una mirada a la situación tecnológica a través del caso intel norberto mateos d.g. de intel...

TRANSCRIPT

1

Norberto Mateos Carrascal

Abril 2011

Una mirada a la situación tecnológica actual a través del caso de estudio de Intel

22

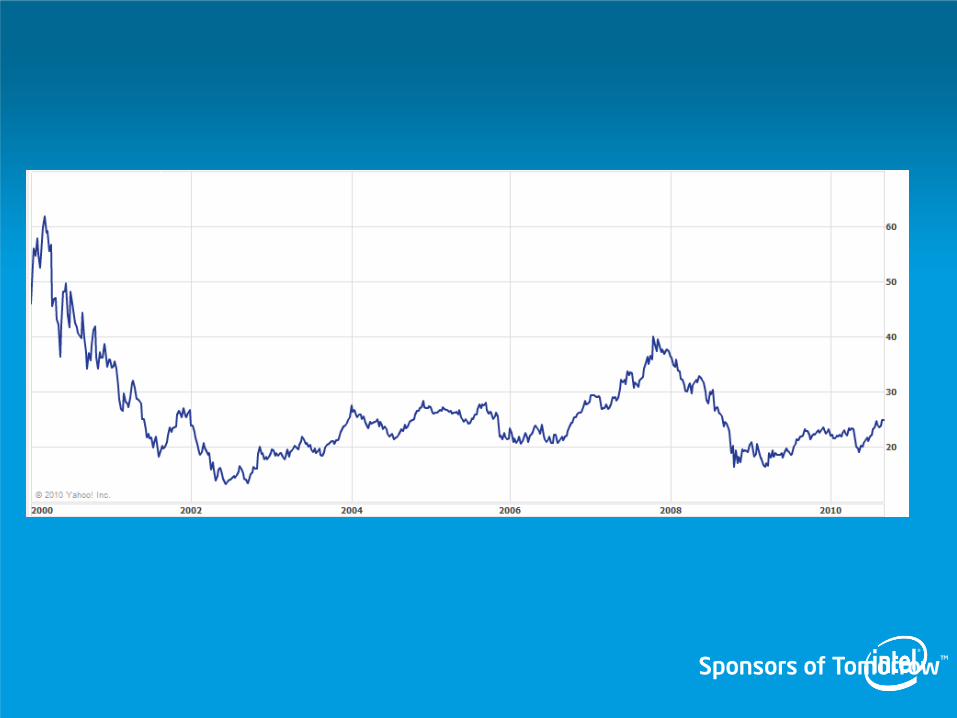

En la peor crisis económica que hemos vivido…

33

Los mejores resultados de la historia ¿?

44

No os sorprenderá…

Grove’s Rules of Recessions

They Always End

You Don’t “Save” Yourself Out Of One

Some Emerge Stronger Than Before

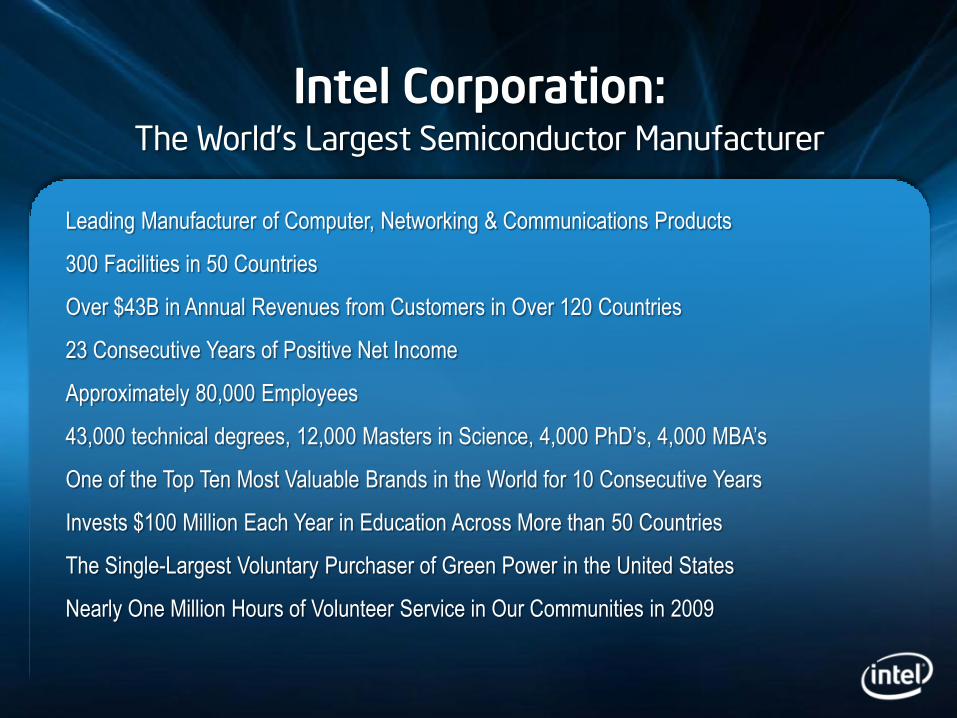

Leading Manufacturer of Computer, Networking & Communications Products

300 Facilities in 50 Countries

Over $43B in Annual Revenues from Customers in Over 120 Countries

23 Consecutive Years of Positive Net Income

Approximately 80,000 Employees

43,000 technical degrees, 12,000 Masters in Science, 4,000 PhD’s, 4,000 MBA’s

One of the Top Ten Most Valuable Brands in the World for 10 Consecutive Years

Invests $100 Million Each Year in Education Across More than 50 Countries

The Single-Largest Voluntary Purchaser of Green Power in the United States

Nearly One Million Hours of Volunteer Service in Our Communities in 2009

Intel Corporation:The World’s Largest Semiconductor Manufacturer

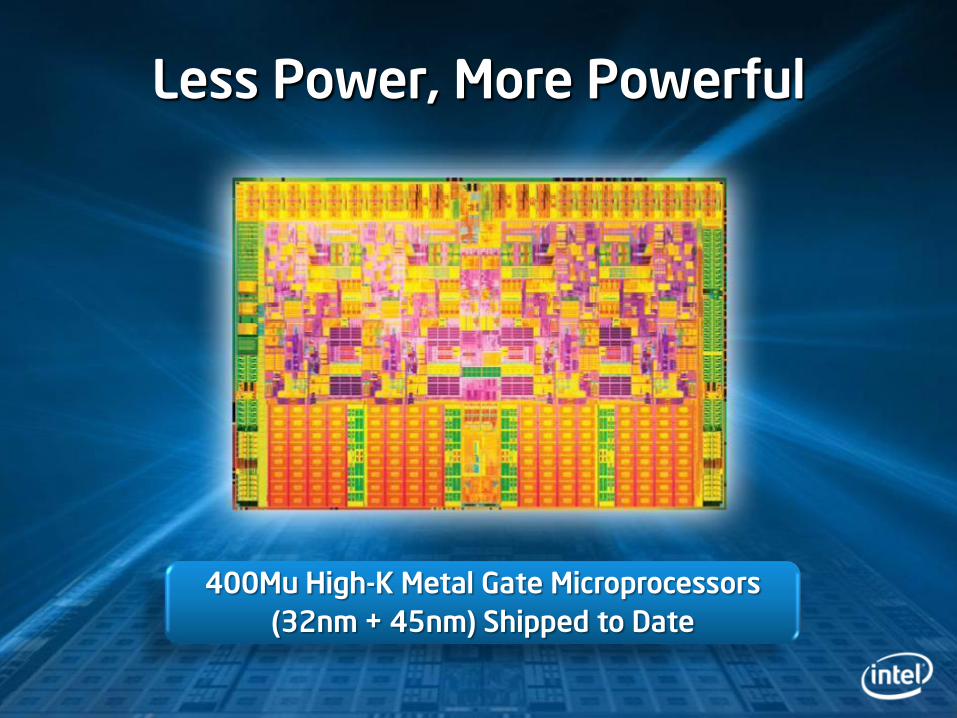

Less Power, More Powerful

400Mu High-K Metal Gate Microprocessors

(32nm + 45nm) Shipped to Date

Relentless Pursuit of Moore’s Law

Opens the Door to Innovations…

“Integrated electronics will make electronic techniques more

generally available throughout all of society, performing

many functions that presently are done inadequately by other

techniques or not done at all.”

Gordon Moore

90nm

300mm

130nm

200mm

180nm

200mm

250nm

200mm

65nm

300mm

45nm

300mm

Feature Width

Wafer Size

32nm

300mm

Number of transistors on a chip doubles every ~2 years

…that Impact Countless Applications

Genomics Research

Medical Imaging

Financial Analysis

Weather Prediction

Oil Exploration

Design Simulation

Cloud Computing

Data Center Refresh

Many opportunities from Genomic Research to Connecting cars, and much, much more…

Point of Sale IP CamerasPower Lines IP PhonesIn-VehicleInfotainment

Home StorageSensors Net book

Security IPTV/IMS Military/AeroLearning Home AutoDigital Signage Portable Medical Net top

Gaming Industrial PC PrintersMedical Transport Robotics FactoryAutomation

MID

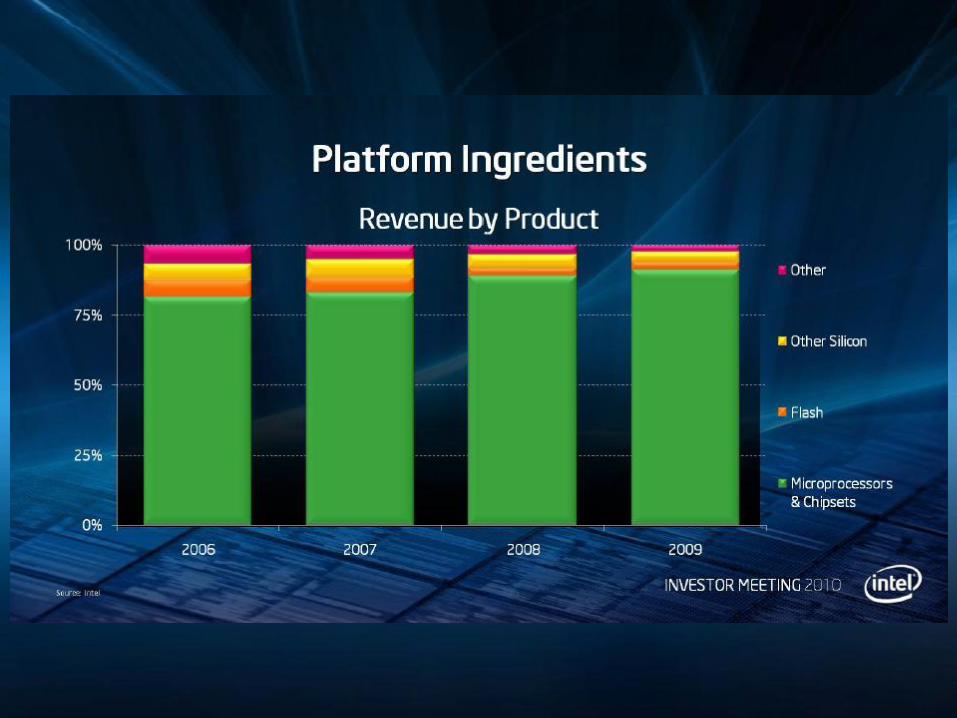

Spending

Capital Additions to Property,

Plant and Equipment(Dollars in Billions)

Research and Development(Dollars in Billions)

5.7 5.7

6.6

3.84.0

4.44.8

5.1

5.9 5.8

2008 2009 20102001 2002 2003 2004 2005 2006 2007

5.2

4.5

5.2

7.3

4.7

3.7 3.8

5.9 5.9

5.0

2008 2009 20102001 2002 2003 2004 2005 2006 2007

Intel’s Investment in

U.S. Manufacturing$6-8 BILLION

for 22nm and Beyond

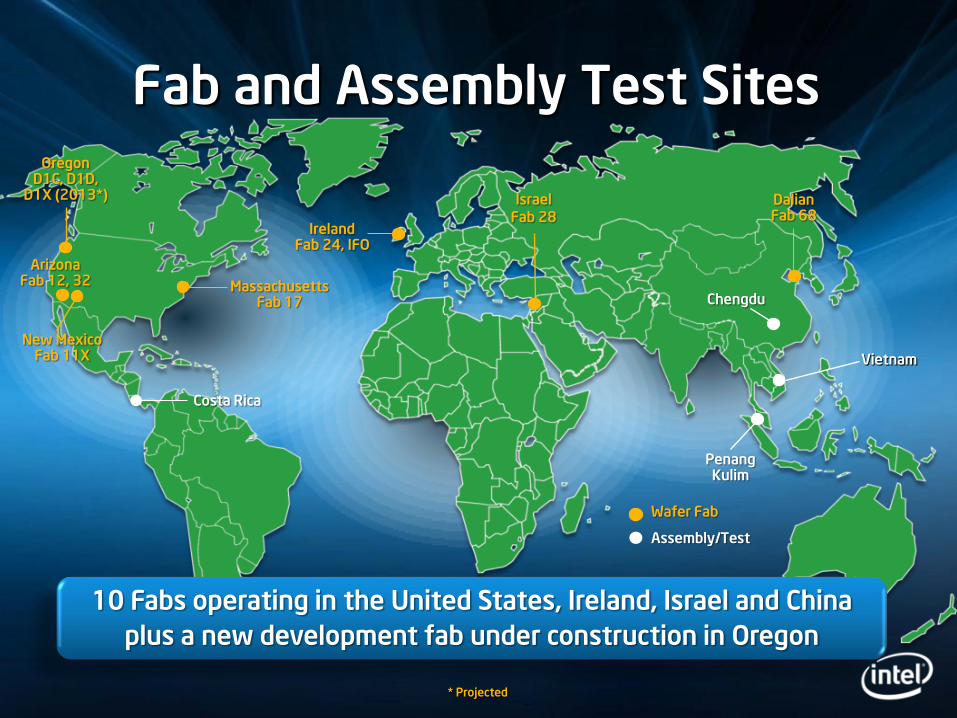

D1DOREGON

D1COREGON

D1XOregon – Development Fab

Fab 12Arizona – 22 nm

Fab 32Arizona – 22 nm

Fab and Assembly Test Sites

IrelandFab 24, IFO

OregonD1C, D1D,

D1X (2013*)

ArizonaFab 12, 32

New MexicoFab 11X

MassachusettsFab 17

Costa Rica

Chengdu

Vietnam

PenangKulim

DalianFab 68

Israel Fab 28

10 Fabs operating in the United States, Ireland, Israel and China

plus a new development fab under construction in Oregon

Wafer Fab

Assembly/Test

* Projected

MarketingThe Intel audio signature

is heard somewhere in the worldevery 40 seconds on average

Operating Profit ($B)Net Revenues ($B)

Finances

5.7

15.6

12.1

5.7

8.2

2009 20102005 2006 2007

35.1

43.6

38.8

35.438.3

2009 20102005 2006 2007 2008

37.6

9.0

2008

2323 Intel Confidential - NDA Use Only

2424

What keeps our CEO awake at night?

Strategicinflection

pointsIntel Confidential - NDA Use Only

2525

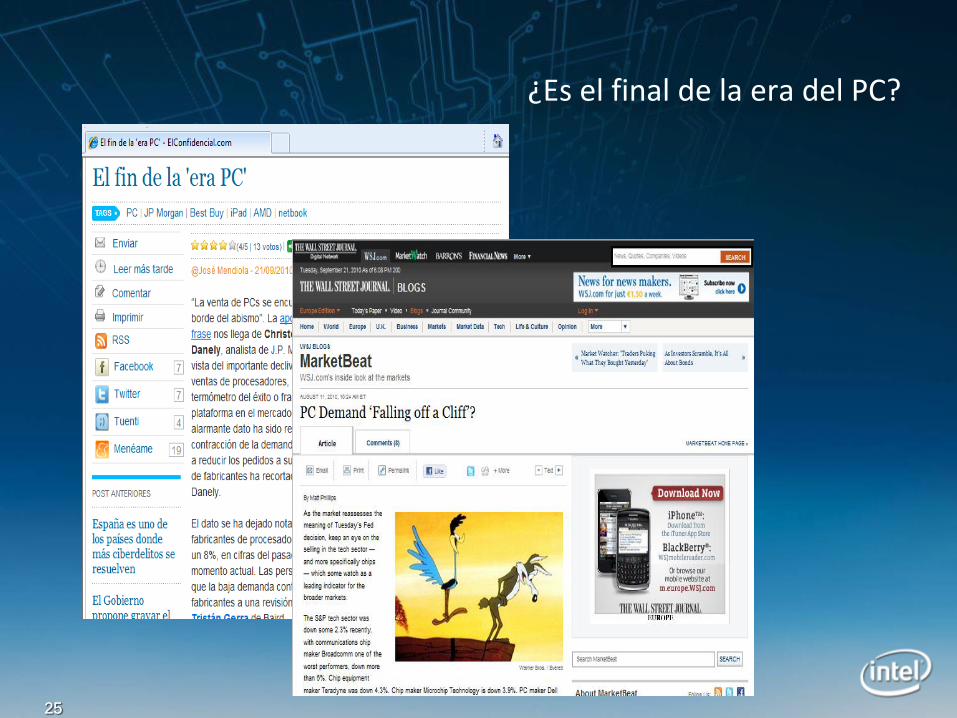

¿Es el final de la era del PC?

2626

A New Era of Computing Is Emerging…

Bigger and richer computing experiences are ahead, driven by connected usages

• Connecting these experiences is an opportunity for Intel hardware, software, and services… across an exploding number of devices.

Mary Meeker, Economy + Internet Trends October 20, 2009 Web 2.0 Summit

Sponsors of Tomorrow™

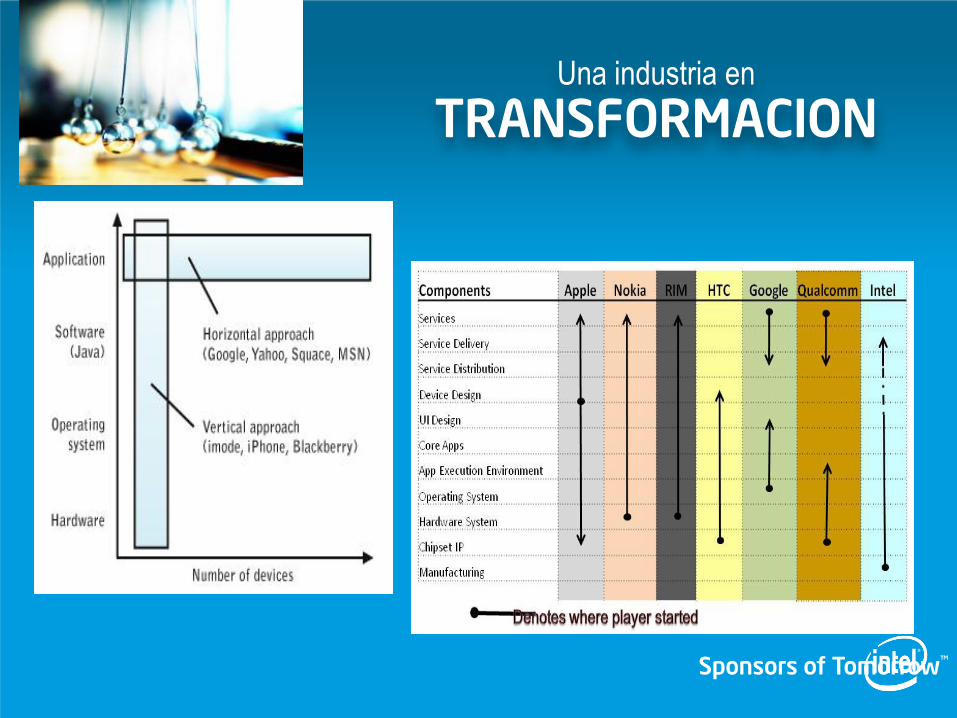

Una industria en

TRANSFORMACION

Sponsors of Tomorrow™

Ejemplos de verticalización en la industria

Sponsors of Tomorrow™

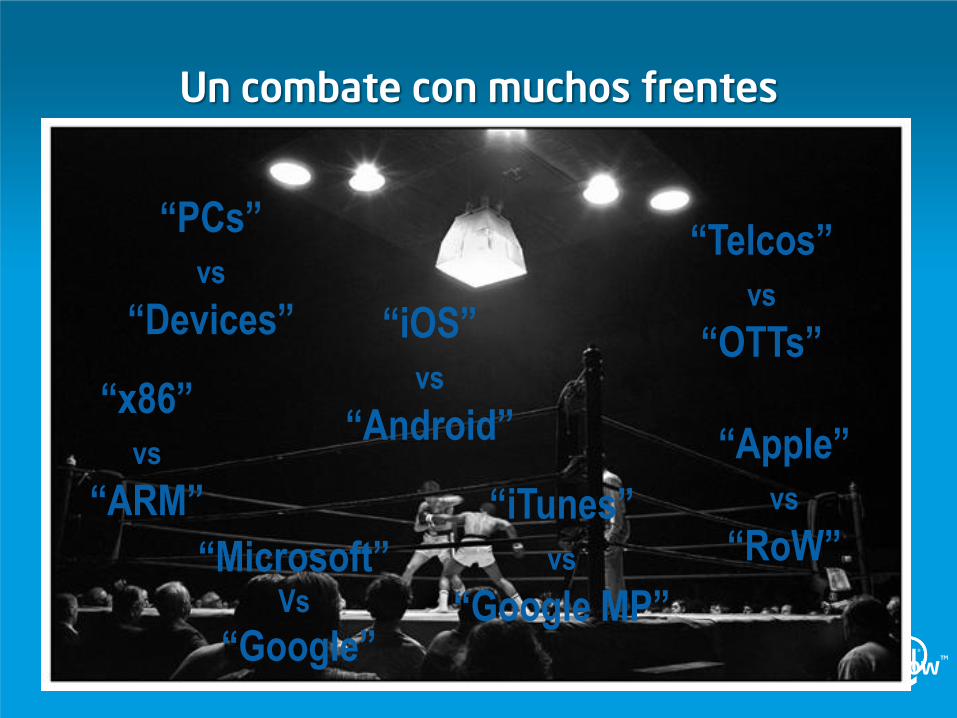

Un combate con muchos frentes

“PCs”

vs

“Devices”

“x86”

vs

“ARM”

“Telcos”

vs

“OTTs”

“Apple”

vs

“RoW”

“iOS”

vs

“Android”

“iTunes”

vs

“Google MP”“Microsoft”

Vs

“Google”

Sponsors of Tomorrow™

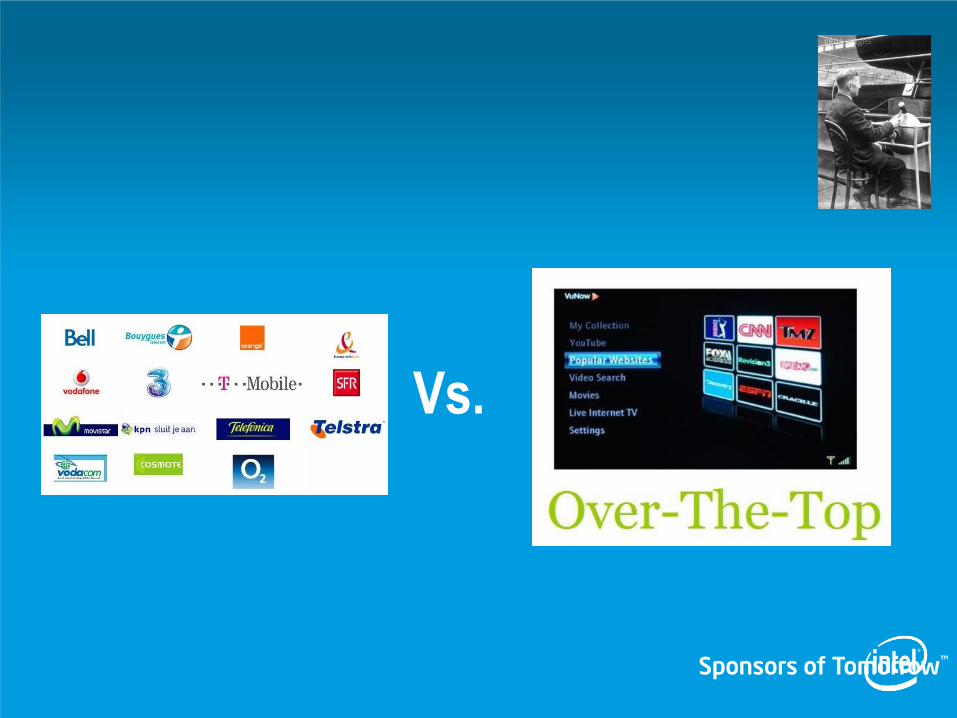

Vs.

Sponsors of Tomorrow™

Las telcos contra las OTT

http://www.youtube.com/watch?v=sTOAyZxOTy0

Sponsors of Tomorrow™

La batalla por el “net neutrality”

Sponsors of Tomorrow™

Sponsors of Tomorrow™

Sponsors of Tomorrow™

Sponsors of Tomorrow™

Sponsors of Tomorrow™

Un nuevo intento de colaboración

Sponsors of Tomorrow™

La batalla por el cliente (i.e. por la “pasta”…)

Sponsors of Tomorrow™

Cuántas tiendas de aplicaciones pueden coexistir?

(la batalla por el cliente)

Sponsors of Tomorrow™

Vs.

Sponsors of Tomorrow™

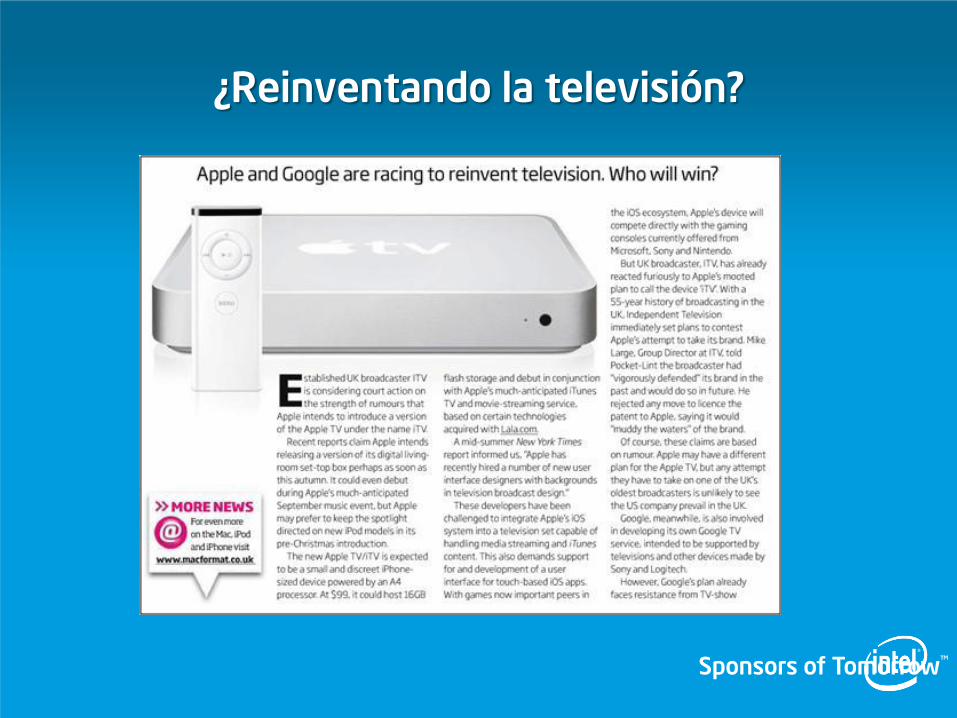

¿Reinventando la televisión?

Sponsors of Tomorrow™

En qué consiste?

Internet (video,

música, información,

juegos, aplicaciones,

redes sociales, etc)

Datos multimedia

(música, películas,

fotos, etc)

Broadcast TV

Sponsors of Tomorrow™

Google TV: first mover

Sponsors of Tomorrow™

Los resultados…

Sponsors of Tomorrow™

Sponsors of Tomorrow™

En resumen

4747

Gracias

Intel Confidential - NDA Use Only