understanding the fair debt collection practices act … the fair debt collection ... mailed to the...

TRANSCRIPT

NALS EDUCATION CONFERENCE & NATIONAL FORUM

October 8 , 2015

Kim Cooper, Esq. Cooper Law Group Ltd. 8668 Spring Mountain Rd. Suite 101 Las Vegas, Nevada 89135 [email protected]

Understanding the Fair Debt Collection

Practices Act 15 USC § 1692 et seq.

C o n g r e s s f o u n d t h a t a b u s i v e d e b t c o l l e c t i o n p r a c t i c e s c o n t r i b u t e t o t h e n u m b e r o f p e r s o n a l b a n k r u p t c i e s , t o m a r i t a l i n s t a b i l i t y , t o t h e l o s s o f j o b s , a n d t o i n v a s i o n s o f i n d i v i d u a l p r i v a c y .

T h e p u r p o s e o f t h e F D C P A i s t o e l i m i n a t e a b u s i v e d e b t c o l l e c t i o n p r a c t i c e s b y d e b t c o l l e c t o r s , t o p r o m o t e f a i r d e b t c o l l e c t i o n , a n d t o p r o t e c t c o n s u m e r s a g a i n s t d e b t c o l l e c t i o n a b u s e s .

T h e F D C P A p r o v i d e s g u i d e l i n e s t o d e b t c o l l e c t o r s , d e f i n e s t h e r i g h t s o f c o n s u m e r s a n d p r e s c r i b e s p e n a l t i e s a n d r e m e d i e s f o r v i o l a t i o n s .

Fair Debt Collection Practices Act PURPOSE

WHO IS A CONSUMER? WHAT IS A DEBT?

Consumer: any natural person obligated or allegedly obligated to pay any debt. 15 USC § 1692a(3)

Consumer also includes the consumer's spouse, lawyer, parent, guardian, executor, administrator or any person with the express permission of the consumer.

Debt: any obligation or alleged obligation of a consumer to pay money arising out of a transaction in which the money, property, insurance, or services which are the subject of the transaction are primarily for personal, family, or household purposes, whether or not such obligation has been reduced to judgment. 15 USC § 1692a(5)

Fair Debt Collection Practices Act

D e b t C o l l e c t o r : a n y p e r s o n o r b u s i n e s s t h e p r i n c i p a l p u r p o s e o f w h i c h i s t h e c o l l e c t i o n o f a n y d e b t s , o r w h o r e g u l a r l y c o l l e c t s o r a t t e m p t s t o c o l l e c t , d i r e c t l y o r i n d i r e c t l y , d e b t s o w e d o r d u e o r a s s e r t e d t o b e o w e d o r d u e a n o t h e r . 1 5 U S C § 1 6 9 2 a ( 6 )

E x a m p l e s :

• C o l l e c t i o n a g e n c i e s

• A t t o r n e y s ( o r l a w f i r m s ) w h o r e g u l a r l y c o l l e c t d e b t s

• D e b t b u y e r s ( a s a p o s t - d e f a u l t a s s i g n e e )

• D e b t c o l l e c t i o n l a w s u i t s

• C r e d i t o r i f c o l l e c t i n g u n d e r a n o t h e r n a m e

Fair Debt Collection Practices Act WHO IS A DEBT COLLECTOR?

IS AN ATTORNEY A DEBT COLLECTOR?

Congress amended the FDCPA in 1986 to delete an exemption and expressly include attorneys.

An attorney is a debt collector if the attorney “regularly collects or attempts to collect, directly or indirectly, debts owed or due or asserted to be owed or due another.” 15 USC § 1692a(6)

IS AN ATTORNEY A DEBT COLLECTOR?

Regularly Collects – 5 factor test:

1. Number of collection cases undertaken;

2. Number, frequency, and pattern of collection communications;

3. Staff and systems assigned to collections work;

4. Marketing of its collection services;

5. Nature of the work generally done for the client.

Goldstein v. Hutton, Ingram, Yuzek, Gainen, Carroll & Bertolotti, 374 F.3d 56 (2nd Cir. 2004)

IS AN ATTORNEY A DEBT COLLECTOR?

2nd Circuit: Goldstein, 374 F.3d 56 (2nd Cir. 2004) (145 notices demanding delinquent rent in 12 month period as part of an ongoing relationship with a landlord was “regularly” collecting debt covered by the FDCPA despite the collection work constituting less than 0.5% of revenues.)

5th Circuit: Garrett v. Derbes, 110 F.3d 317 (5th Cir. 1997) (639 cases in 9 months represented 0.5% of practice.)

IS AN ATTORNEY A DEBT COLLECTOR?

10th Circuit: James v. Wadas, 724 F.3d 1312 (10th Cir. 2013) (Adopting 5 factor test in Goldstein. Not debt collector where never sent demand letter, filed 6-8 collection lawsuits in 10 years, and preceding year’s collection revenue ≥ $1,700.)

3rd Circuit: Crossley v. Lieberman, 868 F.2d 566, 569 (3d Cir. 1989) (“any attorney who engages in collection activities more than a handful of times per year must comply with the FDCPA”)

IS AN ATTORNEY A DEBT COLLECTOR?

But see, Schroyer v. Frankel, 197 F.3d 1170 (6th Cir. 1999)

For a court to find that an attorney or law firm “regularly” collects debts, “a plaintiff must show that the attorney or law firm collects debts as matter of course for its clients or for some clients, or collects debts as a substantial, but not principal, part of his or its general law practice.”

IS FILING A LAWSUIT TO COLLECT A DEBT COVERED UNDER THE FDCPA?

Yes, if the attorney meets the definition of a “debt collector.”

The FDCPA “does apply to lawyers engaged in litigation…In ordinary English, a lawyer who regularly tries to obtain payment of consumer debts through legal proceedings is a lawyer who regularly ‘attempts’ to ‘collect’ those consumer debts.” Heintz v. Jenkins, 514 U.S. 291, 115 S. Ct. 1489, 131 L. Ed. 2d 395 (1995)

• Original creditor (unless using another name)

• Assignee before default

• Government agencies

• Process servers

• Col lect ion is incidental to a bona f ide f iduciary obl igat ion.

15 USC § 1692a(6)(A) -(F)

Fair Debt Collection Practices Act WHO IS NOT A DEBT COLLECTOR?

WHO IS A THIRD PARTY : Anyone who is not a consumer.

WHAT IS THE PURPOSE OF CONTACT : The only permiss ible purpose for contact ing a third party is to obtain locat ion information .

WHAT IS LOCATION INFORMATION : I t is the consumer’s home address, telephone number and place of employment.

Fair Debt Collection Practices Act CONTACTING THIRD PARTIES

CONTACTING THIRD PARTIES

A debt collector representative MUST:

• Identify himself;

• State that he is confirming or correcting location information; and

• Identify his employer only if expressly requested by the third party.

CONTACTING THIRD PARTIES

A debt collector CANNOT:

• State that the consumer owes any debt;

• Communicate with a third party more than once unless:

• Requested to do so by the third party or

• Reasonably believes that the third party’s earlier response was incomplete and now the third party has correct or complete location information.

CONTACTING THIRD PARTIES

FDCPA VIOLATION

If the debt collector already has a consumer’s location information then there is NO permissible purpose to contact a third party.

NOTE: both the consumer and third party have a claim against the debt collector for violation of the FDCPA.

Debt col lector CANNOT communicate with consumer:

• At any unusual t ime or p lace which should be known to be inconvenient

• Default rule: no calls before 8:00 AM or after 9:00 PM (consumer's time zone)

• I f a consumer i s represented by counsel

• At consumer's p lace of employment i f debt col lector knows or has reason to know that the employer prohib i ts i t . 15 USC § 1692c

Fair Debt Collection Practices Act COMMUNICATION WITH A CONSUMER

COMMUNICATION WITH A CONSUMER

If the consumer notifies the debt collector in writing that the consumer refuses to pay the debt or request the debt collector to cease communications, then the debt collector MUST immediately stop all communications with the consumer.

15 USC § 1692c(c)

Except…

COMMUNICATION WITH A CONSUMER

The debt collector can notify the consumer that:

Further collection efforts are being terminated (but the debt collector CANNOT ask for money);

Debt collector or creditor may invoke specified remedies as long as the debt collector normally invokes them;

Debt collector or creditor intends to invoke a specified remedy.

COMMUNICATION WITH A CONSUMER

MINI MIRANDA*

First communication with the consumer requires that the debt collector state that it is attempting to collect a debt and that any information obtained will be used for that purpose.

Subsequent communications with a consumer requires that the debt collector state that the communication is from a debt collector.

15 USC § 1692e(11)

*Third party implications for phone calls and voicemails.

COMMUNICATION WITH A CONSUMER

MINI MIRANDA

Except…Mini Mirada does not apply to a formal pleading made in connection with a legal action.

Senftle v. Landau, 390 F. Supp. 2d 463 (D. Md. 2005) (section 1692e(11) unambiguously exempts formal pleadings from its purview)

Hauk v. LVNV Funding, L.L.C., 749 F. Supp. 2d 358 (D. Md. 2010) (interrogatory is not exempt as formal pleading)

Mini Miranda

This is an attempt to collect a debt. Any information obtained will be used for that purpose.

COMMUNICATION WITH A CONSUMER

Validation of Debt

“G Notice”

A consumer has the right to verify and validate the debt being collected.

Within 5 days after the initial communication with a consumer in connection with the collection of any debt, the debt collector shall send the consumer a written notice.

15 USC § 1692g(a)

COMMUNICATION WITH A CONSUMER

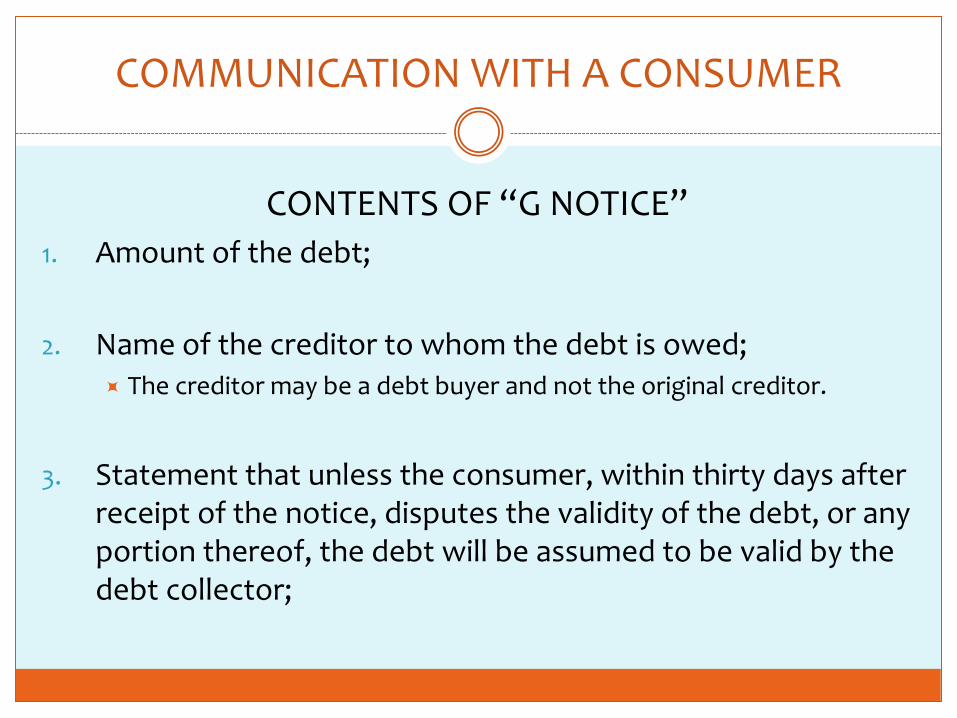

CONTENTS OF “G NOTICE”

1. Amount of the debt;

2. Name of the creditor to whom the debt is owed; The creditor may be a debt buyer and not the original creditor.

3. Statement that unless the consumer, within thirty days after receipt of the notice, disputes the validity of the debt, or any portion thereof, the debt will be assumed to be valid by the debt collector;

COMMUNICATION WITH A CONSUMER

CONTENTS OF “G NOTICE”

4. Statement that if the consumer notifies the debt collector in writing within the thirty-day period that the debt, or any portion thereof, is disputed, the debt collector will obtain verification of the debt or a copy of a judgment against the consumer and a copy of such verification or judgment will be mailed to the consumer by the debt collector; and

5. Statement that, upon the consumer's written request within

the thirty-day period, the debt collector will provide the consumer with the name and address of the original creditor, if different from the current creditor.

CONSUMER DEBT COLLECTOR

If a consumer disputes the debt in writing or requests verification within the 30 day period

Debt collector MUST stop all collection activities until the debt collector:

1. Validates the debt or

2. Obtains the name and address of the original creditor and mails it to the consumer

15 USC § 1692g(b)

COMMUNICATION WITH A CONSUMER “G NOTICE”

Any collection activities and communication during the 30-day period may not overshadow or be inconsistent with the disclosure of the consumer’s right to dispute the debt or request the name and address of the original creditor.

15 USC § 1692g(b

Consumer’s fai lure to dispute a debt is not an admission or waiver.

15 USC § 1692g(c)

Fair Debt Collection Practices Act NO WAIVER

§ 2 2 7 ( b ) R e s t r i c t i o n s o n u s e o f a u t o m a t e d t e l e p h o n e e q u i p m e n t . I t s h a l l b e u n l a w f u l …

( A ) t o m a k e a n y c a l l ( o t h e r t h a n a c a l l m a d e f o r e m e r g e n c y p u r p o s e s o r m a d e w i t h t h e p r i o r e x p r e s s c o n s e n t o f t h e c a l l e d p a r t y ) u s i n g a n y a u t o m a t i c t e l e p h o n e d i a l i n g s y s t e m o r a n a r t i f i c i a l o r p r e r e c o r d e d v o i c e . . .

( i i i ) t o a n y t e l e p h o n e n u m b e r a s s i g n e d t o a p a g i n g s e r v i c e , c e l l u l a r t e l e p h o n e s e r v i c e , s p e c i a l i z e d m o b i l e r a d i o s e r v i c e , o r o t h e r r a d i o c o m m o n c a r r i e r s e r v i c e , o r a n y s e r v i c e f o r w h i c h t h e c a l l e d p a r t y i s c h a r g e d f o r t h e c a l l .

4 7 U . S . C . § 2 2 7

Telephone Consumer Protection Act IMPACT ON DEBT COLLECTORS

Engage in any conduct the natural consequence of which is to harass, oppress, or abuse any person in connection with the collection of a debt.

1 5 U S C § 1 6 9 2 d

Fair Debt Collection Practices Act WHAT DEBT COLLECTORS CANNOT DO

UNFAIR OR UNCONSCIONABLE 15 USC § 1692d

Threaten to use or use violence against a person, her reputation, or her property

Use profanity or abusive language the natural consequence of which is to abuse the hearer or reader

Publish the name of the debtor, except to make accurate reports to credit reporting agencies

Call repeatedly with the intent to annoy, abuse, or harass any person at the called number

Call without disclosing the caller's identity Except when obtaining

location information from third parties

Use any false, deceptive, or misleading representation or means in connection with the collection of a debt .

1 5 U S C § 1 6 9 2 e

Fair Debt Collection Practices Act WHAT DEBT COLLECTORS CANNOT DO

FALSE, DECEPTIVE OR MISLEADING 15 USC § 1692e

Falsely represent or imply that a person is an attorney or a communication is from an attorney

Falsely imply that documents are or are not legal process

Collect any amount not expressly authorized by contract or law

Misrepresent the character, amount, or legal status of the debt

Falsely represent that the consumer committed a crime or other conduct to disgrace the consumer

Falsely threaten to take an action that cannot legally be taken or that the debt collector does not intent to take E.g. threaten consumer with

arrest, jail, seizure, garnishment, attachment, or the sale of consumer's property

E.g. suing or threatening to sue on time-barred debt

FALSE, DECEPTIVE OR MISLEADING 15 USC § 1692e

Use a false business name Falsely represent or imply

that the debt collector is affiliated with any gov’t agency

Falsely imply the debt collector is connected with a credit reporting agency

Threaten to or communicate false credit report information, including failure to report when a debt is disputed*

*Sometimes a FDCPA violation is also a violation of the Fair Credit Reporting Act (FCRA), 15 USC § 1681 et seq. Under the FCRA, a consumer has a right to the fair and accurate reporting of her credit information. A consumer is also entitled to certain privacy rights concerning her credit information and protection from the misuse of her credit information.

Use unfair or unconscionable means to collect or attempt to collect any debt.

1 5 U S C § 1 6 9 2 f

Fair Debt Collection Practices Act WHAT DEBT COLLECTORS CANNOT DO

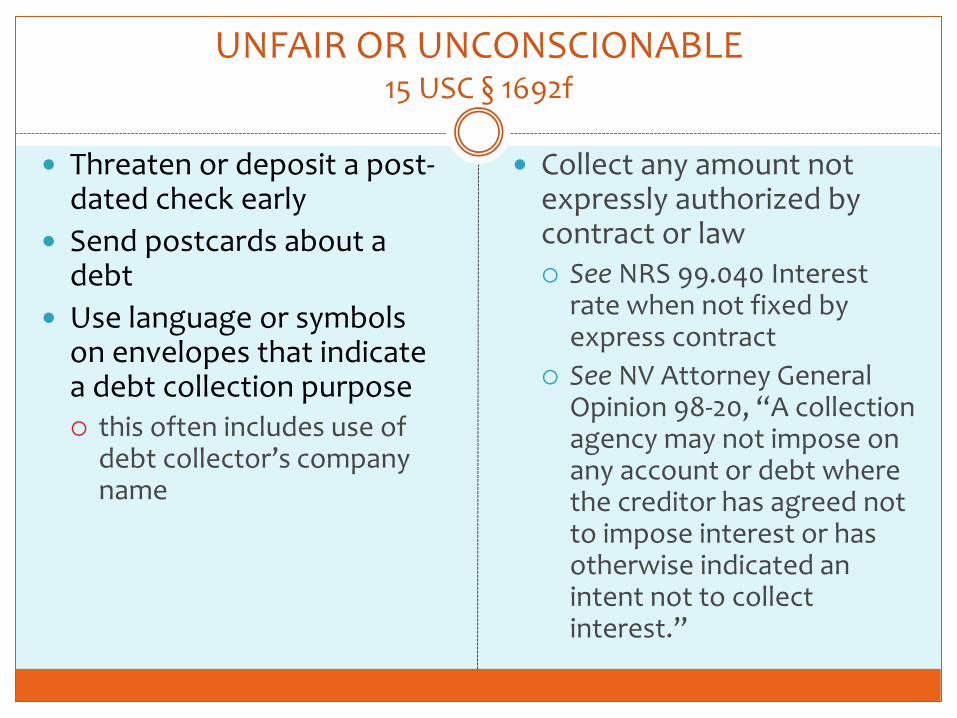

UNFAIR OR UNCONSCIONABLE 15 USC § 1692f

Threaten or deposit a post-dated check early

Send postcards about a debt

Use language or symbols on envelopes that indicate a debt collection purpose this often includes use of

debt collector’s company name

Collect any amount not expressly authorized by contract or law See NRS 99.040 Interest

rate when not fixed by express contract

See NV Attorney General Opinion 98-20, “A collection agency may not impose on any account or debt where the creditor has agreed not to impose interest or has otherwise indicated an intent not to collect interest.”

UNFAIR OR UNCONSCIONABLE 15 USC § 1692f

Debt collectors CANNOT threaten to take or take non-judicial action to effect dispossession or disablement of property if:

They do not have the present legal right to possess it;

The property is exempt by law; or

They do not intend to actually take it.

Repossessions and foreclosures are collection activities regulated by the FDCPA, but they are limited by 1692f(6) and interpretation of state foreclosure laws.

RECAP OF WHAT DEBT COLLECTORS HAVE TO DO

Provide proper G notice Must be included in initial

communication Within 5 days if initial

communication is by phone

Give the “Mini-Miranda” in every communication with the consumer. E.g. This communication is from

a debt collector and any information obtained will be used for that purpose. Calls* Voicemails* Letters

*Third party implications

Stop contacting the consumer if the consumer refuses to pay the debt or says ‘stop contact’ in writing. Some limited exceptions

If a consumer disputes the debt in writing or requests verification within the 30 day period, the debt collector must stop all collection activities until the debt collector validates the debt or obtains the name and address of the original creditor and mails it to the consumer.

D e b t s s e c u r e d b y r e a l p r o p e r t y

• I n t h e c o u n t y w h e r e t h e p r o p e r t y i s l o c a t e d .

A l l o t h e r d e b t s

• I n t h e c o u n t y w h e r e t h e c o n s u m e r s i g n e d t h e u n d e r l y i n g c o n t r a c t ; O R

• I n t h e c o u n t y w h e r e t h e c o n s u m e r n o w r e s i d e s .

1 5 U S C § 1 6 9 2 i ( a )

Fair Debt Collection Practices Act VENUE

A debt col lector may not be l iable i f the debt col lector shows by a preponderance of ev idence that the v io lat ion was not intent ional and resulted from a bona f ide error notwithstanding the maintenance of procedures reasonably adapted to avoid any such error .

1 5 U S C § 1 6 9 2 k

Fair Debt Collection Practices Act BONA FIDE ERROR DEFENSE

BONA FIDE ERROR DEFENSE

Debt collector MUST establish that a FDCPA violation: Was a factual error or an error of state or federal law,

other than the FDCPA;

Was unintentional;

Was the result of a bona fide error; and

Occurred even though the debt collector maintained procedures reasonably adapted to check for and avoid such errors.

Bona fide error is a narrow defense. McCollough v. Johnson, Rodenberg & Lauinger, 637 F.3d 939 (9th Cir. 2011)

Statutory Damages

• Indiv idual : up to $1 ,000

• Class : not to exceed the lesser of $500,000 or 1% of net worth

Actual damages, i f provable

• Emotional distress damages avai lable without meeting state tort requirements

Attorney's fees and costs 15 USC § 1692k

Fair Debt Collection Practices Act REMEDIES

K I M C O O P E R , E S Q .

C O O P E R L A W G R O U P L T D .

8 6 6 8 S P R I N G M O U N T A I N R D . S U I T E 1 0 1

L A S V E G A S , N E V A D A 8 9 1 3 5

K C O O P E R @ C O O P E R L A W L T D . C O M

QUESTIONS?