understanding and countering the private label challenge · understanding and countering the...

TRANSCRIPT

Understanding and Countering the

Private Label Challenge

Prof. dr. Jan-Benedict E.M. Steenkamp

Tilburg University

Zaventem (Brussels), March 20, 2003

Tilburg University (2)

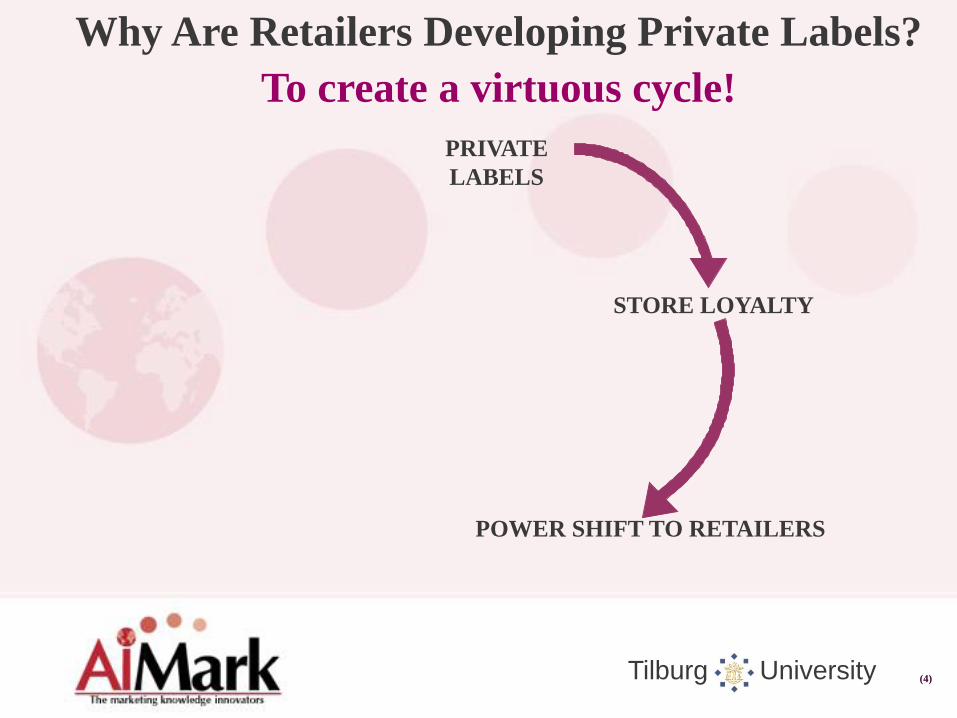

Why Are Retailers Developing Private Labels?

To create a virtuous cycle!

PRIVATE

LABELS

STORE LOYALTY

Tilburg University (3)

0

5

10

15

20

25

30

0 5 10 15 20 25

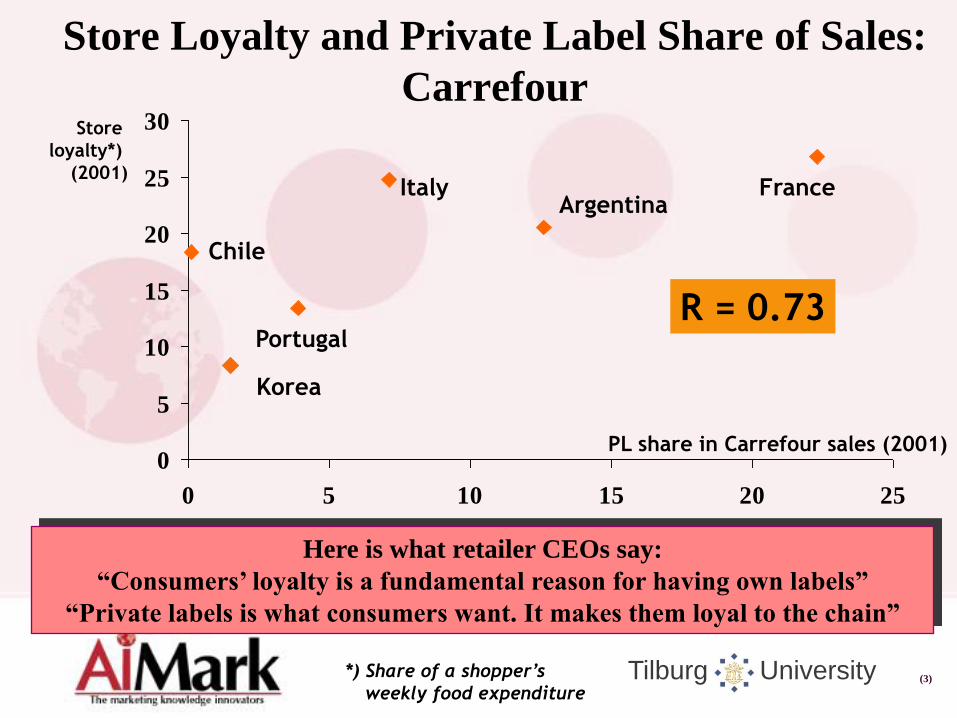

PL share in Carrefour sales (2001)

Store

loyalty*)

(2001) France

Chile

Portugal

Italy Argentina

Korea

Store Loyalty and Private Label Share of Sales:

Carrefour

*) Share of a shopper’s

weekly food expenditure

R = 0.73

Here is what retailer CEOs say:

“Consumers’ loyalty is a fundamental reason for having own labels”

“Private labels is what consumers want. It makes them loyal to the chain”

Tilburg University (4)

Why Are Retailers Developing Private Labels?

To create a virtuous cycle!

PRIVATE

LABELS

STORE LOYALTY

POWER SHIFT TO RETAILERS

Tilburg University (5)

Retailers Are Getting Bigger and Bigger

Vis-à-Vis FMCG Manufacturers

Global Top-10 Sales

Retailers 2001

Rank in FMCGs $bn

1 Wa1-Mart 243.3

2 Carrefour 69.5

3 Royal Ahold 66.6

4 Kroger 60.0

5 Metro 49.5

6 Albertson’s 42.8

7 Kmart 38.7

8 Safeway 38.3

9 Costco 38.1

10 Tesco 38.1

Global Top-10 Sales

Manufacturers 2001

Rank in FMCGs $bn

1 Philip Morris 89.9

2 Nestlé 51.0

3 Unilever 46.7

4 P&G 40.2

5 BAT 37.4

6 Japan Tobacco 31.4

7 ConAgra 24.1

8 PepsiCo 26.9

9 Sara Lee 17.6

10 Diageo 16.4

Tilburg University (6)

Why Are Retailers Developing Private Labels?

To create a virtuous cycle!

PRIVATE

LABELS

STORE LOYALTY

POWER SHIFT TO RETAILERS PROFITABILITY

Tilburg University (7)

Profitability Analysis of Private Label versus

National Brands:

Retail Analysis of the Canadian Market A Study Commissioned by PepsiCo

Private label National brands

Gross margin

for retailer 28.8% 11.6%

Tilburg University (8)

Why Are Retailers Developing Private Labels?

To create a virtuous cycle!

PRIVATE

LABELS

STORE LOYALTY

POWER SHIFT TO RETAILERS PROFITABILITY

EXPANSION

Tilburg University (9)

Retailers Are Becoming Global Players, Especially in FMCGs

Top-20 retailers world-wide with at least some FMCG sales

0

5

10

15

20

25

30

35

0 25 50 75 100

FMCG Sales (%)

No. of countries with operations

Wal-Mart

Carrefour

Ahold

Kroger

Metro

Albertson’s Kmart

Tesco Rewe

Costco

Aldi

ITM Enterprises ITO-Yokado

Daiei Jusco Sainsbury

Tengelmann

Auchan

Edeka Safeway (USA)

Tilburg University (10)

Why Are Retailers Developing Private Labels?

To create a virtuous cycle!

PRIVATE

LABELS

STORE LOYALTY

POWER SHIFT TO RETAILERS PROFITABILITY

EXPANSION

Tilburg University (11)

PL Geneva-04

Countries

Consumers

Cust

om

ers

Cate

gori

es

Private

Label

Success

The 4 C’s of Countering the Private Label Challenge

Tilburg University (12)

Business Model: Factors Explaining PL Share and Growth

Countries • National culture

• Socioeconomic

structure

• Trade structure

PL Market Share

/Growth

Consumers • Socio-demographic

profile of PL buyers

• Perceptions of PL

buyers vs. brand buyers

• Store loyalty vs. Brand

loyalty

Customers

• Consolidation/size

• Strategy

• Advertising for PL

• Chain name for PL

• Access to better

products

• High traffic categories

• Margins/profitability

• Sales fundamentals

• Growth of discounters

• EDLP

Categories

Marketing factors

• Pace of innovation

• Advertising intensity

• Promotion intensity

• Price gap

• PL production by brand

manufacturers

• PL-brands package similarity

• PL penetration

Consumer factors

• Involvement

• Performance risk

• Social importance

• Brand trust

• Quality gap Brands-PLs

• Value gap Brands-PLs

• Price-quality inference

• Desire for variety in offering

• Willingness to pay for brands

• Share of budget

Tilburg University (13)

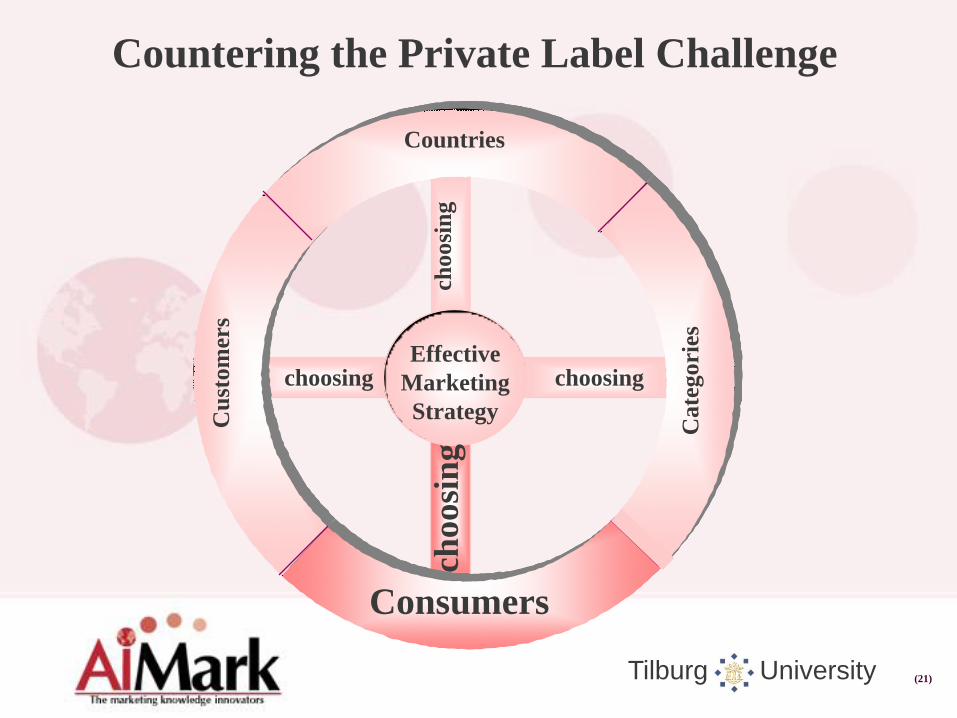

Countering the Private Label Challenge

Countries

choosing choosing

Consumers

cho

osi

ng

ch

oosi

ng

Cu

stom

ers

Cate

gori

es

Effective

Marketing

Strategy

Tilburg University (14)

Choosing Countries

Private labels are more successful in some countries

Why is this the case?

Source: Europanel Private Label 2001

16.0

3.7

23.0 22.9

2.9 2.7

14.3

7.7

3.1

33.0

20.0

Au

stria

Cze

ch

R.

Fra

nce

Germ

an

y

No

rw

ay

Po

lan

d

Sp

ain

Sw

ed

en

Tu

rk

ey

U.K

.

US

A

PL

share

Tilburg University (15)

Differences in Private Label Share between Countries

Are Due to Culture, Socioeconomics, and Retail Factors

Low High

Uncert. Avoid.

Source: Own analyses (Private Label share based on volume)

20.0

10.0

18.1

12.1

18.7

11.6

PL

Share (%)

Small Large

Size of country

Low High

Retail concentration

Tilburg University (16)

Countering the Private Label Challenge

Countries

choosing choosing

Consumers

choosi

ng

ch

oosi

ng

Cu

stom

ers

Cate

go

ries

Effective

Marketing

Strategy

Tilburg University (17)

Choosing Categories Private Labels are more successful in some categories (example U.K.)

Source: Europanel Private Label 2001

36.033.6

32.841.2

62.045.244.6

33.0

28.212.1

31.6

27.420.0

18.011.5

30.322.9

31.415.2

Savouries

Alcohol

Healthcare

Other Toiletries

Bathroom Toiletries

Oral Care

Haircare

Biscuits

Hot beverages

Pickles, Sauces & Ketchups

Pet Foods

Soft drinks

Household Products

Packet & Other Foods

Canned Goods

Bakery

Frozen Foods

Dairy

Total Private Label

Private Label share (%)

Why is this the case?

Tilburg University (18)

Example of Effect of Advertising Intensity

on Current PL Share (2001) and Growth in

PL Share 1997-2001

39%

29%

139

134

PL share (%)

Decrease Increase

Ad spend index 1997-2001

PL share index

Low High

Ad spend % NOS

Tilburg University (19)

Example of Effect of Perceived Quality Gap

(NBs vs. PLs) on Current PL Share (2001) and

Growth in PL Share 1997-2001

39%

27%

149

125

PL share (%) PL share index

Low High

Quality gap

Low High

Quality gap

Tilburg University (20)

Frequent New Product Introductions Counter the Private Label Onslaught

Source: Boston Consulting Group

0

10

20

30

40

50

60

70

0 10 20 30 40 50 60

Detergents

Dog Food

Soup

Soft drinks

Cereals Canned Fish

Coffee Nuts

Jams, jellies

Shortening/

Oils

Beans

Natural Cheese Juices

New

ite

ms

(past

fiv

e yea

rs)

as

% o

f to

tal

mark

et

PL share (%)

Tilburg University (21)

Countering the Private Label Challenge

Countries

choosing choosing

Consumers

choosi

ng

ch

oo

sin

g

Cu

stom

ers

Cate

gori

es

Effective

Marketing

Strategy

Tilburg University (22)

Sociodemographic Profile of PL-Buyers

Baby Category

PL Index

Mother Not employed 125

Baby age 0-6 months 68

6-18 months 97

18-36 months 126

Baby First-born 88

Not first-born 113

Social class Medium/low 110 Heaviest users of PL are low/medium class homemakers with their non-first-born baby after the first 18 months. The PL index for this group can be up to 200.

Tilburg University (23)

Category Perceptions of PL-Buyers vs. NB-Buyers

in a Category in Country A

On several key aspects, PL-buyers differ in their category perceptions from NB-buyers. PL-buyers are characterized by (+ indicates generally large difference):

Smaller quality gap between NBs and PLs (+)

Less positive (typically negative!) value of NBs vis-à-vis PLs (+)

Less quality variation in the category (also between NBs!) (+)

Weaker price-quality association: you don’t get what you pay for! (+)

Lower category involvement

Lower performance risk

More convinced that PLs are produced by brand manufacturers

Lower willingness to pay more for a NB compared to a PL

Tilburg University (24)

Countering the Private Label Challenge

Countries

choosing choosing

Consumers

choosi

ng

ch

oosi

ng

Cu

sto

mer

s

Cate

gori

es

Effective

Marketing

Strategy

Tilburg University (25)

Individual Retailers excl Discounters

FMCG Size 2001 vs Local FMCG PLShare 2001

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

0 5 10 15 20 25 30 35 40 45

PL FMCG Share

FM

CG

Sale

s

The Bigger the Retailer, the Larger the PL Share Risk as retailers expand across countries

France Germany Spain UK

r = .54

Tilburg University (26)

Retailer Image: France’s Top 7

FMCG Retailers and Top 3 Drugstores in the

Value Map

Lidl IntermarchéLeader Price

Leclerc Système U

AuchanGéant

ChampionCarrefour Primo

0

1

2

3

4

5

6

7

0 1 2 3 4 5 6 7

Price

Qu

ality

Superior value

Inferior value

Note: The correlation r between price and quality is .93

Tilburg University (27)

Retailer Image: Germany’s Top 7

FMCG Retailers and Top 3 Drugstores in the

Value Map

Minimal

EdekaRealDM

KauflandRossmannSchlecker

Penny

Lidl

Aldi

0

1

2

3

4

5

6

7

0 1 2 3 4 5 6

Price

Qu

ali

ty

Superior value

Inferior value

Note: The correlation r between price and quality is .15

Tilburg University (28)

Countering the Private Label Challenge

Countries

choosing choosing

Consumers

choosi

ng

ch

oosi

ng

Cu

stom

ers

Cate

gori

es Effective

Marketing

Strategy

Tilburg University (29)

The Manufacturer Holds Some

Trump Cards Too

The retailer cannot:

Always obtain necessary critical mass in a category

Tilburg University (30)

The Amassing of Critical Mass for the Retailers

Contrasted to Manufacturers

Retailer 1

Femcare

(Kotex)

Detergents

(Omo)

Shampoo

(Fructis)

Babycare

(Pampers)

Retailer 2

Retailer 3

Retailer 1’s mass in femcare

Manufacturer’s critical mass for its brand

Retailers’ critical mass for umbrella

brand

Tilburg University (31)

The Manufacturer Holds Some

Trump Cards Too

The retailer cannot:

Always obtain necessary critical mass in a category

Always get the quality it wants

Advertise specific functions of the brand

As convincingly create image as against functional reassurance

Tilburg University (32)

The Manufacturer Holds Some

Trump Cards Too

The retailer cannot:

Always obtain necessary critical mass in a category

Always get the quality it wants

Advertise specific functions of the brand

As convincingly create image as against functional reassurance

Give a sense of wide choice

Invest in in-depth understanding of consumer attitudes and

behavior in all product fields in which they operate

Always achieve higher profit contributions on its private labels

than on national brands

Tilburg University (33)

Are Private Labels Really More Profitable?

Retail Analysis of the Canadian Market

Private label National brands % of sales % of sales

Gross margin 28.8 11.6

Adjusted gross margina 32.3 24.4

Store labor (9.8) (3.0)

Store space / equipment (1.5) (1.5)

Warehouse labor (4.9) .0

Transportation (3.6) .0

Invoice processing (.02) (.03)

Returnable cost (.41) (.12)

Profit contribution 10.5 19.7

aNet of dealbacks

Source: Corstjens and Lal (2000)

Tilburg University (34)

Brand power: Seek missing SKU at another store

Store power: Purchase 1) another SKU of same brand (weak store power)

or 2) another brand at current store (strong store power)

Stand-off: Defer purchase until current store restocks

Power Struggle

The critical role of the consumer’s reaction to ‘out of stock’

Cost of brand switching

(CBS)

Cost of store switching

(CSS)

The tension between

Tilburg University (35)

Example of Action Taken When Preferred Brand

in Category A is Out of Stock

13.6

32.9

18.815.6

48.1

18.421.1

1.1 2.1

0

10

20

30

40

50

28.2

% of respondents

Brand power: Buy item at

another store

Weak store power: Buy other

SKU of same brand at same

store

Hard store power: Buy another

brand at same store

Stand off: Return to

store another day to purchase

desired item

Stand off: Buy

nothing

PL buyers

NB buyers

Tilburg University (36)

These Scenarios Underline the Importance of

Increasing Cost of Brand Switching through...

Building/maintaining brand loyalty

Innovation and differentiation

Communication

Managing the price gap

In-depth knowledge of the consumers

Actions against patent infringement and copy-catting

Can you also team up with some customers?

Tilburg University (37)

Team Up with Customers (1)

Supplying Private Labels: An Alternative Strategy?

Utilizes spare capacity Conflicts with own production needs if own demand picks up

Increases profitability Often illusionary as full costs are not calculated

Strengthens relationship with Really? Is it lasting? At what cost? retailers

Increases control over retailers Brand power = market power and you build PL brand power

Allows to manage private label Private label sets criteria and puts pressure quality on you to share latest technology

Private labels hurt your Private labels hurt your own brands competitors

It gives a boost to business It is addictive: short-run gain is long-run pain

YES: NO:

PL production typically results in reduced focus on own brands

Tilburg University (38)

Team Up with Customers (2):

Inform them: Is an emphasis on PLs more profitable?

To generate high margins, Retailer PL strategy has to be consistent with overall business model (e.g ALDI) ?

Tilburg University (39)

Team Up with Customers (3):

Fight the Common Enemy

Market Share Evolution for Discounters in Germany

6

8

10

12

14

16

18

1998 1999 2000 2001 2002

Aldi

Other Discounters

Mark

et

Sh

are

(%

)

Tilburg University (40)

8

10

12

14

16

Q4

'99

Q1

'00

Q2

'00

Q3

'00

Q4

'00

Q1

'01

Q2

'01

Q3

'01

Q4

'01

Q1

'02

Q2

'02

Q3

'02

Aldi Share

A Challenge for Brands and Mainstream Retailers Alike:

The Growth of Hard Discounters: The German Case

ALDI growth in ‘Q1 waves’

Mark

et

Sh

are

(%

)