uk electricity market reform: lessons from a policy … · •academic struggles between idealised...

TRANSCRIPT

Presentation to Fifth Green Growth Knowledge Platform Annual Conference

Sustainable Infrastructure World Bank, Washington DC, 27-28th November 2017

Michael Grubb

Professor of Energy and Climate Change,

University College London (UCL) – Institute of Sustainable Resources & Energy Institute

Chair, UK Panel of Technical Experts on Electricity Market Reform

UK Electricity Market Reform: Lessons from a policy and regulatory journey

• Broad evolution of UK policy & regulation

• EMR reforms: instruments & emerging results

• Lessons & regulatory journey

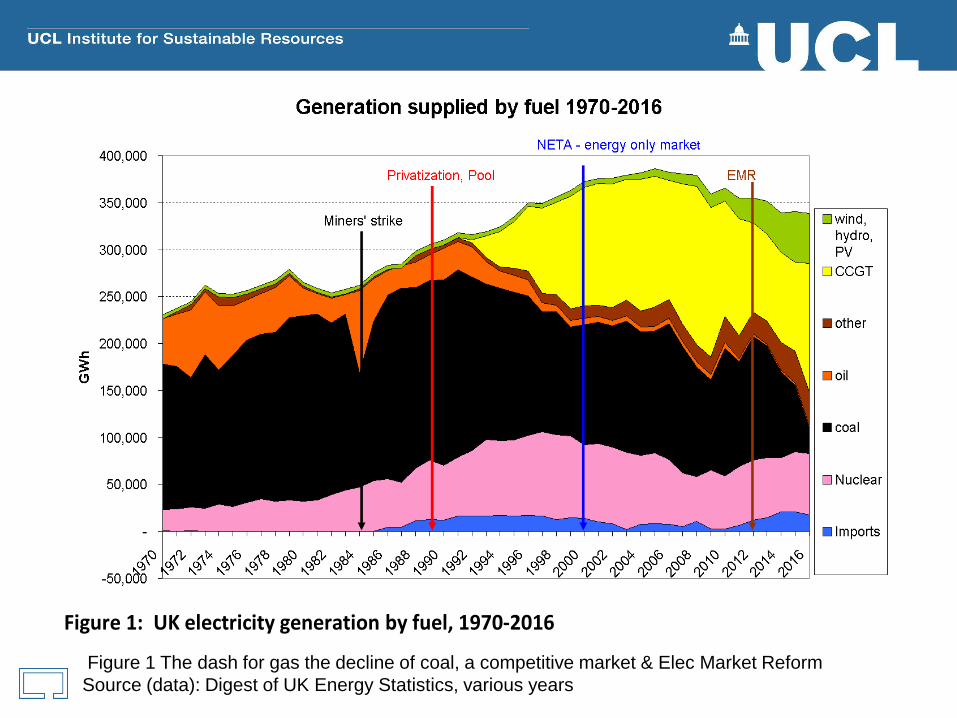

Figure 1 The dash for gas the decline of coal, a competitive market & Elec Market Reform

Source (data): Digest of UK Energy Statistics, various years

Figure 1: UK electricity generation by fuel, 1970-2016

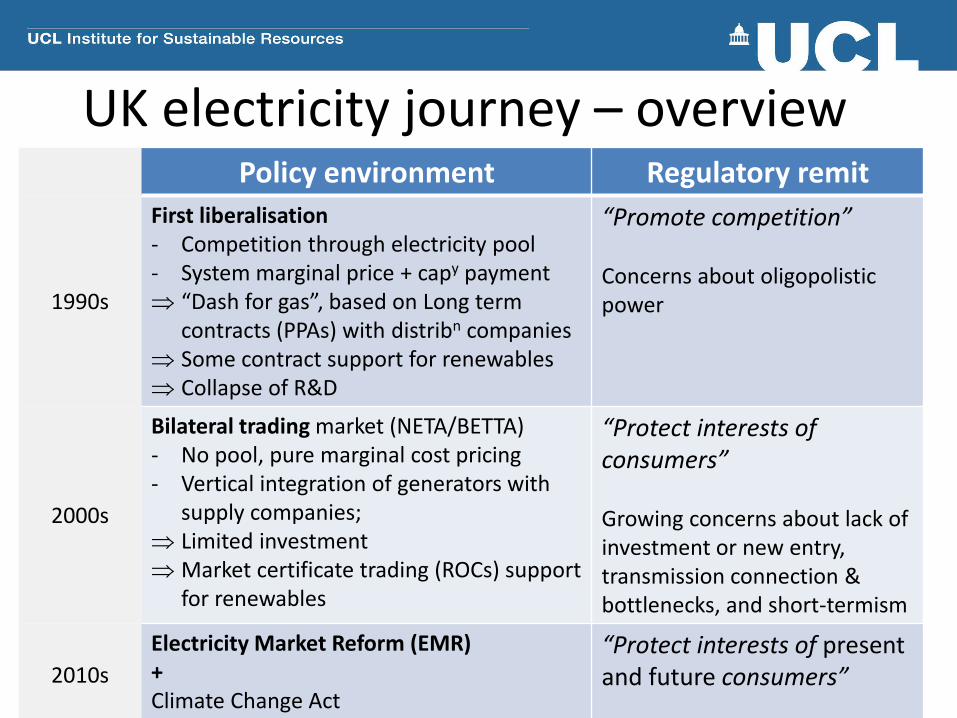

Policy environment Regulatory remit

1990s

First liberalisation- Competition through electricity pool- System marginal price + capy payment “Dash for gas”, based on Long term

contracts (PPAs) with distribn companies Some contract support for renewables Collapse of R&D

“Promote competition”

Concerns about oligopolistic power

2000s

Bilateral trading market (NETA/BETTA)- No pool, pure marginal cost pricing- Vertical integration of generators with

supply companies; Limited investment Market certificate trading (ROCs) support

for renewables

“Protect interests of consumers”

Growing concerns about lack of investment or new entry, transmission connection & bottlenecks, and short-termism

2010s

Electricity Market Reform (EMR)+Climate Change Act

“Protect interests of present and future consumers”

UK electricity journey – overview

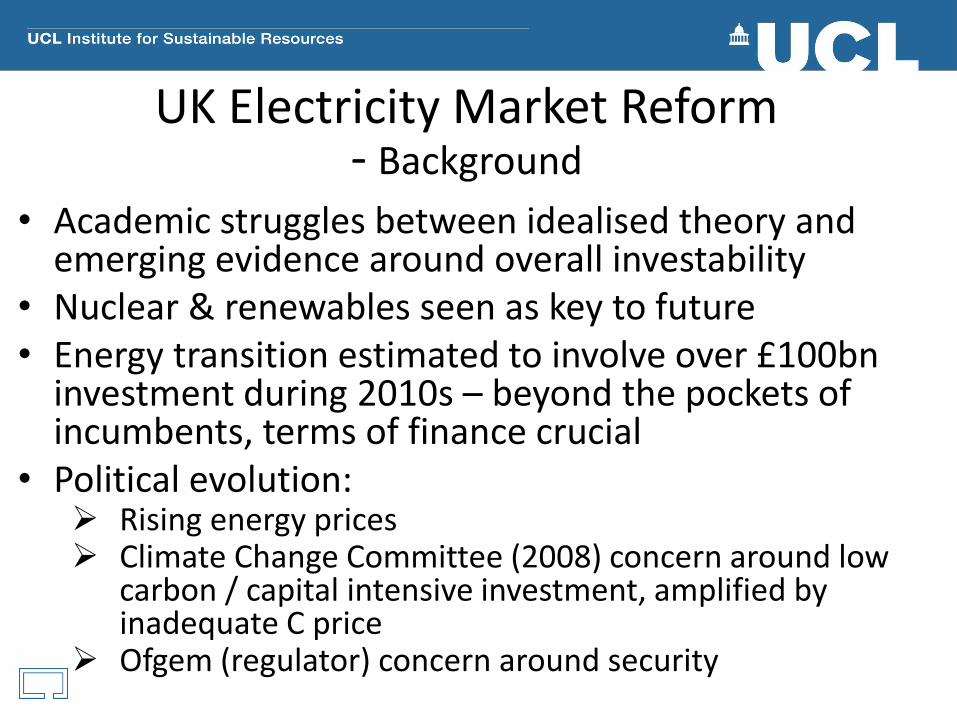

• Academic struggles between idealised theory and emerging evidence around overall investability

• Nuclear & renewables seen as key to future• Energy transition estimated to involve over £100bn

investment during 2010s – beyond the pockets of incumbents, terms of finance crucial

• Political evolution: Rising energy prices Climate Change Committee (2008) concern around low

carbon / capital intensive investment, amplified by inadequate C price

Ofgem (regulator) concern around security

UK Electricity Market Reform - Background

• Controversial step for a pioneer of electricity liberalisation

• Ofgem’s Project Discovery (2009) – Regulator’s detailed study of the future challenges of the electricity market

• Addressing key risks identified became the three aims of EMR:

5

Electricity Market Reform (EMR)

Reduce the risks to security of

supply

Support progress

towards climate change targets

Reduce costs to consumers

1 2 3

Presentation to Fifth Green Growth Knowledge Platform Annual Conference

Sustainable Infrastructure World Bank, Washington DC, 27-28th November 2017

Michael Grubb

Professor of Energy and Climate Change,

University College London (UCL)

Chair, UK Panel of Technical Experts on Electricity Market Reform

UK Electricity Market Reform: Lessons from a policy and regulatory journey

• Broad evolution of UK policy & regulation

• EMR reforms: instruments & emerging results

• Lessons & regulatory journey

7

Contracts for Difference

(fixed-price 15-yr contracts)

Capacity Mechanism

(capacity payments on availability)

Carbon floor price

Emissions Performance

Standard

4 Key Policies

EMR brought major changes to the market. Main regulatory input on design of Capacity Mechanism and overall institutional

Security of Supply

Low Carbon Support

No new coal

What is EMR?

8

1. Contracts for Difference (CfDs)(structure for renewable energy & nuclear)

Initial gain from auctions followed by huge offshore wind cost reduction

Source: From M.Grubb and D.Newbery (2017), ‘UK Electricity Market Reform and the Energy Transition:

Emerging Lessons’, MIT working paper (submitted) * 15-yr Contract prices

£0

£20

£40

£60

£80

£100

£120

£140

£160

£180

Str

ike

Pri

ce

(£

/MW

h)

2013/14 2015/16 2017/18 2019/20 2021/22

Round 1 Admin Strike Price (Offshore Wind)

Round 1 Contracts - Offshore Wind / ACT

Round 2 Contracts - Offshore Wind

£155 £155£150

£140 £140

£57,50 (Hornsea II, Moray East)

£74,75 (Inc. Triton Knoll)

£114.39 (Inc. Neart Na Gaoithe)

£119,89 (Inc. East Anglia 1)

2014, administered CfD prices, £140-£150 /MWh*

2015, first auction, offshore wind price: £114.39/MWh2017, second auction, two projects at £57.50/MWh Competitive CfDs drive down cost – hardware,

supply chain & finance (Newbery (2015) estimates CfDs reduced WACC by 3 % points – saving > £2bn/yron estimated cost of energy transition).

boost to UK low-carbon supply chain, as part of government’s emerging ‘Clean Growth Plan’

Delivery years(to first generation)

Allocation / auction rounds

prices halve

4 years difference in delivery years

strike price for five offshore wind farms depending on completion date

Gains from auctioned contracts

Why

How

10

2. Capacity Mechanism / Market(to reward ‘firm’ generating capacity)

• Ensure market can deliver security of supply• Payment for availability to encourage investment

• Market wide auction of capacity obligations, run by National Grid• Successful bidders get fixed revenue additional to wholesale market• Obligated to deliver capacity when needed or face penalties• Technology neutral – but those receiving CfDs are not eligible• Pilot scheme to help Demand Side Response (DSR)

Reduces price volatilityInsurance against blackoutsEncourages demand side - somewhat? Expected cost – estimate required for new CCGTs, around £50/kw/yr Would give £2.5bn/yr into market, much expected to pass through ? Less peaky prices – impact on interconnector / other investment× Design makes it very difficult for DSR to participate equally

Effect

Lots of bids, low prices, new options, lots of angst ..

(b) Successful New Build capacity by fuel and technology type in the T-4 auctions

First main capacity auction (Dec 2014)

Almost 50GW awarded, clearing price 19.40/kW/year*

Mix of 1-year, 3-year (refurbishment) and 15 year

(2.5GW of new build out of 10GW bid) contracts

Mainly existing nuclear, gas and coal generators

One new CCGT (1,650MW) wins an agreement – but

failed to raise final investment

Only 174MW of demand side response

2.5GW of capacity reserved for 2017 1-year ahead

auction

Second main capacity auction (Dec 2015)

Clearing price £18.00/kW/year

46.35GW awarded – new options replace retiring coal

Interconnectors, 1GW of small reciprocating engine

Concern about diesel

Third main capacity auction (Dec 2016)

Clearing price £22.50/kW/year

52.43GW awarded, inc 3.4 GW new capacity – over

500MW batteries

New diesel largely excluded, but wider concern about

‘embedded benefit’ exemptions from transmission

0

500

1000

1500

2000

2500

3000

3500

2014 for 2018 2015 for 2019 2016 for 2020

MW

New build in Capacity Auctions

Battery Reciprocating engine CHP Waste CCGT OCGT CCGT Withdrawn

Capacity: be careful what you ask for …

Floor price designed to give market value to the government’s Social cost of carbon, through top-up to EU ETS price

- Quickly renamed ‘Carbon Price Support’ (CPS)

Combined with the Emissions Performance Standard, effectively bans new coal and improves economics of gas vis-à-vis existing coal plants

Carbon price floor – compelling economics

Beihang: Planetary Economics and the Political Economy of Energy & Climate ChangeMission accomplished .. ?

Likely to overdeliver on the UK renewables targetDramatic (80%) fall since 2012: first hours / days without coal power for over a Century Driven as declining gas price meets rising carbon price, and renewables + (2016) gasNov 2017: carbon price ‘about right’ till coal phased out Carbon Price Support

£/tCO2, added to EU ETS30

15

£4.94/tCO2

£9.55/tCO2

£18/tCO2

C-Price support doubled to £18/kWh

CPS

0-

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

Gen

erat

ion

fro

m c

oal

, TW

h/y

r

GB coal power generation, 2012 - Q2 2017

Presentation to Fifth Green Growth Knowledge Platform Annual Conference

Sustainable Infrastructure World Bank, Washington DC, 27-28th November 2017

Michael Grubb

Professor of Energy and Climate Change,

University College London (UCL)

Chair, UK Panel of Technical Experts on Electricity Market Reform

UK Electricity Market Reform: Lessons from a policy and regulatory journey

• Broad evolution of UK policy & regulation

• EMR reforms: instruments & emerging results

• Lessons & regulatory journey

Three Components of Impact Assessment

Impact Assessment

Strengthening analysis of these issues is designed to more systematically represent issues related to the interest of future consumers, complementary to a monetised CBA

Improved consistency

Increased transparency

Monetised aggregate Cost-Benefit Analysis

Social & distributional

impacts

Explicit consideration of

strategic & sustainability

issues

Regulatory dimensions includeRemit (future consumers?) and metrics

• For Strategic (“Third Domain”) investments – eg security and sustainability inc emerging renewables - a role for government is inescapable– The public benefits exceed any risk-adjusted return in spot market

• Can shifting some risk to government (eg. long term contract) be good? Yes if– the risks arise from private perception of policy risk;

– markets (particularly capital markets) are myopic; or

– the benefits are partly public (eg. Due to inadequate environmental pricing, or innovation / learning, etc)

• Do we need a Capacity Mechanism in addition to low carbon supports?– Yes in UK conditions – but scope is crucial, so too is design

• Auctions are very valuable – competitive pressures remain important– Better than government decision at cutting costs / finding options

• Institutional complexities – contracting bodies and their governance

• Transmission and distribution – new frontiers?

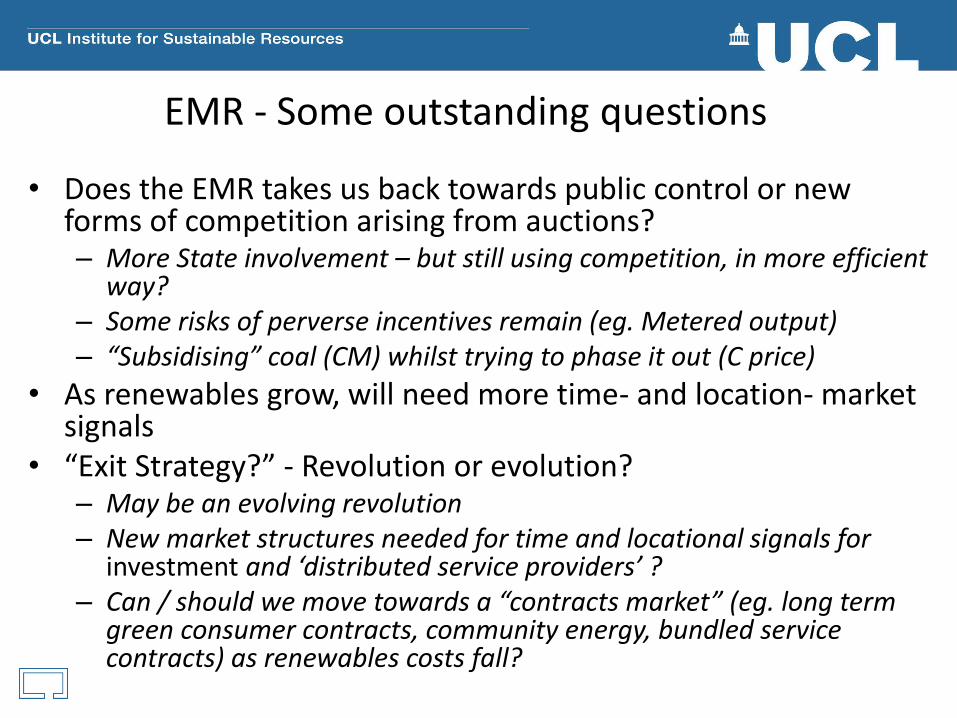

UK Electricity Market Reform - Key lessons

• Does the EMR takes us back towards public control or new forms of competition arising from auctions?– More State involvement – but still using competition, in more efficient

way?– Some risks of perverse incentives remain (eg. Metered output)– “Subsidising” coal (CM) whilst trying to phase it out (C price)

• As renewables grow, will need more time- and location- market signals

• “Exit Strategy?” - Revolution or evolution? – May be an evolving revolution – New market structures needed for time and locational signals for

investment and ‘distributed service providers’ ?– Can / should we move towards a “contracts market” (eg. long term

green consumer contracts, community energy, bundled service contracts) as renewables costs fall?

EMR - Some outstanding questions