upmifa, ppa, and other letters a spelling bee for charitable funds november 9, 2007 ben blanton katy...

TRANSCRIPT

UPMIFA, PPA, and Other Letters

A Spelling Bee for Charitable Funds

November 9, 2007 Ben Blanton

Katy Ruhl© 2007 Baker & Daniels

2

Pension Protection Act of 2006 (“PPA”)

Reforming nation’s pension system Charitable contributions Tax-exempt organizations

3

Background

Code section 501(c)(3) exemption Private foundations

– Net Investment Income Tax– Self-dealing– Minimum Payout– Excess Business Holdings– Jeopardy Investments – Taxable Expenditures

4

Public Charities

Churches Schools, colleges and universities Nonprofit hospitals Fundraising organizations that benefit public

colleges and universities Governmental units Publicly supported charities Publicly operated charities Supporting organizations

5

Supporting Organizations

Type I - operated, supervised, or controlled by

Type II - supervised or controlled in connection with

Type III - operated in connection with

6

Charitable Reforms in PPA

Donor advised funds– Separately identified by reference to

contributions of one or more donors– Owned and controlled by a public charity (the

“sponsoring organization”)– Donor (or the donor’s appointee or designee)

has, or reasonably expects to have, advisory privileges with respect to the distribution or investment of funds

7

Exceptions– Sole designated beneficiary

Distributions only to one identified charitable organization or governmental entity

– Scholarship funds Committee, all of the members of which are

appointed by the sponsoring organization No donor, donor advisor, or related person

control Objective and nondiscriminatory procedure

Charitable Reforms in PPA (cont.)

8

Additional exceptions– Secretary of the Treasury exemptions if:

Committee not directly or indirectly controlled by the donor, donor advisor, or related persons, or

Fund benefits a single identified charitable purpose

Charitable Reforms in PPA (cont.)

9

Permitted and Prohibited Distributions

Permits distributions to –– Public charities– Sponsoring public charity– Donor advised funds– “Expenditure responsibility”

Prohibits distributions to –– Type III supporting organization (not “functionally

integrated”) – Entity controlled by donor, donor advisor, or related

party

10

Excess Benefit Transactions

“Excess benefit transaction” now includes: – Any payment from a donor advised fund to a

donor or the donor's appointee/designee, family members, and 35 percent-controlled entities Excess benefit is the entire payment

– Payments to investment advisors exceeding FMV

11

Reporting Requirements for Donor Advised Funds

Form 990– Total number of donor advised funds– Aggregate value– Aggregate contributions received and grants

paid

Form 1023– Intent to maintain donor advised funds

12

More Charitable Reforms

Supporting Organizations– Codification of Type I, Type II, and Type III

definitions– No donations to Type I and Type III

supporting organizations from persons who control supported organizations

– Minimum payout for Type III supporting organizations that are not “functionally integrated”

13

Excess Benefit Transactions

“Excess benefit transaction” by a supporting organization includes payments to a substantial contributor, family members, or 35 percent-controlled entities

Entire amounts constitute excess benefits Disqualified persons of supporting

organizations deemed disqualified persons of supported organizations

14

Private Foundation Payments No payments to Type III supporting organizations

that are not “functionally integrated” No payments to:

– Supporting organizations controlled (directly or indirectly) by disqualified persons

– Supporting organizations whose supported organizations are controlled (directly or indirectly) by disqualified persons

No payments if the Secretary determines them to be otherwise “inappropriate”

15

Reporting Requirements

$25,000 filing threshold does not apply to supporting organizations

Form 990 must: – Identify supported organizations– Indicate Type I, Type II, or Type III– Certify not controlled by “disqualified

persons”

16

UPMIFA

Uniform Prudent Management of Institutional Funds Act

Replaces UMIFA Addresses expenditure and retention of

assets in institutional and endowment funds

Effective July 1, 2007

17

How Does UPMIFA Update UMIFA?

Broader in application than UMIFA New and more flexible options with respect to

expenditures from endowment funds Introduces a new method through which an

institution may modify or release certain restrictions without court or donor approval

Specifies additional factors and circumstances that all charitable institutions should consider in making investment and management decisions

18

UMIFA vs. UPMIFA

UMIFA applied to:– Approved institutions of higher learning and their

related foundations,– Non-religious Code section 501(c)(3) organizations

with an endowment fund with a value of at least ten million dollars, and

– Community foundations or trusts,

…whose governing boards voluntarily and affirmatively had adopted UMIFA’s provisions

19

UMIFA vs. UPMIFA

UPMIFA– Applies more broadly to virtually all charitable

institutions, including private foundations, community foundations, religious entities, and other charities

– No requirement that an institution’s board of directors affirmatively adopt the law for it to apply

20

Endowment Fund – An institutional fund, or any part of an

institutional fund, that is not wholly expendable by the institution on a current basis under the terms of the applicable gift instrument

– Does not include assets that an institution voluntarily (i.e., not pursuant to a gift instrument) has designated as an endowment fund from which expenditures are limited

Background Definitions

21

Institutional Fund - A fund held by an institution exclusively for charitable purposes

Institution - Any entity that is organized and operated exclusively for charitable purposes

Background Definitions

22

Gift Instrument – Any record, including solicitations prepared

by the institution, under which property is granted or transferred to or held by an institution as an institutional fund

– A community foundation’s fund agreement with a donor should constitute a gift instrument under this definition

Background Definitions

23

Importance of Gift Instrument Provisions

Specific gift instrument language trumps UPMIFA spending provisions

UPMIFA: merely a default rule of construction where a donor has not given specific instructions to the contrary

24

Spending from Endowment Funds: The Rules under the Old UMIFA Statute

Permitted an institution to spend, from the amount of a fund that exceeded “historic dollar value,” as much as the governing board deemed prudent

Historic Dollar Value:– The amount originally donated– Any subsequent gifts to the fund– Any accumulation to the fund directed by the

gift instrument (or fund agreement)

25

Spending from Endowment Funds: The Current Rules under UPMIFA

Eliminates UMIFA’s historic dollar value approach

Permits an institution, subject to the terms of any applicable gift instrument, to “appropriate or accumulate so much of an endowment fund that the institution determines is prudent for the uses, benefits, purposes, and duration of the endowment fund”

26

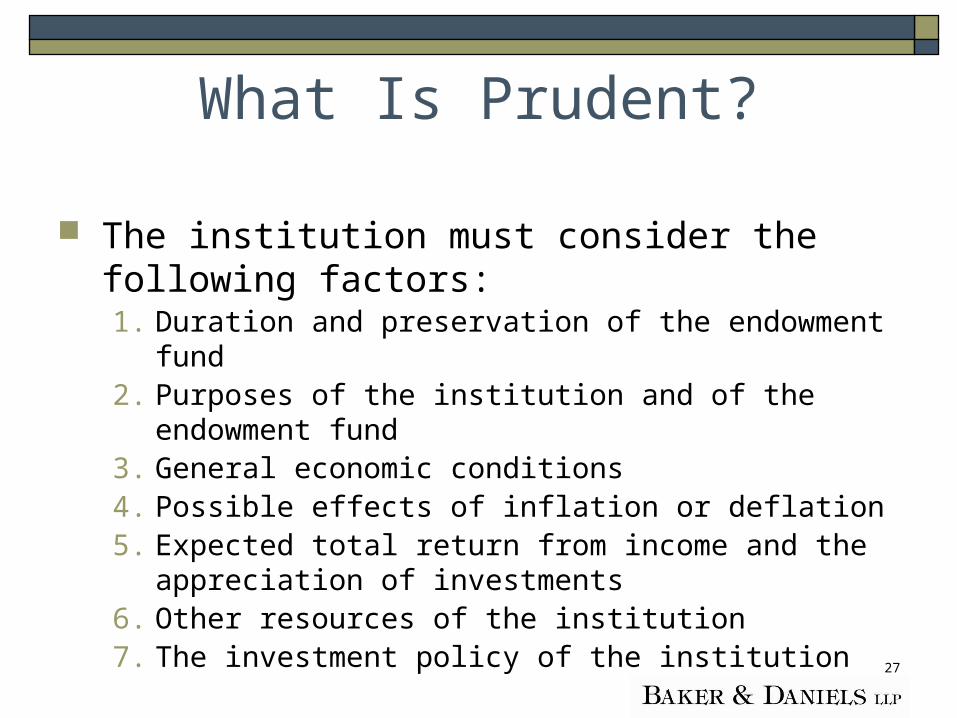

What Is Prudent?

The institution must act in good faith, with the care a prudent person acting in a like position would exercise under similar circumstances

27

What Is Prudent?

The institution must consider the following factors:1. Duration and preservation of the endowment fund2. Purposes of the institution and of the endowment fund3. General economic conditions4. Possible effects of inflation or deflation5. Expected total return from income and the

appreciation of investments6. Other resources of the institution7. The investment policy of the institution

28

Spending from Endowment Funds: Rules of Construction for Gift Agreements under UPMIFA

To override UPMIFA, the applicable gift instrument must specifically state a limitation on the institution’s authority to accumulate or appropriate the endowment fund

General language in the gift agreement that:– Designates the gift as an endowment– Directs the institution to use only income, interest,

dividends, rents, issues, or profits – Similarly directs the institution to protect the principal

...does not limit the authority of the institution to appropriate or accumulate the fund under the default provisions of UPMIFA

29

Release and Modification Rules

Written Consent from Donor Court Action New Modification/Release Provision

under UPMIFA

30

New Modification/Release Provision under UPMIFA

An institution may unilaterally release or modify a restriction in a gift instrument if: A. Restriction is unlawful, impracticable,

impossible, or wasteful;B. Value of the fund is less than $25,000;C. Fund is over twenty years old;D. Fund is used in a manner consistent with the

gift instrument; ANDE. Institution provides 60-day notice to the Indiana

Attorney General

31

Factors to consider in making decisions:1. Donor intent

2. Duty of loyalty

3. Good faith, with ordinary prudent care

4. Incur only reasonable costs

5. Reasonable effort to verify relevant facts

General – Investment and Management Provisions

32

Factors to consider in making decisions:6. Make investment and management decisions

in light of: General economic conditions Possible effects of inflation or deflation Possible tax consequences Role of each investment in relation to the overall investment

portfolio Expected total return Other resources of the institution Needs to make distributions and to preserve capital, and Relationship or value of an asset to charitable purposes

General – Investment and Management Provisions

33

Factors to consider in making decisions:7. Make decisions in the context of an overall

investment strategy

8. Diversify investments unless special circumstances exist

9. Dispose of unsuitable assets

10.Utilize any special skills or expertise possessed by the institution or managers

General – Investment and Management Provisions

34

Note: UPMIFA allows an institution to retain property contributed by a donor as long as the governing board of the institution considers it advisable to do so

General – Investment and Management Provisions

35

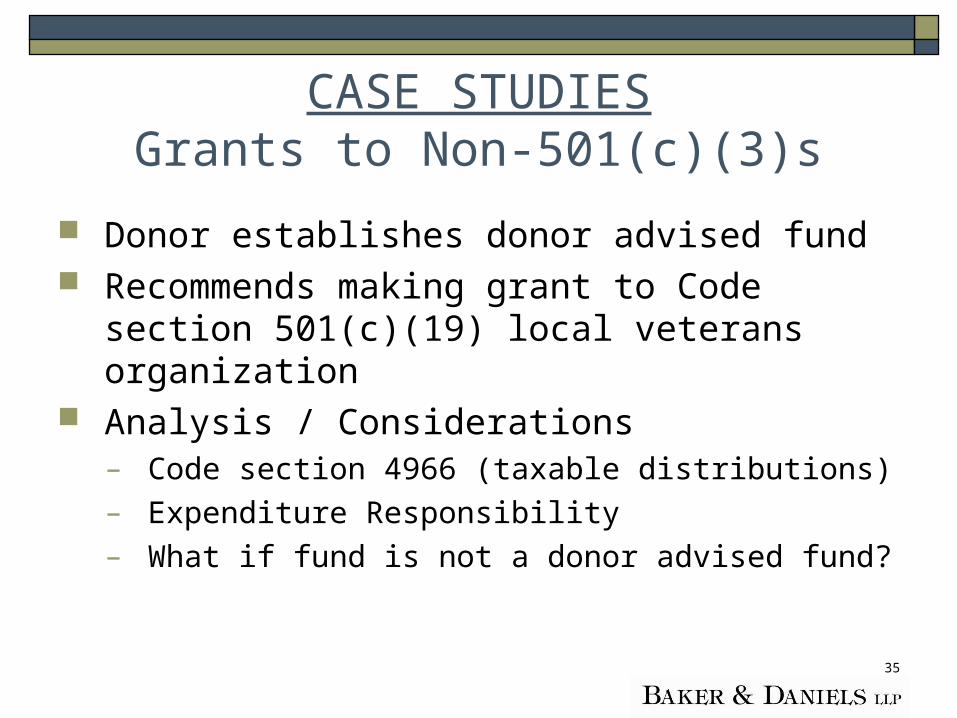

CASE STUDIESGrants to Non-501(c)(3)s

Donor establishes donor advised fund Recommends making grant to Code section

501(c)(19) local veterans organization Analysis / Considerations

– Code section 4966 (taxable distributions)– Expenditure Responsibility– What if fund is not a donor advised fund?

36

CASE STUDIESBroad Applicability of UPMIFA

Community foundation chose, several years ago, not to adopt UMIFA

Required actions / options re UPMIFA?– Board action required to adopt?– Ways to avoid applicability?

Analysis / Considerations

37

CASE STUDIESApplying UPMIFA to Old Fund Agreements

25-year-old endowment fund Fund agreement: “The original gift value must be

maintained” Analysis / Considerations

– Donor Intent (IC 30-2-12-9)– Donor Consent to Modify (IC 30-2-12-13(a))

Note: adding versus dropping restrictions at a donor’s request

– Court Petition (IC 30-2-12-13(c) and (d))– Unilateral Release / Modification (IC 30-2-12-13(e))

38

CASE STUDIESDesignated Funds

Donor establishing fund to benefit single charity Charity expected to take on large community

project Desire to make distributions for project

expenses, as well as directly to charity Analysis / Considerations

– Component part regulations for designated funds– Definition of DAF and exceptions – Taxable distributions from donor advised funds

39

CASE STUDIESCharitable IRA Distributions to Donor

Advised Funds

Elderly donor establishing donor advised fund Wants to take advantage of IRA provision of

PPA Analysis / Considerations

– 4 major requirements (age, qualified recipient, dollar limitation, expiration date)

– Note regarding pending legislation

40

CASE STUDIESReceipt of Investment Advice from Donors

Donor establishing fund to benefit single charity Donor requests particular investment advisor Analysis / Considerations

– Component part regulations Ultimate control by Board Ban on agreements establishing irrevocable relationships

re management, investment, etc. Board power to replace agent for breach of fiduciary duty Board power to replace agent for failure to produce

reasonable return

– Impact on DAF analysis? What if fund to be created were a field of interest rather than designated fund?

UPMIFA, PPA, and Other Letters

A Spelling Bee for Charitable Funds

November 9, 2007Ben BlantonKaty Ruhl

© 2007 Baker & Daniels