union vs. private pension plans - hudson institute

TRANSCRIPT

Union vs. Private Pension Plans:How Secure Are UnionMembers’ Retirements?

DIANA FURCHTGOTT-ROTHHudson Institute

Union vs. Private Pension Plans:

How Secure Are UnionMembers’ Retirements?

Diana Furchtgott-RothSenior Fellow, Hudson Institute

Summer 2008

HUDSONI N S T I T U T E

©2008 Hudson Institute

Hudson Institute is a nonpartisan policy research organization dedicated to innovative research and analy-sis that promotes global security, prosperity, and freedom. We challenge conventional thinking and helpmanage strategic transitions to the future through interdisciplinary and collaborative studies in defense,international relations, economics, culture, science, technology, and law. Through publications, conferences,and policy recommendations, we seek to guide global leaders in government and business. For more infor-mation about Hudson Institute, visit our website at www.hudson.org.

Hudson’s Center for Employment Policy is directed by Senior Fellow Diana Furchtgott-Roth. Its purpose isto explore fundamentally sound economic policies that could encourage economic growth and employmentcreation. Potential policies include legal reform, reduction in burdensome regulation, broader availability oflow-cost, portable fringe benefits, low levels of taxation, expansion of free trade, and immigration reform.Ms. Furchtgott-Roth is a weekly economics columnist for the New York Sun and the editor of the bookOvercoming Barriers to Entrepreneurship in the United States (Lexington Books, 2008). She received herB.A. in economics from Swarthmore College and her M.Phil. in economics from Oxford University. Formore information about the Center for Employment Policy, please visit www.emp.hudson.org.

This report was supported in part by funding from the U.S. Chamber of Commerce, which had no part inthe formulation of the study or the presentation of the results. The views expressed in the paper are those ofthe author alone, and do not necessarily reflect those of any other party. The author takes responsibility forall errors.

Table of Contents

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

What Are Pensions? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Trends in Pension Coverage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

Sources of Information on Pension Plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8

General Health of Pensions in the United States . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

Why Union Plans Tend to Perform More Poorly . . . . . . . . . . . . . . . . . . . . . . . . . . .12

Small Plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

Officer and Staff Pension Plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18

Pension Fund Politics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19

Six Case Histories . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

Service Employees International Union . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

The Sheet Metal Workers National Pension Fund . . . . . . . . . . . . . . . . . . . . . . . . . . .23

Teamsters’ Central States, SE and SW Areas Pension Plan . . . . . . . . . . . . . . . . . . .25

Plumbers and Pipefitters National Pension Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . .27

Laborers National Pension Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28

UNITE Here Fund Administrators Inc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29

Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30

Appendix I: How Do Pensions Work? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .32

Appendix II : Financial Changes Required

by the Pension Protection Act of 2006 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .34

References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35

Endnotes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36

List of Tables and Charts

Chart 1: Number of Pensions Plans Over Time . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

Chart 2: Number of Pension Plans Sponsored by Single Employers Over Time . . . . . . . . . . . . . . . . . . . . . . . . . . .7

Chart 3: Number of Pension Plans Sponsored by Multiple Employers Over Time . . . . . . . . . . . . . . . . . . . . . . . .7

Chart 4: Average Ratio of Asset to Liabilities for Large Defined Benefit Plans . . . . . . . . . . . . . . . . . . . . . . . . . . .9

Chart 5: Percent of Large Defined Benefit Plans That Are Fully Funded . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10

Chart 6: Percent of Large Defined Benefit Plans in Critical Condition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10

Chart 7: Percent of Underfunded Defined Plans Paying Minimum Annual Charges . . . . . . . . . . . . . . . . . . . . . .11

Chart 8: Percent of Plans in Critical Condition Paying At Least Minimum Annual Charge . . . . . . . . . . . . . . . .12

Chart 9: Percent of Defined Benefit Pensions Making Additional Contributions

Because of Funding Deficiency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13

Chart 10: Average Annual Payment to Correct Fund Deficiency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13

Chart 11: Percent of Underfunded Defined Benefit Plans Paying Minimum Annual Charges . . . . . . . . . . . . . . .15

Chart 12: Percent of Defined Benefit Pension Funds That Are Collectively Bargained . . . . . . . . . . . . . . . . . . . .16

Chart 13: Average Number of Participants in Small Defined Benefit Pension Plans . . . . . . . . . . . . . . . . . . . . . . .17

Chart 14: Average Number of Participants in Large Defined Benefit Pension Plans . . . . . . . . . . . . . . . . . . . . . .17

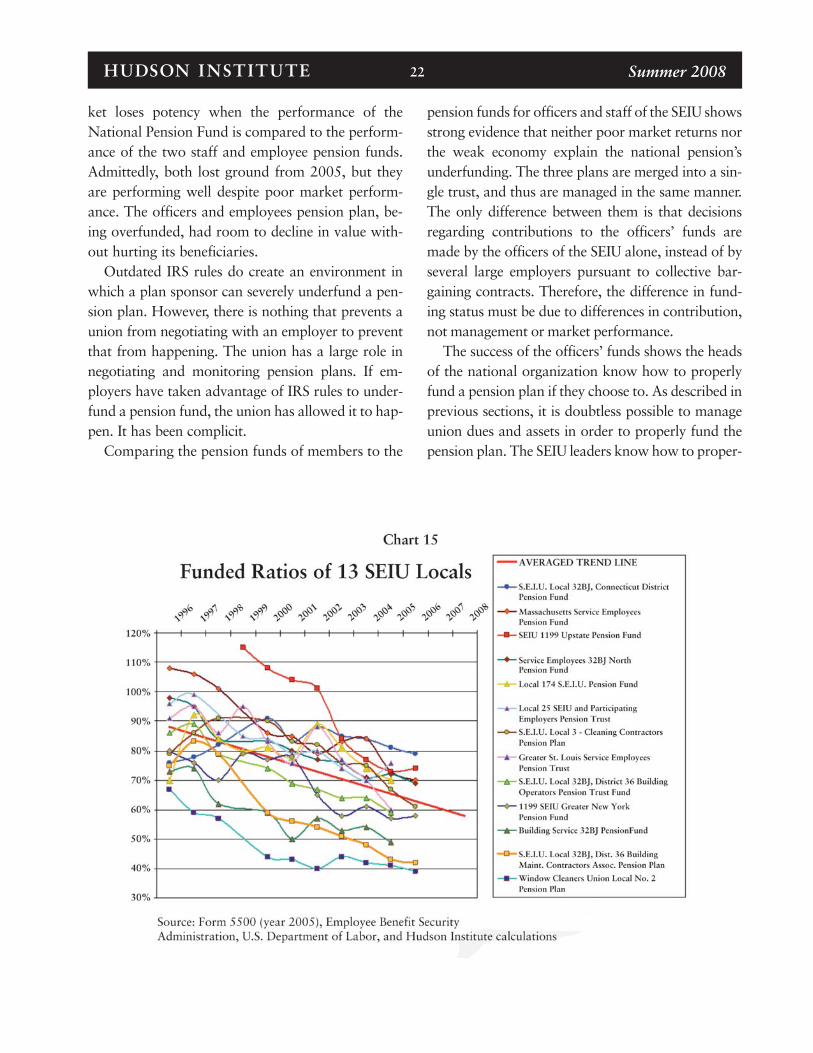

Chart 15: Funded Ratios of 13 SEIU Locals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

At a time when unions are intensifying theirefforts to organize American workers, it istroubling to see a widespread pattern of

poor performance among collectively bargained pen -sion plans. They perform quite poorly relative toplans sponsored unilaterally by employers for non -union employees. The disparity raises this question:are union members getting as good a deal in theirretirement funding as they might? Or, to put itanother way, do collective bargaining contracts lackprovisions for the funding necessary to generate thegenerous retirement income that unions advertise?

This paper offers explanatory background infor-

mation on pensions, on sources of informationabout pensions, on the reporting and disclosurerequirements of Congress and the U.S. Departmentof Labor, and on the data and analysis that illumi-nate sources of the underfunding problem. It alsoexamines the role that union politics may play inpension planning. The paper goes on to analyze thegeneral health of pension plans in the United Statesand, in particular, documents six case histories thatillustrate underfunding patterns in union pensionplans. The data show that, generally, employer plansare better funded, although not all have been ade-quately funded.

Summer 2008HUDSON I NSTITUTE 1

Introduction

American workers depend on pensions forthe bulk of their retirement income. That iswhy Congress and the U.S. Department of

Labor require annual disclosure of the financial sta-tus of individual pension plans. A detailed analysisof these data shows that union-negotiated plans arenot as actuarially sound as those provided by pri-vate companies to their non-union employees.

Pensions come in two broad categories: definedbenefit pensions and defined contribution pensions.A defined benefit pension promises a specific month -ly stipend for a retiree’s lifetime, calculated using thenumber of years worked and some measure of theworker’s earnings over that time. A de fined contribu-tion pension sets up personal investment accounts;typically, the employee can make some choices abouthow the money in his account is invested.

A large part of the difference between union plans

and employer plans appears to be a tendency to -wards low contributions among union plans. In2005, the latest full year of data available, collec-tively bargained pension plans were more poorlyfunded than their non-union counterparts. Largeplans, those with 100 or more participants, strong-ly showed this pattern. While 36.5 percent of non-union plans were fully funded,1 only 19 percent ofunion plans met this criterion. The Pension Pro tec -tion Act of 2006 considers funds underfunded, butnot “at-risk,” if they are at least 80 percent fund ed.While nearly 90 percent of non-union plans met thefunding threshold of 80 percent, only about 60 per-cent of union plans were not “at-risk.” Among col-lectively bargained pensions, around 11 percent wereonly 65 percent funded, low enough to put the larg-er national plans in the heavily-penalized “critical”category. Only two percent of non-union plans werein this condition.

Among small plans, similar patterns emerged. Ofnon-union plans, 57 percent were fully funded as

Executive Summary

The author is grateful for the research assistance of Andrew

Brown and Jeffrey Weaver.

com pared to 28 percent of union plans. While 43percent of non-fully funded non-union plans failedto pay their annual costs, 71 percent of union plansthat were not fully funded were behind on pay-ments. However, as compared to large union plans,small union plans were 37 percent more likely to beless than 80 percent funded, and 16 percent morelikely to be in “critical” condition.

Our analysis finds that pension plans for the offi-cers and staffs of unions were much better fundedthan those for the rank-and-file. On average, the 21largest union pension plans had less than 70 percentof the funds that they would need to cover theirtotal obligations, and none were fully funded. Sevenwere less than 65 percent funded. Yet 23 officer andstaff funds from the same unions had 88.2 percentof the funding they would need to pay promisedpensions, including seven fully funded plans andanother 13 with at least 80 percent of their requiredfunds. Excluding the seven plans strictly for unionoffice employees, staff funds had 98.4 percent oftheir required funds.

Unions have also been caught using their funds toachieve their political ends. In 2005, the Depart -ment of Labor wrote the AFL-CIO a letter telling itto reconsider such practices. Theoretically, pensionfunds are not permitted to make investment deci-sions based on politics or public policy. Using pen-sions as a political tool hurts union members be -cause it may push their retirement funds into loweryielding investments. That diminishes investmentreturns and thus reduces resources available to paypromised benefits.

The histories of several union pension funds helpdemonstrate why they are in poor financial condi-tion. The Sheet Metal Workers International Unionlobbied for more benefits until 2008, when its sig-nificant liabilities required it to negotiate combina-tions of increased payments and decreased benefits.The Teamsters implemented only modest reforms oftheir pension plans and did so too late to forestallthe Pension Protection Act’s automatic penalties.The Plumbers and Pipefitters Union lost millions to

its previous trustees, as it made self-interested invest-ments that yielded criminally-low returns. A book-keeper of the Laborers’ pension fund em bezzledhundreds of thousands of dollars in contributions.

Inadequate funding of plans was allowed formany years under the Employee Retirement IncomeSecurity Act of 1974. Until the passage of the Pen -sion Protection Act of 2006, it was difficult to en surethat contributions matched liabilities. Several verylarge pension funds, despite claiming that work erpensions were well-protected and well-funded untilas late as last year, were subsequently required toadopt emergency recovery measures when the 2006Act became law in January 2008.

The major reason why these abuses and fail-ures occur is that the workings of definedbenefit pension plans are obscure and thus

lessen the accountability of union leadership andemployees. Form 5500, which describes the financialhealth of pension plans, is often not filed for morethan 12 months after the end of a plan year. A sum-mary annual re port sent to union members does notdisclose the cost of promised liabilities, tracking onlyassets and direct annual costs. As a result, the effectsof benefit increases on the overall funding adequacyof a plan may not be seen for two or three years.

This delay makes it difficult for workers to un der -stand how increased pay-outs may affect the likeli-hood of the plan becoming underfunded, and nearlyimpossible for them to detect fraud in a timely fash-ion, compounding the effects of fraud, negligence andloss.2 It also encourages workers and their represen-tatives to view pensions only in terms of gains in an -nual future benefits, omitting the long-term costs oflowered wages or instability of the fund.

Although a defined benefit fund may benefit aworker in certain ways, it is not a transparent sys-tem. Defined contribution plans such as 401(k)plans give workers the privilege and responsibilityof managing the funds, and they are much easier tounderstand and monitor. If five percent of pay-checks are supposed to go into a 401(k) account

Summer 2008HUDSON I NSTITUTE 2

every month, it is much easier for workers to checktheir 401(k) account statements to verify that thedeposits have been made.

The choice of type of pension plan involves sig-nificant trade-offs. Unions have often presenteddefined benefit plans as practically the perfect form

of retirement benefit. This paper presents evidencethat shows how these choices may have hurt rank-and-file workers while giving their leaders greaterinfluence. Workers deserve to understand the trade-offs made in their name and they deserve to havethe opportunity to make their own choices.

Summer 2008HUDSON I NSTITUTE 3

Pensions are regular payments made toretired workers from money that they andtheir employers put aside during theirworking years. In the United States, the

best-known pensions are the monthly SocialSecurity benefits that the federal government pays.In addition, some workers have nongovernmentalpensions earned during their years of employment inthe private sector; others have pensions earnedworking for state, local or federal government.

All types of pensions can be considered deferredcompensation— that is, a part of a worker’s earningsnot paid immediately. In an age when workers wereexpected to work at a single company for most oftheir working lives, this was a useful tool to encour-age company loyalty and get workers invested instaying on beyond a few years. For workers, the pro -mise of income while retired was attractive, and sothey would stay with an employer for dec ades, some-times keeping a job that they found disagreeable orbarely tolerable. Many pensions are not legally owedto a worker until he has worked at a company forseveral years, when the pension be comes “vested.”

Pensions come in two broad categories: definedbenefit pensions and defined contribution pensions.A defined benefit pension promises a specific month-ly stipend for a retiree’s lifetime. This sum is oftencalculated by using the number of years worked andsome measure of the worker’s earnings over thattime. The worker may or may not contrib ute to thepension plans, but the employer always contributes.

A defined contribution pension sets up an invest-ment account for each worker. The worker con-tributes a portion of each paycheck—perhaps fouror five percent—into the account. The employermay make so-called “matching” contributions, al -though the term is something of a misnomer be -cause the employer’s payment is often less than the

worker’s, perhaps one-third or one-half. The moneyin the defined contribution account, often known asa 401(k) account, is invested and appreciates overlong periods of time. How much retirement incomethe defined contribution account will generatedepends on the amount invested, choice of invest-ment, and years invested.

The sponsor of a defined benefit plan contributesa certain amount of money per participant everyyear into a pooled investment account. This isknown as funding future obligations, rather thantry ing to pay these costs as they come due. The em -ployer hopes that enough money will accumulate,with investment income and appreciation, to paythe promised benefits. This approach requires com-panies to predict how much they will pay into thefund in the future. These calculations, especially thefuture value of present contributions, make manag-ing a defined benefit plan complicated. A financialmanager (usually an institution) is hired to makeinvestment decisions so that the fund will growenough to meet the employer’s future pension obli-gations to its employees.

Defined contribution plans create more pre-dictable costs for employers, who, in collective bar-gaining contracts, normally agree to make contribu-tions of a certain size, or to match employee contri-butions to a certain extent.

Upon retirement, holders of defined contributionaccounts can purchase “annuities”—contractualpromises by financial institutions to pay a certainamount of money every month for the rest of theholders’ lives. Or retirees can simply withdraw themoney and consume it at their own pace. If they dothe former, they have effectively transformed theirdefined contribution plans into defined benefit plansat the point of retirement.

Some people prefer defined benefit plans because

Summer 2008HUDSON I NSTITUTE 4

What Are Pensions?3

an employer is usually liable for those promisedfuture benefits. However, in order to get those ben-efits, workers have to stay in the same job for manyyears, a situation that is increasingly unusual in ourdynamic workforce. Also, there is usually some riskthat the employer will experience reversals or willfail, events that may put the pension at risk.

In contrast, participants in a defined contributionplan have a legal claim on the money diverted fromtheir paychecks to personal accounts, as well as theinvestment return on this money. Workers havesome say over how the money is invested—in bonds,stocks, or a mixture. Moreover, defined contribu-tion plans are portable; workers take them whenthey change jobs. This is an important considerationin an economy in which lifetime employment isbecoming increasingly uncommon. With portableaccounts, workers are free to move to more attrac-tive jobs.

Unions prefer defined benefit plans because suchplans prevent workers from leaving their firm for anon-union job. In other words, defined benefit plansmay contribute to union security.

Another important distinction in pension ac count -ing is the difference between “single-em ployer,”“mul ti employer,” and “multiple-employer” pensionplans. A single-employer plan is sponsored by one

firm to support the retirement of its workers. Single-employer plans may be adopted unilaterally by pri-vate employers or be created by negotiation withlabor unions.

Multiemployer pension plans are created by a la -bor union in order to provide retirement income forworkers in several different places of employment.This requires the union, the sponsor of the plan, tonegotiate with each employer to join and contributeto the fund.

Finally, a multiple-employer pension plan is usual-ly adopted by a parent company to provide pensionsfor employees in some number of its affiliated com-panies. Trade associations or other groups of em -ploy ers may also choose to form multiple-em ploy erpension plans.

The rationale behind multiemployer and multi-ple-employer pension plans is that they allow firmsto pool risk among several employers. Multi em -ployer pension plans allow workers to keep theirpensions if they change jobs to another participatingcompany, within a limited range (often within thesame industry). This consolidates union pensioncontributions into larger individual funds. Multi ple-employer pension plans allow parent companies totransfer covered workers between subsid iaries withminimal paperwork.

Summer 2008HUDSON I NSTITUTE 5

In 2005, there were an estimated 679,095 pen-sion plans in existence in the United States.Close to 48,000 of them, about seven percent,were de fined benefit plans. This contrasts

starkly with 1975, when approximately one-third ofthe nation’s 311,094 pension plans were definedbenefit plans. While there are more pension plans inexistence today than in the 1970s, there are fewerdefined benefit plans.

There are three causes for the shift in styles. First,workers began to view pension plans as integral partsof their compensation benefit packages, so more em -ployers began to offer them. Second, workers, findinglifetime employment ever less common, saw the wis-dom of having portable pension ac counts. Chart 1shows that the change in pension plans has been driv-en almost entirely by the rise of defined contributionplans. Third, employers came to regard long-term

future liabilities as undesirable and developed a pref-erence for defined contribution plans, which entail nofuture obligations and risks.

Single-employer plans have driven this shift be -cause plans covering many firms are often multiem-ployer plans, and thus union-run. Chart 2 demon-strates this. The changes in types of pension plansoffered almost exactly reflect the overall trends inChart 1. It is difficult for even a single firm to extri-cate itself from a collectively bargained plan, even if itpromises to transfer all assets into personal accounts.Unions distrust the “personal responsibility” of indi-vidual retirement accounts, perceiving them as ena -bling workers to move out of the union setting.Nevertheless, as Chart 3 shows, plans offered by mul-tiple employers have increasingly been defined contri-bution plans; as of 2005, they made up half of multi-ple employer plans.

Summer 2008HUDSON I NSTITUTE 6

Trends in Pension Coverage

Summer 2008HUDSON I NSTITUTE 7

In 2005, collectively bargained defined benefitpensions held over $800 billion in assets. Multi -employer plans held close to $350 billion. As dis-cussed below, national unions have come to see theseassets as leverage in po l i tical and social battles. Thus,union leadership may also dislike defined contribu-tion plans because they mean fewer assets underunion management and possibly less influence owingto how the assets are managed.

While the Employee Benefits Security Admin -istration of the U.S. Department of Labor and theInternal Revenue Service have been questioning the

pressure unions place on managers of pension funds,some unions continue to use their assets to forcemanagers to either comply with their wishes withrespect to voting on corporate shareholder issues, orlose their accounts. The money in defined contribu-tion plans, however, belongs to individual unionmembers, limiting the ability of the union to affectinvestment choices and corporate policy.

Despite their waning popularity, defined benefitplans supported the retirement of close to 42 millionpeople in 2005, at least 20 million of them currentworkers.

Summer 2008HUDSON I NSTITUTE 8

Most pension funds must file Form5500 annually with the Internal Rev -enue Ser vice and the U.S. Depart -ment of Labor. Form 5500 includes

information about the assets and liabilities of the pen-sion fund; the number of participants; some detailsabout the pension plan; and the investment earningsof the pension fund.

Form 5500 requires estimates of the value of fund’sassets, liabilities, and the present value of all benefitpayments. Because of the complexity of the calcula-tion, companies are asked to calculate only their“accrued” liabilities. They estimate the present valueof all benefits they would have to pay if they closed atthe end of the year and paid all promised benefitsbased on service to that time. That is, if benefits areone percent of wages per year of service, a person whohad worked at the company for 10 years would beowed an annuity of ten percent of his wages each year.

If the ratio of assets divided by liabilities is greaterthan or equal to one, the company would be able topay all of its promised benefits assuming all actuari-al assumptions are correct. This is an important

qual i fication and will be discussed later. If this ratiois less than one, it indicates that the company haspromised to pay more in benefits than it expects tohave when benefits are paid. A ratio of less than oneis the major indication to plan participants that theirpension fund—and possibly their own benefits—arein danger. A ratio less than one, an “underfunded”plan, may suggest mismanagement of funds.

The Employee Retirement Income Security Act of1974 (ERISA), a law written to protect defined bene-fit pension plans, had provisions that specificallyrequired sponsors to pay a minimum contributioneach year of the normal cost4 and annual paymentson their previous loans. However, it included anotherprovision, intended to encourage pension sponsors tokeep their plans well-funded, that has contributed tothe deterioration of funds.

In any year in which a sponsor pays more than thesum of the normal cost and other charges, ERISA al -lowed the fund to gain a “credit” that can be used tore duce the minimum required payment in future years.

That happened during the “dot-com bubble” ofthe late 1990s, when many pension funds ran up

Sources of Information on Pension Plans

large credits due to their ability to pay. But thefunds started performing poorly because of thestock market fall. Thus the fund administratorsused the credits to pay off the debts they accumu-

lated during the fall, and, often, their normal costs.As a result, many employers did not make contri-butions for years, even though their funded ratioshad fallen significantly.

Summer 2008HUDSON I NSTITUTE 9

In 2005, on average, large plans were 94 per-cent funded. This included 3,755 collectivelybargained pension plans (including single andmultiemployer plans) and 5,206 non-collec-

tively bargained plans.Collectively bargained plans, on average, were 88

percent funded. In contrast, non-collectively bar-gained plans were on average 98 percent funded, ascan be seen in Chart 4. This suggests that plans

brought into existence through union negotiationsare worse off. Among “non-bargained” plans, 36.5percent, or 1,904 pension plans, were at least fullyfunded. Among collectively bargained plans, only713, or 19 percent of the plans, were at least fullyfunded (shown in Chart 5, overleaf).

The Employee Benefits Security Administration(EBSA) allows for a certain amount of fluctuation inpension funds. Both legislators and EBSA seem to

General Health of Pensions in the United States

Summer 2008HUDSON I NSTITUTE 10

Summer 2008HUDSON I NSTITUTE 11

recognize that a fund can be less than fully fundedbut not be in a great deal of trouble. Plan sponsorsare permitted to take out loans, thus increasing lia-bilities, and then pay off the loans over a number ofyears. Dips in the stock market may cause dips in thefunding ratio that take several years to recover. So, ingeneral, it is considered acceptable for a fund to haveas little as 80 percent of the value of its liabilities.

In 2005, 4,520 non-bargained pensions, nearly87 percent of the total amount, had at least 80 per-cent of the money they needed to pay all liabilities.Only 61 percent of collectively bargained pensionplans, or 2,304, were at least 80 percent funded.

Unsurprisingly, this pattern repeats itself for thelowest level of funding—critical status, defined asless than 65 percent funded. In 2005, 93, or only 1.8percent of non-bargained pension funds were in crit-ical status. In contrast, 401, or about 11 percent ofcollectively bargained pension funds had less than

65 percent of the money they needed to fulfill theirobligations. This is illustrated in Chart 6.

What leads to the difference between fully fund-ed and poorly funded pension funds? One theory isthat poorly-funded plans rely heavily on their cred-its to reduce payments, which, as described in Ap -pen dix 2, can have a detrimental effect on assetswhen poor market performance reduces investmentreturns. Alternately, poorly-funded plans may havefallen behind on payments, which put them furtherinto debt as funding deficiency charges begin toaccumulate.

In 2005, 31 percent of funds that were not fullyfunded did not contribute enough money to covertheir annual costs. Chart 7 shows that among plansin critical condition, only 13 percent paid theirannual costs.5

For those plans in critical condition, however,union plans were still worse off. One-third of non-

union plans in critical condition paid at least theirannual charges, while only eight percent of unionpensions of the same status did (shown in Chart 8).

While among underfunded plans it is usual tofind that the employer has fallen behind on pay-ments, the data cited above suggest that this prob-lem is more common among union funded plans.Not meeting annual payments is a certain way for apension fund to fall behind on its ability to pay itsparticipants.

Not only are collectively bargained plans morelikely to fall behind on payments, they are more like-ly to be forced to pay large penalties to help make upthe difference between their assets and liabilities.Under ERISA, poorly-funded single and multiple-employer plans may be required to pay additionalfunding charges, regardless of whether or not theyhave eliminated their regular contributions throughcredits. In 2005, of 5,144 non-union plans, 856, orabout 17 percent, had to pay extra fees. Seven hun-dred and thirty five union plans had to do the same.They made up about 30 percent of single and multi-

ple-employer collectively bargained plans (Chart 9).Even comparing only those plans already in

deficit, union plans were in worse financial condi-tion. While underperforming non-union plans wereforced to contribute an average of $2.27 million toput their accounts in order, collectively bargainedplans had to pay an average of $2.94 million for thatpurpose (Chart 10). Union pension plans tend to beboth further in deficit and at higher risk of ending upunderfunded.

Why Union Plans Tend to Perform More Poorly

The financial instability of union plans could bedue to the longevity of collectively bargainedpensions. In many cases, union contracts are

not modified annually. As a result, the problem couldarise from an inability to alter employer contributions

Summer 2008HUDSON I NSTITUTE 12

Summer 2008HUDSON I NSTITUTE 13

from year to year to help correct for poor market per-formance, actuarial changes, and other un plannedincreases in pension liability. If this were the case, theproblem might be exacerbated in multi-employer pen-sion plans. When contributions come from severalemployer-union contracts, it would take more timeand more negotiation to increase con tributions.

There are other possible explanations for the per-formance of union pension funds being worse, onaverage, than that of non-union plans. Union leaderscould be negligent, corrupt, or unwilling to fight forthe “boring” benefit of ensuring that the pensionfund is fully funded. Rank-and-file members do notwant to hear that union leaders have fought withmanagement to ensure that the pension they werepromised is now more likely to be paid, since it sug-gests that pension funds are unstable. Of course, it isworse news to learn that union leaders have not beentrying to make sure that those promises are protected.

It is hard to capture this in the data, but the prac-tice of amending plans is another possible source ofthe disparity between the financial health of unionand non-union pensions. Unions love to win pen-sion increases for their constituents. But, unlikebusinesses, unions do not themselves have to con-form to the bottom line. They can ask for whateverthey think would make them look good as negotia-tors and champions of the rank-and-file. Employersmay be inclined to prefer agreeing to sweetenedretirement benefits because it is usually cheaper topromise a dollar of future benefits than to pay a dol-lar in current wages. Thus it is easy to see how busi-nesses could agree to pension plan amendments inlieu of wage increases.

There is a widespread tendency for unionizedpen sion plans to be less well-funded and less likelyto “catch up” on payments when they fall behind.This trend may in part be caused by incompetentunion leaders. But the failings of union pensions—while real and serious—are also due to the follow-ing structural failings.

First, unions do not, as a rule, negotiate contractsto ensure that annual contributions match the min-

imum payments needed to keep pension funds sta-ble. Multi-employer plans, which are run by singleunions covering many employers6 and require mul-tiple rounds of negotiation, are more likely to fallbehind and stay behind than those run by singleentities managing a fund.

The data show that single-employer and multi-ple-employer pension funds, which require fewerrounds of negotiation than multiemployer funds,are less likely to consistently fall behind on theirpayments, regardless of union status. Thirty-sevenpercent of non-fully funded single or multiple-em -ployer plans paid their annual charges in 2005. Incontrast, only four percent of multiemployer fundsthat were not fully funded met their annual obliga-tions (Chart 11).

Secondly, there is a tendency to increase pensionliabilities by more than merited during negotiations.This occurs because employers are more willing toincrease future obligations rather than current ones,and future benefits may be more important thanwages to workers who are well paid. While due dili-gence is likely exercised in advance by employers todetermine how much pensions will cost them,uncertainty plus the cheaper present cost of futureobligations increase the likelihood that expensiveamendments are adopted.

These explanations, it should be said are, first ofall, hypotheses. There seems to be some evidence oftheir truth, but more data and analysis are needed tovalidate them. If these are the causes of poor unionpension performance, they do not excuse unionleaders for the poor performance of pension funds.Leaders often conceal poor performance, and rank-and-file members seem to express no understandingthat their future income is at risk, or why.

Unions, after all, use benefits to attract new unionmembers. They assert that union members are morelikely to have pensions and health insurance. Suchpromises would be less persuasive if members un der -stood that the benefits were by no means guaranteed.

In other words, union leaders assign a higher pri-ority to raising benefits than to securing them. This

Summer 2008HUDSON I NSTITUTE 14

often occurs in the face of management seeking torestrain costs, suggesting that union leaders haveplaced the level of benefits at a higher priority thanthe benefits’ security.

Workers need to understand that there are advan-tages to having defined benefit pension plans, butonly if the plans are properly funded. They also needto understand that companies are reluctant to in -crease benefits, whether with wages or pensions, be -cause it is hard to rescind previously-promised ben-efits. The rank-and-file should hold union leaders atleast as accountable as employers for failures toprop erly fund their accounts. Neither group canunilaterally decide on inadequate funding, but it iscentral to union leaders’ duties to protect the inter-ests of workers. This means that they should expend

at least as much effort on properly funding pensionsas they do on increasing pensions. Failure to do sois a breach of their responsibilities.

Small Plans

Unlike large plans, most small plans are non-negotiated. Of 25,627 small plans, 856, or3.3 percent are collectively bargained, com-

pared to the 42 percent of large plans (shown inChart 12).

The 856 small union pension plans are, on aver-age, larger than non-union plans. The small unionplans have an average of 54 people each, while the

Summer 2008HUDSON I NSTITUTE 15

24,771 non-union small plans have an average ofabout 13 (Chart 13). This contrasts with largeplans, in which union plans (dominated by 1,000 orso multiemployer plans) were about twice as largeas non-union plans (shown in Chart 14). Excludingmultiemployer plans, the two groups were about thesame size for large plans, demonstrating that muchof the difference in size was due to plans that cov-ered many employers, rather than a tendency forunion plans to cover employers with more workers.This exclusion of multiemployer plans does notchange the results for small plans.

Despite the differences in composition, it is rea-sonable to expect collectively bargained small plansto fare worse than non-union plans.

This is indeed the case. Only 28 percent of bar-gained plans are fully funded, compared with 57percent of non-bargained plans. In 71 percent ofunderfunded union pension plans, the employercontribution was less than costs. Forty-three percent

of employers whose private funds were not fullyfunded contributed less than their annual costs. Ifany thing, the disparities among small plans aremore striking. While small plans are overall morelikely to be fully funded, the difference in fundingbetween the collectively bargained and private plansis greater.

Small union plans do not do as poorly as large,multiemployer plans. On some levels they do aboutas well as small non-union plans. Thirteen percent ofsmall non-union plans were in critical condition in2005, while 16 percent of union plans were. About22 percent of non-union plans were less than 80 per-cent funded, while 37 percent of union funds were.

Size is almost certainly the reason for this. Smallunions are more accountable since their benefits canbe more easily evaluated. A 500,000-person unioncould pretend that $5 billion will be enough to payall pensions. A 50-person union, in contrast, cannotpretend that $150,000 is enough.

Summer 2008HUDSON I NSTITUTE 16

Summer 2008HUDSON I NSTITUTE 17

Hence, problems of underfunding, while lesssevere among small plans, justify concern over theoverall level of funding of all union pension plans.

Officer and Staff Pension Plans

Many unions have staff and officer pen-sion plans at the national level, so unionleaders may not rely on the rank-and-

file plan for their own retirement income. How does the performance of these in-house

employee plans compare to that of rank-and-fileplans? The question is not easily answered.

It is hard to know how many plans cover unionemployees and officers. Some union employee pen-sion plans are collectively bargained, but many arenot. The leaders of local unions may or may not beinvolved in employee and officer pension plans oftheir national union.

To gauge the differences between officer andrank-and-file plans, we extracted a sample of the 21largest union and staff pension plans from the samenational organizations. These staff and nationalpension funds represent some of the biggest namesin labor: SEIU, UNITE-HERE, the United Steel -work ers, the United Food and Commercial Work -ers, the Plumbers and Pipefitters, the InternationalBrotherhood of Electrical Workers, the Sheet MetalWorkers, and the Bakery, Con fec tionery, TobaccoWorkers and Grain Millers International Unions.

As of 2005, each of these plans covered at least64,000 working or retired participants. Combined,the 21 largest multiemployer union pension planshad only 67.7 percent of the funds needed to meettheir obligations. None of the plans was fully fin -anced, and seven were in critical condition. Fourteenhad less than 80 percent of their needed assets.

On the other hand, 23 officer and staff fundsfrom the same unions were much better off.

Together, the funds had 88.3 percent of their need-ed funding. Six of the funds were at least fully fund-ed, and 20 of the funds had more than 80 percent oftheir needed assets. None of the funds was in criti-cal condition. Excluding seven pension funds foroffice employees of the unions, the 16 staff and offi-cer funds had 98.4 percent of their needed funding.The data suggest a worrying disparity: staff pen-sions are more likely to be better funded.

As a rule, staff and officer pension plans atunions, especially retirement plans for the subset ofemployees within a union’s national staff, tend notto be collectively bargained. A few are, such as theOperating Engineers’ Pension Fund employees’plan, the Sheet Metal Workers National PensionFund staff plan, and the Sheet Metal Workers officeemployees’ plan. But officers’ pension funds areperks of their job, and in part reflect the bias of bet-ter funding among non-bargained.

It is easy for union officers to ensure that theirpension plans are well-funded. The officers makethe essential business decisions for the union as em -ployer. Union officers know—or are in a position toknow, if they engage competent accountants—howmuch they should pay into their own pension plan.They control the allocation of union dues to theunion’s several categories of expenditures, althoughsome unions may have procedures for budgetaryreview by rank-and-file, or at least a members’ com-mittee. From year to year, union officers, with thehelp of technical staff experts, such as accountants,can improve deficient pension plan funding moreeasily than a corporation can.

Since their own retirement is affected, union lead-ers have an incentive to ensure that their future issecure before looking to the general union funds.They may spend more effort tracking and correctingpension funding for officers’ pensions.

Unions are fans of “pay-for-performance” forcorporate executives. They argue that a CEO oughtto be punished, or at least not rewarded, for pooroutcomes—flat or declining profits. They decry suchpractices as golden parachutes and stock option re-

Summer 2008HUDSON I NSTITUTE 18

pricing. But it is clear that unions are not structuredin a way that best advantage their members. Theleaders do not have incentives to ensure that thenational pension fund is well-managed because theirown future is not at stake.

There is intuitive sense in giving a manager a per-sonal interest in the future performance of the com-pany he manages. In the same way, it might makesense to put union leaders’ pension funds in the sameboat as the funding for the rank-and-file. By givingthem a personal stake in the future of the pensionfund, the unions would push their leaders to weighthe costs and benefits of benefit increases and thus tomake better decisions at the bargaining table.

Pension Fund Politics

In recent years, pension funds controlled by org -anized labor have become more involved incorporate and political battles that do not seem

directly related to investment returns for their ben-eficiaries. While it is difficult to discern the finan-cial im pact of unions’ political agenda on pensions,engaging in these disputes has not materially im -proved financial performance of pensions and mightwell have a negative effect. In some instances, laborhas even threatened to use their pension funds forexplicit political purposes with little regard to thefinancial consequences.

In theory, pension funds are not permitted tomake investment decisions based on politics ordesired change of public policy. That is, pensioninvestment decisions are not supposed to be moti-vated by a desire to influence elections or Congres -sional action on legislation. Pension fund trusteesare supposed to invest in accordance with “fiducia-ry duty,” which is outlined in the 1974 EmployeeRetirement Income Security Act. The Act says thatpension funds should make investment decisionscalculated to minimize risks and maximize returns,and for no other purpose.

Over the years, unions have successfully changedthe operative meaning of fiduciary duty. Thisprocess of change started in the early 1990s whenthe AFL-CIO published Proxy Voting Guidelines.These guidelines encouraged union pension fundsto consider not only how investment decisionswould affect a pension fund’s financial perform-ance, but also the effect of these decisions on com-munities, the environment, and the economy. Thisoverly broad interpretation of “fiduciary duty” hasallowed unions to join forces with others in the left-leaning progressive community by making invest-ment decisions whose goals are not always consis-tent with traditional investment strictures.

One of the best examples of this came in 2005,when the Bush administration proposed changes tothe Social Security system that would permit work-ers to have personal retirement accounts. Whenpersonal retirement accounts were announced, thePresident had the backing of major Wall Street in -vestment firms. A coalition was formed to bring to -gether these firms to advocate Social Security re -form along the lines proposed by Mr. Bush.

The AFL-CIO opposed adoption of personalretirement accounts. The labor federation worksclosely with the Democratic Party, which also op -posed the initiative. But, lesser known, the federa-tion also had ties to major Wall Street investmentfirms through its pension fund investments. Thefederation was upset with these firms because oftheir support for personal retirement accounts.

In a stunning series of letters to several of thesefirms, organized labor threatened to take into consid-eration a firm’s position on Social Security whendeciding which firms would manage their pensionfund assets. The not-so-subtle threat was: supportSocial Security reform and risk losing our business. Apublic policy issue had now become a criterion forawarding or renewing investment management con-tracts. That was a dubious proposition for plan bene-ficiaries who, in all likelihood, want to stay out of pol-itics and simply ensure solid investment re turns fortheir pension plans. If, for example, Wach ovia Bank

Summer 2008HUDSON I NSTITUTE 19

managed pension funds better than Ed ward Jones,then would it make economic sense to drop Wachoviabecause the bank favored Social Security reform? TheDepartment of Labor eventually was alerted to thesethreats and wrote the AFL-CIO a letter:

“The Department is very concerned about thepotential use of plan assets to promote particularpolicy positions…A fiduciary may never increase aplan’s expenses, sacrifice the security of promisedbenefits, or reduce the return on plan assets, in orderto promote its views on Social Security or any otherbroad policy issue.”7

More indirectly, organized labor’s pension fundshave also become strategically involved in corporateshareholder battles, often introducing resolutions atannual shareholder meetings in the name of better“corporate governance.”

It might make sense for the Autoworkers unionto propose a series of shareholder resolutions at Fordor GM. Obviously, the Autoworkers have a directinterest in how those companies operate be cause somany of their members work for those same compa-nies. But that is not how many pension funds useshareholder resolutions.

For example, in 2004, there was a popular, labor-driven shareholder resolution to split the CEO andchairman of the board roles at some companies.The Teamsters presented the resolution at Merrill

Lynch and Coca-Cola; the Bricklayers at Wal-Mart;the International Brotherhood of Electrical Workersat Kohl’s; the Plumbers at Allergan.8 There is noindication that the Teamsters are going to launch anorganizing campaign for Merrill Lynch employeesor that the Plumbers are trying to unionize Allergan.Rather, the goal was to use pension fund power toinfluence corporate decisions in a way that labor’slow membership numbers otherwise preclude.

It is not clear that these activities of labor-con-trolled pension funds improve returns on invest-ments. Many financial scholars have hypothesizedthat organized labor’s desired reforms, such as split-ting the CEO and chairman roles, might make com-panies less competitive. That could thus ensure low -er returns in the long-run for a plan, since the firmsin which they invest will see diminished profits.Even in cases where there is not a clear negative fin -ancial effect, one can still reasonably question theresources and time that labor dedicates to these bat-tles. Ultimately, pension fund management re -sources are used for purposes that are at best tan-gential to the fund’s presumed goals. In other cases,such as the Social Security example above, it is clearthat labor is inappropriately mixing policy goalswith investing strategy, a blend that can clearlyharm retirees, who depend upon the pension fund’sperformance to realize promised retirement benefits.

Summer 2008HUDSON I NSTITUTE 20

The following six case histories illustrateproblems and weaknesses in union pen-sion plans. Among them are weaknessesin ERISA requirements, poor compliance

efforts by the Labor Depar tment, union officer self-interest, and the tendency of unions towards corrup-tion and seeking greater benefits rather than morestable fund ing. Some of these plans demonstrate long-term negligence or inaction; others represent periodsof fraud and corruption, small-scale and large.

While direct embezzlement of funds is unambigu-ously illegal and punishable, many of the problemsare issues of accountability or compliance. At leastuntil recent years, low funding ratios were allowedby a set of obscure accounting rules. Des pite thelegality of their decisions, the union leaders whoallowed the degeneration of pension funds harmedhundreds of thousands of workers. The case histo-ries below demonstrate that the deterioration ofpension funds was not only due to law-breaking,but also to larger failures that union members maypay for if and when their benefits fall short.

Service EmployeesInternational Union

The SEIU has roughly two million members,with most in low-skill, low-wage jobs. It is astrong supporter of defined benefit pension

plans, arguing that defined contribution plans arebad for workers. On its web site, SEIU says thedefined contribution plans have the following flaws:

1. They place the burden of fund management onworkers.

2. They can fail workers if the market performspoor ly or the worker underestimates how much heneeds to fund his retirement.

3. They do not provide supplemental benefits, suchas early disability, cost of living adjustments, retireehealth coverage, and death benefits.

4. They yield lower returns than defined benefitplans.

The union also asserts that “the purpose of a de -fined benefit fund is to provide employees whoretire with as much replacement income as possiblefor as long as they live.”9 It would seem reasonable,therefore, that SEIU leaders deliver generous, wellfunded pensions for members.

In 2006, the SEIU National Industry PensionPlan, a plan for the rank-and-file covering 100,787SEIU workers, was 75 percent funded. A separatefund for the union’s own employees had 1,305 par-ticipants and was 91 percent funded. The pensionfund for SEIU officers and employees had 6,595mem bers and did even better, at 103 percent funded.

Such inequality was not always the case. In 1996,the SEIU National Industry Pension Fund had closeto 110 percent of the funds it would need to pay allpromised pensions to its workers.10

Of course, stock market performance has falteredsince 1999, and the performance of the fund reflectsthat. In 1998, the fund had slightly more thanenough assets to pay its obligations. In 2000, it hadapproximately 85 percent of needed funds, and ithas not risen higher than 90 percent since.

The SEIU blames the poor performance of pri-vate pensions on “the weak economy, poor invest-ment returns, and outdated IRS rules.”11

The argument for the effects of a weak stock mar-

Summer 2008HUDSON I NSTITUTE 21

Six Case Histories

ket loses potency when the performance of theNational Pension Fund is compared to the perform-ance of the two staff and employee pension funds.Admittedly, both lost ground from 2005, but theyare performing well despite poor market perform-ance. The officers and employees pension plan, be -ing overfunded, had room to decline in value with-out hurting its beneficiaries.

Outdated IRS rules do create an environment inwhich a plan sponsor can severely underfund a pen-sion plan. However, there is nothing that prevents aunion from negotiating with an employer to preventthat from happening. The union has a large role inneg o tiating and monitoring pension plans. If em -ployers have taken advantage of IRS rules to under-fund a pension fund, the union has allowed it to hap-pen. It has been complicit.

Comparing the pension funds of members to the

pension funds for officers and staff of the SEIU showsstrong evidence that neither poor market re turns northe weak economy explain the national pension’sunderfunding. The three plans are merged into a sin-gle trust, and thus are managed in the same manner.The only difference between them is that decisionsregarding contributions to the officers’ funds aremade by the officers of the SEIU alone, instead of byseveral large employers pursuant to collective bar-gaining contracts. Therefore, the difference in fund-ing status must be due to differences in contribution,not management or market performance.

The success of the officers’ funds shows the headsof the national organization know how to properlyfund a pension plan if they choose to. As described inprevious sections, it is doubtless possible to manageunion dues and assets in order to properly fund thepension plan. The SEIU leaders know how to proper-

Summer 2008HUDSON I NSTITUTE 22

ly fund a pension plan, yet have clearly failed to pushtheir corporate partners to properly fund pensions.

The problem of poor funding occurs not only inthe national pension plan. In 2005 and 2006, it wasrevealed that 13 SEIU local pension plans were allless than 80 percent funded. Seven of them were lessthan 65 percent funded. In 1996, all of them weremore than 65 percent funded, and half were morethan 80 percent funded. While those that were inpoor shape back in 1996 merit significant attention,the Mas sachusetts Service Employees Pension Fundis of greatest concern. It fell from nearly 110 percentto 70 percent funded in 10 years, and the SEIU 1199Upstate Pension Fund fell from 115 percent to 74per cent since its inception in 1999. Chart 15 showsthe degeneration of these funds’ strength from 1996to 2006.

Poor market performance can account for someof these falls. However analysis of their latest Forms5500 reveals that 10 of these 13 funds paid less thantwo-thirds of their annual charges. Even if part oftheir problems is due to unstable financial markets,the union’s inability to ensure that annual costs arecovered makes the problem worse.

Part of the problem in local pension managementcould be the more secure future incomes of the lead-ership. Participation in the national officers and em -ployees pension plan (the overfunded plan) is man -datory for the officers and employees of local SEIUunions. If local union employees were dependent forretirement income on the plans that cover unionmembers, they would have more incentive to pro-tect those plans.

Second, these local leaders may be giving intonational pressure regarding shareholder activism.Local and national SEIU pension funds made upmore than 30 percent of Kohlberg Kravis Roberts’2006 Fund, and union president Andy Stern is notabove trying to use that leverage to pressure KKR,private equity firms and other companies to adhereto the SEIU’s principles.12 This pressure could leadto investment choices that do not yield sufficientreturns or take time from other efforts to compen-

sate for weak markets or insufficient contributions.Third, mismanagement is a possibility on the lo cal

level because the same trust does not control severalfunds with divergent returns. While SEIU nationalleaders cannot make a bad investment with outharm ing their own financial futures, it is possible forincompetent local managers to mismanage the fundswithout affecting their own pensions.

The SEIU is one of the fastest-growing unions inthe United States. It trumpets its efforts to securehealth and retirement benefits for service workers.Unfortunately, it is becoming clear that the SEIU isnot truly securing these benefits. Workers drawninto its national pension fund are hurt by a fundwhose adequacy has been falling from year to year.

The Sheet Metal WorkersNational Pension Fund

Started in 1966, the Sheet Metal Workers Na -tion al Pension Fund is a multiemployer plancovering workers who are members of the

Sheet Metal Workers’ International Association. Asof the end of 2006, the plan covered more than136,000 people, 69,164 of whom were then work-ing at plants unionized under the SMWIA. It seemedthat the union-bargained benefits for workerswould carry them through retirement comfortably.After all, according to the SMWIA website, “unionmembers are also more likely to have a guaranteedretirement plan.”

Unfortunately, while the SMWIA offered a retire-ment plan it portrayed as “guaranteed,” the plandid not turn out to be financially sound. As late as2006, the union’s National Pension Fund had“guaranteed” $7.45 billion in benefits to active andformer workers, but had accumulated only $3.1 bil-lion in assets—less than 42 percent of the amountneeded. Due to the accounting rules in force beforethe passage of the Pension Protection Act of 2006,

Summer 2008HUDSON I NSTITUTE 23

past overpayments had allowed SMWIA and its cor-porate partners to pay less than their minimumrequired payment. Even though SMWIA lauded itspension fund for regularly earning a benchmark of8.5 percent, it at best was holding steady at a $4.3billion difference between assets and liabilities.

In a 2008 letter to SMWIA workers, general pres-ident Michael Sullivan acknowledged that “thelargest driving force of funding problems is bene-fits.” That is, the largest source of the funding defi-ciency was the result of benefit increases after thecreation of the fund.

The SMWIA Pension Plan offered up to 10 years ofpast service pension credit,13 a 120-payment pensionplan, several generous early retirement options, and a“COLA” of cost-of-living adjustment, a thirteenthpayment each year that amounted to a bonus of abouteight percent. While many of these benefits had ana-logues in other unions’ pension plans, the “COLA”payment, an annual sum equal to two percent of ben-efits per year of service, was a unique feature that costthe fund heavily. Despite these continuing costs, in2005, a plan amendment was adopted that increasedexpected liabilities by nearly $29 million. The pay-ments on this debt exceed $402 million in 2006, anamount nearly 10 times “normal costs,” the annualincrease in benefits to be paid to current workers.

The essential problem is that until recently, therewas little chance of the debt being paid. In 2006,normal costs and payments on the fund’s debtequaled $483 million, while contributions to thefund equaled $301 million. Failing to meet annualrequired payments increases the risk that the fundwill fall further behind its target value in futureyears, increasing its unfunded liability and therebythe high-interest debt (8.5 percent in 2006) to bepaid off in future years.

The SMWIA Fund was not required to make itsfull payments because of its $1.5 billion in credits(due to earlier overpayment), which allowed it tooffset some of the required payments into the fund.By law, nothing required the union or its participat-ing employers to pay off its $3.7 billion in acknowl-

edged debt until that $1 billion credit were paid off -—around 2022.14

After the passage and implementation of thePension Protection Act of 2006, the managers of thefund no longer had any way to conceal these defi-ciencies.15 The Act demands that a fund with lessthan 65 percent of its promised benefits submit tonew regulations, regardless of fund performance orfunding credits.

Because of the gross deficiencies in the NationalFund, the managers had to develop two recoveryoptions to hasten the fund’s revitalization. In 2008,they might seek to require participating employersto contribute an extra 10 percent to the pensionfund in 2008, followed by increasing additionalsums over the following nine years.16 Alternatively,they put forth a schedule that decreases benefit ac -crual to one percent of annual contributions for theparticipant,17 as opposed to current accrual of 1.5percent of wages for 1200 hours, and 0.7 percent ofwages for hours worked over 1200 hours. Underthis recovery option, contributions would not haveto increase, but could not decrease.18

Each employer and union branch would be freeto determine which option to use.

Either recovery option reduces worker benefits.Both eliminate COLA increases set into the planafter 2002, and both limit lump-sum payments ofmore than $5,000 to retirees. Both eliminate a ben-efit guaranteeing 120 months of payment to theretiree or designated beneficiary, and both reduceoptions and benefits for early retirement.

No matter how optimistic union administratorsprofess to be over their ability to save the union pen-sion fund, someone is going to have to suffer to keepit from going under. Either the companies will haveto pay heavily to keep the fund afloat as-is (it is esti-mated that the increased contributions would drainat least $168 million from employers over the next10 years) or workers will be paid smaller pensionsthan they originally were promised—and expected.Regardless of the outcome, because non-standardplans were frozen, workers intending to rely on early

Summer 2008HUDSON I NSTITUTE 24

retirement options, lump-sum payments or guar -anteed 120 payments will be hurt.

Michael Sullivan, the union president, may bespeaking the truth when he speaks of the “harddecisions” that SMWIA staff had to make to save afailing pension plan. But his concern can be only forhis constituents, not for his own future. Reports tothe government show that the union’s own plan forits employees was funded more than 10 times moregenerously than the collectively bargained generalunion plan for rank-and-file members.

Union filings with the IRS show that in 2006, thelast year available, Mr. Sullivan received, in additionto his salary and expense account, $133,198 fromrank-and-file benefit plan contributions, in cludingcontributions to the SMWIA Staff Pension Plan forhis account. This plan, covering 250 people (69 act -ive workers), had, in 2005, $57 million in assets,and was 81 percent funded. The staff plan held anaverage of $230,848 for each of its participants,com pared with $22,879 per person in the fund thatcovers the rank-and-file.

Recent increases in staff benefits prove even moredisturbing. While the SMWIA rank-and-file mem-bers saw their COLA benefits disappear, the unionstaff’s COLA fund more than tripled in 2006.Incredibly, this increase was entirely due to employ-er contributions. The staff did not have to put downany of their own salary.

To make this picture even more dismal, one needonly look at the name listed under “plan administra-tor” for both of these funds. The union staff fund isadministrated by the general secretary-treasurer ofSMWIA, Joseph Nigro. The general worker fund isadministrated by Michael Sullivan. Admit tedly, Mr.Sullivan was previously SMWIA’s secretary-treasur-er, and the fund was in trouble before he took thejob, but these facts ought to have made it muchclearer that the fund needed help.

In 2007, the Sheet Metal Workers National Pen -sion Fund sponsored at least three pay-for-perform-ance proposals through its stock holdings, like manyunions.19 But the poor performance, management,

and negotiation of its pension fund suggest that moreattention should have been directed inward.

Teamsters’ CentralStates, SE and SWAreas Pension Plan

The Central States, SE and SW Areas PensionPlan covered more than 450,000 members ofthe International Brotherhood of Team sters

in 2006. The Central States fund had—and appearsstill to have—a chronic condition of underfunding.

In October 2007, UPS bought out nearly 45,000workers from the union pension fund. That is, theparcel-delivery company assumed the pension obli-gations of the fund and paid the Teamsters $6.1 bil-lion. The deal boosted the Central States pensionfund’s assets to $26.8 billion. But in 2006, the fundhad liabilities equal to $41.8 billion. Even with ahuge cash infusion in 2008, the fund apparently wasstill around 64 percent funded. As a result, in April2008, under the disclosure requirements of the 2006Pension Protection Act, the Teamsters was to informthe IRS that their fund was in “critical” conditionand required to develop a rehabilitation plan similarto that adopted by the SMWIA.

This was not a new problem. In 2006, the fundhad $19.3 billion to cover $41.8 billion of liabilities,putting it $20 billion in debt in addition to othershortfalls. As early as 2002, the Teamsters hired In -de pendent Fiduciary Services and Watson WyattWorldwide to assess the status of the fund.

Press releases issued by the Teamsters were quick tostate that the Central States Pension Fund is not con-trolled by the Teamsters. By law, the union had givencontrol to outsiders, J.P. Morgan and Gold man Sachs,and is forbidden to make investment decisions.20

Those statements were true, but omissive. TheBoards of Trustees contain union representatives,

Summer 2008HUDSON I NSTITUTE 25

and are responsible for recommending fundingchanges and plan amendments based on incomingfinancial information. The argument that the Team -sters do not control the management of the fund in aweek-to-week sense is therefore irrelevant. The im pli -cit claim that the decisions of the Teamsters, includ-ing the benefits and funding schedules, are less impor-tant than market performance is only part of thestory. If a fund begins to fall behind because of mar-ket performance, the sponsors have a responsibilityto take countervailing measures, by reducing prom-ised benefits or increasing contributions or both.

In 2003, the Teamsters took just such action,reducing benefits to keep the fund from collapsingentirely. This change required not only a reductionin promised payments, but also pressure from theTeamsters for employers to contribute more. Doc -uments on the Teamsters’ web site argue that thefunding inadequacy was not the union’s fault.

“Every pension fund in the United States isunder similar pressure, and that every conflictbetween workers and employers…centersaround rapidly rising health care costs…thereare more retirees than active participants in theCentral States Funds, and that retirees areretiring earlier and living longer …than anyoneever anticipated…as major Fund employers goout of business there are no longer active par-ticipants contributing into the Fund for bene-fits collected by former employees.”21

Many of these points are valid. Unexpected in -creases in costs and demographic shifts make the val-uation of pensions more complex. But the last argu-ment, about the decline in the number of activeworkers who pay into the fund, is disingenuous. Thecontributions of active workers are not supposed topay the benefits of former employees. They are sup-posed to be invested. Systems in which current pay-ments fund current benefits are called unfunded sys-tems. The Social Security Admin istra tion runs onthis model. A truly well-funded system, on the other

hand, would ensure that the fund had enough invest-ment income to pay retirement benefits.

This language suggests that someone in the Team -s ters, whether in upper-level management, mediadepartments, or financial services, funda ment allymisunderstands the nature of the Central StatesFund —or, perhaps, is practicing misdirection. Asystem in which you promise to take an individual’smoney, invest it, and return a certain amount tohim in the future—but instead use it to fulfill cur-rent similar obligations to another person—is notcalled a pension plan. It is called a Ponzi scheme.Now, the Central States Fund is not a Ponzi scheme,as it is not run solely for the benefit of its adminis-trators and early adherents. It is merely a poorly-funded pension plan. But this language and currentsituation demonstrate the problems with Teamsterspension fund.

The eventual buyout of 45,000 UPS workers’pensions by their employer should not, therefore,have come as a surprise. Those lucky workers willhave a better shot at their full pension. The benefitsare generous and supported by UPS alone.

The UPS experience highlights an important ques-tion that union leaders seem unwilling to answer.The problem lies, they claim, in escalating costs,poor market performance, and a rising ratio ofretirees to workers. But why were these issues notaddressed promptly when they became clear? TheTeamsters knew the fund was in trouble as early as2002, and continued to allow a funding arrangementinadequate to cover growing liabilities. The Team -sters deserve some of the blame. In their 2003 reduc-tion of benefits, they said, “putting the entire burdenon increased employer contributions would lead tothe bankruptcy of dozens of Teamster employers andthe loss of thousands of Teamster jobs…whichwould end up canceling out the effect of the in -creased employer contributions.”22

James P. Hoffa, president of the InternationalBrotherhood of Teamsters, did not try to create amanageable contribution/benefit scenario until newlegislation forced him and his colleagues to admit

Summer 2008HUDSON I NSTITUTE 26

that their pension fund was in a severe condition.Indeed, as late as October 4, 2007, the Central StatesFund issued the following statement for Mr. Hoffa:“I can assure you that…there are no plans to reducebenefits for any active or retired participant.”23

It is not the job of the investment managers of apension fund—in this case, J.P. Morgan and Gold -man Sachs—to ensure that the sponsors have agreedto make actuarially adequate contributions. It isonly their responsibility to manage funds res pon -sibly and to alert the administrators if agreed contri-butions are not made.

Ironically, Mr. Hoffa and the IBT’s national rep-resentatives have included among their legislativepriorities “[to] ensure that all Americans are provid-ed with retirement security and work to reverse thedecline in defined pension plans.”24 It is disingenu-ous to claim that the existence of a defined benefitpension plan will automatically ensure retirementsecurity, especially considering the condition ofCentral States’ pension fund. Union leaders areexpected to seek legislative protections and benefitsfor workers. But union members might be wellserved to push their leaders to ensure their benefitsare secure before the leaders lobby Congress tomandate expanding them.

Plumbers and PipefittersNational Pension Fund

In 2005, the Plumbers and Pipefitters NationalPension Fund (known as UA National PensionFund) supported 147,682 people, including

71,570 current workers. Unfortunately, the 2005trustees of the fund were inexperienced. An earlierboard had been removed in 2004 following litiga-tion by the U.S. Department of Labor.

According to DOL documents, this story beganin 1997, when the UA National Pension Fundtrustees agreed to purchase the Diplomat Resort and

Country Club in Hollywood, FL. Without dis-cussing proposed renovations, architectural designsor budget, they spent $40 million of fund money topay in part for the purchase of the seaside resort andagreed to spend an additional $60 million in pen-sion funds to pay for the initial redevelopment.

Their overseer proposed a plan to tear down andrebuild the hotel, increasing total expected costsfrom $277 million to $400 million. In April 1998,the plan was approved. The trustees of the UAPension Fund retained a construction manager withno limit on costs or time. They had essentially ag -reed to pay a group an unspecified and open-endedsum of money for an indefinite period of time on aproject whose benefits they had never considered.Why? Because the construction team involved tworelatives of an official with UA. The trustees invest-ed another $50 million after it became clear thereturn on the original investment in the Diplomatresort was expected to be low.25

It is unsurprising, therefore, that in 2005 the UAPension Fund had only $4.1 billion to cover $8.2billion in promised benefits. In the end, it is estimat-ed that this mistake cost the union “only” $800 mil-lion in pension funds.26 Yet if the Diplomat schemewas at all representative of how their predecessorsran the UA Fund, one should expect more lossesfrom past trustees’ imprudent management.

Poor financial decisions— whether through mal-ice or error—can have a long-lasting effect on unionpension plans. Among these poor decisions is nottrying to shore up a pension fund when it falls be -hind. Other pensions mentioned in this paper, whilefalling behind in annual required expenses, at leastoffset their low payments with amortized credits—actual money that the union had acquired, eitherthrough higher-than-expected returns, a cut in ben-efits, or other changes that reduced liabilities orincreased assets.

The UA National Pension Fund trustees did nothave a deficiency in their funding, but they did notpay their annual charges. Employer contributionsplus amortized credits equaled $540 million in

Summer 2008HUDSON I NSTITUTE 27

2005. Total costs for the year equaled $602 million.The reason that the UA National Pension Fund hasgotten away with not paying its annual expenses(despite having less than 50 percent of the money itwould, eventually, need to pay future obligations) isthat it had contributed more than required in thepast. Its credit grew every year in which the fundcovered its costs, accumulating interest at a constantrate that ignores actual returns on the fund. Everyyear that the fund fell behind, the credits werereduced to cover the deficiency.

Former trustees of the UA National Pension Fundwere poor managers of the union members’ finan-cial future. But the new ones have not shown them-selves to be tremendous improvements. They areignoring a $4.2 billion deficit by relying on financialsleight-of-hand. The Teamsters are right that theproblem cannot be solved by just increasing employ-er contributions. This fund, however, as of June2008 either had 65 percent of its required funds orhad not yet come to a consensus with EBSA. Thus itstill has not been caught in the Pension ProtectionAct compliance net. Even as other pension fundshave acknowledged their unsustainable practicesand tried to remedy them, the UA National PensionFund continues to use credit to cover its overall def -icit in pension funding. As a result, it has continuedto do nothing about its poor balance.

Laborers National Pension Fund

The Laborers National Pension Fund sup-ported 45,849 people in 2005, 14,433 ofwhom were current workers. It had $1.63

billion in assets, and owed $2.2 billion in futurebenefits. An almost 75 percent funding level putLabor ers in a troubled, but not dire, situation.

The fund had two major problems. First, likemany union pension plans, it was not paying all of

its annual charges, meaning that it was moving evenfurther away from a fully funded plan.

Second, one of its bookkeepers, Maile Epley, plead-ed guilty in 2006 to stealing $302,021.45 from theLaborers Pension Fund over the course of her 16-yearcareer at the fund. In January 2007, she was sentencedto two years in prison and ordered to pay back themoney stolen.27 But had the money re mained in thepension fund, returns from investment and com-pounded interest would have in creased its value.

Ms. Epley’s ability to embezzle more than$300,000 undetected for 16 years suggests a designflaw in defined benefit pension plans generally. It isthat the money involved in union pension funds isvast. The largest funds have billions of dollars ofassets. In addition to the temptation involved forpeople even tangentially dealing with this money, itis nearly impossible to monitor such large flows.

If the Laborers had a defined contribution pen-sion plan, then workers would have a flat amountdeducted from each paycheck and deposited intotheir individual retirement accounts. It would be -come apparent within three months, if not sooner(de pending on how accessible the pension state-ments were), if some intermediary had divertedfunds. With defined benefit plans, money is trans-ferred at almost random intervals between employ-ers, the union, and plan administrators.

The only way to tell that it all gets to the rightplace is to have two sets of books, one kept by thoseresponsible for dispatching funds to the moneyman ager and one kept by the money manager. Theentries should match. Someone must be responsiblefor comparing both, possibly an auditor who isunconnected to either party.

Defined benefit plans are obscure and complex.They get into trouble because workers have no ideawhat goes on with them. Contributions are made byparticipating employers and may not equal annualcosts. Money is gained and lost constantly. Eventhough workers might be told how much money isin the account, this does not tell them anythingabout the security of their future income.

Summer 2008HUDSON I NSTITUTE 28