university of missouri - · pdf fileuniversity of missouri ... markets and thus help to...

TRANSCRIPT

Southern Minnesota’s Economic Opportunities: Building on the Region’s StrengthsMark Drabenstott, DirectorRUPRI Center for Regional CompetitivenessUniversity of Missouri

outhern Minnesota is a vibrant region with many assets on which to build a stronger eco-nomic future. Among other things, it has an agricultural powerhouse, world-class health care and associated research, robust factory clus-ters, and a significant and growing footprint in

renewable energy. What is more, many general areas of strength circumscribe these economic assets, notably a skilled workforce, a resilient entrepreneurial spirit, outstanding educational institu-tions, and evident pockets of innovation.

While the region enjoys a generally healthy economy today, it has reasons to aim higher. For several years, the region’s per capita income has trended down relative to Minnesota as a whole. A growing income gap with the Twin Cities is especially noticeable. Residents in the region also cite steady outmigration in its many rural areas as a source of concern, made worse by the fact that this exodus includes many young, talented workers. Finally, many families in the region still depend heavily on commodity agricul-ture and a phalanx of factories for their income. These sectors are likely to see continued consolidation, which may point to further outmigration in the future.

What are Southern Minnesota’s brightest economic opportunities? The southern Minnesota Regional Competitiveness Project aims to answer this very question. The answer comes from two critical pieces of informa-tion. The first is under-standing the economic assets that distinguish the region. That was achieved by holding a series of 10 roundtables with a broad cross-section of leaders from all corners of the region. (A report that summarizes the critical findings from all roundtables is posted on the project web site.) The roundtables bring critical local knowledge to the process that can be missed when looking at data alone. The second is identifying what the region currently does best in the global economy. To discover the region’s best niches, a range of regional economic analysis was conducted by a team of analysts led by the RUPRI Center for Regional Competitiveness. The analytics bring the discipline of market-based information to illuminate the region’s inherent strengths. Together, the twin approaches provide the region with a more robust set of economic development options than either would alone.

This report lays out six economic options that hold the greatest promise for southern Minnesota. These six reflect the region’s

Helping Regions Win in the Global Economic Race

S

Rural Policy Research InstituteUniversity of Missouri

F a l l 2 0 0 8

Southern Minnesota Project Region

8145.ƒƒ.indd 1 11/13/08 9:54:30 AM

current economic footprint, building importantly on health care, agriculture, and manufacturing. To a considerable extent, these three continue to represent the three legs of the region’s economy. But the list also points to new horizons made possible by the emergence of new markets and new technologies—bioscience and renewable energy are the brightest examples of these new hopes. �e first section summarizes the economic foundations for the six economic options, discussing pivotal findings from the round-tables and principal conclusions from the analysis of the southern Minnesota economy. �e second section discusses the region’s six economic options in turn: manufacturing, health care, food and agriculture, renewable energy, bioscience and high technology.

K S S M ESouthern Minnesota has much economic strength, but it must also contend with trends raising fresh concerns in the minds of leaders throughout the region. Perhaps no trend is more challeng-ing than a steady decline in per capita incomes relative to the rest of the state (Chart 1). Despite lying just outside the Twin Cities metroplex and the very strong performance in the farm sector recently, the region has seen steady erosion in income relative to

the state. �e other trend that commands attention in the region is the outmigration felt in many parts, especially areas where agri-culture is king.

Economic leaders throughout southern Minnesota are enthusiastic about raising the economic bar. �ey are in tune with current trends, and are confident the region has distinct assets on which to build a stronger economic future. �ey also believe that fortify-ing an already well-embedded spirit of regional partnership will improve the success of any new regional strategy.

A new development strategy for southern Minnesota will be founded on three pillars of information. �e first is the region’s current economic specialization and performance. �is defines the existing foundation for economic growth, an essential starting point for the region’s strategy. �e second is the business clusters now established and emerging in the region. Development experts believe such clusters give the region a competitive edge in global markets and thus help to highlight where more potential lies. �e third is a comprehensive inventory of the region’s economic assets as understood by those who understand them the best—regional leaders themselves. At least some of these assets may not yet be fully exploited in the global economy. Put another way, these as-sets help determine what could be, not just what is.

Current specialization and performance

�e southern Minnesota economy is diverse, with many moving parts that make it difficult to characterize. �at said, many different views of the underlying data confirm the region has three economic pillars: agriculture, manufacturing, and health care.

One set of data that points to this conclusion is the “specialization” of the region’s workforce. �is approach examines employment by industry in the region, and then compares that profile with what it would be if the region were just like the nation. Comparing the two indicates the industries

University of Missouri 2 Rural Policy Research Institute

2

95%

90%

85%

80%

75%

% of state

trend Line

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Chart 1: Region’s Per Capita Income as Percent of State PCI

8145.ƒƒ.indd 2 11/13/08 9:54:30 AM

in which the region has a strong specialization and those where it is clearly under-represented.

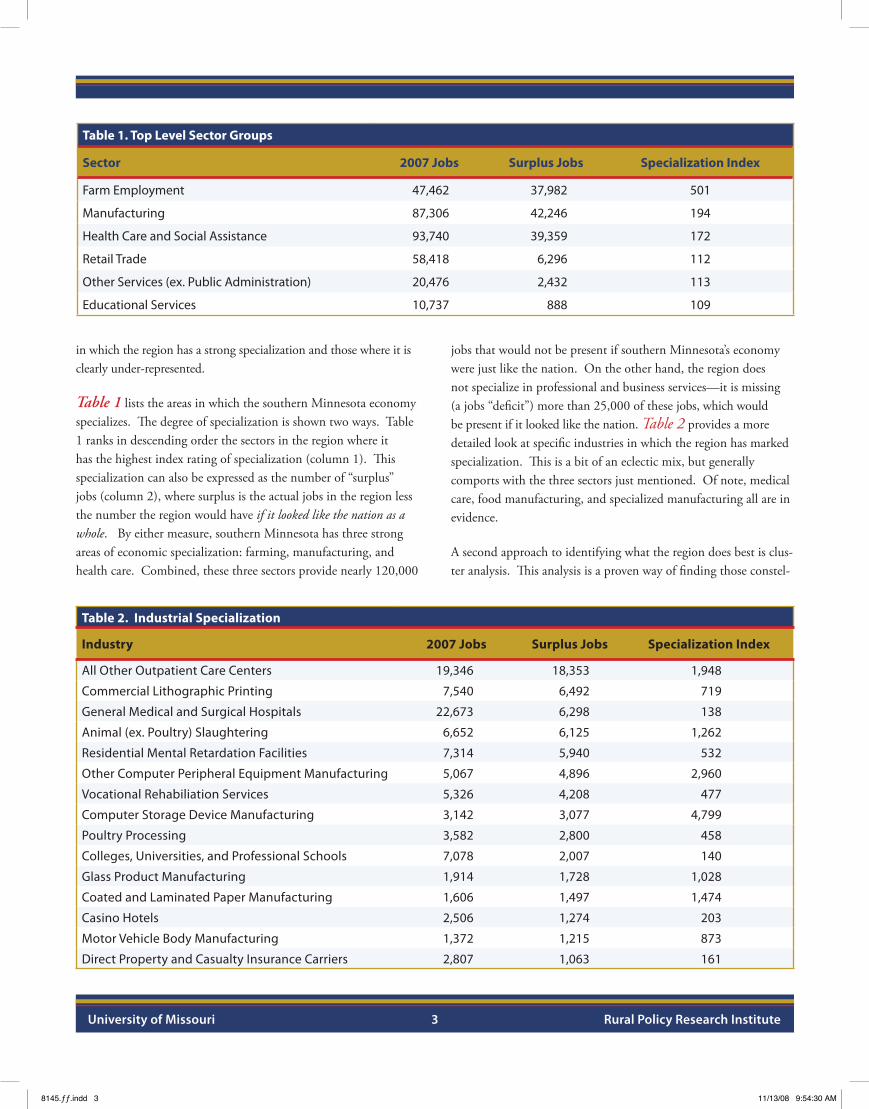

Table 1 lists the areas in which the southern Minnesota economy specializes. The degree of specialization is shown two ways. Table 1 ranks in descending order the sectors in the region where it has the highest index rating of specialization (column 1). This specialization can also be expressed as the number of “surplus” jobs (column 2), where surplus is the actual jobs in the region less the number the region would have if it looked like the nation as a whole. By either measure, southern Minnesota has three strong areas of economic specialization: farming, manufacturing, and health care. Combined, these three sectors provide nearly 120,000

jobs that would not be present if southern Minnesota’s economy were just like the nation. On the other hand, the region does not specialize in professional and business services—it is missing (a jobs “deficit”) more than 25,000 of these jobs, which would be present if it looked like the nation. Table 2 provides a more detailed look at specific industries in which the region has marked specialization. This is a bit of an eclectic mix, but generally comports with the three sectors just mentioned. Of note, medical care, food manufacturing, and specialized manufacturing all are in evidence.

A second approach to identifying what the region does best is clus-ter analysis. This analysis is a proven way of finding those constel-

�

University of Missouri � Rural Policy Research Institute

Table 1. Top Level Sector Groups

Sector 2007 Jobs Surplus Jobs Specialization Index

Farm Employment 47,462 37,982 501

Manufacturing 87,306 42,246 194

Health Care and Social Assistance 93,740 39,359 172

Retail Trade 58,418 6,296 112

Other Services (ex. Public Administration) 20,476 2,432 113

Educational Services 10,737 888 109

Table 2. Industrial Specialization

Industry 2007 Jobs Surplus Jobs Specialization Index

All Other Outpatient Care Centers 19,346 18,353 1,948

Commercial Lithographic Printing 7,540 6,492 719

General Medical and Surgical Hospitals 22,673 6,298 138

Animal (ex. Poultry) Slaughtering 6,652 6,125 1,262

Residential Mental Retardation Facilities 7,314 5,940 532

Other Computer Peripheral Equipment Manufacturing 5,067 4,896 2,960

Vocational Rehabiliation Services 5,326 4,208 477

Computer Storage Device Manufacturing 3,142 3,077 4,799

Poultry Processing 3,582 2,800 458

Colleges, Universities, and Professional Schools 7,078 2,007 140

Glass Product Manufacturing 1,914 1,728 1,028

Coated and Laminated Paper Manufacturing 1,606 1,497 1,474

Casino Hotels 2,506 1,274 203

Motor Vehicle Body Manufacturing 1,372 1,215 873

Direct Property and Casualty Insurance Carriers 2,807 1,063 161

8145.ƒƒ.indd 3 11/13/08 9:54:30 AM

University of Missouri 4 Rural Policy Research Institute

lations of businesses with the strong synergies that lend a competi-tive edge in national and international markets. Employment data for all southern Minnesota business establishments was combed to identify business clusters that are either prominent or beginning to emerge here. �is analysis focused on 45 value chains, or clusters, that are the critical elements of the national economy. �e cluster analysis results, therefore, allow regional leaders to see the critical value chains in which the region has a competitive advantage.

�e region participates in many clusters, as shown in Chart 2.�e circles on the chart are scaled to reflect the size of employment in that cluster. �e two largest “bubbles” are management (which also includes hospitals, and education) and basic health services,

while packaged food products is another large presence. With future development in mind, it is helpful to narrow the discussion with two key factors in mind. �e first is the degree to which the region has a stronger presence in a particular cluster than the rest of the nation. �is corresponds to all those clusters with index val-ues greater than one. �e second is identifying clusters projected to enjoy faster rates of job growth over the next decade (or those to the right of the vertical line). Only eight clusters meet both criteria, as shown in the bottom panel of Chart 3.

A third approach is to identify the distinct assets and emerging in-dustries that regional leaders believe offer the greatest potential for future growth. �is was the singular goal of 10 roundtables held

7

6

5

4

3

2

1

0

-1

-20% 0% 20% 40%

Projected Change in Employment (over 2007–2017 period)

Clu

ster

LQ

Basic Health Services

Management, higher education & hospitals

Hotels & transportation services

Business services

Arts & media

Financial services & insurance

Construction

Information services

Packaged food products

Computer & electronic equipment

Feed Products

Nondurable industry machinery

Appliances

Machine tools

Wood building products

Construction machinery & distribution equipment

Concrete, brick building products

Metalworking & fabricated metal products

Wood products & furniture

Dairy products

Rubber products

Breweries & distilleries

Glass products

Paper

Leather products

Grain milling

Chart 2: Cluster Size, Specialization, and Projected Change in Employment

8145.ƒƒ.indd 4 11/13/08 9:54:31 AM

with more than 500 public and private leaders from throughout the region. The findings from that regional dialogue corroborate many of the analytical findings, but also point to new directions not yet apparent from the data. Three findings stand out:

• There is strong consensus among regional leaders that agriculture, manufacturing, and health care are pillars in the economy. Their continued strength is not taken for granted, but most leaders believe they will figure prominently in the region’s development strategy. That said, the manufacturing activity in the region is so diverse that it is hard to articulate an industrial strategy. Similarly, the region’s excellence in health care underpins a high quality of life, but there are questions about how best to leverage that excellence into more economic growth.

• Several new market opportunities excite leaders in the region, even though most of them are still in early stages of develop-ment. These include renewable energy, bioscience, tourism,

and specialty foods. These new opportunities are evident in pioneering businesses now emerging throughout the region, and the potential is enhanced by a sense that the businesses have tapped into markets with significant upside.

• The region boasts powerful innovation engines—Mayo Clinic, Hormel Institute, various arms of the University of Minnesota, and three MNSCU institutions, among oth-ers—but is not harnessing the full economic potential these provide. The apparent disconnect between innovation and economic growth is nowhere more evident than in Rochester.

• Seizing the new opportunities will take more concerted part-nership across key organizations and sectors in the region. Leaders from all segments take heart that southern Minne-sota demonstrates a strong spirit of collaboration. But they are anxious to see that strengthened, especially in ways that bolster the capacity of the region to innovate.

University of Missouri � Rural Policy Research Institute

8145.ƒƒ.indd 5 11/13/08 9:54:32 AM

Six Strategic OpportunitiesThe strongest economic development strategies are born from combining the best available quantitative and qualitative informa-tion. Drawing on the three approaches described above, six strate-gic opportunities appear to hold the greatest potential for southern Minnesota: manufacturing; health care; food and agriculture; renewable energy; bioscience; and high technology. Each oppor-tunity has its own corresponding geography. Healthcare and high technology will center somewhat more on eastern portions of the region, whereas renewable energy and food and agriculture may be more prominent in the west. Bioscience and manufacturing may be common throughout.

The remainder of this section describes each strategic opportunity in turn. In each case, the goal is to identify the strengths that can propel the strategy and the factors critical to successful develop-ment. An overriding consideration is how the opportunity can help the region raise the bar of per capita incomes in the region.

Manufacturing

Southern Minnesota has a strong industrial base. One in five workers in the region is employed by a manufacturing firm, a much higher proportion than in the nation. The manufacturing activity runs a very wide gamut—from food manufacturing to specialized high technology products. Given the overall size and complexity of the sector, a useful approach is to think of it in three parts: food manufacturing that builds on the region’s agricultural prowess; high technology that builds on the region’s research prow-ess, and a “middle third” that is harder to characterize. The first two parts are discussed in separate strategic opportunities below.

The middle third covers a lot of industrial ground. To give but one sense of this, the top 50 industries employ nearly 32,500

workers at 726 firms. These firms are in everything from machine shops to office furniture to boats. From a strategic point of view, it is hard to put one’s arms around such a diverse set of businesses. Yet doing so seems critical to the region’s future simply because these firms and jobs figure so prominently in the region’s current economy.

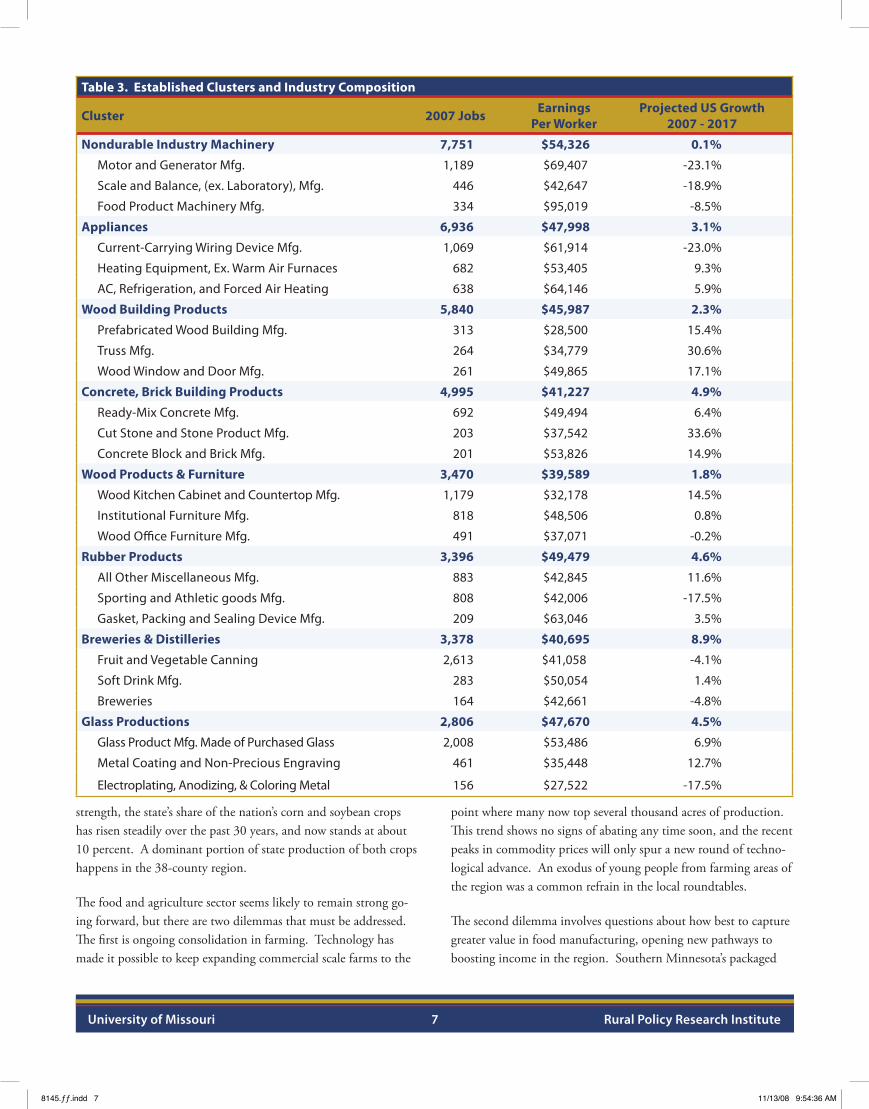

To bring some sense of direction, we began with the business clusters where the region has a strong overall competitive position and jobs are likely to grow (Chart 3). We then looked beneath the broad definitions to the three largest industries found in each cluster in southern Minnesota. Table 3 lists the 24 industries, ranked by total employment. Information is also shown about earnings per worker and projected job growth. These elements are important context in choosing a regional manufacturing strategy, since not all industries will contribute to raising the income bar, nor do they enjoy the same growth prospects. Still, the twenty-four provide one useful starting point for a manufacturing strategy in southern Minnesota.

Food and Agriculture

Southern Minnesota is an agricultural powerhouse. It produces a dominant share of the state’s corn, soybean, turkey, sugar beet, swine, and dairy output. This serves as the foundation for a plethora of value-added activities, which range from all manner of foods to ethanol to animal feed. This strong sector owes its strength not only to the unique productive assets of the region but also to the commanding knowledge and entrepreneurial spirit of its businesses. This business success has also created considerable wealth throughout the region, since it is home to a panoply of lo-cally owned cooperatives.

The competitive position of the region appears strong. The region is blessed with a unique combination of highly productive soils and favorable climate. As but one indicator of the combined

University of Missouri � Rural Policy Research Institute

�

8145.ƒƒ.indd 6 11/13/08 9:54:36 AM

Table 3. Established Clusters and Industry Composition

Cluster 2007 Jobs Earnings Per Worker

Projected US Growth 2007 - 2017

Nondurable Industry Machinery 7,751 $54,326 0.1%

Motor and Generator Mfg. 1,189 $69,407 -23.1%

Scale and Balance, (ex. Laboratory), Mfg. 446 $42,647 -18.9%

Food Product Machinery Mfg. 334 $95,019 -8.5%

Appliances 6,936 $47,998 3.1%

Current-Carrying Wiring Device Mfg. 1,069 $61,914 -23.0%

Heating Equipment, Ex. Warm Air Furnaces 682 $53,405 9.3%

AC, Refrigeration, and Forced Air Heating 638 $64,146 5.9%

Wood Building Products 5,840 $45,987 2.3%

Prefabricated Wood Building Mfg. 313 $28,500 15.4%

Truss Mfg. 264 $34,779 30.6%

Wood Window and Door Mfg. 261 $49,865 17.1%

Concrete, Brick Building Products 4,995 $41,227 4.9%

Ready-Mix Concrete Mfg. 692 $49,494 6.4%

Cut Stone and Stone Product Mfg. 203 $37,542 33.6%

Concrete Block and Brick Mfg. 201 $53,826 14.9%

Wood Products & Furniture 3,470 $39,589 1.8%

Wood Kitchen Cabinet and Countertop Mfg. 1,179 $32,178 14.5%

Institutional Furniture Mfg. 818 $48,506 0.8%

Wood Office Furniture Mfg. 491 $37,071 -0.2%

Rubber Products 3,396 $49,479 4.6%

All Other Miscellaneous Mfg. 883 $42,845 11.6%

Sporting and Athletic goods Mfg. 808 $42,006 -17.5%

Gasket, Packing and Sealing Device Mfg. 209 $63,046 3.5%

Breweries & Distilleries 3,378 $40,695 8.9%

Fruit and Vegetable Canning 2,613 $41,058 -4.1%

Soft Drink Mfg. 283 $50,054 1.4%

Breweries 164 $42,661 -4.8%

Glass Productions 2,806 $47,670 4.5%

Glass Product Mfg. Made of Purchased Glass 2,008 $53,486 6.9%

Metal Coating and Non-Precious Engraving 461 $35,448 12.7%

Electroplating, Anodizing, & Coloring Metal 156 $27,522 -17.5%

�

University of Missouri � Rural Policy Research Institute

strength, the state’s share of the nation’s corn and soybean crops has risen steadily over the past 30 years, and now stands at about 10 percent. A dominant portion of state production of both crops happens in the 38-county region.

The food and agriculture sector seems likely to remain strong go-ing forward, but there are two dilemmas that must be addressed. The first is ongoing consolidation in farming. Technology has made it possible to keep expanding commercial scale farms to the

point where many now top several thousand acres of production. This trend shows no signs of abating any time soon, and the recent peaks in commodity prices will only spur a new round of techno-logical advance. An exodus of young people from farming areas of the region was a common refrain in the local roundtables.

The second dilemma involves questions about how best to capture greater value in food manufacturing, opening new pathways to boosting income in the region. Southern Minnesota’s packaged

8145.ƒƒ.indd 7 11/13/08 9:54:36 AM

food cluster is highly competitive, but wages in many segments fall below the average earnings for the region as a whole. There may be no easy answer to this conundrum, since the food processing is the natural complement to the abundant farm production.

Still, there may be ways to raise the bar. Consumer demand is growing for locally grown food products with special traits (such as organic). The Twin Cities represents a high concentration of con-sumers willing to pay for such traits. There are signs of new firms emerging to capture these new markets, but the activity appears scattered thus far. One way forward may be to aim for a regional brand that could not only command value in the marketplace but also complement the desire of many to bolster the region’s attrac-tion to tourists. Many regions around the world have discovered powerful synergies between the two—Tuscany and Napa Valley are two premier examples.

Health Care

The health care sector has a large and recognized footprint in southern Minnesota. It employs nearly 100,000 workers in the region, nearly 30,000 more than would be the case if the regional economy looked just like the nation. Beyond its sheer size, though, health care is a real source of pride to regional leaders, with Mayo Clinic at the forefront. They also understand how critical it is to providing the quality of life necessary to attract the creative talent necessary to an economic future where innovation and entrepreneurship will be the drivers.

Somewhat surprisingly, quantitative data would suggest the region’s basic health services merely holds par in terms of its competitive position. Put another way, the cluster’s overall index is roughly 1, which means no more or no less competitive than the nation. Such numbers, of course, cannot capture the quality

Projected Change in Employment (over 2007–2017 period)

Clus

ter L

Q

Chart 3: Projected Change in Employment (over 2007–2017 period)

University of Missouri � Rural Policy Research Institute

8145.ƒƒ.indd 8 11/13/08 9:54:37 AM

of the region’s medical institutions. In those terms the region is in a much stronger position, led by Mayo and other high-caliber health care institutions. One proof of this lies in various measures of innovation, such as patents per capita. These are extremely high relative to the nation in Rochester, for instance, one clear indica-tion of competitive strength in health care. There also appears to be an uncommonly effective linkage between higher education and the health care industry that ensures ongoing access to skilled health care workers.

The real question is, “How can the region capture more economic benefit from its high quality health care sector?” The institutions provide high-paying jobs, which earn often greater than the aver-age for the region. Leaders wonder how to further leverage what they all agree is a significant asset.

One option is to consider how to grow elder care in the region. The population of southern Minnesota itself is aging. That will create more demand for elder care. But the region also has the capacity to attract others to its elder care facilities. An enduring core value across the region is to honor seniors and provide loving care. Combining this with the outstanding health care already in the region could be a powerful synergy, but one that likely takes more explicit business partnerships.

Renewable Energy

Southern Minnesota has a clear footprint in renewable energy, but leaders in the region believe that is only the beginning. The region was an early participant in corn ethanol, and now boasts 16 plants. Wind turbines have been a more recent addition, but are multiply-ing across the prairie, especially in western reaches of the region.

There are clear strengths on which to build, but overall they are

small and scattered at present. Ethanol plants are highly capital-intensive and employ comparatively few employees (though wages are high on average). The region is attracting some companies involved in making wind turbine components, and many compa-nies are springing up to maintain the growing number of turbines. Last but not least, landowners across the region are reaping new dividends, though the size of these appears to be somewhat vari-able owing to the fact that the industry represents a new frontier for buyers and sellers.

The region appears to have three strategic options with renewable energy.

• Corn ethanol. The region has a big stake here, but the future appears more uncertain than a few years ago. Many of the factors driving the industry may be beyond the region’s control. New attempts to regulate carbon may disadvantage corn-based ethanol. Corn prices may trade in a higher range in the future than in the past, making industry economics more challenging.

• Cellulosic ethanol. New technologies could open new opportunities even as corn becomes less certain. The region’s industry knowledge may give it a competitive edge in cellulosic feedstock, and the region has great potential to produce biomass, at least some of which could complement the abundant crops already grown.

• Wind. The region enjoys some of the best wind patterns in the nation. And the potential for additional generation is great. Minnesota’s “25% by 2025” legislation only increases the opportunity. The real problem is transmission capacity. By speaking with one voice, the region may be able to influ-ence the location and access to these new lines.

University of Missouri � Rural Policy Research Institute

8145.ƒƒ.indd 9 11/13/08 9:54:40 AM

Bioscience

Southern Minnesota is just beginning to tap its incredible poten-tial in bioscience. Regional leaders all agree the region has impres-sive assets to power future growth—world class medical research, deep expertise in the life sciences, and the agricultural powerhouse described above. The real challenge is connecting these assets in creative ways to capture explosive growth in new markets for bioscience products, whether for new pharmaceutical therapeutics, nutraceutical foods, or just more productive crops or livestock.

To a considerable extent, these economic synergies are being enabled by a powerful convergence in research on human health, animal health, and plant science. Scientists are unlocking the power of DNA, but in the process are also discovering the benefits of thinking across humans, animals, and plants. For instance, genetic therapies that combat the effects of cystic fibrosis can now be produced by inserting new genetic code into plants such as corn or barley. This is not merely a scientific wonder, it turns out that producing the enzymes in plants is far cheaper than in traditional bio-reactors.

The region has powerful research assets that address all three legs of the bioscience triangle. Mayo Clinic has vast scope and an annual research budget topping $700 million. The Hormel Institute is a widely recognized cancer research center, and it leverages partner-ships with both Mayo and the University of Minnesota. South-

west Minnesota has strong clusters of research on plant genetics and animal health. The Southern Research and Outreach Center focuses on agricultural innovation in the region and represents another University of Minnesota research arm in the region.

The real question is whether this impressive list of research can be translated into new economic opportunity within the region. The key, it seems, is creating new partnerships that bring all three legs of the bioscience triangle together with the crop and livestock producers who could produce new horizon bioscience products. Such partnerships are only now beginning to emerge in southern Minnesota. To succeed, the discussions will require engagement from more than just the research organizations and farm groups already mentioned. Growing new bio-science products in the region holds far-reaching implications. Thus, it will also be criti-cal to engage rural development organizations, consumer groups, state regulators, and environmental groups. Project partners have already begun to launch such discussions. A highly productive first meeting was held November 5 in Rochester.

Creating a new bio-science industry in southern Minnesota will not be easy, but the potential is staggering. Success will rest on building consensus answers to the following questions:

• Which therapeutic or disease-preventing plants could be grown in the region?

• Which therapeutic proteins could be grown in plants?

• Which crops in the region are best suited for this purpose?

• What are the production protocols under which the plants could be grown?

• What is the business ownership structure to maximize the win for everyone in the region?

High Technology

Southern Minnesota has a major presence in “high technology,” although the meaning of that term varies. In addition to the bio-science research described above, the region also has a strong cluster of information technology businesses, many involved in the manufacture of precision products. Experts disagree on exactly

University of Missouri 10 Rural Policy Research Institute

8145.ƒƒ.indd 10 11/13/08 9:54:41 AM

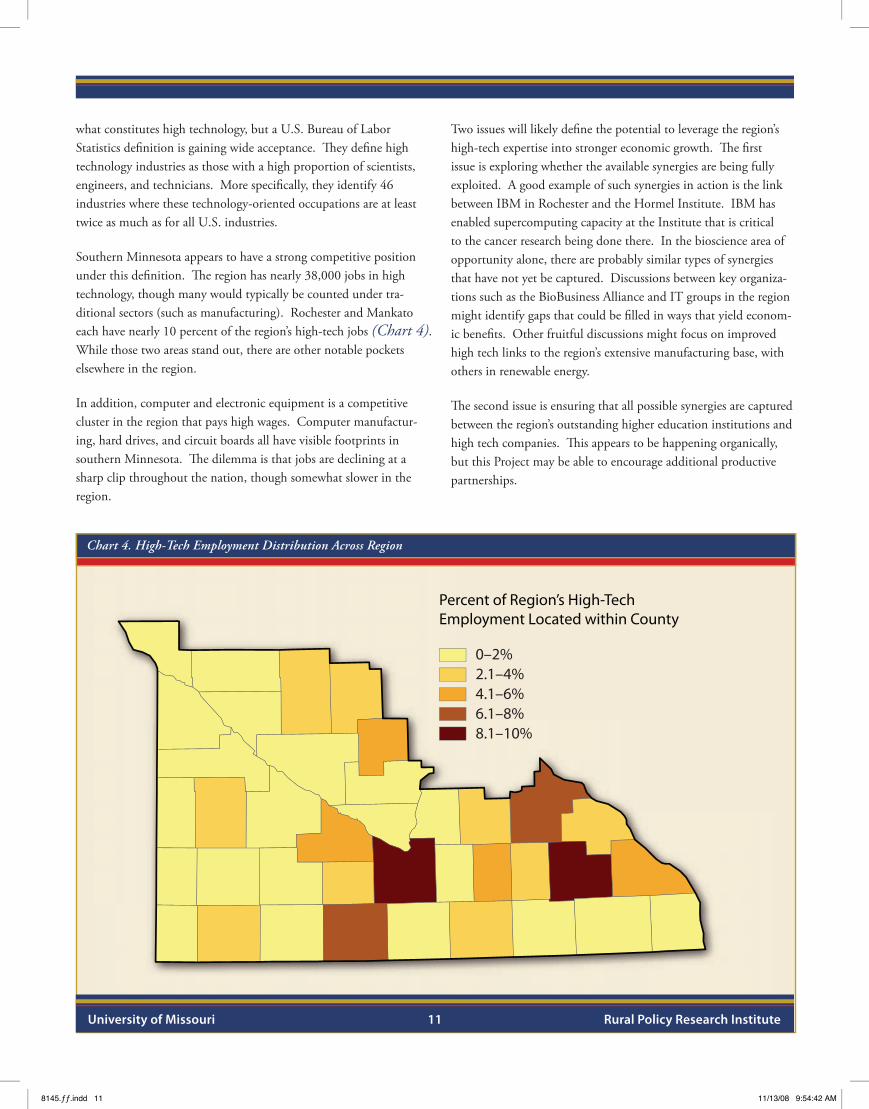

what constitutes high technology, but a U.S. Bureau of Labor Statistics definition is gaining wide acceptance. �ey define high technology industries as those with a high proportion of scientists, engineers, and technicians. More specifically, they identify 46 industries where these technology-oriented occupations are at least twice as much as for all U.S. industries.

Southern Minnesota appears to have a strong competitive position under this definition. �e region has nearly 38,000 jobs in high technology, though many would typically be counted under tra-ditional sectors (such as manufacturing). Rochester and Mankato each have nearly 10 percent of the region’s high-tech jobs (Chart 4). While those two areas stand out, there are other notable pockets elsewhere in the region.

In addition, computer and electronic equipment is a competitive cluster in the region that pays high wages. Computer manufactur-ing, hard drives, and circuit boards all have visible footprints in southern Minnesota. �e dilemma is that jobs are declining at a sharp clip throughout the nation, though somewhat slower in the region.

Two issues will likely define the potential to leverage the region’s high-tech expertise into stronger economic growth. �e first issue is exploring whether the available synergies are being fully exploited. A good example of such synergies in action is the link between IBM in Rochester and the Hormel Institute. IBM has enabled supercomputing capacity at the Institute that is critical to the cancer research being done there. In the bioscience area of opportunity alone, there are probably similar types of synergies that have not yet be captured. Discussions between key organiza-tions such as the BioBusiness Alliance and IT groups in the region might identify gaps that could be filled in ways that yield econom-ic benefits. Other fruitful discussions might focus on improved high tech links to the region’s extensive manufacturing base, with others in renewable energy.

�e second issue is ensuring that all possible synergies are captured between the region’s outstanding higher education institutions and high tech companies. �is appears to be happening organically, but this Project may be able to encourage additional productive partnerships.

Percent of Region’s High-Tech Employment Located within County

0–2%2.1–4%4.1–6%6.1–8%8.1–10%

Chart 4. High-Tech Employment Distribution Across Region

University of Missouri 11 Rural Policy Research Institute

8145.ƒƒ.indd 11 11/13/08 9:54:42 AM

About the Center The Center for Regional Competitiveness (CRC) is the coach expressly created to help regions pull together the pieces of a winning strategy.

The Center was formed at the University of Missouri in the fall of 2006 to provide the tools and analytics regions need to successfully compete in the global economy. The Center’s vision grew out of recognition among experts that many, if not most, regions are ill-prepared for the global economic race. The Center is one of the nation’s premier regional economic strategy organizations. Our approach is to balance world class regional analytics with dialogue within the region to both strengthen regional partnerships and to reveal critical economic assets.

Conclusions

Southern Minnesota is in a favored position to frame its economic future.

It has an abundance of distinctive assets on which its already vibrant economy is built. Regional leaders, though, realize the region can do better, especially with promising new markets for renewable energy and bioscience on the horizon. They are further motivated by the competitive pressures from global markets that pressure farmers and factory owners. Finally, they realize that outmigration and a downward trend in incomes relative to the rest of the state are concerns that must be met.

Manufacturing, health care, and food and agriculture will likely remain mainstays for southern Minnesota for the foreseeable future.

The region has staying power in all three, and analysis suggests that the region owns a competitive edge in all three. That said, the food processing segment and the middle third of manufacturing will both be pressured by global competition, and regional leaders may focus more intently on industries that can raise the bar in terms of income.

Renewable energy and bioscience both hold tantalizing upside for southern Minnesota.

High energy prices will continue to unlock the economic value of wind power and ethanol, whether corn or cellulosic. The key is strengthening synergies across this nascent cluster and building the transmission lines to export the energy. Bioscience can capture the power of converging life sciences while connecting the region’s prowess in research and agricultural production. No other region has mastered the synergies required to do this, but perhaps no other region is better positioned to do so than southern Minnesota.

University of Missouri 1� Rural Policy Research Institute

Center for Regional Competitiveness

Mark Drabenstott, Director [email protected] Moore, Research Analyst [email protected] Ojanen, Research Analyst [email protected]

8145.ƒƒ.indd 12 11/13/08 9:54:43 AM