tritech group limited initiating coverage - nra capital - tritech - initiating coverage.pdf ·...

TRANSCRIPT

ahR 82Des

Source: Bloomberg

Tritech Group Limited

Initiating Coverage

Building on Strong Foundations We initiate coverage on Tritech with a BUY rating and fair value of $0.430 based on blended 13.0x FY3/11F P/E. This is a 32% upside from its current share price of $0.325. We believe that revenue growth for the coming FY will be modest but we expect to see a substantial growth when its water business comes on board. We estimate this to come in from FY3/11. Fundamentally sound company with good growth potential. 2009 was a year of ups and downs with the STI reaching a low of 1,457 pts and subsequently rebounding by 99% to close at 2,898 pts at year end. In 2010, we would expect to see a more modest gain in most stocks as the easy money has been made. In our view, investors need to be more discerning in identifying fundamentally sound companies with good growth potentials. We are convinced Tritech belongs to this group of stocks. Differentiating as Specialists. Tritech seeks to differentiate itself as the specialist in each of the engineering fields that it is engaged in. This allows it to command higher margins by taking on high value jobs. Public sector projects to drive demand. Demand for civil engineering services remains healthy with streams of public projects in the pipeline. According to BCA, annual construction demand for 2010-2011 is expected to reach $20.0-27.0bil with $15.0-17.0bil coming from the public sector. This represents growth of 11-12.5%. Something else is developing. Although it is a Catalist listed company now with market capitalisation of only $77mil, we see potential for the company to grow significantly over the next 3 years. The growth will come from its water business which it is developing now. Propelling through technology advances. We urge investors not to underestimate how technological advancement can leapfrog a company to new heights. With a confluence of several engineering experts, we see the potential for its proprietary water technologies to propel Tritech to greatness once it can capitalise on its technologies. Key Financial Data

FYE 31 March FY08 FY09 FY10F FY11F FY12F Sales 31.3 41.3 41.9 51.6 62.2 Gross Profit 12.7 16.9 16.4 19.0 22.0 Net Profit 7.3 7.0 7.2 7.9 8.8 EPS (cents) 4.37 4.04 3.27 3.34 3.72 EPS growth (%) 251.9% -7.5% -19.1% 2.3% 11.4% PER 7.4 8.0 9.9 9.7 8.7 DPS (cents) 0.0 0.8 0.5 0.5 0.5 Div Yield (%) 0.0% 2.6% 1.7% 1.5% 1.5%

Source: Company, NRA estimates

BUY

Current Price S$0.325

15th

January 2010 Fair Value S$0.430 Yeak Chee Keong, CFA

65-6236-6884 [email protected] Jacky Lee

65-6236-6887 [email protected]

Historical Chart

Source: Bloomberg

Stock Statistics

Market Cap S$76.88m 52-HI S$0.355 52-LOW S$0.070 Avg Vol (1 yr) 954,615 Shares Outstanding

236.583m

Free Float 75.58m

Key Indicators

ROE 35.2% ROA 21.4% P/BK 2.46x Gearing Net cash

Major Shareholders

Tritech Int’l 67.63% Lim Yeok Hwa 0.21% Yong Kwet Yew 0.21%

page 1 NRA Capital Pte Ltd www.nracapital.com

page 2 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

Tritech Group Limited (“Tritech”) is a specialist in Geotechnical, Ground and Structural Engineering. It serves industries ranging from oil and gas, infrastructure, integrated resorts, residential and commercial markets. In addition, Tritech is working on the commercialization of its water treatment membrane technologies. Tritech has been involved in Singapore’s engineering landscape since 1999 and was listed on the Singapore Exchange’s Catalist Board on 20 August 2008. Currently, Tritech generates the bulk of its revenue from Singapore. Business is segmented into 2 main engineering divisions. It is also growing a new business division in water technology: (1) Specialist Engineering Division

Geotechnical instrumentation & monitoring services

Geotechnical and geological site explorations, analysis & testing

Design, consultancy & project management services in infrastructure, environmental, geotechnical and civil engineering works and projects

(2) Ground and Structural Engineering Division

Soil improvements by jet grouting

Design & installation of soil nails, ground anchors and micropiles

Design & build services for retaining wall systems used in slope cutting and stabilisation & basement evacuation projects

Source: Company

Company Profile

Company Structure

page 3 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

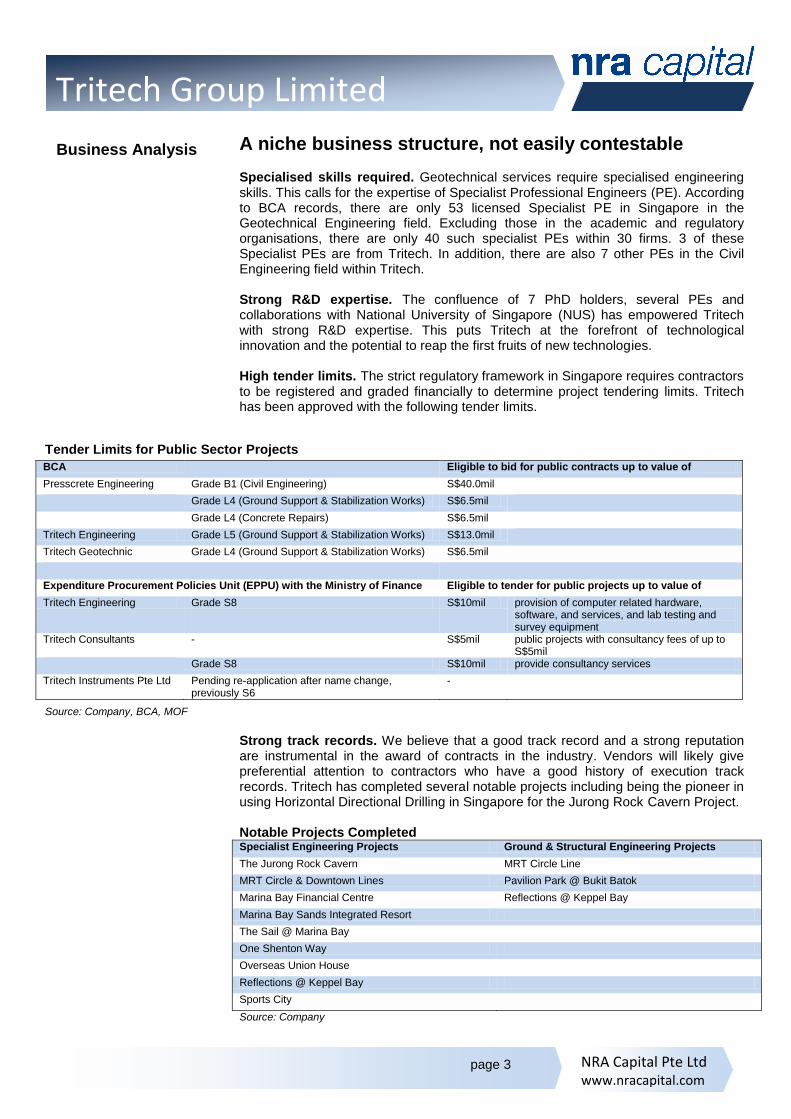

A niche business structure, not easily contestable Specialised skills required. Geotechnical services require specialised engineering skills. This calls for the expertise of Specialist Professional Engineers (PE). According to BCA records, there are only 53 licensed Specialist PE in Singapore in the Geotechnical Engineering field. Excluding those in the academic and regulatory organisations, there are only 40 such specialist PEs within 30 firms. 3 of these Specialist PEs are from Tritech. In addition, there are also 7 other PEs in the Civil Engineering field within Tritech. Strong R&D expertise. The confluence of 7 PhD holders, several PEs and collaborations with National University of Singapore (NUS) has empowered Tritech with strong R&D expertise. This puts Tritech at the forefront of technological innovation and the potential to reap the first fruits of new technologies. High tender limits. The strict regulatory framework in Singapore requires contractors to be registered and graded financially to determine project tendering limits. Tritech has been approved with the following tender limits.

BCA Eligible to bid for public contracts up to value of

Presscrete Engineering Grade B1 (Civil Engineering) S$40.0mil

Grade L4 (Ground Support & Stabilization Works) S$6.5mil

Grade L4 (Concrete Repairs) S$6.5mil

Tritech Engineering Grade L5 (Ground Support & Stabilization Works) S$13.0mil

Tritech Geotechnic Grade L4 (Ground Support & Stabilization Works) S$6.5mil

Expenditure Procurement Policies Unit (EPPU) with the Ministry of Finance Eligible to tender for public projects up to value of

Tritech Engineering Grade S8 S$10mil provision of computer related hardware, software, and services, and lab testing and survey equipment

Tritech Consultants - S$5mil public projects with consultancy fees of up to S$5mil

Grade S8 S$10mil provide consultancy services

Tritech Instruments Pte Ltd Pending re-application after name change, previously S6

-

Strong track records. We believe that a good track record and a strong reputation are instrumental in the award of contracts in the industry. Vendors will likely give preferential attention to contractors who have a good history of execution track records. Tritech has completed several notable projects including being the pioneer in using Horizontal Directional Drilling in Singapore for the Jurong Rock Cavern Project. Notable Projects Completed Specialist Engineering Projects Ground & Structural Engineering Projects

The Jurong Rock Cavern MRT Circle Line

MRT Circle & Downtown Lines Pavilion Park @ Bukit Batok

Marina Bay Financial Centre Reflections @ Keppel Bay

Marina Bay Sands Integrated Resort

The Sail @ Marina Bay

One Shenton Way

Overseas Union House

Reflections @ Keppel Bay

Sports City

Source: Company

Business Analysis

Source: Company, BCA, MOF

Tender Limits for Public Sector Projects

page 4 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

Leading player. Most of Tritech’s direct competitors are not listed companies. We understand from management that in comparison with local companies, Tritech has been awarded with one of the most number of projects related to the construction of MRT lines as most local companies do not have the specialised skills required. Most other firms involved in the more technical aspects of the construction usually go to the foreign experts. Playing a role in every stage. Tritech’s host of subsidiaries has a role to play in almost every stage of a civil engineering project. Tritech’s roles in different phase of a project

Source: Company

A strong management team. Our impression of management is that they have been conservative in their spending and we feel comforted by the careful risk assessments that management considers before making its business decisions. We also like the hands-on approach that management has on its businesses.

Dr Jeffrey Wang Managing Director Dr Wang is the founder of the group and is in charge of overall operation and business development. He was a senior engineer in an engineering consultancy firm from 1991 to 1996, and a chief engineer in an listed engineering company from 1996 to 2000. He has more than 19 years experience in geotechnical engineering and has published many technical papers in geotechnical engineering. Dr Wang is a Fellow member of the Chartered Management Institution (CMI), UK and is a registered Professional Engineer. He holds a PhD from the Chinese Academy of Sciences (awarded with the minister Award of Chinese Academy of Sciences in recognition of outstanding performance) and a PhD from NUS. He was awarded with the Best Entrepreneur Award for Faculty of Engineering by NUS in Sept 2007.

Dr Cai Jungang Executive Director Dr Cai was is in charge of supervision of Tritech's Specialist Engineering Services. He was previously a research scholar and research fellow in NTU. Dr Cai has 15 years of R&D and engineering experience, published more than 100 technical books and journal papers and was involved in many underground facility projects in Singapore. He is a senior member of the Institute of Engineers Singapore (MIES). He holds a MEng and PhD from NTU.

Dr Loh Chang Kaan Executive Director Dr Loh is in charge of supervision of ground and structural engineering services. Previously, he was a research engineer with NUS from 1994 to 1999. Following that he was an executive engineer with a specialist ground engineering firm in charge of geotechnical projects and a project manager for various foundation projects. He is a registered professional engineering in Singapore and Malaysia. Dr Loh holds a MEng and PhD from NUS

Key Management Profiles

Source: Company

page 5 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

Opportunities in the Water Industry Increase in investments in water treatment industry. In its IPO, $0.90mil out of the total of $6.0mil gross proceeds raised was allocated to the commercialisation of its water treatment technologies. This amount has proved to be insufficient as Tritech proceeded to allocate the proceeds intended for the purpose of overseas expansion to the water treatment segment. It also issued placement shares to raise about $6.7mil of additional net proceeds to be utilised for water treatment technologies. The amount of capital commitment allocated to growing this business segment demonstrated the confidence and commitment that management has towards the water treatment industry. Key Milestones in Water Treatment Segment

4-Feb-04 Incorporated Tritech Water to focus on R&D in water treatment technologies

13-Jul-05 Filed an international patent for its UnitCell Desalination System (UDS)

10-Aug-07 Entered into agreement with Prof Wang Yusheng of Shandong Lubao Water Resource Development Institute for development of SPNC RO membrane and the design & manufacture of SPD for desalination of sea water using certain patents owned by Prof Wang

Feb-08 Provided with grant by SPRING Singapore under the Capability Development Scheme (Technology Innovation) - Projects scheme for development & commercialisation of a medium size solar powered seawater desalination system with production capacity of ~20 tons freshwater/day

21-Nov-08 Signed MOU with NUS to collaborate in research and promote commercialisation of technologies in areas of engineering, environment, water & material science

9-Jun-09 Acquired property at 8A Admiralty Street, #06-28 Food Xchange@Admiralty for R&D work and production facilities for water treatment technologies

Jun-09 Provided with grant by SPRING Singapore under the Capability Development Scheme (Technology Innovation) - Projects scheme for the development of SPNC RO membrane

19-Oct-09 Issued placement shares raising ~$6.7m net proceeds to be used for expansion of its water-related business in the PRC

28-Oct-09 Entered into agreement to acquire agricultural land (110 mu ~73,370sqm) in the Economic Development Zone of Jiaonan City, Qingdao, PRC, to set up a production facility to develop & manufacture different types of membranes for use in water treatment

Source: Company, NRA Capital

Several water technologies. Tritech already has a host of water technologies that it can boast of. Its investments in the water sector is also partly subsidised by research and development grants given by organisations such as SPRING Singapore and A*Star. Tritech’s water technologies UnitCell Desalination System (UDS)

high Productivity

no need for pressure vessel

cost efficient

Diesel and/or Solar Powered Small to Medium Scale Desalinator (DPD/SPD)

production capacities range from 1-500 tons/day

Mineralised Bottled Water Factory supplies mineralized drinking water & dispenser

Super Low Pressure Polymer and Nano Compounded (SPNC) RO Membrane

more energy efficient

less requirement for intake

better mechanical properties

high production rate

Design and build works for waste water treatment plants

Capable to design and build plants of any size

Real time water quality monitoring Aims to be a key and leading player in this niche industry

Source: Company

page 6 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

We are excited but cautious. We are excited by these developments but also exercise caution at the same time. Our favorable outlook on the company hinges on our belief that Tritech would be successful in commercialising its technologies. However we also exercise caution as Tritech has not established its reputation in this industry which is a different field from its traditional civil engineering works. Furthermore, competition in this industry is intense with several big-named companies such as Hyflux, Keppel Corp and SembCorp Industries who already have a strong foothold in the industry. Tritech’s competitive advantage comes in its proprietary technologies and R&D capabilities.

page 7 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

Dependent on the Singapore construction industry. Tritech currently derives almost all of its revenue from projects in Singapore. While we believe that the demand for construction projects in the next 2 years appears to be sustainable, the construction industry does experience fluctuations and cyclicality. A dearth of available projects may affect its revenue. If its water treatment venture proves successful, it will help to mitigate its dependency on the Singapore construction industry. However, that in itself will expose it to another set of risks. Dependent on ability to secure projects. The eligibility to bid for public sector projects requires engineering firms to be properly licensed and to meet certain minimum requirements. Its reputation and ability to execute projects safely and efficiently is also important. In the event that Tritech does not meet these requirements or suffers damage to its reputation, it could severely affect its potential in continuing to be awarded with contracts. Human and intellectual resources. We believe that a large part of its business is reliant on the intellectual knowledge and experience of its engineers. This is especially so of its specialist engineering works. These specialized knowledge may not be easily retained in the company if its key people were to leave the company. The lack of such professionals may hinder Tritech in securing related projects. Water treatment segment is untested. Tritech is putting in a substantial amount of investment in the water treatment segment. Management appears confident in the prospects of the industry. However, we exercise caution on the economic potential because this is different from the civil engineering services it has traditionally been engaging in. Although Tritech has been working on water treatment research since 2003, it has yet to prove itself in the execution of manufacturing and production. We do believe that rewards could be sizable but the risk is present. Commercial viability has also not been proven.

Risks

page 8 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

Public sector projects to drive demand Demand for civil engineering services remains healthy with streams of public projects in the pipeline. These include developments to the MRT systems, expressways and other public infrastructure projects. According to BCA, annual construction demand for 2010-2011 is expected to reach $20.0-27.0bil with $15.0-17.0bil coming from the public sector. Comparatively, average annual construction demand was approximately $13-15bil between 1998-2006. Construction demand reached a peak of $34.6bil in 2008, helped by an influx of private development projects which accounted for $20.1bil. In 2009, demand is expected to reach $18-24bil. Therefore there is an expected growth of 11-12.5% in 2010. Notable Public Sector Projects in the pipeline Public Projects Cost Length No. of

Stations Expected Completion

MRT System

Circle Line $6.7bil 33.3 km 29 From 2010

Downtown Line - 40 km 33 2016

East-West Line extension - 14 km - 2015

North-South Line extension - 1 km - 2015

Thomson Line - 27 km 18 2018

Eastern Region Line - 21 km 12 2020

Expressways -

Marina Coastal Expressway $4.1bil 5 Km - 2013

New Sentosa Gateway Tunnel - - - -

Future MRT system line

Industry Outlook

Source: Company

Source: LTA

page 9 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

Stringent safety rules & increasing complexities augurs well with specialists like Tritech. Regulations on building and construction projects have been tougher since unfortunate events like the Nicoll Highway incidents. More stringent checks and monitoring are required and this augurs well for specialists like Tritech. Main contractors for the projects were required to engage independent consultants to carry out checks and monitoring. There is also an increasing need for specialists as civil engineering gets more complex technically. Increased competition as number of private sector projects decline. Private sector projects demand is not expected to be strong in 2010. A potential consequence is the proliferation of bids for public sector projects. We believe margins will be subjected to contraction pressure as competition increases in public sector projects.

Opportunities in the PRC Infrastructure Market Management also shared their insights on opportunities in the PRC market. With huge infrastructure spending rolling out, civil engineering activities are bustling in the PRC. These include public transportation systems such as the MRT. Although there are many local companies with building capabilities, there is a shortage of specialist engineers in the country. With its growing presence in the PRC, Tritech is vying for a share of the pie.

Banking on the Water treatment Industry Desalination is now a viable option. Previously considered to be an overly costly option, advancement in technologies has allowed desalination to become a viable solution to water needs. Water scarcity, pollution, increasing population and economic development have increased the demand for water resources. According to “Desalination Markets 2005 – 2015”, a report published by Media Analytics Ltd, the desalination market is expected to generate US$95bil spending between 2005 and 2015. Out of this, it is projected US$48bil will be spent on new desalination capacities. China a top market for desalination. China’s National Sea Water Utilization Special Program forecasted China’s need for desalinated water to triple over the next 10 years. The PRC government expects desalinated water demand to reach one million tons a day in 2010 and to grow to 3 million tons a day by 2010. Global Water Intelligence also determined China to be one of the top 10 desalination growth markets between 2008- 2016. We believe that there is huge potential in the PRC.

page 10 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

Top 10 Desal Growth Markets 2008 - 2016 Existing competition. The water industry is a big market and there have already been many big established players in the market. A lot of these players however are plant builders and suppliers and may not have their own technologies. We see opportunities for Tritech to be a supplier of technologies to these players while also competing for plant design and building projects at the same time.

Source: 2009 Desalination Market Forecast, GWI

Top 20 Plant Suppliers 2005 - 2008 m3/d

1 Veolia WS&T 3,467,658

2 Fisia Italimpianti 1,746,380

3 Doosan Hl 1,459,120

4 GE Water 889,256

5 Befesa Agua 836,448

6 Cobca/Tedagua 743,024

7 Hyflux 768,808

8 Degremont 650,980

9 IDE 633,208

10 Cadagua 615,024

11 Sadyt 501,600

12 Acciona Agua 497,200

13 Mistubishi Hl 450,990

14 Inima 446,000

15 Aqualia 442,700

16 Biwater AEWT 429,890

17 Aqualyng 256,475

18 Romymar 240,000

19 SembCorp 228,000

20 Aquatech 225,540

Source: Global Water Intelligence

page 11 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

Orderbook. Outstanding orderbook stood at $59mil of which $53mil is from public projects as at 9 Nov 2009. We expect Tritech to continue to secure orders from the public sector as the government agencies launch the tenders for the various public projects.

Est. Est. Contract Contract

Announced Contract Contract Duration Value Awarded

Date Start End (months) (S$mil) Awarded to By Contract Description

26-Aug-08 26-Aug-08 May-09 9 1.78 Tritech Consultants Pte Ltd

- Underground Rock Cavern (URC) usage feasibility study

29-Oct-08 30-Oct-08 Dec-13 62 6.96 Tritech Consultants Pte Ltd

LTA Qualified Person (Supervision) Services for Contract 902 Design, Construction and Completion of Promenade Station incl. Associated Tunnels for Downtown Line Stage 1

31-Oct-08 31-Oct-08 Apr-11 30 3.48 Tritech Consultants Pte Ltd

LTA Qualified Person (Supervision) Services for Contract 1590

1-Dec-08 1-Dec-08 Sep-13 57 3.34 Tritech Engineering & Testing Pte Ltd

LTA Supply, Installation and Monitoring of Instruments for Marina Coastal Expressways - Contracts 483 & 485

1-Dec-08 1-Dec-08 Jun-13 54 4.50 Tritech Engineering & Testing Pte Ltd

LTA Supply, Installation and Monitoring of Instruments for Marina Coastal Expressways - Contracts 486 & 487

3-Jul-09 15-Jul-09 Sep-15 74 13.74 Tritech Consultants Pte Ltd

LTA Supervision of Contract 921, Design & Construction of Stations & Tunnels at Rocher and Little India for Downtown Line Stage 2

1-Sep-09 31-Aug-09 Feb-16 79 4.50 Tritech Engineering & Testing Pte Ltd

LTA Supply, Installation and Monitoring of Instruments for Downtown Line Stage 2 - Contract 921

5-Nov-09 18-Nov-09 Jul-11 20 5.86 Presscrete Engineering Pte Ltd

PUB Sewer Extention in Marina Reservoir Catchment Extention and Changi Coast Areas - Contract 1

44.16

Differentiating as Specialists. Tritech seeks to differentiate itself as the specialist in each of the engineering fields that it is engaged in. This allows it to command a high margin by taking on high value jobs. Water treatment potential. Tritech has completed its first trial test on site of its small to medium size desalinator. It has also developed its own proprietary RO membrane. Tritech claims that its technologies have the potential to reduce the cost of desalination significantly. It has already acquired land in the PRC to set up a production facility for its RO membranes to commercialise its technologies. The size of this plant which sits on a land area of 73,370sqm is not small. According to management guidance, it could take up to 2 years for the plant to be fully operational. Companies already in the water-related business generate gross margins in the range of 25%. With proprietary products and patents, we believe that Tritech could command a higher margin of as much as 30% in the initial stages. Market strategies. Tritech’s areas of focus in growing its water treatment business will be in the following:

1) Manufacture and supply of RO membrane 2) Manufacture and supply of SPD/DPD series of products with Tritech brand 3) Design & build of Waste Water Treatment Plants for Industrial Parks 4) Supply mineralised drinking water & dispenser 5) Provide consultancy services for the industry 6) Become a key player for water quality monitoring

Company Outlook

Annouced Contracts

Source: Company

page 12 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

High value services draws superior margins Strong growth in revenue and profits. Between FY06 and FY09, revenue grew at a CAGR of 77.3% as the construction cycle peaked in 2008. However we believe that growth would be more subdued in FY3/10 and FY3/11. Future growth potential could also come from its water treatment segment. Superior profit margins. Compared to other civil engineering firms, Tritech generates margins which many could not match up to. Unlike traditional construction companies, Tritech do not have to worry about raw material costs such as concrete. Going forward, we expect margin to suffer from compression pressure due to increased competition in the public sector projects. Gross Margins of Civil Engineering related companies

FYE FY05 FY06 FY07 FY08 FY09

Tritech Group Ltd Mar - 57.84 37.27 40.62 40.87

Hock Lian Seng Holdings Ltd Dec - 3.14 16.51 11.64 -

Chip Eng Seng Corp Ltd Dec 10.61 7.65 0.32 3.98 -

CSC Holdings Ltd Mar 13.95 13.04 15.44 20.21 16.52

Hiap Hoe Ltd Dec 7.61 33.44 32.88 44.37 -

Wee Hur Holdings Ltd Dec 10.77 8.35 13.66 12.14 -

Lian Beng Group Ltd May 6.07 6.50 7.61 15.00 11.84

Koh Brothers Group Ltd Dec 10.10 9.36 10.72 12.42 -

OKP Holdings Ltd Dec 5.97 14.26 17.52 20.94 -

Lum Chang Holdings Ltd Jun 1.23 4.23 9.87 7.36 11.32

BBR Holdings Ltd Dec 6.71 10.52 7.06 6.11 -

PSL Holdings Ltd Dec 14.74 24.37 24.41 28.10 -

Source: Bloomberg, NRA Capital

Healthy balance sheet & cashflows. Balance sheet is strong with current ratio of 3.2x and net cash of $7.7mil as at 1H3/10. Its cash position has been growing with positive operating cash flow generated over the past years. Issues of new shares also add to the cash position. Its debt position is also relatively low. However, we foresee the development of its water related business may start to drain its balance sheet. Intended capex for the next 2 years includes the $6.7mil net proceeds raised from the recent placement. Tritech also suggested that it may fund further requirements from its existing funds, loans or other sources.

Financials

Source: Company, NRA Capital

page 13 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

Dupont Analysis FY06 FY07 FY08 FY09

Net Margin 20.8% 10.6% 23.2% 17.0%

Total Asset Turnover 1.7 1.3 1.3 1.3

ROA 35.2% 13.4% 29.3% 21.4%

Financial Leverage 1.7 2.4 2.3 1.6

ROE 58.2% 32.1% 68.8% 35.2%

Source: Company, NRA Capital

Tritech generates a relatively high ROE, which has been fluctuating mainly due to 2 factors, decrease in net profit margin and also decrease in financial leverage resulting from the increase in equity base. We expect ROE to decline with further increase in asset and equity from the issue of placement shares. Ratios FY08 FY09 FY10F FY11F FY12F

Growth

Gross Profit Growth 75.0% 32.9% -3.2% 16.3% 15.5% EBITDA Growth 340.7% -7.7% -8.0% 8.5% 6.1% EBIT Growth 185.3% -1.2% -3.1% 9.3% 10.1% EBT Growth 225.1% -0.6% 0.7% 12.1% 11.2% Net Profit Growth 251.5% -4.0% 2.7% 10.4% 11.4% Liquidity

Working Capital 7,271 18,645 31,245 33,576 42,344 Current Ratio 1.6 3.0 4.4 4.1 4.3

Quick Ratio 1.6 2.9 4.3 4.0 4.2

Efficiency

Inventory Days 5.6 5.3 6.6 6.3 6.3

Receivables Days 45.5 27.7 29.6 27.2 27.4

Payable Days 156.5 118.6 90.1 80.4 81.4

Cash Conversion Cycle -105.4 -85.6 -54.0 -46.9 -47.6

Fixed Asset Turnover 4.0 4.4 3.5 3.2 4.1

Total Asset Turnover 1.1 1.1 0.8 0.8 0.9

Profitability

Adj. Gross Margin 40.6% 40.9% 39.0% 36.9% 35.3%

EBITDA Margin 23.1% 16.1% 14.6% 12.9% 11.3%

EBIT Margin 28.2% 21.1% 20.1% 17.9% 16.3%

Net Margin 23.2% 17.0% 17.1% 15.3% 14.2%

Total Asset Turnover 1.3 1.3 0.9 0.9 0.9

ROA 29.3% 21.4% 15.8% 13.9% 13.4%

Financial Leverage 2.3 1.6 1.4 1.3 1.3

ROE 68.8% 35.2% 21.5% 18.1% 17.3%

Leverage

Total Debt/Equity 0.18 0.11 0.09 0.08 0.07

Long-Term Debt/Equity 0.08 0.06 0.05 0.04 0.04

Net Debt/Equity -0.16 -0.29 -0.47 -0.40 -0.46

Coverage

EBIT/Interest Expense 33.8 38.2 56.3 86.3 95.1

Source: Company, NRA Capital

page 14 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

Per Share Data FY08 FY09 FY10F FY11F FY12F

EPS 0.044 0.040 0.033 0.033 0.037 Diluted EPS 0.044 0.040 0.030 0.033 0.037 BVPS 0.069 0.130 0.171 0.199 0.231 P/E 7.4 8.0 9.9 9.7 8.7 P/B 4.7 2.5 1.9 1.6 1.4 P/S 1.7 1.4 1.7 1.5 1.2 P/FCF 7.7 23.2 10.6 68.3 10.5 EV/EBITDA 9.6 10.4 11.3 10.4 9.8 DPS 0.000 0.008 0.005 0.005 0.005 D/P 0.000 0.026 0.017 0.015 0.015

Source: Company, NRA Capital

page 15 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

We initiate coverage on Tritech with a BUY rating and fair value of $0.430 based on blended 13.0x FY3/11F P/E. This is a 32% upside from its current share price of $0.325. We believe that revenue growth for the coming FY will be modest but we expect to see a substantial growth when its water business comes on board. We estimate this to come in from FY3/11. Tritech’s share price has increased 10% YTD. This is despite the dilution which resulted from the issue of 35,000,000 placement share in Oct 2009. Based on our FY3/11F EPS estimates of $0.033, it is trading at 9.7x P/E. In comparison with other civil engineering stocks which are trading at a forward P/E of 7.1x, valuation appears to be rich. However, we think that making the comparison with other civil engineering peers may be unfair given the specialist nature of Tritech’s work. Other specialist engineering firms in other fields trade at an average P/E of 12.2x. In addition, given its superior margins, ROE and strong balance sheet, we believe that the stock should trade at a premium over its counterparts. We value Tritech’s engineering business at 12.0x P/E. Further, with the water business coming up, we think that Tritech should be accorded with a higher price multiple. However contribution from its water business will not be substantial until 2011. We estimate earnings for this segment to make up between 10-17% of total revenue in FY3/11 and FY3/12 and increasing to up to 30-40% in later years. Our valuation multiple of 13.0x is based on blended P/E of its engineering business (90%/12.0x P/E) and water business (10% 22.0x P/E).

Valuation &

Recommendation

page 16 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

Mkt Cap Price Hist Current Fwd P/S P/B ROE GPM NPM D/E Net D/E Tritech Group Ltd/Singapore 78.1 0.33 8.2 - - 1.4 2.5 35.2 40.9 17.0 10.8 -24.2

Specialist Engineering Peers

Advanced Holdings Ltd 97.8 0.315 12.5 13.1 16.6 1.1 1.4 11.3 26.1 9.1 0.0 -76.8

Technics Oil & Gas Ltd 77.9 0.545 12.7 7.8 7.8 0.6 2.8 21.9 22.0 4.7 110.5 44.2

Average 87.9 0.4 12.6 10.5 12.2 0.9 2.1 16.6 24.1 6.9 55.3 (16.3)

Civil Engineering Peers

Hock Lian Seng Holdings Ltd 163.2 0.32 8.2 - - 0.7 3.8 60.2 11.6 8.0 0.0 -152.4

Chip Eng Seng Corp Ltd 257.0 0.385 4.6 - - 0.7 1.1 25.4 4.0 12.4 100.4 74.5

CSC Holdings Ltd 214.6 0.175 7.6 8.8 6.5 0.6 1.2 27.6 16.5 7.1 59.9 39.9

Hiap Hoe Ltd 214.5 0.565 8.3 - - 2.2 1.3 6.5 44.4 27.9 261.2 253.7

Wee Hur Holdings Ltd 202.3 0.63 24.0 - - 1.5 5.1 30.1 12.1 6.3 0.0 -59.3

Lian Beng Group Ltd 169.5 0.32 8.3 - - 0.5 1.3 14.8 11.8 5.5 98.0 68.9

Koh Brothers Group Ltd 124.7 0.26 1.0 10.4 7.4 0.4 0.8 20.2 12.4 12.8 198.9 186.5

OKP Holdings Ltd 121.2 0.49 11.6 8.9 7.7 1.1 2.7 25.6 20.9 9.3 10.4 -63.3

Lum Chang Holdings Ltd 120.8 0.32 7.0 - - 0.5 0.9 9.2 11.3 4.9 21.5 -14.0

BBR Holdings Ltd 92.5 0.06 12.7 8.6 6.7 0.4 1.6 7.9 6.1 1.4 141.1 84.4

PSL Holdings Ltd 93.8 0.455 7.3 - - 1.2 2.9 55.6 28.1 15.7 51.5 10.9

Average 161.3 0.4 9.1 9.2 7.1 0.9 2.1 25.7 16.3 10.1 85.7 39.1

Water Peers

Hyflux Ltd 1,866.9 3.53 29.7 25.6 22.9 3.5 5.5 22.0 - 10.7 86.8 54.4

Dayen Environmental Ltd 26.1 0.085 - - - 0.5 1.5 -28.4 5.2 -15.6 0.0 -33.6

Sinomem Technology Ltd 299.4 0.585 33.6 12.4 9.9 2.4 1.2 1.4 26.5 2.7 25.7 -5.7

Asia Environment Holdings Ltd 137.0 0.32 10.4 46.3 37.5 1.6 0.8 8.4 34.8 15.0 48.1 33.3

United Envirotech Ltd 144.2 0.33 24.2 27.5 25.4 3.6 1.5 4.9 - 9.3 28.3 4.8

Asia Water Technology Ltd - - - - - - - -4.6 14.9 -4.5 170.7 126.2

Sino-Environment Tech Grp Ltd - - - - - - - -5.0 38.2 -5.8 84.1 -7.5

Epure International Ltd 1,109.4 0.86 20.8 18.7 16.6 4.4 3.7 18.8 33.3 22.6 29.9 -29.1

Average 597.2 0.952 23.7 26.1 22.5 2.7 2.4 2.2 25.5 4.3 59.2 17.9

Source: Bloomberg, NRA Capital

Peer Comparison

page 17 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

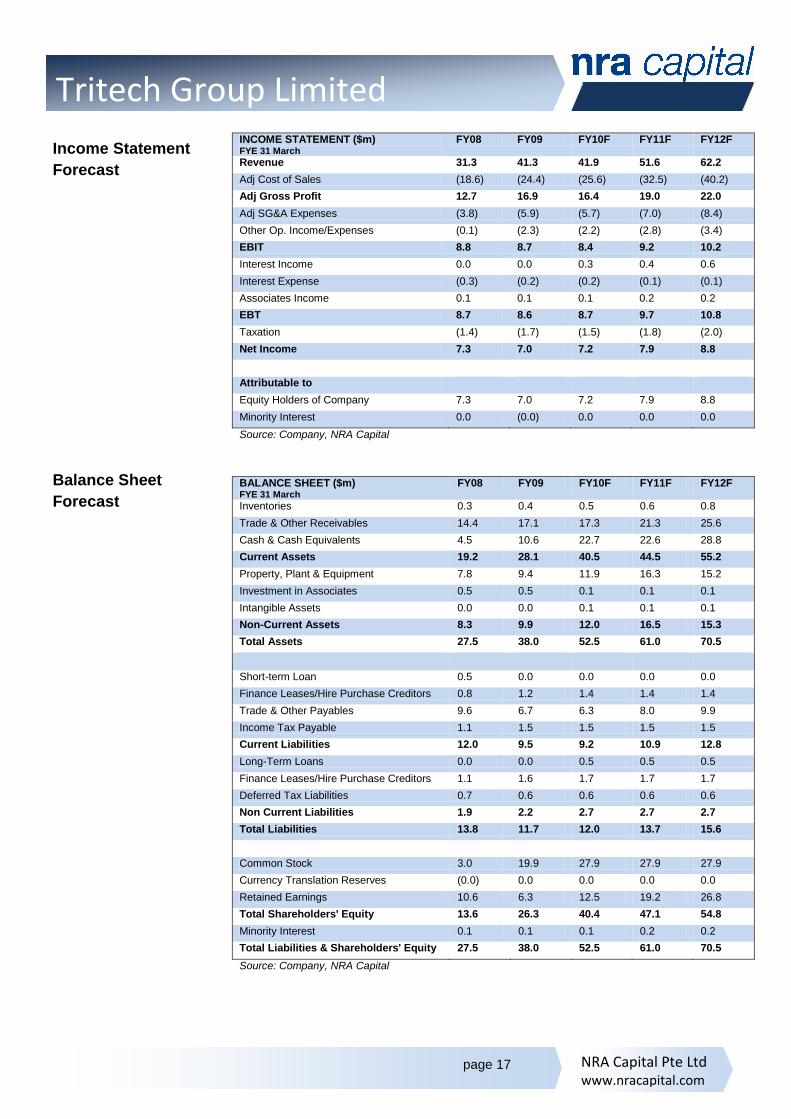

INCOME STATEMENT ($m) FYE 31 March

FY08 FY09 FY10F FY11F FY12F

Revenue 31.3 41.3 41.9 51.6 62.2

Adj Cost of Sales (18.6) (24.4) (25.6) (32.5) (40.2)

Adj Gross Profit 12.7 16.9 16.4 19.0 22.0

Adj SG&A Expenses (3.8) (5.9) (5.7) (7.0) (8.4)

Other Op. Income/Expenses (0.1) (2.3) (2.2) (2.8) (3.4)

EBIT 8.8 8.7 8.4 9.2 10.2

Interest Income 0.0 0.0 0.3 0.4 0.6

Interest Expense (0.3) (0.2) (0.2) (0.1) (0.1)

Associates Income 0.1 0.1 0.1 0.2 0.2

EBT 8.7 8.6 8.7 9.7 10.8

Taxation (1.4) (1.7) (1.5) (1.8) (2.0)

Net Income 7.3 7.0 7.2 7.9 8.8

Attributable to

Equity Holders of Company 7.3 7.0 7.2 7.9 8.8

Minority Interest 0.0 (0.0) 0.0 0.0 0.0

Source: Company, NRA Capital

BALANCE SHEET ($m) FYE 31 March

FY08 FY09 FY10F FY11F FY12F

Inventories 0.3 0.4 0.5 0.6 0.8

Trade & Other Receivables 14.4 17.1 17.3 21.3 25.6

Cash & Cash Equivalents 4.5 10.6 22.7 22.6 28.8

Current Assets 19.2 28.1 40.5 44.5 55.2

Property, Plant & Equipment 7.8 9.4 11.9 16.3 15.2

Investment in Associates 0.5 0.5 0.1 0.1 0.1

Intangible Assets 0.0 0.0 0.1 0.1 0.1

Non-Current Assets 8.3 9.9 12.0 16.5 15.3

Total Assets 27.5 38.0 52.5 61.0 70.5

Short-term Loan 0.5 0.0 0.0 0.0 0.0

Finance Leases/Hire Purchase Creditors 0.8 1.2 1.4 1.4 1.4

Trade & Other Payables 9.6 6.7 6.3 8.0 9.9

Income Tax Payable 1.1 1.5 1.5 1.5 1.5

Current Liabilities 12.0 9.5 9.2 10.9 12.8

Long-Term Loans 0.0 0.0 0.5 0.5 0.5

Finance Leases/Hire Purchase Creditors 1.1 1.6 1.7 1.7 1.7

Deferred Tax Liabilities 0.7 0.6 0.6 0.6 0.6

Non Current Liabilities 1.9 2.2 2.7 2.7 2.7

Total Liabilities 13.8 11.7 12.0 13.7 15.6

Common Stock 3.0 19.9 27.9 27.9 27.9

Currency Translation Reserves (0.0) 0.0 0.0 0.0 0.0

Retained Earnings 10.6 6.3 12.5 19.2 26.8

Total Shareholders' Equity 13.6 26.3 40.4 47.1 54.8

Minority Interest 0.1 0.1 0.1 0.2 0.2

Total Liabilities & Shareholders' Equity 27.5 38.0 52.5 61.0 70.5

Source: Company, NRA Capital

Income Statement

Forecast

Balance Sheet

Forecast

page 18 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

CASHFLOW STATEMENT ($m) FYE 31 March

FY08 FY09 FY10F FY11F FY12F

Net Income 7.3 7.0 7.2 7.9 8.8

Adjustments:

Depreciation & Amortisation 1.6 2.1 2.3 2.6 3.1

(Gain)/Loss on Sale of PPE (1.3) 0.0 0.0 0.0 0.0

Income from Associates (0.1) (0.1) (0.1) (0.2) (0.2)

Interest Income (0.0) (0.0) (0.3) (0.5) (0.6)

Interest Expense 0.2 0.2 0.2 0.1 0.1

Income Tax Expenses 1.4 1.7 1.5 1.8 2.0

Other Adjustments (0.0) 0.0 0.5 0.2 0.2

Op. Profit before Working Capital Charges 9.1 10.8 11.2 12.0 13.5

Change in Working Capital:

Inventories 0.0 (0.1) (0.1) (0.1) (0.1)

Trade & Other Receivables (6.5) (2.3) (0.2) (4.0) (4.4)

Trade & Other Payables 2.2 (2.4) (0.4) 1.7 1.9

Cash Generated from Operations 4.8 6.0 10.6 9.6 10.9

Income Tax paid (0.6) (1.4) (1.5) (1.8) (2.0)

Interest Received 0.0 0.0 0.3 0.5 0.6

Interest paid (0.2) (0.2) (0.2) (0.1) (0.1)

Net Cash From Operations 4.0 4.4 9.2 8.1 9.3

Net CAPEX 4.3 (1.6) (1.9) (7.0) (2.0)

Other (increase) decrease in Net PPE 0.0 0.0 (2.8) 0.0 0.0

Net Investments (0.0) 0.0 0.0 0.0 0.0

Net Cash From Investing 4.2 (1.6) (4.8) (7.0) (2.0)

Share Issue 0.0 5.5 8.0 0.0 0.0

Repurchase of Treasury Stock 0.0 0.0 0.0 0.0 0.0

Dividends Paid 0.0 (0.5) (1.0) (1.2) (1.2)

Increase (Decrease) in Debt (5.7) (1.3) 0.7 0.0 0.0

Others (0.4) (0.5) 0.0 0.0 0.0

Net Cash from Financing (6.1) 3.2 7.7 (1.2) (1.2)

Change in Cash & Cash Equivalent 2.1 6.0 12.1 (0.1) 6.1

Cash & Cash Equivalent at Bgn Year 1.1 3.2 10.6 22.7 22.6

Ex rate changes 0.0 0.0 0.0 0.0 0.0

Cash & Cash Equivalent at End Year 3.2 9.2 22.7 22.6 28.8

Source: Company, NRA Capital

Cashflow Statement

Forecast

page 19 NRA Capital Pte Ltd

www.nracapital.com

Tritech Group Limited

NRA Capital Pte. Ltd (“NRA Capital”) has received compensation for this valuation report. This publication is confidential and general in nature. It was prepared from data which NRA Capital believes to be reliable, and does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. No representation, express or implied, is made with respect to the accuracy, completeness or reliability of the information or opinions in this publication. Accordingly, neither we nor any of our affiliates nor persons related to us accept any liability whatsoever for any direct, indirect, special or consequential damages or economic loss that may arise from the use of information or opinions in this publication. Opinions expressed are subject to change without notice. NRA Capital and its related companies, their associates, directors, connected parties and/or employees may own or have positions in any securities mentioned herein or any securities related thereto and may from time to time add or dispose of or may be materially interested in any such securities. NRA Capital and its related companies may from time to time perform advisory, investment or other services for, or solicit such advisory, investment or other services from any entity mentioned in this report. The research professionals who were involved in the preparing of this material may participate in the solicitation of such business. In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additional information is, subject to the duties of confidentiality, available on request. You acknowledge that the price of securities traded on the Singapore Exchange Securities Trading Limited ("SGX-ST") are subject to investment risks, can and does fluctuate, and any individual security may experience upwards or downwards movements, and may even become valueless. There is an inherent risk that losses may be incurred rather than profit made as a result of buying and selling securities traded on the SGX-ST. You are aware of the risk of exchange rate fluctuations which can cause a loss of the principal invested. You also acknowledge that these are risks that you are prepared to accept. You understand that you should make the decision to invest only after due and careful consideration. You agree that you will not make any orders in reliance on any representation/advice, view, opinion or other statement made by NRA Capital, and you will not hold NRA Capital either directly or indirectly liable for any loss suffered by you in the event you do so rely on them. You understand that you should seek independent professional advice if you are uncertain of or have not understood any aspect of this risk disclosure statement or the nature and risks involved in trading of securities on the SGX-ST.