united states bankruptcy court central … states bankruptcy court central district of ... i...

TRANSCRIPT

1

UNITED STATES BANKRUPTCY COURT

CENTRAL DISTRICT OF CALIFORNIA

In re

DWIGHT M. BOLDEN,

Debtor.

Case No. LA 04-29732 TD

Chapter 7

MEMORANDUM OF DECISIONRE TRUSTEE’S MOTION FOR

AVOIDANCE AND TURNOVER OF TAXPENALTY LIENS AND DEBTOR’S

MOTION FOR ABANDONMENT

DATE: June 1, 2005 TIME: 10:30 a.m. PLACE: Courtroom 1345

INTRODUCTION

On April 6, 2005, I announced my tentative decisions in two matters in Dwight M.

Bolden’s (Mr. Bolden) chapter 7 case. The first matter was the chapter 7 trustee’s

(trustee) motion for turnover of real property, Mr. Bolden’s home. The second matter

was Mr. Bolden’s motion to compel the chapter 7 trustee to abandon real property, Mr.

Bolden’s home. After hearing oral argument, the hearings were continued to May18,

2005, and on May 18, 2005, the hearings were continued again to June 1, 2005. At the

June 1 hearings, I withdrew my April 6 tentative decisions and announced my final

rulings. This memorandum will supplement my findings of fact and conclusions of law

announced orally on June 1.

2

FACTS

Mr. Bolden filed a voluntary chapter 7 bankruptcy petition on September 14,

2004. At the time of filing, Mr. Bolden listed in his schedules $587,875 in assets

($570,000 in real property and $17,875 in personal property), and $585,895.09 in

liabilities ($570,000 in secured claims and $15,895.09 in unsecured, non-priority

claims). In schedule I, Mr. Bolden states that he is self-employed by the Law Offices of

Bolden & Martin (Bolden & Martin), where Mr. Bolden has been employed for 15 years.

Mr. Bolden’s current monthly income is $4,000. Mr. Bolden’s statement of financial

affairs states that as of September 29, 2004, his income for the year to date was

$43,258.50. Mr. Bolden further states that his yearly income in 2002 was $57,678, and

that he received no income in 2003. In schedule J, Mr. Bolden indicates that his current

monthly expenditures are $4,425.

Mr. Bolden’s main asset is his residence, located at 5641 Sherbourne Drive in

Los Angeles (the property). The property contains a 4 bedroom, 4 bathroom, 3,034

square foot house on a 9,250 square foot lot. The house was built in 1959. The house

has an attached garage, central heating and air, a fireplace, and a private pool. The

trustee listed the house for sale on January 17, 2005, for $924,500 .

Mr. Bolden valued the property at $570,000 on schedule A. Schedule D

indicates that there are three secured claims against the property: (1) a 1989 first deed

of trust held by Cenlar Mortgage (Cenlar) in the amount of $285,000, (2) an Internal

Revenue Service (IRS) tax lien in the amount of $285,000; and (3) a California

Franchise Tax Board tax lien listed in an “unknown” amount.

3

The evidence shows that the IRS has eight secured tax liens against the property

totaling $1,324,632.52, comprised of $450,672.75 in unpaid taxes, $249,022.93 in

penalties, and $624,936.84 in interest. Each secured tax lien was recorded on a

different date, with respect to different taxes owed, and with its own priority. All of the

secured tax claims are for unpaid income taxes. The secured tax liens relate to the

following tax years: 1989; 1990; 1993-1995; and 1999-2001. The secured tax liens

were assessed on the following dates: December 12, 1994; September 14, 1992; March

13, 1995; May 27, 1996; December 15, 1997; April 28, 2003; May 5, 2003; and April 14,

2003, respectively. The IRS filed one proof of claim in this case to cover its eight

separate tax liens.

The property also is subject to unsecured priority tax claims held by the IRS in

the total sum of $537,369.60. Mr. Bolden’s Schedule E acknowledges delinquent taxes

for 2002 and 2003 owed to both the IRS and the Franchise Tax Board in “unknown”

amounts. The evidence provided by the IRS indicates that these taxes were assessed

in 1999-2003 and relate to the 1998-2003 tax periods, for income, FICA, and FUTA

taxes.

The IRS also asserts unsecured general claims against Mr. Bolden totaling

$940,773.45, for income, FICA, and FUTA taxes for 1994 and 1999-2003.

Additionally, as of December 27, 2004, Bolden & Martin owed the California

Employment Development Department (EDD) $213,296.63 in unpaid taxes. The EDD

filed a notice of state tax lien against Bolden & Martin as a result of its failure to pay its

state tax liability.

The penalty portions of the IRS secured tax liens total $339,272.

4

On Schedule C, Mr. Bolden claimed a $50,000 homestead exemption pursuant

to California Code of Civil Procedure § 704.730(a)(1). The trustee has not objected to

this exemption. Mr. Bolden now claims that he is entitled to a $75,000 homestead

exemption, but he has not yet amended his schedules to reflect this change.

Mr. Bolden has refused to cooperate with the trustee’s efforts to sell the property.

Four property visits were scheduled for potential buyers. On February 4, 2005, the

trustee’s broker, Ron Bombiger, advised Mr. Bolden’s attorney by fax of a property visit

scheduled for February 5, 2005, at 11:00 a.m. On the same day, the trustee’s broker

advised Mr. Bolden’s attorney by fax of additional property visits scheduled for (1)

February 8 at 5:00 p.m.; (2) February 10 at 5:00 p.m.; and (3) February 12 at 11:00 a.m.

Mr. Bolden’s attorney responded to the first notice by stating that he was unable to

contact Mr. Bolden and that the broker’s 24-hour notice was “stupid and rude.” In

response to the second notice, Mr. Bolden’s attorney left a telephone message for the

trustee’s attorney stating that discussions with Mr. Bolden were underway regarding

making the property available for prospective buyers’ visits. Mr. Bolden did not make

the property available for buyers’ visits on the scheduled dates. A “For Sale” sign was

placed on the property by the trustee’s broker on February 7, 2005. Mr. Bolden

apparently removed the “For Sale” sign from the property. Due to Mr. Bolden’s lack of

cooperation, the trustee’s real estate broker has not had reasonable access to the

property to facilitate the trustee’s efforts to sell the property.

Mr. Bombiger’s telephone log shows that between January 25, 2005, and

February 16, 2005, 41 people called to inquire about the property. These people

required an interior viewing of the property before deciding whether to submit a

1 Unless otherwise indicated, all chapter and section references are to theBankruptcy Code, 11 U.S.C. §§101-1330, and all rule references are to the FederalRules of Bankruptcy Procedure, Rules 1001-9036. Section 554(b) states:

On request of a party in interest and after notice and a hearing, the court mayorder the trustee to abandon any property of the estate that is burdensome to theestate or that is of inconsequential value and benefit to the estate.

Rule 6007(b) states:

A party in interest may file and serve a motion requiring the trustee or debtor inpossession to abandon property of the estate.

5

purchase offer to the trustee. On February 17, 2005, the trustee’s real estate broker

received a written offer to purchase the property for $975,000. The offer was made

subject to inspection of the property.

On February 18, 2005, the trustee filed a motion for turnover of the property. On

March 14, 2005, Mr. Bolden filed a motion to compel the trustee to abandon the

property. On April 6, 2005, the IRS filed a memorandum in support of the trustee’s

motion for turnover of the property. On May 13, 2005, Cenlar filed a joinder to the

trustee’s motion for turnover of the property and in opposition to Mr. Bolden’s motion to

compel abandonment.

DISCUSSION

A. Mr. Bolden’s Motion for Abandonment

Mr. Bolden opposes the trustee’s turnover motion, and pursuant to 11 U.S.C. §

554(b) and Federal Rule of Bankruptcy Procedure 6007(b), Mr. Bolden seeks an order

compelling the trustee to abandon the property.1 Section 554(b) requires the court to

find that the property to be abandoned is either burdensome or of inconsequential value

and benefit to the estate.

2 At this time, Mr. Bolden has claimed a $50,000 homestead exemption, not a$75,000 exemption. Mr. Bolden states that he will be claiming a $75,000 homesteadexemption and bases his analysis on the anticipated homestead exemption.

6

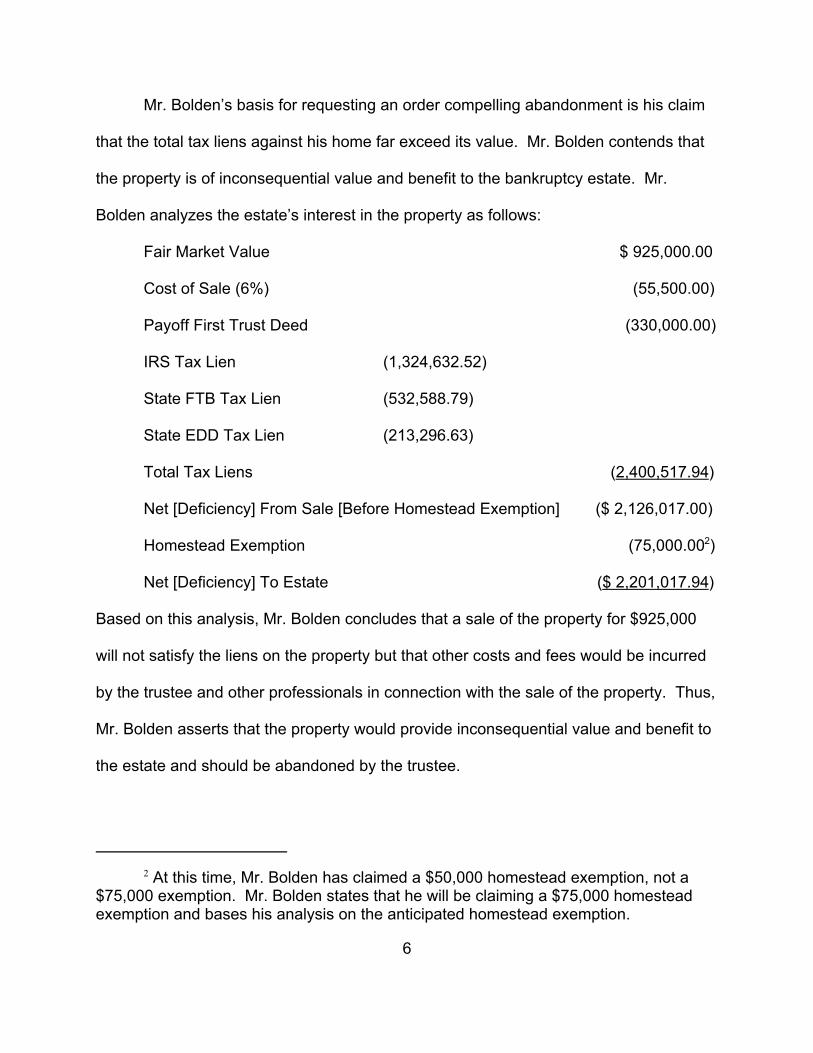

Mr. Bolden’s basis for requesting an order compelling abandonment is his claim

that the total tax liens against his home far exceed its value. Mr. Bolden contends that

the property is of inconsequential value and benefit to the bankruptcy estate. Mr.

Bolden analyzes the estate’s interest in the property as follows:

Fair Market Value $ 925,000.00

Cost of Sale (6%) (55,500.00)

Payoff First Trust Deed (330,000.00)

IRS Tax Lien (1,324,632.52)

State FTB Tax Lien (532,588.79)

State EDD Tax Lien (213,296.63)

Total Tax Liens (2,400,517.94)

Net [Deficiency] From Sale [Before Homestead Exemption] ($ 2,126,017.00)

Homestead Exemption (75,000.002)

Net [Deficiency] To Estate ($ 2,201,017.94)

Based on this analysis, Mr. Bolden concludes that a sale of the property for $925,000

will not satisfy the liens on the property but that other costs and fees would be incurred

by the trustee and other professionals in connection with the sale of the property. Thus,

Mr. Bolden asserts that the property would provide inconsequential value and benefit to

the estate and should be abandoned by the trustee.

3 Section 724(b) states:

Property in which the estate has an interest and that is subject to a lien that is notavoidable under this title and that secures an allowed claim for a tax, or proceedsof such property, shall be distributed -- (1) first, to any holder of an allowed claim secured by a lien on such propertythat is not avoidable under this title and that is senior to such tax lien;(2) second, to any holder of a claim of a kind specified in section 507(a)(1),507(a)(2), 507(a)(3), 507(a)(4), 507(a)(5), 507(a)(6), or 507(a)(7) of this title, tothe extent of the amount of such allowed tax claim that is secured by such taxlien;(3) third, to the holder of such tax lien, to any extent that such holder’s allowedtax claim that is secured by such tax lien exceeds any amount distributed underparagraph (2) of this subsection;(4) fourth, to any holder of an allowed claim secured by a lien on such propertythat is not avoidable under this title and that is junior to such tax lien;(5) fifth, to the holder of such tax lien, to the extent that such holder’s allowedclaim secured by such tax lien is not paid under paragraph (3) of this subsection;and(6) sixth, to the estate.

7

Mr. Bolden suggests the following as his expected order of distribution of sale

proceeds, as prescribed by § 724(b)3, should the property be turned over to the trustee

and sold: (1) Cenlar’s deed of trust; (2) Mr. Bolden’s homestead exemption; (3)

administrative claims; and (4) tax claims secured by liens. According to Mr. Bolden, the

distribution scheme he envisions would satisfy only a small portion of the secured debt

and leave nothing for unsecured creditors. Based on his analysis, Mr. Bolden

concludes that the property is of little, no, or even negative value to the estate, and the

trustee should be ordered to abandon it.

B. Trustee’s Motion for Turnover

The trustee contends that Mr. Bolden makes two errors in his analysis.

According to the trustee, Mr. Bolden first incorrectly lumps the eight IRS tax liens

together as if they were a single secured claim against the property, and secondly, Mr.

8

Bolden assumes incorrectly that his homestead exemption claim will be paid prior to

avoided liens.

The trustee notes that there are eight tax liens, each recorded on a different date,

each respecting different taxes owed, and each with its own priority in relation to other

liens. The evidence here confirms that the tax liens constitute separate liens, not a

single blanket lien and that there are eight separate and distinct IRS secured tax liens,

each with its own priority, for eight separate and distinct tax years.

The trustee and the IRS persuasively argue that the avoided tax liens will come

ahead of Mr. Bolden’s homestead exemption for purposes of distribution. It is true, as

Mr. Bolden argues, that the trustee cannot contest the validity of a claimed exemption

after the 30-day period for objecting has expired and no extension has been obtained,

even if a debtor has no colorable basis for the exemption, citing Taylor v. Freeland &

Kronz, 503 U.S. 638, 112 S.Ct. 1644 (1992). Mr. Bolden claimed a $50,000 homestead

exemption on his Schedule C. The trustee did not object to the homestead exemption

claim within the 30-day period allowed following the conclusion of the creditors meeting.

Pursuant to Rule 4003(b) and the holding in Taylor v. Freeland & Kronz, an objection at

this time would be time-barred, and the $50,000 exemption claimed by Mr. Bolden at

the outset would be allowed whether or not Mr. Bolden had a colorable statutory basis

for claiming it. On the other hand, the trustee can contest the priority of the exemption

with respect to competing liens. The basic rule of “first in time, first in right” is used to

determine the priority of competing liens. United States v. City of New Britian, 347 U.S.

81 (1954).

4 Section 522(c)(2) states in pertinent part:

Unless the case is dismissed, property exempted under this section is not liableduring or after the case for any debt of the debtor that arose . . . before thecommencement of the case, except – * * *(2) a debt secured by a lien that is – (A) (i) not avoided under subsection (f) or (g) of this section . . . ; and (ii) not voidunder section 506(d) of this title . . . ; or(B) a tax lien, notice of which is properly filed . . . .

9

Pursuant to § 522(c)(2), exempt property, such as that represented by Mr.

Bolden’s homestead exemption claim, remains liable for debts secured by a lien that is

not avoided or for which a notice of such things as a federal tax lien has been filed.4

The homestead exemption does not have precedence over the tax liens. Generally, a

debtor is not entitled to claim a homestead exemption on property that is subject to an

IRS levy. Treas. Reg. on Proc. and Admin. § 301.6334-1(c); United States v. Estes,

450 F.2d 62, 65 (5th Cir. 1971); Davenport v. United States, 136 B.R. 125, 127-28

(Bankr. W.D. Ky. 1991) (a state-created homestead exemption is ineffective against a

federal tax lien, but the proceeds of a sale of property are subject to a valid tax lien

under § 522).

It has been recognized that the IRS has its own exemption scheme and that a

“[state] homestead exemption does not erect a barrier around a taxpayer’s home sturdy

enough to keep out the Commissioner of Internal Revenue.” United States v. Estes,

450 F.2d at 65 (no provision of a state’s law may exempt property or rights in property

from levy for the collection of federal taxes owed). The Supreme Court has concluded

that the Supremacy Clause allows the federal government to “sweep aside state-

created exemptions.” United States v. Rodgers, 461 U.S. 677, 701 (1983).

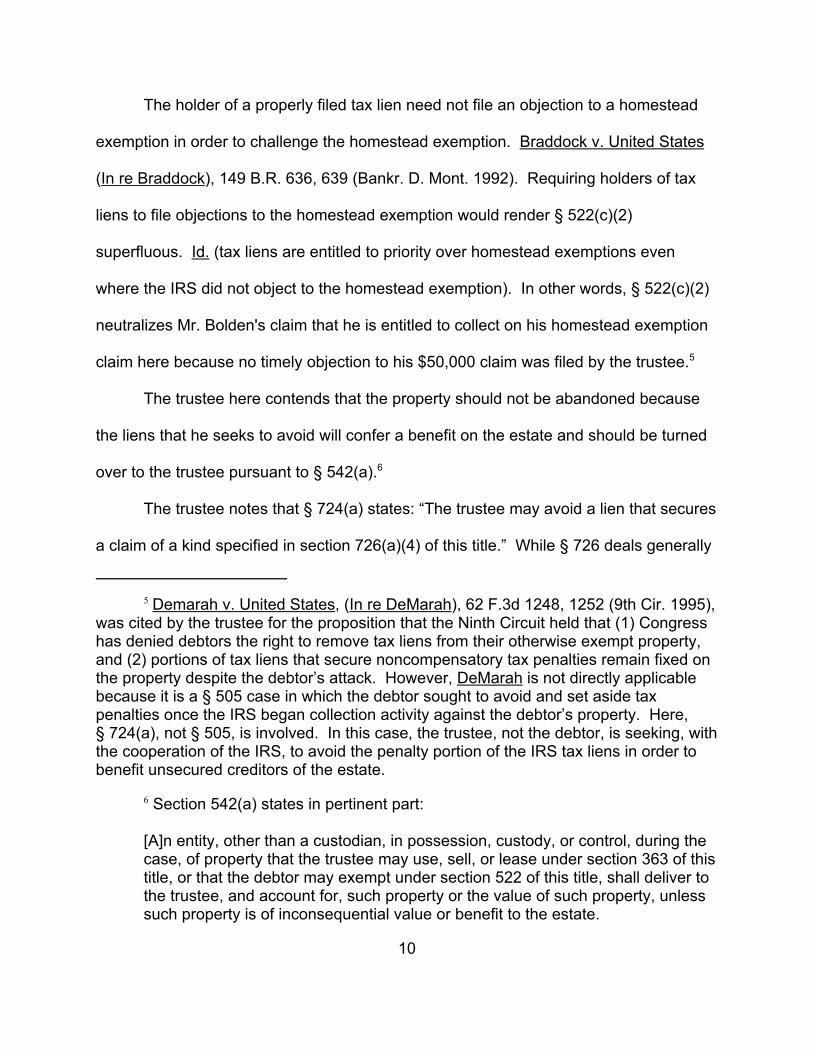

5 Demarah v. United States, (In re DeMarah), 62 F.3d 1248, 1252 (9th Cir. 1995),was cited by the trustee for the proposition that the Ninth Circuit held that (1) Congresshas denied debtors the right to remove tax liens from their otherwise exempt property,and (2) portions of tax liens that secure noncompensatory tax penalties remain fixed onthe property despite the debtor’s attack. However, DeMarah is not directly applicablebecause it is a § 505 case in which the debtor sought to avoid and set aside taxpenalties once the IRS began collection activity against the debtor’s property. Here, § 724(a), not § 505, is involved. In this case, the trustee, not the debtor, is seeking, withthe cooperation of the IRS, to avoid the penalty portion of the IRS tax liens in order tobenefit unsecured creditors of the estate.

6 Section 542(a) states in pertinent part:

[A]n entity, other than a custodian, in possession, custody, or control, during thecase, of property that the trustee may use, sell, or lease under section 363 of thistitle, or that the debtor may exempt under section 522 of this title, shall deliver tothe trustee, and account for, such property or the value of such property, unlesssuch property is of inconsequential value or benefit to the estate.

10

The holder of a properly filed tax lien need not file an objection to a homestead

exemption in order to challenge the homestead exemption. Braddock v. United States

(In re Braddock), 149 B.R. 636, 639 (Bankr. D. Mont. 1992). Requiring holders of tax

liens to file objections to the homestead exemption would render § 522(c)(2)

superfluous. Id. (tax liens are entitled to priority over homestead exemptions even

where the IRS did not object to the homestead exemption). In other words, § 522(c)(2)

neutralizes Mr. Bolden's claim that he is entitled to collect on his homestead exemption

claim here because no timely objection to his $50,000 claim was filed by the trustee.5

The trustee here contends that the property should not be abandoned because

the liens that he seeks to avoid will confer a benefit on the estate and should be turned

over to the trustee pursuant to § 542(a).6

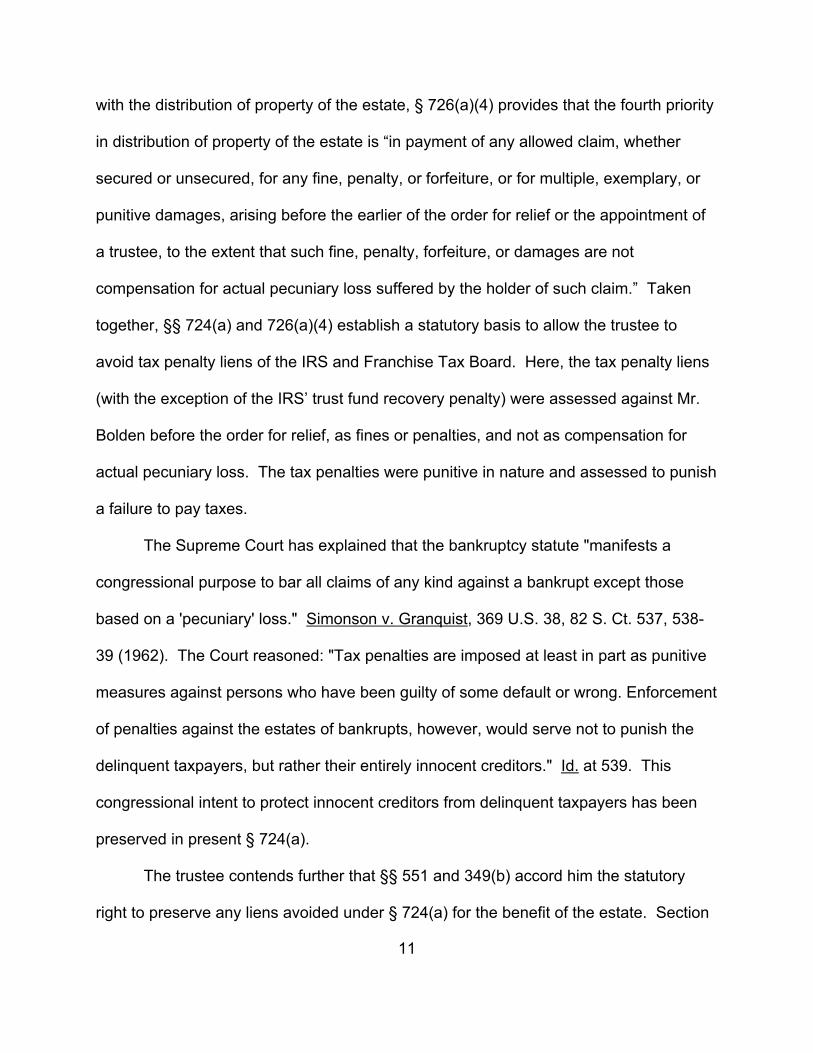

The trustee notes that § 724(a) states: “The trustee may avoid a lien that secures

a claim of a kind specified in section 726(a)(4) of this title.” While § 726 deals generally

11

with the distribution of property of the estate, § 726(a)(4) provides that the fourth priority

in distribution of property of the estate is “in payment of any allowed claim, whether

secured or unsecured, for any fine, penalty, or forfeiture, or for multiple, exemplary, or

punitive damages, arising before the earlier of the order for relief or the appointment of

a trustee, to the extent that such fine, penalty, forfeiture, or damages are not

compensation for actual pecuniary loss suffered by the holder of such claim.” Taken

together, §§ 724(a) and 726(a)(4) establish a statutory basis to allow the trustee to

avoid tax penalty liens of the IRS and Franchise Tax Board. Here, the tax penalty liens

(with the exception of the IRS’ trust fund recovery penalty) were assessed against Mr.

Bolden before the order for relief, as fines or penalties, and not as compensation for

actual pecuniary loss. The tax penalties were punitive in nature and assessed to punish

a failure to pay taxes.

The Supreme Court has explained that the bankruptcy statute "manifests a

congressional purpose to bar all claims of any kind against a bankrupt except those

based on a 'pecuniary' loss." Simonson v. Granquist, 369 U.S. 38, 82 S. Ct. 537, 538-

39 (1962). The Court reasoned: "Tax penalties are imposed at least in part as punitive

measures against persons who have been guilty of some default or wrong. Enforcement

of penalties against the estates of bankrupts, however, would serve not to punish the

delinquent taxpayers, but rather their entirely innocent creditors." Id. at 539. This

congressional intent to protect innocent creditors from delinquent taxpayers has been

preserved in present § 724(a).

The trustee contends further that §§ 551 and 349(b) accord him the statutory

right to preserve any liens avoided under § 724(a) for the benefit of the estate. Section

12

551 states in pertinent part: “Any transfer avoided under section . . . 724(a) of this title . .

. is preserved for the benefit of the estate but only with respect to property of the

estate.” Section 349(b) states in pertinent part: “Unless the court, for cause, orders

otherwise, a dismissal of a case other than under section 742 of this title -- (1) reinstates

-- ( ( ( (B) any transfer avoided under section . . . 724(a) of this title . . . .” Further,

Collier on Bankruptcy states that § 551 applies to § 724(a) dealing with fines, penalties,

and forfeitures. 5-551 Collier on Bankruptcy - 15th Edition Revised ¶ 551.01. Thus, I

conclude, that after avoiding the IRS tax penalty liens under § 724(a), the trustee has

the statutory right under §§ 551 and 349(b) to preserve the liens avoided for the benefit

of the estate.

Ultimately here, turnover of the property will confer a benefit on the estate

because the trustee will avoid what he estimates is $339,272 in tax penalties and

interest on tax penalties for the benefit of the estate, as follows:

7 $38, 582 ÷ ($38,582 + $70,565) x $170,656

8 $45, 532 ÷ ($45,532 + $54,770) x $159,779

9 $29, 901 ÷ ($29,901 + $61,676) x $93,824

10 $32, 902 ÷ ($32,902 + $62,871) x $84,015

13

IRS Lien

Recordation

Date

Total

Amount

Claimed

as a Lien

on

Petition

Date

Principal

Amount

of Taxes

Amount

of

Penalties

to

Petition

Date

Amount of

Interest to

Petition

Date/

Amount of

Interest

Attributed

to

Penalties

Amount

Avoided

and

Preserved

for Estate

(Penalties

+ Interest

on

Penalties)

Amount

Paid to

IRS on

Lien

Balance

Available for

Subsequent

Liens

2/12/93 $279,803 $70,565

(1990)

$38,582 $170,656/

$60,3257

$98,907 $180,896 $386,104

2/8/95 $260,081 $54,770

(1989)

$45,532 $159,779/

$72,5328

$118,064 $142,017 $244,087

7/11/95 $185,401 $61,676

(1995)

$29,901 $93,824/

$30,6359

$60,536 $124,865 $119,222

7/12/96 $179,788 $62,871

(1994)

$32,902 $84,015/

$28,86310

$61,765 $118,023 $1,199

The remaining four IRS tax liens listed on the IRS proof of claim are not included in the

above chart since the proceeds available from the sale of the property would be

exhausted by the first four liens recorded by the IRS. By avoiding the penalty portions

of the tax liens and preserving them for the benefit of the creditors, the estate is

enriched while the IRS still obtains the principal portion of its liens, with interest, in the

order and priority of each respective lien. At the same time, Mr. Bolden cannot use the

14

IRS' tax liens as a shield against the trustee's administration of the property for the

benefit of creditors. This is because, with respect to each lien avoided, the trustee

steps into the shoes of the lienholder, preserving for the estate the respective priority of

each lien. See In re Cavanaugh, 153 B.R. 224 (Bankr. N.D. Ill. 1993). The trustee “who

avoids an interest succeeds to the priority that interest enjoyed over competing

interests.” Retail Clerks Welfare Trust v. McCarty (In re Van de Kamp’s Dutch

Bakeries), 908 F.2d 517, 519 (9th Cir. 1990). Congress’ motivation for instituting this

provision was to “prevent junior lienholders from improving their position at the expense

of the estate when a senior lien is avoided.” Id.; See also Staats v. Barry (In re Barry),

31 B.R. 683 (Bankr. S.D. Ohio 1983); 5-551 Collier on Bankruptcy - 15th Edition

Revised ¶ 551.01.

The avoided tax penalties will be distributed according the distribution scheme

set forth in § 726.

1. What happens to the proceeds of a lien avoided under § 726(a)?

Section 726 provides the general distribution scheme for property of the estate.

Section 726(a) specifies in part that “property of the estate shall be distributed – (1) first,

in payment of claims of the kind specified in, and in the order specified in, section 507 of

this title, proof of which is timely filed under section 501 of this title or tardily filed before

the date on which the trustee commences distribution under this section.”

11 Section 507(a) states in pertinent part:

The following expenses and claims have priority in the following order: (1) First, administrative expenses allowed under section 503(b) of this title, andany fees and charges assessed against the estate under chapter 123 of title 28; * * *(3) Third, allowed unsecured claims . . . earned within 90 days before the date ofthe filing of the petition or the date of the cessation of the debtor’s business,whichever occurs first, for – (A) wages, salaries, or commissions . . . ; or (B) sales commissions earned by an individual or by a corporation with only 1employee . . . ; * * *(8) Eighth, allowed unsecured claims of governmental units; only to the extentthat such claims are for – (A) a tax on or measured by income or gross receipts – [as limited by subsection(i) -(iii)];* * *(C) a tax required to be collected or withheld and for which the debtor is liable inwhatever capacity; [or](D) an employment tax on a wage, salary, or commission . . . earned from thedebtor before the date of the filing of the petition . . . .

15

Section 507 sets forth priorities for distribution of expenses and claims.11 The

potentially relevant priorities under § 507(a) are as follows: (1) administrative expenses;

and (8) allowed unsecured claims of governmental units. According to the priorities set

forth under § 507, the administrative costs would be paid first. Section 507(a)(3) may

be irrelevant, as it deals with wage claims, and there is no evidence that Mr. Bolden has

employees or wage claims of employees to pay. The only other applicable priority is

§ 507(a)(8). Thus, it seems, the unsecured portions of the tax claims would be paid

second, after the administrative expense claims.

16

2. If there is a benefit to the estate, turnover to the trustee is appropriate

and the Debtor’s motion to compel abandonment should be denied.

Based on the distribution scheme of § 726(a)(1) and the trustee’s statutory right

under § 551 to preserve liens avoided under § 724(a) for the benefit of the estate, a sale

of the property will generate benefits to the estate in the form of significant anticipated

payments to unsecured priority creditors.

The fair market value of the property appears to be about $975,000 based on the

purchase offer received by the trustee on February 17, 2005. I assume a cost of sale of

about $78,000 (8% of $975,000). From the proceeds, Cenlar’s deed of trust in the

amount of about $330,000 would be paid. The net that would be realized from a sale of

the property, before tax liens, is about $567,000. The sale will be conducted free and

clear of the liens of the taxing agencies, with such liens to attach to the sale proceeds.

The liens would be paid from the sale proceeds, to the extent available. Pursuant to §§

724(a) and 551, the trustee would receive from the sale proceeds about $339,272 in

avoided tax penalties and avoided interest on tax penalties. This would allow the estate

to pay administrative claims and a dividend to unsecured priority claimants. First, under

§ 507(a)(1), administrative claims will be paid. Second, under § 507(a)(8) unsecured

claims of governmental units will be paid to the extent that such claims are for selected

taxable years and for a tax on or measured by income or gross receipts or required to

be collected or withheld and for which the debtor is liable. Unsecured, as well as

secured creditors, would receive payment from the proceeds of a sale of the property.

Thus, there is a benefit to the estate in allowing turnover of the property, avoidance of

the penalty portions of the tax liens for the benefit of the estate, and sale of the property.

17

Mr. Bolden’s request to compel the trustee to abandon the property should be

denied. The principal of abandonment was developed by the courts to protect

bankruptcy estates from the costs and burdens of administering property when such

adminstration could not conceivably benefit unsecured creditors of the estate. Justice

Rehnquist commented in his dissent from the majority opinion denying abandonment in

Midlantic Nat’l Bank v. New Jersey Dep’t of Envtl. Prot., 474 U.S. 494, 106 S.Ct. 755,

763 (1986) as follows: “[C]ourts . . . developed a rule permitting the trustee to abandon

property that was worthless or not expected to sell for a price sufficiently in excess of

encumbrances to offset the costs of administration. . . .” See Carey v. Pauline (In re

Pauline), 119 B.R. 727, 728 (9th Cir. BAP 1990) (citing In re Paolella, 79 B.R. 607, 609

(Bankr. E.D. Penn. 1987)).

As stated by the Court of Appeals for the Sixth Circuit, “An order compelling

abandonment is the exception, not the rule. Abandonment should only be compelled in

order to help the creditors by assuring some benefit in the administration of each asset.”

Morgan v. K.C. Machine & Tool Co. (In re K.C. Machine & Tool Co.), 816 F.2d 238, 246

(6th Cir. 1987). Where the benefits of administration exceed the costs of administration,

abandonment should not be compelled. Id. In K.C. Machine & Tool Co., the court

stated, “Absent an attempt by the trustee to churn property worthless to the estate just

to increase fees, abandonment should very rarely be ordered.” Id.

In Pauline, the Ninth Circuit Bankruptcy Appellate Panel upheld the bankruptcy

court’s decision requiring the trustee to find a buyer for the debtor’s home within 60

days at a price sufficient to satisfy all liens on the home plus the allowed amount of the

18

debtor’s homestead exemption, in the absence of which the debtor’s home would be

deemed abandoned. In re Pauline, 119 B.R. at 727. However, in Pauline, the Panel

affirmed the bankruptcy court decision in part, because (1) the IRS did not ask the

debtor to sell the property for the IRS’ benefit, and (2) the trustee apparently had

”engaged in . . . conduct designed to enhance the size of his bank account rather than

the size of the funds available for the Debtor’s unsecured creditors . . . .” Id. at 728.

Unlike in Pauline, (1) the IRS here supports the trustee’s turnover efforts and seeks a

sale of the property by the trustee, and (2) a sale will benefit unsecured priority

creditors, including the IRS, not just increase the fees paid to the trustee and his

professionals.

By contrast to the situation discussed by the Panel in Pauline, here, once the

trustee avoids $339,272 in penalty portions of the tax liens and sells the property, there

will be a material benefit to the estate. Abandonment is not proper here because the

property is not burdensome or of inconsequential benefit and value to the estate, as

required by § 554(b). Based on the inquiries and offers received by the trustee's broker,

the property should sell quickly once the trustee has access to the property. Real

estate commissions, legal fees, and other costs of administration that may total about

$90,000 will be offset by the excess value to the estate created by the sale. While the

trustee and his attorneys and broker will receive fees as a result of a sale of the

property, the fact that unsecured creditors will benefit significantly from a sale shows

that this is not an attempt by the trustee merely to increase his fees. The efforts of the

trustee and his professionals are necessary to value, market, and sell the property. The

property should be turned over to the trustee so that the estate can realize the benefits

19

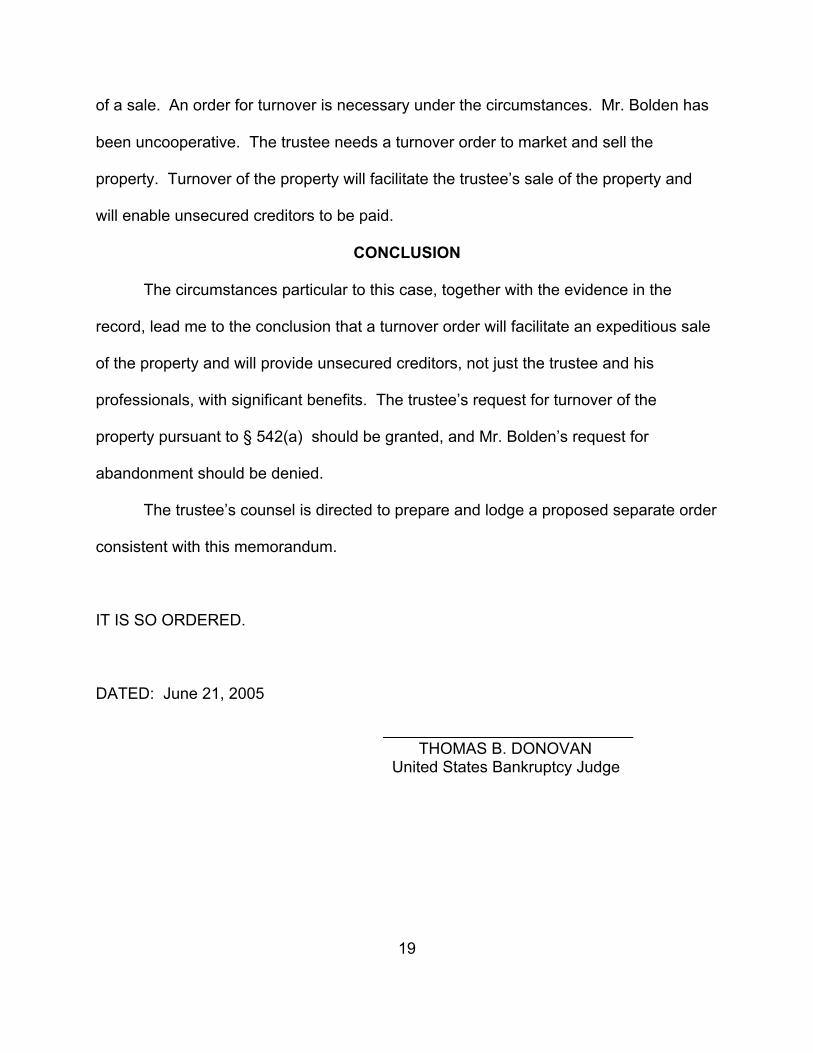

of a sale. An order for turnover is necessary under the circumstances. Mr. Bolden has

been uncooperative. The trustee needs a turnover order to market and sell the

property. Turnover of the property will facilitate the trustee’s sale of the property and

will enable unsecured creditors to be paid.

CONCLUSION

The circumstances particular to this case, together with the evidence in the

record, lead me to the conclusion that a turnover order will facilitate an expeditious sale

of the property and will provide unsecured creditors, not just the trustee and his

professionals, with significant benefits. The trustee’s request for turnover of the

property pursuant to § 542(a) should be granted, and Mr. Bolden’s request for

abandonment should be denied.

The trustee’s counsel is directed to prepare and lodge a proposed separate order

consistent with this memorandum.

IT IS SO ORDERED.

DATED: June 21, 2005

THOMAS B. DONOVAN United States Bankruptcy Judge