types of energy assessments - pertan group

TRANSCRIPT

www.granlund.fiCopyright Granlund |

Different types of Energy Assessments and some ExperiencesErja Reinikainen

Olof Granlund Oy / FinlandEnergy Assessment Protocol Demonstration,

September 17, 2009

www.granlund.fiCopyright Granlund | 2EAR |

What exactly is an Energy Audit?

www.granlund.fiCopyright Granlund | 3

Energy Auditing has many names

• the activity has different names in different countries

• in Europe mainly term Energy Audit is used

• in the US Energy Assessments

• other names: energy surveys, energy scans...

• but we all mean the same thing: identifying energy saving possibilities and reporting them to the building owner

www.granlund.fiCopyright Granlund | 4

What is an Energy Audit?

Energy audit is a systematic procedure where the purpose is to

• evaluate the existing energy consumption

• identify of the saving measures

• report the findings

in existing buildings/sites/objects...

www.granlund.fiCopyright Granlund | 5

Evaluation

Identification of saving measures

Reporting

This is the heart of the energy audit

The ”topping” is how it is done in practice in different countries / sites / levels of audits

Energy Audit Model Theory

www.granlund.fiCopyright Granlund | 6

Energy audits / assessments -

some background and history

www.granlund.fiCopyright Granlund | 7

Energy Auditing is a good tool

• energy auditing since 1980’s in many countries

• audits are essential for finding the most effective measures to improve energy efficiency

• energy auditing is a useful tool for reducing energy costs and CO2 -emissions

• energy auditing is often used as the practical tool in energy efficiency agreements, environmental management, facility management long term planning, etc

www.granlund.fiCopyright Granlund | 8

EU-level targets

•

• Greenhouse gas emissions

• Reduction of by 20% from 1990 level by 2020

• Reduction target 30% if other industrialized countries take

similar action

• Reduction of 60-80% by 2050 in industrialized countries

• Renewable energy:

• Increase the share of renewables to 20% in the EU by 2020

• In the transport sector increase renewable fuels to 10% by 2020

• Energy efficiency improvement 20% by 2020 from baseline of

2005

• EU stands in front line against climate change

www.granlund.fiCopyright Granlund | 9

EU Energy-efficiency Policies / Energy Audits

Energy Auditing has a key role in the EU-level directives:

• energy performance of buildings -directive

• energy certification of buildings is mandatory

• the certificate includes a list of energy saving measures

• energy end-use efficiency and energy services -directive

• energy audit schemes must be available in EU member states

• national audit programmes are being developed

www.granlund.fiCopyright Granlund | 10

The AUDIT-projects

The material in this slideshow is partly based on the material from 2 international projects that created energy auditing theory:

• SAVE-project AUDIT I 1998-2000• comprehensive study on energy auditing in EU countries• developing definitions on energy auditing• developing state-of-the-art approaches to energy auditing

• SAVE-project AUDIT II 2001-2003• Finland (Motiva), Norway (IFE), Austria (EVA), France

(ADEME), Greece (CRES), Portugal (Adene)• The main aim is to start EU-level co-operation• Country reports on Energy Auditing (EU)• Topic reports on Audit Program Elements

www.granlund.fiCopyright Granlund | 11EAR |

What are the different options for doing an audit?

www.granlund.fiCopyright Granlund | 12

Energy Audit Procedure in general

COLLECTING COLLECTING BASIC DATABASIC DATA

FIELD WORK FIELD WORK

ANALYSIS ANALYSIS OF THE DATA OF THE DATA

REPORTING REPORTING

STARTSTART--UP MEETING UP MEETING

IMPLEMENTATION OFIMPLEMENTATION OFSAVING MEASURES SAVING MEASURES

...but there are many different ways to do it

www.granlund.fiCopyright Granlund | 13

Why different Audit Models?• An energy audit analyses the present energy use

and points out profitable saving measures, but• energy is used for different purposes

(e.g. heating or process)• the scale of energy consumption varies

(e.g. school or power plant)• the site can be at various stages of its life cycle

(e.g. new, updated, completely renovated)• the size of the site varies

(e.g. petrol station or city hospital)• the scope of the energy audit varies (walk-through / thorough

analysis, system-specific / wide scope…)

• Different needs for• amount of work• audit phases• reporting

www.granlund.fiCopyright Granlund | 14EAR | September 2007

What kind of audit?

• what is the aim:• to find easy savings (“cream skimming”)

• to define all saving possibilities (comprehensive audit)

• to identify possible areas for further assessments (first step)

• to identify possibilities for ESCO /EPC

• what is the scope:• whole building or site

• a specific area of energy use

• what does the audit work include:• quick walk-through

• more detailed assessment with measuring

www.granlund.fiCopyright Granlund | 15

Every System / All SiteTHE SCOPE

THE THOROUGHNESS

FINE COMB

NARROW WIDE

ROUGH COMB

THE AIM

TO POINT OUT TO PROPOSE

Specific System/Area

General Potential Assessment

General Energy Saving Areas

Detailed Potential Assessment

Specific Energy Saving Measures

Energy Audit Scope and Aim

www.granlund.fiCopyright Granlund | 16

SCANNING MODELS

point out saving areas

ANALYSING MODELS

propose saving measures

WALK- THROUGH

AUDIT

PRELIMINARY AUDIT

SELECTIVE AUDIT

TARGETED AUDIT

COMPREHENSIVE AUDIT

Small site

Large site

Auditor chooses

Defined in guidelines

SYSTEM- SPECIFIC AUDIT

…

MA

GN

ITU

DE

AC

CU

RA

CY

Different targets for audits

www.granlund.fiCopyright Granlund | 17

THE WALK THROUGHENERGY AUDIT

THE PRELIMINARYENERGY AUDIT

“The main aim is to point out areas, where energy saving potentials exist or may exist and also the obvious, normally “good housekeeping” and no-cost

measures. Do not go deeply into the profitability of the measures”

Area of application:• small tertiary sector, industrial • buildings with standard

systems in general

Content of work:• overview of site´s energy use• rough consumption breakdown• points out the obvious savings• rough estimates of potentials• may have simple calculations• simple & brief documentation • suggestions for the next steps

Working time:• from a few hours to a day or two

Area of application:• energy intensive process

industryContent of work:• detailed consumption analysis• defining of areas where energy

consumption is significant and• where the Analysing Modelsare needed as a second step

• listing the obvious savings• complete reporting on break-down but brief on measures

Working time:• typically 3 to 6 weeks

Scanning Energy Audits

www.granlund.fiCopyright Granlund |

18

“The aim is to cover the whole site, locate all profitable energy saving opportunities and propose concrete measures with adequate data for decision making ”

Area of application:• all buildings, all sectors• for good and target-oriented energy auditors

Content of work:• only general guidelines• auditor has freedom to

choose what to do on site• concentrates on majors,• ignores the minors, • points out the obvious• can be very cost-effective • but also cream-skimming• detailed report on “findings”Working time:• few days to 1…2 weeks

Area of application:• medium & large industryContent of work:• covers everything “inside

the fence”, work balance based on the breakdown

• detail calculations onsavings and investments

• detailed standard reporting

Working time:• 3…5+ weeks

THE SELECTIVEENERGY AUDIT

THE TARGETEDENERGY AUDIT

THE COMPREHENSIVEENERGY AUDIT

THE SYSTEM SPECIFICENERGY AUDIT

Area of application:• all “standard” buildings• no special requirements

for the auditorsContent of work:• detail guidelines• all systems audited and

work is in balance• systems to be auditedare known in advance

• consumption breakdown• detail calculations on

savings and investments• detailed standard reporting

Working time:• 1,2…1,5 x Selective

• requires “special auditors”• very compact procedure• detailed standard reporting

Analysing Energy Audits

www.granlund.fiCopyright Granlund | 19EAR |

LEVEL 0LEVEL 0= = Pre-assessment phase•• Selection of objects for energy audits Selection of objects for energy audits

LEVEL ILEVEL I Screening = Preliminary energy & process Screening = Preliminary energy & process optimization optimization assessment, qualitative analysis assessment, qualitative analysis•• Walk-through audit Walk-through audit•• Analysis of consumption figures & documents Analysis of consumption figures & documents•• List of possible energy saving opportunities List of possible energy saving opportunities

LEVEL IILEVEL II = In-depth quantitative analysis to verify Level I results = In-depth quantitative analysis to verify Level I results•• Full energy audit Full energy audit•• Measurements Measurements•• List of measures for funding & implementation List of measures for funding & implementation

LEVEL IIILEVEL III = Detailed engineering analysis = Detailed engineering analysis•• Implementation Implementation•• Performance measurement & verification Performance measurement & verification•• Continuous commissioning Continuous commissioning

Different levels of audits

Scanning

energy audit

Comprehensive

energy audit

www.granlund.fiCopyright Granlund | 20

Energy audits -

yes,

but how to run the show?

www.granlund.fiCopyright Granlund | 21

The Elements of an Energy Audit Scheme

ADMINISTRATIONGOALS OFTHE PROGRAMME

STRUCTURE OFADMINISTRATION

KEYPLAYERS

ENERGY AUDITMODELS

MONITORINGSYSTEM

QUALITYCONTROL

AUDITOR´STOOLS

TRAINING OFAUDITORS

AUTHORISATIONOF AUDITORS

SUBSIDYPOLICY

LEGISLATIVEFRAMEWORK

PROMOTION &MARKETING

IMPLEMENTING INSTRUMENTS

QUALITY OF AUDITS

www.granlund.fiCopyright Granlund | 22EAR |

ADMINISTRATION

GUIDELINES

AUTHORISATION

TRAINING

MARKETING

PROMOTION

MONITORING

INTEGRATION

QUALITY CONTROL

SUBSIDY POLICY

AUDIT WORK

Key Players and their Roles

www.granlund.fiCopyright Granlund | 23EAR |

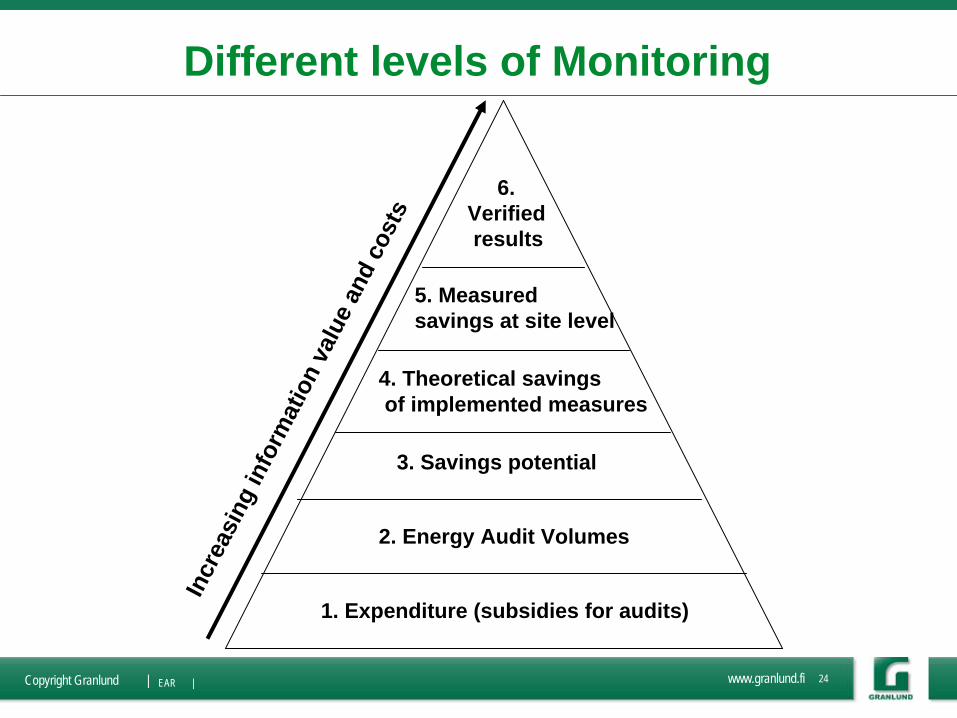

Why Monitoring?

To be able to prove it has been effective.

Monitoring and evaluation are essential elements in an energy auditing activity to provide information on the impact of the activity.

The financier will want to know exactly what comes out of the money and resources they allocate to the activity.

In addition, monitoring and evaluation are of interest for the clients and auditors, since it will give them feedback on the results and the quality of the work.

www.granlund.fiCopyright Granlund | 24EAR |

Different levels of Monitoring

1. Expenditure (subsidies for audits)

2. Energy Audit Volumes

3. Savings potential

4. Theoretical savings of implemented measures

5. Measured savings at site level

6. Verified results

Incr

easi

ng in

form

atio

n va

lue

and

cost

s

www.granlund.fiCopyright Granlund | 25EAR |

Data available from a Monitoring System

• Data for clients, auditors, administrator, media

• Annual reports on the Energy Audit Programme

• subsidies, audit volumes, saving potentials• implemented savings• typical savings

• Sample studies

• number of audits in sample• specific consumption data (kWh/m3…)• total energy use, total cost• total saving potential, typical saving measures

• Connection to Voluntary Agreements monitoring

www.granlund.fiCopyright Granlund | 26EAR |

Why Training and Quality Control?

It is all about quality.

The final aim of an energy auditing activity is to save money and reduce greenhouse gas emissions.

To make this happen, the auditors must be able to do good energy audits and produce reports, which provide the client adequate information for the implementation of the measures.

www.granlund.fiCopyright Granlund | 27EAR |

Training, Authorisation, Quality Control

Trainingof

auditors

Qualitycontrol of

audits

Authorisationof

auditors

Pre-qualification

ofauditors

www.granlund.fiCopyright Granlund | 28EAR |

Quality Control- Main points to check

• The general guidelines have been followed

• The presented numbers are realistic

• saving potential compared to present consumption level

• investment costs for suggested measure

• The content of the report is technically correct

• The proposed measures are appropriate and realistic

• The report “looks ok”

www.granlund.fiCopyright Granlund | 29EAR |

Why Tools for Auditors?

The auditors' tools include a large family of support documents and applications which are intended to facilitate the work of auditors in the view both of minimising audit costs and maximising audit quality.

The tools usually describe the Energy Audit Models but may address different stages in the audit procedure and provide help either on technical matters or on marketing aspects.

www.granlund.fiCopyright Granlund | 30EAR |

Tools for Auditors

COLLECTING COLLECTING BASIC DATABASIC DATA

FIELD WORK FIELD WORK

ANALYSIS ANALYSIS OF THE DATA OF THE DATA

REPORTING REPORTING

STARTSTART--UP MEETING UP MEETING

IMPLEMENTATION OFIMPLEMENTATION OFSAVING MEASURES SAVING MEASURES

Information, brochures,

case studies,benchmarks

Check list,Walk through

guide

Data collection forms

Audit guide or handbook

Calculation methods or

softwareReport templates

Quality check list

Data transfer tools (automatic), ..

www.granlund.fiCopyright Granlund | 31

Energy Audit Scheme

Scheme properties:

- key players- legislative framework- subsidies- audit procedure- monitoring - quality control - auditors’ training- etc

Energy AuditModel 1

Modelfeatures:- time and cost- phasing- reporting

Energy AuditModel 2

Modelfeatures:- time and cost- phasing- reporting

Model 3 Model 4

Energy Audit Model Features

www.granlund.fiCopyright Granlund | 32EAR |

Some Experiences & Results

from Finland

www.granlund.fiCopyright Granlund | 33EAR |

”Subsidy scheme”1981-82

First EA developmentproject and campaign

”Subsidy scheme”1986-87

”Subsidy scheme”1992…

1993Goals set for

the EA Programme

Long history of Energy Auditing

VoluntaryAgreements

1997>

VoluntaryAgreements

2008>>The Finnish Energy Audit Programme is one of the pioneers - and still going strong

www.granlund.fiCopyright Granlund | 34EAR

• Energy Audits are connected to Voluntary Energy Conservation Agreements (industry, service sector, energy production) - large volumes

• Monitoring system proves that it has been efficient

• Client feedback is positive

• Energy auditors do audits as a part of their regular business

• Implementation tools have been developed to help clients

And why has it been successful?

www.granlund.fiCopyright Granlund | 35EAR | September 2007

CONTACT BETWEEN CLIENT AND AUDITOR

APPLICATION FOR SUBSIDIES

STARTSTART--UP MEETINGUP MEETING•• Evaluation of the client needs and goalsEvaluation of the client needs and goals•• Timetables and contact personsTimetables and contact persons••Special interests and requirements in reportingSpecial interests and requirements in reporting

COLLECTING BASIC DATACOLLECTING BASIC DATA•• Energy consumption from 3 to 5 years periodEnergy consumption from 3 to 5 years period•• Design, operation and maintenance documentsDesign, operation and maintenance documents•• Planning of the field work and measurementsPlanning of the field work and measurements

FIELD WORKFIELD WORK•• Auditing the buildingAuditing the building•• MeasurementsMeasurements•• Implementation of the noImplementation of the no--cost saving measurescost saving measures

Energy Audit Procedure 1

www.granlund.fiCopyright Granlund | 36EAR |

ANALYSIS OF THE DATAANALYSIS OF THE DATA•• Breakdown of the total consumptionBreakdown of the total consumption•• Evaluation of possible saving measuresEvaluation of possible saving measures•• Calculation of investments and savingsCalculation of investments and savings•• Feasibility studyFeasibility study

REPORTING• Writing the Final report• Presentation to the Client

• Quality control• Results to database

IMPLEMENTATION OF THE SAVING MEASURES• monitoring of results

• Subsidy request

Energy Audit Procedure 2

www.granlund.fiCopyright Granlund | 37

Energy Audit Models in Finland 1

• Service sector• Building Energy Audit - the basic model for service sector buildings,

includes two categories of buildings: simple (schools, offices, etc) and complicated (swimming halls, ice arenas, etc)

• Energy Inspection - the model for small buildings, light reporting

• Post-acceptance Energy Audit - the model for new and renovated buildings, “tuning” the energy use to optimal level

• Follow-up Energy Audit - the model to update the previous energy audit

• In these models the audit cost (and subsidy) are related to the building volume

www.granlund.fiCopyright Granlund | 38

Energy Audit Models in Finland 2

• Industry• Energy Inspection - can be applied for extra-small SME’s

• Industrial Energy Audit - the model for sites with low energy intensive production process, looks at the energy use of the building and the process supply systems

• Industrial Energy Analysis - the heavier model for sites with medium energy intensive production process, includes the process analysis

• Process Industry Energy Analysis - the two-phase model for energy intensive process industry, the first step scans the needs for following Industrial Energy Audits and Analyses

• These models can be used as Follow-up Audits also

• In these models the audit cost (and subsidy) are related to yearly energy and water cost

www.granlund.fiCopyright Granlund | 39

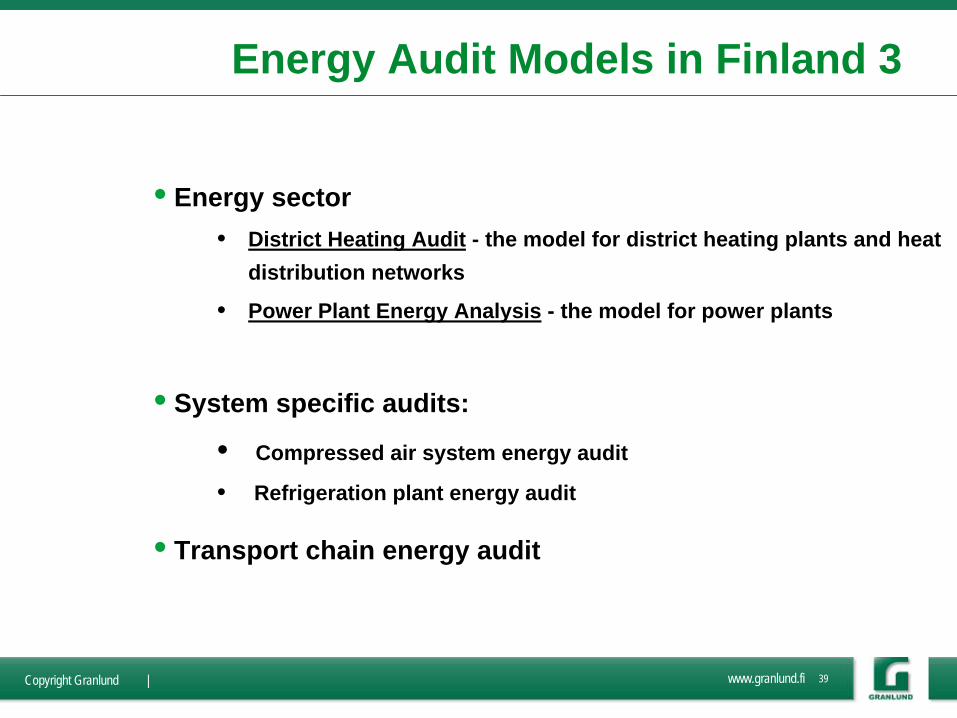

Energy Audit Models in Finland 3

• Energy sector• District Heating Audit - the model for district heating plants and heat

distribution networks

• Power Plant Energy Analysis - the model for power plants

• System specific audits:

• Compressed air system energy audit

• Refrigeration plant energy audit

• Transport chain energy audit

www.granlund.fiCopyright Granlund | 40EAR |

Total consumption, costs, saving potential, investments of 1 164 energy audits in the service sectors (37 milj. rm3) reported 2002-2007

Energy Audit Results 1 / Motiva database

Present consumption SERVICE SECTOR

1164 Saving potential 2002-2007

Heat

1 181 076 MWh/a 173 382 MWh/a 14,7 %

39 405 161 €/a 5 596 519 €/a 14,2 %

Electricity

1 023 810 MWh/a 66 456 MWh/a 6,5 %

57 909 814 €/a 4 080 196 €/a 7,0 %

Water

3 547 825 m3/a 213 873 m3/a 6,0 %

7 777 341 €/a 449 799 €/a 5,8 %

Total consumptions Total savings Investments

105 092 316 €/a 10 126 515 €/a 9,6 % 16 142 906 €

www.granlund.fiCopyright Granlund | 41EAR |

Total consumption, costs, saving potential, investments of 177 energy audits in the industrial sector with total energy consumption of less than 70 GWh/a during the period 2002-2007

Energy Audit Results 2 / Motiva database

Present consumption INDUSTRY, Energy consumption < 70 GWh/a

177 Saving potential 2002-2007

Heat

1 199 462 MWh/a 257 815 MWh/a 21,5 %

35 296 540 €/a 7 599 559 €/a 21,5 %

Electricity

1 019 827 MWh/a 61 452 MWh/a 6,0 %

45 969 711 €/a 3 361 503 €/a 7,3 %

Water

6 219 977 m3/a 657 969 m3/a 10,6 %

7 050 586 €/a 778 167 €/a 11, %

Total consumptions Total savings Investments

88 316 837 €/a 11 739 229 €/a 13,3 % 32 743 365 €

www.granlund.fiCopyright Granlund | 42EAR |

Sector-specific saving potential in the 5 228 energy audits reported in 1997-2007

Energy Audit Results 3 / Motiva database

REPORTED BUILDINGS 1992-2007 (5228 BUILDINGS)

SECTOR BUILD- SAVINGS- PBT INVEST- SAVING POTENTIAL

INGS POTENTIAL MENT HEAT ELECTRICITY WATER

TOTAL energy costs energy costs water costs

energy power energy power

pcs milj. €/a a milj.€ GWh/a milj. €/a milj. €/a GWh/a milj. €/a milj. €/a km³/a milj. €/a

PJ Public services 3124 17,6 1,9 33,4 397,1 9,5 1,0 74,8 3,9 1,7 743,2 1,4

PY Private services 1338 17,7 1,7 30,0 339,6 8,5 0,7 122,4 6,3 1,4 458,9 0,9

TE Industry, Energy consumption < 500 GW 738 41,1 2,2 89,2 1 184,5 24,0 1,6 239,8 9,7 2,6 3 718,2 3,2

TE Industry, Energy consumption > 500 GW 8 21,6 3,7 79,9 1 202,1 14,5 0,1 197,0 5,1 1,7 6 872,8 0,2

EA Heat and power 20 0,2 1,4 0,2 6,2 0,1 0,0 1,5 0,1 0,0 21,9 0,0

TOTAL 5228 98,1 2,4 232,8 3 129 56,5 3,3 636 25,1 7,5 11 815 5,7

www.granlund.fiCopyright Granlund | 43

The saving potential of the 1 368 energy audits (reported 2002-2007) divided according to pay back time

Energy Audit Results 4 / Motiva database

0

1

2

3

4

5

6

7

8

9

10

0 0-1 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 >10

Pay back time (year)

Sav

ing p

oten

tial

mill

ion €

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

Num

ber

of m

easu

res

Saving potential Number of measures

www.granlund.fiCopyright Granlund | 44

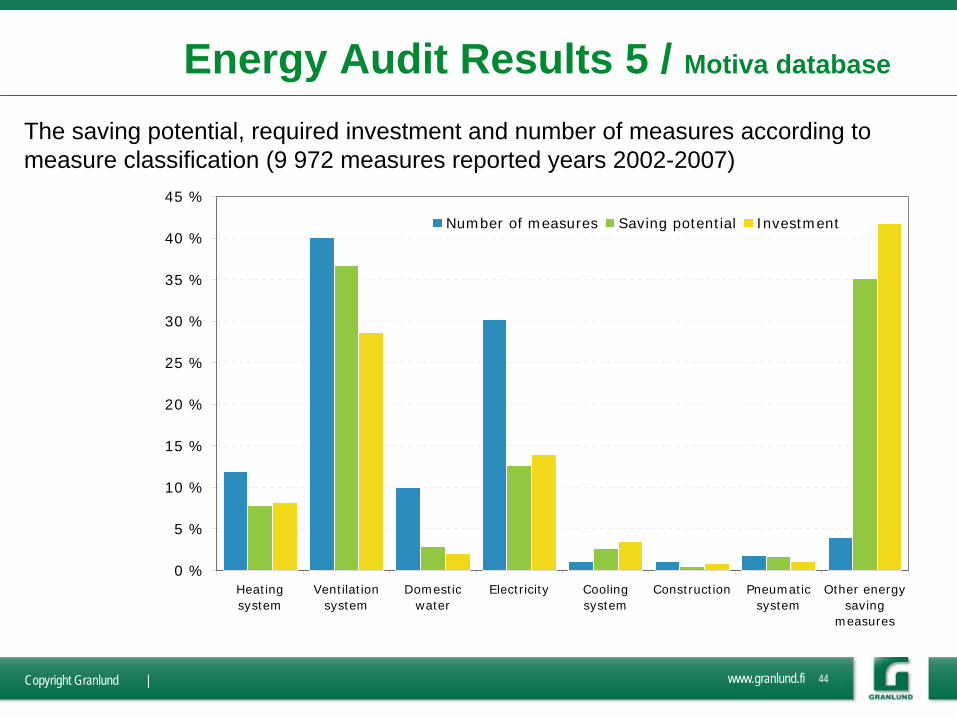

The saving potential, required investment and number of measures according to measure classification (9 972 measures reported years 2002-2007)

Energy Audit Results 5 / Motiva database

0 %

5 %

10 %

15 %

20 %

25 %

30 %

35 %

40 %

45 %

Heatingsystem

Ventilationsystem

Domesticwater

Electricity Coolingsystem

Construction Pneumaticsystem

Other energysaving

measures

Number of measures Saving potential Investment

www.granlund.fiCopyright Granlund | 45

Top 7 saving measures in the service sector

• Reduction of ventilation running hours

• Changes in lighting (low energy bulbs, schedules, controls, etc)

• Adjustment of temperature settings (heating and ventilation)

• Reduction of water flows in faucets and toilets

• Changes in tariffs = cost savings

• Adjustments in electrical heating (freezing protection, car heating, etc)

• Improvement of heat recovery system (existing or new)

www.granlund.fiCopyright Granlund | 46

Experiences: savings• saving potential in old and new buildings is about the same

• top 7 measures apply to most buildings

• no-cost measures are the majority

• in industry process-related savings =high potential + cost

• simple is beautiful, high-tech solutions considered expensive and unreliable

• clear suggestions are appreciated in report

• savings must not be over-estimated

• pay-back time requirements: 2-3 years

• maintenance staff training useful during audit

www.granlund.fiCopyright Granlund | 47

Implementation rate of saving potential by pay back time (1 957 energy audits, 14 868 savings measures)

Energy Audit Results 6 / Motiva database

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

0 0-1 1-2 2-3 3-4 4-5 5-6 6-7 7-8 8-9 9-10 10Pay back time (year)

Sav

ings

mill

ion €

Implemented Decided Considered Not implemented No information

www.granlund.fiCopyright Granlund | 48EAR |

Why are not all measures implemented?

• why saving measures are not implemented?

• No risks taken (indoor air quality, process, etc)

• No resources (good idea, but no staff for implementation)

• No money for investment

• Energy is not an important cost factor

• Audit report does not convince the client

www.granlund.fiCopyright Granlund | 49EAR |

More information about Energy Audits

• www.motiva.fi > choose English website >• Areas of operation > Energy auditing in Finland

• Projects and Campaigns > SAVE II -projects > Audit I and Audit II

• Projects and Campaigns > IEE-projects > Audit ‘06 conference material

•