us loan market 2021: charting the market rebound

TRANSCRIPT

US Loan Market –2021: Charting the Market Rebound

A Refinitiv LPC Special Report

June 2021

2

Effectiveness of vaccine rollout and distribution saves lives in the USFor 137 days straight, between Nov. 6, 2020, and Mar. 22, 2021, the US averaged over 1,000 Covid-related deaths per day, totaling over 307k during that span

Since late December, Covid-related deaths have dropped below 500/day as over 300 million Americans have been vaccinated against the Covid-19 virus

Source: Our World in Data

0

50

100

150

200

250

300

350

0.0

500.0

1,000.0

1,500.0

2,000.0

2,500.0

3,000.0

3,500.0

4,000.0

7-M

ar-

20

20-M

ar-

20

2-A

pr-

20

15-A

pr-

20

28-A

pr-

20

11-M

ay-2

0

24-M

ay-2

0

6-J

un-2

0

19-J

un-2

0

2-J

ul-20

15-J

ul-20

28-J

ul-20

10-A

ug-2

0

23-A

ug-2

0

5-S

ep-2

0

18-S

ep-2

0

1-O

ct-2

0

14-O

ct-2

0

27-O

ct-2

0

9-N

ov-2

0

22-N

ov-2

0

5-D

ec-

20

18-D

ec-

20

31-D

ec-

20

13-J

an-2

1

26-J

an-2

1

8-F

eb-2

1

21-F

eb-2

1

6-M

ar-

21

19-M

ar-

21

1-A

pr-

21

14-A

pr-

21

27-A

pr-

21

10-M

ay-2

1

23-M

ay-2

1

5-J

un-2

1

(Left) US Covid-19 deaths (7-day avg) & (Right) US Total Vaccinations (m)

US Covid-19 deaths (7-day avg) US Total Vaccinations (m)

Refinitiv LPC Special Report - June 2021

3

Refinitiv LPC Special Report - June 2021

Despite inflation concerns and recent employment numbers coming up short of expectations, vaccine rollout accelerates reopening

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

1Q

21

US Gross Domestic Product (% change from preceding period)

Source: U.S. Bureau of Economic Analysis, Bureau of Labor Statistics/U.S. Department of Labor, The Conference Board

0%2%4%6%8%

10%12%14%16%

Jul 2010

Nov 2

010

Mar

2011

Jul 2011

Nov 2

011

Mar

2012

Jul 2012

Nov 2

012

Mar

2013

Jul 2013

Nov 2

013

Mar

2014

Jul 2014

Nov 2

014

Mar

2015

Jul 2015

Nov 2

015

Mar

2016

Jul 2016

Nov 2

016

Mar

2017

Jul 2017

Nov 2

017

Mar

2018

Jul 2018

Nov 2

018

Mar

2019

Jul 2019

Nov 2

019

Mar

2020

Jul 2020

Nov 2

020

Mar

2021

US Unemployment Rate

-1.0%

-0.5%

0.0%

0.5%

1.0%

May-1

9

Jun-1

9

Jul-19

Aug-1

9

Sep-1

9

Oct

-19

Nov-1

9

Dec-

19

Jan-2

0

Feb-2

0

Mar-

20

Apr-

20

May-2

0

Jun-2

0

Jul-20

Aug-2

0

Sep-2

0

Oct

-20

Nov-2

0

Dec-

20

Jan-2

1

Feb-2

1

Mar-

21

Apr-

21

May-2

1

US Consumer Price Index

One lender recently told Refinitiv LPC that supply chain logistical issues and the struggle for companies to hire people were impacting things “across the

board,” but noted it was not devastating, and more a market functionality frustration

70.080.090.0

100.0110.0120.0130.0140.0

1-J

un-2

019

1-J

ul-2019

1-A

ug-2

019

1-S

ep-2

019

1-O

ct-2

019

1-N

ov-2

019

1-D

ec-

2019

1-J

an-2

020

1-F

eb-2

020

1-M

ar-

2020

1-A

pr-

2020

1-M

ay-2

020

1-J

un-2

020

1-J

ul-2020

1-A

ug-2

020

1-S

ep-2

020

1-O

ct-2

020

1-N

ov-2

020

1-D

ec-

2020

1-J

an-2

021

1-F

eb-2

021

1-M

ar-

2021

1-A

pr-

2021

1-M

ay-2

021

US Consumer Confidence

4

Refinitiv LPC Special Report - June 2021

OpenTable seated diner data shows restaurants are near-to 2019 levels, while TSA travel numbers show continued increases in number of airline passengersHowever, airlines expect to continue to see sub-2019 travel volumes due to a slower pick-up in business and international travel

Source: OpenTable Inc, TSA.gov

OpenTable Seated Diners: 2021 vs 2019, 2020 vs 2019

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1-J

an

8-J

an

15-J

an

22-J

an

29-J

an

5-F

eb

12-F

eb

19-F

eb

26-F

eb

5-M

ar

12-M

ar

19-M

ar

26-M

ar

2-A

pr

9-A

pr

16-A

pr

23-A

pr

30-A

pr

7-M

ay

14-M

ay

21-M

ay

28-M

ay

TSA Checkpoint Travel Numbers (M): Jan. through May 2019, 2020, 2021

2021 Traveler Throughput 2020 Traveler Throughput 2019 Traveler Throughput

5

Wells Fargo & Co

The bank said in March it plans to start bringing workers

back to its offices after Labor Day due to the increasing

availability of vaccines. The company is evaluating whether

to allow certain businesses or functional subgroups in the

United States to return to the workplace before Labor Day.

Refinitiv LPC Special Report - June 2021

Major financial institutions are plotting a return to the office and laying out visions for a future hybrid model

Goldman Sachs Group Inc

The bank is planning to bring U.S. employees back to

the office by mid-June.

JPMorgan Chase & Co

The largest U.S. bank will bring its employees in the United

States back to the office on a rotational basis from July and

plans to maintain a 50% occupancy cap during the return-to-

office phase.

Citigroup Inc

Chief Executive Officer Jane Fraser said in a memo in March

that post-pandemic, most of the employees would be able to

work in a "hybrid" setting, allowing them to work from home for

up to two days a week.

Barclays Plc

Chief Executive Officer Jes Staley has said the bank will adopt

a hybrid working model and will reduce its real estate footprint

but maintain its main offices in London and New York.

Credit Suisse

Credit Suisse in July 2020 launched a global program

evaluating various work-from-home options, which are

expected to shape its post-pandemic working models. It has

been monitoring and adapting work arrangements since

launching work-from-home globally in March 2020, taking into

account local guidelines.

Source: Reuters

6

Refinitiv LPC Special Report - June 2021

Refinitiv LPC’s lender survey showed most respondents are expecting that by this fall they will shake hands, network at conferences, or get on a plane to win new business

Source: Refinitiv LPC’s Quarterly Buyside & Sellside Survey

0% 20% 40% 60% 80%

Never

Once I'm vaccinated

Fall '21

Summer '21

Spring '21

Winter '20

Fall '20

Summer '20

When do you expect to shake hands?

2Q20 Survey 3Q20 Survey

4Q20 Survey 1Q21 Survey

0% 20% 40% 60% 80% 100%

Never

Once I'm vaccinated

Fall '21

Summer '21

Spring '21

Winter '20

Fall '20

Summer '20

When do you expect to attend a local conference/networking event?

2Q20 Survey 3Q20 Survey

4Q20 Survey 1Q21 Survey

0% 20% 40% 60% 80%

Never

Once I'mvaccinated

Fall '21

Summer '21

Spring '21

Winter '20

Fall '20

Summer '20

When do you expect to get on a plane to do introductory face to face meeting for new business or due diligence?

2Q20 Survey 3Q20 Survey

4Q20 Survey 1Q21 Survey

7

Refinitiv LPC Special Report - June 2021

Most surveyed lenders said winning new business and the quality of engagement with clients and co-workers had some upsides but plateaued by this spring while the pace of virtual meetings increased as deal flow picks up dramatically

Source: Refinitiv LPC’s Quarterly Buyside & Sellside Survey

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

No – struggles

with finding new

business are the same

Maybe – Hopeful

for a shift as

things open up

Yes – it has

become easier

Have the wins/losses shifted as you work to win new business virtually? (% of respondents)

1Q21 Survey

0%

10%

20%

30%

40%

50%

60%

Deteriorated –

Harder to reach

people

Improved - Moremeaningful and

substantive

Stayed the same

– Moderate to

meaningful

How has the quality of engagement with clients and co-workers changed?

4Q20 Survey 1Q21 Survey

0%

10%

20%

30%

40%

50%

60%

Meeting requestsare about the

same

Meeting requestshave slowed

There aren’t

enough hours in

the day to reply to all the meeting

requests

How has the pace of meetings and calls changed?

4Q20 Survey 1Q21 Survey

8

Refinitiv LPC Special Report - June 2021

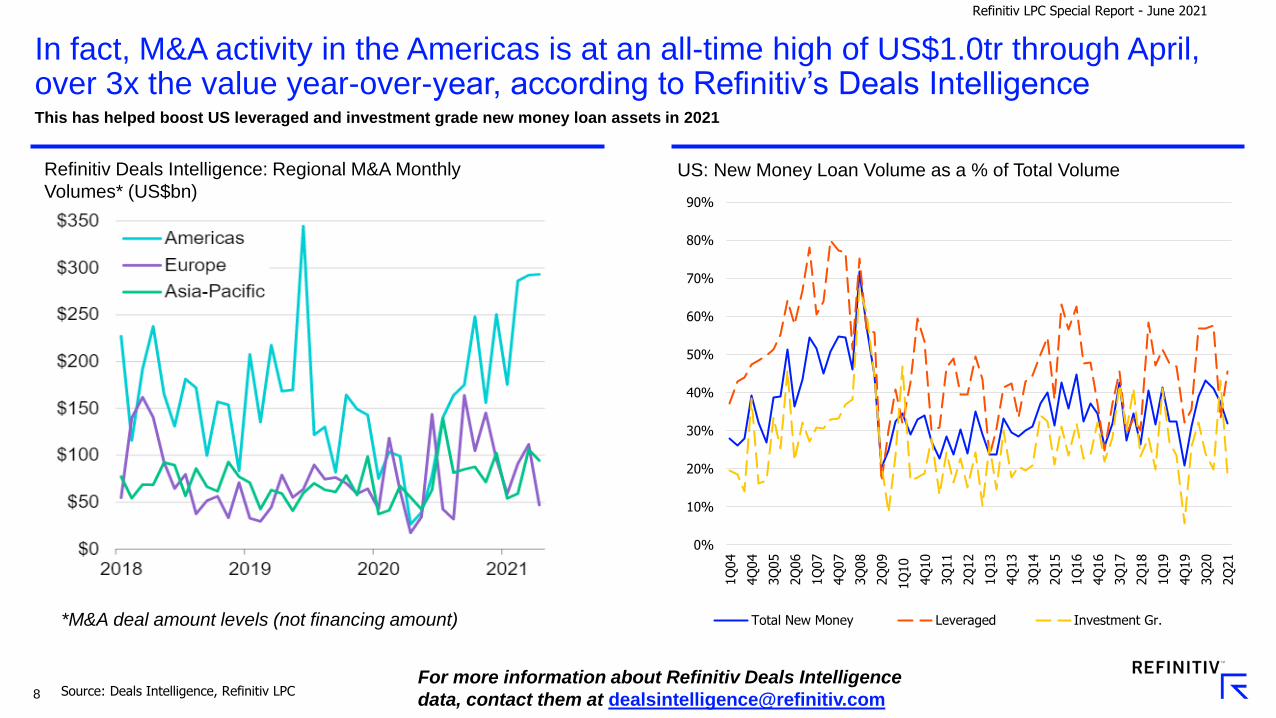

In fact, M&A activity in the Americas is at an all-time high of US$1.0tr through April, over 3x the value year-over-year, according to Refinitiv’s Deals IntelligenceThis has helped boost US leveraged and investment grade new money loan assets in 2021

Source: Deals Intelligence, Refinitiv LPC

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1Q

04

4Q

04

3Q

05

2Q

06

1Q

07

4Q

07

3Q

08

2Q

09

1Q

10

4Q

10

3Q

11

2Q

12

1Q

13

4Q

13

3Q

14

2Q

15

1Q

16

4Q

16

3Q

17

2Q

18

1Q

19

4Q

19

3Q

20

2Q

21

US: New Money Loan Volume as a % of Total Volume

Total New Money Leveraged Investment Gr.

Refinitiv Deals Intelligence: Regional M&A Monthly

Volumes* (US$bn)

*M&A deal amount levels (not financing amount)

For more information about Refinitiv Deals Intelligence

data, contact them at [email protected]

9

Refinitiv LPC Special Report - June 2021

Public and private equity fundraising are going full throttleUS private equity has surpassed US$180bn this year and is on pace for another >US$300bn year

According to Refinitiv Deals Intelligence, a global total of 670 IPOs were tracked through mid-May, the most in more than 20 years

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

YTD

-21

US Private Equity Fundraising (US$bn)

Turnaround/Distressed Debt Mezzanine Generalist Buyouts

Source: Refinitiv, Refinitiv Deals Intelligence

Refinitiv Deals Intelligence: Global IPO Volume

For more information about Refinitiv Deals Intelligence

data, contact them at [email protected]

10

Refinitiv LPC Special Report - June 2021

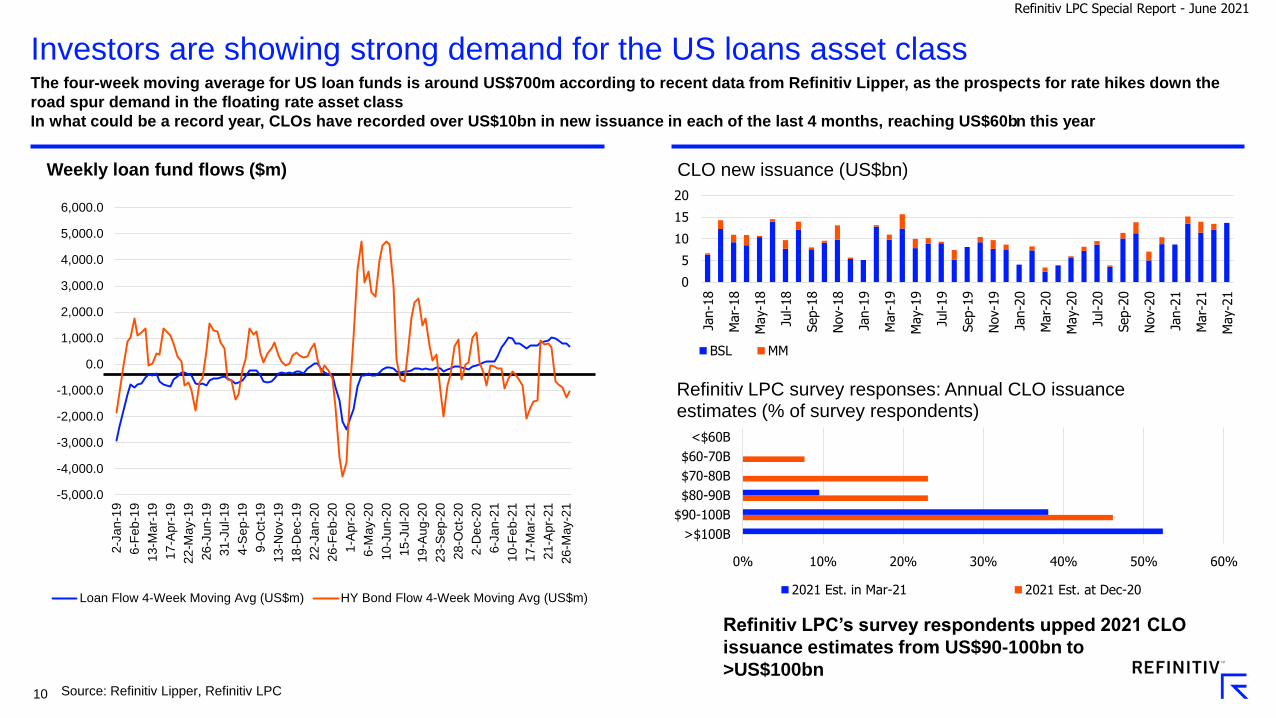

Investors are showing strong demand for the US loans asset class

Source: Refinitiv Lipper, Refinitiv LPC

The four-week moving average for US loan funds is around US$700m according to recent data from Refinitiv Lipper, as the prospects for rate hikes down the

road spur demand in the floating rate asset class

In what could be a record year, CLOs have recorded over US$10bn in new issuance in each of the last 4 months, reaching US$60bn this year

0

5

10

15

20

Jan-1

8

Mar-

18

May-1

8

Jul-18

Sep-1

8

Nov-1

8

Jan-1

9

Mar-

19

May-1

9

Jul-19

Sep-1

9

Nov-1

9

Jan-2

0

Mar-

20

May-2

0

Jul-20

Sep-2

0

Nov-2

0

Jan-2

1

Mar-

21

May-2

1

CLO new issuance (US$bn)

BSL MM

0% 10% 20% 30% 40% 50% 60%

>$100B

$90-100B

$80-90B

$70-80B

$60-70B

<$60B

Refinitiv LPC survey responses: Annual CLO issuance estimates (% of survey respondents)

2021 Est. in Mar-21 2021 Est. at Dec-20

-5,000.0

-4,000.0

-3,000.0

-2,000.0

-1,000.0

0.0

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

6,000.0

2-J

an-1

9

6-F

eb

-19

13

-Ma

r-1

9

17

-Ap

r-1

9

22

-Ma

y-1

9

26

-Ju

n-1

9

31

-Jul-

19

4-S

ep-1

9

9-O

ct-

19

13

-No

v-1

9

18

-De

c-1

9

22

-Ja

n-2

0

26

-Fe

b-2

0

1-A

pr-

20

6-M

ay-2

0

10

-Ju

n-2

0

15

-Ju

l-2

0

19

-Au

g-2

0

23

-Sep

-20

28

-Oct-

20

2-D

ec-2

0

6-J

an-2

1

10

-Fe

b-2

1

17

-Ma

r-2

1

21

-Apr-

21

26

-Ma

y-2

1

Weekly loan fund flows ($m)

Loan Flow 4-Week Moving Avg (US$m) HY Bond Flow 4-Week Moving Avg (US$m)

Refinitiv LPC’s survey respondents upped 2021 CLO

issuance estimates from US$90-100bn to

>US$100bn

11

Refinitiv LPC Special Report - June 2021

82% of CLO portfolio assets were marked at 98 or higher by the end of May, up from December’s 68%

Source: Refinitiv LPC

0%

10%

20%

30%

40%

50%

60%

0

<1

1 t

o <

2

2 t

o <

3

3 t

o <

4

4 t

o <

5

5 t

o <

10

10 t

o <

15

15 t

o <

20

>=

20

Share of US CLO universe / Percent of assets in default

Feb-20 Mar-20 Jun-20 Sep-20

Dec-20 Mar-21 Apr-21 May-21

0%

10%

20%

30%

40%

50%

60%

Share of US CLO Loan Holdings / Avg. bid (% of Par)

May-20 Dec-20 Mar-21 Apr-21 May-21

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Share of US CLOs / Weighted avg. bid (% of Par)

Feb-20 Mar-20 Jun-20 Dec-20

Mar-21 Apr-21 May-21

*excludes CLOs less than $50 million in size.

At the height of the pandemic, last May, the share of highly bid assets was just 6%

22% of US CLOs had a weighted average bid between 99-99.9 in May compared with 0% during February through December 2020

12

US broadly syndicated CLO AAA spreads have flattened in recent months after tightening near to post-pandemic lows back in March due to strong investor demand

80

100

120

140

160

180

200

220

240

260

280

Jan-1

6

Mar-

16

Mar-

16

Apr-

16

May-1

6

Jun-1

6

Jul-16

Aug-1

6

Sep-1

6

Oct

-16

Nov-1

6

Dec-

16

Jan-1

7

Feb-1

7

Mar-

17

Apr-

17

May-1

7

Jun-1

7

Jul-17

Aug-1

7

Sep-1

7

Oct

-17

Nov-1

7

Dec-

17

Jan-1

8

Feb-1

8

Mar-

18

Apr-

18

May-1

8

Jun-1

8

Jul-18

Aug-1

8

Sep-1

8

Oct

-18

Nov-1

8

Dec-

18

Jan-1

9

Feb-1

9

Mar-

19

Apr-

19

May-1

9

Jun-1

9

Jul-19

Aug-1

9

Sep-1

9

Oct

-19

Nov-1

9

Dec-

19

Jan-2

0

Feb-2

0

Mar-

20

Apr-

20

May-2

0

Jun-2

0

Jul-20

Aug-2

0

Sep-2

0

Oct

-20

Nov-2

0

Dec-

20

Jan-2

1

Feb-2

1

Mar-

21

Apr-

21

May-2

1

AAA Discount Margin (bp)

Source: Refinitiv LPC

*based on deals where discount margin is available

Refinitiv LPC Special Report - June 2021

The record supply seen earlier this year put pressure on spreads which has caused the leveling off

13

Refinitiv LPC Special Report - June 2021

US secondary loan bids have been stable most of this year, while lower rated loans make up for lost ground, gaining 5.6%

Source: ICE BAML, Refinitiv LPC/LSTA Mark to Market Pricing

The LPC 100 has increased 0.76% YTD, but most of that gain came in early January; meanwhile loans rated down the risk scale (<B3), have increased 5.6% YTD

The share of US secondary loans bid at par or better has increased to an 18% share of actively traded loans in recent weeks

76.0

78.0

80.0

82.0

84.0

86.0

88.0

90.0

92.0

94.0

96.0

98.0

100.0

102.0

104.0

106.0

2-J

an-1

8

8-A

pr-

18

13

-Jul-

18

17

-Oct-

18

21

-Jan

-19

27

-Apr-

19

1-A

ug-1

9

5-N

ov-1

9

9-F

eb

-20

15

-May-2

0

19

-Aug

-20

23

-Nov-2

0

27

-Fe

b-2

1

3-J

un-2

1

Avg. secondary bids: high yield bonds vs. US leveraged loans (% of par)

LPC 100 ML HY Bond Index

86.0

87.0

88.0

89.0

90.0

91.0

92.0

93.0

94.0

95.0

96.0

97.0

98.0

99.0

100.0

1-J

an-2

1

15

-Jan

-21

29

-Jan

-21

12

-Fe

b-2

1

26

-Fe

b-2

1

12

-Mar-

21

26

-Mar-

21

9-A

pr-

21

23

-Apr-

21

7-M

ay-2

1

21

-May-2

1

4-J

un-2

1

Average US secondary loan bids by ratings

Ba1/Ba2 Ba3 B1

B2/B3 < B3 Not Rated

< B3+5.6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1-J

an-2

0

1-F

eb-2

0

1-M

ar-

20

1-A

pr-

20

1-M

ay-2

0

1-J

un-2

0

1-J

ul-20

1-A

ug-2

0

1-S

ep-2

0

1-O

ct-2

0

1-N

ov-2

0

1-D

ec-

20

1-J

an-2

1

1-F

eb-2

11-M

ar-

21

1-A

pr-

21

1-M

ay-2

1

1-J

un-2

1

Secondary loan bid levels (share of loans)

x < 70 70-<90 90-<95

95-<98 98-<100 >=100

14

Oil and gas secondary bid levels are up roughly 24bp from pandemic lows as oil prices reach levels not seen since October 2018

-60

-40

-20

0

20

40

60

80

100

50

60

70

80

90

100

110

2-J

an-1

8

2-F

eb-1

8

2-M

ar-

18

2-A

pr-

18

2-M

ay-1

8

2-J

un-1

8

2-J

ul-18

2-A

ug-1

8

2-S

ep-1

8

2-O

ct-1

8

2-N

ov-1

8

2-D

ec-

18

2-J

an-1

9

2-F

eb-1

9

2-M

ar-

19

2-A

pr-

19

2-M

ay-1

9

2-J

un-1

9

2-J

ul-19

2-A

ug-1

9

2-S

ep-1

9

2-O

ct-1

9

2-N

ov-1

9

2-D

ec-

19

2-J

an-2

0

2-F

eb-2

0

2-M

ar-

20

2-A

pr-

20

2-M

ay-2

0

2-J

un-2

0

2-J

ul-20

2-A

ug-2

0

2-S

ep-2

0

2-O

ct-2

0

2-N

ov-2

0

2-D

ec-

20

2-J

an-2

1

2-F

eb-2

1

2-M

ar-

21

2-A

pr-

21

2-M

ay-2

1

2-J

un-2

1

Oil and Gas (North America) - Avg. Bid

Oil and Gas (North America) - Avg. Bid WTI (NYMEX)

NYMEX WTI (US$ per barrel)

Source: Refinitiv LPC/LSTA Mark to Market Pricing, Refinitiv Eikon

Refinitiv LPC Special Report - June 2021

As COVID-19 restrictions have eased, demand for gas and jet fuel has been on the rise. Meanwhile, OPEC and allies have agreed on supply restraints

through July. US West Texas Intermediate crude oil futures hit $70 per barrel for the first time since October 2018 the week starting June 7. As the

pandemic took hold and lockdowns were enforced around the world, oil prices went on a downward spiral, plummeting into negative territory for the

first time on April 20, 2020. Oil and gas bids followed, tumbling to a pandemic low of 71.95. The sector faced many challenges and defaults soared. But

as oil prices have recovered, so have oil and gas bids which are currently at the 95.7 level

15

Refinitiv LPC Special Report - June 2021

Behind strong demand from investors, US leveraged loan volume has flourished so far this yearCompleted US leveraged volume totaled US$569bn through June 3, 57% above the year-ago level and 86% ahead of 2019’s level through the same period

LBO volume totals around US$50bn so far in 2Q21, on pace for its best year since 2018

Source: Refinitiv LPC

-

20

40

60

80

100

120

140

160

180

Jan-1

8

Mar-

18

May-1

8

Jul-18

Sep-1

8

Nov-1

8

Jan-1

9

Mar-

19

May-1

9

Jul-19

Sep-1

9

Nov-1

9

Jan-2

0

Mar-

20

May-2

0

Jul-20

Sep-2

0

Nov-2

0

Jan-2

1

Mar-

21

May-2

1

US Leveraged Loan Volume (US$bn)

Pro rata Institutional

-

10

20

30

40

50

60

Jan-1

8

Mar-

18

May-1

8

Jul-18

Sep-1

8

Nov-1

8

Jan-1

9

Mar-

19

May-1

9

Jul-19

Sep-1

9

Nov-1

9

Jan-2

0

Mar-

20

May-2

0

Jul-20

Sep-2

0

Nov-2

0

Jan-2

1

Mar-

21

May-2

1

US Leveraged Loan M&A Volume (US$bn)

Non-LBO LBOs

16

Refinitiv LPC Special Report - June 2021

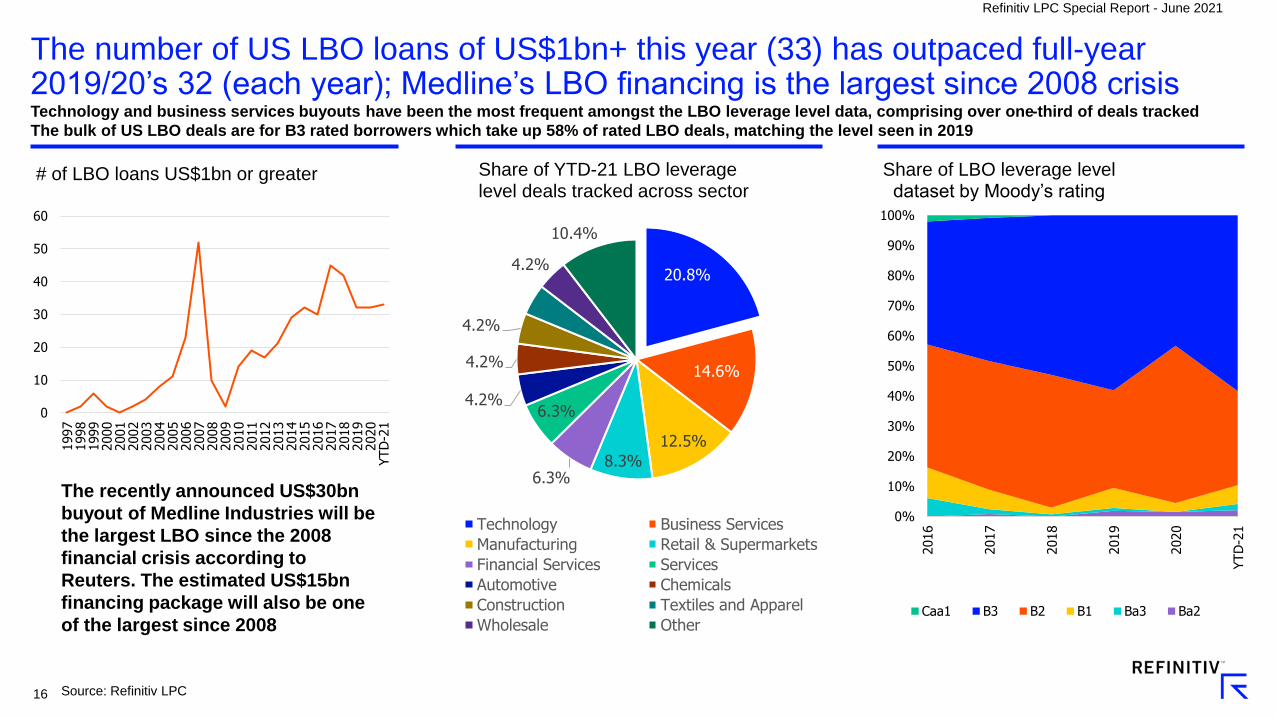

The number of US LBO loans of US$1bn+ this year (33) has outpaced full-year 2019/20’s 32 (each year); Medline’s LBO financing is the largest since 2008 crisisTechnology and business services buyouts have been the most frequent amongst the LBO leverage level data, comprising over one-third of deals tracked

The bulk of US LBO deals are for B3 rated borrowers which take up 58% of rated LBO deals, matching the level seen in 2019

Source: Refinitiv LPC

0

10

20

30

40

50

60

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

YTD

-21

# of LBO loans US$1bn or greater

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016

2017

2018

2019

2020

YTD

-21

Share of LBO leverage level dataset by Moody’s rating

Caa1 B3 B2 B1 Ba3 Ba2

20.8%

14.6%

12.5%

8.3%6.3%

6.3%4.2%

4.2%

4.2%

4.2%

4.2%

10.4%

Share of YTD-21 LBO leverage level deals tracked across sector

Technology Business Services

Manufacturing Retail & Supermarkets

Financial Services Services

Automotive Chemicals

Construction Textiles and Apparel

Wholesale Other

The recently announced US$30bn

buyout of Medline Industries will be

the largest LBO since the 2008

financial crisis according to

Reuters. The estimated US$15bn

financing package will also be one

of the largest since 2008

17

Refinitiv LPC Special Report - June 2021

Stiff competition for good targets has allowed leverage and purchase price multiples to remain elevated for large corporate US LBO deals60% of US LBO deals tracked have had total leverage 7x or greater so far this year, while purchase price multiples remain in the 13x area

Equity contributions have come down from 2019-20 levels but remain above 40%

Source: Refinitiv LPC

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

YTD

-21

Share (%) of large corporate LBOs levered >= 6.0x, 7.0x

>= 6x >=7x

6.0x

7.0x

8.0x

9.0x

10.0x

11.0x

12.0x

13.0x

14.0x

0

1,000

2,000

3,000

4,000

5,000

6,000

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

YTD

-21

Large Corp LBOs: Purchase Price (US$M) & Multiple (x:1)

Avg. Purchase Price PP Multiple

20%

25%

30%

35%

40%

45%

50%

55%

60%

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

YTD

-21

Large Corp LBO Avg. Equity Check Share (%)

18

Refinitiv LPC Special Report - June 2021

Strong institutional appetite led to a drop in institutional yields to 17-year lows in 1Q21; despite slight widening in 2Q21, yields remain at historically low levels

Source: Refinitiv LPC

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1H

08

1H

09

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

2Q

16

4Q

16

2Q

17

4Q

17

2Q

18

4Q

18

2Q

19

4Q

19

2Q

20

4Q

20

2Q

21TD

Middle market and large corporate quarterly average first-lien institutional primary term loan yields (3-year)

Large Corp MM

LIBOR+ Spread+OID (3-year)LIBOR+ Spread

*Due to lack of activity, 2Q20 MM yield level is an estimate assuming a 1.21% MM yield premium (avg. MM premium from 2009-1Q20)

Issuers took advantage of lower yields in 1Q21 to reprice their deals; so far this quarter, yields have widened as more M&A deals have entered the mix

At 4.62% for large corporate issuers and 5.99% in the middle market, 2Q21 primary yields are much lower than pre-pandemic levels

19

Refinitiv LPC Special Report - June 2021

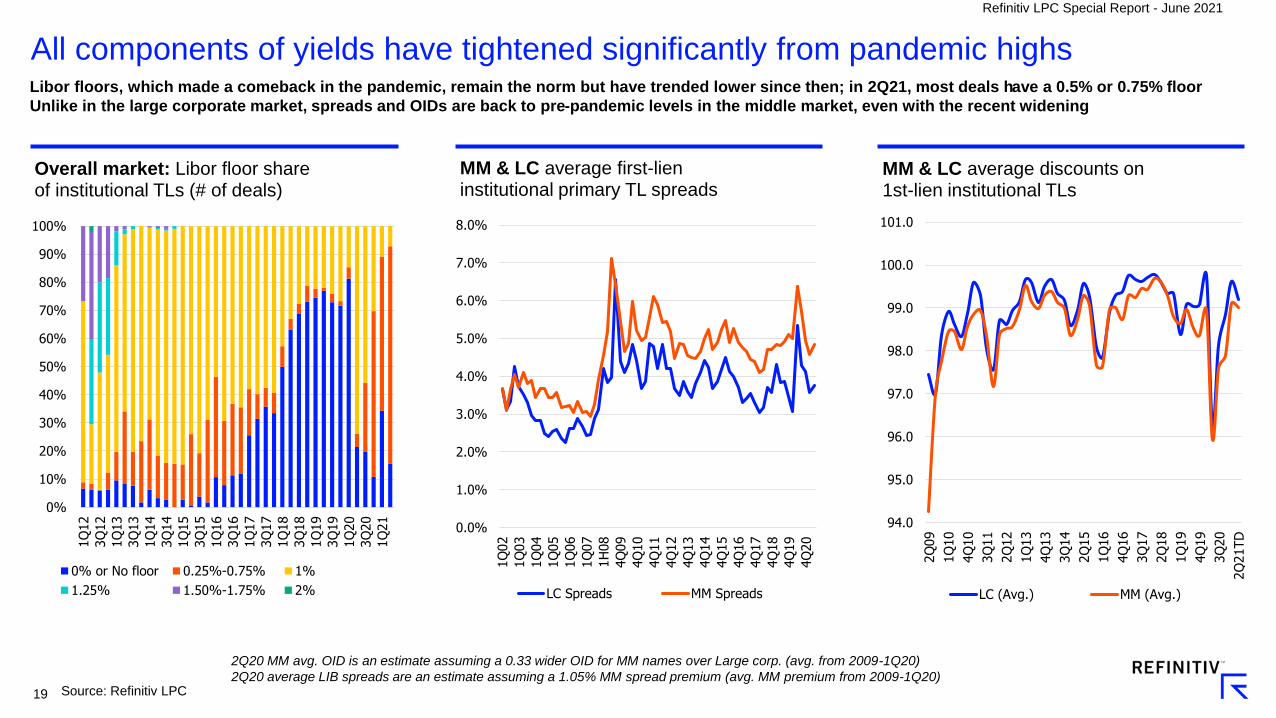

All components of yields have tightened significantly from pandemic highsLibor floors, which made a comeback in the pandemic, remain the norm but have trended lower since then; in 2Q21, most deals have a 0.5% or 0.75% floor

Unlike in the large corporate market, spreads and OIDs are back to pre-pandemic levels in the middle market, even with the recent widening

Source: Refinitiv LPC

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

3Q

17

1Q

18

3Q

18

1Q

19

3Q

19

1Q

20

3Q

20

1Q

21

Overall market: Libor floor share of institutional TLs (# of deals)

0% or No floor 0.25%-0.75% 1%

1.25% 1.50%-1.75% 2%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

1Q

02

1Q

03

1Q

04

1Q

05

1Q

06

1Q

07

1H

08

4Q

09

4Q

10

4Q

11

4Q

12

4Q

13

4Q

14

4Q

15

4Q

16

4Q

17

4Q

18

4Q

19

4Q

20

MM & LC average first-lien institutional primary TL spreads

LC Spreads MM Spreads

94.0

95.0

96.0

97.0

98.0

99.0

100.0

101.0

2Q

09

1Q

10

4Q

10

3Q

11

2Q

12

1Q

13

4Q

13

3Q

14

2Q

15

1Q

16

4Q

16

3Q

17

2Q

18

1Q

19

4Q

19

3Q

20

2Q

21TD

MM & LC average discounts on 1st-lien institutional TLs

LC (Avg.) MM (Avg.)

2Q20 MM avg. OID is an estimate assuming a 0.33 wider OID for MM names over Large corp. (avg. from 2009-1Q20)

2Q20 average LIB spreads are an estimate assuming a 1.05% MM spread premium (avg. MM premium from 2009-1Q20)

20

Refinitiv LPC Special Report - June 2021

There has been only $4.6bn of defaulted institutional loan volume in 2021, down 87% year over year, with just 3 defaults recorded since the end of FebruaryOf the 28 loans downgraded by Moody's, Fitch, S&P and/or DBRS in May, utilities, beverage food and tobacco and REITs were the top sectors

By contrast, May 2020 saw 169 loans downgraded with business services, retail/supermarkets, and automotive as the top 3 sectors

Source: Source: Fitch U.S. Leveraged Loan Default Index, Refinitiv LPC

0%

2%

4%

6%

8%

10%

12%

14%

16%

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Utilit

ies

Bevera

ge/F

ood

REIT

S

Tech

nolo

gy

Leis

ure

/Ente

rtain

Busi

ness

Serv

ices

Reta

il/Superm

ark

ets

Serv

ices

Tele

com

Whole

sale

Fin

anci

al Serv

ices

Manufa

cturing

Media

May 2021: Top Sectors of Downgraded Loans*, U.S. Issuers by count & share

No. of downgradedloans within each sector

Share (%)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Jan-1

9

Feb-1

9

Mar-

19

Apr-

19

May-1

9

Jun-1

9

Jul-19

Aug-1

9

Sep-1

9

Oct

-19

Nov-1

9

Dec-

19

Jan-2

0

Feb-2

0

Mar-

20

Apr-

20

May-2

0

Jun-2

0

Jul-20

Aug-2

0

Sep-2

0

Oct

-20

Nov-2

0

Dec-

20

Jan-2

1

Feb-2

1

Mar-

21

Apr-

21

May-2

1

Institutional Leveraged Loan Defaults: Defaulted Par Value (US$bn) and TTM default rate (%)

Par Value of Defaulted Inst Loans TTM Default Rate

*prior 30 days from May 31, 2021

21

Refinitiv LPC Special Report - June 2021

In the US investment grade loan market, activity has been strong all yearHigh-grade lenders were optimistic that 2021 could be a big year, and so far, they were right; YTD volume of US$460bn is 34% higher YOY and 17% ahead of

2019’s pace

Activity in the BBB space, the most suppressed in the IG market during the pandemic, has increased substantially, comprising a high 65% of overall IG volume

Source: Refinitiv LPC

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

YTD

-21

Investment grade market share by issuer rating

AAA AA A BBB

$0.0

$25.0

$50.0

$75.0

$100.0

$125.0

$150.0

$175.0

$200.0

$225.0

$250.0

$275.0

$300.0

$325.0

$350.0

1Q

03

4Q

03

3Q

04

2Q

05

1Q

06

4Q

06

3Q

07

2Q

08

1Q

09

4Q

09

3Q

10

2Q

11

1Q

12

4Q

12

3Q

13

2Q

14

1Q

15

4Q

15

3Q

16

2Q

17

1Q

18

4Q

18

3Q

19

2Q

20

1Q

21

Quarterly IG volume (US$bn)

22

Refinitiv LPC Special Report - June 2021

High-grade M&A financings, including jumbo deals, return to the foldThe WarnerMedia/Discovery deal totals US$47.5bn in loans, including a US$31.5bn bridge loan, the 8th highest in the US all-time

That deal will push US investment grade M&A volume to over US$100bn this year, on pace for the levels seen in the years before the pandemic

Source: Refinitiv LPC

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0

$80.0

$90.0

1Q

03

4Q

03

3Q

04

2Q

05

1Q

06

4Q

06

3Q

07

2Q

08

1Q

09

4Q

09

3Q

10

2Q

11

1Q

12

4Q

12

3Q

13

2Q

14

1Q

15

4Q

15

3Q

16

2Q

17

1Q

18

4Q

18

3Q

19

2Q

20

1Q

21

Quarterly IG M&A volume (US$bn)

WarnerMedia/Discovery IG M&A issuance ($bn)

Rank BorrowerBridge Loan

Size ($bn)Year

1 Verizon Communications $61.00 2013

2 CVS $49.00 2017

3 AT&T $40.00 2016

4 Abbvie $38.00 2019

5 Walt Disney Co* $35.70 2018

6 Allergan Plc/Actavis Plc $35.60 2014

7 Bristol Myers Squibb $33.50 2019

8 WarnerMedia/Discovery $31.50 2021

9 Cigna Corp $23.70 2018

10 Anthem Inc $22.50 2015

Largest US IG bridge loans

23

Refinitiv LPC Special Report - June 2021

Investment grade tenors and pricing are back to or nearing pre-pandemic levelsThe five-year tenor market has returned, comprising an over 50% share of revolver volume after 364-day terms became the popular go-to in 2020

Spreads for A-rated names have returned to the 95bp area on average while BBB spread averages have come down considerably compared to last year

Source: Refinitiv LPC

70.0

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

3Q

17

1Q

18

3Q

18

1Q

19

3Q

19

1Q

20

3Q

20

1Q

21

Average drawn investment grade spreads (bps)

A BBB

0%

10%

20%

30%

40%

50%

60%

70%

80%

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

3Q

17

1Q

18

3Q

18

1Q

19

3Q

19

1Q

20

3Q

20

1Q

21

Share of IG revolver volume across tenor

364-Day Facility 3-year 4-year 5-year

24

Refinitiv LPC Special Report - June 2021

Americas green & ESG loan activity officially takes off, jumping over 4.5x year-over-year; YTD global green & ESG loan volume already exceeds full year 2020 totals; Over US$22bn of ESG linked institutional loan volume has hit the global loan mart so far this year

0

50

100

150

200

250

300

350

0.0

25.0

50.0

75.0

100.0

125.0

150.0

175.0

200.0

225.0

250.0

2017

2018

2019

2020

YTD

2021

Global Green & ESG loan volume (US$bn)

Americas APAC EMEA Deal Count

Source: Refinitiv, Refinitiv LPC

0.0

0.5

1.0

1.5

2.0

2.5

Fle

nder

Sta

rk

Asd

a

Klo

ckner

Ple

nta

pla

st

Els

an

Quantu

m B

idco

Euro

Eth

nic

Foods

Bid

co S

AS

Ahls

ell

AB

Ahls

ell

AB

Gro

upe G

org

e S

A

Belron I

nte

rnational Ltd

Belron I

nte

rnational Ltd

EW

T H

old

ings

III

Corp

Cere

lia S

AS

UPC B

roadband H

old

ing B

V

UPC B

roadband H

old

ing B

V

Logopla

ste C

onsu

ltore

s…

Logopla

ste C

onsu

ltore

s…

Ram

say G

enera

le D

e S

ante

SA

Cerb

a H

ealthCare

SAS

Mehila

inen O

y

Sante

Cie

SASU

ESG Linked Institutional loan volume(US$bn)

25

Refinitiv LPC Special Report - June 2021

Syndicated US middle market activity has been stronger this quarter with over $33bn of completed volume tracked through early June

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

3Q

17

1Q

18

3Q

18

1Q

19

3Q

19

1Q

20

3Q

20

1Q

21

US syndicated middle market loan issuance (US$bn)

Source: Refinitiv LPC

Middle market definition: issuers with revenues of $500M and below and a total loan package of $500M and below* Syndicated: facilities syndicated to at least one participant up to $500M in deal size or clubbed up to $150M in deal size

2Q21 volume is on pace to be the highest level since the onset of the pandemic

There has been more institutional middle market volume as well, over US$8bn so far this quarter, which is on pace for the highest level since 3Q19

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

3Q

17

1Q

18

3Q

18

1Q

19

3Q

19

1Q

20

3Q

20

1Q

21

US syndicated middle market institutional Issuance (US$bn)

26

Refinitiv LPC Special Report - June 2021

Syndicated middle market M&A activity has been a driver of loan volume, with over US$9bn used for M&A purposes so far this quarter

Source: Refinitiv LPC

2021 middle market M&A loan activity has been more focused on business services and technology issuers compared with pre-pandemic

0%

5%

10%

15%

20%

25%

30%

35%

Healthca

re

Busi

ness

Serv

ices

Serv

ices

Tech

nolo

gy

Manufa

cturing

Whole

sale

Oil/

Gas

Busi

ness

Serv

ices

Healthca

re

Tech

nolo

gy

Serv

ices

Whole

sale

Manufa

cturing

Chem

icals

/Pla

stic

s

Busi

ness

Serv

ices

Tech

nolo

gy

Healthca

re

Manufa

cturing

Serv

ices

Whole

sale

Bevera

ge/F

ood

Top Sectors: Share of Syndicated Middle Market M&A Volume

Share of MM M&A volume

2020 YTD-212019

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

3Q

17

1Q

18

3Q

18

1Q

19

3Q

19

1Q

20

3Q

20

1Q

21

Middle market M&A loan volume (US$bn)

27

Refinitiv LPC Special Report - June 2021

Middle market loan fundraising remains consistently strongRefinitiv LPC has tracked roughly $43bn in YTD US middle market fundraising through the end of May, after over US$100bn was raised in 2020

More sponsors have found the ease of execution in the direct lending market more favorable, leading that market to see around two times more volume

compared to the syndicated market over the last six quarters

Source: Refinitiv LPC

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

1Q

21

2Q

21-T

D

Quarterly: Middle market loan fundraising (US$bn)

MM CLO BDC Public Equity Private Debt Funds Mezzanine

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

1Q

21

MM Direct Lending Sponsored Volume relative to Syndicated MM Sponsored volume (x:1)

Direct Lending MM Sponsored Issuance/ Syndicated MM SponsoredIssuance

28

Refinitiv LPC Special Report - June 2021

US unitranche volume scored a record in 1Q21 as larger uni deals returnLarge corporate unitranche deals bounced back in 1Q21, and in April, Calypso Technology obtained a US$2.3bn unitranche loan as part of its LBO financing

Delay-draw term loans have become more popular to include in direct lending loan structures, sometimes for a specific acquisition in mind, or to back an

overall strategy that includes potential tack-on acquisitions

Source: Refinitiv LPC

*Includes both large corp. and middle market unitranches Refinitiv LPC relies on lenders to flag deals as unitranchesRefinitiv LPC also looks at a combination of spread (in conjunction with EBITDA size), leverage and loan-to-value (LTV) to flag unitranchesMiddle market is for issuers with a deal size and revenue size of $500M and below. Large corp. is either deal size or revenue size > $500M

0%

2%

4%

6%

8%

10%

12%

14%

16%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

1Q

21

MM Delay Draw Term Loan Volume (US$bn)

Direct DDTL Syndicated DDTL % of volume

% of issuance

0

50

100

150

200

250

300

350

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

1H

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

1Q

21

2Q

21-T

D

Avg. Loan D

eal Siz

e (

$M

ils.)

Unitra

nch

e V

olu

me (

$B.)

Quarterly US Unitranche Volume (US$bn)*

Middle Market Large. Corp. Avg. Deal Size

29

BDC originations saw the two highest levels on record in 4Q20 and 1Q21

Refinitiv LPC Special Report - June 2021

Source: Refinitiv’s BDC Collateral & Wells Fargo Securities, LLC

Note: Origination analysis includes bulk of the public BDCs and a few of the bigger private BDCs, roughly 45 names in the cohort

0.30

0.35

0.40

0.45

0.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

5/1

1/2

011

5/1

1/2

012

5/1

1/2

013

5/1

1/2

014

5/1

1/2

015

5/1

1/2

016

5/1

1/2

017

5/1

1/2

018

5/1

1/2

019

5/1

1/2

020

5/1

1/2

021

BDC share price to Net Asset Value (per share)*

-60%

-40%

-20%

0%

20%

40%

60%

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

YTD

2021

Cross asset returns %

Wells Fargo BDC Index S&P/LSTA Index S&P500

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

2Q

16

4Q

16

2Q

17

4Q

17

2Q

18

4Q

18

2Q

19

4Q

19

2Q

20

4Q

20

Quarterly BDC origination volume (US$bn)

Originations

BDC share price to NAV recently rose above 1x for the first time since 2017; by contrast, that average bottomed out at 0.39x in March 2020

Looking at cross asset returns shows the Wells Fargo BDC Index is returning over 30% so far this year, well above the S&P/LSTA Index and S&P500 returns

30

Why choose BDC Collateral?BDC Collateral provides a standardized view of the BDC asset

class, arming CFOs within BDC managers, research analysts,

investors, and valuation firms with news, data and analytical insights on nearly 100 public and private BDCs.

That data is enhanced with exclusive analysis from across the

universe of Refinitiv and LPC offerings, including Refinitiv™ Loan

Connector®, DealScan, LPC Collateral, Eikon and the LSTA/Refinitiv Mark-to-Market Pricing Service.

Use BDC Collateral to view the underlying assets of BDCs and

track exposures by many different metrics.

BDC Collateral is your one-stop source for critical analysis and

insights including:

• BDC-level news

• Links to Investor earnings calls and special events

• Institutional equity ownership for each BDC

• Web links to borrower and manager sites and BDC filings

• Current/historical industry and financial product concentrations

• Market-level news

• Asset-level secondary loan pricing (where available)

• Historical and special dividends

• Broker recommendations and reports

• Competitor/peer comparison analysis

BDC COLLATERALThe one-stop resource for analyzing BDCs, holdings and performance

For more information

loanpricing.com

bdccollateral.com

View an introductory BDC Collateral video here!

31

Refinitiv LPC’s US Analyst Team

David Puchowski

Director of Market Analysis

Diana Diquez

Contributor Relations Manager

Hugo Pereira

Director of Market Analysis

Elizabeth Han

Director of Market Analysis

Ioana Barza

Head of Market Analysis

Maria C. Dikeos

Head of Global Loans

Contributions

Jordan Ruck

Market Analyst

Alp Zavaro

Market Analyst

David Miao

Contributor Relations Manager

Bryan Diaz

Deals Contribution Analyst

32

Refinitiv Copyright Notice

©2021 Refinitiv. All rights reserved. The Refinitiv content received through

this service is the intellectual property of Refinitiv or its third-party

suppliers. Republication or redistribution of content provided by Refinitiv is

expressly prohibited without the prior written consent of Refinitiv, except

where permitted by the terms of the relevant Refinitiv service agreement.

Neither Refinitiv nor its third-party suppliers shall be liable for any errors,

omissions or delays in content, or for any actions taken in reliance

thereon. Contact Refinitiv at [email protected]