us subprime crisis

Post on 19-Oct-2014

2.938 views

DESCRIPTION

The project gives a detailed understanding of the US Sub prime Crisis and how things unfolded. Though the scope of the project is limited to a specific time frame, the project report entails all the nitty gritties of the occurrence of eventsTRANSCRIPT

0

The U.S. Sub-prime Crisis – A Study of the recent economic development in the U.S. and their likely impact on the Indian Economy

A report submitted in partial fulfillment of the requirements of MBA program at ICFAI Business School, Ahmedabad.

Submitted to: Submitted to: Prof. Vivek Ranga Mr. Sunil Chandra Faculty Guide (Country Head-DPM) IBS, Ahmedabad. Almondz Global Securities Ltd.

1

A REPORT ON

The U.S. Sub-prime Crisis – A Study of the recent economic development in the U.S. and their likely impact on the Indian Economy

BY

PARAMJEET KAUR

AT ALMONDZ GLOBAL SECURITIES LIMITED

NEW DELHI

A report submitted in partial fulfillment of the requirements of MBA program at ICFAI Business School, Ahmedabad.

Submitted to: Submitted to: Prof. Vivek Ranga Mr. Sunil Chandra Faculty Guide (Country Head-DPM) IBS, Ahmedabad. Almondz Global Securities Ltd.

2

SUMMER INTERNSHIP PROGRAMME

The U.S. Sub-prime Crisis – A Study of the recent economic development in the U.S. and their likely impact on the Indian Economy

Submitted By: Name: Paramjeet Kaur Enrollment No.:07 BS 2784

Mobile No.:09974339611 Email ID:[email protected]

3

4

ACKNOWLEDGEMENT

Across the road to the Corporate World, Unknown pursuits came my way. A ‘Thanks’ would be too small a token, for all that with what I stand today!

The fourteen weeks Summer Internship Programme needs a laudable appreciation for the novel experience of practical knowledge and the true insights of the clichéd Corporate Culture. Thanking all the affiliates’, veterans in knowledge and virtuoso in experience would be a mere token of gratitude, which may not be sufficient for all the knowledge imparted, and all the blessings bestowed upon me.

I would like to express my immense gratitude to Mr. Sunil Chandra (Country Head, Debt Portfolio Management) for guiding me throughout the whole project with his impeccable knowledge. I owe my gratitude to Ms. Rajni Dasgupta (Vice President) who taught me the first lesson of corporate culture. Mr. Abhilash Kumar (Manager) owes a special mention for the invaluable insights that he provided me, which would be carried forward as a legacy of knowledge and learning all through my life.

I am also thankful to all the staff members’ of Almondz Global Securities Limited, who have always guided me whenever I needed help and acquainted me with the minutest details of etiquettes and behavioral aspects.

I sincerely thank Mr. Vivek Ranga, who has always been a continuous source of encouragement all through the project. I am also thankful to my faculty members and Prof. P. Bala Bhaskaran for guiding me all the way. All the more, ICFAI University needs to be praised which has provided the students with such a bright opportunity to have an exposure of the real corporate environment for the valuable period of three and a half months to get the corporate ambience imprinted on our minds to carry forward the learning’s of this first tryst with corporates in the future struggle in the path of professional success.

Last but not the least, a special mention must be made to all those who have knowingly and unknowingly helped me in the completion of this project. I owe my gratitude to my parents who have always encouraged me in the pursuit of excellence.

Paramjeet Kaur 07 BS 2784

5

TTAABBLLEE OOFF CCOONNTTEENNTTSS

ABSTRACT 10

INTRODUCTION 11

Purpose of the Study 11

Scope of the Study 12

Limitations of the Study 12

Methodology of the Study 13

INTRODUCTION 14

HOUSING MARKETS IN U.S.A.: Major Contributor to Growth 16

Homeownership‐ The American Dream 16

Economic Impacts of the Housing Sector 18

Housing Sector having Macro‐economic Implications 20

Impact on Communities 20

Impact on Individuals 21

Housing Contribution to Society 22

LEVERAGED SECURITY MARKETS: The Double Edged Sword 23

Leveraging 23

Housing Sector: The Initial Fuel 23

Securitization: Prime Mover of the Crisis 24

Sub‐prime Crisis: A result of Leveraging 26

SUB‐PRIME LENDING: The Flaws 29

THE CRISIS AND CHRONONOLOGY OF EVENTS: Timeline of Implosion 32

Chronology of Events 36

6

THE PARTIES IN THE CRISIS AND THEIR ROLE: Walking the Line 53

Role of Borrowers 53

Role of Financial Institutions 55

Role of Securitization 56

Role of Mortgage Brokers and Mortgage Underwriters 57

Role of Government and Regulators 58

Role of Credit Rating Agencies 58

Role of Central Banks 59

IMPACT OF THE CRISIS ON THE U.S.A.: Entering A Possible Recession 61

Collapsing US Housing markets 63

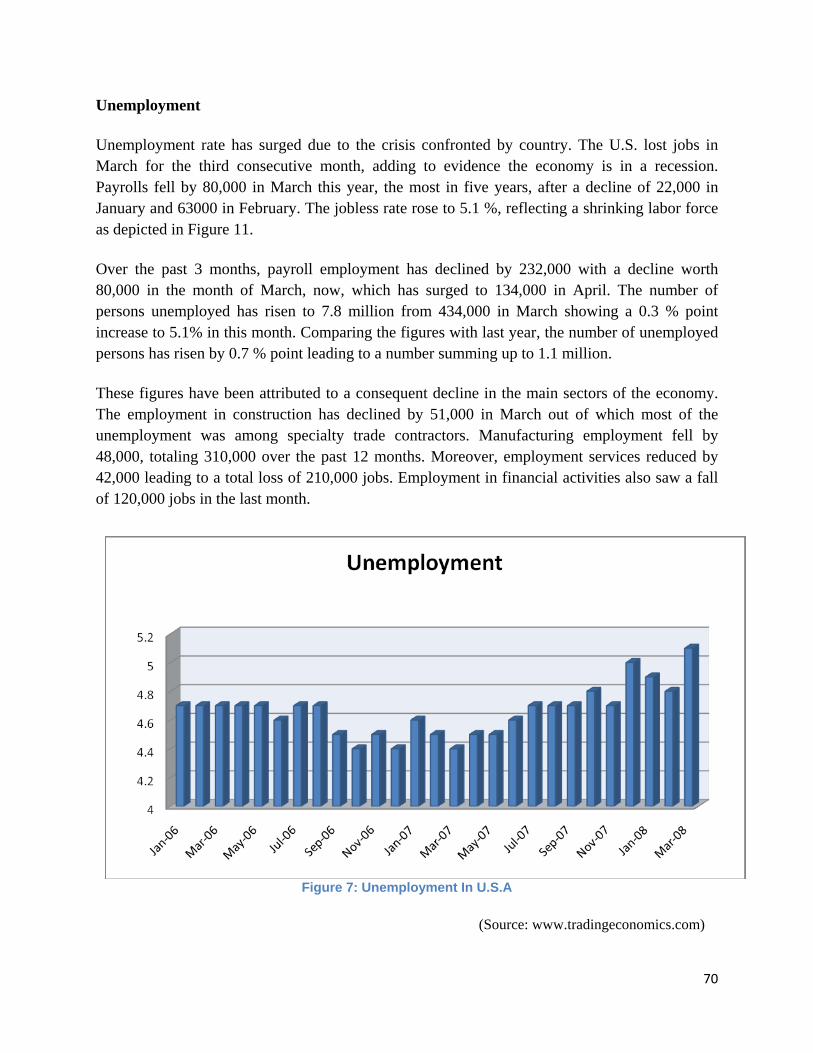

Unemployment 68

Fed rate cut 69

Inflation 70

Falling dollar 71

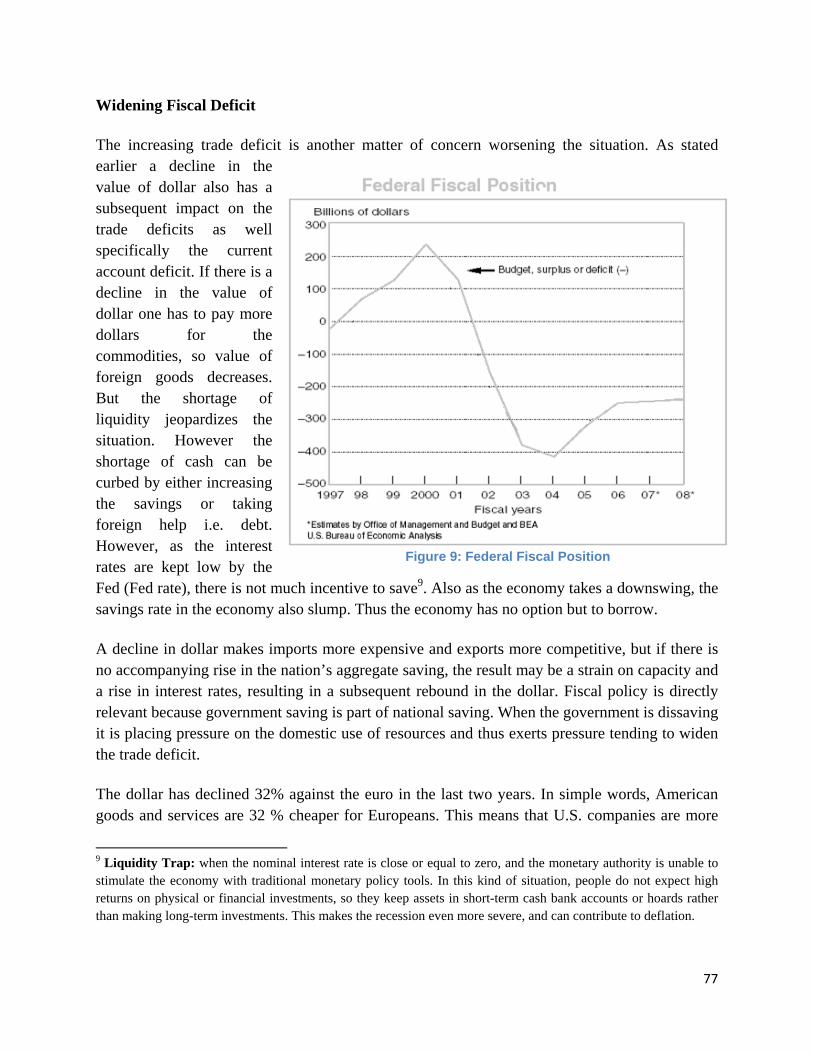

Widening fiscal deficit 75

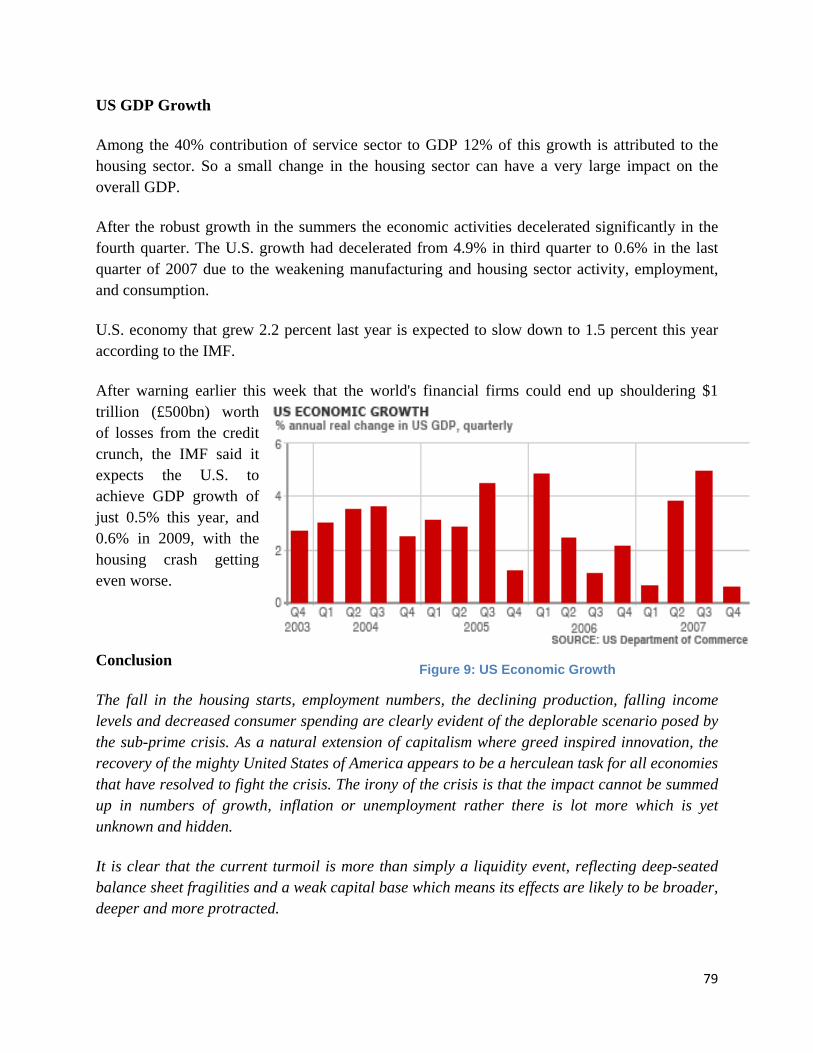

US GDP growth 77

IMPACT OF THE CRISIS ON THE WORLD FINANCIAL MARKETS 78

Impact on the Commodities Markets: Markets pivot on its head 82

Gold Markets 83

Crude Oil 85

Metals 86

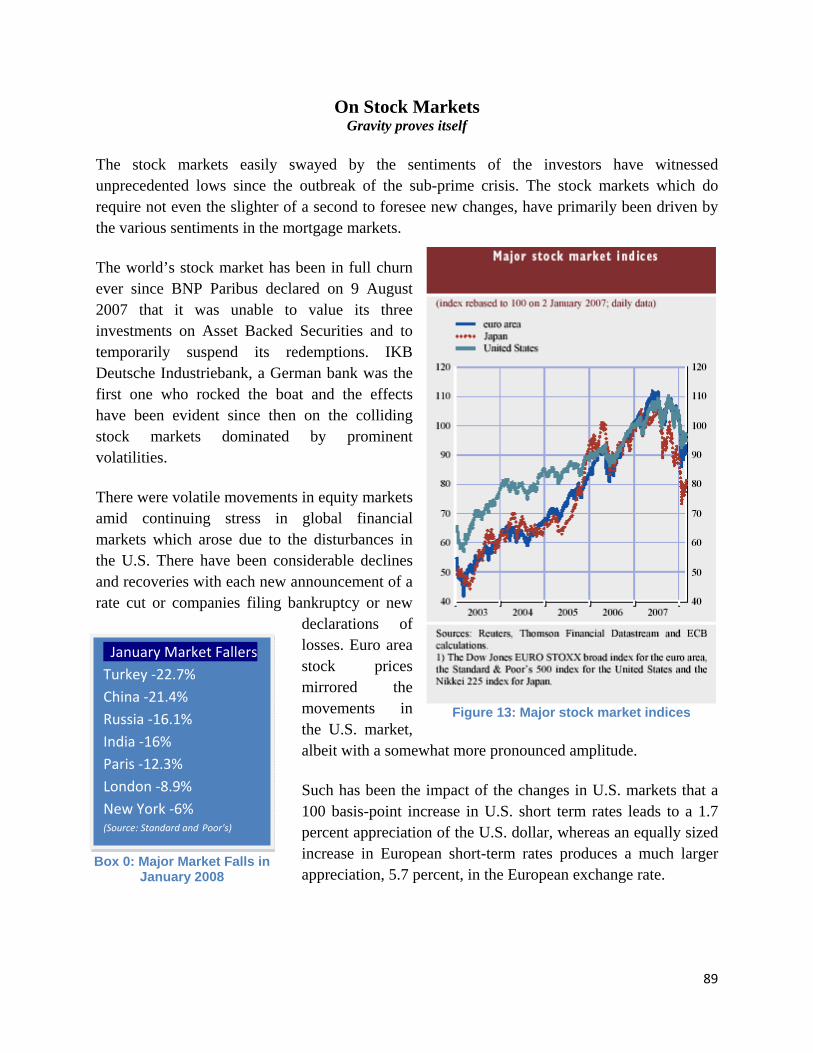

On Stock Markets: Gravity proves itself 87

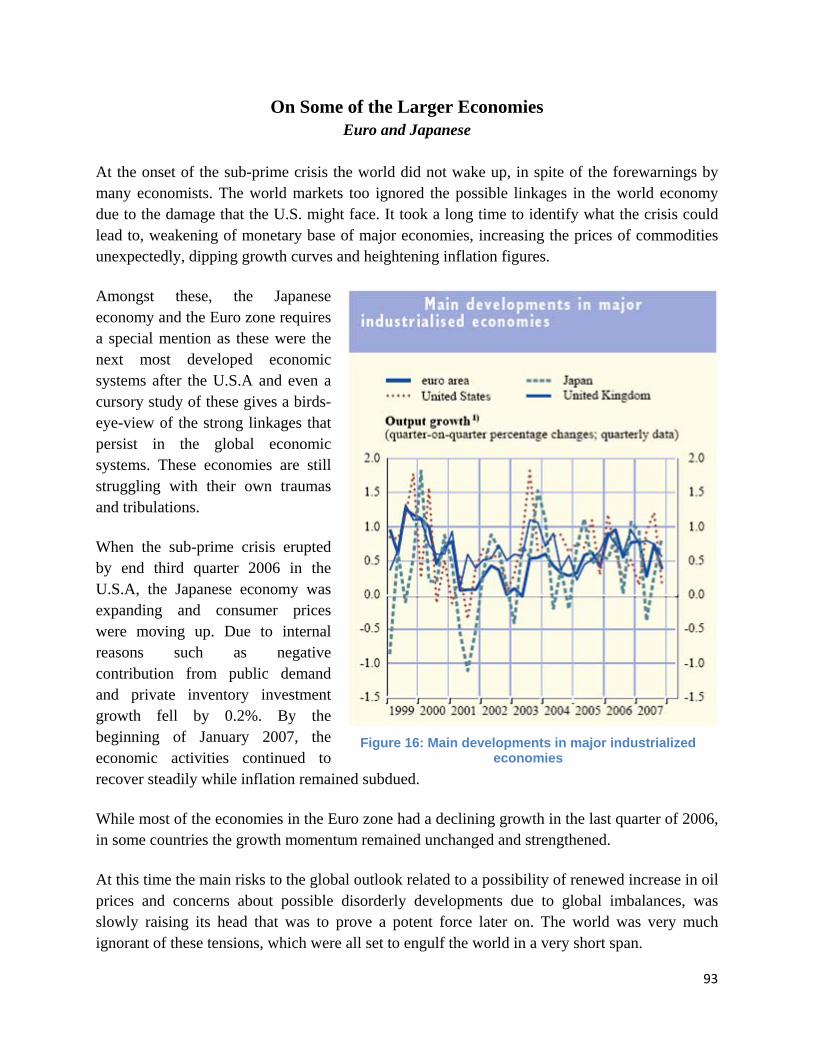

On Some of the Larger Economies: Euro and Japanese 91

7

IMPACT ON INDIA 96

The First Signs: First Blood 98

On Financial Markets: Stock Markets lose their Sheen 100

On Commodities markets with special emphasis on Crude oil: A fuel to inflation 102

On Money Markets and Interest Rates: The Hinges of Growth 104

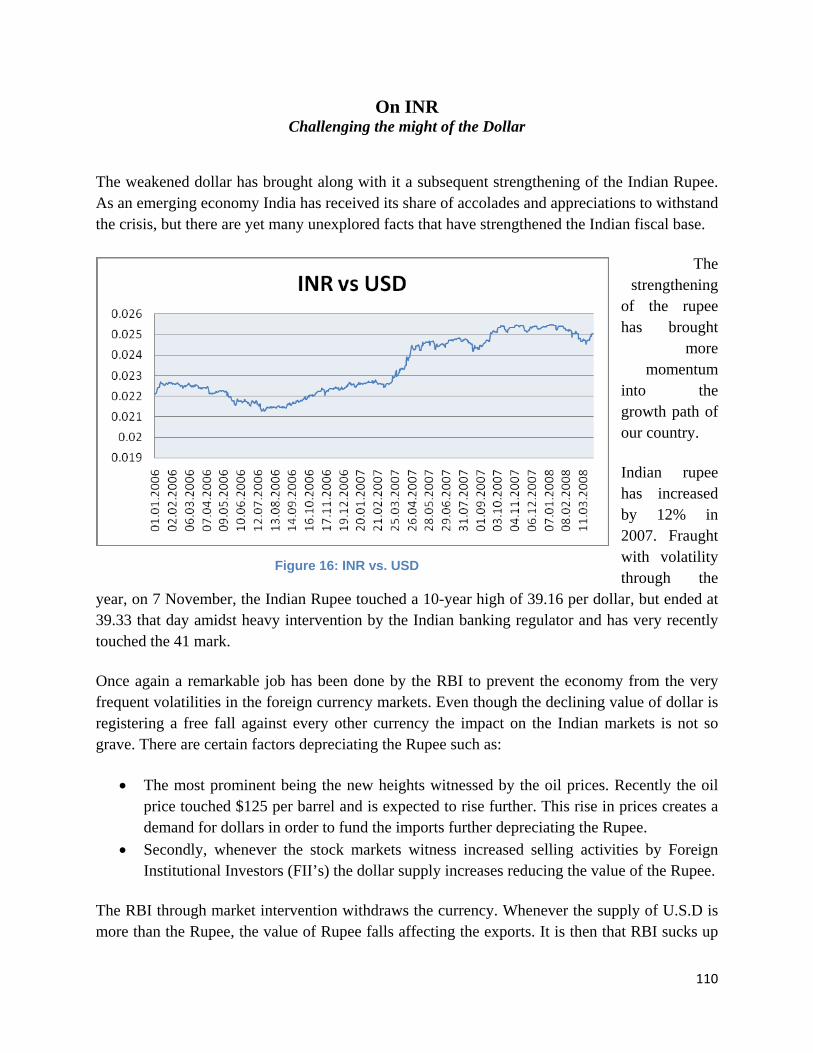

On INR: Challenging the might of the Dollar 107

Indian Housing Markets: Following the Footsteps 109

On Indian Economy: Structural Changes: The proverbial struggle of Good vs. Bad 112

THE NEW WORLD ORDER: Rise Of the Behemoth 114

APPENDIX

Appendix 1: Borrowers Protection Act 2007 118

Appendix 2: Beige Book 125

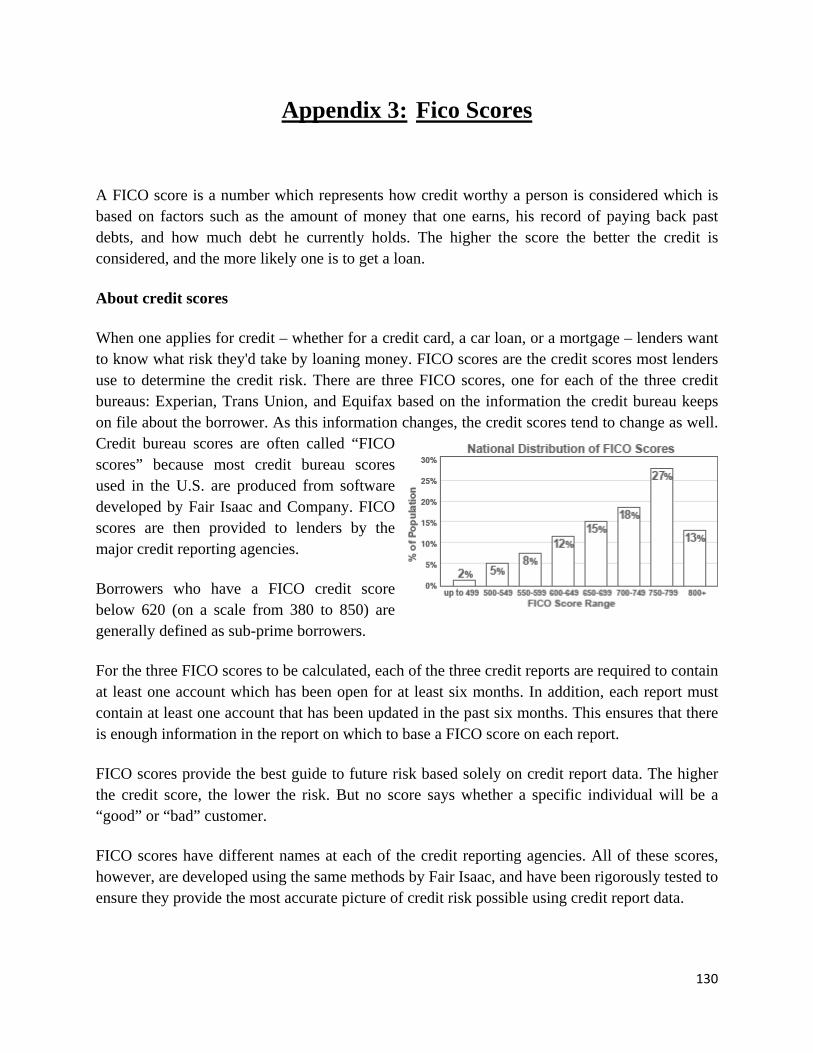

Appendix 3: Fico Scores 127

Appendix 4: Role of Freddie Mac and Fannie Mae 129

Appendix 5: Housing Market Correction & Bursting of Housing Bubble 131

Appendix 6: Asian Currency Crisis 131

Appendix 7: Russian debt Crisis 132

Appendix 8: Long‐Term Capital Management 133

Appendix 9: Relation between Crude Oil & Dollar Value 134

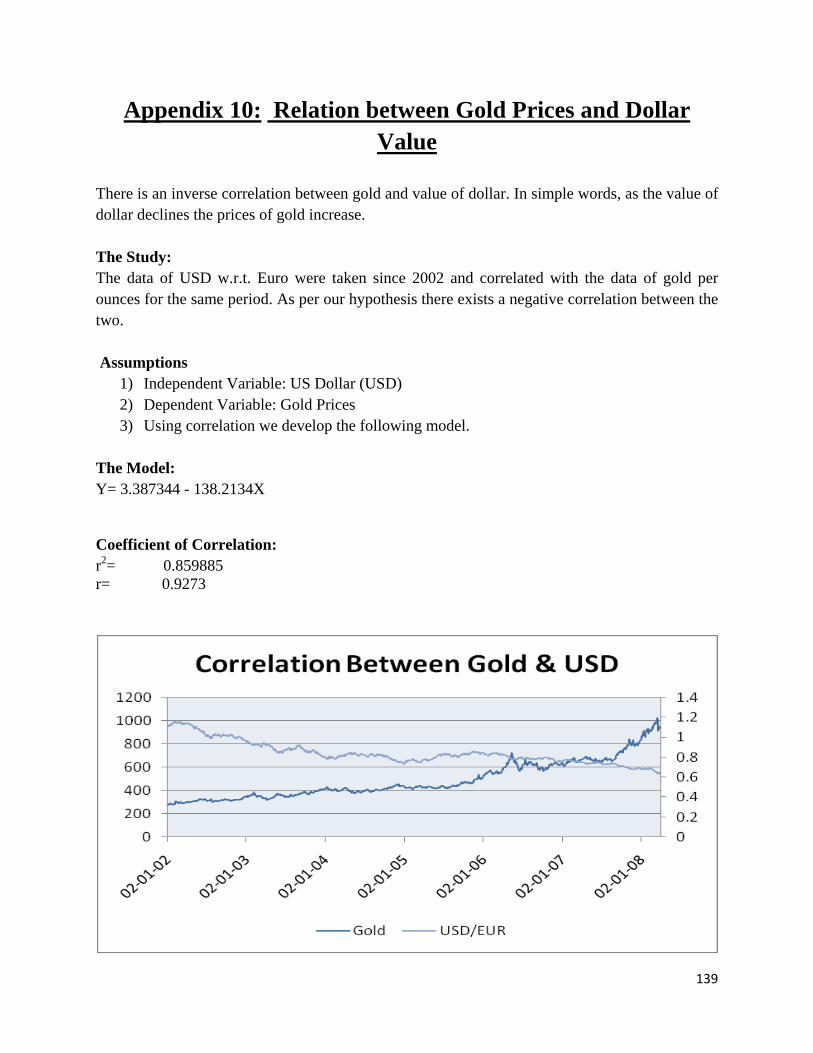

Appendix 10: Relation between Gold Prices & Dollar Value 136

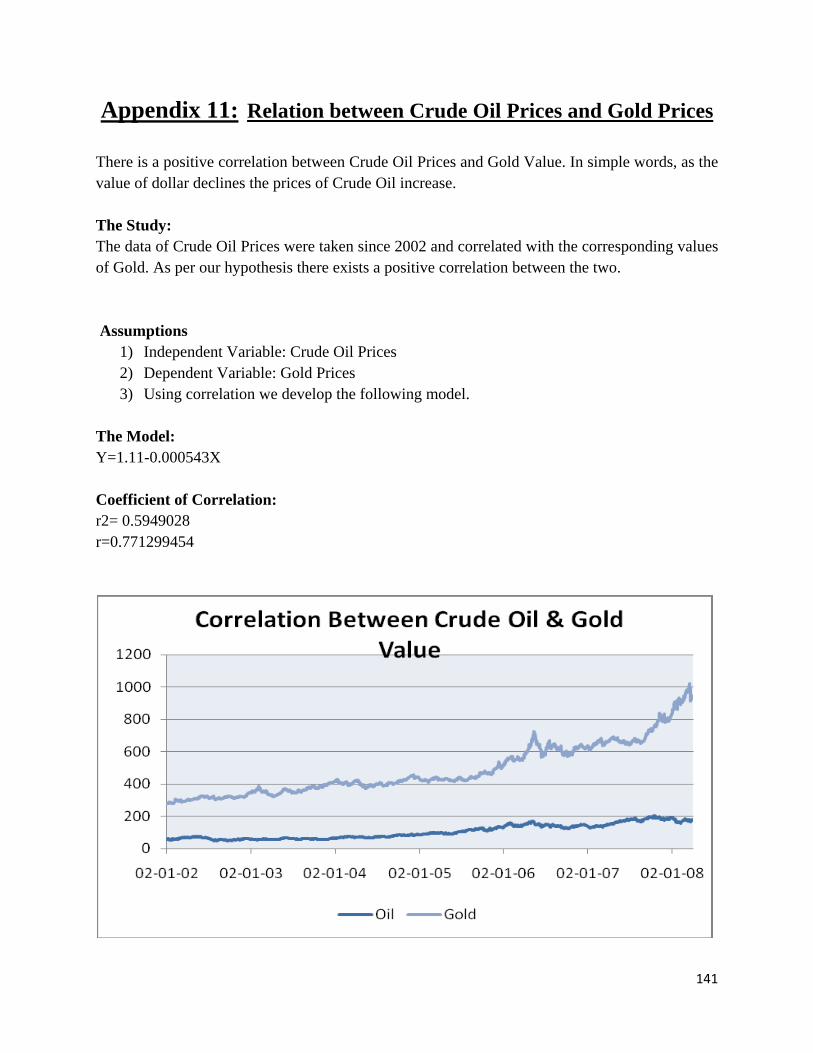

Appendix 11: Relation between Crude Oil & Gold Prices 138

Appendix 12: Theory of Decoupling 140

GLOSSARY 141

BIBLIOGRAPHY 143

8

TTAABBLLEE OOFF FFIIGGUURREESS AANNDD IILLLLUUSSTTRRAATTIIOONNSS

Figure 1: Housing Sector creates a vicious circle 14

Figure 2: Real Median Household Income 17

Figure 3: Homeownership trends in USA (in '000) 18

Figure 4: Mechanism of Securitization 25

Figure 5: Timeline of Implosion 34

Figure 6: US Foreclosure Filings 55

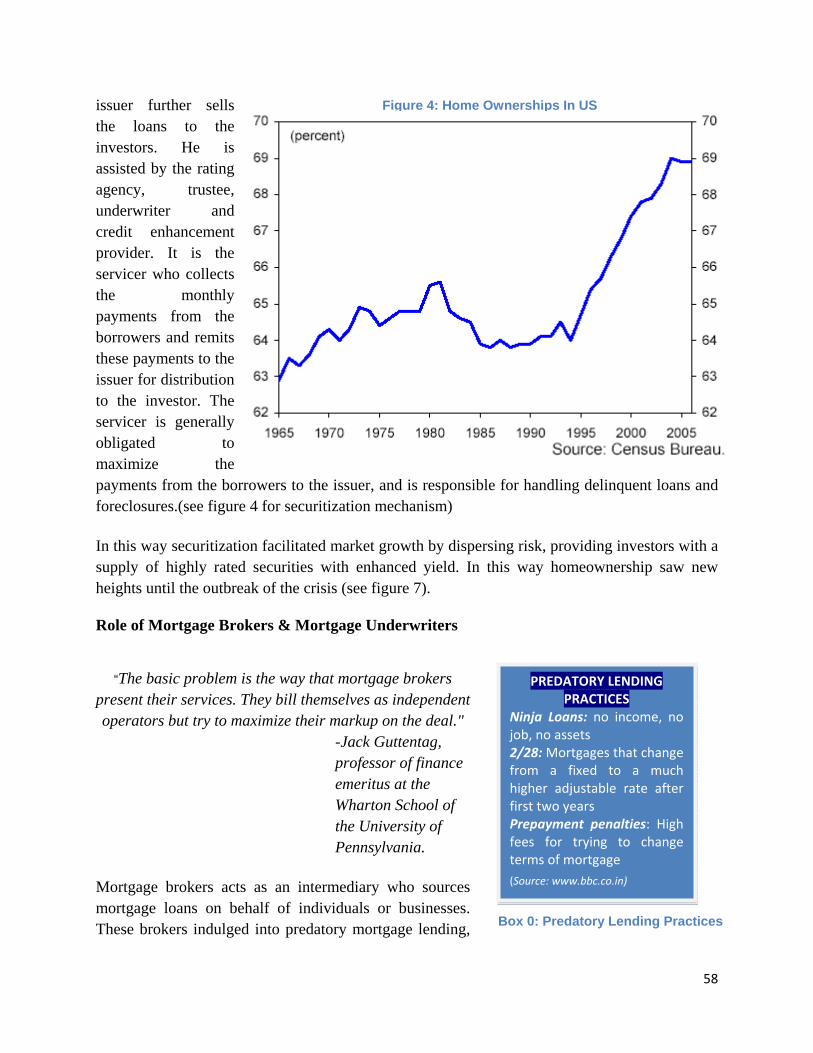

Figure 7: Home Ownerships in US 57

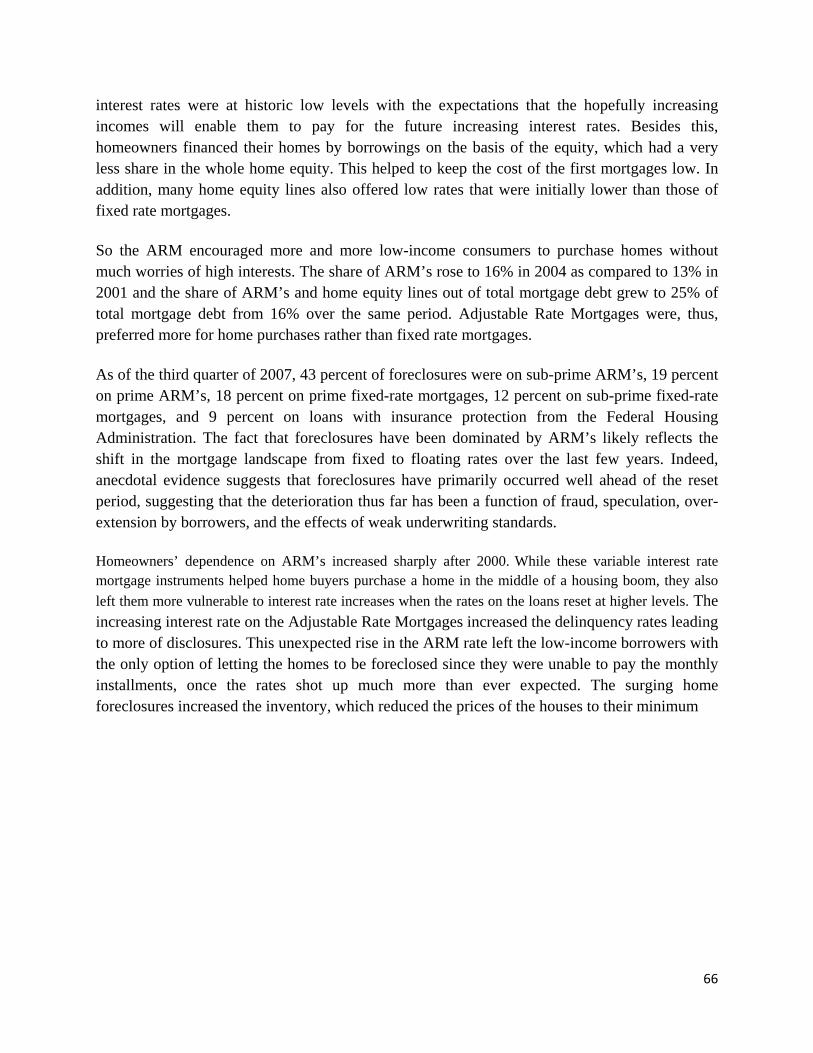

Figure 8: Relative Size of Variable Interest Rate Mortgages 65

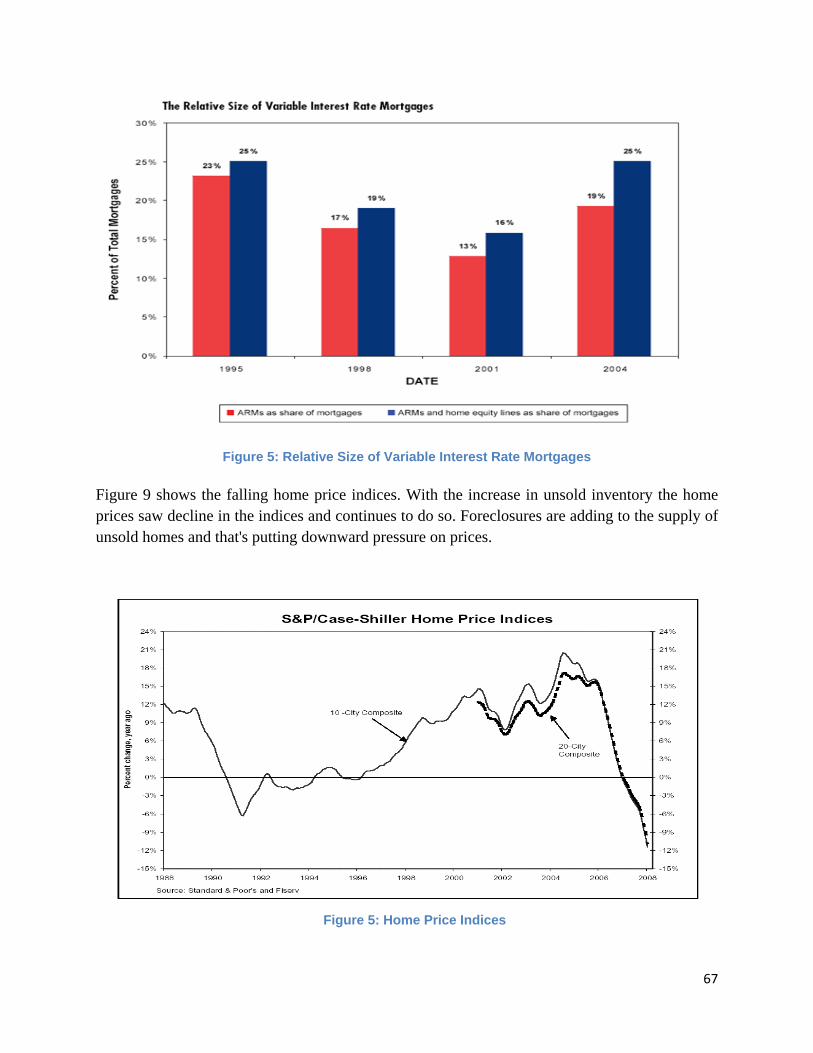

Figure 9: Home Price Indices 65

Figure 10: Foreclosure starts rate 66

Figure 11: Unemployment in USA 68

Figure 12: Fed Rate cuts in US 69

Figure 13: Inflation Rate in USA 70

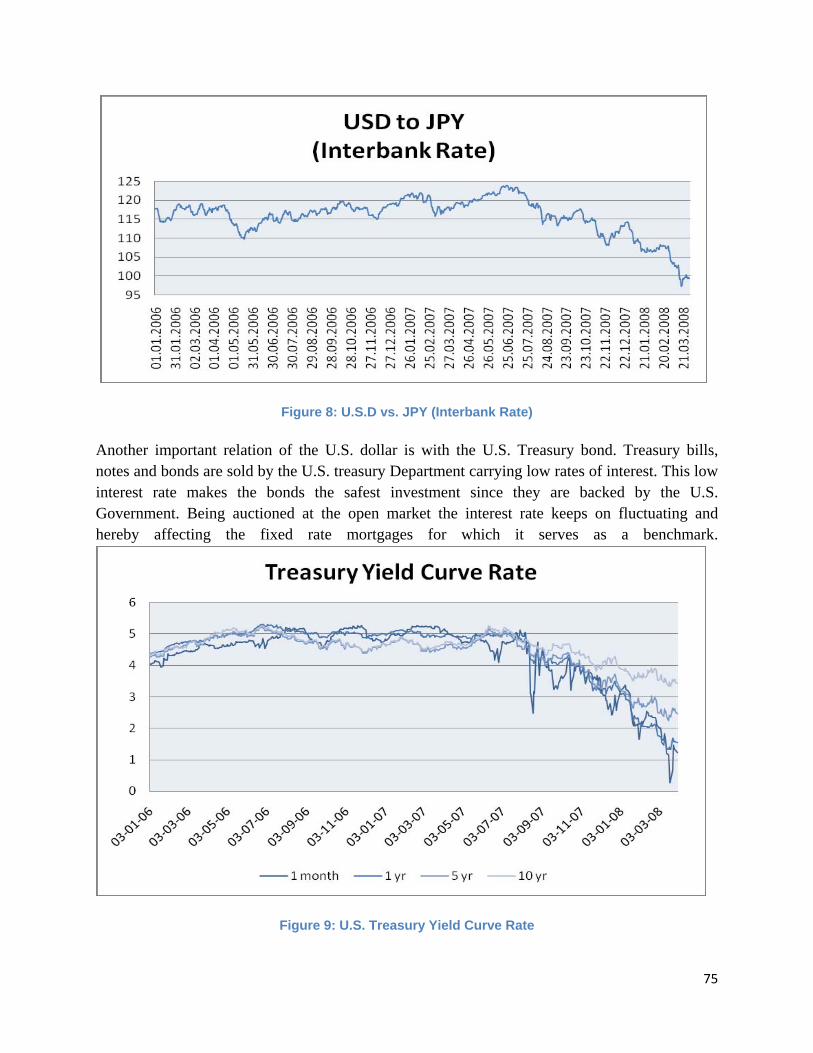

Figure 14: USD vs. Euro (Interbank Rate) 72

Figure 15: USD vs. JPY (Interbank Rate) 73

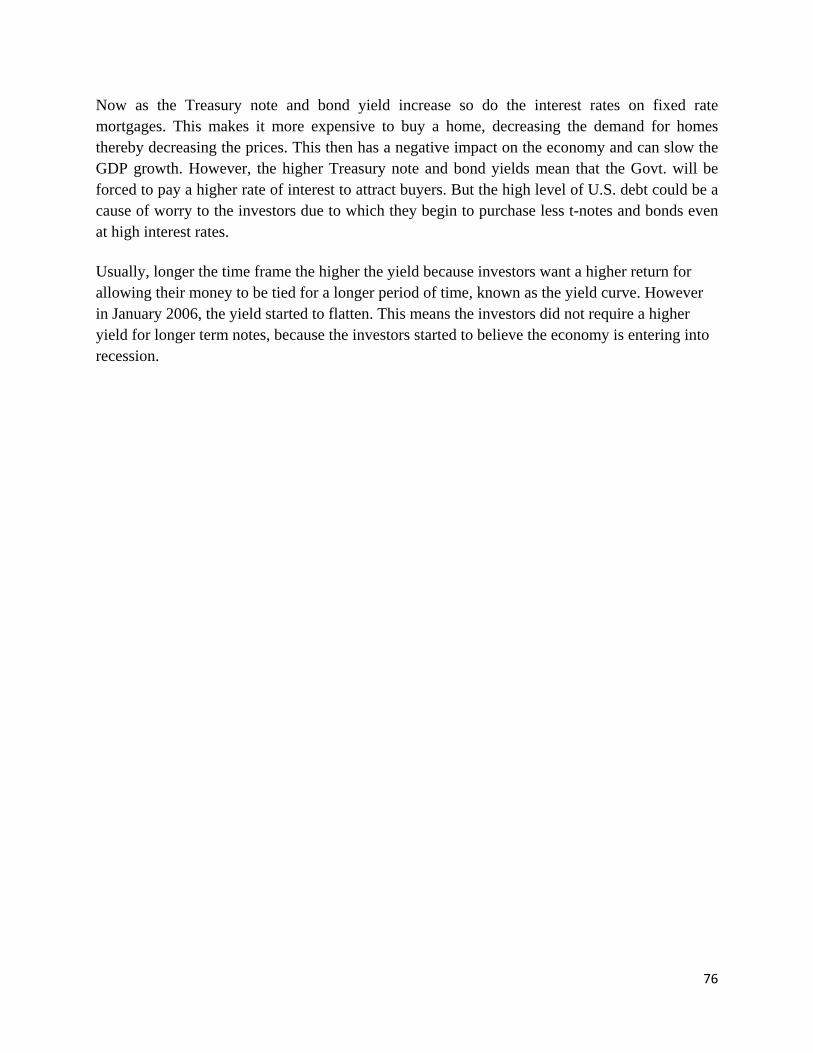

Figure 16: U.S. Treasury Yield Curve Rate 73

Figure 17: Federal Fiscal Position 75

Figure 18: US Economic Growth 77

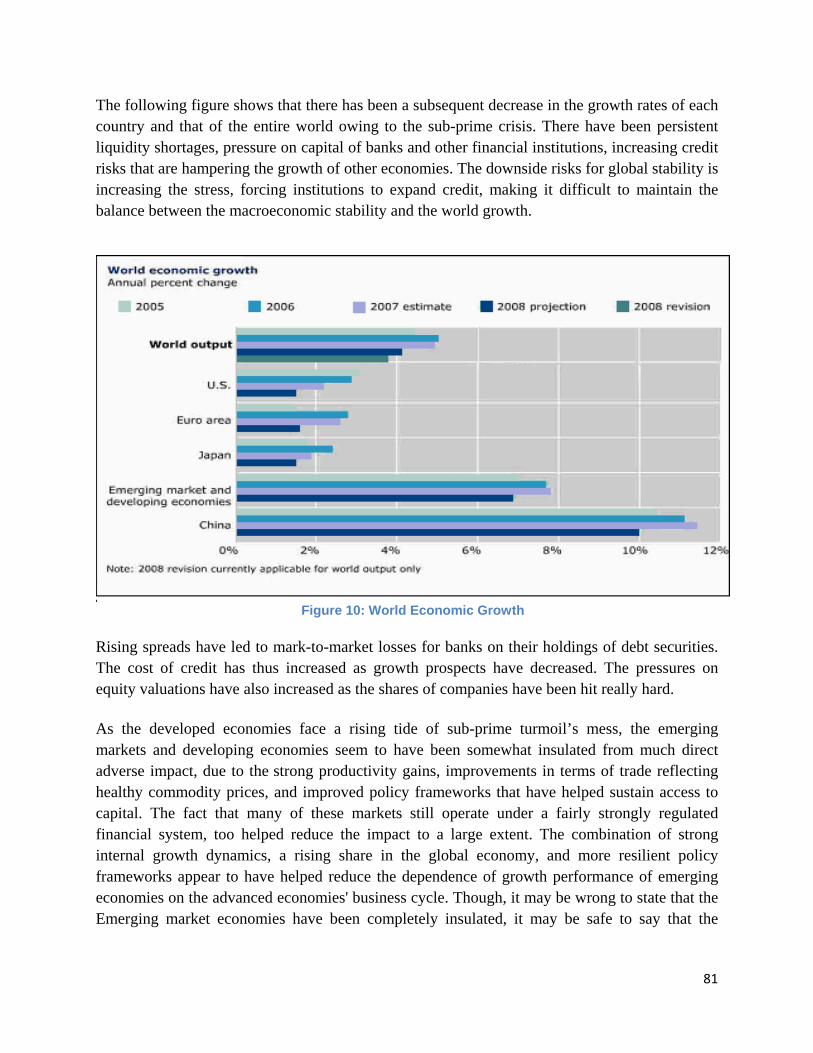

Figure 19: World Economic Growth 79

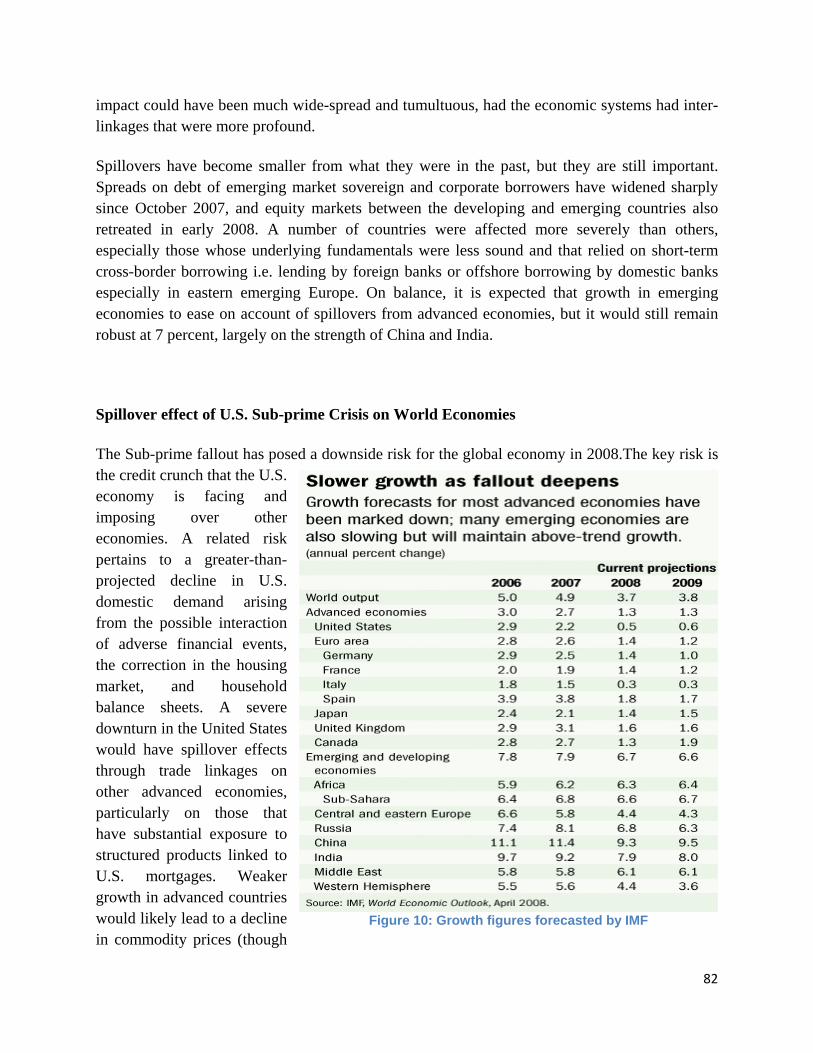

Figure 20: Growth figures forecasted by IMF 80

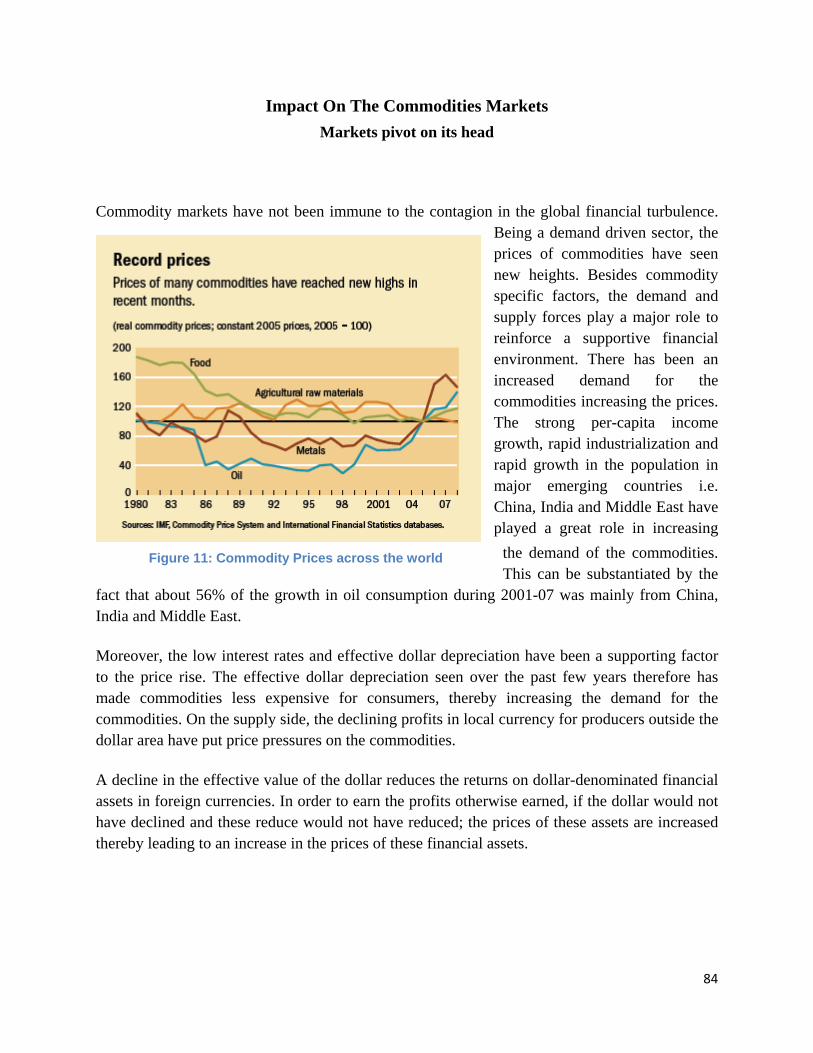

Figure 21: Commodity Prices across the world 82

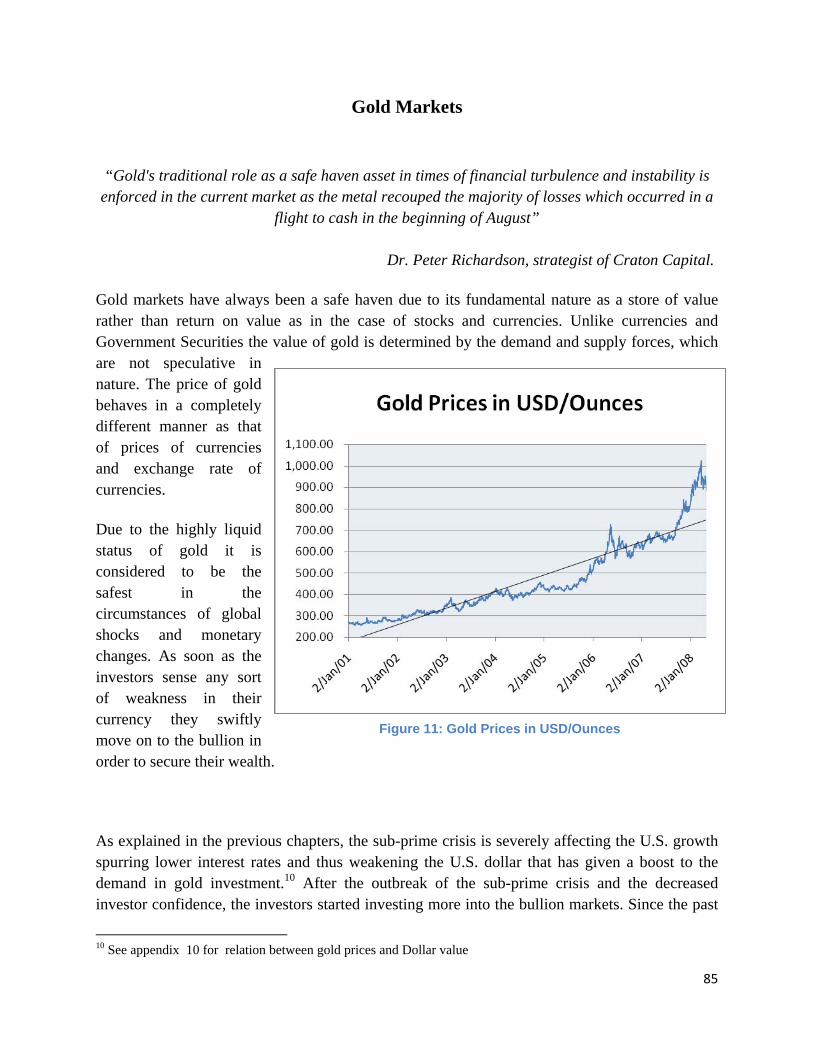

Figure 22: Gold Prices in USD/Ounces 83

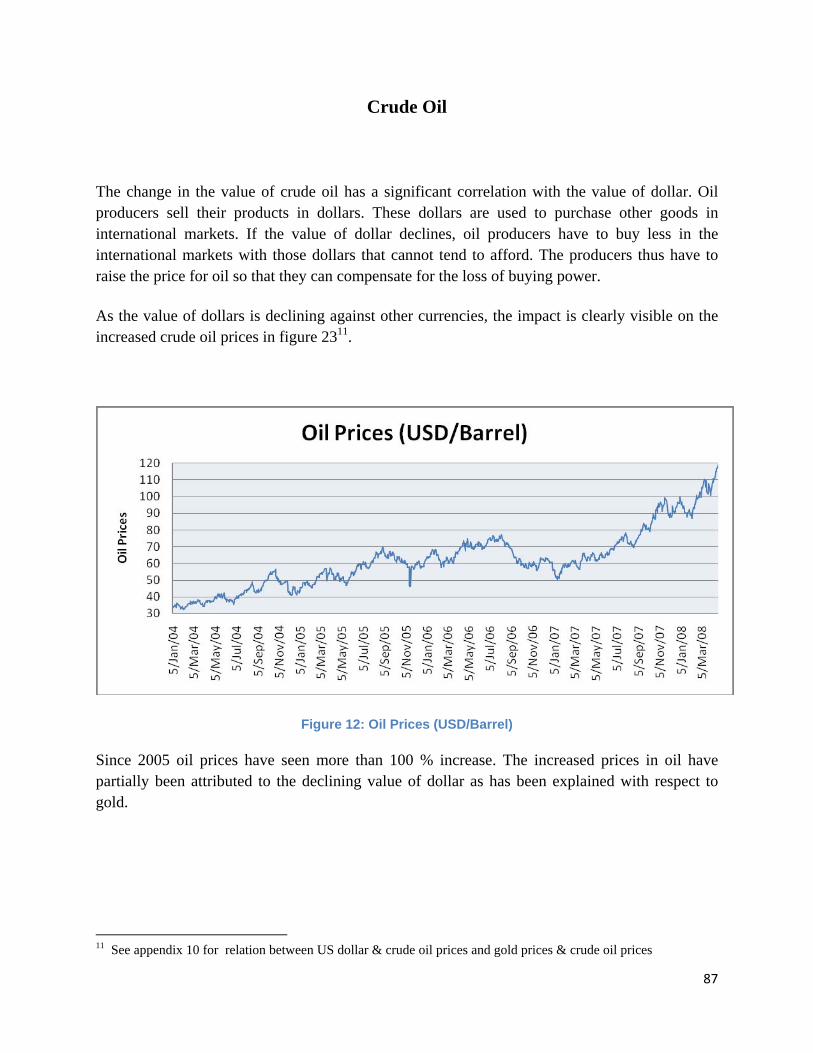

Figure 23: Oil Prices in USD/Barrel 85

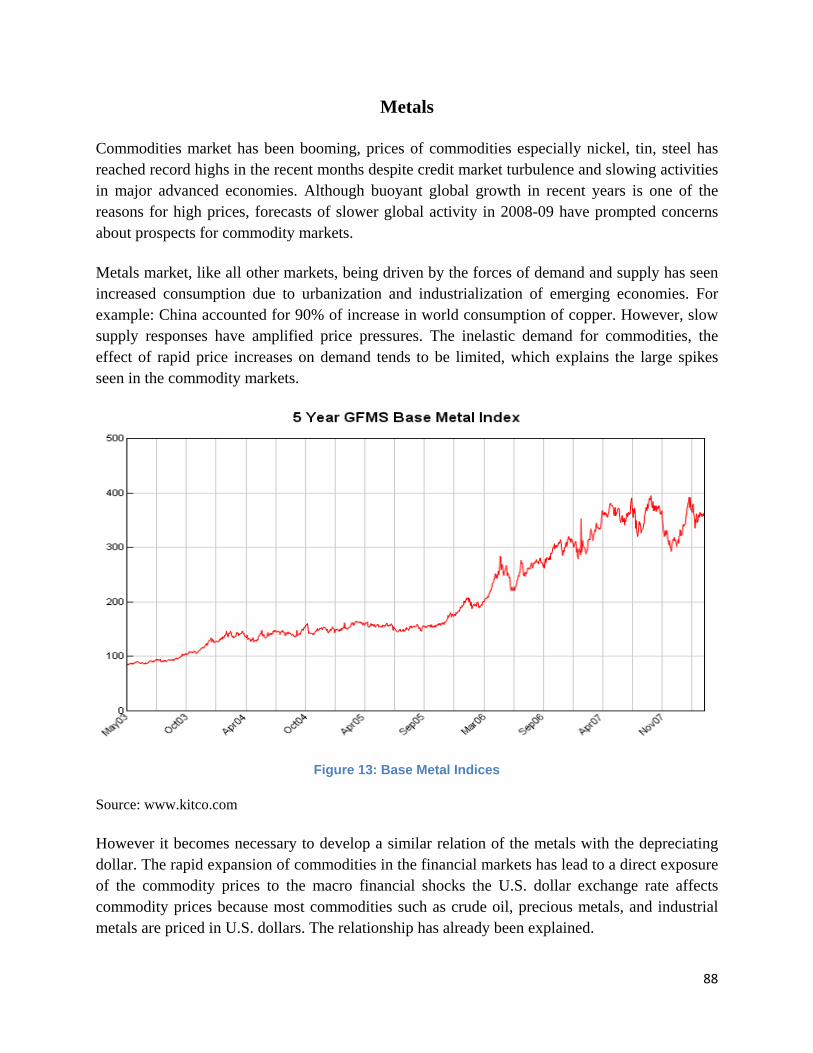

Figure 24: Base Metal Indices 86

9

Figure 25: Major stock market indices 87

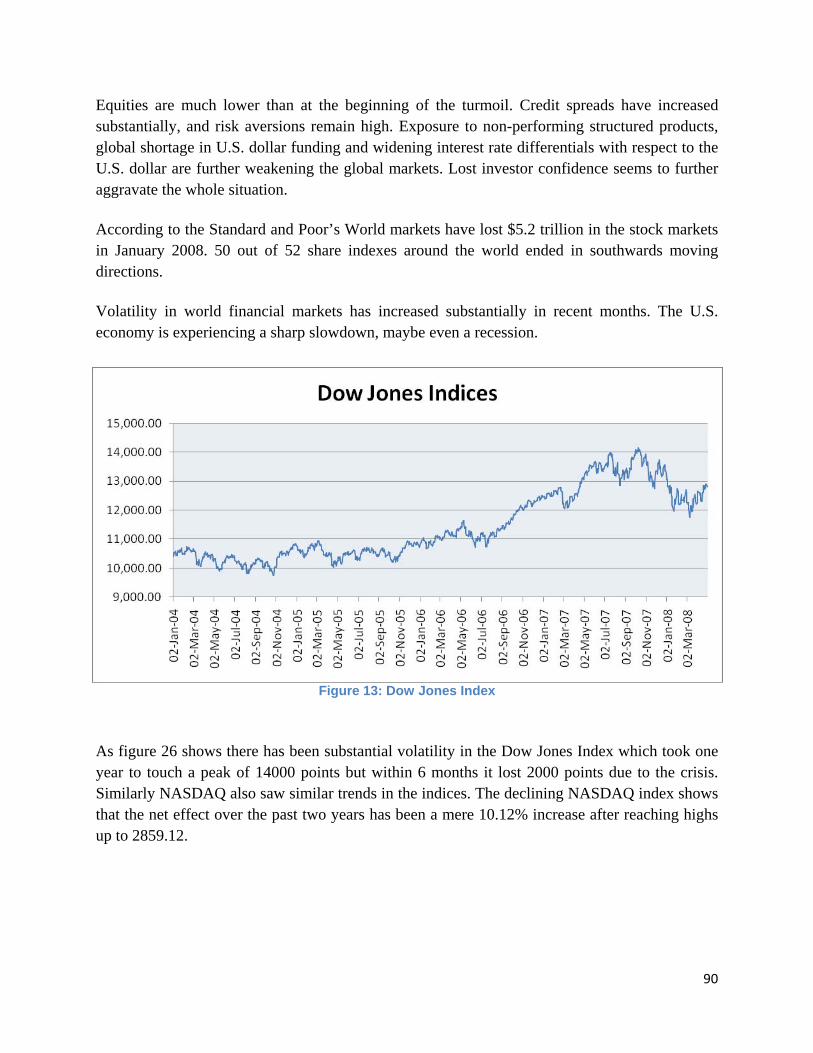

Figure 26: Dow Jones Index 88

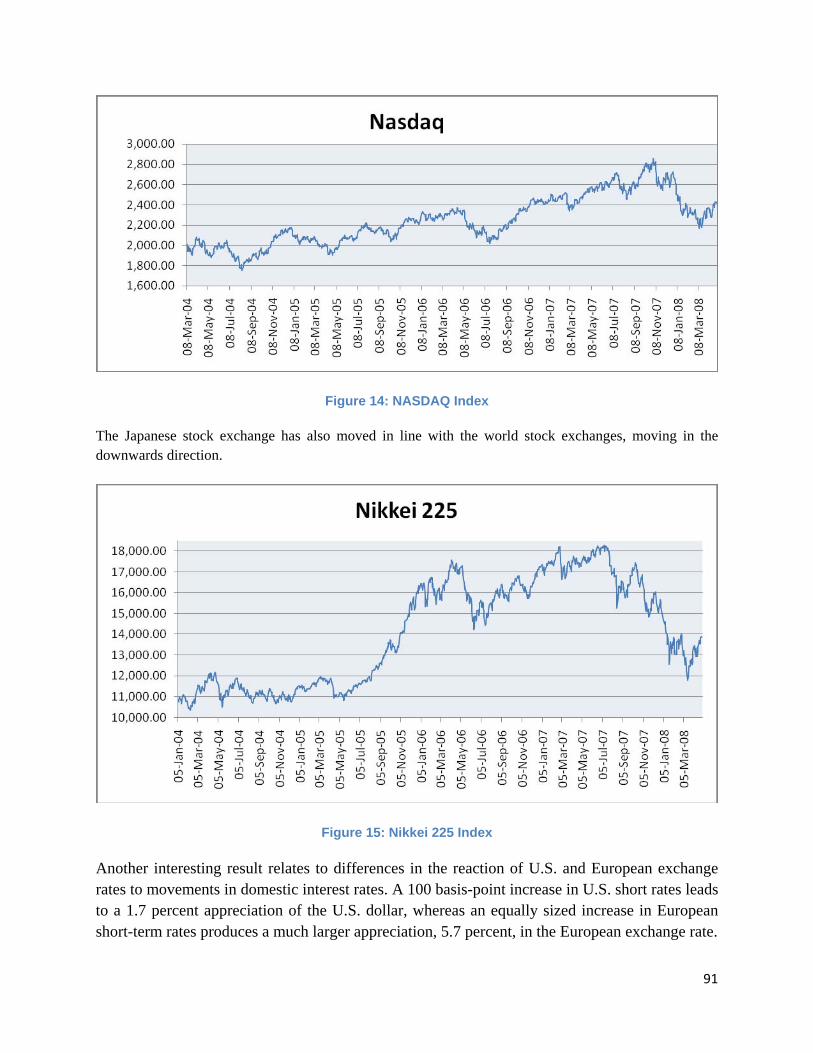

Figure 27: NASDAQ Index 89

Figure 28: Nikkei 225 Index 89

Figure 29: DAX Index 90

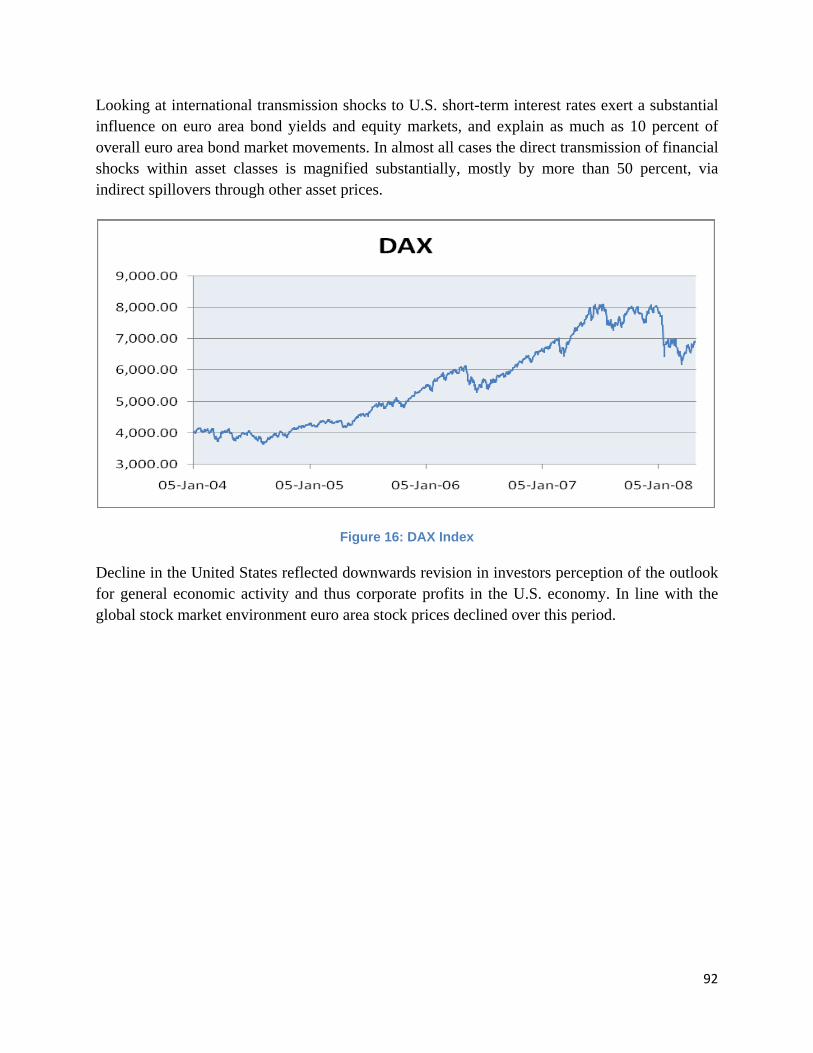

Figure 30: Main developments in major industrialized economies 91

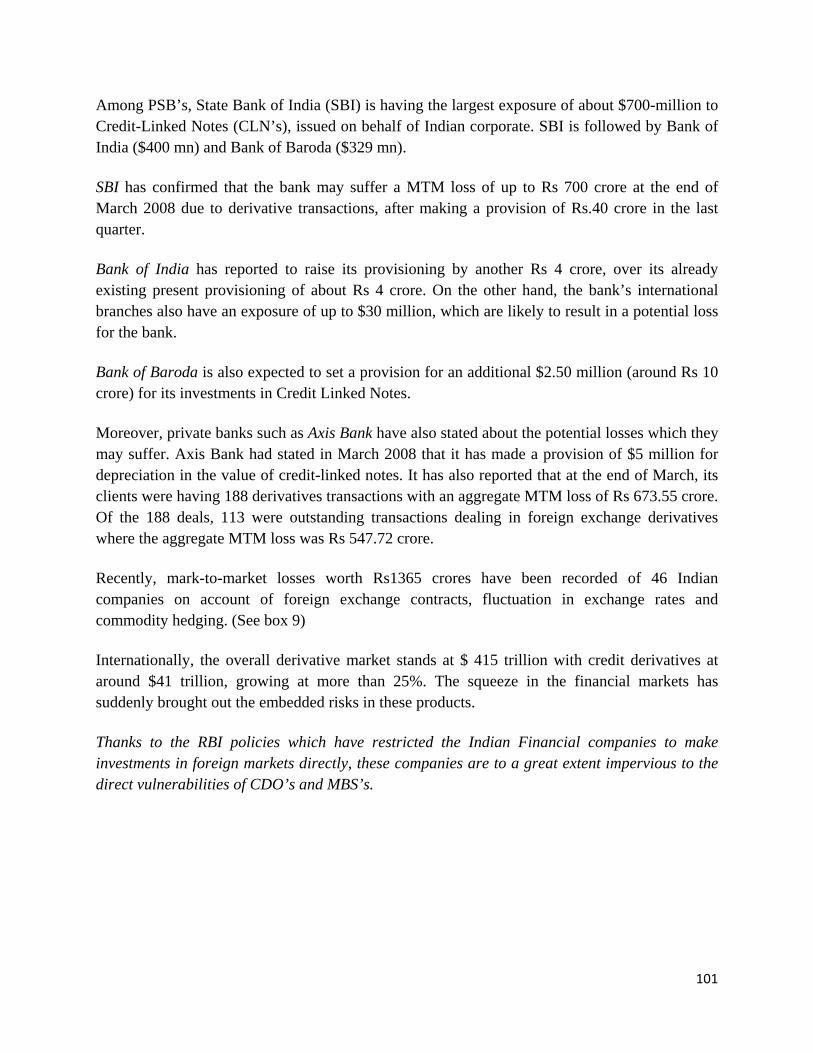

Figure 31: BSE Sensex 100

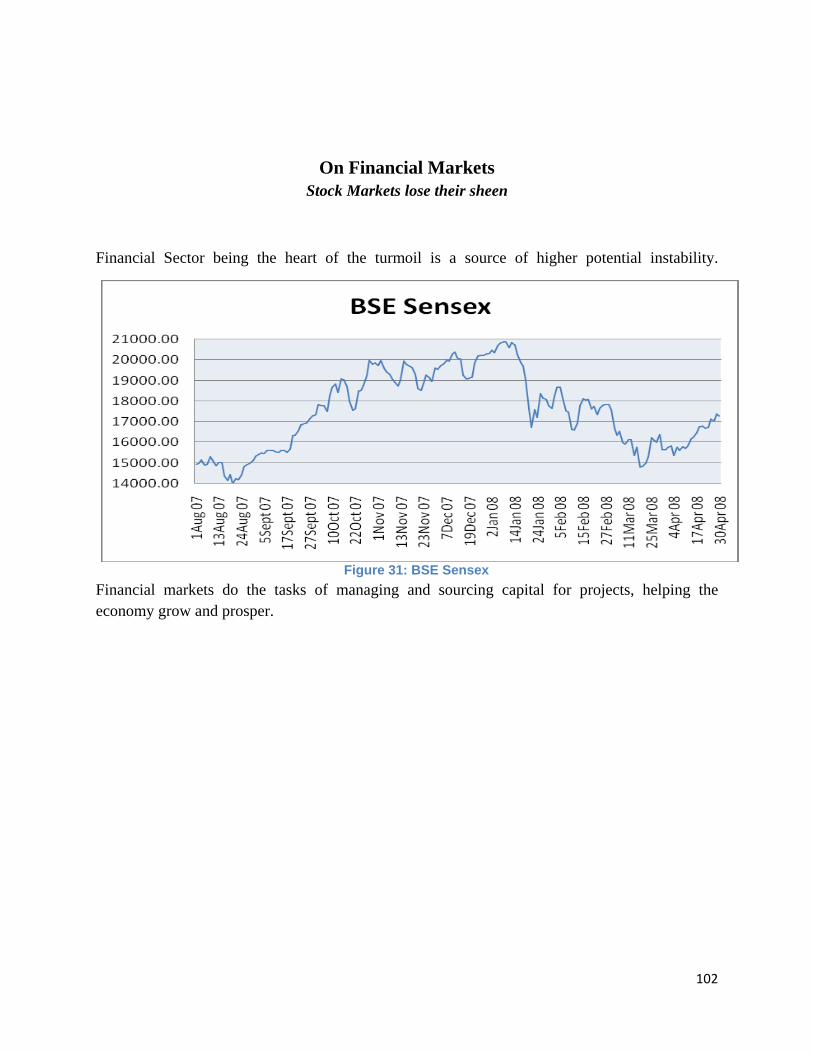

Figure 32: Nifty Index 100

Figure 33: Bank Nifty 101

Figure 34: CRR (Cash Reserve Ratio) 104

Figure 35: Call Money Borrowing 105

Figure 36: INR vs. USD 107

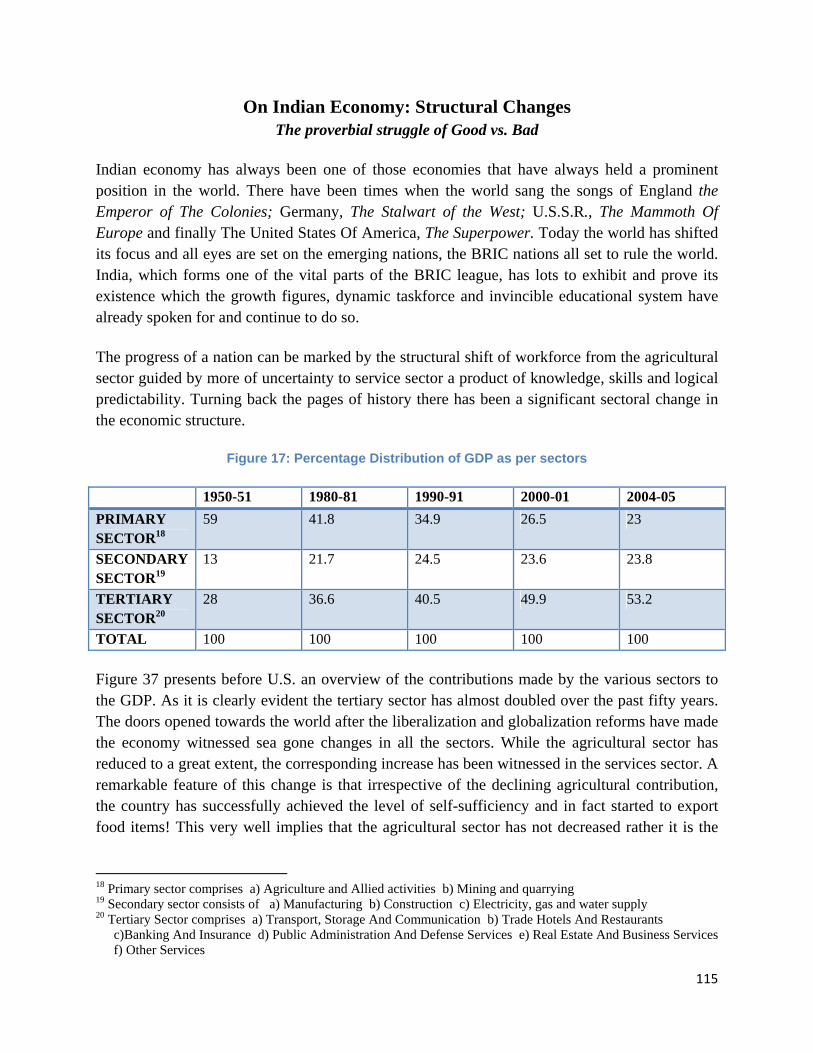

Figure 37: Percentage Distribution of GDP as per sectors 112

TTAABBLLEE OOFF BBOOXXEESS

Box 1: Mechanism of Leveraging 26

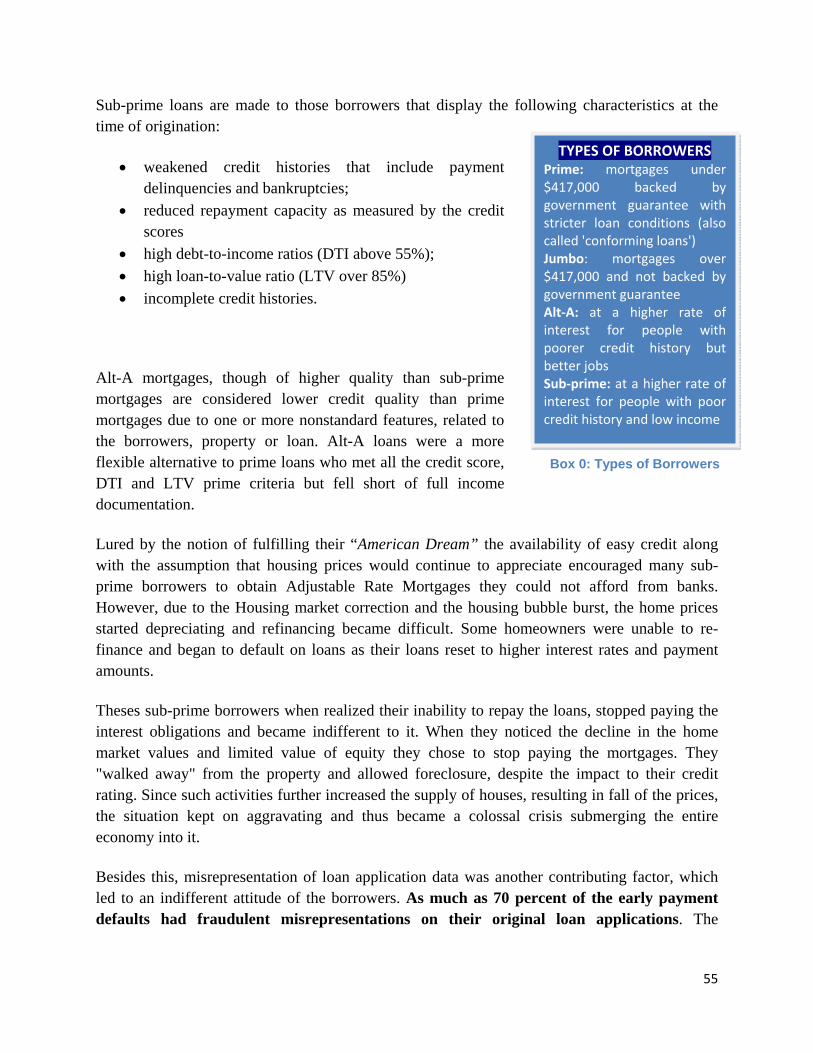

Box 2: Types of Borrowers 54

Box 3: Predatory Lending Practices 57

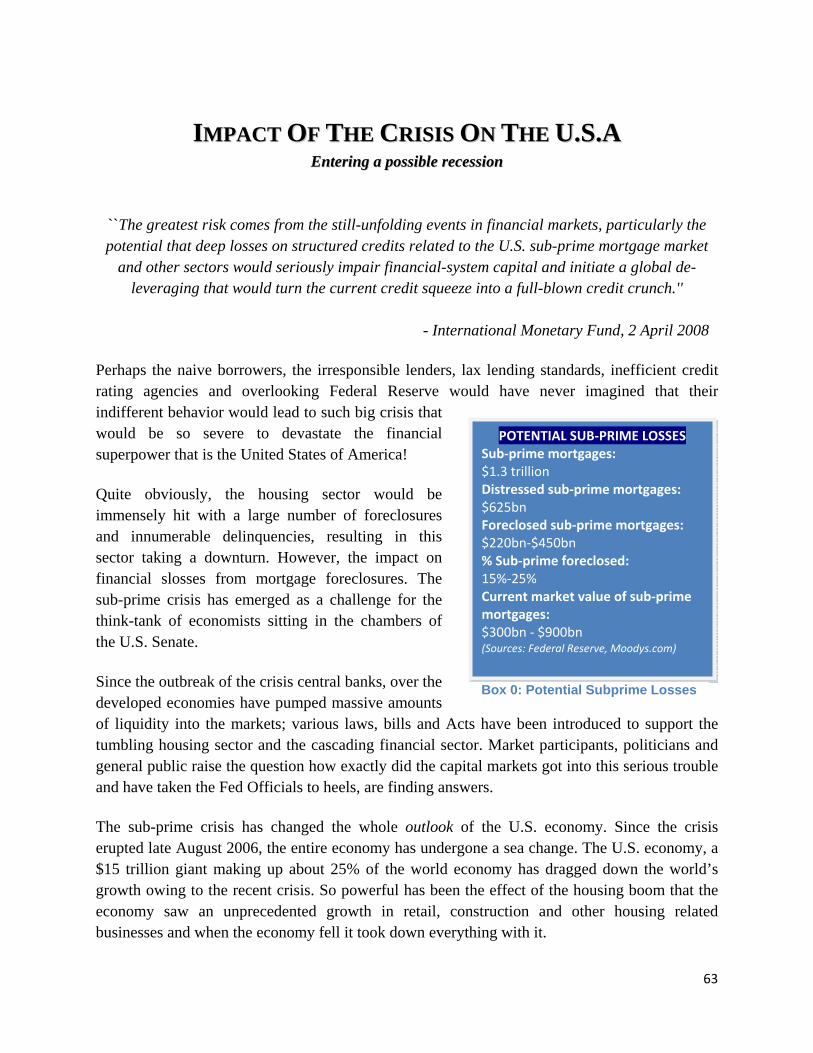

Box 4: Potential Subprime Losses 61

Box 5: Main Credit Losses so Far 62

Box 6: Projected Economic Losses 67

Box 7: Major Market Falls in January 2008 87

Box 8: House Price Developments In Central & Eastern European Countries 93

Box 9: Indian Companies with Foreign Losses 98

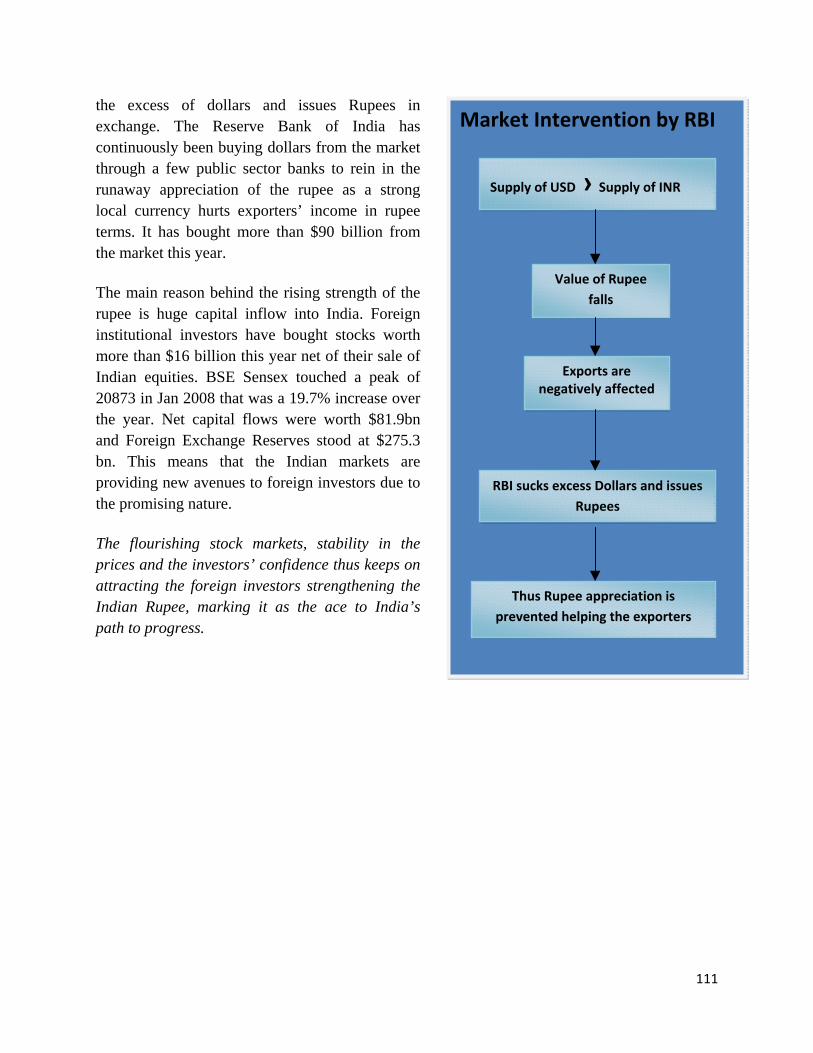

Box 10: Market Intervention by RBI 108

10

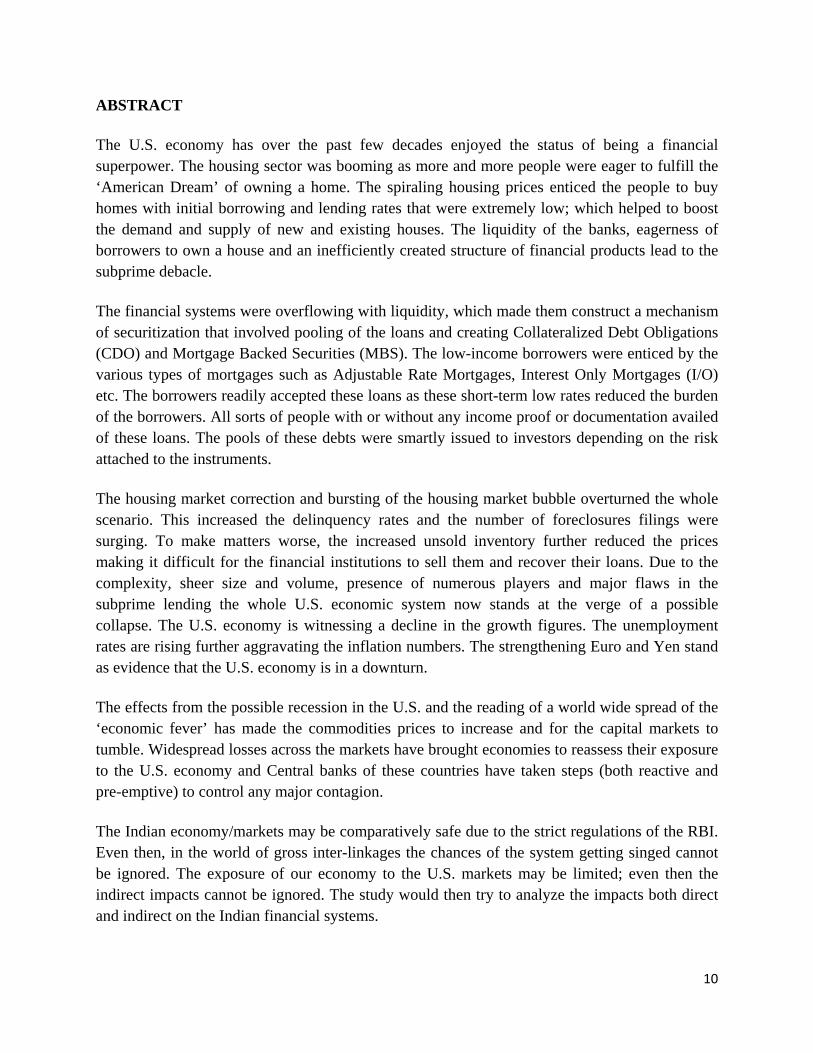

ABSTRACT

The U.S. economy has over the past few decades enjoyed the status of being a financial superpower. The housing sector was booming as more and more people were eager to fulfill the ‘American Dream’ of owning a home. The spiraling housing prices enticed the people to buy homes with initial borrowing and lending rates that were extremely low; which helped to boost the demand and supply of new and existing houses. The liquidity of the banks, eagerness of borrowers to own a house and an inefficiently created structure of financial products lead to the subprime debacle.

The financial systems were overflowing with liquidity, which made them construct a mechanism of securitization that involved pooling of the loans and creating Collateralized Debt Obligations (CDO) and Mortgage Backed Securities (MBS). The low-income borrowers were enticed by the various types of mortgages such as Adjustable Rate Mortgages, Interest Only Mortgages (I/O) etc. The borrowers readily accepted these loans as these short-term low rates reduced the burden of the borrowers. All sorts of people with or without any income proof or documentation availed of these loans. The pools of these debts were smartly issued to investors depending on the risk attached to the instruments.

The housing market correction and bursting of the housing market bubble overturned the whole scenario. This increased the delinquency rates and the number of foreclosures filings were surging. To make matters worse, the increased unsold inventory further reduced the prices making it difficult for the financial institutions to sell them and recover their loans. Due to the complexity, sheer size and volume, presence of numerous players and major flaws in the subprime lending the whole U.S. economic system now stands at the verge of a possible collapse. The U.S. economy is witnessing a decline in the growth figures. The unemployment rates are rising further aggravating the inflation numbers. The strengthening Euro and Yen stand as evidence that the U.S. economy is in a downturn.

The effects from the possible recession in the U.S. and the reading of a world wide spread of the ‘economic fever’ has made the commodities prices to increase and for the capital markets to tumble. Widespread losses across the markets have brought economies to reassess their exposure to the U.S. economy and Central banks of these countries have taken steps (both reactive and pre-emptive) to control any major contagion.

The Indian economy/markets may be comparatively safe due to the strict regulations of the RBI. Even then, in the world of gross inter-linkages the chances of the system getting singed cannot be ignored. The exposure of our economy to the U.S. markets may be limited; even then the indirect impacts cannot be ignored. The study would then try to analyze the impacts both direct and indirect on the Indian financial systems.

11

INTRODUCTION

The whole world being linked with the common ties of globalization has necessitated the study of the turbulence in the U.S. economy and its impacts on the world with special relevance to the Indian economy. The subprime crisis and its effects on the U.S. economy and the world economies have been studied in detail moving onto the Indian economy.

PURPOSE OF THE STUDY

The main objective of the study is to have:

• An understanding of the ongoing Sub-prime crisis • The impact on Financial Markets, Commodities Markets (Crude Oil), Money Market of

our country • Study its impact on U.S.A, developed economies and the Indian Economy. • Future implications on the World Economic system in general. • Study the possible impact it may have on India. • Expected changes to the Indian Economy post Subprime Crisis

The world economies are at present passing through one of the most difficult phases in recent times. The sub-prime crisis, which has its roots in the U.S., threatens to rage onto the other developed economies eventually to scathe the emerging market economies in wake. Sitting in India, we may appear, at present, seem to be unaffected by the world economic problems. Statements by heads of important agencies have time and again impressed that the Indian economy has a very little exposure to the subprime and that, aside from scratches, the economy, in general, would walk tall.

However, in spite of the Indian economic systems seemingly direct insulation from the impacts, the fact remains that in the world of integrated economic systems, the U.S. recession is bound to test the resilience of the domestic economy. Already the stock markets, which seem to have the maximum exposure, have entered into a highly unpredictable and volatile state. The domino effect on the other sectors would take some more time to incident.

12

SCOPE OF THE STUDY

The project involves studying the subprime crisis as a whole. The main topics under this project are - Housing markets in the U.S.A, Leveraged Security Market & the Process of Subprime Lending. A study of the chronology of events will also be made to ascertain its incidence and the way it turned into a huge crisis engulfing the global economies. The project will also involve studying the parties in the crisis such as borrowers, lenders, banks etc. and their role.

After having an insight of all this the project shall move on to the impact and implications on U.S., some leading world economies and finally India. This will include studying:

• The Commodities Market with special emphasis on the Crude oil market and how it effects inflation.

• The Stock Markets of the world • Overall effect of subprime crisis on the money markets and interest rates in India. • Changes in forex rate of INR and the U.S.D. • The Structural Changes of Indian economy posed by the subprime crisis will also

be done.

LIMITATIONS OF THE STUDY

Subprime crisis and the fallouts to the economy thereof is a very expansive area that has gripped the biggest economy of the world. No matter how deep one goes into it, the chances of understanding it to the core may be difficult. The study would also not include aspects that are topical to U.S.A and would include

only those that are relevant in the Indian context or, which may have a bearing on India. Due to the ‘lag effect’ all the resultants may not manifest itself at the time of the study, so

while a theoretical study may be made, a comparison of the actual results may leave a lot wanting.

13

METHODOLOGY

The methodology comprises an in-depth search of various news articles, journals, reports, relevant laws and other literary work on this topic.

The report involves an analysis of the latest movements in the U.S. and the Indian Financial Markets. A search on the internet and books is another aid to the successful completion. A systematic approach has been followed which involves concentrating on the lowest

level accentuating the role of various parties who were party to the entire debacle. The next level of the study involved studying the timeline of how it transformed into such a huge problem. The impact of U.S. economy, then the inter-related world economies is the next step under the study. Finally the subprime crisis spreading its wings to the Indian Economy will be studied.

14

IINNTTRROODDUUCCTTIIOONN

“What began as a fairly contained deterioration in portions of the U.S. sub-prime market has metastasized into severe dislocations in broader credit and funding markets that now pose risks

to the macroeconomic outlook in the United States and globally”

Global Financial Stability Report, IMF, April 2008.

The recent turmoil that has inflicted the world economies is the sub-prime crisis. Related to the housing prices and engulfing the entire banking system of the U.S. economy, this crisis has spread its wings to encompass the worldwide economies in its realm translating it into a major financial crisis. The impact of this crisis has been so severe that the entire banking system of the world’s largest economy may collapse, leaving little scope for recuperations out of this crisis. The fact that the housing crisis has led to the present imbroglio is obviously undeniable.

Introduction

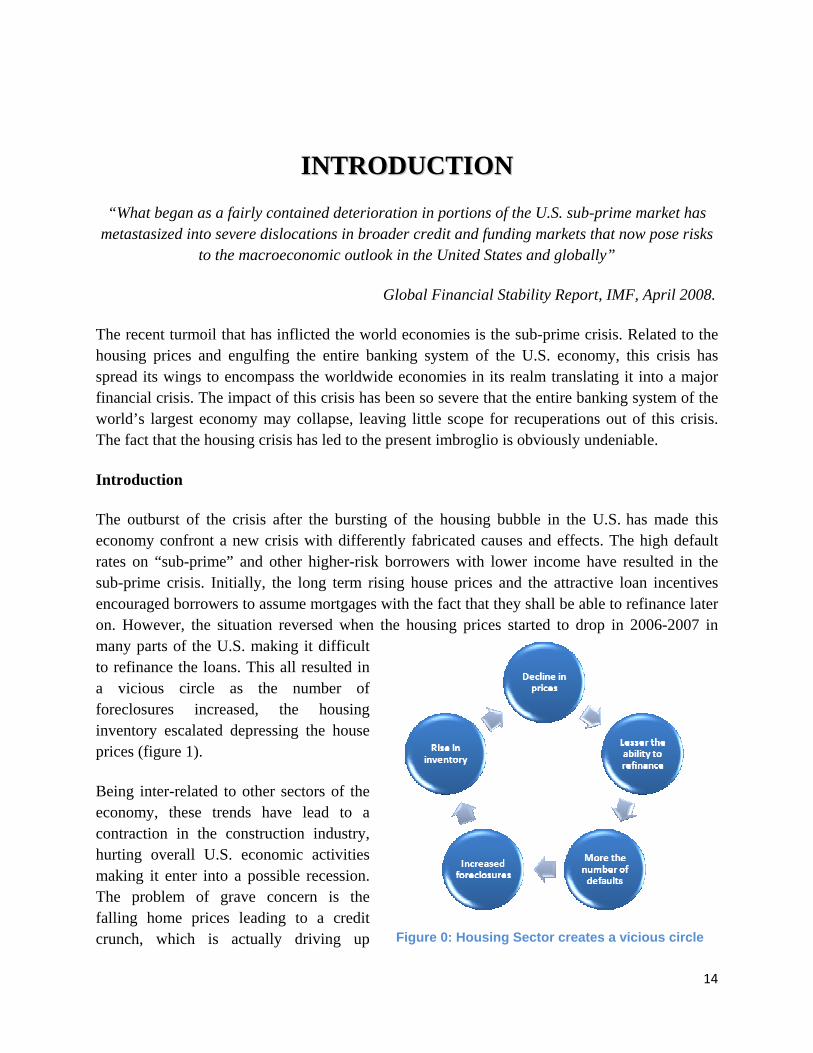

The outburst of the crisis after the bursting of the housing bubble in the U.S. has made this economy confront a new crisis with differently fabricated causes and effects. The high default rates on “sub-prime” and other higher-risk borrowers with lower income have resulted in the sub-prime crisis. Initially, the long term rising house prices and the attractive loan incentives encouraged borrowers to assume mortgages with the fact that they shall be able to refinance later on. However, the situation reversed when the housing prices started to drop in 2006-2007 in many parts of the U.S. making it difficult to refinance the loans. This all resulted in a vicious circle as the number of foreclosures increased, the housing inventory escalated depressing the house prices (figure 1).

Being inter-related to other sectors of the economy, these trends have lead to a contraction in the construction industry, hurting overall U.S. economic activities making it enter into a possible recession. The problem of grave concern is the falling home prices leading to a credit crunch, which is actually driving up Figure 0: Housing Sector creates a vicious circle

15

mortgage rates and making mortgages unavailable, leading to a further decline in home prices.

The whole carnage revolves around sub-prime lending by financial institutions. These institutions being accompanied by other parties such as Credit Rating Agencies, Mortgage Brokers and Underwriters etc. created a complex structure of lending and borrowing process, through the process of securitization. Being unified with common ties of globalization this American fiasco soon turned into a worldwide crisis affecting the major economies of the world.

This project studies the entire housing sector, which saw great heights and steep depths within a very short period of time. How the booming housing sector, which was a major asset of the weakest people of the society through innovative instruments and loans facilitated by various parties, saw its downfall is an interesting part, which is analyzed. Being one of the pillars of the American economy, how the movement in this pillar affected the whole economy inter-linked in various dimensions of employment, finances, and other macro-economic indicators (inflation, currency etc) has been thoroughly done. The world bonded by the Theory of Decoupling has seen new changes in growth brackets, trade movements and other global changes throughout this period.

Being an emerging economy, the Indian economy has also seen new pursuits in its economic framework and there still remain unknown pursuits and dimensions connected to the global economic architecture.

This project thus has various pursuits to explore about the American economy, world economies and Indian economy. There is a whole gamut of linkages between, inter-related and intra-related sectors, which have been studied in this project.

16

HHOOUUSSIINNGG MMAARRKKEETTSS IINN UU..SS..AA

MMaajjoorr CCoonnttrriibbuuttoorrss ttoo GGrroowwtthh

The real estate sector is amongst the largest sectors in the U.S.A. It has been a significant contributor to the U.S. economy, providing millions of jobs and had been generating hundreds of millions of dollars of economic output each year. It has traditionally been an important source of wealth building. The housing sector has been the main driver of economic growth of U.S. Therefore the weakening of this sector tends to have ominous implications for continuing expansion in the period ahead.

The housing sector accounts for about 6% of GDP, but has been a much more important component of growth, contributing 0.50% directly to GDP growth (translating to some U.S. $60 billion/year) and on the average adding 30,000 new jobs monthly in 2005. Some estimates suggested that wealth (home prices) and liquidity (home equity extraction) effects might have been contributing up to 1.5% to GDP growth in the last few years. Over the past four years ending 2006, consumer spending and residential construction together have been accounting for 90% of the total growth in GDP. And over two-fifths of all private sector jobs created since 2001 till the advent of crisis have been in housing-related sectors, such as construction, real estate and mortgage broking.

Homeownership – The American Dream

Housing (or an availability of dwelling) is one of the most important wants of any human. As the society and civilizations progressed, so did the desire to have a comfortable home. This desire cuts across all the income segments, race, and income levels. However, the common denominator remained – owning a house (see chart below). Two reasons why there was a housing boom was

- Increased level of income and - Easy availability of money.

Increased level of income Since 1967, the median household income in the United States had risen by 31%. The rise in household income has been largely the result of an increase in personal income among college graduates, a group that had doubled in size since the 1960s, and women entering the labor force. Today, 42% of all households have two income earners.

17

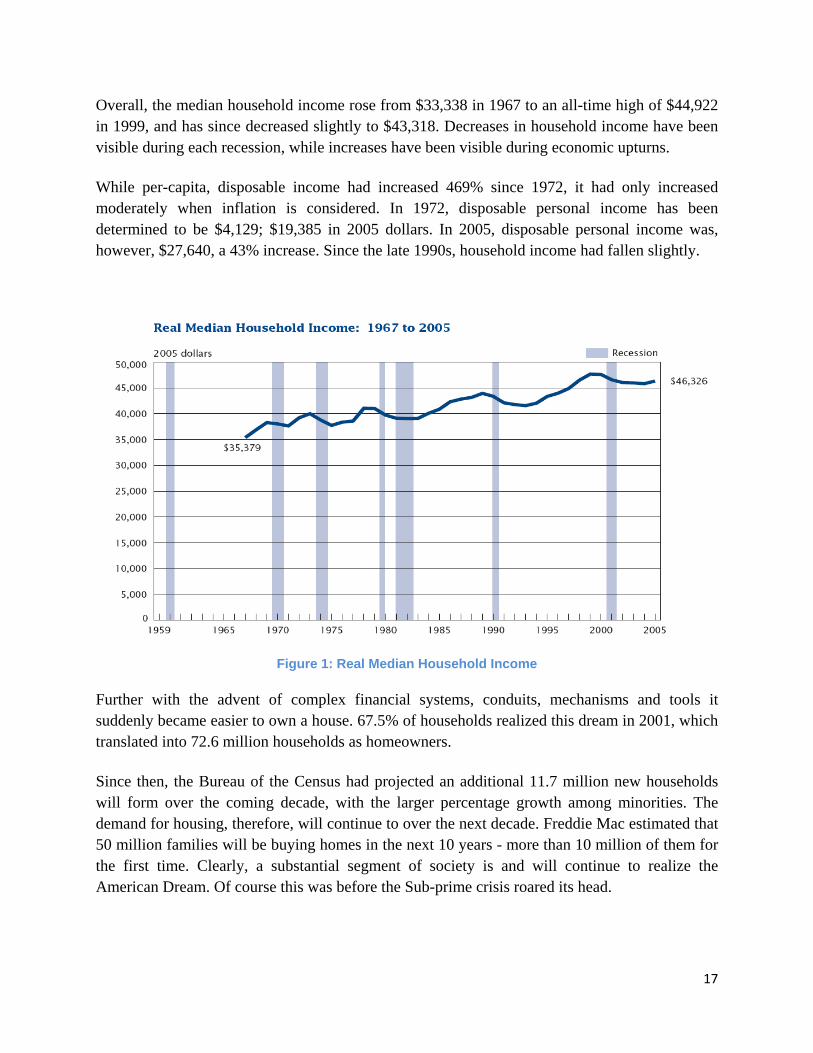

Overall, the median household income rose from $33,338 in 1967 to an all-time high of $44,922 in 1999, and has since decreased slightly to $43,318. Decreases in household income have been visible during each recession, while increases have been visible during economic upturns.

While per-capita, disposable income had increased 469% since 1972, it had only increased moderately when inflation is considered. In 1972, disposable personal income has been determined to be $4,129; $19,385 in 2005 dollars. In 2005, disposable personal income was, however, $27,640, a 43% increase. Since the late 1990s, household income had fallen slightly.

Figure 1: Real Median Household Income

Further with the advent of complex financial systems, conduits, mechanisms and tools it suddenly became easier to own a house. 67.5% of households realized this dream in 2001, which translated into 72.6 million households as homeowners.

Since then, the Bureau of the Census had projected an additional 11.7 million new households will form over the coming decade, with the larger percentage growth among minorities. The demand for housing, therefore, will continue to over the next decade. Freddie Mac estimated that 50 million families will be buying homes in the next 10 years - more than 10 million of them for the first time. Clearly, a substantial segment of society is and will continue to realize the American Dream. Of course this was before the Sub-prime crisis roared its head.

18

55,6

52

63,4

52

56,8

44

57,9

15

58,7

00

59,7

55

60,2

48

61,0

10

61,8

23

62,9

99

63,1

31

64,7

40

66,0

41

67,1

43

68,6

37

70,0

98

71,2

50

72,5

93

71,2

78

72,0

53

73,5

75

74,5

53

75,3

78

75,1

59

30,6

95 31,7

31

32,2

99

32,6

02

33,3

20

33,7

35

33,9

75

34,2

43

34,5

69

34,7

30

35,5

59

35,2

46

34,9

43

35,0

59

34,8

96

34,8

31

34,4

70

34,4

17

33,6

87

33,5

06

33,0

14

33,6

78

34,1

94

35,1

47

8,90

8 9,44

8

10,1

64

10,5

85

11,6

33

12,2

41

12,0

58

11,9

25

11,9

87

12,2

58

12,6

69

13,1

53

13,4

18

13,7

47

14,1

14

13,9

08

14,4

68

14,3

15

15,2

76

15,5

98

15,6

95

16,4

37

17,6

52

12,0

24

127,

958

126,

009

123,

926

122,

187

120,

835

119,

280

121,

478

119,

628

119,

043

117,

280

115,

620

114,

137

112,

655

110,

948

109,

716

108,

317

107,

277

106,

281

105,

731

103,

653

101,

102

99,3

07104,

631

95,2

55

0

20000

40000

60000

80000

100000

120000

140000

1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2006

Vacant TotalRenter TotalOwner Total

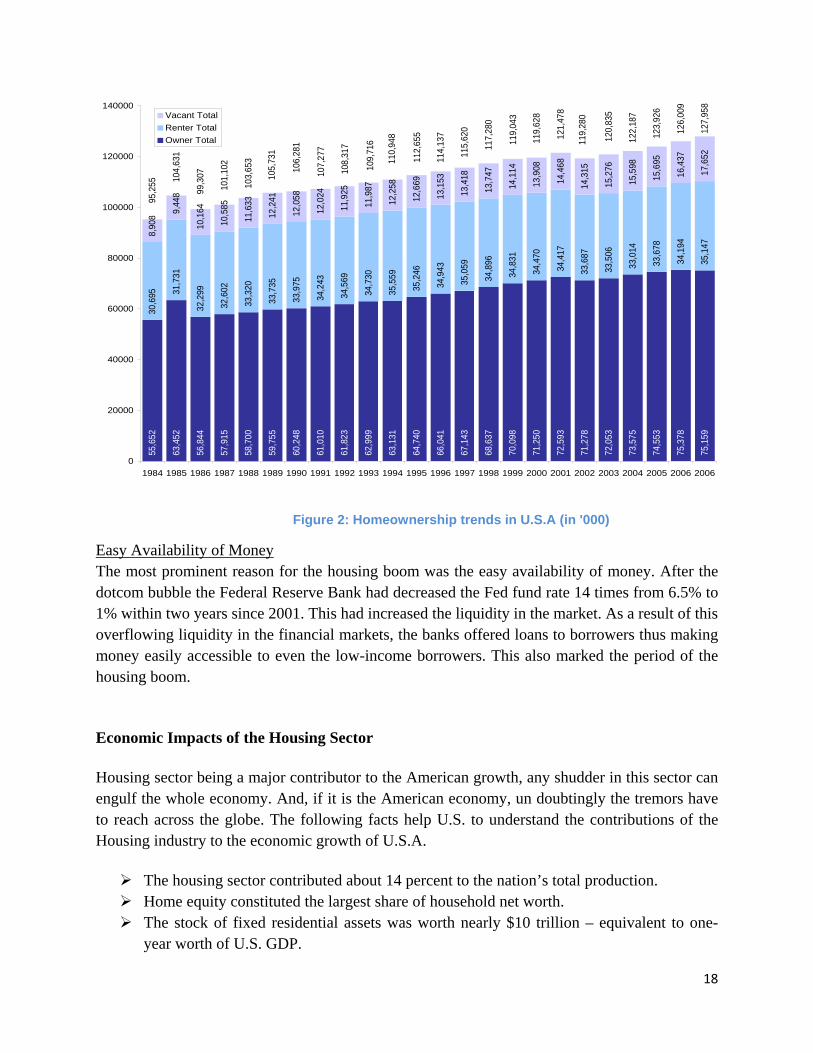

Figure 2: Homeownership trends in U.S.A (in '000)

Easy Availability of Money The most prominent reason for the housing boom was the easy availability of money. After the dotcom bubble the Federal Reserve Bank had decreased the Fed fund rate 14 times from 6.5% to 1% within two years since 2001. This had increased the liquidity in the market. As a result of this overflowing liquidity in the financial markets, the banks offered loans to borrowers thus making money easily accessible to even the low-income borrowers. This also marked the period of the housing boom.

Economic Impacts of the Housing Sector

Housing sector being a major contributor to the American growth, any shudder in this sector can engulf the whole economy. And, if it is the American economy, un doubtingly the tremors have to reach across the globe. The following facts help U.S. to understand the contributions of the Housing industry to the economic growth of U.S.A.

The housing sector contributed about 14 percent to the nation’s total production. Home equity constituted the largest share of household net worth. The stock of fixed residential assets was worth nearly $10 trillion – equivalent to one-

year worth of U.S. GDP.

19

About 1.5 million newly housing units were started each year. Housing starts have been one of the key factors in the macroeconomic business cycle. About 40 percent of monthly consumer expenditures were housing related. More than $1 trillion exchanged hands from the sale of existing and new homes. There were 288,273 establishments categorized as “real estate & rental & leasing with

over 1.7 million paid employees. 40% of the employment growth in the entire economic expansion was a result of soaring

home sales and prices. This included employment in home building directly as well as in ancillary factors such as supplies, real estate agents, appraisers, title searches and mortgage servicing.

Thus the housing sector has been one of the main sectors, which contribute both directly and indirectly to economic activity in the U.S.A.

The two line items in GDP directly associated with the housing sector are residential fixed investment1 consisting of value-put-in-place of new housing units, production of mobile homes, brokers’ commissions on the sale of existing residential properties, expenditures related to improving and additions to existing units, and net purchases of used structures from government agencies and housing service for personal consumption expenditures, purchased by residents in the United States, in the form of rent for tenants or as rental equivalence for homeowners. In 2000, residential fixed investment totaled $415 billion and housing service expenditure was $956 billion. The combined total of $1.37 trillion represented 14 percent of GDP.

Also, all economic activities produced a “Keynesian” multiplier effect. A home purchase usually resulted in further spending in other sectors of the economy (landscaping, appliances, and so on). The income earned by the landscapers was re-circulated into the economy as they spend, generating another round of income and purchases. The degree of multiplier depends on the degree of monetary policy accommodation and the “crowding out” effect. The multiplier was between 1.34 and 1.62 in the first year or two after an autonomous increase in spending. This meant that for each dollar increase in direct housing activity would increase the overall GDP by $1.34 to $1.62.

Many people’s livelihoods depended on real estate. The February 2001 report showed that 1.49 million workers were employed in the real estate industry. The Real Estate and Rental and Leasing sector, which comprises establishments primarily engaged in renting, leasing, selling, and buying real estate for others, and appraising real estate, totaled 288,273 establishments with 1.7 million paid employees. The annual payroll amounted to $41.6 billion.

Housing Sector Having Macro-economic Implication 1 Consists of purchases of private residential structures and residential equipment that is owned by landlords and rented to tenants. From www.bea.gov

20

In addition to its direct contribution to GDP, the housing sector has been playing an important role in the overall direction of the nation’s economy over the course of macroeconomic business cycles. Conversely, housing starts have made just as dramatic a change, coming out of a recession. In fact, housing starts lead the rest of the economy preceding changes in GDP. In other words, disruptions to the housing sector (arising from policy changes) are likely to be followed by a significant macroeconomic slowdown, while a stimulus to housing can lead the rest of the economy out of a slowdown.

During an economic slowdown, the Federal Reserve has been lowering the interest rates, other things equal. Consequently, the fall in interest rates during an economic slowdown has been acting as a strong buffer often providing a stimulus to the interest-sensitive housing sector. A drop in mortgage rates means lower monthly mortgage payments. This, in turn, means a lower qualifying income necessary to purchase a home. Conservatively, a one percentage drop in mortgage rates has translated into roughly 3 million additional households who would have the necessary income to qualify for a mortgage for purchasing a median priced home. Furthermore, many homeowners have refinanced their mortgages with the falling interest rates, leaving additional spending money to counter economic downturns. The economic slowdown from the mid-2000 to 2001 is a prime example of how this scenario is being played out. Housing starts and home sales began declining in spring of 2000 as the Fed has raised interest rates to cool the exceptionally fast growing economy. However, the economy has cooled much more drastically than desired and the Fed began reversing the interest rate policy by cutting the rates in early 2001. The subsequent falling interest rates have kept the housing starts and home sales to rebound to healthy levels even as the overall economy began sinking further. The economy would have undoubtedly tipped into a recession in early 2001 without the support of the housing sector during this period.

Impact on Communities

Construction of new homes provided jobs and higher tax revenues for local, state, and federal governments. Construction of each new single-family home required 1,591 worker-hours or the equivalent of 0.869 year of full-time labor. Each multifamily unit required 0.402 year of full-time labor. Projecting these estimates and accounting for productivity and price changes over the years, it is was estimated that the construction of 1,000 single-family homes generated 2,448 full-time jobs in construction and construction-related industries, $79.4 million in wages, and $42.5 million in combined federal, state and local revenues and fees. The construction of 1,000 multifamily units is estimated to have generated 1,030 full-time jobs in construction and construction-related industries, $33.5 million in wages; and $17.8 million in combined federal, state and local tax revenues and fees. Furthermore roughly 30 percent of the new home occupant’s income was spent on items produced by local businesses, such as hospitals, daycare centers, dry cleaners, and auto repair shops.

21

Almost 70 percent of all tax revenues raised by local governments in the United States came from property taxes. Homeowners contributed about 43 percent of property taxes, while commercial property accounted for 57 percent of real property tax revenues. Construction of new homes expanded the tax base and so increased the property tax revenues. using the average sales price of new homes in 2000, the local tax revenue base will increase by $185 billion.

Aside from tax revenue to local communities, home production and subsequent homeownership provided additional intangible values. Homeowners did not move as frequently as renters, providing a source of neighborhood stability. Neighborhood stability in turn conferred benefits of higher social and community involvement such as crime prevention programs. Homeowners had a stake in their neighborhoods and communities, and so were likely to behave in ways that provided benefit to everyone in the community. Owners maintain their properties in better condition than do renters of comparable housing. Such behavioral differences had been observed regardless of the age or income of homeowners. All of these social benefits to homeownership can impact property values.

Impact on Individuals

Homeownership also provided individuals with a way to accumulate wealth for the future while benefiting from the provision of shelter. A tabulation of household wealth from the Federal Reserve’s Survey of Consumer Finances (1998) shows that home equity (the value of the home net of mortgages) was the largest component of total wealth. Equity in primary residences accounted for 28% of the total family asset. Furthermore, the survey shows that 12.8% of families had some form of residential real estate in addition to primary residence (second homes, time shares, and other type of residential property), an increase from 11.8% in 1995. The value of the asset in other residential property accounted for additional 5% of the total household asset. Retirement accounts were the largest financial assets outside of primary residence, with 19.8% of the total. Only for the very wealthy (income over $100,000 per year) did the home equity portion of wealth fall below 50% of the total household wealth.

A separate survey from the Census Bureau also shows the dominant importance of home equity in determining household net worth. The Survey of Income and Program Participation periodically collects detailed wealth and asset data as a supplement to its core questions about labor force participation, income, demographic characteristics, and program participation. In 1995, median household net worth was $40,200; Median home equity for home-owning households was $50,000. Home equity constituted the largest share of household net worth, accounting for 44 percent of total net worth.

A privately owned home, therefore, was an important vehicle for wealth accumulation for a large segment of society. In addition, home investment played an important role in portfolio diversification. Home prices in the U.S., on average, have risen steadily, and have much lower

22

volatility than stock or bond prices. The historically standard deviation for stocks and bonds had been 20% and 9%, respectively. For housing, the standard deviation was about 4%. Furthermore, the correlation between home prices with stock or bond prices was very low. Homeowners were also benefited from the easy availability of home equity loans. Whether as a readily available source of funds, or just the security of a credit source, certainly added value to homeownership.

Housing Contribution to Society

Although the level and benefits of community involvement are hard to measure, several researchers have found that homeowners tend to be more involved in their communities and local governments then renters. For instance, owners participated in a greater number of non-professional organizations and had higher voter participation rates. In addition to higher civic participation, owners also tend to remain in their homes longer, adding stability and familiarity to the neighborhood, and also tend to spend more time and money maintaining their residence.

Home equity is one of the largest sources of collateral for bank loans to start new businesses. Over 740,000 businesses in 1992 reported a mortgage or home equity loan as a source of start-up capital for their business. It had been estimated in the UK that a 10 percent rise in the aggregate value of home equity increases the number of new business registration by 5 percent.

Furthermore, people want to be homeowners. Fifty eight percent of the renters responded that owning a home is either the top or very important priority according to 2000 Fannie Mae’s National Housing Survey. Freedom to alter their homes or engaging in home maintenance and improving may provide intrinsic joys.

Furthermore, others have noted that the home buying process and homeownership improve self-efficacy or a person’s sense of control over life events. And from extensive psychological studies self-efficacy is associated with better health status.

Whether it be America’s dream or an economic indicator of growth or a tool for changing the course of Macro-economic policies, the American Housing Market was such an important sector that any vibrations in the housing led banking mechanism could lead to a shake up in the entire world economies. The highly leveraged market and the whole dream of owning homes turned into a huge debacle. Economists call it bursting of the housing “bubble.” In the following pages we have tried to present the build-up of this bubble, the dynamism of the leveraged security markets, the role of parties in this crisis and the likely impact on the U.S. and other economies of the world.

23

LLEEVVEERRAAGGEEDD SSEECCUURRIITTYY MMAARRKKEETTSS TThhee DDoouubbllee EEddggeedd SSwwoorrdd

“…but in the modern fixed-income markets - where leverage is king and cheap credit is only the

current jester - a move of that magnitude can do a lot of damage.”

-Ryan Barnes, The Fuel That Fed The Sub-prime Meltdown.

Leveraging

The leveraging procedure, which intended to multiply the investments, opened new horizons for banks to offer the investors with innovatively designed debt instruments i.e. mortgage-backed securities (MBS), and collateralized debt obligations (CDO).

Leveraging is borrowing to invest. Financial leverage takes the form of a loan or other borrowings (debt), the proceeds of which are reinvested with the intent to earn a greater rate of return than the cost of borrowing. The most familiar use of leverage is using a mortgage to buy a home. In return for a down payment one receives funds to purchase an asset that would otherwise be too expensive. The homeowners either try to pay out the money from the rent that would be saved or from the income streams (the rent earned) that their vocations generate.

Leveraging helps both the investor and the firm to invest or operate. While leverage can play a positive role in the financial system, problems can arise when financial institutions go too far in extending credit to their customers and counter parties. If an investor uses leverage to make an investment and the investment moves against the investor, his or her loss is much greater than it would've been if the investment had not been leveraged - leverage magnifies both gains and losses. In the business world, a company can use leverage to try to generate shareholder wealth, but if it fails to do so, the interest expense and credit risk of default destroys shareholder value.

The build-up of the sub-prime crisis is based on the mechanism of leveraging. The layer upon layer of leverage that propelled the expansion is now operating in reverse as the leverage is being unwound.

Housing Sector: The Initial Fuel

Housing sector has been one of the prominent drivers of the U.S. economy. Not only has it made contributions to the employment, production and GDP, it has also been a major stimulus for the overall economic growth of this huge economy leading the global world. This sector has

24

important linkages to every macroeconomic aggregate like GNP, savings, interest and inflation rate and also highlights its importance in public policy decisions. The American Financial Institutions being over-flooded with liquidity magnified the housing sector as a lucrative area. The leveraging mechanism with its off springs i.e. Mortgage-Backed Securities (MBS) and Collateralized Debt Obligations (CDO) generated great opportunities for even those who could not afford to pay the cash flow mandated as among the key requirements for taking loans.

These sophisticated instruments, lackadaisical approach to adherence to prudent lending policy and the surplus of funds all contributed to the housing sector becoming the most booming sectors. As it grew, it took with itself almost the entire economy. Then an asset bubble began to form, frenzy fed on frenzy and the prices started to soar beyond what can safely be said to be the fundamentally correct prices. However, perhaps the key reason why the sub-prime crisis entrenched itself deep into the very sinews of the financial system of the U.S. was the creation of exotic leveraged instruments. That way banks now started lending more than the actual base money and that too to entities that had a very high risk-premium attached to it.

Securitization: Prime Mover of the Crisis

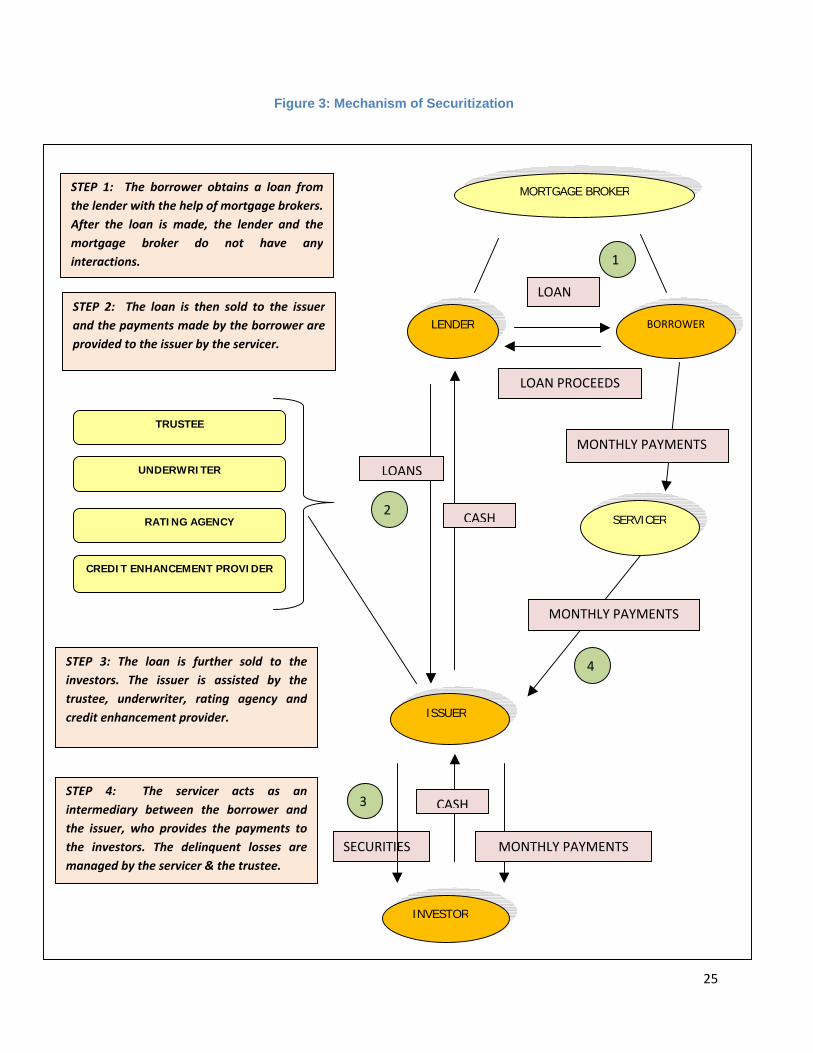

Securitization, an innovative form of financial engineering introduced two new instruments i.e. Mortgage Backed Securities and Collateralized Debt Obligations. Securitization is a structured finance process in which assets; receivables or financial instruments are acquired, classified into pools, and offered as collateral for third-party investment. Due to securitization, investor need for mortgage-backed securities (MBS), and collateralized debt obligations (CDO) as a profitable venture and the tendency of rating agencies to assign investment-grade ratings to these loans even though having a high risk of default could be originated, packaged and the risk readily transferred to others. The process of securitization has been explained with help of figure 4.

Mortgage Backed Securities (MBS) and Collateralized Debt Obligations (CDO’s) the two instruments of securitization played an important role in aggravating the whole sub-prime saga.

A mortgage-backed security (MBS) is an asset-backed security whose cash flows are backed by the principal and interest payments of a set of mortgage loans mainly on residential property. Collateralized debt obligations (CDO’s) are also type of asset-backed security and structured credit product but they are constructed from a portfolio of fixed-income assets. These assets are divided into different tranches: senior tranches (rated AAA), mezzanine tranches (AA to BB), and equity tranches (unrated). Here junior tranches offer higher coupons (interest rates) to compensate for the added default risk while senior tranches offer the lowest coupon rate offering highest safety level.

25

STEP 1: The borrower obtains a loan fromthe lender with the help of mortgage brokers.After the loan is made, the lender and themortgage broker do not have anyinteractions.

STEP 2: The loan is then sold to the issuerand the payments made by the borrower areprovided to the issuer by the servicer.

STEP 3: The loan is further sold to theinvestors. The issuer is assisted by thetrustee, underwriter, rating agency andcredit enhancement provider.

STEP 4: The servicer acts as anintermediary between the borrower andthe issuer, who provides the payments tothe investors. The delinquent losses aremanaged by the servicer & the trustee.

MORTGAGE BROKER

LENDER BORROWER

SERVICER

ISSUER

INVESTOR

TRUSTEE

UNDERWRITER

RATING AGENCY

CREDIT ENHANCEMENT PROVIDER

LOAN PROCEEDS

LOAN

MONTHLY PAYMENTS

MONTHLY PAYMENTS

LOANS

CASH

MONTHLY PAYMENTS

CASH

SECURITIES

1

2

3

4

Figure 3: Mechanism of Securitization

26

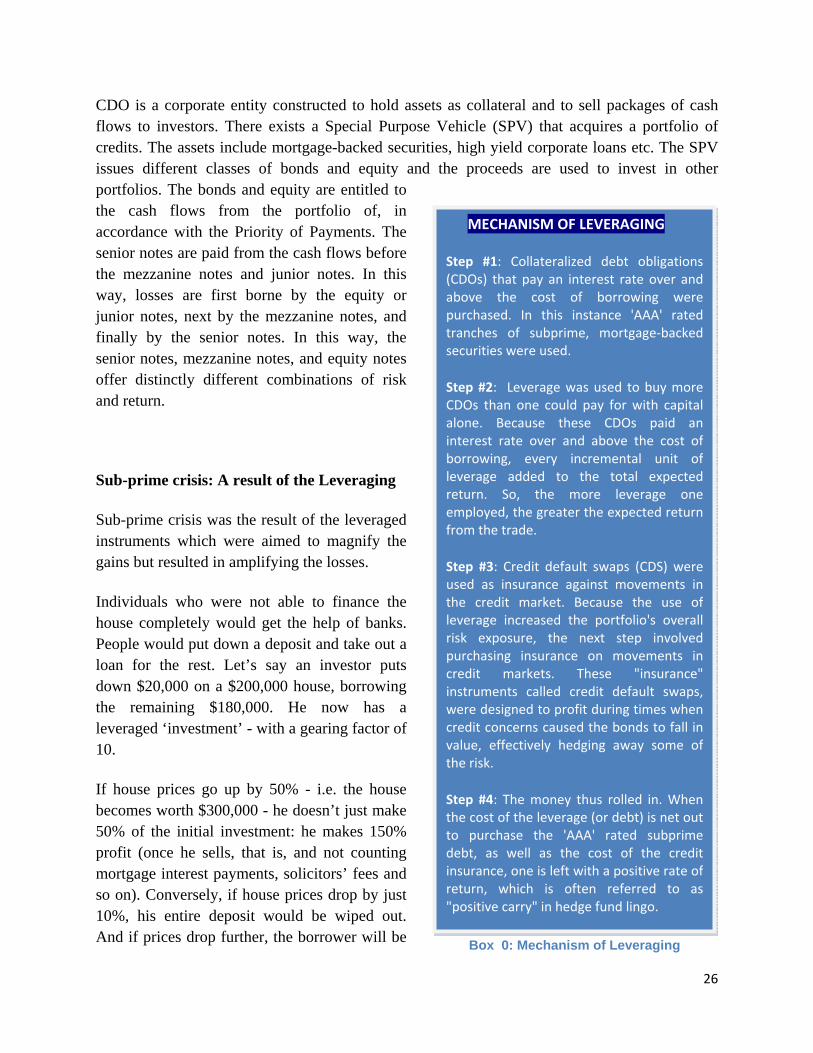

CDO is a corporate entity constructed to hold assets as collateral and to sell packages of cash flows to investors. There exists a Special Purpose Vehicle (SPV) that acquires a portfolio of credits. The assets include mortgage-backed securities, high yield corporate loans etc. The SPV issues different classes of bonds and equity and the proceeds are used to invest in other portfolios. The bonds and equity are entitled to the cash flows from the portfolio of, in accordance with the Priority of Payments. The senior notes are paid from the cash flows before the mezzanine notes and junior notes. In this way, losses are first borne by the equity or junior notes, next by the mezzanine notes, and finally by the senior notes. In this way, the senior notes, mezzanine notes, and equity notes offer distinctly different combinations of risk and return.

Sub-prime crisis: A result of the Leveraging

Sub-prime crisis was the result of the leveraged instruments which were aimed to magnify the gains but resulted in amplifying the losses.

Individuals who were not able to finance the house completely would get the help of banks. People would put down a deposit and take out a loan for the rest. Let’s say an investor puts down $20,000 on a $200,000 house, borrowing the remaining $180,000. He now has a leveraged ‘investment’ - with a gearing factor of 10.

If house prices go up by 50% - i.e. the house becomes worth $300,000 - he doesn’t just make 50% of the initial investment: he makes 150% profit (once he sells, that is, and not counting mortgage interest payments, solicitors’ fees and so on). Conversely, if house prices drop by just 10%, his entire deposit would be wiped out. And if prices drop further, the borrower will be

MECHANISM OF LEVERAGING

Step #1: Collateralized debt obligations(CDOs) that pay an interest rate over andabove the cost of borrowing werepurchased. In this instance 'AAA' ratedtranches of subprime, mortgage‐backedsecurities were used.

Step #2: Leverage was used to buy moreCDOs than one could pay for with capitalalone. Because these CDOs paid aninterest rate over and above the cost ofborrowing, every incremental unit ofleverage added to the total expectedreturn. So, the more leverage oneemployed, the greater the expected returnfrom the trade.

Step #3: Credit default swaps (CDS) wereused as insurance against movements inthe credit market. Because the use ofleverage increased the portfolio's overallrisk exposure, the next step involvedpurchasing insurance on movements incredit markets. These "insurance"instruments called credit default swaps,were designed to profit during times whencredit concerns caused the bonds to fall invalue, effectively hedging away some ofthe risk.

Step #4: The money thus rolled in. Whenthe cost of the leverage (or debt) is net outto purchase the 'AAA' rated subprimedebt, as well as the cost of the creditinsurance, one is left with a positive rate ofreturn, which is often referred to as"positive carry" in hedge fund lingo.

Box 0: Mechanism of Leveraging

27

in negative equity, owing the bank more than the current value of their house.

Enticed by the high returns on the ever-appreciating value of housing many investment banks, hedge funds and other institutional investors have done so, making phenomenally good returns over the five years starting year 2000.

Then the worst that was feared occurred- these leveraged investments started to go awry. Instead of profits, many investors have been hit by significant losses.

In the above example where the individual had put down $20,000 and took a debt of $180,000, as long as he sells before the value of the asset becomes less than the value of the debt, there isn’t any problem. Till the time it is secured on an asset that’s worth at least $180,000 the actual risk is just $20,000. But what if the investor can’t set a stop-loss (as is usually the case- since the house is not just for investment purpose but is actually an asset purchased to reside). Suddenly there’s no market for what his trying to sell or if everyone is so scared that nobody wants to put a price on what his selling, for fear that it’s too low and will in turn cause them to lose vast amounts of money too, because they hold similar investments.

Not long ago frenzy fed on frenzy and buoyed the prices up and now frenzy feeds on frenzy and pulling the prices down rather dramatically.

Now here stands the trouble of the leveraged market. Because the leveraging factor was much higher than what the system could withstand, and because the sub-prime ‘network’ was ingrained in almost the entire financial systems of the U.S., when the debacle happened, it simply collapsed the whole system.

The leveraging that helped the sector grow and propel the economy to boom is now dragging the same down. In the previous chapter we had covered the importance of the Housing sector. The effect of this importance can be gauged by a simple fact – Housing sector bust is dragging the entire U.S. economy to recession. And no matter what levels of fire-fighting that the monetary authorities undertake, the chances are that the U.S. economy has been dealt a major blow and it would take some serious and coordinated efforts to sail the boat through.

That is where the U.S. economy stands today. Efforts range from prudent (cutting interest rates) to near desperate (lending money to commercial banks taking the tainted mortgage-backed securities as collateral) steps. The hope is that by accepting these investments at face value central banks will release the credit blockage and get the U.S. economy moving again.

Due to the high amount of liquidity, which was somehow to be put into use, leverage was needed to boost returns over the last few years, owing to a lack of distressed debt. This led to 7 times

28

(and sometimes as much as 10 times) leverage on U.S. leveraged buyouts. In Europe, debt multiples also were stretched, with leverage of 5.5 times in 2007, versus 4.7 times in 1998.

Thus leveraging which was intended to increase the returns and provide shelter to the people of U.S. plunged economy downwards and contributed to the chronicle of Sub-prime Crisis.

In the global economy, effects in one area of investment quickly spread to others. So when institutional investors started losing money on collateralized debt obligations (CDO’s) and residential mortgage-backed securities (RMBS’s) because of the U.S. sub-prime crisis, they quickly liquidized other investments in order to cover their losses.

For example, some of them shifted cash out of the carry trade (in which money borrowed in low-interest currencies such as the Yen is invested in higher interest currencies such as the Pound), causing the Yen to rapidly appreciate and leading to a whole slew of currency investors losing money on their leveraged positions. These currency investors in turn had to find the money to cover their losses, perhaps by selling gold, temporarily shifting the gold price downwards and causing a tranche of leveraged gold investors to face severe losses. And so it went on, and continues to go on.

The total amount of leveraged investment in the world is unknown, but it has been estimated to be many multiples of global GDP.

Thus leveraging was a double-edged sword, which was aimed at multiplying the profits, but if it acted reversely, the losses would magnify much more than the expected profits. Perhaps, that is what happened in the U.S. economy, where the reverse took place and brought the world at the verge of this crisis. The tool of leveraging mechanism i.e. the sub-prime lending provides U.S. an insight of how the construct of the sub-prime crisis took place.

29

SSUUBB PPRRIIMMEE LLEENNDDIINNGG TThhee FFllaawwss

The financial institutions overflowing with liquidity devised the securitization mechanism for which they classified the lending into three categories namely, The Prime category, the Alt-A category and Sub-prime category. The parameters of categorizing the credit seekers were:

1. Credit worthiness and documentation prudence 2. Ability to pay back the money 3. Ability to pay down payments 4. Whether it’s a first loan or an already mortgaged asset.

While the prime category of borrowers fulfilled all the parameters, the sub-prime borrowers stood at fulfilling none. Alt-A borrowers mainly were short of documentation, including proof of income. Yet these borrowers had clean histories they either had higher loan-to-value or debt-to-income ratios.

Sub-prime lending (also known as B-paper, near-prime, or second chance lending) is lending at a higher rate than the prime rate. A higher rate of interest is charged due to limited or tarnished credit history or inadequate documentation, higher loan-to-value and debt-to-income ratios. However, with the higher rates comes additional risk for lenders because there is a lack of documentation - including limited proof of the borrower's income poor credit history, and adverse financial situations usually associated with sub-prime applicants.

A high risk based pricing system is used in order to calculate the terms of loans, which are offered to borrowers with varying credit histories. The sub-prime borrowers charge high rates of interest, but still credit risk is more than interest rate risks due to the increased chances of defaults and less opportunities to refinance the loans.

Sub-prime lending was initially a helping hand to all those borrowers who aimed to fulfill their dream of owning a home. Sub-prime loans increased opportunities for homeownership and added 9 millions of households to the new status of homeowners in less than a decade and increased employment opportunities thereby increasing the growth rate.

30

However, providing loans to the low-income sections of the society was a benefit as well as fallout of the sub-prime loans. The availability of liquidity was the prominent factor that prompted the banks to provide loans at high rates, on the surety that even if the borrower fails to pay the loan amount, they may still have the option to sell the houses and recover the amount. The fact that the housing prices usually tend to appreciate, furthermore, made the bankers free from any apprehensions of recovering the losses. Also since sub-prime lending, a direct result of high liquidity, prompted banks to issue loans without any strict regulations which could help them to earn high amount of profits by the securitization mechanism as explained later.

Sub-prime borrowing was as such not flawed; rather it was the high quantum of sub-prime loans granted without proper regulations that appeared to be the major reason for the fallout. The positive picture of profit earnings hid the shortcomings of improper regulations, irresponsible lending and inefficient rating system by the credit rating agencies.

Sub-prime lending became highly controversial: Sub-prime lenders often engaged in predatory lending practices such as deliberately lending to borrowers who could never meet the terms of their loans, thus leading to default, seizure of collateral, and foreclosure. They often employed unscrupulous means by enticing, inducing, and/or assisting a borrower in taking a mortgage that carried high fees, a high interest rate etc.

Property Fraud by Lenders: With the increase in sub-prime lending there was a similar increase in the property frauds. By selling overpriced apartments to the unsuspecting buyers, the sellers took the money and disappeared. So now the entire deal was between the banks and he borrowers. In this way the sellers, earned huge amounts on the overpriced sold houses.

Second Mortgages: Irrespective of the bad credit histories, the sub-prime lending had made second mortgages easier on the existing mortgaged houses. The repayment of another loan burdened the borrowers, which ultimately had to borne by the lenders i.e. the banks, when the borrowers defaulted in making the payments.

Lax Lending Rules: Analysts say lax lending standards led some mortgage firms to grant home loans to tens of thousands of borrowers who did not have the means to meet their mortgage payments when interest rates increased.

Irresponsible Credit Rating Agencies: Credit rating agencies such as Standard and Poor's, Moody's and Fitch Ratings were urged by the panel to improve their influential reports and assumptions about a wide range of securities and corporations.

Major Banks meanwhile were encouraged to disclose more information about the securitization of complex credit instruments, such as mortgage, credit card and student loans, which they package or cut up and sell to other banks and investors.

31

Besides that the other reason why the Sub-prime mortgage crisis unfolded the way it did had also to do with the complex financial wizardry that was devised around the lending that had the effect of ‘over-lending’. That is the financial systems geared up by multiples in excess of what they could or rather should have. Due to the complexity, sheer size and volume, presence of numerous players and major flaws in the sub-prime lending have all caused the system to collapse. New forces have played important roles in Sub-prime crisis that had in the post been absent.

1. Complex investments: Financial firms wield ever more sophisticated financial tools. CDOs and MBAs enabled complex and opaque investments.

2. New institutions: Players like hedge funds and buyout firms – also called Private Equity, represent a large and rising sharing of overall investment money. Hedge funds also have taken exposure to the subprime investments. These players are significantly less regulated than the listed companies-these are less transparent and generally have a free will to do pretty much what they want. Besides that Rating agency and Credit enhancers played a very important role in certifying the quality of the subprime credit. These too are outside the purview of the agencies.

3. Leverage: the growing use of Debt or leverage by financial players magnifies the first two forces. An era of easy money has enabled more risk taking built on borrowed funds. That can accentuate in both the ups and downs of a cycle, raising the chances of panic selling during down turns and frenzied buying in upturns.

4. Globalization: Today all the nations in the world are linked through easy movement of funds. In the less regulated markets money moves both in and out freely. In the medium regulated markets like India, the movement is not easy but even then the movement is copious enough to affect massive hemorrhage. This has very telling effect. In this case for example large banks across the world had exposure to the subprime conundrum. And when the damage occurred the ripple effect wiped out a lot of financial players across the globe.

Given the gearing up and the various reasons as explained above, the subprime imbroglio was a time-bomb which was waiting to implode. And as it did it took down with it the most powerful economy in this globe.

32

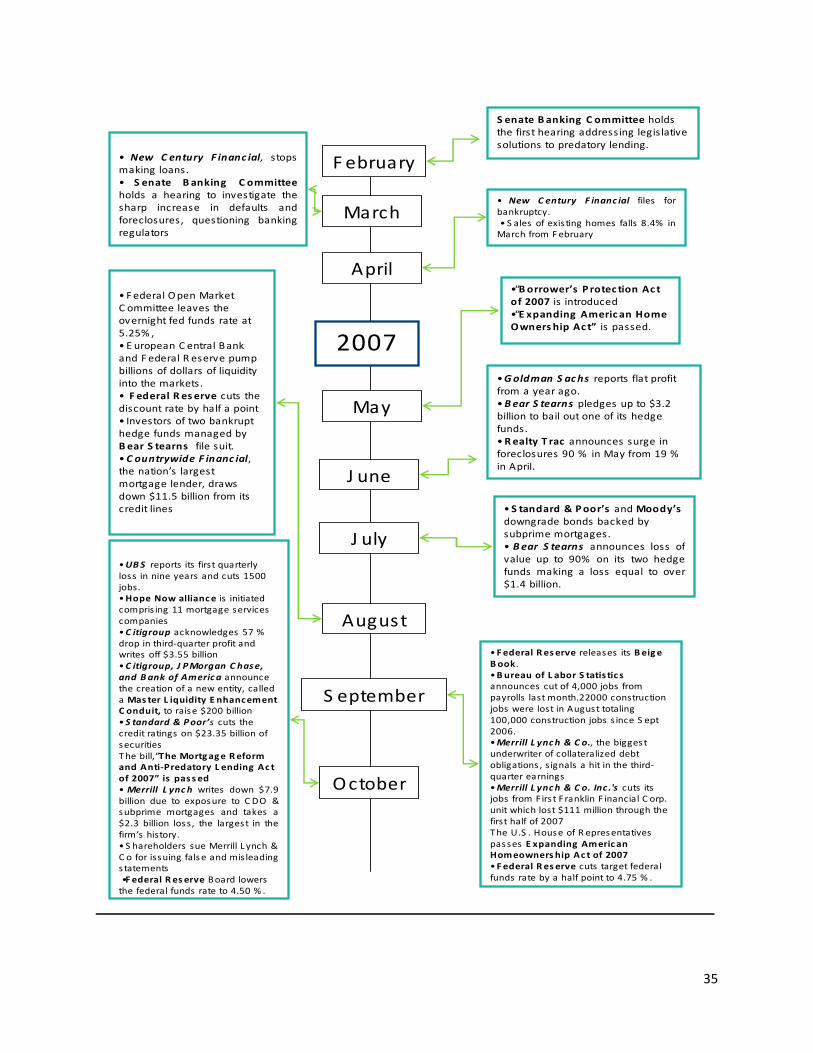

TTHHEE CCRRIISSIISS AANNDD CCHHRROONNOOLLOOGGYY OOFF EEVVEENNTTSS TTiimmeelliinnee ooff IImmpplloossiioonn

“What began as a tremor in the sub-prime mortgage market that affected a relative few, has sadly gained momentum, creating a broader credit crisis that continues to threaten the middle

class and overall economic growth.”

-Senator Jack Reed

The U.S. economy was at the peak of invincible growth and incessant development with every sector enjoying a boom since the past two decades. The unemployment rates were fairly low, inflation under control, stock markets scaling new heights, banking sectors overflowing with liquidity and growth figures rising steadily accounting for 26% of the worlds GDP.

The American economy flooded with enormous liquidity and the low income citizens striving to fulfill their imperative dream of shelter had an incomprehensible tryst with each other and resulted in the whole sub-prime saga.

As it has been said that invention is the mother of necessity the financial institutions devised an innovative mechanism of securitization with Mortgage Backed Securities and Collateral Bonds Obligations as the two offsprings. The low-income people who had tarnished credit histories or no documentation were issued loans without any such requirements to be fulfilled. The funds generated from these instruments were used to create new investment vehicles i.e. MBS’s and CDO’s that were issued to investors by the bankers at varying rates of interest depending on the ability of the borrowers to repay.

The whole mechanism was a laudable creation of the financial know-how and desperately fulfilled dreams. So the sub-prime lending mechanism was an efficient fabrication of converting attractive dreams to a moneymaking business with the creation of two ingeniously thought over instruments.

The boom in the housing sector, enticing interest rates and high profit margins kept on luring the financial institutions, that they shut their eyes to the pessimistic notion that if those borrowers

33

failed to pay their debt obligations or if the collateralized houses faced a surge in the prices, the aftermath could result in the collapse in the whole banking segment on the threshold of which lies a whole economy with all the sectors interlinked to each other presenting the cascading effect.

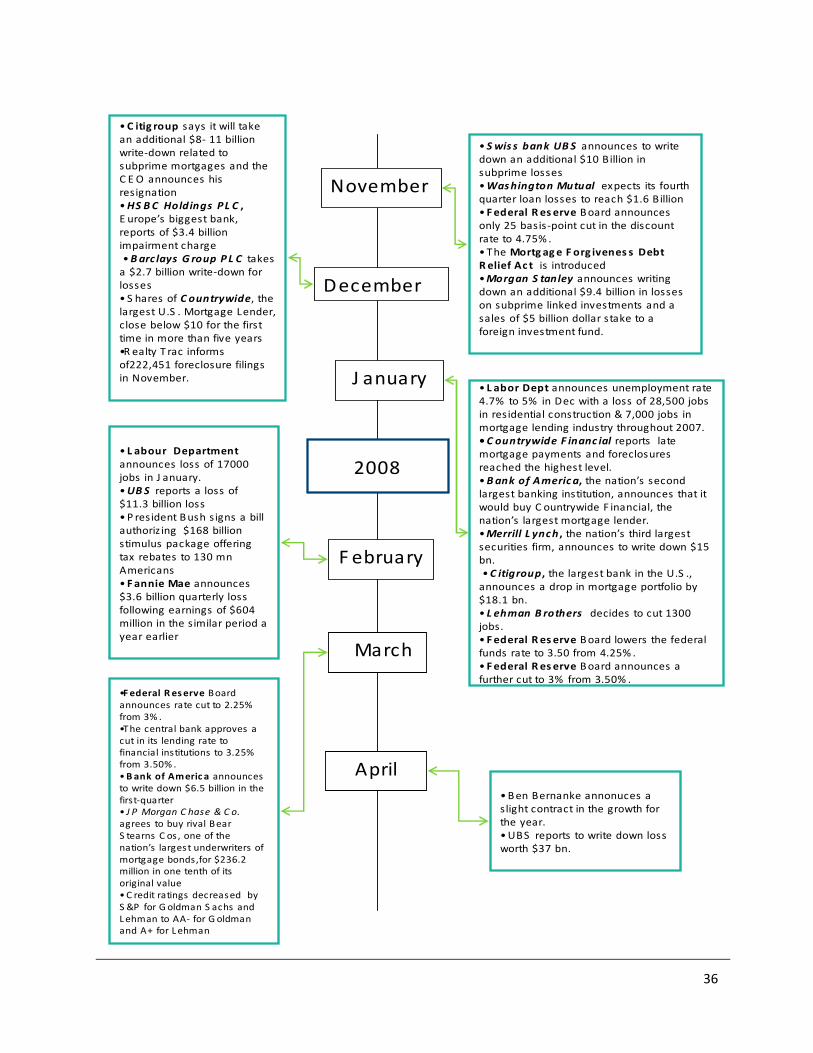

Housing markets have gone bust, interest rates have touched the pinnacles, stock markets across the world have collapsed, unemployment toll has increased, growth rates have plummeted, global inflation has been scaling to new heights, the fiscal deficit gaps are widening, corporate giants have been announcing billion dollar losses with colossal business houses being taken over at the lowest of their values. Figure 5 shows the timeline of the events.

34

Figure 4: Timeline of Implosion

35

2007

S enate Banking C ommittee holds the first hearing addressing legislative solutions to predatory lending.

S eptember

August

J uly

J une

May

April

March

F ebruary• New C entury F inanc ial, stops making loans.• S enate Banking C ommittee holds a hearing to investigate the sharp increase in defaults and foreclosures, questioning banking regulators

• S tandard & Poor’s and Moody’sdowngrade bonds backed by subprime mortgages.• Bear S tearns announces loss of value up to 90% on its two hedge funds making a loss equal to over $1.4 billion.

•“Borrower’s Protec tion Act of 2007 is introduced•“E xpanding Americ an Home Owners hip Act” is passed.

• New C entury F inanc ial files for bankruptcy.• S ales of existing homes falls 8.4% in March from F ebruary

• Federal Open Market C ommittee leaves the overnight fed funds rate at 5.25% ,• E uropean C entral Bank and F ederal R eserve pump billions of dollars of liquidity into the markets.• F ederal Res erve cuts the discount rate by half a point• Investors of two bankrupt hedge funds managed by Bear S tearns file suit.•C ountrywide F inanc ial, the nation’s largest mortgage lender, draws down $11.5 billion from its credit lines

October

•UBS reports its first quarterly loss in nine years and cuts 1500 jobs.•Hope Now alliance is initiated compris ing 11 mortgage services companies•C itigroup acknowledges 57 % drop in third‐quarter profit and writes off $3.55 billion•C itigroup, J PMorgan C hase, and Bank of Americ a announce the creation of a new entity, called a Mas ter L iquidity E nhancement C onduit, to raise $200 billion•S tandard & Poor’s cuts the credit ratings on $23.35 billion of securitiesThe bill,“The Mortgage Reform and Anti‐Predatory L ending Ac t of 2007” is pass ed• Merrill L ynch writes down $7.9 billion due to exposure to C DO & subprime mortgages and takes a $2.3 billion loss, the largest in the firm’s history.• S hareholders sue Merrill L ynch & C o for issuing false and mis leading s tatements•Federal Res erve Board lowers the federal funds rate to 4.50 % .

•Federal Res erve releases its Beige Book.•Bureau of L abor S tatis tic s announces cut of 4,000 jobs from payrolls last month.22000 construction jobs were lost in August totaling 100,000 construction jobs s ince S ept 2006.•Merrill L ynch & C o., the biggest underwriter of collateralized debt obligations , signals a hit in the third‐quarter earnings•Merrill L ynch & C o. Inc .'s cuts its jobs from F irst Franklin F inancial C orp. unit which lost $111 million through the first half of 2007The U.S . House of R epresentatives passes E xpanding American Homeowners hip Ac t of 2007•Federal Res erve cuts target federal funds rate by a half point to 4.75 % .

•Goldman S achs reports flat profit from a year ago.•Bear S tearns pledges up to $3.2 billion to bail out one of its hedge funds.•Realty T rac announces surge in foreclosures 90 % in May from 19 % in April.

36

November

•C itig roup says it will take an additional $8‐ 11 billion write‐down related to subprime mortgages and the C E O announces his resignation •HS BC Holdings PL C , E urope’s biggest bank, reports of $3.4 billion impairment charge •Barc lays G roup PL C takes a $2.7 billion write‐down for losses •S hares of C ountrywide, the largest U.S . Mortgage Lender, close below $10 for the first time in more than five years•R ealty T rac informs of222,451 foreclosure filings in November.

December

• Swis s bank UBS announces to write down an additional $10 Billion in subprime losses•Washington Mutual expects its fourth quarter loan losses to reach $1.6 Billion• Federal Res erve Board announces only 25 basis‐point cut in the discount rate to 4.75% . •The Mortg age F org ivenes s Debt Relief Act is introduced•Morgan S tanley announces writing down an additional $9.4 billion in losses on subprime linked investments and a sales of $5 billion dollar stake to a foreign investment fund.

J anuary• L abor Dept announces unemployment rate 4.7% to 5% in Dec with a loss of 28,500 jobs in residential construction & 7,000 jobs in mortgage lending industry throughout 2007.•C ountrywide F inanc ial reports late mortgage payments and foreclosures reached the highest level.•Bank of America, the nation’s second largest banking institution, announces that it would buy C ountrywide F inancial, the nation’s largest mortgage lender.•Merrill L ynch , the nation’s third largest securities firm, announces to write down $15 bn.•C itigroup, the largest bank in the U.S ., announces a drop in mortgage portfolio by $18.1 bn.• L ehman B rothers decides to cut 1300 jobs.• Federal Res erve Board lowers the federal funds rate to 3.50 from 4.25% . • Federal Res erve Board announces a further cut to 3% from 3.50% .

• L abour Department announces loss of 17000 jobs in J anuary.•UBS reports a loss of $11.3 billion loss •P resident Bush signs a bill authoriz ing $168 billion stimulus package offering tax rebates to 130 mnAmericans• Fannie Mae announces $3.6 billion quarterly loss following earnings of $604 million in the similar period a year earlier

F ebruary

•Federal Reserve Board announces rate cut to 2.25% from 3% . •The central bank approves a cut in its lending rate to financial institutions to 3.25% from 3.50% .•Bank of Americ a announces to write down $6.5 billion in the first‐quarter• J P Morgan C hase & C o. agrees to buy rival Bear S tearns C os , one of the nation’s largest underwriters of mortgage bonds,for $236.2 million in one tenth of its original value•C redit ratings decreased by S &P for Goldman S achs and Lehman to AA‐ for Goldman and A+ for Lehman

•Ben Bernanke annonuces a slight contract in the growth for the year.•UBS reports to write down loss worth $37 bn.

March

April

2008

37

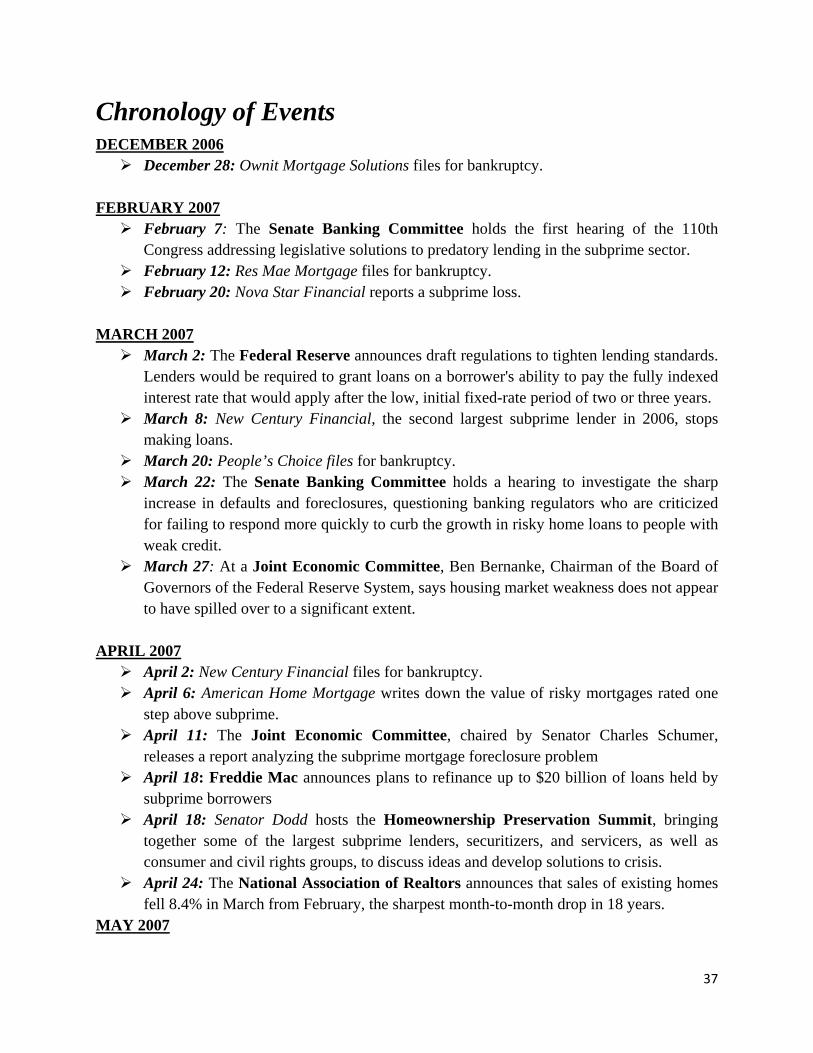

Chronology of Events

DECEMBER 2006 December 28: Ownit Mortgage Solutions files for bankruptcy.

FEBRUARY 2007

February 7: The Senate Banking Committee holds the first hearing of the 110th Congress addressing legislative solutions to predatory lending in the subprime sector. February 12: Res Mae Mortgage files for bankruptcy. February 20: Nova Star Financial reports a subprime loss.

MARCH 2007

March 2: The Federal Reserve announces draft regulations to tighten lending standards. Lenders would be required to grant loans on a borrower's ability to pay the fully indexed interest rate that would apply after the low, initial fixed-rate period of two or three years. March 8: New Century Financial, the second largest subprime lender in 2006, stops

making loans. March 20: People’s Choice files for bankruptcy. March 22: The Senate Banking Committee holds a hearing to investigate the sharp

increase in defaults and foreclosures, questioning banking regulators who are criticized for failing to respond more quickly to curb the growth in risky home loans to people with weak credit. March 27: At a Joint Economic Committee, Ben Bernanke, Chairman of the Board of

Governors of the Federal Reserve System, says housing market weakness does not appear to have spilled over to a significant extent.

APRIL 2007 April 2: New Century Financial files for bankruptcy. April 6: American Home Mortgage writes down the value of risky mortgages rated one

step above subprime. April 11: The Joint Economic Committee, chaired by Senator Charles Schumer,

releases a report analyzing the subprime mortgage foreclosure problem April 18: Freddie Mac announces plans to refinance up to $20 billion of loans held by

subprime borrowers April 18: Senator Dodd hosts the Homeownership Preservation Summit, bringing

together some of the largest subprime lenders, securitizers, and servicers, as well as consumer and civil rights groups, to discuss ideas and develop solutions to crisis. April 24: The National Association of Realtors announces that sales of existing homes

fell 8.4% in March from February, the sharpest month-to-month drop in 18 years. MAY 2007

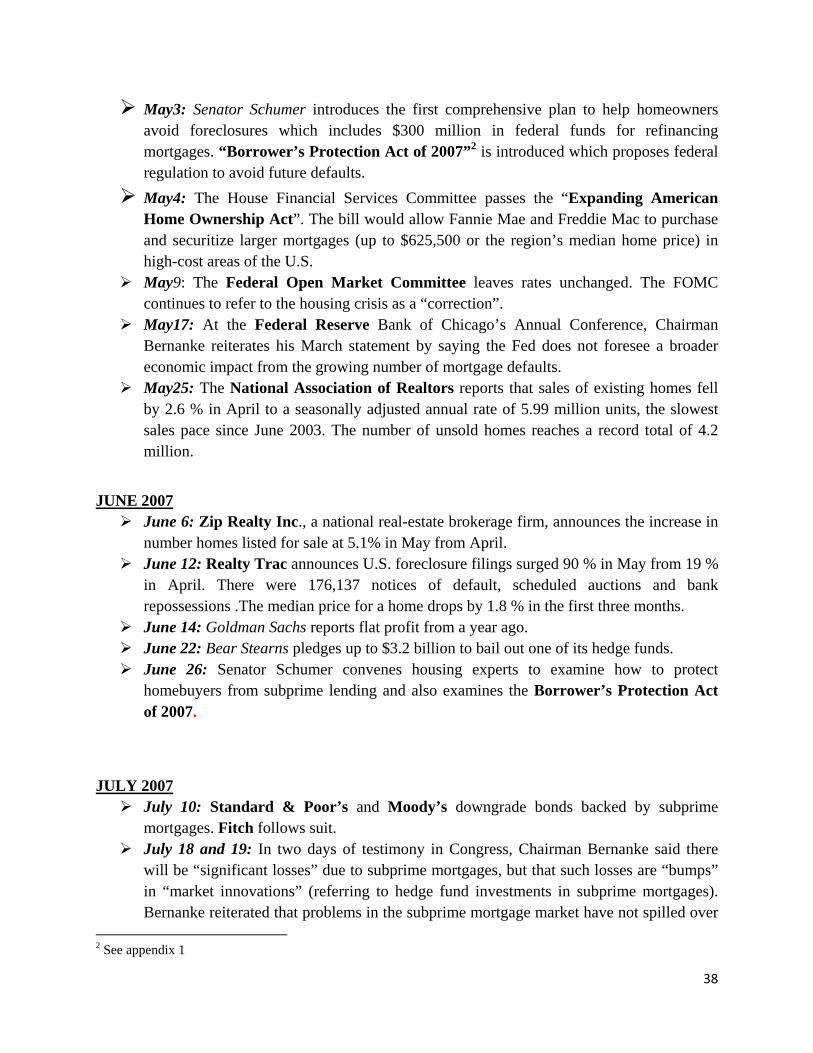

38

May3: Senator Schumer introduces the first comprehensive plan to help homeowners avoid foreclosures which includes $300 million in federal funds for refinancing mortgages. “Borrower’s Protection Act of 2007”2 is introduced which proposes federal regulation to avoid future defaults. May4: The House Financial Services Committee passes the “Expanding American Home Ownership Act”. The bill would allow Fannie Mae and Freddie Mac to purchase and securitize larger mortgages (up to $625,500 or the region’s median home price) in high-cost areas of the U.S. May9: The Federal Open Market Committee leaves rates unchanged. The FOMC

continues to refer to the housing crisis as a “correction”. May17: At the Federal Reserve Bank of Chicago’s Annual Conference, Chairman

Bernanke reiterates his March statement by saying the Fed does not foresee a broader economic impact from the growing number of mortgage defaults. May25: The National Association of Realtors reports that sales of existing homes fell

by 2.6 % in April to a seasonally adjusted annual rate of 5.99 million units, the slowest sales pace since June 2003. The number of unsold homes reaches a record total of 4.2 million.

JUNE 2007 June 6: Zip Realty Inc., a national real-estate brokerage firm, announces the increase in

number homes listed for sale at 5.1% in May from April. June 12: Realty Trac announces U.S. foreclosure filings surged 90 % in May from 19 %

in April. There were 176,137 notices of default, scheduled auctions and bank repossessions .The median price for a home drops by 1.8 % in the first three months. June 14: Goldman Sachs reports flat profit from a year ago. June 22: Bear Stearns pledges up to $3.2 billion to bail out one of its hedge funds. June 26: Senator Schumer convenes housing experts to examine how to protect

homebuyers from subprime lending and also examines the Borrower’s Protection Act of 2007.

JULY 2007 July 10: Standard & Poor’s and Moody’s downgrade bonds backed by subprime

mortgages. Fitch follows suit. July 18 and 19: In two days of testimony in Congress, Chairman Bernanke said there

will be “significant losses” due to subprime mortgages, but that such losses are “bumps” in “market innovations” (referring to hedge fund investments in subprime mortgages). Bernanke reiterated that problems in the subprime mortgage market have not spilled over

2 See appendix 1

39

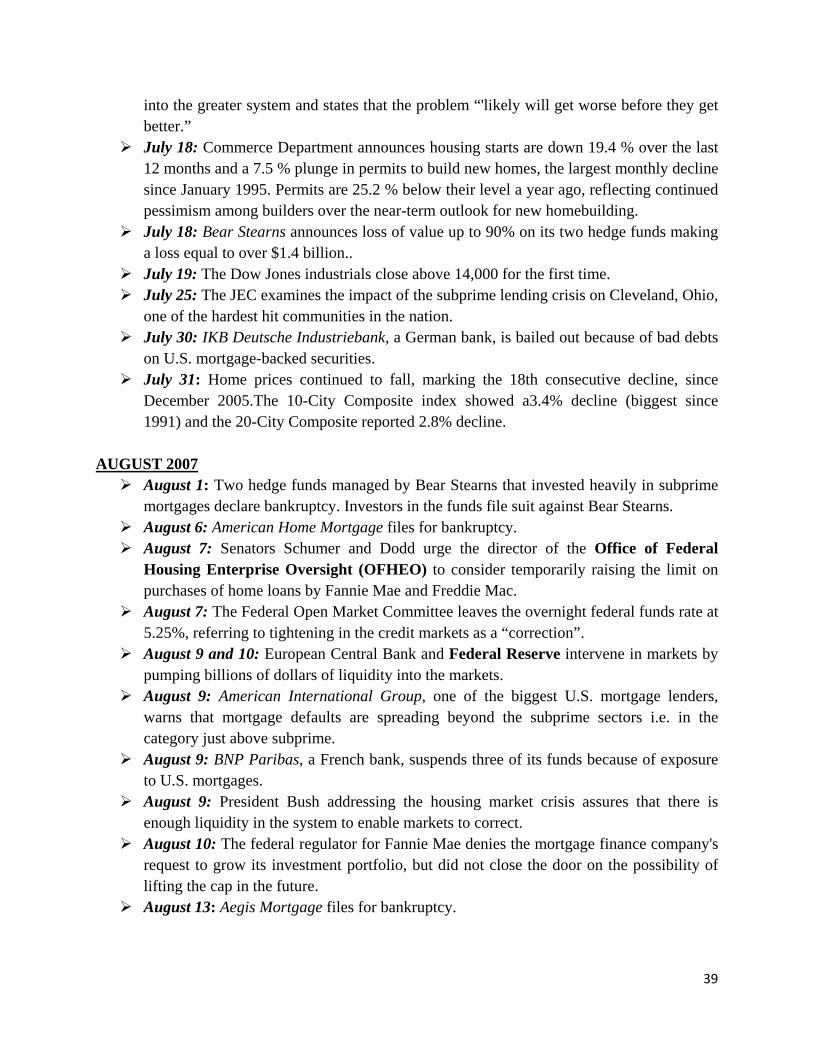

into the greater system and states that the problem “'likely will get worse before they get better.” July 18: Commerce Department announces housing starts are down 19.4 % over the last

12 months and a 7.5 % plunge in permits to build new homes, the largest monthly decline since January 1995. Permits are 25.2 % below their level a year ago, reflecting continued pessimism among builders over the near-term outlook for new homebuilding. July 18: Bear Stearns announces loss of value up to 90% on its two hedge funds making

a loss equal to over $1.4 billion.. July 19: The Dow Jones industrials close above 14,000 for the first time. July 25: The JEC examines the impact of the subprime lending crisis on Cleveland, Ohio,

one of the hardest hit communities in the nation. July 30: IKB Deutsche Industriebank, a German bank, is bailed out because of bad debts

on U.S. mortgage-backed securities. July 31: Home prices continued to fall, marking the 18th consecutive decline, since

December 2005.The 10-City Composite index showed a3.4% decline (biggest since 1991) and the 20-City Composite reported 2.8% decline.

AUGUST 2007

August 1: Two hedge funds managed by Bear Stearns that invested heavily in subprime mortgages declare bankruptcy. Investors in the funds file suit against Bear Stearns. August 6: American Home Mortgage files for bankruptcy. August 7: Senators Schumer and Dodd urge the director of the Office of Federal

Housing Enterprise Oversight (OFHEO) to consider temporarily raising the limit on purchases of home loans by Fannie Mae and Freddie Mac. August 7: The Federal Open Market Committee leaves the overnight federal funds rate at

5.25%, referring to tightening in the credit markets as a “correction”. August 9 and 10: European Central Bank and Federal Reserve intervene in markets by

pumping billions of dollars of liquidity into the markets. August 9: American International Group, one of the biggest U.S. mortgage lenders,

warns that mortgage defaults are spreading beyond the subprime sectors i.e. in the category just above subprime. August 9: BNP Paribas, a French bank, suspends three of its funds because of exposure

to U.S. mortgages. August 9: President Bush addressing the housing market crisis assures that there is

enough liquidity in the system to enable markets to correct. August 10: The federal regulator for Fannie Mae denies the mortgage finance company's

request to grow its investment portfolio, but did not close the door on the possibility of lifting the cap in the future. August 13: Aegis Mortgage files for bankruptcy.

40

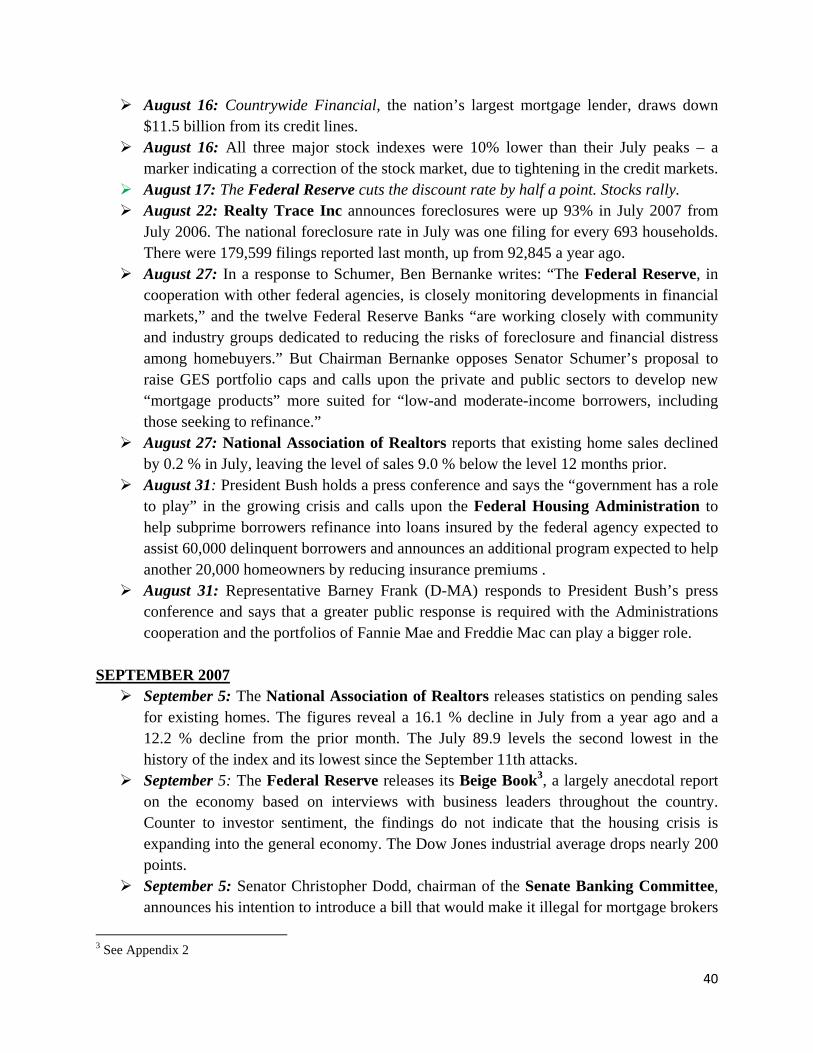

August 16: Countrywide Financial, the nation’s largest mortgage lender, draws down $11.5 billion from its credit lines. August 16: All three major stock indexes were 10% lower than their July peaks – a

marker indicating a correction of the stock market, due to tightening in the credit markets. August 17: The Federal Reserve cuts the discount rate by half a point. Stocks rally. August 22: Realty Trace Inc announces foreclosures were up 93% in July 2007 from

July 2006. The national foreclosure rate in July was one filing for every 693 households. There were 179,599 filings reported last month, up from 92,845 a year ago. August 27: In a response to Schumer, Ben Bernanke writes: “The Federal Reserve, in

cooperation with other federal agencies, is closely monitoring developments in financial markets,” and the twelve Federal Reserve Banks “are working closely with community and industry groups dedicated to reducing the risks of foreclosure and financial distress among homebuyers.” But Chairman Bernanke opposes Senator Schumer’s proposal to raise GES portfolio caps and calls upon the private and public sectors to develop new “mortgage products” more suited for “low-and moderate-income borrowers, including those seeking to refinance.” August 27: National Association of Realtors reports that existing home sales declined

by 0.2 % in July, leaving the level of sales 9.0 % below the level 12 months prior. August 31: President Bush holds a press conference and says the “government has a role

to play” in the growing crisis and calls upon the Federal Housing Administration to help subprime borrowers refinance into loans insured by the federal agency expected to assist 60,000 delinquent borrowers and announces an additional program expected to help another 20,000 homeowners by reducing insurance premiums . August 31: Representative Barney Frank (D-MA) responds to President Bush’s press

conference and says that a greater public response is required with the Administrations cooperation and the portfolios of Fannie Mae and Freddie Mac can play a bigger role.

SEPTEMBER 2007 September 5: The National Association of Realtors releases statistics on pending sales