trust procedures and pitfalls part ii - step canada · withholding on distributions capital ` the...

TRANSCRIPT

Trust Procedures and PitfallsPart II

December 2008

1

Distributions to aNon-resident BeneficiaryIncome

Domestic law states that income that is allocated to a non-resident beneficiary will be subject to Canadian withholding tax of 25%This rate is reduced withholding rate may be reduced under certain tax treatiesNew ss 212(1)(b) exempts arm’s length interest after 2007Income that is taxed in the trust (i.e. not allocated to a beneficiary) is added to the capital of the trust in the year after it is earned.

2

Distributions to aNon-resident BeneficiaryCapital

When capital is distributed, the beneficiary is considered to have disposed of a portion of his or her capital interest in the trustThere will be no capital gain or loss to the beneficiary because proceeds are deemed to equal the adjusted cost baseSubject to exemption for “treaty-protected property” (discussed later) Non-resident beneficiary is required to file a Canadian tax return to report the disposition (even though there is no gain).

3

Withholding on DistributionsCapital

The trust is required to withhold 25% of a capital distribution made to a non-resident beneficiary (subject to treaty reduction) If a section116 Certificate is obtained, no withholding is required.

Must file no later than10 days after the distribution; generally use Form T2062.After 2008, a simpler notification to CRA for “treaty-protected property” can be used.Risk exists re “reasonable enquiry” so third party executors or trustees will prefer the usual section 116 method.

4

Foreign Withholding Taxes onDistributed Income

If the trust earns income from foreign sources, withholding taxes may apply in the foreign country. If the income is distributed to a beneficiary, the beneficiary may be able to claim a credit for the foreign taxes.The trustee should advise the beneficiary of taxes withheldExample:

If a Canadian trust (with a US beneficiary) invests in shares of U.S. corporations, a 15% withholding tax will be deducted from the U.S. dividends. A U.S. individual beneficiary should be able to claim the US tax withheld as a “tax paid “on Form 1040 – U.S. Individual Income Tax Return.

5

U.S. Beneficiaries ofForeign Non-grantor Trusts

A non-grantor trust generally arises where the person who creates or makes a gratuitous transfer to a trust does not retain economic interests or control of the trustAn trust of a Canadian-resident decedent will frequently be a “foreign non-grantor trust” for U.S. purposes. U.S. beneficiaries of foreign non-grantor trusts are subject to punitive taxation in the United States if the trust’s income (including capital gains) is not distributed annually.

6

U.S. BeneficiariesAccumulation Distributions

For US purposes, income that is not distributed in the year will become part of the “undistributed net income” (“UNI”) of the trust.

Income includes capital gains, which might otherwise be on account of capital.

When UNI is paid in a later year it will taxed punitivelyIncome will not retain its character and will be taxed to the beneficiary as ordinary income - the 15% rate for qualifying dividends and long-term capital gains will not be available. The income will be taxable in the actual year it was earned, so interest will be charged by the IRS.

Foreign tax credit not available if Canadian tax has been paid in a prior year by the trust.

7

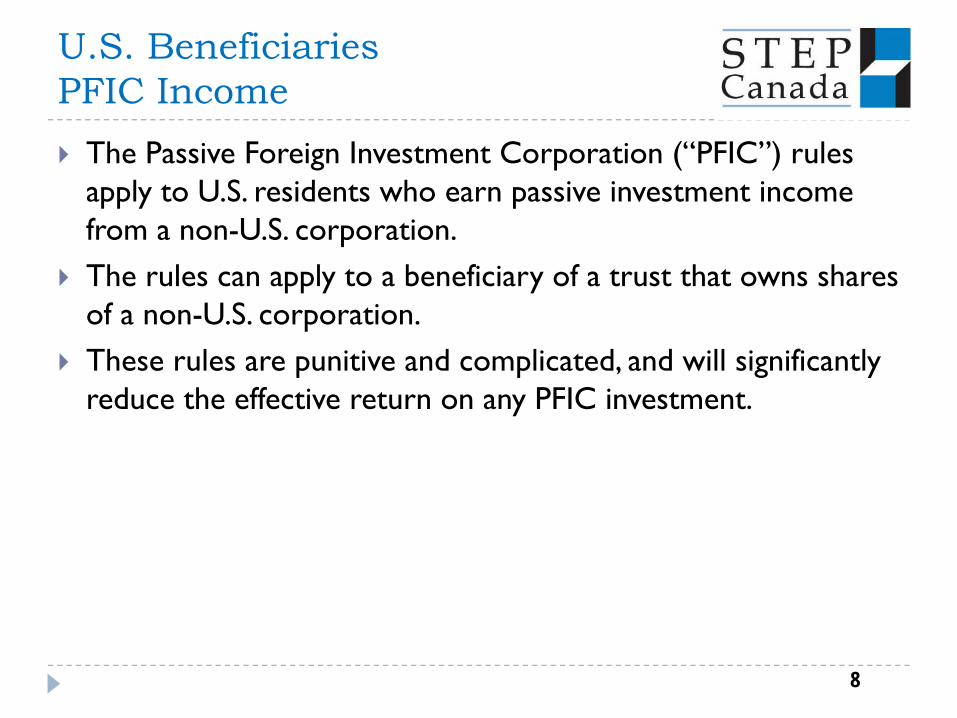

U.S. BeneficiariesPFIC Income

The Passive Foreign Investment Corporation (“PFIC”) rules apply to U.S. residents who earn passive investment income from a non-U.S. corporation. The rules can apply to a beneficiary of a trust that owns shares of a non-U.S. corporation. These rules are punitive and complicated, and will significantly reduce the effective return on any PFIC investment.

8

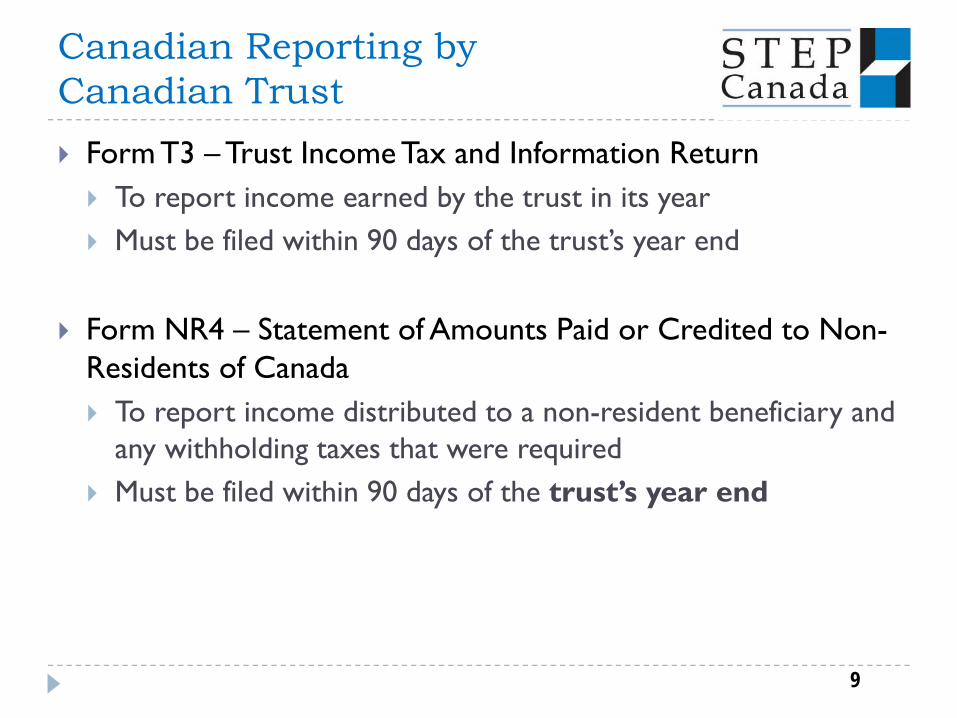

Canadian Reporting byCanadian Trust

Form T3 – Trust Income Tax and Information Return To report income earned by the trust in its yearMust be filed within 90 days of the trust’s year end

Form NR4 – Statement of Amounts Paid or Credited to Non-Residents of Canada

To report income distributed to a non-resident beneficiary and any withholding taxes that were requiredMust be filed within 90 days of the trust’s year end

9

Canadian Reporting byNon-resident Beneficiary

T1 Individual Income Tax Return For any year in which a capital distribution is received from a Canadian trust, even if no Canadian income tax will be payable. This requirement is eliminated for 2009 where the capital interest qualifies as “treaty-protected property”.

T2062 – Request by a Non-Resident of Canada for a Certificate of Compliance Related to the Disposition of Taxable Canadian Property

10

U.S. Reporting byU.S.-resident Beneficiary

Trustee will need to provide sufficient information for beneficiary to file:

Form 3520 – Annual Return to Report Transactions with Foreign Trusts and Receipt of Certain Foreign GiftsForm 8621 – Return by a Shareholder of a Passive Foreign Investment Company or Qualified Electing Fund(if there are any PFIC investments in the trust)

Forms are due at the same time as the beneficiary’s U.S. Individual Income Tax Return (April 15th, subject to extensions)Penalties for beneficiary (i.e. for you as trustee) are significant but exclusion for “reasonable cause” may be available

11

The Legal, Tax and Administrative Aspects of Administering an Estate

Maintaining a Trust’s Testamentary Status

Brian E. Cohen Borden Ladner Gervais LLP

December 10, 2008

12

Testamentary Trusts-The Why?

Ability to Income SplitTestamentary trusts are taxed at graduated marginal rates - inter vivos trusts taxed at top marginal rateTrust is usually a separate taxpayer

Protection of Vulnerable BeneficiariesMinorsSpouses not previously involved in businessDisabled BeneficiariesAddicts

Protection of Family AssetsSeparation, divorce or spendthrift

13

Testamentary Trusts – The What?

Section 108 of the Income Tax Act defines “testamentary trust” as:

…a trust that arose on and as a consequence of the death of an individual…

Two key features:It is a “trust” – I.e. must meet the 3 certaintiesIt arose as a consequence of the death of an individual.

The Income Tax Act definition of the term “trust” includes an estate

As it is a trust it is stuck with normal trust rules such as:Rule against Perpetuities; Accumulation rules;Even hand principle;Saunders v. Vautier; andCharacterization of income and capital

14

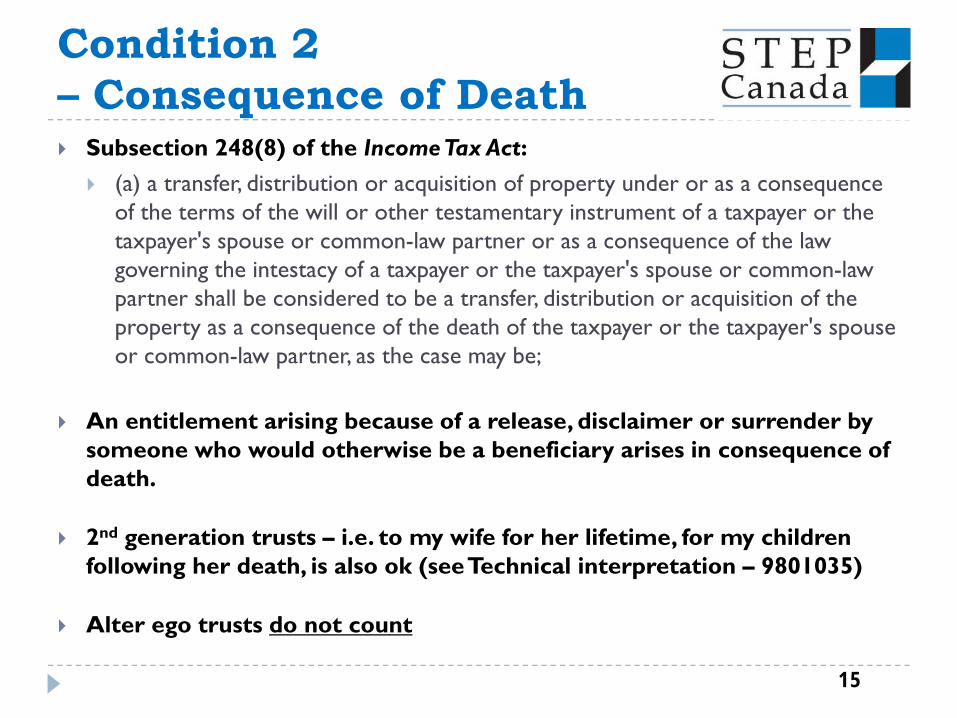

Condition 2– Consequence of Death

Subsection 248(8) of the Income Tax Act:(a) a transfer, distribution or acquisition of property under or as a consequence of the terms of the will or other testamentary instrument of a taxpayer or the taxpayer's spouse or common-law partner or as a consequence of the law governing the intestacy of a taxpayer or the taxpayer's spouse or common-law partner shall be considered to be a transfer, distribution or acquisition of the property as a consequence of the death of the taxpayer or the taxpayer's spouse or common-law partner, as the case may be;

An entitlement arising because of a release, disclaimer or surrender by someone who would otherwise be a beneficiary arises in consequence of death.

2nd generation trusts – i.e. to my wife for her lifetime, for my children following her death, is also ok (see Technical interpretation – 9801035)

Alter ego trusts do not count

15

Tainting the Testamentary Trust

Section 108 of the Act lists items that can “taint” a trust causing it to lose its testamentary status.

Tainting will cause the trust to lose access to the graduated marginal rates.

First exclusion is simple – a testamentary trust cannot be created by a person other than the one referred to in the phrase “consequence of death of an individual”.

A testamentary trust will lose its status if property is contributed to the trust by anyone other than the individual in consequence of whose death the trust was to be created.

The CRA does not want people to be able to effectively use a testamentary trust to circumvent the inter vivos trusts tax rate

16

Loans by Beneficiaries to Trusts (2nd reading)

For trusts that arise after December 20, 2002, rules exist for loans by non-arm’s length beneficiaries to the trust.

Where such a beneficiary:

loans or guarantees a debt;or incurs any other obligation on behalf of the trust

the trust may lose its testamentary status.

17

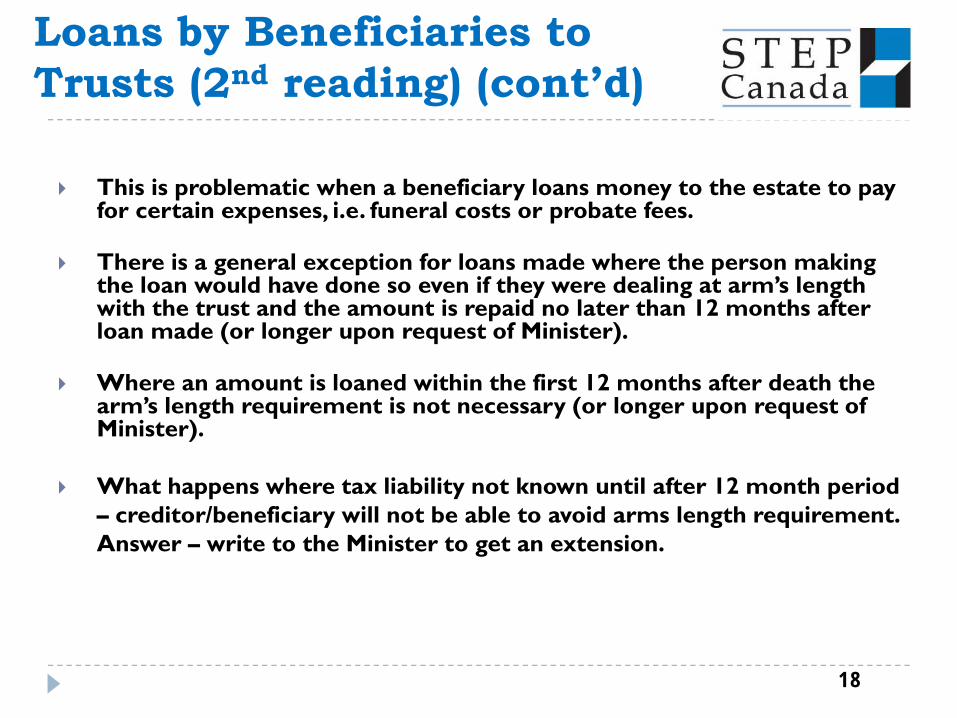

This is problematic when a beneficiary loans money to the estate to pay for certain expenses, i.e. funeral costs or probate fees.

There is a general exception for loans made where the person making the loan would have done so even if they were dealing at arm’s length with the trust and the amount is repaid no later than 12 months after loan made (or longer upon request of Minister).

Where an amount is loaned within the first 12 months after death the arm’s length requirement is not necessary (or longer upon request of Minister).

What happens where tax liability not known until after 12 month period – creditor/beneficiary will not be able to avoid arms length requirement. Answer – write to the Minister to get an extension.

Loans by Beneficiaries to Trusts (2nd reading) (cont’d)

18

Testamentary Spousal Trusts

A Testamentary Trust with the following tax benefits:

All capital assets transferred to trust on a tax deferred basis;

Disposition on death delayed until death of surviving spouse;

21 year disposition rule not applicable until death of spouse (if a 2nd generation trust exists that trust will be subject to 21 year deemed dispositions).

19

A Testamentary Spousal Trust is one that is:

Created by the taxpayer’s will;

Assets vested indefeasibly in trust within 36 months of testators death –question of fact – shareholder agreements may be issue.

Spouse and Trust need to be resident in Canada;

Spouse entitled to receive all of the income of the trust that arises prior to his/her death – note not annual requirement;

No person other than Spouse may receive or obtain use of any income or capital of the trust while spouse is alive – watch out for non-commercial loans and guarantees.

Testamentary Spousal Trusts (cont’d)

20

Tainted Testamentary Spousal Trusts

If the trust is tainted it may still be a normal testamentary trust.

A tainted trust may be untainted if the taint arises from a requirement to pay debts or other testamentary duties of the deceased’s estate (see subsection 70(7)).

Requirement to pay another beneficiary is a problem, but a disclaimer can cure.

21

Taxation of Testamentary Trust - Review Testamentary Trusts are taxed in the same manner as inter vivos trusts but pay tax at the graduated marginal rates.

Income paid or payable to a beneficiary is taxed in the beneficiary’s hands.

Capital gains and dividends can be flowed through to beneficiaries.

21 year disposition rules apply unless testamentary spousal trust.

22

Taxation of Testamentary Trust – Income Splitting Multiple trusts will, subject to certain conditions, be considered multiple taxpayers – multiple levels of marginal rate utilization.

Better to have 2 shareholders earn $75,000 than 1 earn $150,000 – but watch out for 2 trusts deemed to be one by the CRA (ss. 104(2))

What assets go into each trust will be a consideration.

Spousal trust should receive appreciated capital assets so as to defer capital gain taxation upon death of first spouse.

Other trusts can receive income producing assets.

Consider utilizing capital losses on death to facilitate a tax efficient transfer of capital assets to non-spousal beneficiaries or trusts.

23

Taxation of Testamentary Trust – Same Beneficiary Concerns

CRA view of class of beneficiary:

Members of the same family can be a class of beneficiaries, but CRA will look at facts as well, including:

whether will makes it clear intent to create separate trusts;

whether trusts have common beneficiaries;

have trustees kept assets of separate trusts segregated;

general conduct of trustees.

24

CRA notes it will examine:

Trust A – Child A and Spouse;

Trust B – Child B and Spouse;

Trust C – Child C and Spouse.

But likely would not examine

Trust A – Child A;

Trust B – Child B;

Trust C – Child C.

Taxation of Testamentary Trust –Same Beneficiary Concerns (cont’d)

25

Other Tax Considerations

Loss Carry Back Rules:

Losses accruing in the spousal trust cannot be carried back under s. 164(6) to the terminal year of the deceased.

Upon death of surviving spouse spousal trust does not need to be wound up –consider extending for a maximum of 3 years as losses can be carried back during this time.

Rules re: income and capital distributions during extension period to be drafted in trust.

Doc #3961853

26

The Legal, Tax and Administrative Aspects of Administering an Estate

Passing Of Accounts

Brian Cohen Borden Ladner Gervais LLP

December 10, 2008

27

Common Law Responsibility to Account

Trustees, executors, guardians etc. must keep a complete set of accurate accounts of the assets under such fiduciary’s care.

With reasonable notice, a beneficiary is entitled to inspect these accounts and the supporting documentation.

Fundamental obligation and fiduciaries can be removed from office, sued or liable for damages when accounts passed if breached.

ONTARIO BIASED - SORRY28

Common Law Duty -Legislated

Rule 74.16 - 74.18 of the Rules of Civil Procedureprovides estate trustees with the obligation to keep accurate records of the assets and transactions of the estate.

Duty covers keeping all supporting documentation –such as cheques, receipts and invoices.

Keep accurate records from the beginning to ensure easy to convert to court passing format at the end.

Estate accounting is not normal accounting.

29

When Do You Pass Accounts?

No legal requirement to pass accounts.

Trustee entitled to voluntarily pass accounts.

Trustee may be compelled to pass accounts.

Not necessary when quick distribution and beneficiaries all of age, mentally competent and in agreement with distribution plan and trustee compensation.

30

What is Passing Accounts?

Formal court proceeding.

Court asked to approve accounts submitted by fiduciary for a specified period of time.

Accounts must be in prescribed form (big headache to play catch up - tell clients to keep proper records from the get go – if possible).

If court approves the accounts, the judgment is the equivalent of a release to the estate trustee – but limited to the time period covered by the judgment.

31

Voluntary Passings

Ss. 23(1) of the Trustee Act provides a trustee with the authority to pass accounts in the Superior Court of Justice. Other provinces have similar legislation.

Trustee would seek to do this where:

The beneficiary is a minor or mentally incapacitated and cannot approve the estate trustee’s accounts and the compensation claimed by the estate trustee; and

Where the estate trustee cannot secure the consent of any one or more of the beneficiaries of the estate to the accounts and/or to the estate trustee’s proposed compensation.

Ongoing trusts and trustee wants surety as he or she proceeds – often pass every 3-5 years.

32

Compulsory Passing

Executor not required to pass accounts unless a person interested in the property of the deceased (s. 50 - Estates Act).

A person is interested in an estate where they have a financial interest in the estate and in that case, they may seek an order for assistance requiring a trustee to pass accounts (74.15 - Rules of Civil Procedure). A provision in a will that passings are not required does not remove the jurisdiction of the court to compel a passing.

If trustee does not comply with the successful order, a motion for contempt can be made.

33

Other Passing Issues and Notes

Where a personal representative is removed by court order, court will require a passing prior to the resumption of duties by a successor personal representative (unless consents of all parties obtained).

PGT may be required where there is a gift to a not-for-profit or charitable entity or purpose and in these situations, the PGT can compel a passing.

34

Where do You Pass Accounts?

In Ontario, back to the court that the original Certificate of Appointment was issued.

Court has jurisdiction to pass accounts even where Certificate of Appointment was never obtained.

When seeking to pass accounts, give notice to all contingent and vested beneficiaries as well as the PGT and OCL as required (or similar government body).

If someone disagrees with the accounts, they can object.

35

Form of Accounts

Following must be provided:Statement of Original Assets at beginning of periodStatement of Capital ReceiptsStatement of Capital DisbursementsStatement of InvestmentsStatement of Revenue ReceiptsStatement of Revenue DisbursementsStatement of Original Assets at end of PeriodStatement of Money and Assets on Hand at end of PeriodStatement of LiabilitiesStatement of Compensation

36

Unopposed Applications

Not necessary for the parties to attend if unopposed.

To get there, lawyer serves all parties and should be available to answer questions and prevent unnecessary objections.

Documents frequently requested are tax returns, appraisals, valuations, receipts etc.

Compensation should be agreed to during this time as well and then can go over the counter.

37

Opposed Applications

If objections filed and not resolved prior to hearing date, accounts will be passed before a judge – date initially in the Notice of Application to Pass.

Hearing will also be required if counsel seek increased costs.

Hearing will only look to issues in objections unless court orders otherwise.

Judge can permit a trial of an issue, if necessary and complex,

38

Judgment

Once have judgment – accounts are considered settled and they cannot be opened, corrected or challenged again except in cases of fraud, omission or mistake.

39

Trustee Compensation

S. 61 of the Trustee Act provides for compensation based on “fair and reasonable allowance for his care, pains and trouble, and his time expended in or about the estate”.

Compensation value not actually established in Ontario, rather there is a court accepted Tariff. OCA says look first to the usual percentages and tariffs and then the appropriateness of the result based upon five factors namely: (i) magnitude of the estate, (ii) the care and responsibility required, (iii) time spent, (iv) skill and ability applied, and (v) success of the administration.

40

Trustee Compensation(cont’d)

Only one compensation award so needs to be divided if more than one trustee. Court does not like to decide who gets how much but will do so if absolutely necessary.

If trust deed or Will provides for compensation, that governs (at least for the first trustee).

Compensation is attributed to the capital and revenue of the estate as applicable.

41

Usual Percentages –the Tariff

2.5% for capital receipts (i.e what comes in) and for capital disbursements (what goes out).

2.5% for revenue receipts and revenue disbursements.

Management Fee - 1/5 of 1% per annum on the average value of the estate (generally 1/3 charged to revenue and 2/3 to capital).

42

Compensation –Other IssuesWhether or not one can pre-take is an issue –specifically provide for it in Will.

Work done by a lawyer that should have been done by the trustee is deducted from the compensation award.

Other work, including legal, accounting etc. are to chargeable to the estate.

If very simple estate i.e. straight distribution and GICs only, compensation can be reduced from Tariff as well.

Doc #3963766

43

Final Return

The final T3 return must be filed and any balance owing must be paid no later than 90 days after the trust's wind-up date. Enter the wind-up date on page 1 of the T3 return.

For a testamentary trust, the tax year will end on the date of the final distribution of the assets. For an inter vivos trust, the trustee may want to file a final return before the end of the trust's tax year.

44

Clearance Certificiate

Trustees can be liable for any amount the trust owesA clearance certificate can be obtained from the CRA to certify that all amounts owing by the trust to CRA have been paid, or security has been accepted for the payment. Trustees should obtain a clearance certificate before the final distribution of trust property.

Most of the trust property may be distributed prior to obtaining a clearance certificate; however, sufficient property should be retained in the trust to cover potential liabilities.

45

Clearance Certificiate

Form TX19 – Asking for a Clearance Certificate Submitted to CRA after the notices of assessment have been received for all the returns filed and all amounts owing are paid or securedTo be included:

a copy of the trust document; a statement showing the properties and distribution plan including the date chosen for the distribution of properties, and a list of the recipients of each of the properties

It can take a year or more to be processed by CRAAssets are considered to be distributed on the date stated in Form TX19

46