trinidad & tobago - t&t ifc · trinidad & tobago mark yeandle mba fcim © the z/yen...

TRANSCRIPT

© The Z/Yen

Group 2014

Z/Yen Group Limited

90 Basinghall Street

London EC2V 5AY

United Kingdom

tel: +44 (20) 7562-9562www.longfinance.net

Trinidad & Tobago

Mark Yeandle MBA FCIM

© The Z/Yen

Group 2014

♦ Special – City of London’s leading think-tank and

research house

♦ Services – projects, coaching/training, expertise on

demand, research

♦ Sectors – technology, finance, voluntary, professional

services, outsourcing

British Computer Society IT Director of the Year for

PropheZy and VizZy

DTI Smart Award for PropheZy

Sunday Times Book of the Week, Clean Business Cuisine

£1.9M Foresight Challenge Award for Financial £aboratory

visualising financial risk

Z/Yen

© The Z/Yen

Group 2014

What We Already Know

Five Areas of Competitiveness:♦ Business Environment

♦ Financial Sector Development

♦ Infrastructure

♦ Human Capital

♦ Reputation

© The Z/Yen

Group 2014

A Recognised Taxonomy

© The Z/Yen

Group 2014

A Global Phenomenon

© The Z/Yen

Group 2014 ةيمالعال ةيالمال زكارمال رشؤم

Índice de Centros Financieros Globales

Indice dei Centri Financieri Globali

Indice des Centres Financiers Globaux

世界的な金融

センターインデックス

Σφαιρικός οικονομικός κεντρικός δείκτης

Глобальный индекс финансовых центров

Wskaźnik Globalnych Finansowych Centrów

Индекс на Световните Финансови Центрове

Goelydh Nírnaeth Arnoediad Blebithar

Globaler Finanzzentrenindex

全球金融中心指数全(quán) 球(qiú) 金(jīn) 融(róng) 中(zhōng) 心(xīn) 指(zhǐ) 数(shù)

A Global Phenomenon

© The Z/Yen

Group 2014

GFCI to Date

Edition Date Published Respondents Assessments

GFCI 1 March 2007 491 3,992

GFCI 2 September 2007 825 11,685

GFCI 3 March 2008 1,236 18,878

GFCI 4 September 2008 1,406 24,014

GFCI 5 March 2009 1,455 26,629

GFCI 6 September 2009 1,805 31,497

GFCI 7 March 2010 1,690 30,170

GFCI 8 September 2010 1,876 29,044

GFCI 9 March 2011 1,970 27,995

GFCI 10 September 2011 1,887 26,604

GFCI 11 March 2012 1,778 26,853

GFCI 12 September 2012 1,890 24,780

GFCI 13 March 2013 2,307 23,043

GFCI 14 September 2013 2,786 25,749

GFCI 15 March 2014 3,246 25,441

3,633 Respondents

29,226 Assessments

© The Z/Yen

Group 2014

The GFCI Process

GFCI 16 uses 29,226

assessments from

3,633 respondents

GFCI 16 uses 105

Instrumental

Factors

© The Z/Yen

Group 2014

Top 15 GFCI 16 Centres

Sao Paulo 34 666

Buenos Aires 40 657

Mexico City 44 652

Rio de Janeiro 45 650

British Virgin Islands 47 639

Panama 49 637

Cayman Islands 54 632

Bermuda 58 628

© The Z/Yen

Group 2014

The GFCI World

© The Z/Yen

Group 2014

Profile of Financial Centres

© The Z/Yen

Group 2014

Profile of Global Centres

© The Z/Yen

Group 2014

Profile of Transnational Centres

© The Z/Yen

Group 2014

Profile of Local Centres

© The Z/Yen

Group 2014

Profile of Local Centres

Bahamas +2Cayman Islands +18British Virgin Islands +18Panama 0Rio de Janeiro -12Sao Paulo -22Buenos Aires -15

© The Z/Yen

Group 2014 Less volatility and uncertainty

Headline Findings (1)

© The Z/Yen

Group 2014

♦ New York, London, Hong Kong and Singapore remain the

top 4 centres but 5th placed San Francisco is only 27 points

behind.

Headline Findings (2)

New York / London Trend Line

Hong Kong / Singapore Trend Line

© The Z/Yen

Group 2014

Headline Findings (3)

Eight of the top ten Asia/Pacific centres saw a decline in their ratings.

The progress made by the leading Asia/Pacific centres in GFCI 15 was

reversed with Hong Kong, Singapore, Tokyo, Seoul and Shanghai dropping

in the ratings. Significant gains were however made by Taipei, Beijing,

Manila and Mumbai.

© The Z/Yen

Group 2014

Headline Findings (4)Financial centres in Western Europe are still in turmoil. Leading

centers in the region all fell in the ratings, with Zurich, Geneva,

Luxembourg and Frankfurt joining London in losing ground.

© The Z/Yen

Group 2014

Headline Findings (5)

Middle East centres continue to rise in the index. Dubai, Abu Dhabi and

Riyadh all saw improved ratings. Qatar saw a small fall in its rating but

climbed in the ranks.

© The Z/Yen

Group 2014

Headline Findings (6)

Latin America centres continue to make progress. Both Brazilian

centres declined slightly in the ranks. Caribbean centres continue to

suffer reputational damage.

Cayman Islands

BVI

© The Z/Yen

Group 2014

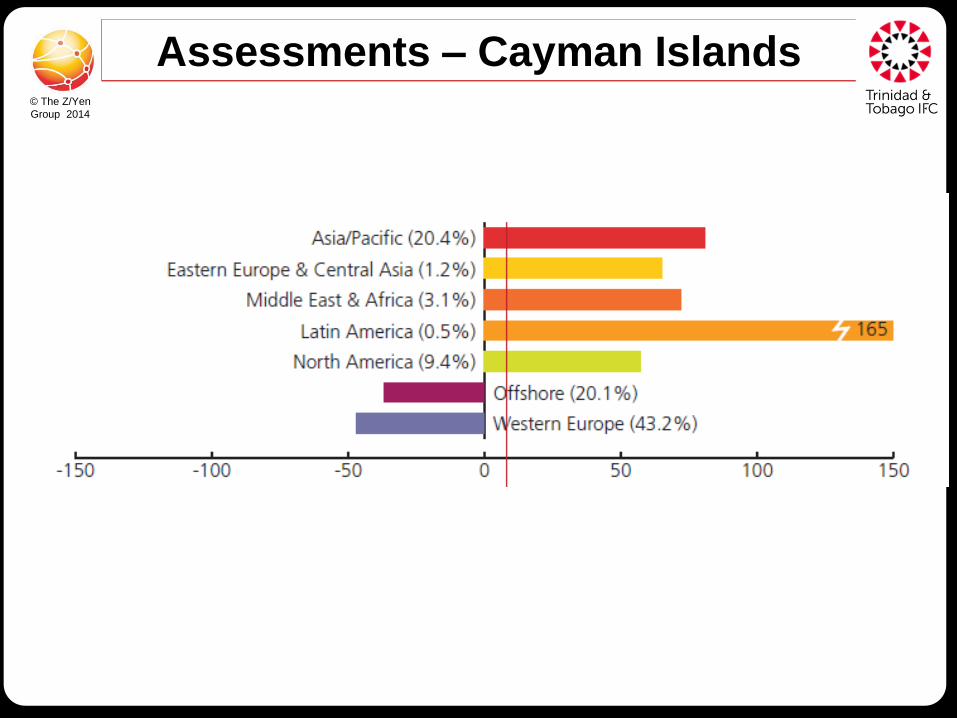

Assessments – Cayman Islands

© The Z/Yen

Group 2014

Assessments – Sao Paulo

© The Z/Yen

Group 2014

Industry Sectors

Sao Paulo

30th 25th 44th 43rd 27th

Cayman Islands

26th 43rd 61st 44th 36th

© The Z/Yen

Group 2014

Assessments by Size

© The Z/Yen

Group 2014

Stability – Selected Centres

Cayman Islands

British Virgin Islands

Rio de Janerio

© The Z/Yen

Group 2014

Areas of Competitiveness

Sao Paulo

21st 50th 31st 36th 27th

Cayman Islands

53rd 60th 66th 74th 65th

© The Z/Yen

Group 2014

Reputational “Advantage”

Sao Paulo 696 666 30

Cayman Islands 636 632 4

© The Z/Yen

Group 2014

Reputational “Disadvantage”

© The Z/Yen

Group 2014

Respondents

© The Z/Yen

Group 2014

Top 15 Instrumental Factors

© The Z/Yen

Group 2014

Business Environment

© The Z/Yen

Group 2014

Financial Sector Development

© The Z/Yen

Group 2014

Infrastructure

© The Z/Yen

Group 2014

Human Capital

© The Z/Yen

Group 2014

Reputational and General

© The Z/Yen

Group 2014

Generalities about Financial Centres

You can’t be good at everything – specialise

You can’t be an international centre without international people

Successful people want to live in successful cities

People want to live in cosmopolitan places

Reputation is vital – and you can lose a good one overnight

© The Z/Yen

Group 2014

Caribbean Centres

Sectors

♦ Strong in Wealth Management

♦ Strong in Professional Services

♦ Weak in Government & Regulatory

♦ Weak in Insurance

Pressures

♦ Larger nations – applying ongoing pressure trying to prevent tax

competition

♦ OECD – TIEAs, continuing peer reviews of regulatory framework

and implementation and sanctions for non compliance

♦ OECD members – e.g. US, UK France – still planning to limit use

of ‘havens’ for tax minimisation

♦ Publicity around aggressive tax planning schemes

♦ FATF/IMF – increased focus on AML and terrorist finance

♦ Foreign Account Tax Compliance Act (FATCA)

© The Z/Yen

Group 2014

Dos and Don’ts for Caribbean Centres

Do

Work together with others

Act to provide conduits

Act for the long term – Long Finance

Increase transparency wherever possible

Continue to demonstrate commitment to meeting

international standards

Continue to demonstrate skill levels and specialisations

Publicise benefits and functions

Don’t Be secretive

Help tax evaders

be deliberately unhelpful to the international community

© The Z/Yen

Group 2014

GFCI Modelling

All InfrastructureBusiness

Environment

Human

CapitalFinancial

Sector

Development

Reputation

© The Z/Yen

Group 2014

Building a Financial Centre

Infrastructure

Factors

Business

Environment

Factors

Human

Capital

Financial

Sector

Development

Reputation

© The Z/Yen

Group 2014

Trinidad and Tobago can be Successful!

© The Z/Yen

Group 2014

GFCI 17 – 23 March 2015

Participate yourself for GFCI 18 at:

www.long finance.net/gfci

© The Z/Yen

Group 2014

GFCI 17 – 23 March 2015

Participate yourself for GFCI 18 at:

www.long finance.net/gfci

© The Z/Yen

Group 2014

GFCI 17 – 23 March 2015

Participate yourself for GFCI 18 at:

www.long finance.net/gfci

© The Z/Yen

Group 2014