unlocking opportunities - pwc · unlocking opportunities perspectives on strategic and emerging...

TRANSCRIPT

Unlocking opportunitiesPerspectives on Strategic and Emerging Issues in Africa West Coast banking

www.pwc.com/za

February 2011

2 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Table of contents

Foreword 3

About the author 4

Introduction 5

Angola 17

Côte d’Ivoire 43

Democratic Republic of Congo 77

Ghana 115

Nigeria 147

Appendices 177

Contacts 189

PwC 3

I would like to thank:

• the Chief Executive Officers and Senior Executives who participated in this survey for their time, commitment and support in making this publication possible;

• the partners and staff in our offices on the West Coast of Africa and our Johannesburg office who have assisted in producing this report; and

• in particular, Dr Brian Metcalfe for his work in producing this report.

We trust that you will find the results and analysis insightful and we welcome any feedback you may have on the report so that we can incorporate it into future PwC surveys.

Tom Winterboer

Financial Services Leader: Southern Africa and Africa

February 2011

Foreword

We are pleased to launch this PwC survey of mainly the banking industry on the West Coast of Africa with references to the insurance markets in certain countries. The survey attempts to gather and compare diverse views from senior banking executives from banking institutions in Angola, Democratic Republic of Congo (DRC), Cote d’Ivoire, Ghana and Nigeria, whilst at the same time protecting confidentiality of the participants. As in our South African Banking and Insurance surveys, this survey offers perspectives on the strategic and emerging issues in these territories.

This survey has been developed by PwC and Dr Brian Metcalfe and the key objectives are to:

• offer perspectives on certain strategic and emerging issues in Africa West Coast Banking;

• establish data on certain industry trends;

• encourage timely discussion and debate on the best options for capitalising on trends to enhance and improve performance of the various banks; and

• provide perspectives on how Africa West Coast Banking could evolve over the next three years.

4 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

About the author

Dr Brian Metcalfe is an Associate Professor in the Business School at Brock University, Ontario, Canada. He has a doctorate in financial services marketing and has researched and produced over 40 reports, such as this one, on behalf of PwC firms in 11 different countries including Australia, Canada, China, India, a number of African countries(2007) and South Africa.

Previous reports in South Africa have examined strategic and emerging issues in banking, short and long-term insurance, insurance broking and wealth management.

He has consulted for a wide range of organisations, including Royal Bank of Canada, Bank of Nova Scotia, Barclays Bank, Sun Life Insurance Company, Equitable Life of Canada, and several major consulting firms.

He has also taught an executive management course entitled ‘Financial Services Marketing’ at the Graduate School of Business, University of Cape Town.

This report was researched and written by Dr Brian Metcalfe, Ph.D. Information presented herein, while obtained from sources believed reliable, is not guaranteed as to accuracy or completeness. This report has been commissioned by and distributed through PwC, Johannesburg.

Additional copies of this report can be obtained from Tom Winterboer, Financial Services Leader: Southern Africa and Africa – PwC, 2 Eglin Road, Sunninghill, 2157.

Telephone: +27 11 797 5407 Fax: +27 11 209 5407 E-mail: [email protected]

© 2011 PricewaterhouseCoopers (“PwC”), a South African firm, PwC is part of the PricewaterhouseCoopers International Limited (“PwCIL”) network that consists of separate and independent legal entities that do not act as agents of PwCIL or any other member firm, nor is PwCIL or the separate firms responsible or liable for the acts or omissions of each other in any way. No portion of this document may be reproduced by any process without the written permission of PwC.

PwC 5

Introduction

Introduction

6 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Introduction

“Scepticism about Africa is waning, says African Development Bank (ADB) president Donald Kaberuka.

He points to the high growth figures predicted for the continent - 5% this year and up to 6% next year - as proof that real change is happening.

This growth is not only about resources, he maintains. “Something has happened since 2000 that is not simply explained by the price of raw materials. That is maybe 30% of the momentum - the rest is accounted for by fundamental reforms taking place at the macroeconomic level.”Source: Business Day November 2010

PwC 7

Introduction

The following findings are based on interviews with a sample of banks in five financial markets in West and Central Africa.

The report examines the five markets in separate sections. In this introductory section, some of the common themes and major differences are highlighted. This sets the scene for the more detailed analysis that follows.

To place the five different markets in a broader African context, the four segment economic model devised by McKinsey has been used.

This model classified countries according to their level of diversification and exports per capita. Examination of past economic development has found that as countries develop they migrate along both of these axiis. Africa has 53 different countries and the growth prospects will vary for individual countries. The evolution of the financial sector in these countries will mirror their respective stages of economic development. The five banking markets documented in this report fall into different development segments.

Pre-transition segment

The Democratic Republic of Congo (DRC) can be positioned in the pre-transition stage. The pre-transition economies are very poor. Although some markets such as DRC which stagnated in the 1990s, have since grown very rapidly. In the pre-transition stage international development agencies often play an important role in trying to put in place economic fundamentals.

The DRC’s banking industry is therefore at a very early stage of development.

Oil exporter segment

The oil exporter segment is characterised by strong exports per capita but weak levels of diversification. This segment contains two of the report’s participants, Angola and Nigeria.

Both markets have benefited from oil but also suffered from the global financial crisis and the subsequent drop in commodity prices. Oil revenues have had far reaching influences on these countries’ banking structures. For example, in Angola Sonangol, the state owned oil company, has shareholdings in six banks. Sonangol is the largest shareholder in Banco Africano de Investimentos the country’s largest bank.

In Nigeria the drop in oil revenues and the lack of loan diversification opportunities in the broader economy have been cited as a major cause of the recent banking crisis.

The Nigerian economy was unable to absorb the excess liquidity that flowed into the capital markets. As a result, the market capitalisation of the NSE increased 5.3 times between 2004 and 2007, while bank stocks increased 9 times. These dramatic increases set the stage for the resultant market crash.

The five banking markets and their level of economic development

8 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Introduction

Transition segment

The third segment includes economies in transition and are characterised by rapidly growing economies. Ghana fits into this group and is also well endowed with natural resources. Gold and cocoa are traditional exports and as of December 2010 oil will support export earnings. It is expected that oil will contribute an annual average of US$1.2 billion to state revenues over the next twenty years. The banking sector which is already relatively advanced can be expected to benefit as the economy diversifies and develops.

Diversified segment

Only one country reviewed in this report can be placed in the diversified group. Cote d’Ivoire is positioned on the periphery of this segment and the on-going political instability there will affect its economic progress.

However, it is important to recognise that Cote d’Ivoire has a relatively sophisticated infrastructure and is not only a significant exporter of coffee and palm oil but is also the world’s largest producer of cocoa beans.

Exhibit 3

Zambia

Uganda

Tunisia

Tanzania

Sudan

South Africa

Sierra Leone

Senegal

Rwanda

Namibia

Mozambique

Morocco

Mauritius

Mali

90

Libya

Kenya

Gabon

Ethiopia

EquatorialGuinea

EgyptCongo, Rep.

Chad

Exports per capita, 2008, $

10000

1000

100

10

Economic diversificationManufacturing and service sector share of GDP, 2008, %

8070605040

Madagascar

3020 100

Cameroon

BotswanaAlgeria

DiversifiedOil exporters

Transition

Pre-transition

Size of bubble proportional to GDP $500–1,000

$1,000–2,000

$2,000–5,000

>$5,000

<$500

GDP per capita

DRC

Nigeria

Angola

Cote d’Ivoire

Ghana

22 countries that account for less than 3% of African GDP in 2008 are not shown in this figure.

Source: McKinsey Global Institute using OECD and World Bank Development Indicators

PwC 9

Introduction

Participating banks (28 banks)

Angola

• Banco Africano de Investimentos(BAI)

• Banco Caixa Geral Totta Angola1

• Banco Comercial do Huambo

• Banco de Fomento Angola2

• Banco Millenium Angola3

• Standard Bank Angola4

Cote d’Ivoire

• Société Générale de Banques enCôte d’Ivoire (SGBCI)5

• Banque Atlantique Côte d’Ivoire(BACI) 6

• Société Ivoirienne de Banque(SIB)7

• Ecobank Côte d’Ivoire 6

• Banque Nationale d’Investissement(BNI)

• Diamond Bank**

Democratic Republic of Congo

• Advans Banque

• Banque Commerciale du Congo(BCDC)

• Citigroup

• ProCrédit Bank Congo

• Rawbank

• Stanbic Bank Congo 4

Ghana

• Barclays Bank of Ghana

• Ecobank Ghana 6

• Ghana Commercial Bank

• HFC Bank

• Stanbic Bank Ghana 4

Nigeria

• Citibank Nigeria

• Standard Chartered Bank Nigeria

• Standard Bank IBTC 4

• Ecobank 6

• HSBC

1 51% owned by Santander Totta and Geral de Depositos 2 Major shareholder Portuguese Bank BPI 3 Major shareholder Portuguese Bank BCP 4 Standard Bank of South Africa 5 Société Générale France 6 HQ in Togo 7 Part of Attijariwafa Bank based in Morocco 8 Diamond Bank based in Nigeria

10 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Introduction

Summary of the major drivers of change by market

It is readily acknowledged that all five markets examined are embracing massive changes in their financial sectors.

Two important themes were found across the markets, the ongoing performance of the domestic economy and the application of regulation and reporting in the respective countries.

The most important drivers of change in each market is recorded below:

• Angola - liquidity

• Cote d’Ivoire - demographics

• DRC - new foreign entrants

• Ghana - regulation and reporting

• Nigeria - mergers andconsolidation

Angola Cote d’Ivoire

DRC Ghana Nigeria

Capital markets 2

Demographics 1

Fiscal pressures 3

Foreign entrants 1 2

Foreign exchange control 2 3

Funding constraints 3

Governance 2

Liquidity 1

Mergers/Consolidation 1

Money laundering 2

Performance of domestic economy 1 3 2

Recession 3

Regulation and reporting 1 3

Technology 3 2

PwC 11

Introduction

Summary of the most pressing issues/major concernes by market

Angola • Availability of key skills

• Credit risk management

• Risk management

Cote d’Ivoire

• Risk management

• Credit risk management

• Retaining existing customers

• Banking the previously unbanked

• Improving revenue growth

DRC • Availability of key skills

• Banking the previously unbanked

• Business continuity

• Currency fluctuations

• Improving revenue growth

• Litigation risk

• Tax legislation

Ghana • Brand awareness

• Credit risk management

• Margins

• Risk management

• Service quality

• Improving revenue growth

Nigeria • The true health of banks’ loan portfolios

• Central bank resources

• Ability to sell all failed banks

• The stability of the Nigerian stock market

Individual factors that are mentioned more than three times are shown in bold

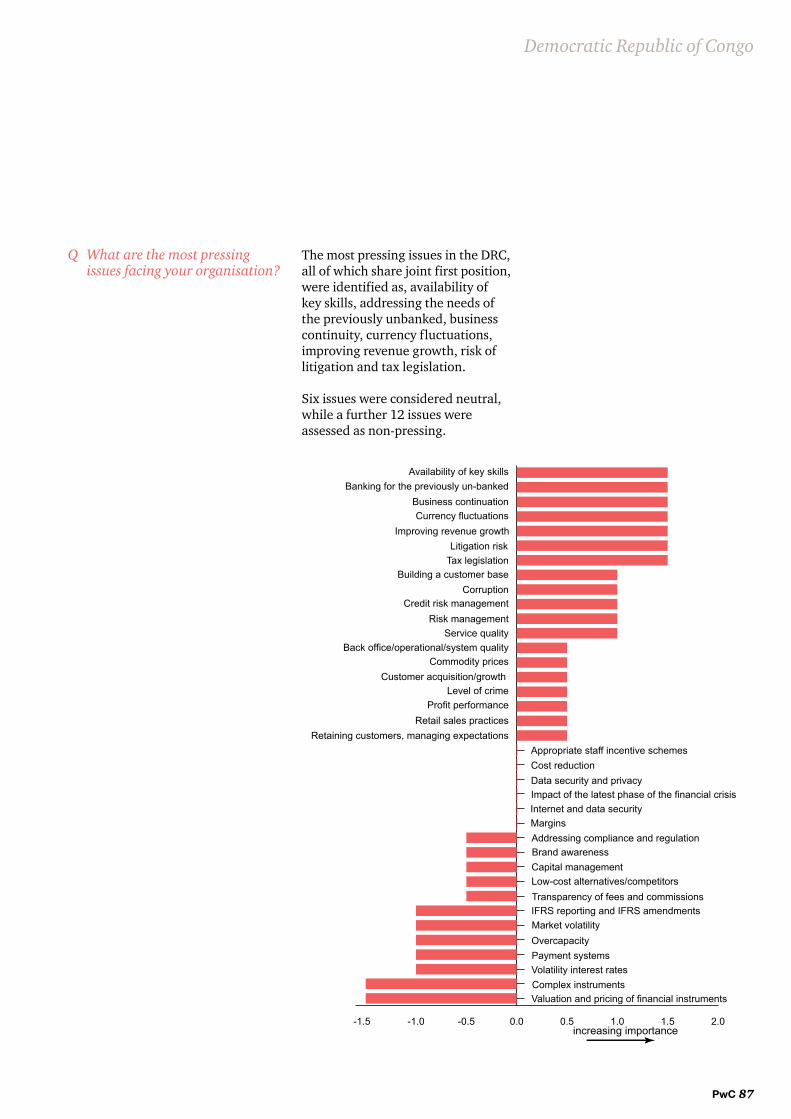

The following table provides a summary of the issues that are at the forefront of the minds of the bankers interviewed in this survey.

Three issues are repeated on at least three occasions. They are credit risk management, risk management and improving revenue growth.

In Angola, Cote d’Ivoire and Ghana risk management is a critical issue.

In DRC, it is subservient to other issues such as a skill shortages, business continuity, banking the unbanked, currency fluctuations and improving revenue growth.

12 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Introduction

Summary of major skill shortages by market

There is a widespread shortage of skills in the banking industry in the markets surveyed.

Two skill deficits received particular attention, capital management and risk management.

Other skill shortages have more specific relevance in individual markets.

For example, all types of risk in the DRC, compliance in Ghana and Nigeria, executive directors in Cote d’Ivoire and Ghana and non-executive directors in DRC.

Angola Cote d’Ivoire

DRC Ghana Nigeria

Administration 5 6 4 7 4

Audit committee 4 3 4 6 4

Capital management 1 5 5 2 2

Compliance 3 3 4 3 2

Credit risk 1

Executive directors 2 2 3 3 3

Financial reporting 1 5 5 5 3

Information technology (IT) 2 3 6 5 3

Internal audit 4 5 4 7 4

Liquidity / ALM 1

Market risk 1

Non-executive directors 6 4 1 4 5

Operational risk 1

Regulatory risk (e.g. Basel) 1

Risk management 1 1 2 1 1

PwC 13

Introduction

Summary of major changes by market

Angola • Impact of the global economic crisis and the drop in oil prices

• Increasing competition

• Improvements in bank supervision

• Movement away from a dollarised economy to local currency

• Anti-money laundering legislation

• Creation of a credit bureau

Cote d’Ivoire

• Increasing competition

• Hiring pressures, skill shortages

• Development of the credit card market

• The “National Crisis”

• Regulation and an increase in bank capital requirements

• Technology electronic payments, ATMs and mobile banking

DRC • New bank entrants

• Growing confidence in the banking sector

• Introduction of new technology

• Growth in number of SMEs

Ghana • Creation of a credit bureau

• Creation of a collateral registry

• Increase in bank capital requirements

• Increased threat of competition from the telecom sector

• Pressure to reduce high levels of interest rates

Nigeria • New banking guidelines set out by the Central Bank

• Recapitalisation of the banks

• Creation of AMCON (Asset Management Agency)

• The dismissal by the Central Bank of the CEOs of one third of the country’s

24 banks

The table below summarises the major changes highlighted by the participants. They display some common themes such as: increasing levels of competition (Angola and Cote d’Ivoire), new technologies (Cote d’Ivoire, DRC and Ghana), new bank capital requirements (Cote d’Ivoire, Ghana and Nigeria) and credit bureau formations (Angola and Ghana).

In addition there are some changes that are more specific to particular markets such as oil and Angola, bank market restructuring and Nigeria, new bank entrants and DRC and the political environment and Cote d’Ivoire.

14 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Introduction

Angola Cote d’Ivoire

DRC Ghana Nigeria

Retail banking

asset based financing a a

asset management a

cards a

consumer loans a a

credit cards a a

debit cards a a

electronic payments (both debit

and credit)a

internet banking a

leasing a

mobile banking a a a

mortgages a a a

pre-paid cards a

residential mortgages a

savings products a a

Corporate banking

asset management a

capital markets a a

cash management a a

corporate bond offerings a

debt markets a

derivatives a

financial advisory services a

fixed income products at the

government levela

foreign exchange a

infrastructure financing a

investment banking a

leasing a

project finance a

trade finance a a a a

treasury products a

Summary of products that will become more important over the next three years in each market

The participants shared their views on both retail and corporate products that they believe will increase in importance over the next three years.On the retail side, mobile banking featured strongly. Debit cards are important and there will be an increase in the issuance of credit cards. As the middle class grows in the markets examined, mortgages and asset based financing will expand.

On the corporate side, cash management as well as trade finance will grow rapidly and capital markets will play a more important role. Capital markets are expected to develop in Cote d’Ivoire and Angola and increase in their scope and sophistication in the most advanced market examined in the report - Nigeria. Project financing received a mention in Ghana and infrastructure financing was thought to be of critical importance in Nigeria.

PwC 15

Introduction

The Banker Tier 1 Capital

World Rank

Date Tier 1 Capital US$m

Assets US$m

a. Nigeria First Bank of Nigeria 285 3/09 2,277 13,658

Zenith Bank 287 12/09 2,270 11,202

Guaranty Trust Bank 429 12/09 1,298 7,198

Access Bank 438 3/09 1,247 4,827

United Bank for Africa 482 12/09 1,115 10,450

Date Capital US$m

Assets US$m

b. Angola Banco Africano de Investimentos na 12/09 637 8,288

Banco Espírito Santo Angola. na 12/09 400 6,494

Banco de Fomento Angola na 12/09 556 5,930

Banco de Poupança e Crédito na 12/09 526 5,200

Banco BIC na 12/09 461 4,329

c. Cote d’Ivoire Societe Generale de Banques na 12/09 32 1347

Ecobank na 12/09 28 698

Banque Internationale pour

l’Afrique Occidentale

na 12/09 41 661

Banque Internationale pour Ie

Commerce et l’lndustrie

na 12/09 34 661

Banque Nationale

d’investissement

na 12/09 42 502

d. DRC Rawbank na 12/09 32 308

Banque Commerciale du Congo na 12/09 30 300

Banque Congolaise na 12/09 40 263

Banque Internationale pour

l’Afrique au Congo

na 12/09 14 223

Trust Merchant Bank na 12/09 35 185

e. Ghana Ghana Commercial Bank na 12/09 49.6 1,242

Barclays Bank of Ghana na 12/09 79.3 904

Standard Chartered Bank Ghana na 12/09 42 899

Ecobank Ghana na 12/09 69 870

Stanbic Bank Ghana na 12/09 43 473

a: The Banker July 2010 b: fxtop.com c: Refer to page 55 d: Refer to page 82 e: Refer to page 120

Comparison of banking statistics

16 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Introduction

The Banker Tier 1 Capital World Rank

Date Tier 1 Capital US$m

Assets US$m

France BNP Paribas 8 12/09 90,648 2,964,983

Credit Agricole Group 13 12/09 75,504 2,440,634

Group BPCE 18 12/09 54,141 1,482,424

Societe Generale 19 12/09 49,990 1,475,073

Credit Mutuel 29 12/09 39,595 834,349

Portugal Millenium bcp 112 12/09 8,793 137,681

Caixa Geral de Depositos 113 12/09 8,699 174,330

Banco Espirito Santo Group 123 12/09 7,794 118,584

Banco Santander Totta F 12/09 4,174 70,014

Banco BPI 211 12/09 3,235 68,371

South Africa Standard Bank Group 106 12/09 9,562 182,260

ABSA Group F 12/09 6,636 97,255

FirstRand Bank 158 6/09 5,285 82,550

Nedbank Group 181 12/09 4,253 77,331

Investec 212 3/09 3,207 48,263

UK Royal Bank of Scotland 4 12/09 123,859 2,749,572

HSBC 5 12/09 122,157 2,364,452

Barclays 10 12/09 80,449 2,234,893

Lloyds Banking Group 12 12/09 77,034 1,664,919

Standard Chartered 42 12/09 24,582 436,653

US Bank of America 1 12/09 160,388 2,223,299

JPMorgan Chase 2 12/09 132,971 2,031,989

Citigroup 3 12/09 127,034 1,856,646

Wells Fargo 6 12/09 93,795 1,243,646

Goldman Sachs 16 12/09 64,642 848,942

Source: The Banker July 2010

Comparison of banking statistics (continued)

PwC 17

Angola

Banks interviewed:

• Banco Africano de Investimentos(BAI)

• Banco Caixa Totta Angola

• Banco Comercial do Huambo

• Banco de Fomento Angola (BFA)

• Banco Millennium Angola

• Standard Bank

Angola

18 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

The economy in general

Angola became independent from Portugal in 1975. From the founding of the state Angola was engulfed in a civil war between three factions, the Popular Movement for the Liberation of Angola (MPLA), the National Front for the Liberation of Angola (FNLA) and the National Union for Total Independence of Angola (UNITA).

In 1991 the Bicessa Accord led to a ceasefire between MPLA and UNITA and a national election. Although the MPLA won a plurality of the vote UNITA rejected the result and civil war returned. In 1994, the Lusaka Protocol led to a new ceasefire but fighting between various factions continued until 2002. It has been estimated that 1.5 million people died in the civil wars and 4 million people were displaced. President Jose Eduardo dos Santos has been in power for 19 years and elections are scheduled for 2012.

Angola is estimated by the World Bank to have a population of 18.5 million. In 2009 its life expectancy was 38.48 years. In 2009 it had an estimated GDP per capita of US$8,300.

Oil accounts for over 90% of Angola’s exports. Angola is China’s most important supplier of oil. According to the Economist oil production stands at 1.9 million barrels making Angola sub-Saharan Africa’s second largest producer after Nigeria. Oil accounts for more than half of Angola’s GDP, 80% of government revenues and 90% of export earnings. Sonangol, the state oil company, has an equity stake in a number of banks (see table).

The second largest export is diamonds. Endiama is the state-owned diamond company.

Angola’s GDP growth between 2004 and 2008 averaged above 10% per annum with a record high of 20% in 2005. However, the global financial crisis and the drop in the price of oil at the time caused the economy to stall and record 0.7% growth in 2009 and approximately 5% in 2010.

Financial institutions

A modernisation project (1992-2003) helped Angola move away from the state-controlled financial system. The banking and insurance sectors were liberalised and new regulatory and supervisory systems were introduced. Prior to liberalisation, Angola had two state-owned banks, Banco Nacional de Angola which is now the Central Bank and Banco de Poupança e Crédito (BPC).

Insurance

The insurance sector has begun to open up with the assistance of the World Bank. In 2003, the state-owned insurance company ENSA was restructured into three companies, a holding company, an insurance company (SARL) and a reinsurance company Ango-Re.

Stock market (BVDA)

Although a financial markets law was passed and it was hoped that a stock market would open in 2006, this date continues to slip. In March 2010, the former Finance Minister suggested it would be launched in 2010 but this failed to take place. The chairman of the Capital Market Installing Commission, said in 2010 that arrangements to set up the Bolsa de Valores e derivativos de Angola (BVDA) are far advanced.

General background on Angola

Angola

PwC 19

However in January 2011 Angop, the state news agency, announced that because of “the commercial, business and legal situation,” the Angola exchange would not open in 2011.

The brokerage firm IMARA Angola has predicted that the Angola exchange will become the third largest in sub-Saharan Africa after South Africa and Nigeria. IMARA estimates there could be 14 IPO candidates when the market opens. This number might include up to 10 banks. One bank that has stated publicly that it would list on the BVDA is Banco Espirito Santo de Angola (BESA). Banco Espirito Santo of Portugal is the largest shareholder of BESA with a 52% holding. This is unusual relative to the other Portuguese banks in Angola which now are either owned by Angolan shareholders or the state-owned oil company Sonangol.

Infrastructure rebuild

The government has begun reconstruction of much of the infrastructure that was destroyed during the civil war. Financial support for new infrastructure has been provided in most instances by China through the Chinese Exim Bank and the China International Fund.

Before the civil war, agriculture was the mainstay of the economy. The country was largely self-sufficient and exported coffee, sugar cane, bananas and cotton. Today Angola is a major food importer.

The government has a strategy to lift agriculture production. One example of this is the U$1 billion Capanda Agro-Industrial Pole (Malanga Province) where a consortium of Angolan and Brazilian companies plan to produce sugar and electricity.

African Economic Outlook has summarised its assessment of Angola as follows:

“Angola’s main challenges are to manage its non-renewable national wealth more efficiently, and create jobs. Better management will require strengthening institutions and relaxing the tight grip of power, both political and economic, by the country’s leadership. Angola’s economy remains largely driven by public investment, which is marred by political patronage and corruption. Over the medium term, Angola’s economy will need to rely less on public investment and more on private sector activity.”

Source: www.AfricanEconomicOutlook.org

Angola

20 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

The Angolan banking system is dominated by five banks, which together control about 80% of deposits and lending. These banks are:

• Banco Africano de Investimentos(BAI)

• Banco Espirito Santo Angola(BESA)

• Banco de Fomento Angola (BFA)

• Banco de Poupanca e Credito(BPC)

• Banco BIC.

Between December 2008 and 2009, domestic deposits rose by 23.6% and credit by 35.2%. This contrasted dramatically with the 2008 increases of 92% in deposits and 140% in credit.

Three Angolan banks have subsidiaries in Portugal – BAI, BIC and Banco Privado Atlântico.

BAI offers customers Platinum, Gold and Classic credit cards. According to its 2009 Annual Report, 3,583 cards were issued..

In 2010 Novo Banco was renamed BAI Micro Financas (BMF). BAI is the main shareholder holding 92.93% while Chevron Sustainable Development owns 7.07%. BMF has eight branches and offers Western Union services.

31 December 2009 US$m* Equity mAOA

%

**Banco Millenium BCP 5,534 512,308 9,96%

Banco Caixa Geral Totta Angola 244 22,630 24,00%

Banco Millenium Angola 193 17,838 29,90%

Banco Privado Atlantico 41 3,816 9,50%

**Banco Privâdo Atlantico - Europa 19 1,796 20,00%

Bolsa de Valores e Derivados de Angola (BVDA) 13 1,221 29,71%

Shareholdings of Sonangol (the national oil company) in Associated Banks and Financial Companies

Source: SONANGOL Annual Report 2009

The Top FiveMarket share by assets 2009

Others

BIC

BPC

BFA

BESA

BAI

21.9%

17.2%

15.7%13.8%

19.9%

11.5%

* 1US$ = 92.5757 AOA 31/12/2010 exchangerate.com ** Portuguese banks

December 2009 September 2010 Increase

Total deposits 2,603,550 2,815,124 8.1%

(% in local currency) (49%) (50%)

Total credit 2,241,166 2,420,366 8%

(% short term) (62%) (63%)

Banking system (Volume of Deposits and Credit) mAOA

Angola

PwC 21

Bank Date Formed

Total Assets 31 Dec 2009 mAOA

Total Assets 31 Dec 2009 US$ m*

Banco Africano de Investimentos 1996 739,063 7,983

Banco Espírito Santo Angola 2002 579,059 6,255

Banco de Fomento Angola 1993 528,802 5,712

Banco de Poupança e Crédito 1976 463,665 5,008

Banco BIC 2005 386,013 4,170

Banco Privado Atlântico 2006 136,885 1,479

Banco de Negócios Internacional 2006 106,788 1,154

Banco Sol 2001 103,650 1,120

Banco Millennium Angola 1993 95,725 1,034

Banco de Comércio e Indústria 1991 77,581 838

Banco Caixa Geral Totta Angola 1993 68,673 742

Banco Regional do Keve 2003 37,442 404

Banco Comercial Angolano 1999 21,924 237

Finibanco Angola 2008 8,881 96

Banco Angolano de Negócios e Comércio 2007 8,795 95

Banco BAI Micro Finanças 2004 4,693 51

VTB Angola 2007 ** **

Banco Quantum Angola 2008 ** **

Banco Comercial do Huambo 2010 ** **

Standard Bank Angola 2010 ** **

** Data not yet available

Banks in Angola ranked by total assets

Extract from two speeches made by BNA Governor Jose Lima Massano at the end of 2010 and displayed on the BNA website

* 1US$ = 92.5757 AOA 31/12/2010 exchangerate.com

The percentage of the population served by the banks remains low and is estimated at 11%. The level of financial education also needs to increase. We seek to develop a banking system that is financially sound and socially responsible. By the end of 2012 we would like to see banking initiatives in all the cities and the number of branches close to one thousand. (There are currently 875 branches). By 2013 we would like to see the banks serving 20% of the population.

Extract from a speech made by BNA Governor Jose Lima Massano at the ABANC forum to 24 November, 2010 displayed on the BNA website

In the field of banking supervision the Governor noted the continued modernisation of inspection services and the implementation of standards of good governance.

A Financial Intelligence Unit has been created by the BNA to analyse, prevent and detect attempts to use the financial system for money laundering and terrorist financing. It is expected to begin operations in the first quarter of 2011

The soundness of the financial system will also benefit from the Banking Consolidation Programme which will strengthen the capital structure of banks and adopt

prudential standards in line with international best practices for the financial industry.

Consumer financial services also will be strengthened in 2011 with the introduction of a unit dedicated to the recording and tracking of consumer complaints.

Extract from a speech made by BNA Governor Jose Lima Massano at the end of year 2010 displayed on the BNA website

Angola

22 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Bank Initials

Banco Africano de Investimentos BAI Founded in 1996, it's the largest bank in Angola (considering total assets, credit,

deposits and capital). BAI is also present in Portugal, through BAI Europa, in Cape Verde,

through BAI Capo Verde and in Sao Tomé e Príncipe.

Banco Espírito Santo Angola BESA Founded in 2002, the major shareholder is the Portuguese bank, BES (Banco Espírito

Santo). It's currently present in 10 provinces in Angola.

Banco de Fomento Angola BFA Founded in 1993, it's the second-largest Angolan private bank (deposits and capital).

The major shareholder is the Portuguese bank BPI (Banco Português de Investimento).

Banco de Poupança e Crédito BPC Government-owned bank (99% by the Angolan state). It has one of the largest number of

clients and is the second-largest bank in Angola based on credit.

Banco BIC BIC Founded in 2005, major shareholders include Portuguese Amorim Holding Financeira

SGPS. It's the fourth largest bank in Angolan (both credit and deposits).

Banco Privado Atlântico BPA Angolan shareholder structure. Founded in 2006. Provides investment banking services.

Ranked third in 2009 regarding ROAE (48%).

Banco de Negócios Internacional BNI Private Angolan shareholder structure, founded in 2006. Provides personal credit and

investment banking services.

Banco Sol Sol Founded in 2001 to provide micro-finance.

Banco Millennium Angola. BMA Founded in 1993. The major shareholder is the Portuguese bank Banco Millennium BCP.

It has experienced solid growth from 2006.

Banco de Comércio e Indústria BCI Founded in 1991. Recently privatised.

Banco Caixa Geral Totta Angola BCGTA Major shareholders are the Portuguese bank Caixa Geral de Depósitos, and Santander

Totta. Has the best cost to income ratio in the sector in 2009.

Banco Regional do Keve Keve The bank is a private capital institution founded in 2003. It also provides insurance

services through the Global – Companhia de Seguros, of whom the bank is the largest

shareholder.

Banco Comercial Angolano BCA Founded in 1999. BCA is a privately owned bank based in Luanda whose shareholding

structure is held locally; ABSA no longer has a 50% shareholding. Offers retail banking

with limited corporate banking.

Finibanco Angola FNB Founded in 2008. The major shareholder is the Portuguese bank Montepio Geral.

Banco Angolano de Negócios e

Comércio

BANC Founded in 2007. Small bank.

Banco BAI Micro Finanças BAI BMF Founded in 2004. Major shareholder is Banco Africano de Investimentos. Devoted

exclusively to the small business sector.

VTB Angola VTB Founded in 2007. The bank is focused on providing corporate banking services to

Russian and Western companies active in Angola.

Standard Bank Founded in 2010. 20% of South Africa’s Standard Bank is held by China’s ICBC.

Banco Quantum Founded in 2008. Angolan shareholders. Corporate and investment bank.

Banco Comercial do Huambo BCH Founded in 2010. Angolan shareholders. Regional bank.

Background on banks in Angola (Ranking information relates to December 2009)

Angola

PwC 23

Maturity Values in thousands AOA

63 days 91 days 182 days 364 days TotalTotal US$ thousands*

Banco BIC - 44,485 14,032,950 13,747,534 27,824,969 300,565

Banco Africano de Investimento - 3,602,450 1,470,370 13,680,640 18,753,460 202,574

Banco Fomento de Angola - 909,320 4,054,294 10,082,310 15,045,924 162,526

Banco de Negócios Internacional - - 9,182,770 705,340 9,888,110 106,811

Banco Regional do Keve - - 103,560 661,690 765,250 8,266

Banco de Poupança e Crédito - 1,165,580 18,935,121 2,937,307 23,038,008 248,856

Banco Sol - - 8,790,560 240 8,790,800 94,958

Banco Comercial Angolano - - 1,404,540 1,183,460 2,588,000 27,956

Banco Totta de Angola 200,000 10,520 18,480 17,760 246,760 2,665

Banco Desenvolvimento de Angola - 2,000,000 - - 2,000,000 21,604

Banco Angolano de Negócios e

Comércio- - 1,188,371 - 1,188,371 12,837

Banco Espírito Santo de Angola - 1,030 101,250 31,250 133,530 1,442

Banco Privado Atlântico - - 10,349,990 4,467,750 14,817,740 160,061

Banco de Comércio e Indústria - 21,413 5,000,671 3,450,476 8,472,560 91,520

Finibanco Angola - - 1,850,000 - 1,850,000 19,984

Banco Millennium de Angola - 2,350 2,609,878 2,001,720 4,613,948 49,840

Bai Micro Finanças - - 63,852 1,452,530 1,516,382 16,380

Banco Nacional de Angola - - 3,077,477 1,086,290 4,163,767 44,977

Banco Quantum - - - - - -

Banco Comercial do Huambo - 120,000 - - 120,000 1,296

Total 200,000 7,877,148 82,234,134 55,506,297 145,817,579 1,575,117

Source: BNA financial statements

Securities of Central Bank at 31 December 2009

* 1US$ = 92.5757 AOA 31/12/2010 exchangerate.com

Angola

24 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Moderate

Intense

None

Light

Nochange

Minorchange

Significantoperationaland or -ganisationalchange

Fundamentalchange instrategyandpositioning

Note: Based on responses from 3 banks

Response

16.7%

50%

16.7%

16.7%

Com

pet

ition

Moderate

Intense

None

Light

Nochange

Minorchange

Significantoperationaland or -ganisationalchange

Fundamentalchange instrategyandpositioning

Note: Based on responses from 3 banks

Response

50%

25%

Com

pet

ition 25%

Moderate

Intense

None

Light

Nochange

Minorchange

Significantoperationaland or -ganisationalchange

Fundamentalchange instrategyandpositioning

Note: Based on responses from 3 banks

Response

16.7%

33.3%

16.7%

33.3%

Com

pet

ition

Retail banking

Corporate banking

Investment banking

Retail banking

Although retail banking is in a developmental stage it was considered intensely competitive by four participants.

The majority of participants have made significant or fundamental changes over the last year.

Corporate banking

The majority of participants view corporate banking as intensely competitive. They also claim to have made significant or fundamental changes to strategy.

Investment banking

Perhaps reflecting the nature of the economy and the lack of opportunities, investment banking was assessed to have only light or moderate competition.

Q In your view, what is the level of intensity of competition in the following markets, and how will this affect your competitive response?

The following charts illustrate how the banks perceive the level of competition in three different markets; retail banking, corporate banking and investment banking.

Angola

PwC 25

Moderate

Intense

None

Light

Nochange

Minorchange

Significantoperationaland or -ganisationalchange

Fundamentalchange instrategyandpositioning

Note: Based on responses from 3 banks

Response

40% 20%

40%

Com

pet

ition

Micro-financeMicro-finance

Micro-finance was not considered to be a competitive market at present. As the economy grows, this can be expected to change.

The competitive assessment of the market by participants suggests that demand for micro-finance exceeds the appetite of the current micro-finance providers.

Angola

26 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

0

100

200

300

400

500

600

700

800

900

1000

200920082007200620052004

Number of ATMs

0

1000

2000

3000

4000

5000

6000

7000

8000

200920082007200620052004

Number of POS

terminals

0

5

10

15

20

25

30

35

40

45

50

200920082007200620052004

Number of ATM

Transactions(million)

0

0.5

1.0

1.5

2.0

2.5

3.0

200920082007200620052004

Number of POS

transactions(million)

0

500

1000

1500

2000

2500

20092008200720062005

ATMWithdrawalsUS$ millions

0

50

100

150

200

250

300

350

20092008200720062005

POSSpend

US$ millions

Source: www.emis.co.ao

Angola’s electronic payment system is managed by Empresa Interbancária de Serviços (EMIS), which is owned by the National Bank of Angola, with a 51% share, and retail banks operating in the market, with the remaining 49%.

Data from Empresa Interbancária de Serviços (EMIS) Angola shows that the number of ATMs grew from below 100 in 2004 to 1,000 by 2009.

The number of POS terminals increased dramatically between 2008 and 2009 from 2,660 to 7,587.

Both the number of POS transactions and spend has also grown dramatically as a result of the POS terminal expansion.

In an EMIS consumer survey in December 2010, 86% of multicaixa e-card holders said that the most important reason for using a bank card was to avoid bank queues.

Electronic banking in Angola

Growth in ATMs Growth in ATM transactions Growth in ATM withdrawals

Growth in POS terminals Growth in POS transactions Growth in POS spending

Angola

PwC 27

• The impact of the global economiccrisis and the drop in the price ofoil caused a major reduction inAngola’s revenues.

• Many banks had relationships withlocal companies that had dollar-denominated debt but limited orno dollar revenue.

• Fierce levels of competition. Itis expected that this will lead tofuture consolidation.

• Improvements in bank supervision.

• Improvements in infrastructure.

• Banks need to internationalise asmuch of the development has beenat a domestic level.

• Development of a credit bureau.Although data was collected a fewyears ago it was not maintained.As a result the initiative has beenrestarted and was anticipated tobegin in early 2011.

• The transition from a dollarisedeconomy to the local Kwanzacurrency will take a long time.Much of the economic activity iscentred on dollars.

• Once the stock market opens manybanks will seek listings.

• Anti-money laudering legislation.The banks are preparing for closeAML monitoring. (The Governorof the Central Bank, José LimaMassano, announced in early 2011that the bank will create a unitdesigned to prevent and detectacts that use the Angolan financialsystem to finance terrorism andmoney laundering. Massanoanticipates that the unit willbecome operational during the firstquarter of 2011.)

Q What are the most important changes taking place in your financial services market?

Angola

28 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Participants highlighted the following:

Strengths

• The financial system is one ofthe more developed parts of theeconomy.

• Implementation of technology, forexample the interbank ATM system,electronic payment of salaries, etc.

• The banks are well capitalised.

• Rapid development of branchnetworks.

• Presence of international investorsin the banking system with goodknowledge.

• Strong competition.

Weaknesses

• Need to improve corporategovernance.

• No credit database being sharedbetween banks.

• Some banks have been tooaggressive in their networkexpansion.

• Strong Portuguese rather thanmultinational influence.

• Quality and training of staff is weak.Some banks have set up their owntraining institutes.

• Improvements needed insupervision and regulation.

• With the proliferation of bankssome may develop capital problems.

• Rules of the financial system yet tobe provided in terms of consistencyand transparency.

Q What are the strengths and weaknesses of the financial services sector?

Angola

PwC 29

A number of banks expressed concern over liquidity.

There was a general concern about the industry’s exposure to the real estate sector. One bank predicted an imminent correction in the real estate market.

Concern was also expressed about the continued independence of the Central Bank in determining monetary policy.

Further concerns were also expressed over the raising of deposit reserves to 30%, the high level of the discount rate at 30% and the future of the local currency.

One bank predicted a shakeout in the industry. They suggested the current number of around 20 banks today will be reduced to 10 banks in five years’ time.

Concerns around the reliability of customers’ financial information provided for credit analysis.

Q Do you have any major concerns about the financial sector in Angola?

Q Can you rate from 1 to 10 the level of development of the financial services sector in Angola relative to other markets in West Africa? (10 = maximum development.)

The banks awarded a score of 6 out of 10 in assessing the level of development in Angola relative to other West African markets.

One bank commented that the industry had developed very rapidly after the war.

Another bank believed that the Portuguese banks had injected very high levels of competition.

A Portuguese banker placed Angola and Mozambique at the same stage of development - 6 out of 10.

Angola

30 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

One participant suggested that credit needed to be disseminated more widely in the country and not just to a “select few”.

The exchange rate mechanism needs to be more consistent and transparent. One banker said that market rules need to apply to the buying and selling of currency. Three currency auctions are held each week. At the end of 2009 following the drop in oil prices, the Kwanza was unofficially devalued by around 25% and there was a surge in demand for dollars. In November 2009 the IMF agreed to provide a US$1.4 billion standby credit.

There is a need for improvement in supervision. One bank indicated that supervisors are not well trained and that regulation is often unclear. Risk management policies have not been sufficiently developed.

The bureaucracy often slows down simple transactions such as overseas funds transfers.

The limited development of the legal environment means that some products such as leasing or factoring are yet to be made available.

Q What developments are needed to move the financial services market forward?

Although there are no recognised statistics it is generally believed that only 11% of the population has bank accounts.

The use of internet banking is very limited but is expected to grow.

Mobile banking will increase in importance.

The number of cards in use remains small but is expanding. The 2009 Banco BAI annual report stated that it had issued just 3,583 cards. As the country’s largest bank it is clear that the number of credit cards in circulation remains very limited.

Q How will consumer needs in 2013 differ from those of today?

Angola

PwC 31

0 5 10 12

Foreign entrants

Fiscal pressures

Money laundering

Mergers/Consolidation

Capital markets

Demographics

Corporate social responsibility

Compensation of professionals

Funding constraints

Regulation and reporting

Technology

Foreign exchange control

Performance of domestic economy

Liquidity

Based on responses from 5 banks

Score

Q What are the major drivers of change in the financial services industry today? Please rank the “top 5” in order of importance.

The top three drivers of change in the Angolan financial market were identified as liquidity, the local economy and foreign exchange controls. (Angola has a complex foreign exchange and control system administered by the National Bank of Angola).

These drivers were closely followed by the use of technology and the regulatory environment.

In August 2010 the Angola Government acknowledged that some banks were struggling with liquidity issues. Local media has reported that this has caused some banks to limit lending and prevent some withdrawals.

In its 2010 budget, the government indicated that it would allow banks to access government loans if they met collateral requirements and followed a restructuring and recapitalisation programme.

Angola

32 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Q What are the most pressing issues facing your organisation?

-1.0 -0.5 0.0 0.5 1.0 1.5 2.0

Complex instrumentsLow-cost alternatives/competitorsIFRS reporting and IFRS amendmentsValuation and pricing of financial instrumentsTransparency of fees and commissionsTax legislationMarginsLitigation risk Internet and data securityDeregulation of commissionCost reductionBusiness continuationBanking for the previously un-bankedRetail sales practicesCapital management

Volatility interest ratesProfit performancePayment systems

Impact of the latest phase of the financial crisisData security and privacy

CorruptionOvercapacity

Building a customer baseBrand awareness

Back office/operational/system qualityImproving revenue growth

Retaining existing customersMarket volatility

Level of crimeAddressing compliance and regulation

Appropriate staff incentive schemesService quality

Customer acquisition/growth Currency fluctuations

Commodity pricesRisk management

Credit risk managementAvailability of key skills

Based on responses from 4 banks

More pressing issues

2.0 1.5

The top three pressing issues identified by participants were the availability of key skills in the banking industry followed by credit risk management and risk management in general.

The significance of oil resources was reflected in the next two most important pressing issues, being commodity prices and currency fluctuations.

Angola

PwC 33

None of the banks interviewed were involved in a merger or acquisition during the last year.

Q Have you completed a merger or an acquisition in the last year and are any planned for next year?

Q Will there be an entrance of new financial services players into Angola in the next 3 years?

The participants unanimously agreed that there would be more financial institutions entering the market over the next three years.

Although Citibank left Angola in 2003 and ABSA (Barclays Bank) sold its 50% shareholding in Banco Comercial Angolano to six existing shareholders in 2009, a number of new foreign banks are expected to enter over the next three years.

Banks from other parts of Africa are expected to enter the market. Ecobank was mentioned as a possible new entrant along with several South African banks. In announcing its departure, ABSA stated in media reports that it would consider a re-entry if the conditions were right.

One participant said that the oil companies were pressuring the foreign banks to enter the market.

Q What is your institution’s primary method of growth in Angola ?

The participants agreed unanimously that organic growth was the primary method of growth in Angola.

Q Do you anticipate further demands on the need for increased transparency on pricing and product comparisons?

Four of the five banks that answered this question believe there will be demands for increased transparency on pricing and product comparisons in Angola as they move forward.

Angola

34 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

The participants agreed unanimously that regulations would increase substantially over the next three years. Two areas which were mentioned specifically were capital adequacy and operational risk.

All the participants agreed that they would increase compliance spending over the next three years. Three participants specifically expect to increase their spending by 100%.

All the participants agreed that financial institutions’ risk management systems were not sufficiently robust at this time.

Several areas could benefit from improvements in risk management, including:

• operational risk.

• credit risk.

• policies and procedures for specificsectors such as real estate, liquiditypolicies etc.

• fraud and corruption.

One bank suggested that once the credit bureau gets up and running, market knowledge will improve and this will assist more effective risk management.

Q Do you see the intensity of regulation of the financial services industry increasing or decreasing over the next three years?

Q Do you plan increased compliance spending over the next three years?

Q Do you believe financial services organisations’ risk management systems are sufficiently robust?

Q In which area could there be improvements in your organisation’s risk management systems?

Q Do you support the concept of deposit insurance?

While four banks support deposit insurance, two banks remain opposed.

Of the four banks in support of deposit, two banks think it is at least 10 years in the future.

No

Yes

Support for Deposit Insurance

Angola

PwC 35

Q In which areas are you currently experiencing the greatest shortage of skills? 1 is low, 5 is high

0 5 10 15 20 25

Non-executive directors

Administration

Internal audit

Audit committee

Compliance

Information technology (IT)

Executive directors

Risk management

Financial reporting

Capital management

Score

The availability of key skills was identified earlier in this section as the most pressing issue in Angolan banking.

The three key areas of skills shortage are:

• capital management;

• financial reporting; and

• risk management.

These shortages are closely followed by the limited availability of skilled executive directors and IT specialists.

Angola

36 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Q Has your organisation adopted IFRS (International Financial Reporting Standards)? What do you see as the key benefits of adopting IFRS?

Four of the five participants indicated that they have adopted IFRS for group purposes.

The most important benefits of IFRS were identified as more transparent disclosures and increased reliability in financial reporting.

Q Do you think that the adoption of IFRS will enhance market reporting? How confident are you that you have a full understanding of the impact of IFRS on your organisation?

The participants agreed unanimously that IFRS will enhance market reporting.

The majority of participants believe that they fully understand the impact of IFRS on their bank.

Somewhat confident

Very confident

Full understanding of the impact of IFRS

Q Do you currently use a CRM (Client Relationship Management) system?

No

Yes

Currently have a CRM systemThe banks have not yet installed comprehensive CRM systems. At this stage only one foreign-based bank claimed to have an effective CRM system. (It scored 3 on a scale of 1 to 5 on effectiveness).

Angola

PwC 37

Q Do you agree or disagree with the following statements?

Our organisation will undergo a significant business disposal over the next three years

Our organisation will undergo significant M&A over the next three years

Our organisation will seek a strategic foreign investor or a partner in a significant new venture in the next three years

Our organisation will seek a strategic domestic investor or a partner in a significant new venture in the next three years

Joint ventures and partnerships will be key to our expansion plans

Neither

Agree

Disagree

Neither

Agree

Disagree

Neither

Agree

Disagree

Neither

Agree

Disagree

Neither

AgreeDisagree

Our organisation is already structured in the way we want

Neither

Agree

Disagree

Only one bank plans to be involved in M&A over the next three years.

Two banks agreed that joint ventures and partnerships will be an integral part of future expansion.

The banks, reflecting on their foreign shareholders, do not envisage any future foreign investor partnerships.

The banks are in growth mode and do not plan any business disposals.

Only one bank indicated that it might seek a strategic domestic investor.

Considerable change can be anticipated in the banks’ business models. Two banks agreed that their current structure matched their future business expansion.

Angola

38 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

The respondents unanimously indicated that they planned significant investments in risk management and compliance processes over the next 12 months.

There is a major branch expansion programme underway in Angola. One bank suggested that new branches could be staffed by up to 15 employees. Another bank suggested eight to ten employees while, and yet another, just five employees.

One bank suggested that it would expand on two fronts with large full service branches in conjunction with smaller, satellite branches.

Q Are significant investment and business process changes envisaged for risk management and compliance purposes over the next 12 months?

Q What will the role of branches be in 2013?

Q Which product areas will become increasingly important over the next three years?

Retail products

• Mortgages

• Leasing (legislation not yet in place)

• Savings products

• Cards

Wholesale products

• Capital markets (in May 2010Angola received credit ratingsfrom S & P, (B+), Moody’s (B1)and Fitch (B+) paving the way forinternational bond issues.

• Investment banking

• Asset management including a realestate investment fund

• Debt markets

• Leasing

Angola

PwC 39

Q Which foreign financial institution do you believe may choose to move into Angola over the next three years?

Banks from South Africa, Brazil, China and the rest of Africa are expected to move into Angola over the next few years.

Some of the banks mentioned by participants included ABSA, Bank of Brazil, Citibank, HSBC, Ecobank, Société Générale and BNP Paribas.

Q What are the top three offshore markets you believe your organisation should focus on going forward?

The Angolan banks are interested in expanding their activities in SADC (Southern African Development Community).

SADC (founded in 1980) includes 15 member states: Angola, Botswana, DRC, Lesotho, Madagascar, Malawi, Mauritius, Mozambique, Namibia, Seychelles, South Africa, Swaziland, Tanzania, Zambia and Zimbabwe. The SADC area has a combined population of 258 million.

Countries that were singled out for special attention included South Africa, Mozambique, Brazil and China. One bank that mentioned an interest in Asia noted their involvement in China and East Timor.

As noted elsewhere in this report there has been growing usage of both ATMs and POS terminals.

Further investment in broadband will stimulate the adoption of internet banking.

Both mobile banking and internet banking are expected to become more widely used.

A government statement in May 2010 put mobile phone ownership at 8 million.

Q How will the financial services markets needs of the consumers of 2013 differ from those of today?

Foreign banks and Angolan oilBP’s Angolan unit launched a syndication arranged by BNP Paribas SA and Standard Chartered Bank to obtain a $3 billion term loan facility backed by crude oil sales from its Angolan production.

The facility for BP Angola is a five year amortizing term loan maturing June 30, 2015, the banks said in a joint statement.

Source: BNP Paribas SA , Standard Chartered Bank Statement, 2 September, 2010

Angola

40 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Q What is your estimate of annual growth in revenue for 2010 and over the next three years?

0 10 20 30 40 50 60 70 80 90 1000

10

20

30

40

50

60

70

80

90

100

Expected annual growth rate in 2013

Exp

ecte

d a

nnua

l gro

wth

rat

e in

201

0

Two participants expected minimal growth in 2010 but all expect to be growing by 15% or more by 2013.

Two banks anticipate annual growth of 30% in 2013 while one bank forecast they could be expanding by 50% in 2013.

Angola

PwC 41

Angola Peer Review

1 2 3

Corporate banking BAI/BFA BIC

Retail banking BFA BAI BPC

Credit cards BFA BNI/BIC

Trade Finance BFA/BIC BAI/ Millennium

Micro-finance Banco Sol BAIMF BPC

Peer Review

A simple scoring method awarded 3 points to first place, 2 points to second and 1 point to third place. This allowed the banks to be ranked based on a total score.

Banks were asked not to record an opinion unless they were active in that segment and were comfortable in providing an accurate ranking in terms of success (performance, presence and momentum) as opposed to mere size.

They were not permitted to rank their own institution. Often banks chose just to indicate first and/or second place.

The Peer Review highlights a number of banks. BFA was awarded two first place positions in retail banking and credit cards, BAI was the most recognised for corporate banking while BIC was in first position for trade finance and Banco Sol for micro-finance.

Q Can you name the top three banks in terms of success (performance, presence, momentum, etc.) across a variety of different markets?

42 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

PwC 43

Côte d’Ivoire

Banks interviewed:

• Société Générale de Banques enCôte d’Ivoire (SGBCI)

• Banque Atlantique Côte d’Ivoire(BACI)

• Société Ivoirienne de Banque (SIB)*

• Ecobank Côte d’Ivoire

• Banque Nationale d’Investissement(BNI)

• Diamond Bank**

* Part of Attijariwafa Bank based in Morocco

** Part of Diamond Bank based in Nigeria

Côte d’Ivoire

44 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

The economy in general

Côte d’Ivoire has a population of approximately 21 million. It is estimated that it had GDP growth of 2.3% in 2008 and 3.2% in 2009. GDP per capita is estimated to be US$1,700.

The Côte d’Ivoire economy has historically been highly dependent on the production and export of tropical products. It is the world’s largest producer of cocoa beans and a significant exporter of coffee and palm oil. Since 2007 oil and gas production have grown in relative importance. Dependence on agricultural exports has exposed the economy to swings in commodity prices.

In comparison to other developing countries, Côte d’Ivoire has a sophisticated infrastructure. Abidjan is the most modern port in West Africa. In the past it has been viewed as the economic engine of Francophone West Africa.

The political and social crisis that began in 2002 has had a major impact on economic development. The U.S. State Department has noted that “Economic growth has been negative or low each year since the outbreak of the armed rebellion in late 2002, with a cut-off of most external assistance, (except humanitarian aid) mounting domestic and foreign arrears and a drastic slowdown in foreign and domestic investment.”

In March 2009, Côte d’Ivoire received debt relief under the Enhanced Heavily Indebted Poor Countries (HIPC) Initiative. The IMF approved a US$565.7 million Poverty Reduction and Growth Facility. The IMF Board noted Côte d’Ivoire’s performance under its two Emergency Post-Conflict Assistance programmes and called for continued reforms toward HIPC completion point. (Source: U.S. State Department).

Recent elections

Côte d’Ivoire’s elections were held in November 2010 having been delayed six times.

Although conflict ended in 2007 political tensions remain high and future stability remains uncertain. During the civil war the country was divided between the pro-government South and the anti-government forces in the North.

At the time of publication of this report the political crisis that resulted from the disputed winner in the November 2010 presidential election, remains.

The incumbent President Laurent Gbago disputes the result with the rival candidate Mr Alassane Ouattara and a political stalemate exists.

The African Union is trying to negotiate an end to the crisis.

General background on Côte d’Ivoire

Côte d’Ivoire

PwC 45

Current employment in the six banks interviewed is 2,753 and this is expected to increase by 14% to 3,150 employees by 2013.

The six banks have 199 branches in 2010 and they expect these to more than triple by 2013 to 335 branches.

The banks expect to almost double the number of ATMs from 296 to 520 by 2013.

Four banks provided data on debit cards. These are anticipated to grow from 280,000 in 2010 to 460,000 in 2013.

Only three banks supplied credit card estimates. In 2010 they estimated 35,000 credit cards expanding to 160,000 by 2013.

Background on participants The number of retail bank accounts at the six banks in 2010 was estimated to be 820,000 rising to 980,000 over three years.

On the corporate side, fee income as a percentage of total income was estimated to exceed 40% for three banks in 2010 and by 2013 this will rise to 60% for two of these banks.

The banks indicated that they had 38 corporate clients with loan facilities exceeding US$25 million and by 2013 this would grow to 53 corporate clients.

Estimates of middle market customers were distorted by one bank’s figures and as a result have not been included.

Côte d’Ivoire

46 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

IMF Statement on Côte d’Ivoire issued in September 2010

“Economic activity has held up well in 2010. Economic growth appears on track to reach the program target of 3% for the year despite sporadic power outages, difficulties in the oil and refinery sectors, and some civil unrest during the first half of 2010.

Continued strong world cocoa prices, in particular, have helped support economic activity and construction is having a significantly better year. Inflation has remained in the range of 2%. The external current account continues to show a sizeable surplus as both exports and imports are growing robustly.

With respect to the economic program in 2010, the budget outcome at the end of June was generally in line with program commitments. Revenue performance accounted for much of a better-than-programmed overall budget deficit (0.5 percent of GDP), but this is not expected to affect the outlook for the year as a whole.

Public expenditure remained within the planned envelope, with foreign-funded investment being executed especially well, though the target for pro-poor spending was missed by a narrow margin.

Structural reform implementation was slow and appears to have stalled in critical areas: reducing the large financial imbalances in the electricity sector, establishing medium-term sustainability of the government wage bill and reforming the civil service and judicial reforms needed to improve the poor business environment.

These delays impose costs on the budget. Also, the implementation of cocoa and coffee sector reforms is important for the floating completion point under the HIPC Initiative.

The mission welcomed the authorities’ reaffirmation of their main economic policy objectives: facilitating higher economic growth and reducing the widespread poverty in Côte d’Ivoire.

In line with the country’s poverty reduction strategy, budget expenditure will continue to shift towards pro-poor spending, including basic health care and education.

But with an investment rate of less than 10% of GDP, the country urgently needs substantial new investment in the coming years, especially in power and transport infrastructure.

Thus it will be important that the authorities develop a comprehensive borrowing strategy, one that takes into account debt sustainability issues and the long-run fiscal path in setting borrowing objectives.”

Côte d’Ivoire

PwC 47

Morocco

Algeria Libya

MauritaniaMali

Senegal

Guinea

Gha

na

NigerChad

Nigeria

BurkinaFaso

Togo

Ben

in

CôteSierra Leone

Guinea Bissau

Cameroon

Gabon Congo

Liberia

Equatorial Guinea

Gambia

Cape Verde

unisiaT

d’Ivoire

Western Sahara

The Central Bank of West African States (BCEAO) oversees banks and financial institutions conducting activities in the member states of the West African Economic and Monetary Union (WAEMU). These relations mainly fall within the scope of the functions performed by BCEAO as far as the surpervision of the banking sector and the control and distribution of credit are concerned.

Composition of WAEMU

Seven groups dominate the WAEMU banking system through 39 establishments with relatively wide national networks.

Banking Law

The Banking Law provides a definition of banks and financial institutions, and of the credit and investment activities they offer. It specifies the conditions of entry and determines the obligations which must be met by banks and financial institutions in the execution of their operations. The Banking Law defines the scope of the control exerted by the Central Bank and the Banking Commission, and spells out the rules governing the Monetary Union and the sanctions applicable in case these rules are not respected.

Banks and financial institutions must be authorised and registered on the list of banks and financial institutions to be able to operate. This authorisation is granted by the Minister of Finance after BCEAO has examined the application and the WAEMU Banking Commission has certified its conformity with applicable laws.

The conditions of approval are mainly based on :

• the name

• the legal status of theestablishment

• at the end of 2010 the minimumcapital which currently stands atCFA 1 billion (US$ 2 million)* forbanks throughout the States willbe raised to CFA 10 billion (US$20.4 million)*, and that of financialinstitutions will be raised from CFA300 million (US$ 0.6 million)* toCFA 3 billion (US$ 6 million)*.

• the adequacy between theresources and objectives of theestablishment to be created

• the quality of shareholders

• the worthiness and experience ofmanagers, and

• an activity programme showing theviability of the operation.

In order to enable all banks and financial institutions of the Union to have access to the banking market of each member state, in optimal competition conditions, the Council of Ministers of the Union decided, at its meeting held on 3 July 1997, to adopt the principle of unique approval. Thus, as from 1 January 1999, any bank or financial institution duly authorised by a state of the Union, may carry out a banking or financial activity in the other states of the Union, and provide services of the same nature in any other area in the Union, without having to request new authorisations.

Source: BCEAO and WAEMU

Banking in Francophone West Africa

Bénin, Burkina Faso, Côte-d’Ivoire, Guinée Bissau, Mali, Niger, Sénégal and Togo.

* 1US$ = CFA BCEAO 489.87 31/12/2010 Exchange-rates.org

Côte d’Ivoire

48 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Bank groups in Francophone West Africa (UEMOA)

In 2009, the number of financial institutions expanded from 116 to 118. This total included 99 banks of which 20 were located in Côte d’Ivoire.

As the adjacent table indicates, 39 of these banks are associated with seven banking groups who in turn, account for 65% of assets.

The bank groups are Ecobank, Société Générale, Bank of Africa, Attijariwafa Bank, BNP Paribas, Banque Atlantique Group and UBA.

The largest group is Ecobank with 14.8% of assets and a presence in all member states. Société Générale is in second place with 12.9% of assets and Bank of Africa with 10.7%.

Collectively the banks employed 8,987 people in 2009 in the region.

Bank Group Number Institutions

Market share

Teller windows

Number of customer accounts

Staff

Ecobank (ETI) 8 14,8% 216 825,632 2,537

Société Générale 4 12,9% 119 466,689 1,976

BOA GROUP 8 10,7% 103 361,074 1,240

(of which two are

financial companies)

2 0,3% 2 0 18

Attijariwafa Bank 4 10,3% 141 646,725 1,373

BNP Paribas 5 8,5% 95 288,752 1,473

AFG 7 5,5% 145 223,429 1,228

United Bank for Africa

(UBA)

3 2,6% 51 175,923 770

Total 39 65,3% 870 2,988,224 10,597

Côte d’Ivoire

PwC 49

Banks Fin.instit

Total

Bénin 12 1 13

Burkina 11 5 16

Côte d’Ivoire 20 3 23

Guinée-Bissau 4 - 4

Mali 13 4 17

Niger 10 1 11

Sénégal 18 3 21

Togo 11 2 13

Total 99 19 118

Source: Rapport Annuel de la Commision Bancaire de l’UMOA - 2009 Au 31 décembre 2009 trois (3) établissements de crédit agréés n’avaient pas démarré leurs activités.

Q Number of financial institutions in each UEMOA country

Activitès principales

Bénin Burkina Côte d'Ivoire

Guinée- Bissau

Mali Niger Senegal Togo UEMOA Market share

Teller windows

Number of bank accounts

Effective

Banks 12 11 18 4 13 10 16 11 95 98,9% 1.335 4.474.801 16.940

- general 10 9 15 3 9 8 12 10 76 90,5% 1.202 3.931.533 15.109

- specialist 2 2 3 1 4 2 4 1 19 8,4% 133 543.268 1.831

. agriculture - - 1 - 1 - 1 - 3 3,1% 58 235.68 587

. morgage 1 1 1 - 1 1 1 - 6 3,2% 30 241.168 526

. micro-finance 1 1 1 1 2 1 2 1 10 2,1% 45 66.332 718

Financial

etablishments

1 5 2 - 3 1 3 2 17 1,1% 50 5.747 263

Credit sales - 1 - - - - 1 - 2 0,0% 30 5.623 82

Credit sales

and/or leasing

1 4 2 - 2 - 2 - 11 0,8% 17 124 157

Venture capital

and guarantee

funds

- - - - 1 1 - 2 4 0,3% 3 0 24

The adjacent table shows that Côte d’Ivoire has 20 banks within the UEMOA total of 99 banks, based on the Central Bank’s statistics for December 2009.

Senegal has the second largest representation with 18 banks.

The structure of the financial sector within the Francophone region is shown in the table below. The broad-based banks account for 91% market share in UEMOA.

Bank Group Number Institutions

Market share

Teller windows

Number of customer accounts

Staff

Ecobank (ETI) 8 14,8% 216 825,632 2,537

Société Générale 4 12,9% 119 466,689 1,976

BOA GROUP 8 10,7% 103 361,074 1,240

(of which two are

financial companies)

2 0,3% 2 0 18

Attijariwafa Bank 4 10,3% 141 646,725 1,373

BNP Paribas 5 8,5% 95 288,752 1,473

AFG 7 5,5% 145 223,429 1,228

United Bank for Africa

(UBA)

3 2,6% 51 175,923 770

Total 39 65,3% 870 2,988,224 10,597

Côte d’Ivoire

50 Perspectives on Strategic and Emerging Issues in Africa West Coast banking

Regional Economic Integration in Francophone West Africa

The West African Economic and Monetary Union (WAEMU) or Union économique et monétaire ouest-africaine (UEMOA) is an organisation of eight states of West Africa established to promote economic integration among countries that share a common currency, the CFA franc.

UEMOA was created by a Treaty signed in Dakar, Senegal, on 10 January 1994, by the Heads of State and Government of Benin, Burkina Faso, Côte d’Ivoire, Mali, Niger, Senegal, and Togo. In 1997, Guinea-Bissau became its eighth member state.

UEMOA is a customs and monetary union between some of the members of Economic Community of West African States (ECOWAS). Its objectives are:

• greater economic competitiveness,through open and competitivemarkets, along with therationalisation and harmonisationof the legal environment;

• the convergence of macroeconomicpolicies and indicators;

• the creation of a common market;

• the coordination of sectoralpolicies; and

• the harmonisation of fiscal policies.

In terms of its achievements, UEMOA members have implemented macroeconomic convergence criteria and an effective surveillance mechanism; have adopted a customs

union and common external tariffs (early 2000); have harmonised indirect taxation regulations; and have initiated regional structural and sectoral policies. A September 2002 IMF survey cited the UEMOA as “the furthest along the path toward integration” of all the regional groupings in Africa.

UEMOA institutions include:

• a common central bank – BanqueCentrale des Etats de l’Afrique del’Ouest (BCEAO);

• a Regional Banking Commission,and regional Stock Exchange since1998, and a partially functioningSecurities Exchange Commission;

• BOAD (Banque Ouest Africainede Développement) which isconsidered an independent,specialised institution under theUEMOA treaty; and

• Institutions also include a Courtof Justice, a General AccountingOffice, regional Chamber ofCommerce, and, eventually, aParliament, none of which is fullyfunctioning.

UFMOA

Morocco

Algeria EgyptLibya

MauritaniaMali

Senegal

Guinea

Gha

na

SudanNigerChad

Nigeria

BurkinaFaso

Togo

Ben

in

CÙteSierra Leone

Guinea Bissau

Cameroon

Ethiopia

Somalia

CentralAfrican Republic

Gabon Congo

DemocraticRepublicof Congo

Uganda

Kenya

AngolaZambia

Malawi