us weekly kickstart - betandbetter · us weekly kickstart ... source: i/b/e/s, firstcall, ......

TRANSCRIPT

Goldman Sachs Global Investment Research 1

December 5, 2014

United States

US Weekly Kickstart Portfolio Strategy Research

A lower interest rate scenario vs. our forecast would support a higher 2015 S&P 500 target

The drop in 10-year Treasury yields from 3% to 2.3% has been one of the biggest market surprises of 2014. We expect rates to rise

next year in conjunction with an initial Fed hike and accelerating GDP growth. The persistence of low rates has led many investors to

question our economists’ year-end 2015 forecast of fed funds at 0.6% and 10-year Treasuries at 3%. As the yield curve normalizes, if

interest rates remain lower than we anticipate, equity returns could be greater than we forecast. Within the confines of a Fed model,

an end-2015 S&P 500 level of 2300 would be consistent with 2.5% 10-year Treasuries while our forecast of 2100 assumes a 3% yield.

Performance

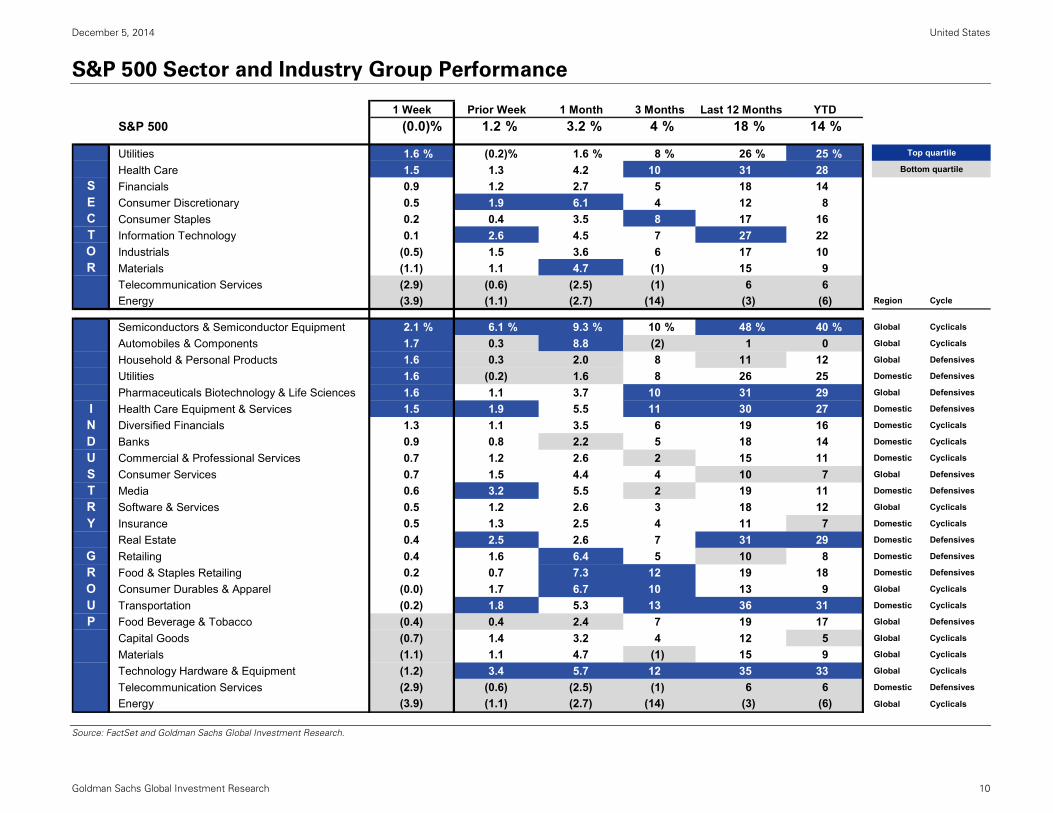

The S&P 500 was flat this week. Utilities was the

best-performing sector (+1.6%) while Energy was

the worst-performing sector (-3.9%). We expect

the S&P 500 will likely trade at 2100 in 12 months

(+1.4%). See pages 5-15 for performance charts by

sector, style, size, themes.

S&P 500 earnings and valuation

Source: I/B/E/S, FirstCall, and Goldman Sachs Investment Research.

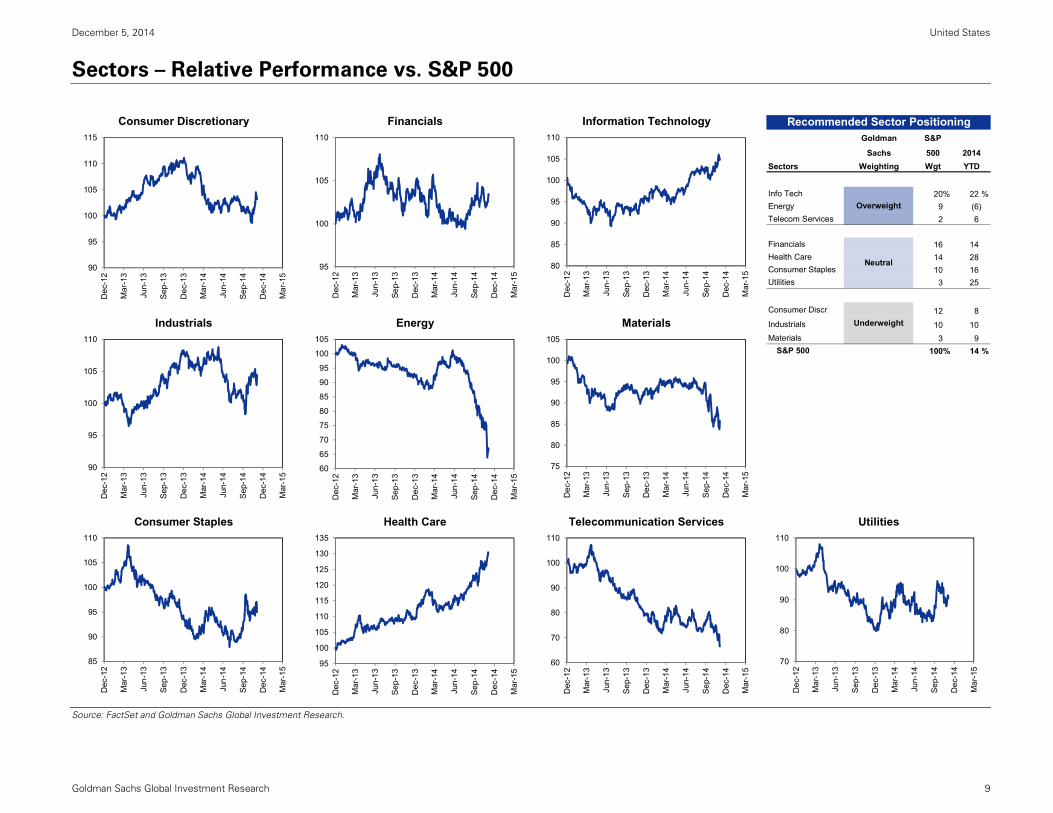

Sector views and performance

Domestic Cyclicals up 14.5% vs. Global Cyclicals

up 9.8% YTD. O/W Information Technology,

Energy, and Telecom Services. U/W Consumer

Discretionary, Industrials, and Materials.

Key pages for portfolio managers

Markets and Money flow (page 5)

Absolute and risk-adjusted returns for markets,

sectors, styles, and strategies (page 6)

Fund flows, correlation, and dispersion (page 18)

Chart of the Week: Sentiment Indicator

Sentiment continues to rise (page 5)

US Portfolio Strategy recommendations

Buy S&P 500 / Sell 10-year Treasury: +4.6% YTD

Buy US vs. Western Europe Revenues: +5.7%

Buy Total Cash Return to shareholders vs.

S&P 500: -0.3%

Buy Low Turnover vs. High Turnover: +2.4%

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S.

The Goldman Sachs Group, Inc. Global Investment Research

Goldman Sachs ConsensusPortfolio Strategy Bottom-Up

2014E 2015E 2014E 2015E$116 $122 $116 $127

9 % 5 % 9 % 9 %

NTM 2015E NTM 2015E17.1x 17.0x 16.5x 16.3x

December 5, 2014 United States

Goldman Sachs Global Investment Research 2

Conversations we are having with clients: Yield curve scenarios and the path of stocks

Interest rates dominated our discussions with fund managers this week.

The various interest rate scenarios articulated by clients translate into a 10

percentage point difference in the prospective 12-month price return of the

S&P 500. Our interest rate projections support a 1% rise to 2100 while a lower

interest rate scenario vs. our expectation would suggest an 11% gain to 2300.

Goldman Sachs Economics forecasts the Fed will start to tighten in 3Q

and the funds rate will eventually climb to a neutral level of 3.9% by the

end of 2018 (see Exhibit 1). At the same time, 10-year Treasury yields will

rise to 3.0% by year-end 2015 and reach 4.3% in four years (see Exhibit 2).

Our economists forecast several years of above-trend US economic

expansion will be accompanied by rising interest rates. Domestic GDP

growth should accelerate to 3.1% in 2015 and remain above 3% for several

years. Today’s non-farm payrolls surpassed even the most optimistic

estimates with 321K jobs created in November. Monthly wage inflation

accelerated to 0.4%. The unemployment rate was steady at 5.8%. This week

ISM manufacturing printed 58.7 and ISM non-manufacturing rose to 59.3, both

near their post Global Financial Crisis highs. Goldman Sachs Current Activity

Indicator (CAI), a real-time proxy for GDP growth, currently stands at 4.4%.

In contrast, many clients believe the Fed will hike policy rates next year

but that structural changes in the US economy will keep potential GDP

growth low and the funds rate will rise to just 2% during next few years.

Adherents of the “secular stagnation” thesis believe the financial crisis left

the US economy irreversibly weaker, and the economy will not be capable

of tolerating higher rates. Clients validate these views by pointing to forward

market prices, which imply fed funds at 0.5% and 10-year rates at 2.5% by

year-2015, compared with our forecasts of 0.6% and 3.0%, respectively. A

sizeable number of clients have the view that no rate hike will occur in 2015.

Interest rates continue to hover near recent lows despite very strong

US economic data. We believe current low US Treasury yields reflect

unconventional monetary policy and transitory declines in inflation. Nominal

Treasury yields can be disaggregated to two factors: expected real rates and

inflation. Inflation-protected TIPS show that 50 bp of the 70 bp decline in 10-

year Treasuries during 2014 was driven by falling inflation. Most of these

declines coincided with the 40% drop in crude oil prices since June. Our

economists expect inflation will gradually trend higher as the labor market

improves. The remaining 20 bp were due to lower real rates, which we

attribute to continued accommodative actions by both the ECB and the BOJ.

In September, the Fed released its Summary of Economic Projections (SEP)

and the median forecast indicates a 3.75% fed funds rate by 2018,

consistent with the view of Goldman Sachs Economics. Comments from

Fed officials this week suggested that rate hikes are likely during 2015. On

Monday, New York Fed President Dudley stated that rate hikes in “mid-2015

seem reasonable to me.” The Fed will release its next SEP on December 17th.

S&P 500 has returned 14% YTD. We forecast the index will continue its

upward trajectory during the first half of 2015, reflecting the ongoing

economic expansion and rising profit growth. We expect EPS will rise by 5%

to $122 in 2015 and by 8% to $131 in 2016. However, the forward P/E multiple

will likely compress from the current 17.0x to 16.0x by the end of 2015, sparked

by the first Fed rate hike since 2006.

If interest rates in 2015 remain below our forecast, then equity returns may

exceed our expectations. A Fed model with 10-year Treasury rates at 2.5% and

no changes to both EPS and the equity risk premium would imply a level of

2300 for the S&P 500 at year-end 2015 representing an 11% gain. The P/E

multiple would expand to 17.4x, higher than our baseline forecast of 16.0x. A

“reach for yield” argument would support rising P/E multiples in a low interest

rate environment. In that scenario, investors would be incentivized to purchase

higher yielding equity assets. The 6.1% earnings yield on the S&P 500 is

currently 380 bp higher than the 10-year Treasury yield of 2.3%. The yield gap

has averaged 410 bp during the past 10 years and 235 bp since 1976.

Low interest rates and falling oil prices also suggest further upside to S&P

500 EPS. We forecast Brent crude will average $85 a barrel during 2015, 20%

below the YTD average of $103, but 23% above the current $69 price. Our

models indicate that every $10 reduction from our $85 crude oil forecast

represents roughly $2 in incremental EPS in 2015 and $4 in 2016, all else equal.

Low interest rates allow corporations to trim borrowing costs, boosting future

earnings. However, we believe the impact of low rates on interest expense

would be muted given most firms have already refinanced their borrowings.

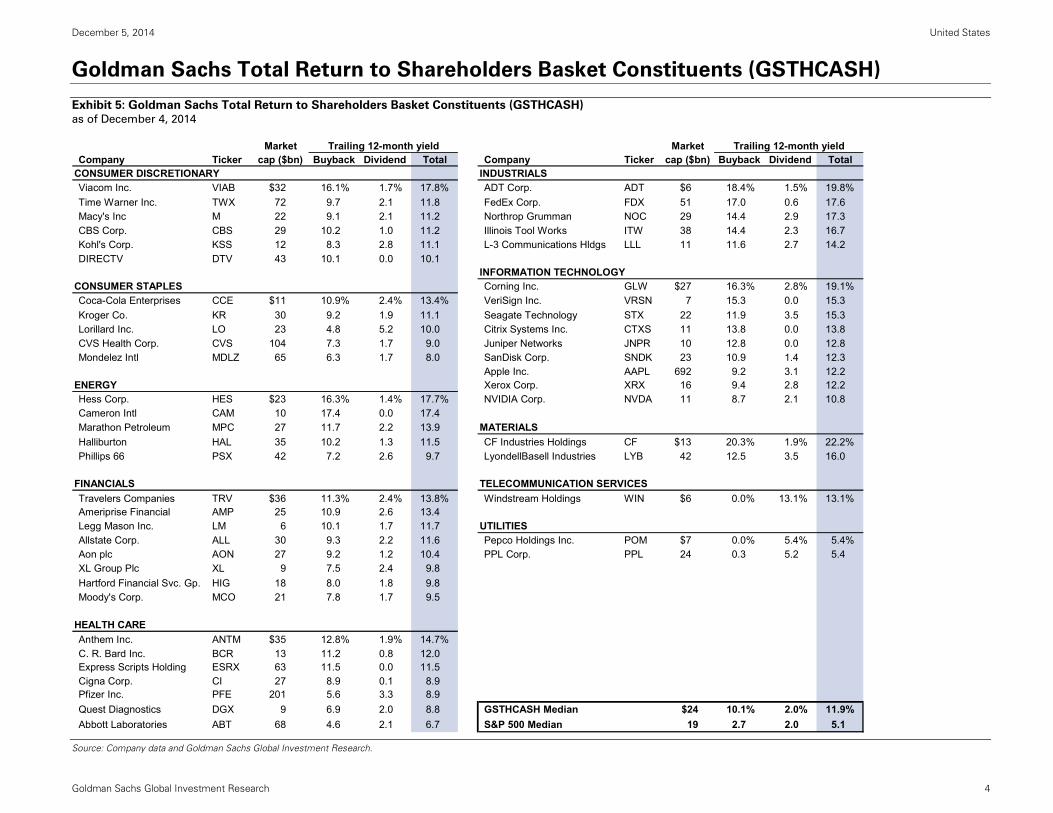

Investors who believe interest rates will remain below the Goldman Sachs

Economics forecast in 2015 should focus on stocks returning cash to

shareholders via buybacks and dividends (Bloomberg ticker:

<GSTHCASH>). The median cash return to shareholders for the 50 stocks in

this portfolio was more than twice the median for the S&P 500 index (12% vs.

5%). The basket has outperformed S&P 500 by 230 bp YTD (16.7% vs. 14.4%).

Selected Buy-rated constituents with 10%+ upside potential: ABT, LLL, NOC,

and PFE.

Goldman Sachs Global Investment Research 3

Charts we are watching: Lower interest rates, higher equity valuations

Exhibit 1: Our fed funds forecasts are in-line with Fed but above the market as of December 4, 2014

Exhibit 2: Goldman Sachs Economics expects rates to rise across the curve as of December 4, 2014

Source: Federal Reserve, Bloomberg, and Goldman Sachs Global Investment Research. Source: Federal Reserve and Goldman Sachs Global Investment Research.

Exhibit 3: The spread between Treasuries and Bunds is close to a record highas of December 4, 2014

Exhibit 4: Lower 10-year yields would support a higher equity valuation as of December 4, 2014

Source: Haver and Goldman Sachs Global Investment Research. Source: Compustat, I/B/E/S, FRB, and Goldman Sachs Global Investment Research.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2014 2015 2016 2017 2018

Fed funds rate path:GS vs. Fed vs. Market GS Forecast

Market-Implied

2018E:3.9%

2018E:2.5%

Federal Reserve

2018E:3.8%

0

1

2

3

4

5

FedFunds

1 2 3 4 5 6 7 8 9 10

Yiel

d (%

)

Years to Maturity

Current

Goldman Sachs Yield Curve Forecasts

2014E

4.3%3.8%3.5%

3.0%

2.5%

0.1%

3.9%

2.9%

1.6%

0.6%

2.3%

2015E

2016E

2017E

2018E

(100)

(50)

0

50

100

150

200

250

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Bas

is p

oint

s

10-year yield spreadUS Treasury less German Bund

+1 stdev: 92 bp

-1 stdev: -12 bp

Avg: 40 bp

156 bp

125 bp

GS Forecast2015 Scenarios

US 10-Yr Yield Earnings NTM S&P 500Scenario T-Yield Gap Yield P/E Level

GS 3.0 % 325 bp 6.3 % 16.0x 2100

Alternative 2.5 325 5.8 17.4 2300

Current 376 bp

5-Year 516

10-Year 408

1976 - Present 235

December 5, 2014 United States

Goldman Sachs Global Investment Research 4

Goldman Sachs Total Return to Shareholders Basket Constituents (GSTHCASH)

Exhibit 5: Goldman Sachs Total Return to Shareholders Basket Constituents (GSTHCASH)

as of December 4, 2014

Source: Company data and Goldman Sachs Global Investment Research.

Market Trailing 12-month yield Market Trailing 12-month yieldCompany Ticker cap ($bn) Buyback Dividend Total Company Ticker cap ($bn) Buyback Dividend Total

CONSUMER DISCRETIONARY INDUSTRIALSViacom Inc. VIAB $32 16.1% 1.7% 17.8% ADT Corp. ADT $6 18.4% 1.5% 19.8%Time Warner Inc. TWX 72 9.7 2.1 11.8 FedEx Corp. FDX 51 17.0 0.6 17.6Macy's Inc M 22 9.1 2.1 11.2 Northrop Grumman NOC 29 14.4 2.9 17.3CBS Corp. CBS 29 10.2 1.0 11.2 Illinois Tool Works ITW 38 14.4 2.3 16.7Kohl's Corp. KSS 12 8.3 2.8 11.1 L-3 Communications Hldgs LLL 11 11.6 2.7 14.2DIRECTV DTV 43 10.1 0.0 10.1

INFORMATION TECHNOLOGYCONSUMER STAPLES Corning Inc. GLW $27 16.3% 2.8% 19.1%Coca-Cola Enterprises CCE $11 10.9% 2.4% 13.4% VeriSign Inc. VRSN 7 15.3 0.0 15.3Kroger Co. KR 30 9.2 1.9 11.1 Seagate Technology STX 22 11.9 3.5 15.3Lorillard Inc. LO 23 4.8 5.2 10.0 Citrix Systems Inc. CTXS 11 13.8 0.0 13.8CVS Health Corp. CVS 104 7.3 1.7 9.0 Juniper Networks JNPR 10 12.8 0.0 12.8Mondelez Intl MDLZ 65 6.3 1.7 8.0 SanDisk Corp. SNDK 23 10.9 1.4 12.3

Apple Inc. AAPL 692 9.2 3.1 12.2ENERGY Xerox Corp. XRX 16 9.4 2.8 12.2Hess Corp. HES $23 16.3% 1.4% 17.7% NVIDIA Corp. NVDA 11 8.7 2.1 10.8Cameron Intl CAM 10 17.4 0.0 17.4Marathon Petroleum MPC 27 11.7 2.2 13.9 MATERIALSHalliburton HAL 35 10.2 1.3 11.5 CF Industries Holdings CF $13 20.3% 1.9% 22.2%Phillips 66 PSX 42 7.2 2.6 9.7 LyondellBasell Industries LYB 42 12.5 3.5 16.0

FINANCIALS TELECOMMUNICATION SERVICESTravelers Companies TRV $36 11.3% 2.4% 13.8% Windstream Holdings WIN $6 0.0% 13.1% 13.1%Ameriprise Financial AMP 25 10.9 2.6 13.4Legg Mason Inc. LM 6 10.1 1.7 11.7 UTILITIESAllstate Corp. ALL 30 9.3 2.2 11.6 Pepco Holdings Inc. POM $7 0.0% 5.4% 5.4%Aon plc AON 27 9.2 1.2 10.4 PPL Corp. PPL 24 0.3 5.2 5.4XL Group Plc XL 9 7.5 2.4 9.8Hartford Financial Svc. Gp. HIG 18 8.0 1.8 9.8Moody's Corp. MCO 21 7.8 1.7 9.5

HEALTH CAREAnthem Inc. ANTM $35 12.8% 1.9% 14.7%C. R. Bard Inc. BCR 13 11.2 0.8 12.0Express Scripts Holding ESRX 63 11.5 0.0 11.5Cigna Corp. CI 27 8.9 0.1 8.9Pfizer Inc. PFE 201 5.6 3.3 8.9Quest Diagnostics DGX 9 6.9 2.0 8.8 GSTHCASH Median $24 10.1% 2.0% 11.9%Abbott Laboratories ABT 68 4.6 2.1 6.7 S&P 500 Median 19 2.7 2.0 5.1

December 5, 2014 United States

Goldman Sachs Global Investment Research 5

Markets and Money Flow

Source: Haver, Lipper, FactSet, CFTC, and Goldman Sachs Global Investment Research.

S&P 500 level and EPS 10-yr. Treasury Yields Stocks vs. Bonds

Sentiment Indicator Rotation Index Volatility

80

100

120

140

160

180

200

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Dec

-16

Dec

-17

SPX/UST

Goldman Sachs

Forecast

S&P 500 Total Return vs. 10-Year UST

(Constant Maturity, Rolled Monthly)

10

15

20

25

30

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Mar

-14

Jun-

14

Sep

-14

Dec

-14

Mar

-15

VIX(2.0)

(1.5)

(1.0)

(0.5)

0.0

0.5

1.0

1.5

2.0

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Mar

-14

Jun-

14

Sep

-14

Dec

-14

Mar

-15

Stan

dard

dev

iatio

ns

Risk off; favors BOND flows

Risk on; favors EQUITY flows

Rotation Index (4-wk moving avg)

6-month trend

0

20

40

60

80

100

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Mar

-14

Jun-

14

Sep

-14

Dec

-14

Mar

-15

S&P

500

Futu

res

Sent

imen

t

Sentiment Indicator (SI)

>90 = HIGH net positions

<10 = LOW net positions

86

1.0 %

1.5 %

2.0 %

2.5 %

3.0 %

3.5 %

4.0 %

4.5 %

5.0 %

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Dec

-16

Dec

-17

US 10-Year Treasury Yield

2016E3.50%

Current2.3%

2014E2.50%

2015E3.00%

90

100

110

120

130

140

150

1250

1500

1750

2000

2250

2500D

ec-1

2

Dec

-13

Dec

-14

Dec

-15

Dec

-16

Dec

-17

Dec

-18

S&P 500 EPSS&

P 50

0 Pr

ice

Goldman SachsEPS Forecast

S&P 500Price

Current2072

2014E2050

2016E2200

2013A$107

2014E$116

2015E$122

2016E$131

2017E$141

2015E2100

Note: Sentiment Indicator ranks net futures positioning versus the past 12 months. Readings

below 10 or above 90 indicate extreme positions that are significant in predicting future returns.

Note: Rotation Index plots the first principal component of weekly reallocation activity

across equity and debt mutual fund categories as a measure of retail risk appetite.

December 5, 2014 United States

Goldman Sachs Global Investment Research 6

Market Performance: 2014 YTD absolute and risk-adjusted returns

Source: Haver, Lipper, FactSet, and Goldman Sachs Global Investment Research.

Total Return Risk Adjusted Return (Sharpe Ratio)

14

(6)

6

8

9

10

14

16

22

25

28

(37)

(10)

(4)

(0)

0

1

2

2

5

7

9

13

14

14

15

(60) (50) (40) (30) (20) (10) 0 10 20 30 40 50

Brent Crude Oil

$/Euro

ENERGY

Event-Driven HF Index

Composite Hedge Fund Index

Gold

MSCI Emerging Markets

Equity L/S HF Index

Russell 2000

Global Macro HF Index

TELECOM SERVICES

MSCI Developed Markets

CONSUMER DISCRETIONARY

Barclays 7-10yr Treasury ETF

MATERIALS

INDUSTRIALS

Russell 1000 Value

Russell 1000

Russell 1000 Growth

FINANCIALS

S&P 500

Nasdaq

CONSUMER STAPLES

INFORMATION TECHNOLOGY

UTILITIES

HEALTH CARE

(1.9)

(1.8)

(0.8)

(0.1)

0.0

0.1

0.1

0.3

0.8

1.2

1.2

1.2

1.3

1.3

1.9

(0.4)

0.5

0.6

0.7

0.8

1.2

1.7

1.8

2.0

2.1

1.4

(3.0) (2.5) (2.0) (1.5) (1.0) (0.5) 0.0 0.5 1.0 1.5 2.0 2.5 3.0

Brent Crude Oil

$/Euro

Event-Driven HF Index

ENERGY

Composite Hedge Fund Index

Gold

MSCI Emerging Markets

Russell 2000

Equity L/S HF Index

TELECOM SERVICES

CONSUMER DISCRETIONARY

MATERIALS

INDUSTRIALS

MSCI Developed Markets

Nasdaq

Global Macro HF Index

FINANCIALS

Russell 1000 Growth

Russell 1000

Russell 1000 Value

S&P 500

INFORMATION TECHNOLOGY

CONSUMER STAPLES

Barclays 7-10yr Treasury ETF

UTILITIES

HEALTH CARE

December 5, 2014 United States

Goldman Sachs Global Investment Research 7

Sector Baskets – Performance Relative to S&P 500

Source: FactSet and Goldman Sachs Global Investment Research.

Cyclicals Defensives Domestic Global

Domestic Cyclicals Global Cyclicals Domestic Defensives Global Defensives

94

95

96

97

98

99

100

101

102

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSSBCYCLBloomberg <ticker>

94

96

98

100

102

104

106

108

110

112

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSSBDCYC

94

96

98

100

102

104

106

108

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSSBDEFS

84

86

88

90

92

94

96

98

100

102

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSSBGCYC

97

98

99

100

101

102

103

104

105

106

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSSBDOMS

92

94

96

98

100

102

104

106

108

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSSBDDEF

95

96

97

98

99

100

101

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSSBGLBL

96

98

100

102

104

106

108

110

112

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSSBGDEF

December 5, 2014 United States

Goldman Sachs Global Investment Research 8

Sector Basket Performance

Source: FactSet and Goldman Sachs Global Investment Research.

Cyclicals vs. Defensives Domestic vs. Global

85

90

95

100

105

110

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

CYCLICALSoutperforming

DEFENSIVESoutperforming

90

92

94

96

98

100

102

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GLOBALoutperforming

DOMESTICoutperforming

Performance and fundamentals of our sector baskets Bloomberg % of

Ticker # of S&P 500 Non-US Earnings Growth Sales Growth NTM LTM Div Total ReturnBasket <GSSBXXXX> Stocks Cap Beta Sales 2014 2015 2014 2015 P/E P/B Yield 1 Wk 1 Mo 3 Mo LTM YTD

Defensives DEFS 210 41 % 0.9 21% 12 % 9 % 6 % 5 % 18.6x 4.0x 2.1 % 1 % 4 % 7 % 21 % 19 %Cyclicals CYCL 290 59 1.1 42 4 9 2 1 15.3 2.4 1.8 (1) 3 2 16 11

Domestic DOMS 228 39 % 0.9 16% 7 % 12 % 6 % 5 % 16.1x 2.2x 1.9 % 1 % 4 % 6 % 19 % 16 %Global GLBL 272 61 1.0 49 7 7 2 1 16.8 3.6 2.0 (0) 3 3 17 13

Global Defensives GDEF 67 19 % 1.0 49% 12 % 10 % 3 % 3 % 19.0x 5.3x 2.2 % 1 % 3 % 9 % 23 % 21 %Domestic Cyclicals DCYC 85 17 1.1 23 3 16 2 4 14.0 1.5 1.6 1 3 6 19 14Domestic Defensives DDEF 143 23 0.9 13 11 9 7 6 18.2 3.3 2.1 0 4 6 19 17Global Cyclicals GCYC 205 42 1.1 49 5 6 1 1 15.9 3.1 2.0 (1) 3 1 15 10

S&P 500 500 100 % 1.0 33% 9 % 9 % 4 % 3 % 16.5x 2.9x 2.0 % (0)% 3 % 4 % 18 % 14 %

December 5, 2014 United States

Goldman Sachs Global Investment Research 9

Sectors – Relative Performance vs. S&P 500

Source: FactSet and Goldman Sachs Global Investment Research.

Consumer Discretionary Financials Information Technology Recommended Sector PositioningGoldman S&P

Sachs 500 2014Sectors Weighting Wgt YTD

Info Tech 20% 22 %Energy 9 (6)Telecom Services 2 6

Financials 16 14Health Care 14 28Consumer Staples 10 16Utilities 3 25

Consumer Discr 12 8Industrials Energy Materials Industrials 10 10

Materials 3 9S&P 500 100% 14 %

Consumer Staples Health Care Telecommunication Services Utilities

Underweight

Overweight

Neutral90

95

100

105

110

115

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

90

95

100

105

110

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

95

100

105

110

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

60

65

70

75

80

85

90

95

100

105D

ec-1

2

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

80

85

90

95

100

105

110

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

75

80

85

90

95

100

105

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

85

90

95

100

105

110

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15 95

100

105

110

115

120

125

130

135

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

60

70

80

90

100

110

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

70

80

90

100

110

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

December 5, 2014 United States

Goldman Sachs Global Investment Research 10

S&P 500 Sector and Industry Group Performance

Source: FactSet and Goldman Sachs Global Investment Research.

1 Week Prior Week 1 Month 3 Months Last 12 Months YTDS&P 500 (0.0)% 1.2 % 3.2 % 4 % 18 % 14 %

Utilities 1.6 % (0.2)% 1.6 % 8 % 26 % 25 % Top quartile

Health Care 1.5 1.3 4.2 10 31 28 Bottom quartile

S Financials 0.9 1.2 2.7 5 18 14E Consumer Discretionary 0.5 1.9 6.1 4 12 8C Consumer Staples 0.2 0.4 3.5 8 17 16T Information Technology 0.1 2.6 4.5 7 27 22O Industrials (0.5) 1.5 3.6 6 17 10R Materials (1.1) 1.1 4.7 (1) 15 9

Telecommunication Services (2.9) (0.6) (2.5) (1) 6 6Energy (3.9) (1.1) (2.7) (14) (3) (6) Region Cycle

Semiconductors & Semiconductor Equipment 2.1 % 6.1 % 9.3 % 10 % 48 % 40 % Global Cyclicals

Automobiles & Components 1.7 0.3 8.8 (2) 1 0 Global Cyclicals

Household & Personal Products 1.6 0.3 2.0 8 11 12 Global Defensives

Utilities 1.6 (0.2) 1.6 8 26 25 Domestic Defensives

Pharmaceuticals Biotechnology & Life Sciences 1.6 1.1 3.7 10 31 29 Global Defensives

I Health Care Equipment & Services 1.5 1.9 5.5 11 30 27 Domestic Defensives

N Diversified Financials 1.3 1.1 3.5 6 19 16 Domestic Cyclicals

D Banks 0.9 0.8 2.2 5 18 14 Domestic Cyclicals

U Commercial & Professional Services 0.7 1.2 2.6 2 15 11 Domestic Cyclicals

S Consumer Services 0.7 1.5 4.4 4 10 7 Global Defensives

T Media 0.6 3.2 5.5 2 19 11 Domestic Defensives

R Software & Services 0.5 1.2 2.6 3 18 12 Global Cyclicals

Y Insurance 0.5 1.3 2.5 4 11 7 Domestic Cyclicals

Real Estate 0.4 2.5 2.6 7 31 29 Domestic Defensives

G Retailing 0.4 1.6 6.4 5 10 8 Domestic Defensives

R Food & Staples Retailing 0.2 0.7 7.3 12 19 18 Domestic Defensives

O Consumer Durables & Apparel (0.0) 1.7 6.7 10 13 9 Global Cyclicals

U Transportation (0.2) 1.8 5.3 13 36 31 Domestic Cyclicals

P Food Beverage & Tobacco (0.4) 0.4 2.4 7 19 17 Global Defensives

Capital Goods (0.7) 1.4 3.2 4 12 5 Global Cyclicals

Materials (1.1) 1.1 4.7 (1) 15 9 Global Cyclicals

Technology Hardware & Equipment (1.2) 3.4 5.7 12 35 33 Global Cyclicals

Telecommunication Services (2.9) (0.6) (2.5) (1) 6 6 Domestic Defensives

Energy (3.9) (1.1) (2.7) (14) (3) (6) Global Cyclicals

December 5, 2014 United States

Goldman Sachs Global Investment Research 11

Style and Size

Source: FactSet and Goldman Sachs Global Investment Research,

Growth vs. Value

96

97

98

99

100

101

102

103

104

105

106

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Value outperforming

Growth outperforming

Large-cap vs. Small-cap

92

94

96

98

100

102

104

106

108

110

112

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

S&P 500 outperforming

Russell 2000 outperforming

Sectors: Russell 1000 Growth vs. Value

Weight (%) 1-Week (% Return) YTD (% Return)Sector Value Growth Value Growth ∆ (bps) Value Growth ∆ (bps)Energy 11 5 (4) (7) 346 (6) (5) (114)

Information Tech 10 28 1 (0) 113 30 17 1,302

Cons Discretionary 6 18 1 0 89 12 7 499

Utilities 6 0 1 1 74 24 21 245

Financials 30 5 1 0 64 14 12 212

Consumer Staples 7 11 0 0 34 16 15 141

Health Care 14 14 2 1 18 24 32 (752)

Telecom Services 2 2 (3) (3) (55) 3 8 (467)

Materials 3 4 (2) (0) (101) 8 10 (186)

Industrials 10 12 (1) 0 (166) 6 12 (516)

Index 100 100 0 (0) 29 13 14 (47)

Sectors: S&P 500 vs. Russell 2000

Weight (%) 1-Week (% Return) YTD (% Return)Sector SP500 R2000 SP500 R2000 ∆ (bps) SP500 R2000 ∆ (bps)Energy 9 4 (4) (17) 1,270 (6) (36) 2,986

Health Care 14 14 2 (1) 260 28 13 1,477

Financials 16 24 1 (1) 166 14 6 775

Cons Discretionary 12 14 1 (1) 131 8 (1) 891

Utilities 3 3 2 0 130 25 16 879

Telecom Services 2 1 (3) (4) 112 6 (6) 1,134

Industrials 10 14 (1) (1) 94 10 (3) 1,297

Materials 3 5 (1) (2) 87 9 (5) 1,424

Consumer Staples 10 3 0 0 16 16 8 801

Information Tech 20 18 0 0 2 22 5 1,662

Index 100 100 (0) (1) 146 14 2 1,227

December 5, 2014 United States

Goldman Sachs Global Investment Research 12

US Portfolio Strategy Baskets

For details and constituents of our baskets see Strategy Baskets: Anatomy of our US Portfolio Strategy Thematic and Sector Baskets, July 23, 2014.

Source: FactSet and Goldman Sachs Global Investment Research.

Bloomberg Total Return P/E P/B DivTicker 1 wk 1 mo YTD NTM LTM Yield

Macroeconomic

Dual Beta GSTHBETA (1)% 1 % 6 % 20x 4.3x 1.0 %Interest Rate Sensitive GSTHUSTY (1) 1 10 17 3.2 1.5High Operating Leverage GSTHOPHI (1) 3 13 21 3.8 1.4Low Operating Leverage GSTHOPLO (1) 2 16 19 6.7 2.3High Tax GSTHHTAX 0 4 19 21 6.6 1.7Low Tax GSTHLTAX (1) 3 10 16 3.4 2.7

Geographic Sales

Domestic Sales GSTHAINT (0)% 3 % 18 % 19x 4.6x 1.6 %International Sales GSTHINTL (0) 3 9 16 4.5 2.0BRICs Sales GSTHBRIC (0) 4 9 17 5.4 1.8Western Europe Sales GSTHWEUR 0 4 8 18 3.9 1.7

Fundamental

High Revenue Growth GSTHREVG (1)% 2 % 10 % 25x 6.7x 0.9 %ROE Growth GSTHGROE 0 3 14 19 4.7 2.0High Quality Stock GSTHQUAL 0 2 13 19 5.7 1.5Strong Balance Sheet GSTHSBAL 0 4 17 25 7.6 1.0Weak Balance Sheet GSTHWBAL (1) 3 19 17 3.5 1.9

Shareholder Return

Dividend Growth GSTHDIVG 0 % 3 % 12 % 16x 4.5x 2.8 %Buyback GSTHREPO (1) 3 14 17 4.3 1.4Total Cash Return to Shareholder GSTHCASH (1) 3 16 16 4.2 1.9Earnings Held Overseas GSTHSEAS 0 4 14 17 3.6 2.0

Hedge Fund

Hedge Fund "VIP" List GSTHHVIP (0)% 5 % 16 % 21x 6.2x 1.1 %Hedge Fund Very Important Shorts GSTHVISP 0 4 16 18 5.3 2.3High Hedge Fund Concentration GSTHHFHI (0) 5 20 20 4.9 0.6Low Hedge Fund Concentration GSTHHFSL 0 4 15 17 4.1 2.7

Mutual Fund

High Sharpe Ratio GSTHSHRP (1)% 2 % 14 % 17x 4.6x 1.6 %Mutual Fund Overweight Positions GSTHMFOW (0) 3 10 18 5.0 1.3Mutual Fund Underweight Positions GSTHMFUW 0 3 17 19 5.2 2.9

S&P 500 (0)% 3 % 14 % 17x 2.9x 2.0 %S&P 500 Average 19 4.6 1.9S&P 500 Median 17 3.2 1.7

YTD Performance

20

19

19

18

17

17

16

16

16

16

15

14

14

14

14

13

13

12

10

10

10

10

9

9

8

6

14

(5) 0 5 10 15 20 25 30

High Hedge Fund Concentration

Weak Balance Sheet

High Tax

Domestic Sales

Strong Balance Sheet

Mutual Fund Underweight Positions

Total Cash Return to Shareholder

Hedge Fund Very Important Shorts

Hedge Fund "VIP" List

Low Operating Leverage

Low Hedge Fund Concentration

High Sharpe Ratio

ROE Growth

S&P 500

Earnings Held Overseas

Buyback

High Quality Stock

High Operating Leverage

Dividend Growth

Mutual Fund Overweight Positions

High Revenue Growth

Low Tax

Interest Rate Sensitive

BRICs Sales

International Sales

Western Europe Sales

Dual Beta

December 5, 2014 United States

Goldman Sachs Global Investment Research 13

US Portfolio Strategy Baskets – Relative performance vs. S&P 500

Source: FactSet and Goldman Sachs Global Investment Research.

Macroeconomic Geographic SalesDual Beta Interest Rate Sensitive US Sales International Sales

High vs. LowOperating Leverage

High vs. LowTax Rate BRICs Sales Western Europe Sales

90

95

100

105

110

115

120

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHBETABloomberg <ticker>

96

98

100

102

104

106

108

110

112

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHOPHI/GSTHOPLO

95

100

105

110

115

120

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHUSTY

96

98

100

102

104

106

108

110

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHAINT

82

86

90

94

98

102

106

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHBRIC

94

96

98

100

102

104

106

108

110

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHINTL

95

100

105

110

115

120

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHWEUR

96

101

106

111

116

121

126

Feb-

13

May

-13

Aug-

13

Nov

-13

Feb-

14

May

-14

Aug-

14

Nov

-14

Feb-

15

GSTHHTAX/GSTHLTAX

December 5, 2014 United States

Goldman Sachs Global Investment Research 14

US Portfolio Strategy Baskets – Relative performance vs. S&P 500 (continued)

Source: FactSet and Goldman Sachs Global Investment Research.

Fundamentals Shareholder ReturnRevenue Growth ROE Growth Dividend Yield & Growth Buybacks

High QualityStrong vs. WeakBalance Sheet Total Cash Return Earnings Held Overseas

94

96

98

100

102

104

106

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHREVGBloomberg <ticker>

92

93

94

95

96

97

98

99

100

101

102

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHQUAL

98

99

100

101

102

103

104

105

106

107

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHGROE

98

99

100

101

102

103

104

105

106

107

108

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHDIVG

95

100

105

110

115

120

125

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHCASH

95

100

105

110

115

120

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHREPO

97

98

99

100

101

102

Jul-1

3

Oct

-13

Jan-

14

Apr-1

4

Jul-1

4

Oct

-14

Jan-

15

GSTHSEAS

60

65

70

75

80

85

90

95

100

105

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHSBAL/GSTHWBAL

December 5, 2014 United States

Goldman Sachs Global Investment Research 15

US Portfolio Strategy Baskets – Relative performance vs. S&P 500 (continued)

Source: FactSet and Goldman Sachs Global Investment Research.

Hedge Fund Ownership Mutual FundsHedge Fund VIP Short Positions Overweight Positions Underweight Positions

High Concentration Low Concentration High Sharpe Ratio

95

100

105

110

115

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHHVIPBloomberg <ticker>

95

100

105

110

115

120

125

130

135

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHHFHI

95

96

97

98

99

100

101

102

103

104

105

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHVISP

80

85

90

95

100

105

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHHFSL

95

100

105

110

115

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHMFOW

96

98

100

102

104

106

108

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHSHRP

75

80

85

90

95

100

105

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

GSTHMFUW

December 5, 2014 United States

Goldman Sachs Global Investment Research 16

S&P 500 Earnings, Sales and Revisions

Source: FirstCall, I/B/E/S, FactSet, and Goldman Sachs Global Investment Research.

GS Top-Down EPS vs. Consensus Bottom-UpAnnual earnings

Contribution to EPS growth ratesGS Top-Down Bottom-up GS Top-Down Bottom-Up2015E 2016E 2015E 2016E 2015E 2016E 2015E 2016E

Information Technology $24 $25 $25 $28 9 % 6 % 16 % 12 %Health Care 15 17 17 19 8 11 20 13Utilities 4 4 4 4 7 5 5 4Consumer Discretionary 13 13 13 16 6 6 14 15Consumer Staples 10 11 11 12 6 3 6 9Industrials 13 13 13 15 5 7 10 10Telecom Services 3 4 4 4 4 4 7 5Materials 3 4 4 5 (9) 7 15 20Energy 12 13 12 14 (12) 8 (11) 15

S&P 500 ex-Financials 96 103 102 114 4 7 10 12Financials 26 28 25 28 9 11 7 10

S&P 500 Operating EPS $122 $131 $127 $142 5 % 8 % 9 % 12 %

Earnings & Sales Revisions (Consensus)EPS REVISIONS SALES REVISIONS

1 month 3 month 1 month 3 month14E 15E 14E 15E 14E 15E 14E 15E

Information Technology 0.2 % (0.3)% 0.1 % (0.6)% (0.1)% (0.1)% (0.1)% 0.1 %

Health Care 0.2 0.0 0.7 0.1 0.0 0.1 0.3 0.7

Utilities 0.1 (0.0) 0.6 0.2 NM NM NM NM

Consumer Discretionary 0.0 (0.3) (1.8) (2.9) 0.0 (0.1) (0.5) (0.8)

Industrials 0.0 (0.2) 0.6 (1.1) (0.1) (0.2) (0.3) (1.1)

Financials 0.0 0.1 (0.7) (0.4) NM NM NM NM

S&P 500 (0.0) (1.2) (0.8) (3.4) (0.2) (1.0) (0.6) (2.0)

Consumer Staples (0.1) (0.5) (0.8) (2.8) (0.2) (0.2) 0.0 (0.0)

Materials (0.4) (1.2) (0.3) (3.9) (0.1) (0.2) (0.6) (1.7)

Telecom Services (0.5) (0.7) (2.0) (3.1) 0.1 0.3 (0.2) 0.5

Energy (0.6) (9.7) (4.8) (20.9) (0.8) (5.9) (2.7) (10.3)

Earnings Growth (consensus bottom-up)

2014E Earnings Per Share Growth Annual1QA 2QA 3QE 4QE 2014E 2015E

Materials 0 % 44 % 13 % 18 % 17 % 15 %Health Care 6 17 8 29 15 20Information Technology 0 16 9 12 9 16Industrials 8 14 7 8 9 10Financials 6 8 12 9 9 7S&P 500 6 12 10 7 9 9Energy 4 4 22 4 8 (11)Consumer Discretionary 12 10 5 6 8 14Utilities 29 (9) 8 3 7 5Consumer Staples (0) 8 3 (6) 1 6Telecom Services 35 39 21 (49) (4) 7

S&P 500 (ex-Financials) 6 13 9 6 8 10

Sales Growth (consensus bottom-up)

2014E Sales Per Share Growth Annual1QA 2QA 3QE 4QE 2014E 2015E

Health Care 7 % 13 % 12 % 9 % 10 % 6 %Consumer Discretionary 14 8 6 5 8 5Industrials 5 6 4 4 5 3S&P 500 4 6 4 3 4 3Information Technology (2) 6 8 5 4 4Consumer Staples 1 4 3 3 3 5Materials 4 5 (3) (6) (0) 1Energy 2 4 (2) (6) (1) (2)Telecom Services (11) (9) 2 5 (4) 4

December 5, 2014 United States

Goldman Sachs Global Investment Research 17

Valuation: Absolute and Relative

Source: FactSet, I/B/E/S, FirstCall, and Goldman Sachs Global Investment Research.

S&P 500 NTM P/E S&P 500 Cost of Equity = ERP + 10-yr UST

S&P 500 LTM P/B

We estimate the equity risk premium (ERP) using our DDM framework to model expected future cash flows.

We solve for the cost of equity that implies the market is at ‘fair value’ and then deduct the 10-year US treasury.

Current Aggregate Valuation Metrics - Absolute Current vs. 10-year average (Z-score)EV/

SalesEV/

EBITDAPrice/ Book

FCF Yield

PEG Ratio

NTM P/E

EV/ Sales

EV/ EBITDA

Price/ Book

FCF Yield P/E

PEG Ratio

Median Z-Score

S&P 500 1.9x 9.8x 2.9x 4.4 % 1.5x 16.5x S&P 500 2.2 0.7 0.9 1.1 1.9 1.9 1.5Consumer Staples 1.5 12.1 4.9 4.6 2.3 19.3 Telecommunication Services (0.9) (1.3) 2.5 0.6 (1.2) (1.1) (1.0)Consumer Discretionary 1.7 9.8 4.5 3.9 1.2 18.6 Energy (1.7) (1.3) (2.4) 0.4 0.2 (0.4) (0.8)Health Care 2.1 12.9 4.3 4.8 1.5 18.2 Utilities NM (0.4) (1.1) (0.3) (0.4) (0.4) (0.4)Materials 1.9 9.7 3.2 3.1 1.5 17.1 Financials NM NM (0.6) NM (0.3) 0.1 (0.3)Utilities NM 9.1 1.8 0.0 3.1 17.1 Consumer Discretionary 0.4 (0.2) 1.4 (0.1) (0.4) (0.9) (0.1)Industrials 2.1 11.2 3.4 4.9 1.5 16.7 Materials 0.0 (0.1) (0.2) 0.9 (0.2) (0.1) (0.1)Information Technology 3.3 11.1 4.4 6.0 1.4 16.5 Industrials (1.4) (0.3) 0.2 0.5 (0.6) 0.2 (0.1)Energy 1.3 5.9 1.8 1.1 1.2 14.4 Information Technology 1.6 (0.1) (0.0) (0.7) (0.5) 0.3 (0.1)Financials NM NM 1.4 NM 1.5 14.1 Health Care 0.7 2.3 1.9 1.1 0.6 (0.6) 0.9Telecommunication Services 2.2 5.5 3.2 7.3 2.1 13.9 Consumer Staples (0.2) 1.1 1.1 (1.2) 0.9 1.6 1.0

16.5

0

5

10

15

20

25

30

1/76 1/81 1/86 1/91 1/96 1/01 1/06 1/11 1/16

NTM

P/E

(x)

10-yr rolling avg

P/E

2.9

0

12

3

45

6

1/76 1/81 1/86 1/91 1/96 1/01 1/06 1/11 1/16

LTM

P/B

(x)

10-yr rolling avg

P/B 0.0

2.0

4.0

6.0

8.0

10.0

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Mar

-14

Jun-

14

Sep

-14

Dec

-14

Mar

-15

Cost ofEquity

10 YearUST

ERP5.2%

2.3%

7.5%

December 5, 2014 United States

Goldman Sachs Global Investment Research 18

Fund Flows, Correlation and Dispersion

Source: FactSet, Lipper, and Goldman Sachs Global Investment Research.

Domestic equity fund flows

(8)

(6)

(4)

(2)

0

2

4

6

8

10

12

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Mar

-14

Jun-

14

Sep

-14

Dec

-14

Mar

-15

$ B

illio

ns

Domestic equity fund flows (4wk avg)

Mutual funds

ETFs

Net flows

Sector and Stock Correlation

0.34

0.65

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Mar

-14

Jun-

14

Sep

-14

Dec

-14

Mar

-15

Ave

rage

Cor

rela

tion

Average stock correlation

Average sector correlation

Weekly mutual fund flowsLipper Weekly Mutual Fund Flows, ex-ETFs ($ billions)

Total Lipper Weekly Flows Total Flows Inflow/(Outflow)Assets 4-Week Avg 2014 YTD (Cons. Weeks)

All Equity 3,840 (1.9) 49.1 (2)

U.S. Equity 2,698 (1.4) 1.6 (2)

Int'l Equity 860 (0.2) 39.5 (2)

Global 282 (0.3) 8.0 (4)

Equity Income 191 (0.1) (2.2) (3)

Gold & Nat Res 43 0.0 10.4 (1)

Money Market 2,382 12.0 (23.4) 7

All Taxable Bond 2,022 2.5 111.8 17

Gov't Treasury 27 0.0 (0.2) (1)

Return Dispersion+/- 1 Standard Deviation

1-Month Returns 3-Month Returns

Current 30-Year Historical Current 30-Year HistoricalDec 4 Average %ile Dec 4 Average %ile

S&P 500 13 pp 17 pp 18 % 26 pp 29 pp 42 %

Energy 20 pp 14 pp 88 % 30 pp 24 pp 82 %

Materials 8 15 2 27 26 64

Consumer Staples 10 13 31 18 21 31

Telecom Services 12 13 57 14 23 29

Health Care 9 15 8 19 25 24

Industrials 8 14 5 19 24 24

Utilities 5 10 2 11 18 19

Consumer Discretionary 11 17 4 23 29 19

Financials 10 14 33 15 23 12

Information Technology 12 20 5 19 36 2

December 5, 2014 United States

Goldman Sachs Global Investment Research 19

US Economics

Our Current Activity Indicator (CAI) measures the growth signal in major high-frequency activity indicators for the US economy, expressed in GDP-equivalent units.

Our Global Leading Indicator (GLI) aggregates 10 global macro time series to provide an early signal of the global industrial cycle. Our “swirlogram” uses GLI growth and acceleration to define four cycle phases.

Source: FactSet and Goldman Sachs Global Investment Research.

GDP Current Activity (CAI) Global Leading Indicator (GLI)

Core PCE and CPI Economic Surprise (MAP) Financial Conditions (FCI)

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Year

ove

r Yea

r cha

nge

(%)

Core CPI

Core PCE

99.4

99.5

99.6

99.7

99.8

99.9

100.0

100.1

100.2

100.3

100.4

100.5

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Financial Conditions Index

Tighter

Looser

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Current Activity Indicator

2.7

1.8

4.5

3.5

(2.1)

4.6

3.9

2.4 3.0 3.0 3.0 3.0

(3.0)%

(2.0)%

(1.0)%

0.0 %

1.0 %

2.0 %

3.0 %

4.0 %

5.0 %

6.0 %

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

GD

P G

row

th (q

oq a

nnua

lized

%)

2013 2014 2015

Goldman SachsEconomics

Consensus

(100)

(75)

(50)

(25)

0

25

50

75

100D

ec-1

2

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Rol

ling

1-M

onth

US-

MAP

Sco

re

Rolling 1-MonthUS MAP Score

PositiveData Surprises

NegativeData Surprises

Nov-14

Dec-12

(0.08)%

(0.06)%

(0.04)%

(0.02)%

0.00 %

0.02 %

0.04 %

0.06 %

(0.2)% (0.1)% 0.0 % 0.1 % 0.2 % 0.3 % 0.4 % 0.5 %

GLI

Acc

eler

atio

n

GLI Growth

Expansion

Slowdown

Recovery

Contraction

December 5, 2014 United States

Goldman Sachs Global Investment Research 20

Goldman Sachs Global Macro Forecasts

Source: FactSet and Goldman Sachs Global Investment Research.

Goldman Sachs Global Macro Forecasts

units Current 3m 6m 12m TargetEquities

TOPIX level 1441 1450 1550 1650 15 %STOXX Europe 600 level 345 360 375 390 13Asia Pac Ex-Japan level 475 490 505 520 10S&P 500 level 2072 2100 2150 2100 1

Ten Year RatesUS % 2.3 2.6 2.8 3.0 74 bpEuro Area (Germany) % 0.7 1.1 1.2 1.3 52Japan % 0.4 0.7 0.7 0.8 37

CurrenciesUS Dollar / Yen $/¥ 120 120 125 130 9 %Sterling / US Dollar £/$ 1.57 1.60 1.58 1.53 (3)Euro / US Dollar EUR/$ 1.24 1.23 1.20 1.15 (8)

EnergyBrent Crude Oil $/bbl 70 85 80 85 22 %WTI Crude Oil $/bbl 67 75 70 75 12NYMEX Nat. Gas $/mmBtu 3.65 4.00 4.10 4.00 10

MetalsLME Copper $/mt 6491 6600 6200 6000 (8)%COMEX Gold $/troy oz 1208 1195 1135 1050 (13)

EPS Forecast EPS Growth NTM P/E Div

2013 2014 2015 2014 2015 Current YE 2014 Yield

TOPIX ¥ 81 ¥ 91 ¥ 111 12 % 22 % 15.9 x 12.9 x 1.9 %

STOXX Europe 600 € 21 € 22 € 23 6 6 15.7 14.6 3.6

Asia Pac(Ex-Japan) $ 35 $ 37 $ 40 6 7 12.7 12.3 3.3

S&P 500 $ 107 $ 116 $ 122 9 5 17.8 16.8 2.1

Goldman Sachs US Economics Forecasts% Annual Change

2013 2014E 2015EReal GDP 2.2% 2.3% 3.1%

Consumer Spending 2.4 2.3 3.0Total Fixed Investment 4.7 5.1 6.5

Business Fixed Investment 3.0 5.9 5.6Residential Investment 11.9 2.0 9.7

Federal Government Spending (5.7) (1.9) (1.4)State and Local Government 0.5 0.9 1.8Net Exports (Bil.) (420) (442) (471)

InflationHeadline CPI 1.5 1.7 1.3Core CPI 1.8 1.8 1.9Core PCE 1.3 1.4 1.5

Unemployment Rate 7.4 6.2 5.6Fed Funds Rate 0.1 0.1 0.610-year Treasury Rate 3.0 2.5 3.0

Global Equity Market performancePrice Return (%) US Dollar Local

Market 1-Week 1-Month 3-Month 2014 YTD Currency

U.S. (S&P 500) (0)% 3 % 4 % 12 % 12 %China (MSCI China) 0 2 (4) 4 4Japan (TOPIX) 1 (0) (2) (3) 11Spain (IBEX 35) (1) 3 (8) (3) 7Europe (DJ Stoxx 600) (1) 3 (5) (5) 5Australia (ASX 200) (2) (6) (15) (6) 0UK (FTSE 100) (1) 2 (7) (6) (1)Korea (KOSPI) (0) (1) (12) (7) (1)Germany (Dax) (1) 6 (3) (7) 3Mexico (Bolsa) (7) (8) (14) (7) 0Brazil (Bovespa) (10) (8) (27) (9) (0)France (CAC 40) (2) 4 (8) (9) 1

Average (2)% (0)% (8)% (4)% 3 %

Goldman Sachs Global Investment Research 21