turning innovation into patient benefit409c6700-fe35-4bc8-9af0-d98a7d4e8d… · turning innovation...

TRANSCRIPT

Turning innovation into patient benefit

Karl Mahler

Head of Investor Relations

London, December 2015

This presentation contains certain forward-looking statements. These forward-looking

statements may be identified by words such as ‘believes’, ‘expects’, ‘anticipates’, ‘projects’,

‘intends’, ‘should’, ‘seeks’, ‘estimates’, ‘future’ or similar expressions or by discussion of,

among other things, strategy, goals, plans or intentions. Various factors may cause actual

results to differ materially in the future from those reflected in forward-looking statements

contained in this presentation, among others:

1 pricing and product initiatives of competitors;

2 legislative and regulatory developments and economic conditions;

3 delay or inability in obtaining regulatory approvals or bringing products to market;

4 fluctuations in currency exchange rates and general financial market conditions;

5 uncertainties in the discovery, development or marketing of new products or new uses of existing products, including without limitation negative results of clinical trials or research projects, unexpected side-effects of pipeline or marketed products;

6 increased government pricing pressures;

7 interruptions in production;

8 loss of or inability to obtain adequate protection for intellectual property rights;

9 litigation;

10 loss of key executives or other employees; and

11 adverse publicity and news coverage.

Any statements regarding earnings per share growth is not a profit forecast and should not be interpreted

to mean that Roche’s earnings or earnings per share for this year or any subsequent period will

necessarily match or exceed the historical published earnings or earnings per share of Roche.

For marketed products discussed in this presentation, please see full prescribing information on our

website – www.roche.com

All mentioned trademarks are legally protected 2

Performance update

Innovation and efficiency

Improving the standard of care

Outlook

3

Q3 2015: Sales growth for fifth consecutive year

4 All growth rates at constant exchange rates (CER)

0% 0% 1%

4%

2%

6%

4%

6% 6%

4%

8%

7%

5%

4%

5%

6%

5%

7%

6%

0%

2%

4%

6%

8%

10%

Q1

11

Q2

11

Q3

11

Q4

11

Q1

12

Q2

12

Q3

12

Q4

12

Q1

13

Q2

13

Q3

13

Q4

13

Q1

14

Q2

14

Q3

14

Q4

14

Q1

15

Q2

15

Q3

15

HY 2015: Strong underlying Group core operating

profit & margin

5

% of sales

CHFbn

CER=Constant Exchange Rates

* Excluding sale of filgrastim rights in 2014 at CER

8'3 8'6 9'5 9'4 9'2

38'1% 38'5%

40'7% 41'0%

39'2%

HY 2011 HY 2012 HY 2013 HY 2014 HY 2015

+2% at CER (+7%*)

(+0.4%p

excl. filgrastim*)

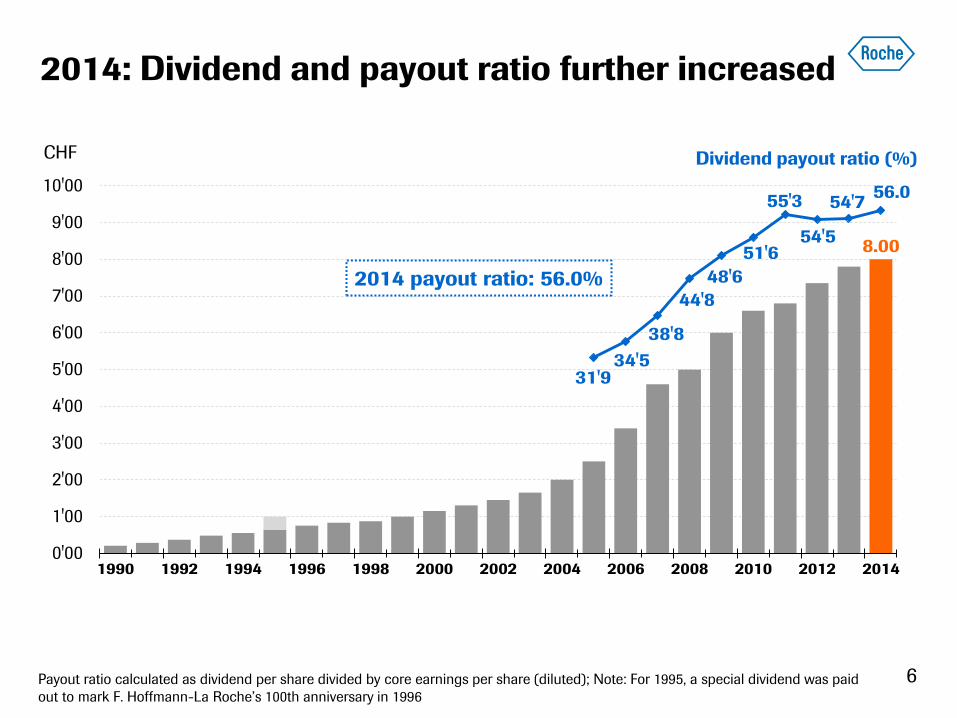

2014: Dividend and payout ratio further increased

6 1 compound annual growth rate

8.00

31'9 34'5

38'8

44'8

48'6

51'6

55'3

54'5

54'7 56.0

0'00

1'00

2'00

3'00

4'00

5'00

6'00

7'00

8'00

9'00

10'00

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Dividend payout ratio (%) CHF

2014 payout ratio: 56.0%

Payout ratio calculated as dividend per share divided by core earnings per share (diluted); Note: For 1995, a special dividend was paid

out to mark F. Hoffmann-La Roche’s 100th anniversary in 1996

Performance update

Innovation and efficiency

Improving the standard of care

Outlook

7

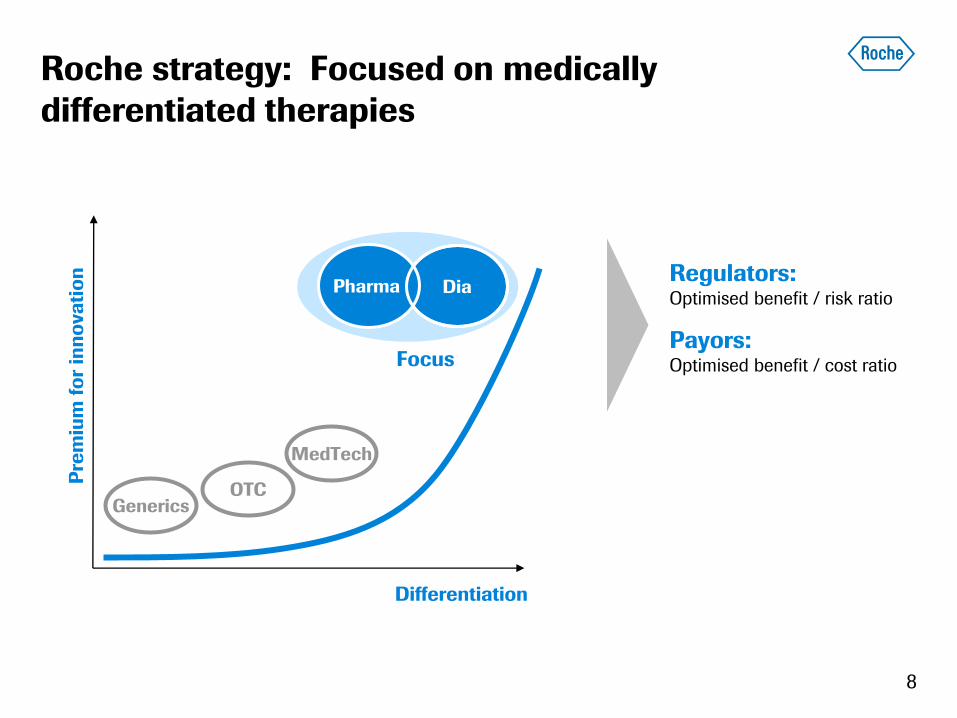

Roche strategy: Focused on medically

differentiated therapies

8

Generics

Differentiation

MedTech

OTC

Pre

miu

m f

or

inn

ova

tio

n

Dia Pharma

Focus

Regulators: Optimised benefit / risk ratio

Payors: Optimised benefit / cost ratio

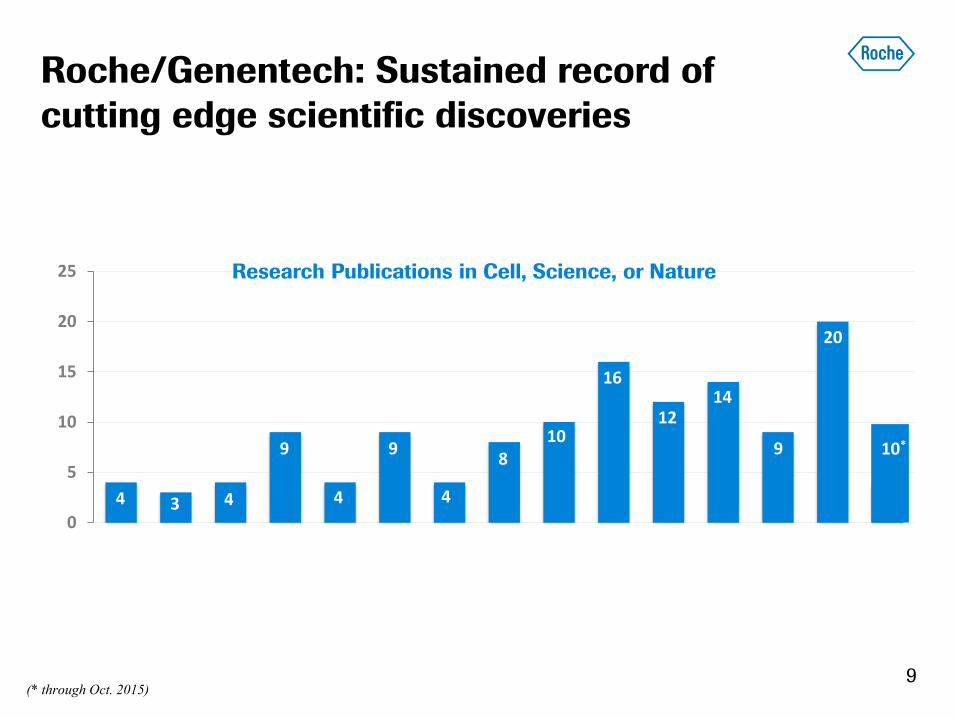

Roche/Genentech: Sustained record of

cutting edge scientific discoveries

0

5

10

15

20

25

(* through Oct. 2015)

4 3 4

9

4

9

4

8 10

16

12 14

9

20

Research Publications in Cell, Science, or Nature

10*

9

Roche’s strategy remains unchanged

Success hinges on excellence in innovation & execution

• Focus investment on differentiated molecules

• Continuously improve processes

10

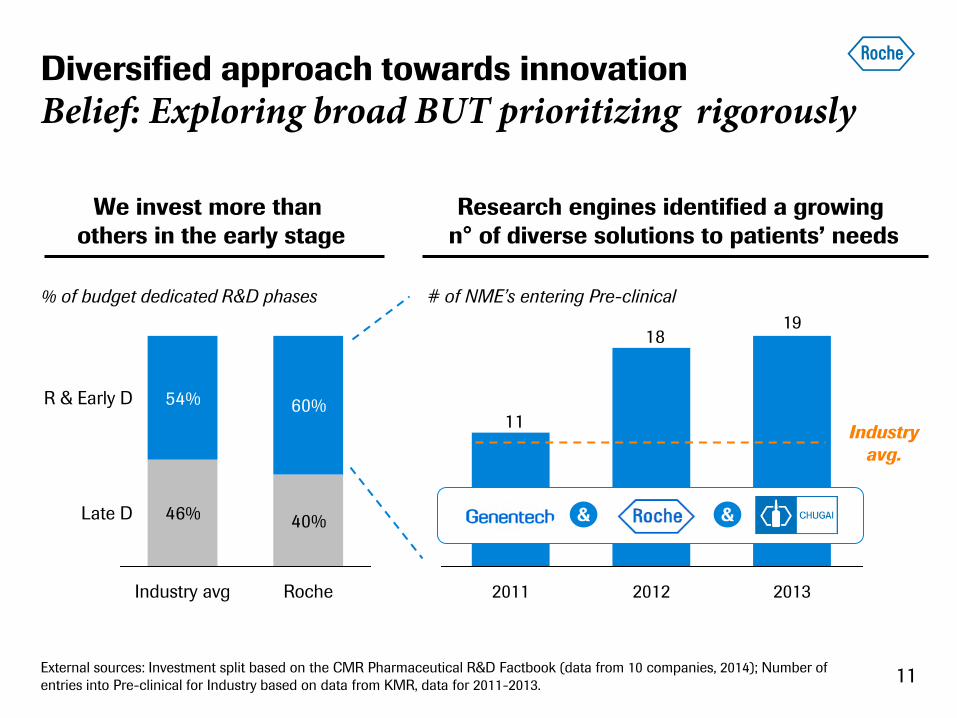

Diversified approach towards innovation

Belief: Exploring broad BUT prioritizing rigorously

We invest more than

others in the early stage

Research engines identified a growing

n° of diverse solutions to patients’ needs

46% 40%

54% 60%R & Early D

Roche

Late D

Industry avg

18

11

19

2013 2011 2012

# of NME’s entering Pre-clinical

Industry

avg.

% of budget dedicated R&D phases

<<< & &

External sources: Investment split based on the CMR Pharmaceutical R&D Factbook (data from 10 companies, 2014); Number of

entries into Pre-clinical for Industry based on data from KMR, data for 2011-2013. 11

However, we set a high bar for our R&D pipeline …

Targeting clear differentiation in areas of unmet need

Assessment for late stage entry

candidates & line extensions

Clinical differentiation

Threshold

high low

low

high

Greater

differentiation

Sa

les

Time

Un

me

t m

ed

ica

l n

ee

d

Continued

Disqualified

Illustrative

Total sales potential

12

Roche’s strategy remains unchanged

Success hinges on excellence in innovation & execution

• Focus investment on differentiated molecules

• Continuously improve processes

13

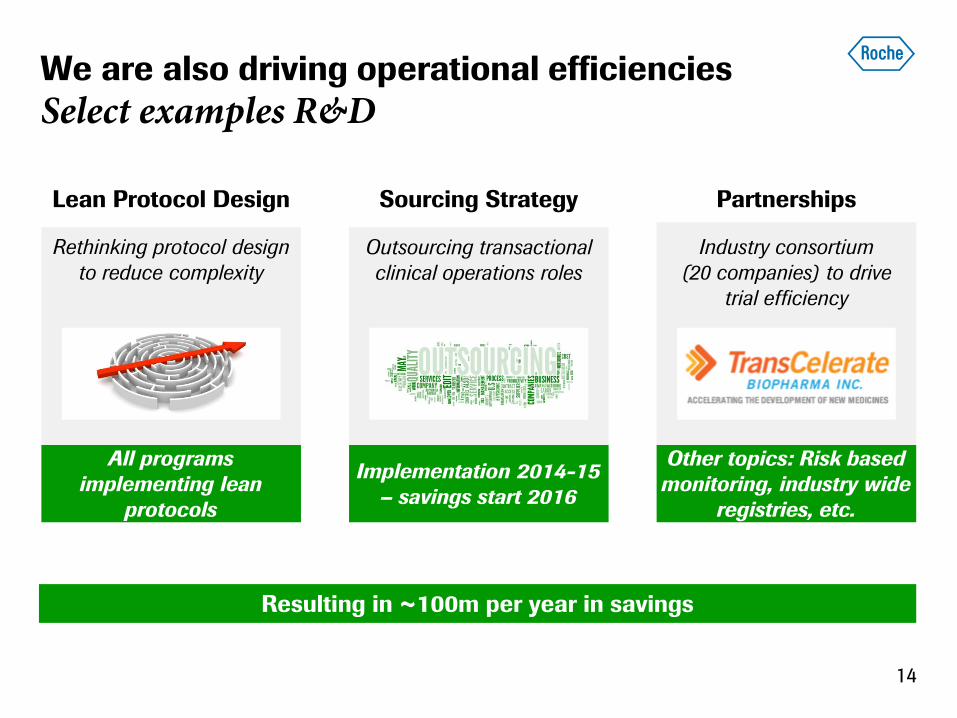

We are also driving operational efficiencies

Select examples R&D

Lean Protocol Design Sourcing Strategy Partnerships

Rethinking protocol design

to reduce complexity

All programs

implementing lean

protocols

Outsourcing transactional

clinical operations roles

Implementation 2014-15

– savings start 2016

Other topics: Risk based

monitoring, industry wide

registries, etc.

Industry consortium

(20 companies) to drive

trial efficiency

Resulting in ~100m per year in savings

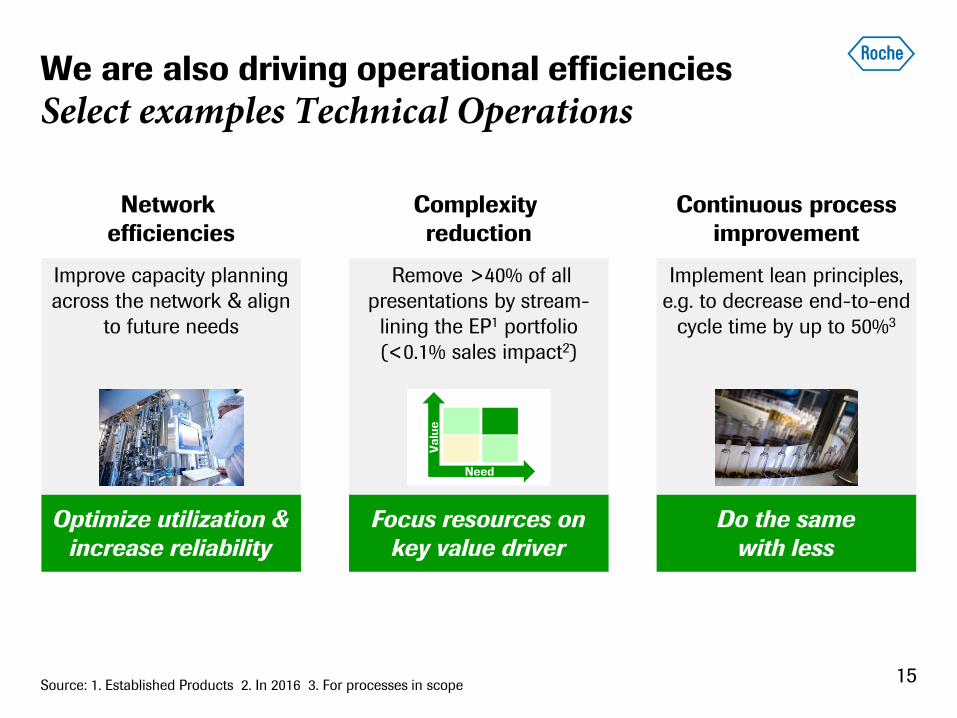

14

Network

efficiencies

Complexity

reduction

Continuous process

improvement

Optimize utilization &

increase reliability

Do the same

with less

Focus resources on

key value driver

Remove >40% of all

presentations by stream-

lining the EP1 portfolio

(<0.1% sales impact2)

Improve capacity planning

across the network & align

to future needs

Implement lean principles,

e.g. to decrease end-to-end

cycle time by up to 50%3

Source: 1. Established Products 2. In 2016 3. For processes in scope

Need

Va

lue

We are also driving operational efficiencies

Select examples Technical Operations

15

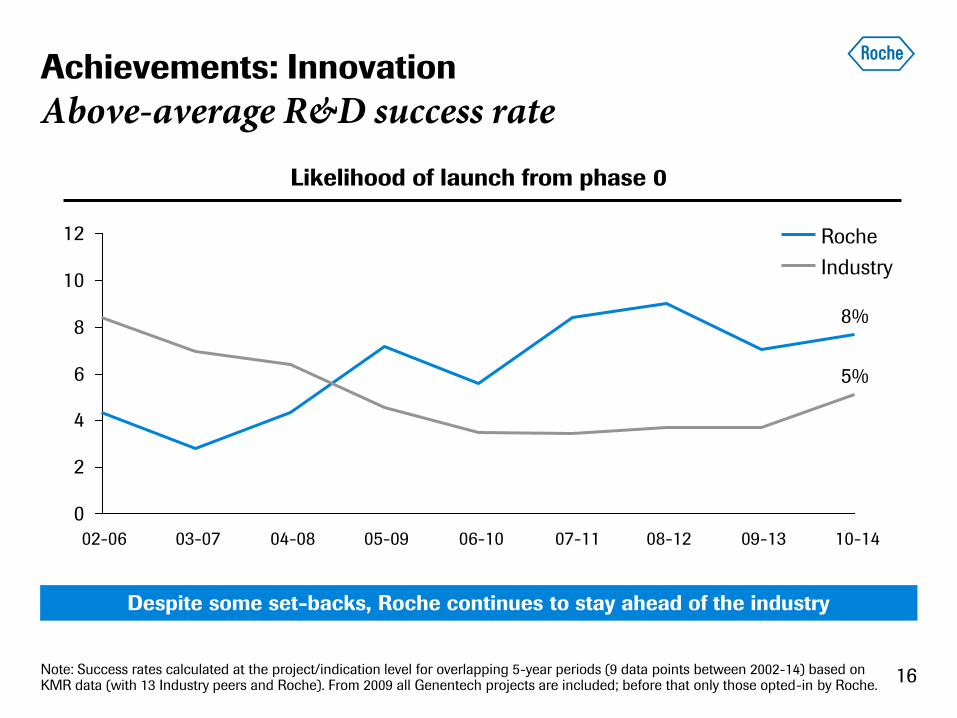

8%

5%

0

2

4

6

8

10

12

10-14 09-13 08-12 07-11 06-10 05-09 04-08 03-07 02-06

Roche

Industry

Despite some set-backs, Roche continues to stay ahead of the industry

Likelihood of launch from phase 0

Achievements: Innovation

Above-average R&D success rate

Note: Success rates calculated at the project/indication level for overlapping 5-year periods (9 data points between 2002-14) based on KMR data (with 13 Industry peers and Roche). From 2009 all Genentech projects are included; before that only those opted-in by Roche.

16

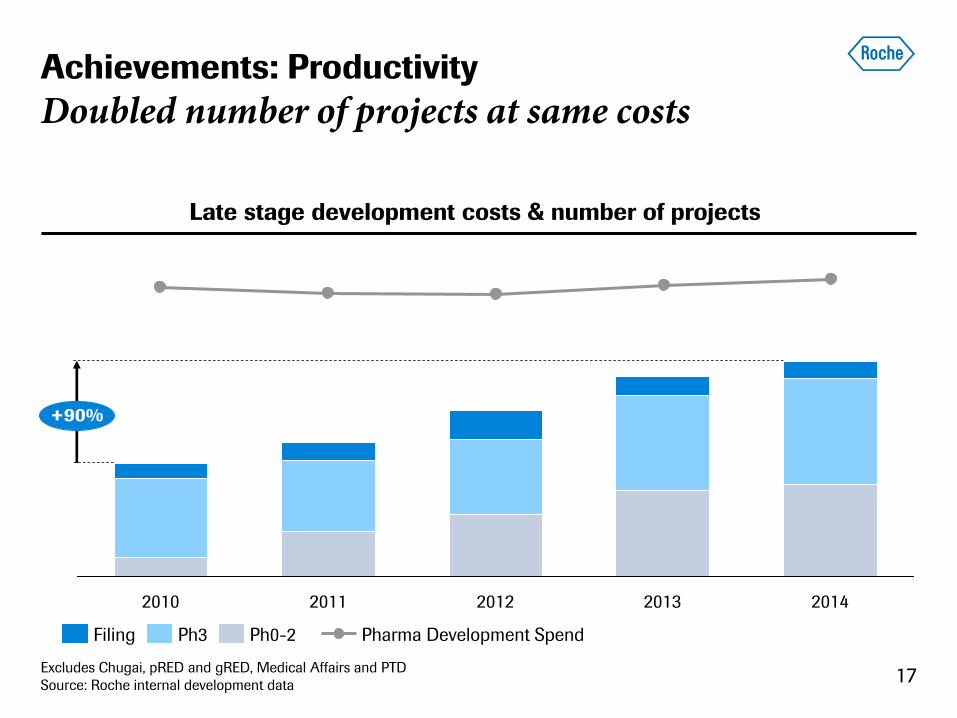

Achievements: Productivity

Doubled number of projects at same costs

2012 2013 2014 2010 2011

+90%

Filing Ph0-2 Ph3 Pharma Development Spend

Late stage development costs & number of projects

Excludes Chugai, pRED and gRED, Medical Affairs and PTD

Source: Roche internal development data 17

Performance update

Innovation and efficiency

Improving the standard of care

Outlook

18

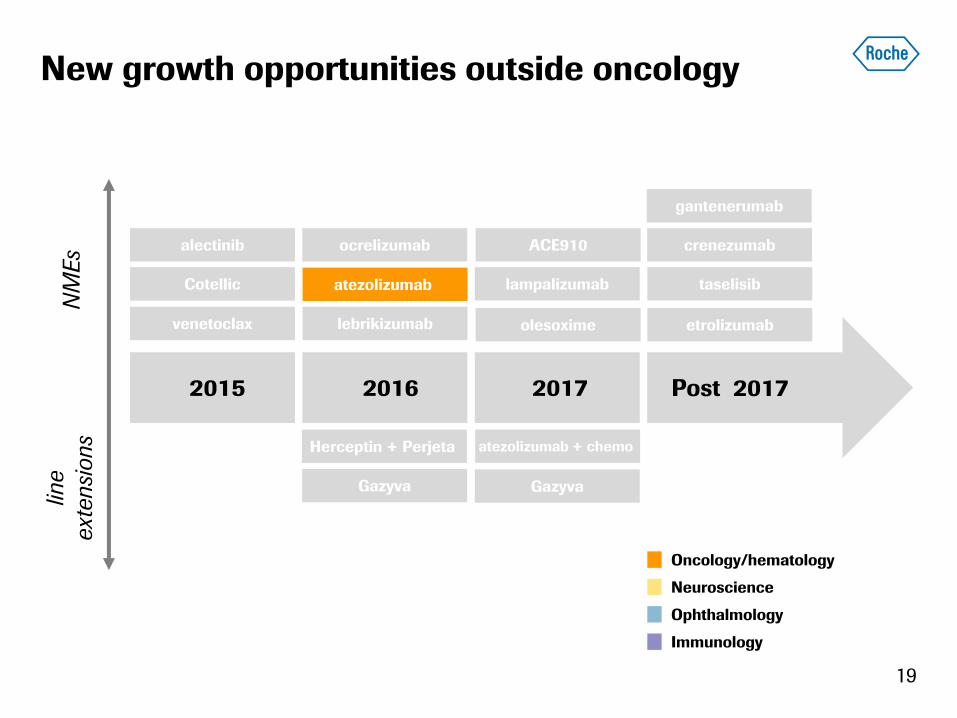

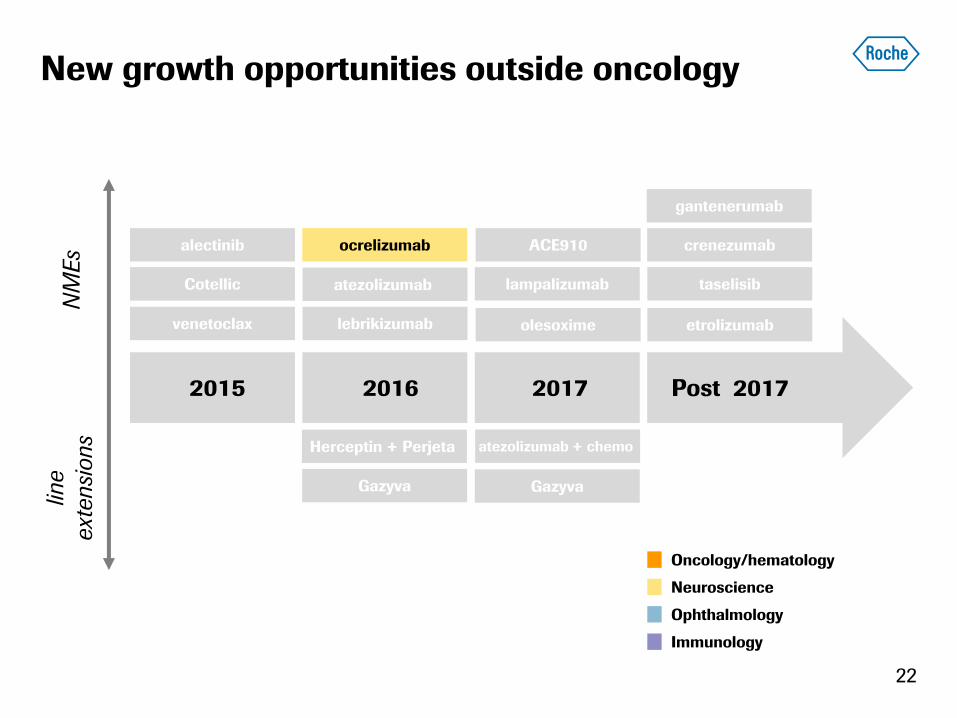

taselisib

19

NM

Es

line

ext

ensi

ons

2015 2016 2017

venetoclax

alectinib

Cotellic

lebrikizumab

atezolizumab

ocrelizumab

lampalizumab

ACE910

Post 2017

etrolizumab

crenezumab

gantenerumab

olesoxime

Herceptin + Perjeta

Gazyva

atezolizumab + chemo

Gazyva

New growth opportunities outside oncology

Oncology/hematology

Neuroscience

Ophthalmology

Immunology

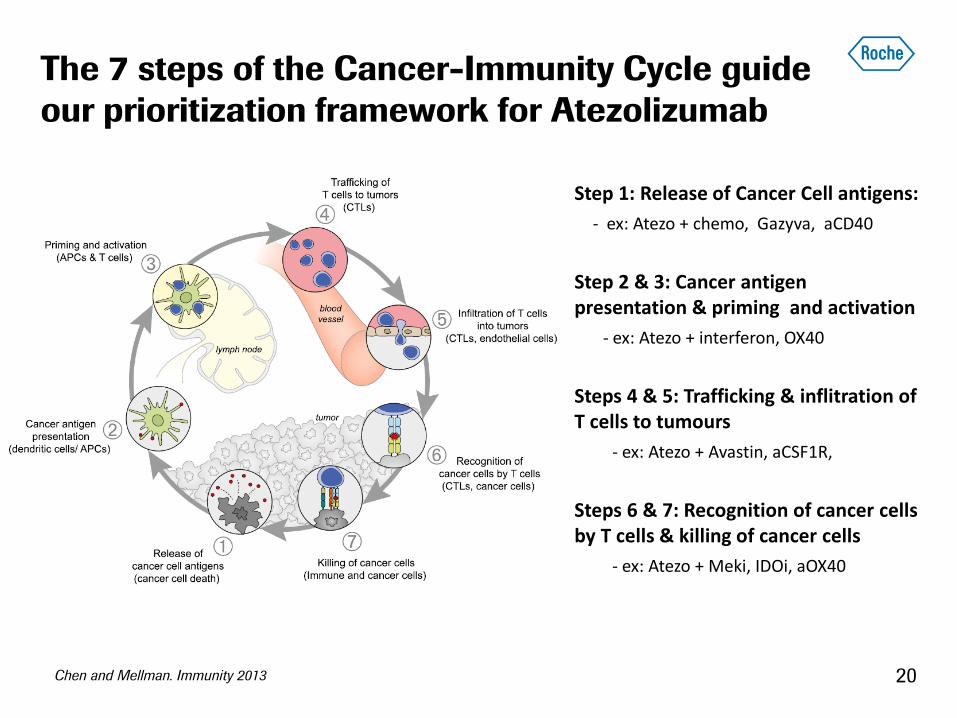

The 7 steps of the Cancer-Immunity Cycle guide

our prioritization framework for Atezolizumab

Step 1: Release of Cancer Cell antigens:

- ex: Atezo + chemo, Gazyva, aCD40

Step 2 & 3: Cancer antigen presentation & priming and activation

- ex: Atezo + interferon, OX40

Steps 4 & 5: Trafficking & inflitration of T cells to tumours

- ex: Atezo + Avastin, aCSF1R,

Steps 6 & 7: Recognition of cancer cells by T cells & killing of cancer cells

- ex: Atezo + Meki, IDOi, aOX40

Chen and Mellman. Immunity 2013 20

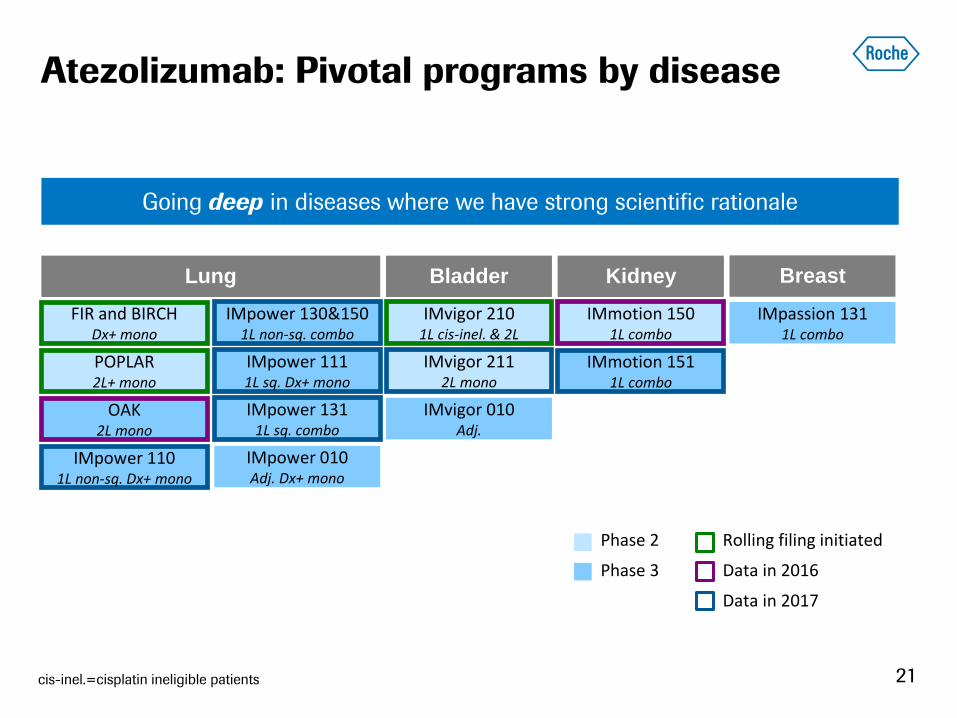

Atezolizumab: Pivotal programs by disease

21

KIDNEY

Going deep in diseases where we have strong scientific rationale

cis-inel.=cisplatin ineligible patients

Lung

FIR and BIRCH Dx+ mono

Bladder

IMvigor 210 1L cis-inel. & 2L

Breast Kidney

POPLAR 2L+ mono

IMpower 110 1L non-sq. Dx+ mono

IMpower 130&150 1L non-sq. combo

IMpower 111 1L sq. Dx+ mono

IMpower 131 1L sq. combo

OAK 2L mono

IMpower 010 Adj. Dx+ mono

IMvigor 211 2L mono

IMvigor 010 Adj.

IMmotion 150 1L combo

IMmotion 151 1L combo

IMpassion 131 1L combo

Rolling filing initiated

Data in 2016

Data in 2017

Phase 2

Phase 3

taselisib

22

NM

Es

line

ext

ensi

ons

2015 2016 2017

venetoclax

alectinib

Cotellic

lebrikizumab

atezolizumab

ocrelizumab

lampalizumab

ACE910

Post 2017

etrolizumab

crenezumab

gantenerumab

olesoxime

Herceptin + Perjeta

Gazyva

atezolizumab + chemo

Gazyva

New growth opportunities outside oncology

Oncology/hematology

Neuroscience

Ophthalmology

Immunology

23

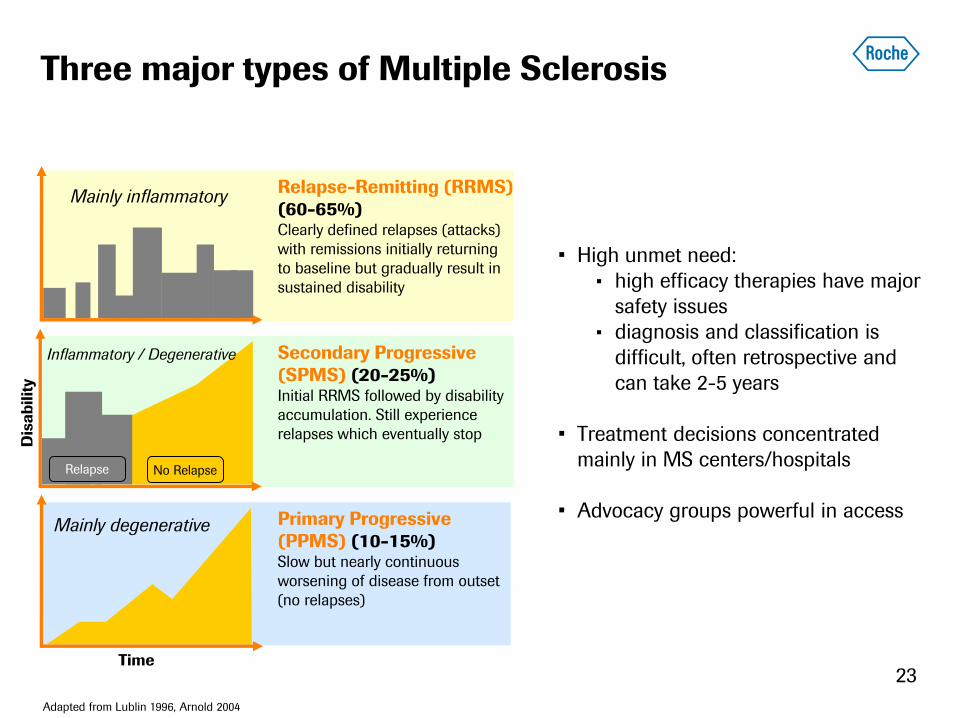

Secondary Progressive

(SPMS) (20-25%) Initial RRMS followed by disability

accumulation. Still experience

relapses which eventually stop

Primary Progressive

(PPMS) (10-15%) Slow but nearly continuous

worsening of disease from outset

(no relapses)

Relapse-Remitting (RRMS)

(60-65%) Clearly defined relapses (attacks)

with remissions initially returning

to baseline but gradually result in

sustained disability

Three major types of Multiple Sclerosis

Dis

ab

ilit

y

Time

Relapse No Relapse

Mainly degenerative

Mainly inflammatory

Adapted from Lublin 1996, Arnold 2004

Inflammatory / Degenerative

• High unmet need:

• high efficacy therapies have major

safety issues

• diagnosis and classification is

difficult, often retrospective and

can take 2-5 years

• Treatment decisions concentrated

mainly in MS centers/hospitals

• Advocacy groups powerful in access

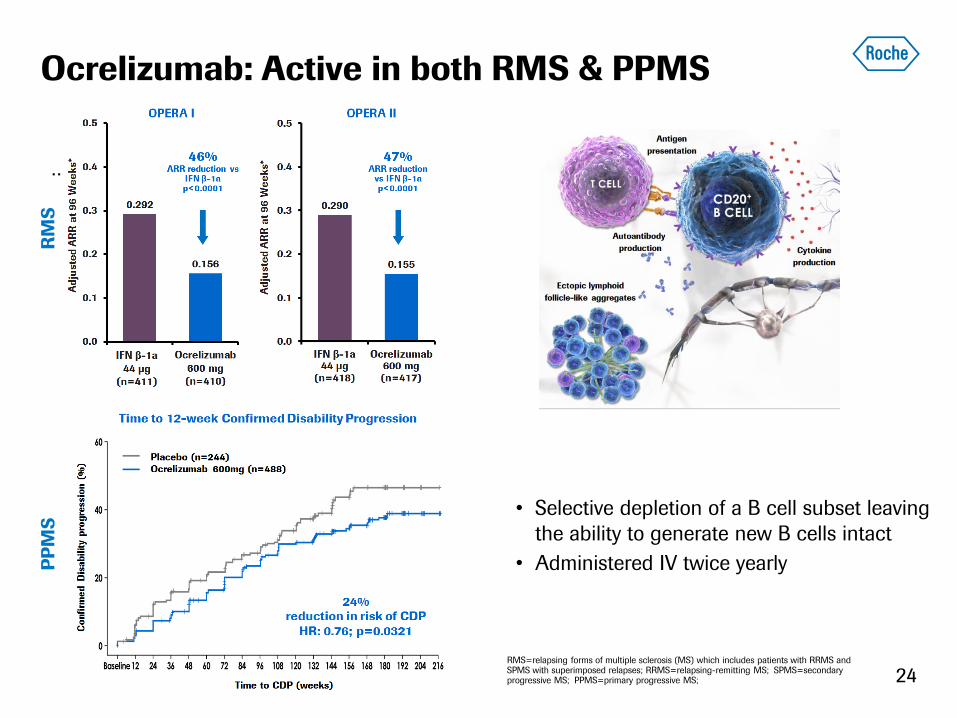

Ocrelizumab: Active in both RMS & PPMS

24

• Selective depletion of a B cell subset leaving

the ability to generate new B cells intact

• Administered IV twice yearly

RMS=relapsing forms of multiple sclerosis (MS) which includes patients with RRMS and SPMS with superimposed relapses; RRMS=relapsing-remitting MS; SPMS=secondary progressive MS; PPMS=primary progressive MS;

PPMS:

: R

MS

P

PM

S

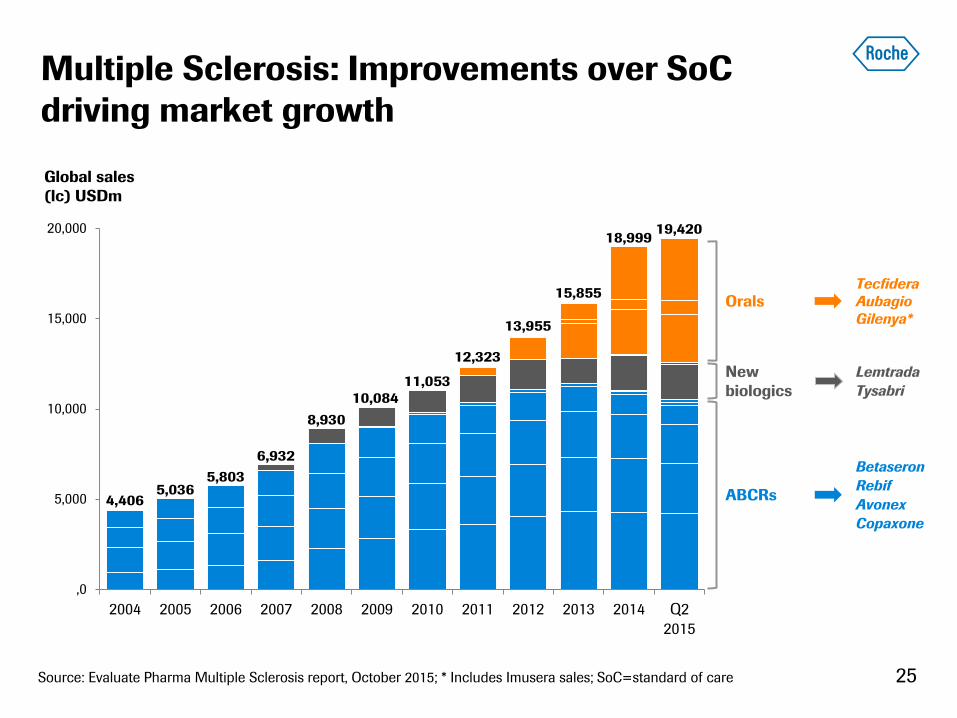

Multiple Sclerosis: Improvements over SoC

driving market growth

25

,0

5,000

10,000

15,000

20,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Q2

2015

19,420 18,999

15,855

13,955

12,323

11,053

10,084

8,930

6,932

5,803 5,036

4,406

Global sales

(lc) USDm

Source: Evaluate Pharma Multiple Sclerosis report, October 2015; * Includes Imusera sales; SoC=standard of care

Betaseron

Rebif

Avonex

Copaxone

Lemtrada

Tysabri

Tecfidera

Aubagio

Gilenya*

ABCRs

Orals

New

biologics

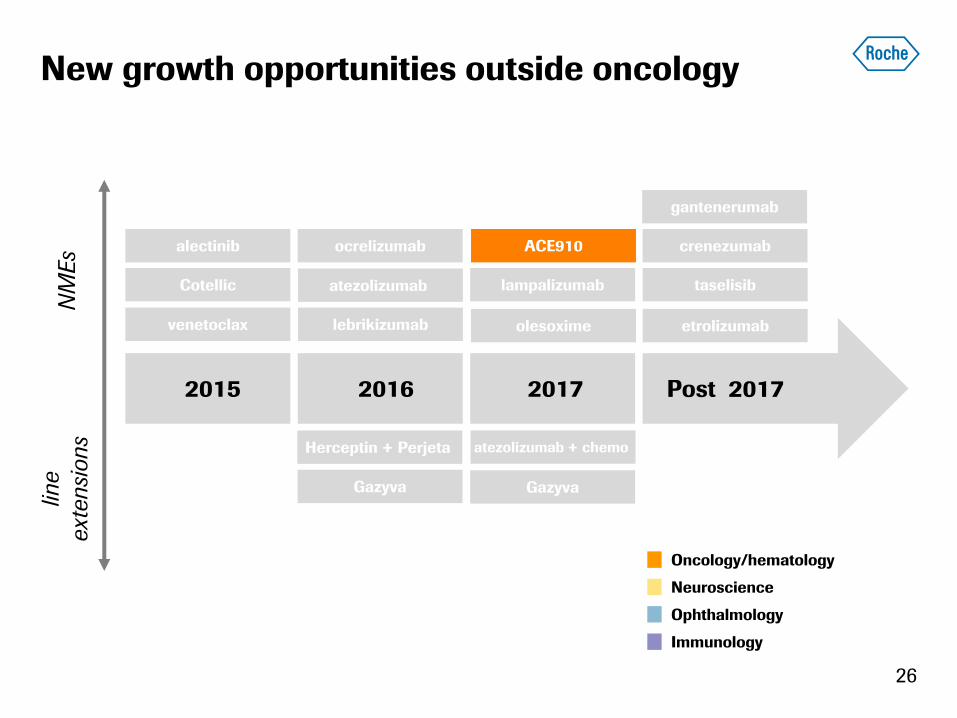

taselisib

26

NM

Es

line

ext

ensi

ons

2015 2016 2017

venetoclax

alectinib

Cotellic

lebrikizumab

atezolizumab

ocrelizumab

lampalizumab

ACE910

Post 2017

etrolizumab

crenezumab

gantenerumab

olesoxime

Herceptin + Perjeta

Gazyva

atezolizumab + chemo

Gazyva

New growth opportunities outside oncology

Oncology/hematology

Neuroscience

Ophthalmology

Immunology

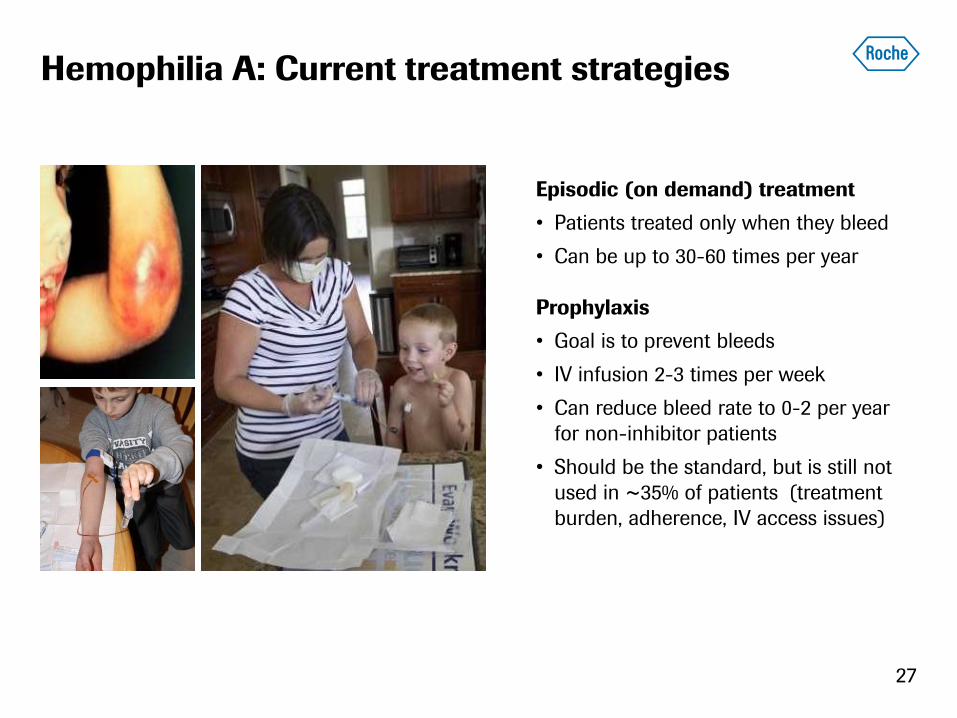

Hemophilia A: Current treatment strategies

27

Episodic (on demand) treatment

• Patients treated only when they bleed

• Can be up to 30-60 times per year

Prophylaxis

• Goal is to prevent bleeds

• IV infusion 2-3 times per week

• Can reduce bleed rate to 0-2 per year

for non-inhibitor patients

• Should be the standard, but is still not

used in ~35% of patients (treatment

burden, adherence, IV access issues)

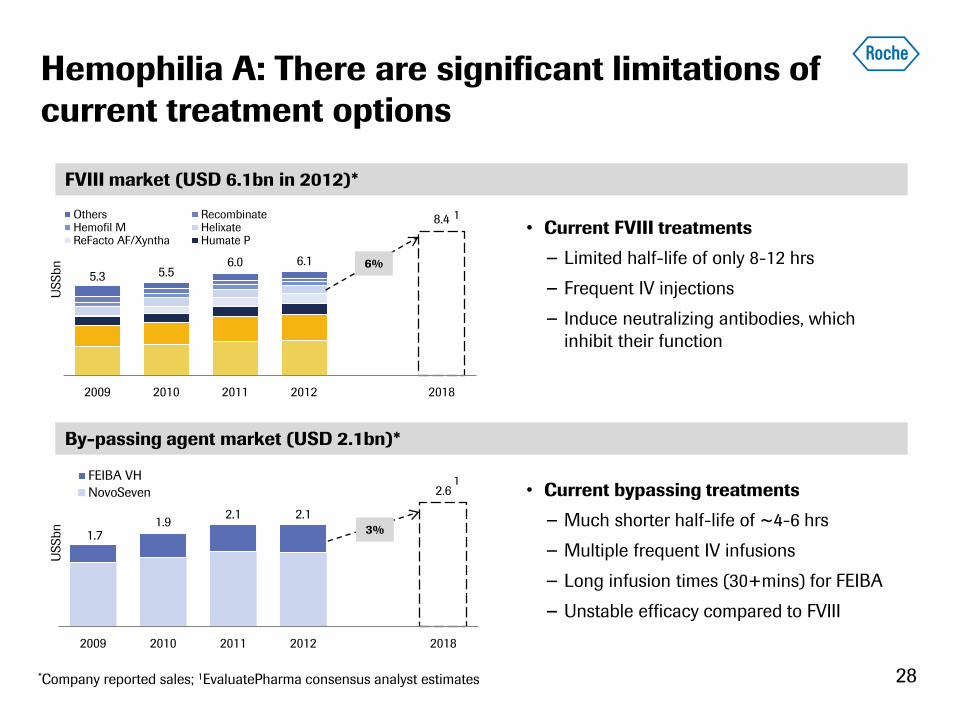

Hemophilia A: There are significant limitations of

current treatment options

1.7 1.9

2.1 2.1

2.6

2009 2010 2011 2012 2018

FEIBA VH

NovoSeven

3%

5.3 5.5 6.0 6.1

8.4

2009 2010 2011 2012 2018

Others RecombinateHemofil M HelixateReFacto AF/Xyntha Humate P

6%

*Company reported sales; 1EvaluatePharma consensus analyst estimates

1

FVIII market (USD 6.1bn in 2012)*

By-passing agent market (USD 2.1bn)*

• Current FVIII treatments

− Limited half-life of only 8-12 hrs

− Frequent IV injections

− Induce neutralizing antibodies, which

inhibit their function

• Current bypassing treatments

− Much shorter half-life of ~4-6 hrs

− Multiple frequent IV infusions

− Long infusion times (30+mins) for FEIBA

− Unstable efficacy compared to FVIII

28

1

US

Sb

n

US

Sb

n

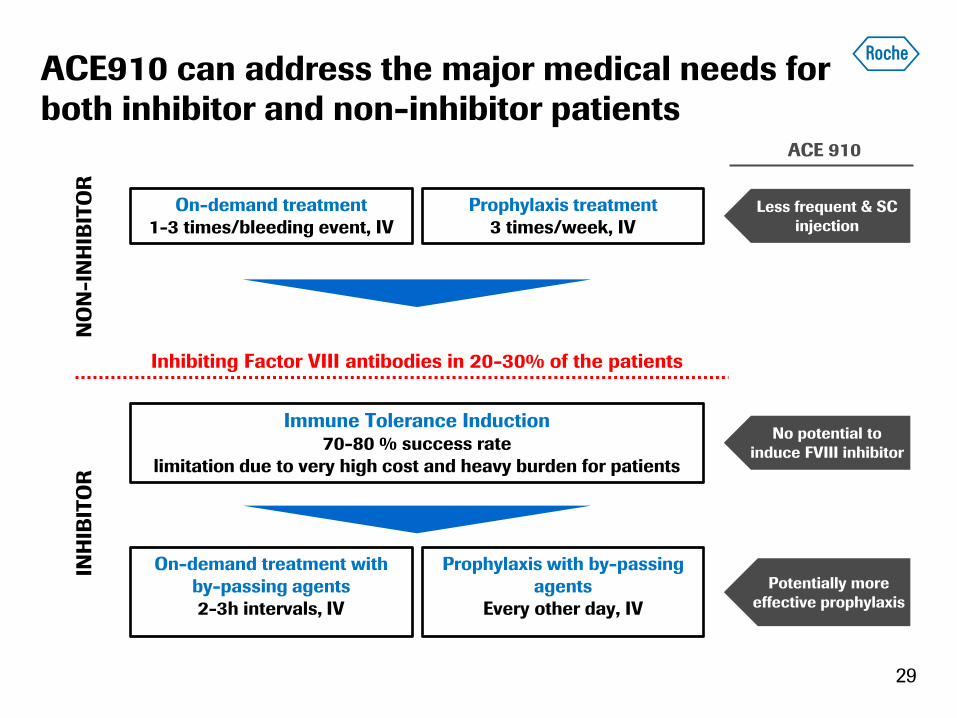

ACE910 can address the major medical needs for

both inhibitor and non-inhibitor patients

29

Potentially more

effective prophylaxis

No potential to

induce FVIII inhibitor

ACE 910

Prophylaxis treatment

3 times/week, IV

On-demand treatment

1-3 times/bleeding event, IV

Inhibiting Factor VIII antibodies in 20-30% of the patients

NO

N-I

NH

IBIT

OR

Prophylaxis with by-passing

agents

Every other day, IV

On-demand treatment with

by-passing agents

2-3h intervals, IV

INH

IBIT

OR

Immune Tolerance Induction 70-80 % success rate

limitation due to very high cost and heavy burden for patients

Less frequent & SC

injection

30

Performance up-date

Maximising existing franchises

New growth opportunities

Biosimilars

Outlook

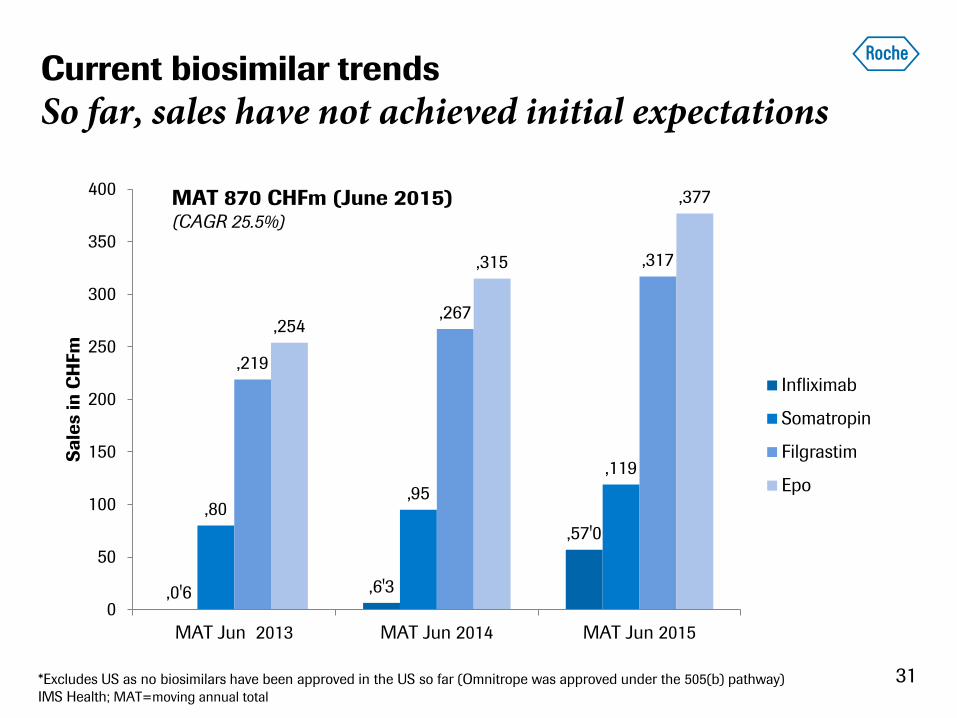

,0'6 ,6'3

,57'0

,80 ,95

,119

,219

,267

,317

,254

,315

,377

0

50

100

150

200

250

300

350

400

MAT Jun 2013 MAT Jun 2014 MAT Jun 2015

Sa

les in

CH

Fm

Infliximab

Somatropin

Filgrastim

Epo

Current biosimilar trends

So far, sales have not achieved initial expectations

31

MAT 870 CHFm (June 2015) (CAGR 25.5%)

*Excludes US as no biosimilars have been approved in the US so far (Omnitrope was approved under the 505(b) pathway)

IMS Health; MAT=moving annual total

Generics vs biosimilars

Clear divide in uptake; complex market drivers

0%

20%

40%

60%

80%

100%

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

32

Market share

Zyprexa (Eli Lilly)

Diovan (Novartis)

Filgrastim

EPO

Somatropin

Small molecule

Virtually disappear

Payer driven: 7 biosimilars

Efficacy visible immediately

High turnover of patients

Driven by price and patient offering

9 innovators, one biosimilar

Efficacy visible only longer term

No switching

Sources: IMS Biosimilar Dashboard, IMS & Roche analysis 1 Volume market share based on EU5 average; 2 Volume market share based on average of France & Germany EPO; 3 Data based on % remaining sales in EU

1

1

2

3

3

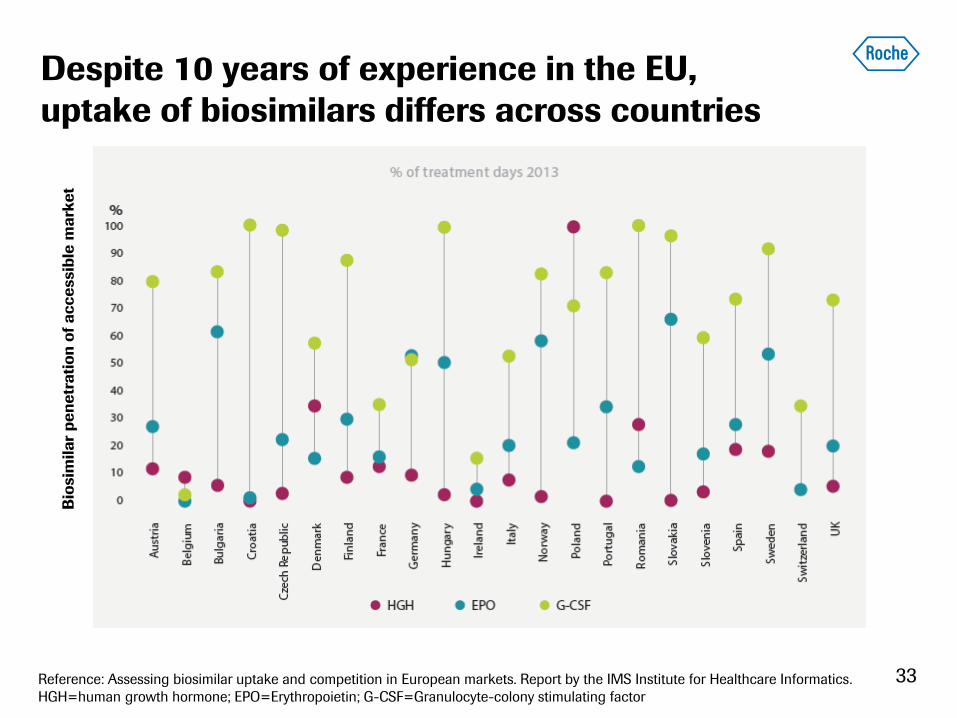

Despite 10 years of experience in the EU,

uptake of biosimilars differs across countries

33

Bio

sim

ila

r p

en

etr

ati

on

of

ac

ce

ssib

le m

ark

et

Reference: Assessing biosimilar uptake and competition in European markets. Report by the IMS Institute for Healthcare Informatics.

HGH=human growth hormone; EPO=Erythropoietin; G-CSF=Granulocyte-colony stimulating factor

34

Performance up-date

Maximising existing franchises

New growth opportunities

Biosimilars

Outlook

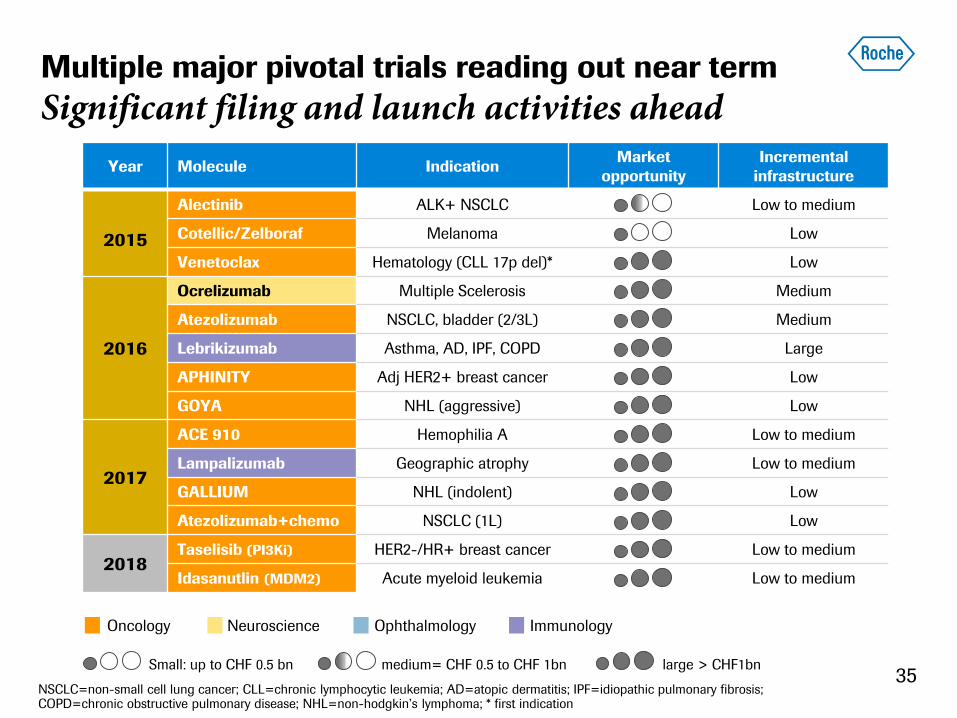

Multiple major pivotal trials reading out near term

Significant filing and launch activities ahead

35

Year Molecule Indication Market

opportunity

Incremental

infrastructure

2015

Alectinib ALK+ NSCLC Low to medium

Cotellic/Zelboraf Melanoma Low

Venetoclax Hematology (CLL 17p del)* Low

2016

Ocrelizumab Multiple Scelerosis Medium

Atezolizumab NSCLC, bladder (2/3L) Medium

Lebrikizumab Asthma, AD, IPF, COPD Large

APHINITY Adj HER2+ breast cancer Low

GOYA NHL (aggressive) Low

2017

ACE 910 Hemophilia A Low to medium

Lampalizumab Geographic atrophy Low to medium

GALLIUM NHL (indolent) Low

Atezolizumab+chemo NSCLC (1L) Low

2018 Taselisib (PI3Ki) HER2-/HR+ breast cancer Low to medium

Idasanutlin (MDM2) Acute myeloid leukemia Low to medium

Oncology Neuroscience Ophthalmology Immunology

Small: up to CHF 0.5 bn medium= CHF 0.5 to CHF 1bn large > CHF1bn

NSCLC=non-small cell lung cancer; CLL=chronic lymphocytic leukemia; AD=atopic dermatitis; IPF=idiopathic pulmonary fibrosis; COPD=chronic obstructive pulmonary disease; NHL=non-hodgkin’s lymphoma; * first indication

Positive outlook

Strong pipeline mitigates biosimilar impact

2014 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E

Marketed

products

Sales

Pipeline

Biosimilars

MabThera, Herceptin, Avastin

NME launches

Venetoclax, Alectinib, Cotellic, Ocrelizumab, Atezolizumab,

Lebrikizumab, ACE910, Lampalizumab

36

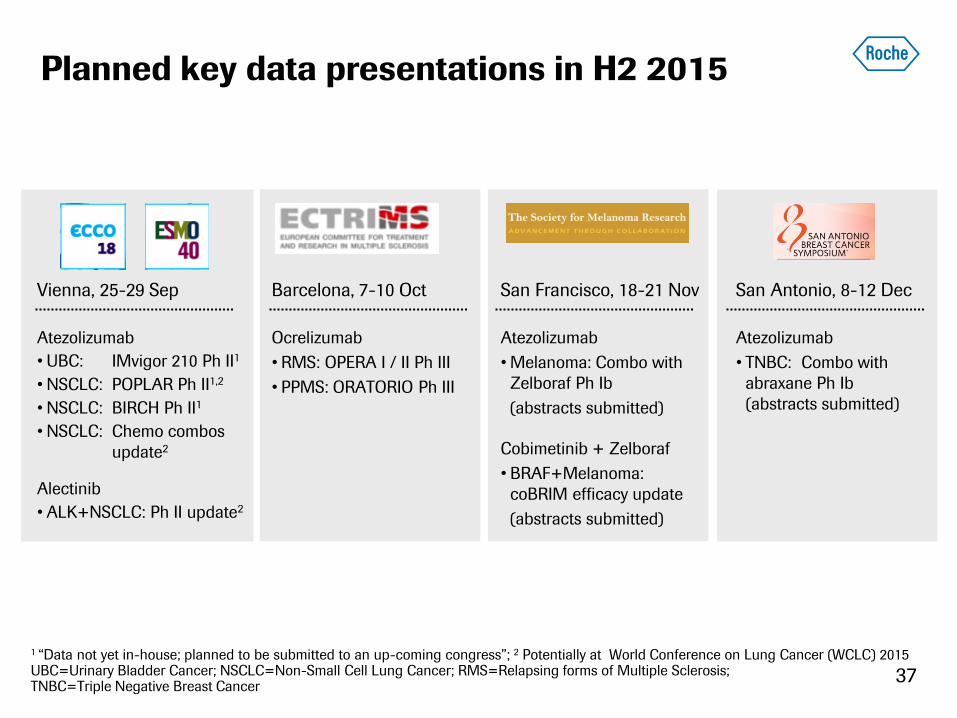

Planned key data presentations in H2 2015

37

Vienna, 25-29 Sep

Atezolizumab

• UBC: IMvigor 210 Ph II1

• NSCLC: POPLAR Ph II1,2

• NSCLC: BIRCH Ph II1

• NSCLC: Chemo combos

update2

Alectinib

• ALK+NSCLC: Ph II update2

San Antonio, 8-12 Dec

Atezolizumab

• TNBC: Combo with

abraxane Ph Ib

(abstracts submitted)

San Francisco, 18-21 Nov

Atezolizumab

• Melanoma: Combo with

Zelboraf Ph Ib

(abstracts submitted)

Cobimetinib + Zelboraf

• BRAF+Melanoma:

coBRIM efficacy update

(abstracts submitted)

Barcelona, 7-10 Oct

Ocrelizumab

• RMS: OPERA I / II Ph III

• PPMS: ORATORIO Ph III

1 “Data not yet in-house; planned to be submitted to an up-coming congress”; 2 Potentially at World Conference on Lung Cancer (WCLC) 2015 UBC=Urinary Bladder Cancer; NSCLC=Non-Small Cell Lung Cancer; RMS=Relapsing forms of Multiple Sclerosis; TNBC=Triple Negative Breast Cancer

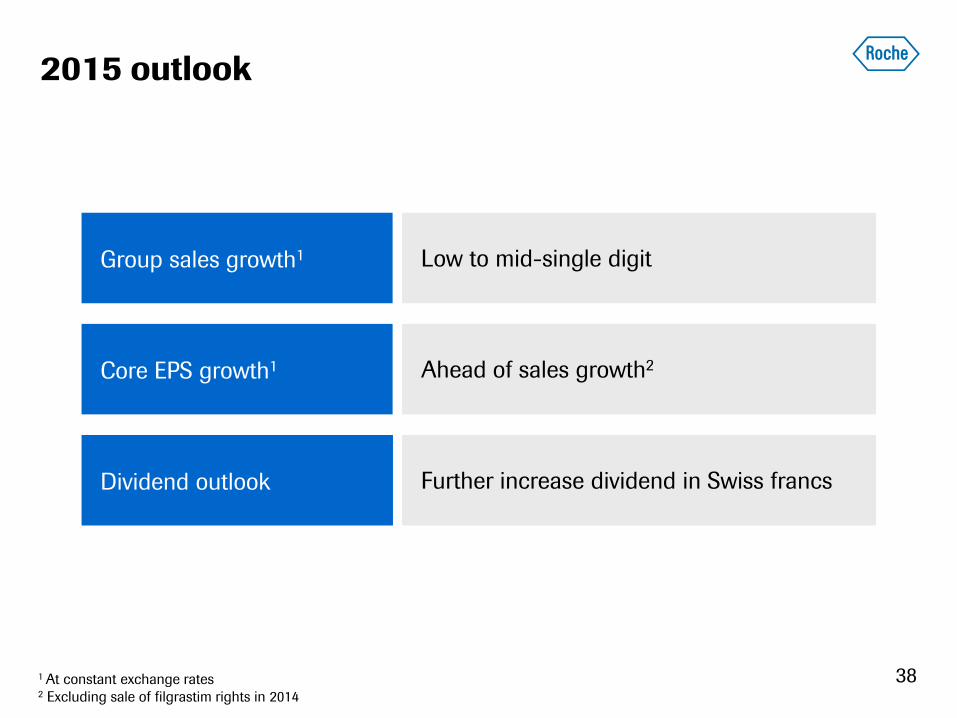

2015 outlook

Group sales growth1 Low to mid-single digit

Core EPS growth1 Ahead of sales growth2

Dividend outlook Further increase dividend in Swiss francs

1 At constant exchange rates 2 Excluding sale of filgrastim rights in 2014

38

Appendix

39

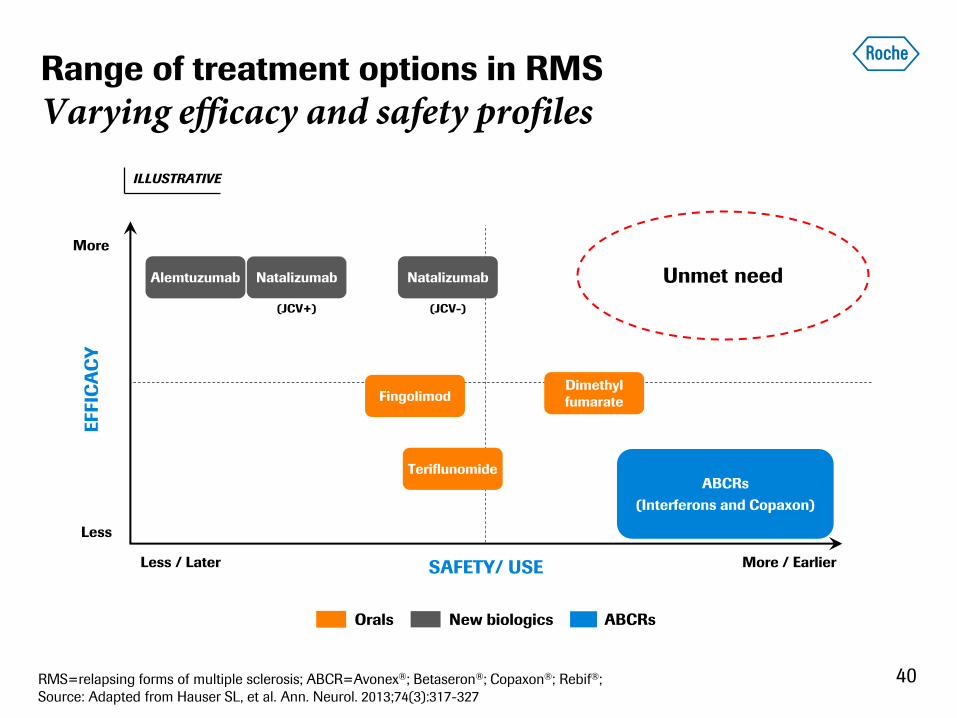

Fingolimod

Teriflunomide ABCRs

(Interferons and Copaxon)

More

Less

More / Earlier Less / Later SAFETY/ USE

EFFIC

AC

Y

Alemtuzumab Natalizumab

Dimethyl

fumarate

Range of treatment options in RMS

Varying efficacy and safety profiles

40

ILLUSTRATIVE

Natalizumab

(JCV+) (JCV-)

Unmet need

New biologics Orals ABCRs

RMS=relapsing forms of multiple sclerosis; ABCR=Avonex®; Betaseron®; Copaxon®; Rebif®;

Source: Adapted from Hauser SL, et al. Ann. Neurol. 2013;74(3):317-327

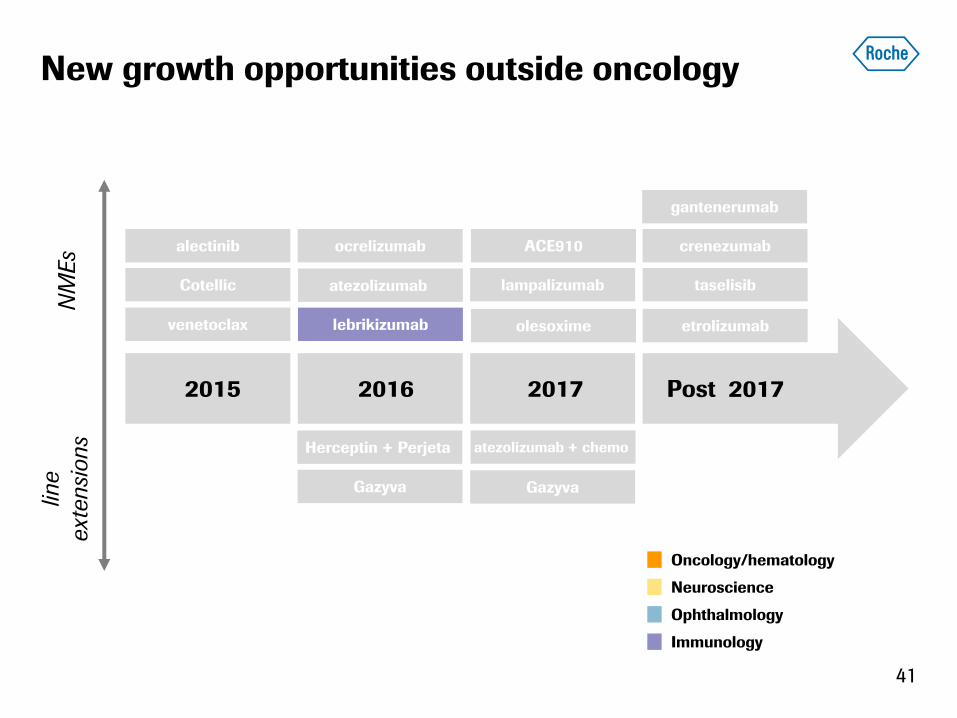

taselisib

41

NM

Es

line

ext

ensi

ons

2015 2016 2017

venetoclax

alectinib

Cotellic

lebrikizumab

atezolizumab

ocrelizumab

lampalizumab

ACE910

Post 2017

etrolizumab

crenezumab

gantenerumab

olesoxime

Herceptin + Perjeta

Gazyva

atezolizumab + chemo

Gazyva

New growth opportunities outside oncology

Oncology/hematology

Neuroscience

Ophthalmology

Immunology

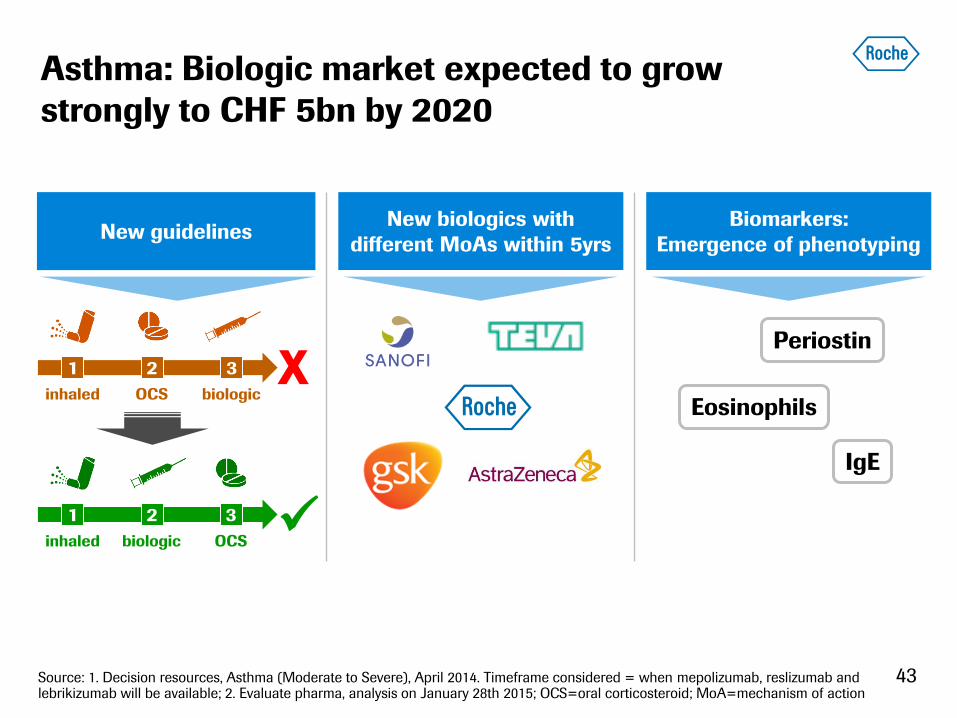

Severe asthma: High unmet need in growing

market

42

Global asthma market 2014 vs 2020

11%

29%

Small Molecules Biologics

2014 1 biologic

Shifting clinical practice

2020 6 biologics

Note: Market shares based on value (sales); Source: Evaluate; defined by daily use of ≥500ug ICS + LABA

• Approx. 300m patients worldwide and

growing strongly

• 5-10% asthma patients have severe

disease, and ~30% of severe disease

is uncontrolled despite maximal

therapy

• Over 4.5m severe asthmatics with

uncontrolled disease

Asthma: Biologic market expected to grow

strongly to CHF 5bn by 2020

Biomarkers:

Emergence of phenotyping New guidelines

New biologics with

different MoAs within 5yrs

Periostin

Eosinophils

IgE

1 2 3

inhaled OCS biologic

1 2 3

inhaled OCS biologic

X

43 Source: 1. Decision resources, Asthma (Moderate to Severe), April 2014. Timeframe considered = when mepolizumab, reslizumab and lebrikizumab will be available; 2. Evaluate pharma, analysis on January 28th 2015; OCS=oral corticosteroid; MoA=mechanism of action

Doing now what patients need next