us inbound insights

TRANSCRIPT

US Inbound insights

US Business, policy and trade December 10, 2019

US Economic & Federal Budget

outlook

3

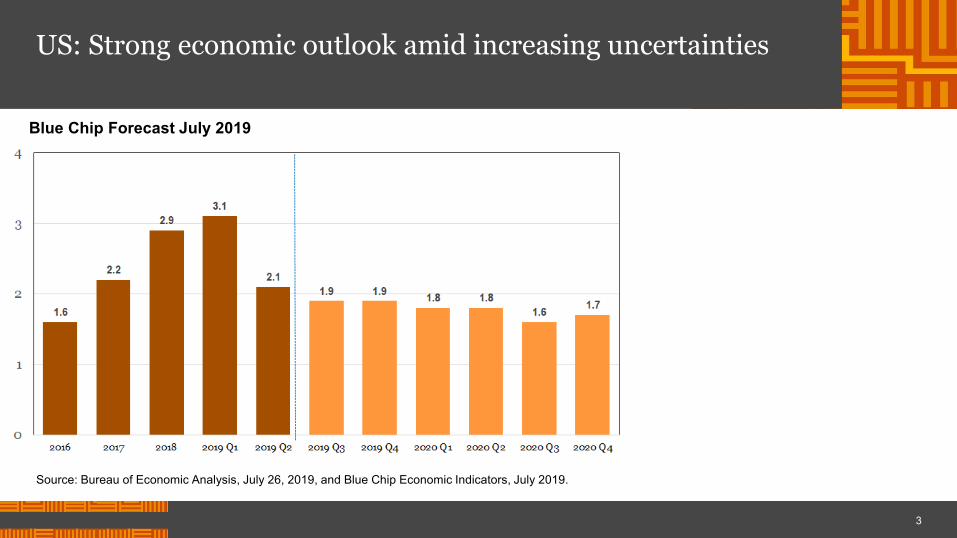

Source: Bureau of Economic Analysis, July 26, 2019, and Blue Chip Economic Indicators, July 2019.

Blue Chip Forecast July 2019

US: Strong economic outlook amid increasing uncertainties

4

Source: Bureau of Labor Statistics, US Department of Labor, July 2019.

US: Job openings exceed number of unemployedMillions of workers

5

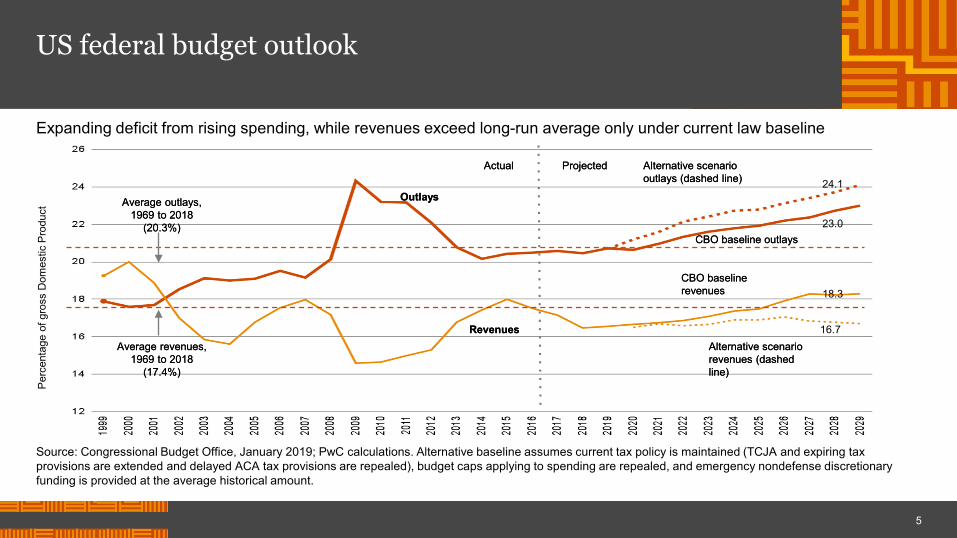

Source: Congressional Budget Office, January 2019; PwC calculations. Alternative baseline assumes current tax policy is maintained (TCJA and expiring tax provisions are extended and delayed ACA tax provisions are repealed), budget caps applying to spending are repealed, and emergency nondefense discretionary funding is provided at the average historical amount.

Expanding deficit from rising spending, while revenues exceed long-run average only under current law baseline

Perc

enta

ge o

f gro

ss D

omes

tic P

rodu

ct

Average outlays, 1969 to 2018

(20.3%)

Outlays

Revenues

Actual Projected Alternative scenario outlays (dashed line)

CBO baseline outlays

CBO baseline revenues

Alternative scenario revenues (dashed line)

Average revenues, 1969 to 2018

(17.4%)

24.1

23.0

18.3

16.7

US federal budget outlook

US Political

developments

US: Divided government defines the 116th Congress

7

8

US: 2020 Senate elections Democrats need +4 net gain (+3 with Democratic Vice President)

Source: University of Virginia Center for Politics (updated October 3, 2019)

9

President Trump’s narrow victory margin in key states may pose challenge in 202010 states were decided by less than 5% in 2016

PA

ME*

NC

MIWI

MN

NV

FL

NH-4

AZ

NH

OHWV VA

NY

SCGA

KY

IN

LATX

OK

IDOR

WA

CA

NM

CO

WY

MT ND

SD

IA

UT

AR

MO

MS AL

NE

KS

AK

HI

IL

NY

VT

TN

Trump by 1% (27,257 votes)

Trump by 0.3% (13,080 votes)

Clinton by 1.5% (44,470 votes)

Clinton by 2.7% (19,995 votes)

Trump by 3.9 % (91,682 votes)

Clinton by 2.4% (26,434 votes)

Trump by 3.8% (177,009 votes)

Trump by 1.2% (68,236 votes)

Trump by 1.2% (112,911 votes)

Clinton by 0.4% (2,701 votes)

Clinton won 232Trump won 306

* Clinton won Maine’s statewide vote, but Trump received an electoral vote for winning the 2nd districtSource: National Journal research 2019

Electoral College majority: 270

Tax Policy

today

Some tax reform provisions are ‘permanent’ but others are temporary/subject to sunset

11

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027Corporate rate reductionCorporate AMT repealCost recovery (full/partial expensing)Business interest limitationGlobal intangible low-taxed incomeBase erosion anti-avoidance taxForeign-derived intangible incomeNOL limitationR&E capitalizationPass-through deductionIndividual rate reductionModification of individual AMTIncreased standard deduction$10k limit state & local deductionIncreased estate tax exemption

Temporary Permanent

12

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029Deficit as % of GDP -3.8 -4.2 -4.1 -4.2 -4.7 -4.6 -4.3 -4.5 -4.4 -4.1 -4.8 -4.4Debt held by the public (% of GDP) 77.8 78.3 79.6 81.2 83.2 85.0 86.2 87.7 89.0 90.0 91.5 92.7

Deficit in $billion

2019CFC look-thru expires

2022163(j) EBIT limit and R&E capitalization begin

2023Expensing phase-out (80%, 60%, 40%, 20%, 0%) begin

2025Final year of tax reform individual provisions

2026Higher taxes under GILTI, BEAT and FDII begin

Rising budget deficits may affect future tax policy

Source: Congressional Budget Office, January 2019

US tax reform International Update

Agenda

• Status of the Treasury Guidance in Response to U.S Tax Reform

• BEAT Final and Proposed Regulations

14

15

Regulatory Guidance

1

16

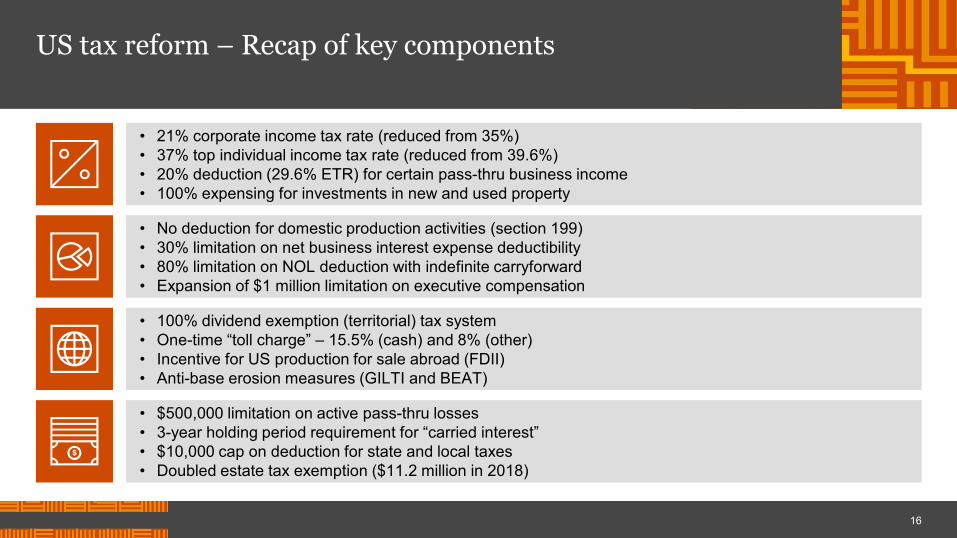

• 21% corporate income tax rate (reduced from 35%)• 37% top individual income tax rate (reduced from 39.6%)• 20% deduction (29.6% ETR) for certain pass-thru business income• 100% expensing for investments in new and used property

• No deduction for domestic production activities (section 199)• 30% limitation on net business interest expense deductibility• 80% limitation on NOL deduction with indefinite carryforward• Expansion of $1 million limitation on executive compensation

• 100% dividend exemption (territorial) tax system• One-time “toll charge” – 15.5% (cash) and 8% (other)• Incentive for US production for sale abroad (FDII)• Anti-base erosion measures (GILTI and BEAT)

• $500,000 limitation on active pass-thru losses• 3-year holding period requirement for “carried interest”• $10,000 cap on deduction for state and local taxes• Doubled estate tax exemption ($11.2 million in 2018)

US tax reform – Recap of key components

17

US hybrid system under tax reform expands current taxation (without deferral) to certain active income (GILTI) while exempting certain other income with 100% exemption

Method of Taxation OECD Countries (excluding US)Dividend exemption percentage

Territorial Tax Systems (29 countries)Exempt foreign-source dividends from domestic income taxation through territorial tax system

Australia, Austria, Canada, Czech Republic, Denmark, Estonia, Finland, Greece, Hungary, Iceland, Latvia, Luxembourg, Netherlands, New Zealand, Poland, Portugal, Slovak Republic, Spain, Sweden, Turkey, United Kingdom

100% exemption

Norway 97% exemptionBelgium, France, Germany, Italy, Japan, Slovenia, Switzerland

95% exemption

Worldwide Tax Systems (5 countries)Worldwide system of income taxation with deferral and foreign tax credit

Country 2017 Tax Rate 0% exemptionChile 25.0%Ireland 12.5%Israel 24.0%Korea 24.2%Mexico 30.0%

International taxation – A hybrid US tax system

18

Key provisions Release datesProposed guidance for anti-hybrid transactions under Section 267A December 20, 2018Final guidance relating to Section 965 transition tax January 15, 2019Final guidance under Section 199A (computational) January 18, 2019Proposed Section 250 guidance on deductions for foreign derived intangible income (FDII) and GILTI March 4, 2019Final and proposed regulations on global intangible low-taxed income (GILTI) under Section 951A June 14, 2019Temporary regulations limiting certain otherwise available Section 245A dividend deductions June 14, 2019Proposed guidance under Section 382(h) built-in gain or loss September 9, 2019Final and proposed guidance under Section 168(k) bonus depreciation September 13, 2019Proposed guidance on ownership attribution under Section 958 October 1, 2019Final guidance for base erosion & anti-avoidance tax (BEAT) December 2, 2019Final guidance for foreign tax credits under new tax law December 2, 2019Final guidance for Section 163(j) business interest limitation/ FDII/ Section 245A/ GILTI (HTE) Dec. 2019/Jan. 2020

Source: Treasury Department and OMB Office of Information and Regulatory (Expected guidance shown in italics)

US: Treasury and IRS focus on tax reform guidance

19

BEAT Final and Proposed Regulations

2

20

Background● The BEAT, enacted as Section 59A, is intended to subject both US corporations and non-US corporations doing

business within the United States to a minimum tax if deductions arising from ‘base erosion payments’ exceed a threshold percentage of total deductions in any tax year.

● A base erosion payment generally is a payment to a foreign related party that results in a deduction, either currently or in the future (e.g., depreciation deductions resulting from a purchased asset).

● The BEAT is imposed to the extent that 10% of the taxpayer’s Modified Taxable Income (MTI) exceeds the taxpayer’s regular tax liability, reduced by certain credits.

○ MTI is taxable income determined without regard to any base erosion tax benefits plus the base erosion percentage of the net operating loss (NOL) deduction for the tax year.

● The BEAT rate is 5% for tax years beginning in calendar year 2018; 10% for tax years beginning in 2019 through 2025; and 12.5% for tax years beginning after December 31, 2025.

● The BEAT is effective for base erosion payments paid or accrued in tax years beginning after 2017.

● Treasury and the IRS on December 21, 2018, released the 2018 Proposed Regulations relating to BEAT.

21

Applicability Final Regulations

● Generally are applicable for tax years ending on or after December 17, 2018.● Taxpayers may rely on the Final Regulations in their entirety for tax years ending before December 17,

2018, but must do so consistently and cannot selectively choose which particular provisions to apply.Proposed Regulations

● Generally are applicable to tax years beginning on or after the date the regulations are filed as final regulations in the Federal Register.

● Partnerships’ allocation of income in lieu of deductions, curative allocations, and transactions involving derivatives on a partnership interest and partnership allocations to eliminate or reduce a base erosion payment apply to tax years ending on or after December 2, 2019.

● Taxpayers may rely on the 2019 Proposed Regulations in their entirety for tax years beginning after December 31, 2017 and before the final regulations are finalized.

Highlights of the Final Regulations

23

Provisions retained as proposed ● No exception to the definition of ‘base erosion payment’ for payments that are subpart F, GILTI,

or PFIC inclusions

● No further expansion of the Services Cost Method (SCM) exception

● No deemed cost of goods sold (COGS) for services

○ Language was added explicitly providing that COGS are not base erosion payments

● Netting of payments is not allowed except where generally applicable US tax law allows computation of deductions on a net basis

● The “add-back” approach for calculating MTI is retained

● Foreign tax credits continue to reduce MTI

○ The Final Regulations do add the corporate alternative minimum tax credit to the list of credits that do not reduce MTI

24

2018 Proposed Regulations● Provided that non-cash payments to a foreign related party, in a non-recognition transaction, will qualify

as base erosion payments (e.g., transactions described in Sections 351, 332, and 368)Final Regulations● Exclude from the definition of base erosion payment amounts transferred to, or exchanged with, a

foreign related party in a ‘specified nonrecognition transaction’ (i.e., transactions described in Sections 332, 351, 355, and 368).○ Added addressing specified nonrecognition transactions that have a principal purpose of

increasing the adjusted basis of property that a taxpayer acquires in the nonrecognition transaction.■ Deemed anti-abuse when a transaction between related parties increases the adjusted

basis of property within the six-month period before the taxpayer acquires the property in a specified nonrecognition transaction.

■ If a taxpayer transfers ‘other property’ to a foreign related party pursuant to a Section 351, 355, or 368 nonrecognition transaction, the other property is treated as a base erosion payment regardless of whether gain is recognized on the transaction.

Non-recognition transactions

25

Facts:● During the current year FP transferred depreciable

property with an adjusted basis of $80 and a fair value of $100 to USCo in exchange for USCo stock in an exchange that qualified under Section 351(a).

Analysis● The Final Regulations provide that any amount

transferred to, or exchanged with, a foreign related party pursuant to a “specified nonrecognition transaction” (which includes a transaction to which section 351 applies) is not a base erosion payment.

● Under the Final Regulations, the depreciation on the depreciable property will not qualify as a base erosion payment under Prop. Reg. sec. 1.59A-3(b).

USCo

FP

Depreciable property:AB: $80FV: $100

Depreciable property

Depreciable property

Depreciable property

USCo stock

Depreciable property:AB: $80FV: $100

Example - Non-recognition transactions

26

Loss transactions

2018 Proposed Regulations● The preamble stated that “a base erosion payment also includes a payment to a foreign related party resulting

in a recognized loss; for example, a loss recognized on the transfer of property to a foreign related party.”

Final Regulations● Provide that a loss recognized from the sale or transfer of property (e.g., stock or receivables) to a foreign related

party is not itself a base erosion payment○ If the transfer of built-in-loss property would otherwise qualify as a base erosion payment, the amount of

the base erosion payment will be limited to the fair market value of the property transferred.

27

Facts:● USCo transferred built-in loss property with an

adjusted basis of $500 and a fair market value of $100 to its foreign parent (FP) in exchange for depreciable property from FP valued at $100.

Analysis

● USCo recognized a $400 loss on the distribution of the property. Under the Final Regulations the loss does not qualify as a base erosion payment.

● Because USCo receives depreciable property (where the depreciation to USCo would otherwise qualify as a base erosion payment) in exchange for the built-in loss property, USCo has a base erosion payment equal to $100 (the FMV of the built-in loss property).

USCo

FP

AB: $500FMV: $100

Built-in loss property

Built-in loss property

Depreciable Property (valued at $100)

AB: $500FMV: $100

Example - Loss Transactions

28

Application of Section 152018 Proposed Regulations● For a fiscal-year taxpayer, Section 15 would apply to any tax year beginning after January 1, 2018.● Fiscal-year taxpayers would have a

○ (1) 0% BEAT rate for the tax year that includes January 1, 2018○ (2) blended rate between 5% and 10% for the tax year that includes January 1, 2019○ (3) blended rate between 10% and 12.5% for the tax year that includes January 1, 2026

Final Regulations● Reverse the 2018 Proposed Regulations and provide that Section 15 does not apply to change the tax

rate for fiscal years ending in 2019. However, Section 15 will apply for fiscal-years ending in 2026.● Fiscal-year taxpayers have a

○ (1) 0% BEAT rate for the tax year that includes January 1, 2018○ (2) a 5% rate for the tax year that includes January 1, 2019○ (3) blended rate between 10% and 12.5% for the tax year that includes January 1, 2026

Highlights of the Proposed Regulations

Waiver of deductions

30

Statute

● Section 59A(d)(1) defines “base erosion payment” as any amount paid or accrued by the taxpayer to a foreign person which is a related party of the taxpayer and with respect to which a deduction is “allowable.”

● Section 59A(c)(2)(A) defines “base erosion tax benefit” in reference to deductions “allowed” for the taxable year.

2019 Proposed Regulations

● Provide that all deductions that could be claimed by a taxpayer for the tax year are treated as allowed deductions for purposes of determining a taxpayer’s base erosion tax benefits and thus the taxpayers base erosion percentage.

○ Provide that taxpayers may elect, on an annual basis, to waive certain deductions (on an original return, an amended return, or during exam) and thus not take those deductions into account as base erosion tax benefits.

○ Any deduction that is electively waived is treated as having been waived for all purposes of the Code and regulations.

Application to partnerships

31

Curative Allocations

● The Final Regulations treat deductions allocated by a partnership to an applicable taxpayer as base erosion tax benefits (assuming the deductions are base erosion payments).

● The proposed regulations address scenarios where partnerships, rather than allocating deductions that could give rise to base erosion tax benefits, curatively allocate less income to applicable taxpayer. In this scenario, the applicable taxpayer is treated as having a base erosion tax benefit equal to the amount of deduction that would have been allocated absent the curative allocation.

Anti-abuse Rules

● Added new anti-abuse rules aimed at derivatives on partnership interests and targeting allocations by a partnership to prevent or reduce a base erosion payment.

US Trade

developments

US: President Trump taking action on trade

Statute Presidential powersNAFTA Implementation Act of 1993

May terminate agreement with six months notice. Ability to proclaim a return to most-favored-nation tariffs on imports from Canada and Mexico. Ability to proclaim additional duties following consultations with Congress.

International Emergency Economic Powers Act of 1977

Regulation of all forms of international commerce, including the power to freeze all kinds of foreign-owned assets, if the President declares a “national emergency” with respect to a foreign threat

Trade Act of 1974, Section 122 Imposition of tariffs up to 15%, quantity restrictions, or both, for up to a 150-day period, when large US payment deficits exist, or to prevent a significant depreciation of the dollar

Trade Act of 1974, Section 301 Ability to take retaliatory actions (e.g., tariffs and quotas) against any country that violates or otherwise denies benefits under any trade agreement with the United States

Trade Expansion Act of 1962, Section 232(b)

Ability to take action (e.g., impose tariffs or quotas) against imports to mitigate a threat to or impairment of national security when the Secretary of Commerce finds certain imports to impose such a threat

Tariff Act of 1930, Section 338 Provides broad authority to raise tariffs and block imports in situations where the President determines that a foreign country has unfairly affected commerce in the United States.

Trading with the Enemy Act of 1917

Regulation of all forms of international commerce, including the power to freeze all kinds of foreign-owned assets, during a time of war

US trade war roadmap

Mexico Tariffs threatened ranging from 5% to 25%, but postponed for unknown time frame.

IndiaSpecial trade preference (GSP) removed.

Japan25% tariff threatened on autos and auto parts and emerging deal on agriculture.

CanadaDespite progress on the USMCA, the US and Canada have exchanged trade blows to each other, including retaliatory tariffs previously put in place by Canada.

IranVarious sanctions levied, including in 2018 for using funds from oil sales to support the Assad regime and terrorism.

VenezuelaSanctions related to human rights violations, anti democratic action, terrorism and drug-related activities.

RussiaVarious sanctions in place since March 2014 for violating the sovereignty and territorial integrity of Ukraine.

CubaVarious sanctions with recent additions in 2019 related to channel economic activities away from the Cuban military, intelligence, and security services

North KoreaVarious sanctions due to North Korea's nuclear weapons program.

Saudi Arabia / SudanVarious sanctions, including in 2018 related to the killing of Saudi journalist and Virginia resident Jamal Khashoggi.

Turkey & Crimean RegionSanctions imposed due to human rights violations, terminated preferential trade status, and imposed tariffs.

EURetaliatory US tariffs on certain products such as whiskey, motorcycles, and orange juice

UK / FranceIn response to the UK / France digital services tax, there is a chance that Trump may response with tariffs on UK / French products.

China - Tariff war in both directions

US tariffs: List 1 - 3 tariffs at 25% and may increase to 30% (Oct 1 date postponed for trade talks)

List 4A&B 15% partial tariffs Sept 1 and remainder Dec 15 at 15%

China retaliatory tariffs: 5 % and 10% on $75 billion of U.S. imports Sept 1 and remainder Dec 15

Unreliable Entities List - Watch for US Companies to be named

Trade-Con Level

PeaceWatchIncreased RiskTariffs ImminentTariffs Sanctions

54

123

US trade war roadmap

Volatility in US trade policy is causing a shift in focus to the issues of customs and trade

March 23, 2018Steel and aluminum tariffs go into effect with exemptions for selected countries

May 2018Trump administration goes to Beijing to begin bilateral trade talks; Chinese VP visits D.C. to continue discussions. Joint statement of an agreement reached released on May 19

June 1, 2018US ends steel and aluminum tariff exemptions for EU, Canada and Mexico

March 27, 2018Section 301 report on China released

April 3, 2018US released list of $50B of tariffs. China retaliates on April 4

July 6, 2018US implements 25% tariffs on $34B of Chinese products. China responds in kind on a dollar for dollar basis

August 3, 2017China announces they will impose tariffs of various rates on another $60B of US goods if US proceeds

July 10, 2018USTR released list on $200B of Chinese goods with 10% tariffs to implement

July 1, 2018Canada imposes tariffs on US products totaling $12.8B

August 7, 2018USTR publishes final list of Chinese imports hit with 10% tariffs; China announces retaliatory tariffs on August 8

August 23, 2018US and China imposed additional tariffs worth $16B, both at 25%

August 31, 2018The U.S. kicks off process to sign NAFTA 2.0 September 17, 2018

US moves forward with $200B at 10% (rather than 25% threatened)

September 30, 2018NAFTA negotiators strike a new deal: USMCA

May 10, 2019 September 24 $200B tariffs increase to 25%

September 24, 2018US $200B of tariffs go into effect at 10%

Sanctions:North Korea, Russia, Iran, Venezuela, Turkey, Saudi Arabia

May 13, 2019 USTR publishesList “4” proposing tariffs up to 25%on $300B

Aug. 1, 2019 President Trump announces 10% tariffs on broad range of China exports

% o

f GD

P

Source: OECD

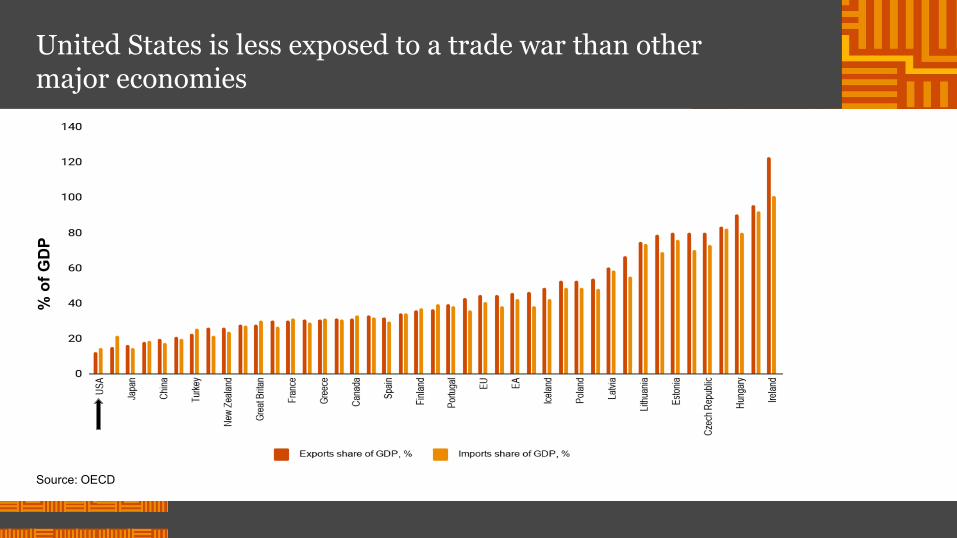

United States is less exposed to a trade war than other major economies

Practical Consideration

Tax Functions

PwC - San Paulo - December 2019|38

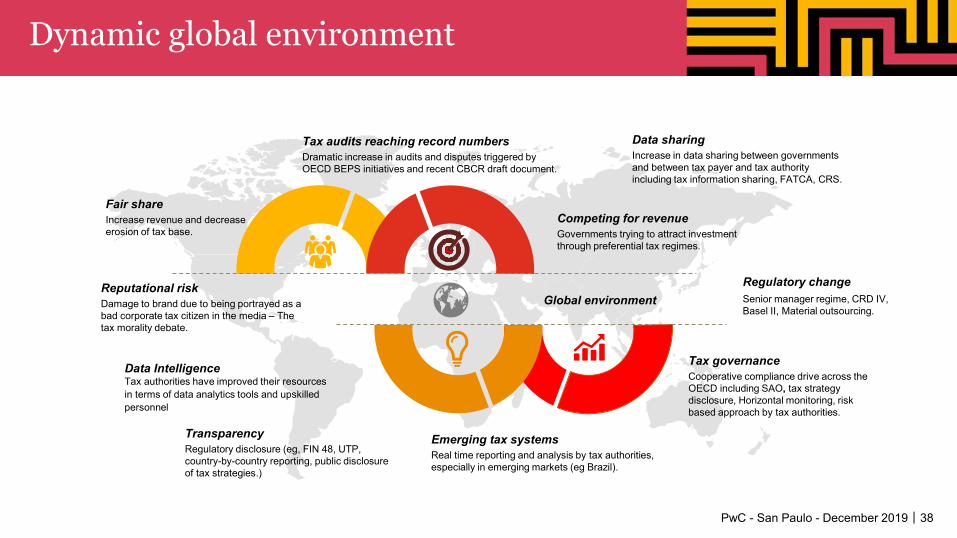

Dynamic global environment

Fair share Increase revenue and decrease erosion of tax base.

Tax audits reaching record numbersDramatic increase in audits and disputes triggered by OECD BEPS initiatives and recent CBCR draft document.

Data sharingIncrease in data sharing between governments and between tax payer and tax authority including tax information sharing, FATCA, CRS.

Competing for revenueGovernments trying to attract investment through preferential tax regimes.

Reputational riskDamage to brand due to being portrayed as a bad corporate tax citizen in the media – The tax morality debate.

TransparencyRegulatory disclosure (eg, FIN 48, UTP, country-by-country reporting, public disclosure of tax strategies.)

Emerging tax systemsReal time reporting and analysis by tax authorities, especially in emerging markets (eg Brazil).

Global environment

Tax governanceCooperative compliance drive across the OECD including SAO, tax strategy disclosure, Horizontal monitoring, risk based approach by tax authorities.

Regulatory changeSenior manager regime, CRD IV, Basel II, Material outsourcing.

Data IntelligenceTax authorities have improved their resources in terms of data analytics tools and upskilled personnel

PwC - San Paulo - December 2019|39

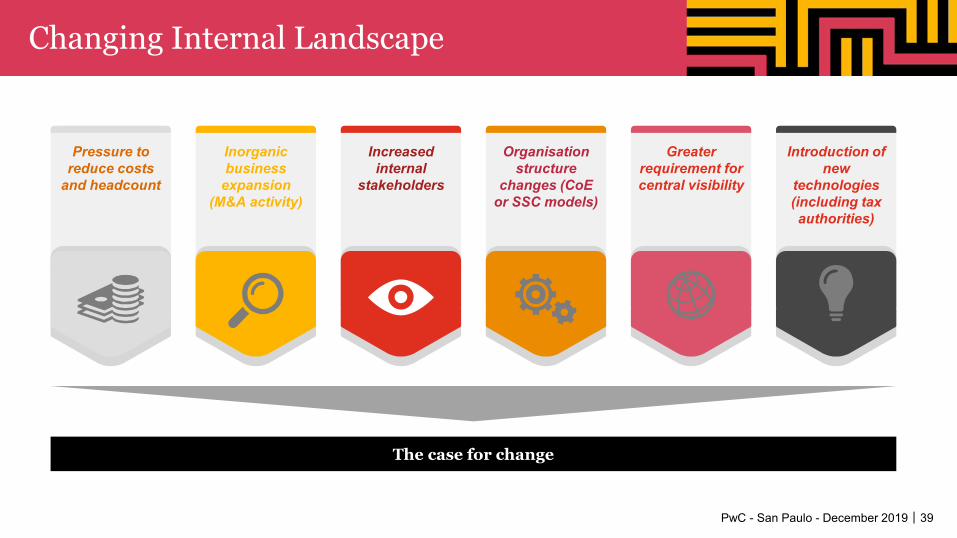

Changing Internal Landscape

The case for change

Pressure to reduce costs

and headcount

Inorganic business

expansion (M&A activity)

Increased internal

stakeholders

Organisation structure

changes (CoE or SSC models)

Greater requirement for central visibility

Introduction of new

technologies(including tax authorities)

PwC - San Paulo - December 2019|40

Leading tax functions are responding by…

Tax function of the Future

GovernanceEnhancing control frameworks. Real-time monitoring of tax risks.

Business partneringTime is spent on business partnering. Tax is seen as a value driver.

Process review and AutomationLeverage technology and data -refine and update processes to efficiently meet changing business strategies and priorities. End to end compliance automation is now achievable. Use of machine learning and AI to make tax judgements and decisions.

Tax function structure and sourcing modelsEffective tax structures to manage risk. Optimizing sourcing models, especially the trend of increased use of Shared Service Centers for tax and tax outsource providers, including Managed Tax Services

Managing an extensive people functionMaintain the right mix of expertise and leverage while balancing the challenges of recruiting, training and mobility

PwC |41

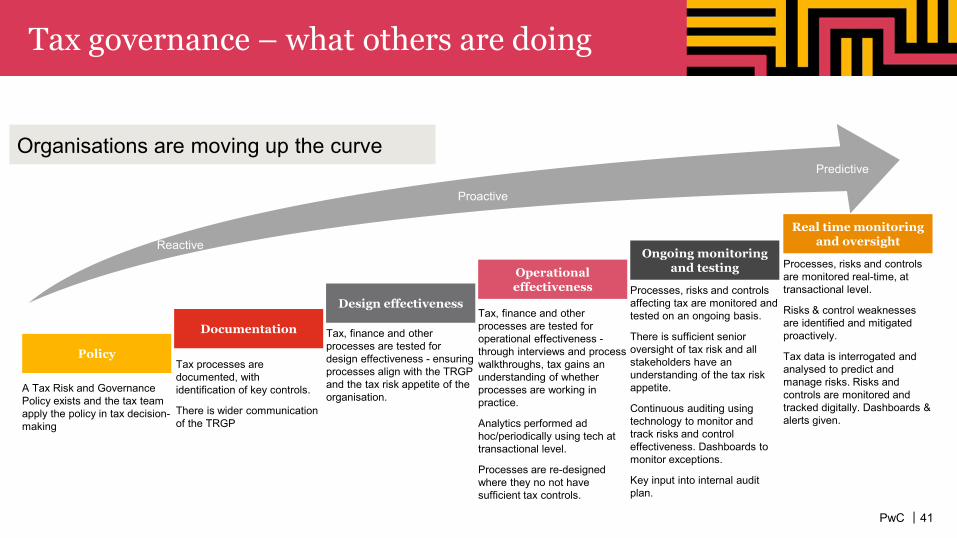

Tax governance – what others are doing

Policy

Documentation

Design effectiveness

Operational effectiveness

Ongoing monitoring and testing

A Tax Risk and Governance Policy exists and the tax team apply the policy in tax decision-making

Tax processes are documented, with identification of key controls.

There is wider communication of the TRGP

Tax, finance and other processes are tested for design effectiveness - ensuring processes align with the TRGP and the tax risk appetite of the organisation.

Tax, finance and other processes are tested for operational effectiveness -through interviews and process walkthroughs, tax gains an understanding of whether processes are working in practice.

Analytics performed ad hoc/periodically using tech at transactional level.

Processes are re-designed where they no not have sufficient tax controls.

Processes, risks and controls affecting tax are monitored and tested on an ongoing basis.

There is sufficient senior oversight of tax risk and all stakeholders have an understanding of the tax risk appetite.

Continuous auditing using technology to monitor and track risks and control effectiveness. Dashboards to monitor exceptions.

Key input into internal audit plan.

Organisations are moving up the curve

Real time monitoring and oversight

Processes, risks and controls are monitored real-time, at transactional level.

Risks & control weaknesses are identified and mitigated proactively.

Tax data is interrogated and analysed to predict and manage risks. Risks and controls are monitored and tracked digitally. Dashboards & alerts given.

Reactive

Proactive

Predictive