MALONE, T. YATES, J. AND BENJAMIN, R. 1987. Electronic Markets and Electronic Hierarchies, Communications of the ACM 16 RAYPORT, J.F. and SVIOKLA, J.J. Exploiting the Virtual Value Chain 17 MALONE, T. YATES, J. AND BENJAMIN, R. 1987. Electronic Markets and Electronic Hierarchies, Communications of the ACM

19

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

6.4 Value Chain Michael Porter first introduced the concept of a value chain18. It enables a visual separation of the company’s activities into the technologically and economically distinct parts it is com-prised of. Porter also introduced an embedding of the firm into a value system that include all the players that create value both upstream and downstream the value chain. The primary use of the value chain is to create a limited number of functional bins into which the firm activities could be categorised.

This native value chain has been criticised to be very linear and that it resembles a Fordian assembly line19 and that many of the dynamics of the firm is lost on this linear visualisation. The value chain has, since its introduction, been extended to better suit the actual market. An extension of great importance for this thesis is the treatment of information as value given that digital distribution of music is technically a transfer of information. This will be more thoroughly described under the virtual value chain section below

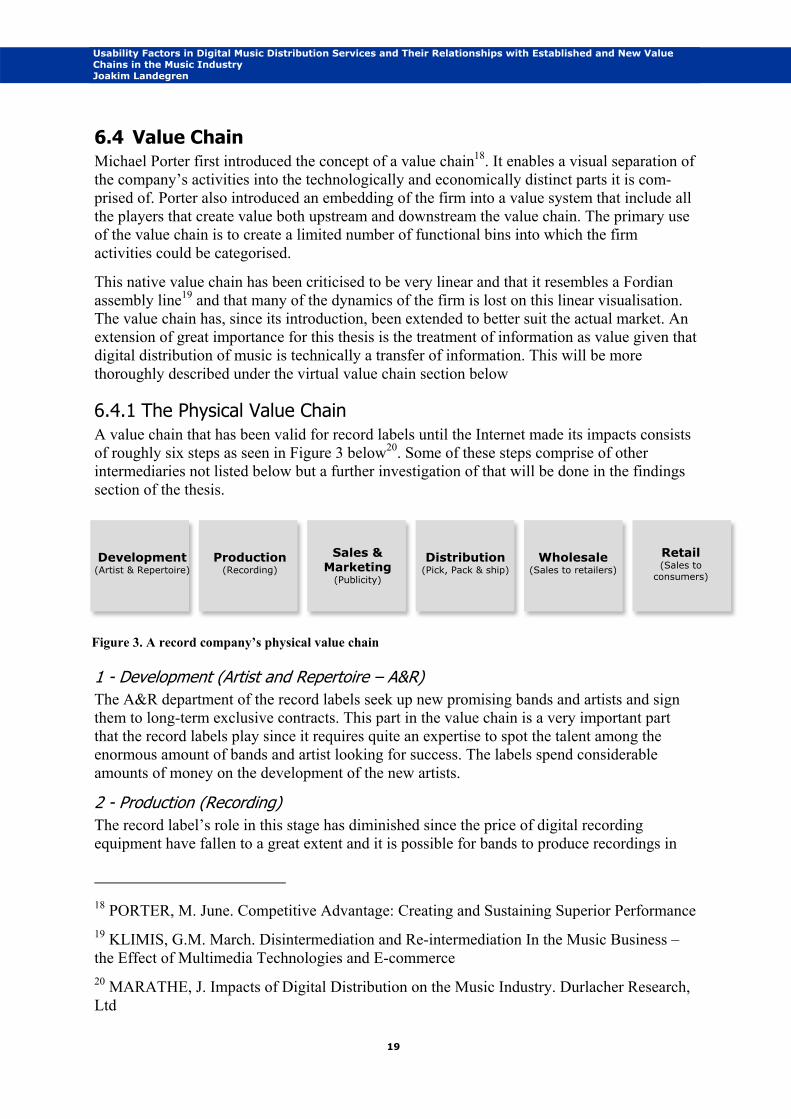

6.4.1 The Physical Value Chain A value chain that has been valid for record labels until the Internet made its impacts consists of roughly six steps as seen in Figure 3 below20. Some of these steps comprise of other intermediaries not listed below but a further investigation of that will be done in the findings section of the thesis.

1 - Development (Artist and Repertoire – A&R) The A&R department of the record labels seek up new promising bands and artists and sign them to long-term exclusive contracts. This part in the value chain is a very important part that the record labels play since it requires quite an expertise to spot the talent among the enormous amount of bands and artist looking for success. The labels spend considerable amounts of money on the development of the new artists.

2 - Production (Recording) The record label’s role in this stage has diminished since the price of digital recording equipment have fallen to a great extent and it is possible for bands to produce recordings in

18 PORTER, M. June. Competitive Advantage: Creating and Sustaining Superior Performance 19 KLIMIS, G.M. March. Disintermediation and Re-intermediation In the Music Business – the Effect of Multimedia Technologies and E-commerce 20 MARATHE, J. Impacts of Digital Distribution on the Music Industry. Durlacher Research, Ltd

Figure 3. A record company’s physical value chain

Development (Artist & Repertoire)

Production (Recording)

Sales & Marketing

(Publicity)

Distribution (Pick, Pack & ship)

Wholesale (Sales to retailers)

Retail (Sales to

consumers)

20

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

home studios or at least record and produce their CDs much cheaper than before. The labels finance production and often provide an advance payment for signed bands at this stage.

3 - Sales and Marketing (Publicity) The labels have a well-established relation with music stores and media channels such as press, radio and TV stations. Through these relations they are able to work out profitable sales and promotion deals. The label decides the amount of promotional spent on a single or album according to its potential popularity and profitability.

4 - Distribution (Pick, Pack and Ship) This stage of the value chain is quite different for a major label compared to an independent label. The majors often have a global network of branch offices that can handle sales, distribution and marketing issues and sometimes they even own the distribution channels as well. Independent labels, in contrast, have to license local distributors.

5 - Wholesale Distribution companies most often work towards the big retail chains and to some of the smaller chains dealing with large quantities. Because of the quantities smaller shops can have difficulties with striking a profitable deal and thus they make their purchases from a whole-saler to avoid being forced to buy a minimum amount of CDs from the distributor.

6 - Retail Retailers place their orders at the wholesalers as and when the albums and singles are required. The music is then sold to the consumers.

6.4.2 The Virtual Value Chain

Rayport and Sviokla21 mean that almost every business today competes in the virtual world of information as well as the physical, and thus has to create value in both worlds accordingly. But the processes for value creation work are not the same for both worlds. Value creation in any stage in a Virtual Value Chain (VVC) involves a series of five activities: gathering, organising, selecting, synthesising and distributing information as seen in Figure 4 above.

They claim that every company observed have adopted value-adding information processes in three stages. In the first stage, visibility, companies use information to acquire ability to overview their Physical Value Chain (PVC) as an integrated system rather than a set of discrete but related activities. In practice this means that the company performs actions in the marketplace while it monitors and coordinates those actions in the marketspace.

21 RAYPORT, J.F. and SVIOKLA, J.J. Exploiting the Virtual Value Chain

Figure 4. The five steps for creating value of information

Gathering Organising Selecting Synthesising Distribution

21

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

Physical value chain

Virtual value chain

Value matrix

New markets New markets New markets

Gather

Organise

Select

Synthesise

Distribute

Figure 5. The value matrix

In the second stage, mirroring capability, companies have established a necessary infrastruc-ture for visibility and move on by managing operations and even implement value-adding steps in the marketspace. The latter is often done by studying the PVC and transferring the value-adding activities to the new virtual environment. By moving from the marketplace to the marketspace the company starts the creation of a VVC that parallels and improves on the PVC. But ultimately companies must not just add value to the VVC, but extract value from it. This is done in the third and final stage, new customer relationships, where customer relationships are established through the marketspace. Collecting information about the customer that can be distributed through the company or sold to other businesses is a method often used but not totally accepted since it often is done without the customer’s knowledge. The reason, however, is to create more value for users by serving a broader set of their needs. This is done by personalised and hopefully attractive offers that can be given to the customer when he makes contact with the company. One must not forget that it is still important to specify what information will be collected so the customer feels secure when dealing with the company. Customer feelings of insecurity are still a major concern for online transactions22.

6.4.3 The Value Matrix New relationships with the customers that companies develop can be derived from a matrix of value opportunities.23 From each stage on the VVC (mirrored from the PVC) an extract of information can be tapped and this could form a new product or service. In order to perform this the company must use processes to gather the information, organise it in a proper way for the customer, extract the valuable information, package or synthesise it and finally distribute it according to the five value-adding steps above unique for the information world. These five steps in combination with the VVC form a value matrix that makes it easier to identify the customers’ desires more effectively and fulfil them more efficiently. The resulting matrix is shown in Figure 5.

This model is a logical choice in this thesis since the traditional linear music industry value chain has become insufficient in the new marketspace.

22 LIEBOWITZ, S. Re-thinking the network economy: the true forces that drive the digital marketplace 23 RAYPORT, J.F. and SVIOKLA, J.J. Exploiting the Virtual Value Chain

22

Landegren, J. and Liu, P. Usability Factors in Digital Music Distribution Services and Their Relationships with Established and New Value Chains in the Music Industry Joakim Landegren

7 Methods

7.1 Evaluation of Services An evaluation of the available services gives an overview of the current implementation level of digital distribution. One effective way to investigate what a consumer experiences is to act consumer and actually use the services. This method was chosen because of its effectiveness and low resource consumption. Minor case studies have been chosen instead of major to enable coverage of as many different sorts of services as possible. To extend the coverage maximally the different kinds of services have been categorised in classification matrices and additional criteria have been divided into so called selection models described below. The tests were performed during a four months period.

The goal of the evaluation is to find the most important factors that are stated in the problem definition.

7.1.1 Selection Models All services have different ways of storing and distributing their material, and they also have different sources of income. Below are the main groups of categories for the services. The purpose of this categorisation is to easier decide which business models seem to be most successful. As shown later, the focus and main comparisons will be between the major services (Pressplay, MusicNet and Rhapsody) and the P2P networks without any licenses. MP3.com will also play an important role as an independent platform. There are also minor comparisons with other business models such as Internet radio, small services and user communities

Distribution Models There are several distribution models in use today. Some are easier to use than others.

P2P: Almost all P2P services are without any license today, with only a few exceptions that try to be legal. Some services like Wippit, have ensured legality, but are not very popular. There are both centralised services where a central server keeps record of all nodes in the network, and decentralised services that are true Peer-to-Peer protocols.

Internet radio: Internet radio works like traditional radio, but using the Internet as distribution channel. As with radio it is used mainly as a marketing tool, and not as a source of income.

Central server: A central server enables full control over the material, but requires a large amount of resources to maintain. It is often accessed through a web interface and a proprietary client. This model ensures a good quality of service.

Income Sources Several pay models are used by the services today, all with their own advantages and disadvantages for the user.

Subscription: A sum is paid in advance each month, which enables the user to obtain a limited or unlimited amount of music. Often an unlimited amount of streamed music is offered, a limited amount of downloads and a limited amount of music which can be burned to a writable CD. In most cases the music is in fact rented, since it will cease to work when the subscription is cancelled.

23