uniapravi was founded on 1964, and it is an international ... congress 2013/2... · 3 household and...

TRANSCRIPT

Of. Central Bajada Balta 169, 4º Piso, Lima 18, Perú Casilla Postal 18-1366

Teléfonos: (51-1) 444-6605/444-6611/444-6975, Fax: (51-1) 444-6600

E-mail: [email protected]

Website: www.uniapravi.org

UNIAPRAVI was founded on 1964, and it is an international private institution, non profit organisation

which is part of the advisory Committe of the Economic ans Social Council of the United Nations.

It has over 200 members of 27 countries in the American Continent

Population in Latin America

118,6

67,6

28,4 28,017,3 15,0 11,1 8,2

2,0

194,9

113,7

46,140,9

30,0 29,8

17,4 15,03,6

Brasil México Colombia Argentina Perú Venezuela Chile Ecuador Panamá

1980 2011

Population in Selected Countries 1980-2011* (million people)

•The population in Latin America has grown 1.7 times in 30 years

- FMI – World Economic Outlook –

1.6 V

1.7 V

1.6 V 1.5 V 1.7 V 2.0 V 1.6 V 1.8 V 1.8 V

2

MÉXICO 2012

3

Household and Housing growth in

Latin America 2010 to 2020

During the present decade the number of new households will

increase by nearly 50 million - and they will demand over 40

million new houses in the middle and large cities

4

The major challange is to plan, finance and develop over 20 million

houses in the largest 35 cities in Latin America until the year 2020

This will require investments in Infrastructure, housing and

mortgages in the size of 1,3 trillion USD

Housing in Latin America’s Largest Cities

2010 to 2020

Strategic Goals 2020

1. Public and Private coordination that promotes the

creation of long term institutions

2. Develop a stronger real estate market and a deeper

financial system in order to reach 4% of GNP

3. Use the Housing sector as a driving force in economic

development

4. Promote the development of competitive cities with

urban desing, that create wealth, employment and

sustainable growth.

Challenges in Creating

New Houses and Cities

Land

Urban Development

Infrastructure

Construction

Mortgages

6

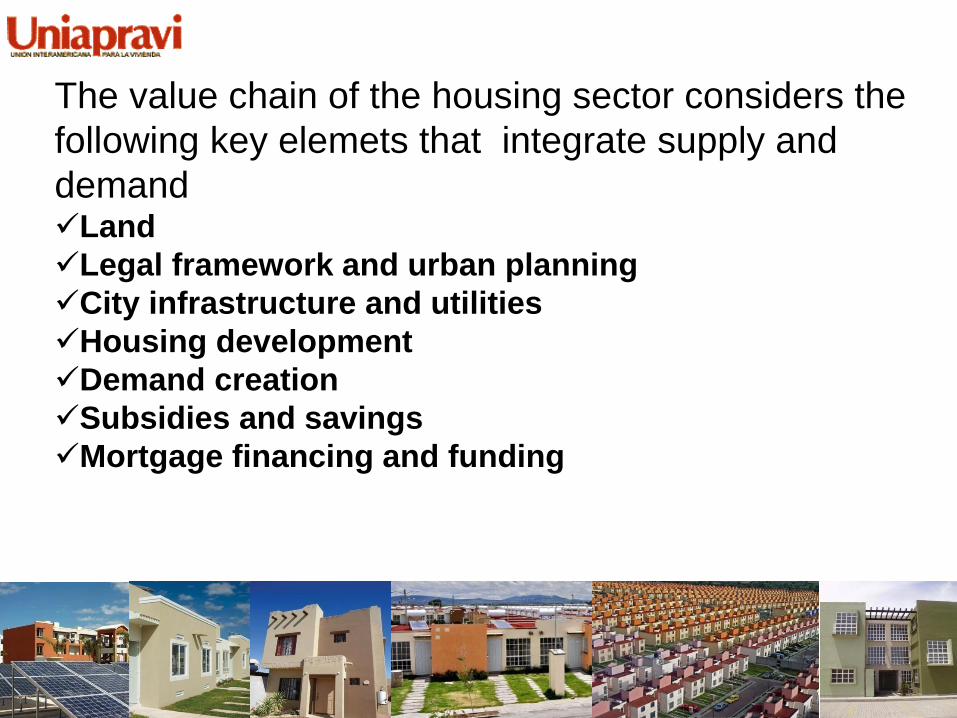

The value chain of the housing sector considers the

following key elemets that integrate supply and

demand Land

Legal framework and urban planning

City infrastructure and utilities

Housing development

Demand creation

Subsidies and savings

Mortgage financing and funding

1,800,000

Land Infrastructure Construction

Savings

& subsidies

Mortgage

finance

3,500,000

2013 2015

2017 2019 2021

Permits

Housing Process as a Pipeline

Units

Units

Developing the Supply

Supply elements

1. Urban development - formal and Informal improvement of present conditions

2. Urban planning for new communities

3. Financing the municipal services and utilities

4. Government sponsored entities and development banks

5. Public and private policies and coordination

6. Capital investment

Land Infrestructure Savings

& subsidies

Mortgage

finance Permits

Construction

Fuente: Softec

Unidades Valor Total

Distribution of Latin America´s Housing Inventory

Media 100m2

( 55,000 -100,000 USD)

Entry Subsidised 45m2

(10 -20,000 USD)

Social 50m2

(20 -55,000 USD)

Residencial 200m2

(100-200,000 USD)

35% of the housing stock represents

75% of the value of houses

0

%

100%

60%

40%

20%

80%

150 million

Ban

ks

M

ort

ga

ge

an

d S

&L

Residencial Plus 350m2

(> 200,000 USD)

Rural 30m2

7,200 trillion USD

Urban development: formal vs informal

Disorder in the use of land and development

Use of land in high risk areas and

without the proper legal ownership

Explosive migration to the cities

Disorder in the

development of formal

vs informal solutions

Before After

Projects that regenerate inner Cities

Before After

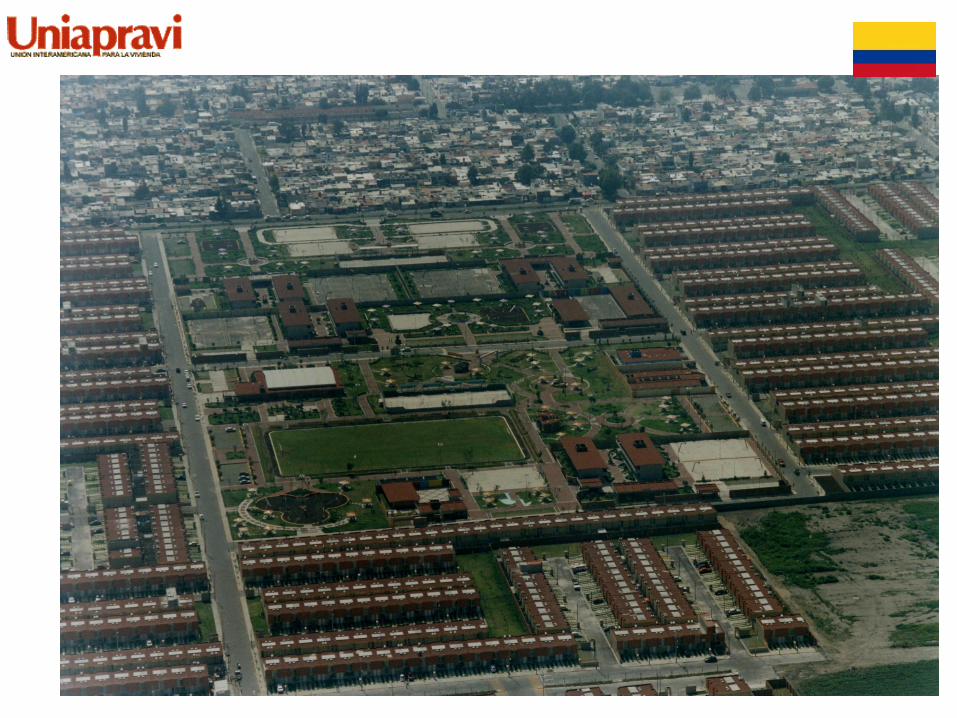

Mexico 1990 -2010

• In the last 20 years Mexico’s housing stock grew by 15 million

houses, from 21 million to 36 million dwellings

• Eight million houses were produced by the industrial process and

seven million in a disordered way

• The challenge is to reduce the informal production that has

limitations in terms of legal ownership, municipal services and

capital formation

Distribution of Mexico´s Housing Inventory

Urban planning

• In the last ten years, innitiatives for better land and city

organization have been developed

• The organization of urban development has been more

on a project by project basis

• This has improved the conditions of the housing

developments because

– It is legal and complies with local requirements

– It creates wealth for the families

– It can be financed

– It has a lower negative impact on resources and

promotes sustainability and ecological measures

14

Public and Private Policies

• In the Latin American region, a key element for better urban

development is the formulation of public and private long term

policies.

• The role of the Government is very important. It creates the conditions

for new developments and city planning

• The introduction/development of infrastructure – water, sewage, roads

and electricity – remains under goverment control

There have been interesting initiatives in Brazil and Mexico:

– Ministries that integrate housing, infrastructure and land use

– Advisory boards with members from the federal goverment, local

autorities, private sector and experts

– Long term vision and economic development as the key driving

force

19

1. ESTRUCTURA ORGANIZACIONAL MINISTERIO DE LAS CIUDADES

SECRETARIA

NACIONAL DE

HABITACIÓN

SECRETARIA NACIONAL

DE PROGRAMAS

URBANOS

MINISTRO

SECRETARIA NACIONAL

DE TRANSPORTE Y

MOVILIDAD URBANA

CONSEJO DE LAS CIUDADES

SECRETARIA NACIONAL

DE PROGRAMAS

URBANOS

SECRETARIA

NACIONAL DE

HABITACIÓN

SECRETARIA NACIONAL

DE PROGRAMAS

URBANOS

SECRETARIA NACIONAL DE

SANEAMENTO AMBIENTAL

SECRETARIA NACIONAL DE

HABITACIÓN SECRETARIA NACIONAL DE

PROGRAMAS URBANOS

CBTU

TRENSURB

DENATRAN

GABINETE

CBTU

TRENSURB

CBTU

TRENSURB

CONSEJO DE LAS CIUDADES

CBTU

TRENSURB

GABINETE

CONSEJO DE LAS CIUDADES

CBTU

TRENSURB

GABINETE

CONSEJO DE LAS CIUDADES

CBTU

TRENSURB

DENATRAN SERETARIA EXECUTIVA

GABINETE

CONSEJO DE LAS CIUDADES

CONTRAN

CBTU

TRENSURB

SECRETARIA NACIONAL DE

HABITACIÓN SECRETARIA NACIONAL DE

PROGRAMAS URBANOS

SECRETARIA NACIONAL DE

SANEAMENTO AMBIENTAL

SECRETARIA NACIONAL DE

HABITACIÓN SECRETARIA NACIONAL DE

PROGRAMAS URBANOS

SECRETARIA

NACIONAL DE

HABITACIÓN

SECRETARIA NACIONAL

DE PROGRAMAS

URBANOS

SEDATU

URBAN AND REGIONAL

INFREASTRUCTURE

CONSEJO DE LAS CIUDADES

SECRETARIA NACIONAL

DE PROGRAMAS

URBANOS

SECRETARIA

NACIONAL DE

HABITACIÓN

SECRETARIA NACIONAL

DE PROGRAMAS

URBANOS

SECRETARIA NACIONAL DE

SANEAMENTO AMBIENTAL

SECRETARIA NACIONAL DE

HABITACIÓN SECRETARIA NACIONAL DE

PROGRAMAS URBANOS

CONSEJO DE LAS CIUDADES CONSEJO DE LAS CIUDADES CONSEJO DE LAS CIUDADES

COMISION

INTERSECRETARIAL

CONSEJO DE NACIONAL DE

VIVIENDA

SECRETARIA NACIONAL DE

HABITACIÓN SECRETARIA NACIONAL DE

PROGRAMAS URBANOS

URBAN AND LAND

REGULATIONS HOUSING LAND REGISTRY

J Yarza Wien 2013

Challenges in Creating

new Houses and cities Demand

Formal vs Not Formal

Income

Mortgage availability

21

The Demand for Housing

1. Increasing the disposable income

2. Subsidies

3. Savings

4. Mortgage market development

Demand elements

Land Infrastructure Savings

& subsidies

Mortgage

finance Permits

Construction

Economic Outlook

2.294

1.662

716

472374 302 300

127 51

FMI – World Economic Outlook

17.516 17.222

14.610 14.09712.568

11.76910.249 10.062

8.492

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

GNP 2011 (Billions USD – PPP) GNP per capita 2011 (USD – PPP)

•The economic outlook is positive and the economy is expected to continue to grow in the

future throughout Latin America

•There has been a continiuous growth in consumption and wealth

23

Employment

Asobancaria Colombia 2012 24

76% 70% 70% 70% 66% 66%

60% 56% 54%

48% 47% 47% 44% 43% 42% 38% 32%

24% 30% 30% 31% 34% 34%

40% 44% 46% 52% 53% 53% 56% 57% 58% 62%

68%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% Informalidad % Formalidad

Urban Employment in Latinamerica

MÉXICO 2012

J Yarza Vienna 2013

25

Middle Class formation

• Throughout the region there has been an increase in the formation of

middle class families

• These families have used their homes as a source of capital formation

• In the next ten years we will see an upward mobility of the families in

Latin America

Income Distribution in Brasil

Income Distribution in Mexico

Relationship of the Banking assets to GNP

Fontes: Global Property Guide, Bancos Centrais

0%

50%

100%

150%

200%

250%

Mexico Brasil Chile Colombia España India UK USA

11% 6%19%

5%

45%

3%

73%86%

25%

47%63%

32%

110%

35%

150%

210%

Cartera Bancaria e Hipotecaria

Cartera Hipotecaria /PIB Cartera Bancaria/PIB

The banking system in Latin America has the potential to grow;

in the next decade, it might achieve a size comparable to

European countries.

Rates and Payments

27

0,00%

2,00%

4,00%

6,00%

8,00%

10,00%

12,00%

Mexico Brasil Chile Colombia Perú

Delinquency Rate %

0%

2%

4%

6%

8%

10%

12%

14%

16%

Mexico Brasil Chile Colombia Perú

Inflation and Mortgage Rates

Tasa H

tasa CT

INPC

• Interest rates are at a low point in this moment, allowing families to enhance

their buying capacity at a reasonable monthly payment

• Delinquency rates are relatively low, considering the effects of the crisis and

the growth of the mortgage portfolio

J Yarza Wien 2013

Challenges in Creating

New Houses and Cities Forecast for 2013

Conclusions

Best Practices

29

Mortgage Finance Fundamentals Expected to GROW in 2013

We expect the 2013 mortgage market activity level to be larger than last year’s

level for a number of reasons, including:

1. Interest rates are forecasted to remain at current low levels during the next

12 months;

2. Low cap rates are expected and moderate levels of price increases

3. Housing sales are expected to remain healthy in metro areas with solid

forecasted fundamentals

4.The moderate funding for construction loans will influence below-average

construction starts;

5. The expectation of continued improvement in job growth.

30

2012 Economic recovery Housing as a key driving force Subsidies Housing sector 2% of GNP

2015 Housing as social & economic driving force Shared vision of the housing sector Mortgage sector as key element Urban planning Housing sector 3% of GNP

2020 Integration of the real estate markets Development of housing, mortgage and stock markets Competitive cities Green agenda Housing sector 4% of GNP

• Housing for Latin America

• 50 millon houses

• 1.3 Trillion USD

Strategic Vision 2010-2025

Competitive

cities and

regional

economics

Public &

private

coordination

Urban

planning for

housing and

cities

Develop

mortgage and

financial

system

Wealth

creation and

social

mobility

Reduce

poverty and

targeted

subsidies

Conclusions

There are six strategic lines that need to be pursued