treasury management

DESCRIPTION

BankingTRANSCRIPT

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 1/48

Treasury Management

Virtual classes for CAIIB

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 2/48

Treasury management

Introduction to Treasury management

Treasury products

Funding and regulatory aspects Treasury risk management

Derivative products

Treasury and ALM

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 3/48

Concept of treasury

Originally engaged as a service

centre

only in daily cash management

preemptive reserve

management

Restricted deployment of surplusfunds

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 4/48

Concept of treasury contd

Currently !eing looked as a profit centre

"ith active operations in all the

markets in the country and a!roade#cept commodity markets

Continues to deal in only short term

markets e#cepting in case of $LR

investments and capital market

products

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 5/48

Integrated treasury Implies merger of !oth domestic and foreign

markets meaning t%o %ay movement of funds

depending upon changing market scenarios

and emerging opportunities Fore#& money and e'uity markets

(eing possi!le due to li!eralised environment

As markets are integrated so are the risksDerivatives are used e#tensively for the risk

management

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 6/48

)na!ling environment

Creation of clearing corporation of India

)sta!lishment of *$DL

Large num!er of *(FCs and mutual funds+rivate insurance providers

FIIs and FDIs

Availa!ility of derivative products in money&e'uity and fore# markets for interest and

price risk hedging

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 7/48

Treasury,s role in profit ma#imisation

Treasury operations are more profita!le

due to

Large si-e deals leading to lesseroperational e#penses

Relatively risk free markets

*eed for lesser capital outlay .ighly leveraged and %ith higher

return on capital

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 8/48

$ources of Treasury/s profits

Fore# market operations

!oth merchant and proprietary

Ar!itrage in different markets due to

time differentials though negligi!le

(oth in cash and derivative markets

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 9/48

$ources of Treasury/s profits

Money market

$huffling of investments taking

advantage of price changes ininvestment holdings

(orro%ing and Lending in money and

Repos markets taking advantage of

inherent strengths

Retailing of 0ovt1 securities

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 10/48

Organisation of treasury

Front office or dealing room Dealers in various segments carrying

actual tradesFore# markets 2 there can !e specialists

operating in for%ards& derivatives$ecurities markets2 generally in

secondary marketsInvestment desk operating in primary

markets

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 11/48

Organisation of treasury

(ack office 3erification of deals done and

settlements thereof Accounting& maintenance of *ostros

and reporting to regulator

Middle office

Risk management and adherence tovarious e#posure limits and MI$ to(oard

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 12/48

Fore# treasury products

$pot trades

For%ards

(oth for merchant cover operations

and proprietary trade for profits

0enerally for%ard rates are related

to interest differentials !ut in our

country also on demand and supply

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 13/48

Fore# treasury products

ContdCurrency $%aps for customers and for funding of proprietary transactions and

interest ar!itrageOptions and futures Investments

$urpluses in short and long term foreigncurrency assets 4treasury !onds& inter!ank loans& *ostro !alances and also FCloans to domestic customers

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 14/48

Money marketsCall money*otice money

Term money

Treasury !illCommercial paper

Certificate of deposit

Repos and reverse repos 5over night !yR(I6 7 acts as upper !and and floor ofmoney market rates

(ill rediscounting

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 15/48

$ecurities market products

0overnment securities 502sec6 and other

approved securities for $LR compliance

Market sta!ilisation schemeCorporate de!t 4non $LR securities

(oth medium 7 long term

Ratings& credit 'uality determineyields

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 16/48

Corporate de!t

De!entures transfera!le only !y

registration

(onds transfera!le !y endorsement and

deliveryConverti!le !onds

Floating and fi#ed rate !onds

Calla!le !onds$tep up coupon !onds

Deep discounting8-ero coupon !onds

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 17/48

(onds Contd11

+eriod !onds %here repayment is in

instalments

+remium !onds %here premium is paidon redemption

Collaterlised !onds

Creation of trustee for managing theaffairs and protecting interest of

investors in case of de!entures

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 18/48

Investments in e'uity market

Cap on investments at 9:; of net %orth

(oth in primary and secondary markets

As a <ualified institutional investor +rivate placement

Re'uires an research desk

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 19/48

Investments from8in

overseas markets FII investments

ADR8 0DR issues of Indian corporates

))FC funds Foreign currency funds of !anks

!orro%ings 7 lending in call money

markets su!=ect to ceiling of >:: ; and9? ; of net %orth

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 20/48

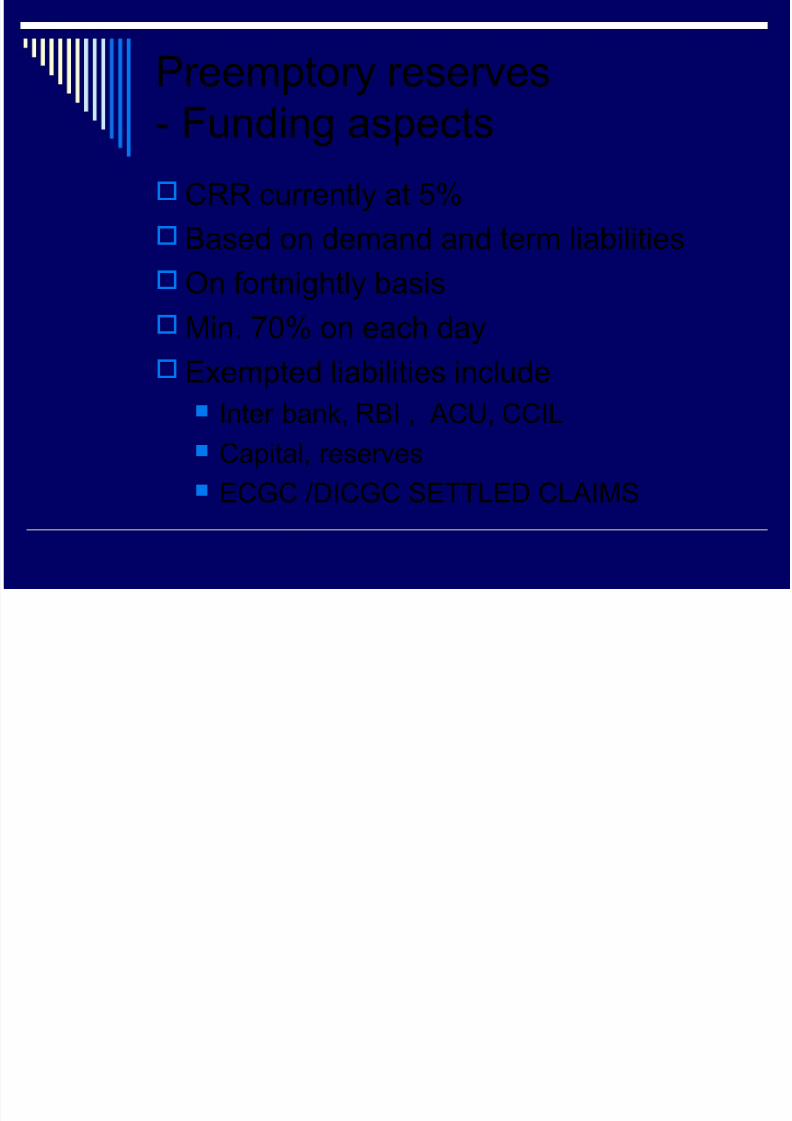

+reemptory reserves

2 Funding aspectsCRR currently at ?;

(ased on demand and term lia!ilities

On fortnightly !asisMin1 @:; on each day

)#empted lia!ilities include

Inter !ank& R(I & AC& CCIL Capital& reserves

)C0C 8DIC0C $)TTL)D CLAIM$

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 21/48

$LR investments

Currently at minimum 9B; of *DTL

$hortly going to !e 9? ;

Approved securities include in addition to0OI securities )#cess cash %ith !ranches

$tate govt1 securities

Other securities as identified !y R(I

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 22/48

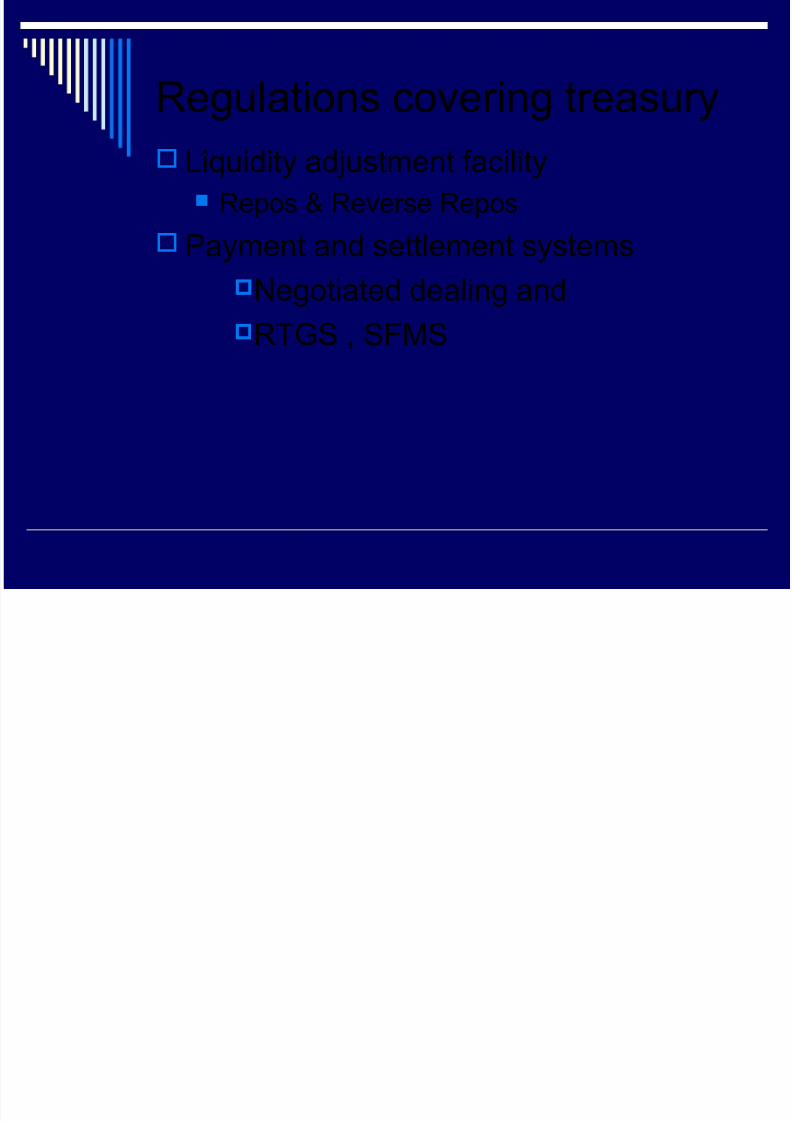

Regulations covering treasury

Li'uidity ad=ustment facility Repos 7 Reverse Repos

+ayment and settlement systems

*egotiated dealing and

RT0$ & $FM$

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 23/48

Risks in treasury

"e have credit& market and operational

risks even in treasury operations

Credit risk in de!t& e'uity and fore# OTCactivities

Market risks 4li'uidity and interest2in all

operations

Operational risk is very much present

!ecause of %holesale nature of !usiness

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 24/48

Risk management

Organisational controls Dual control on activities

Internal controls )#posure ceiling limits

position limits

Deal si-e limits

Open position limits $top Loss limits

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 25/48

Risk measurement

3alue at risk 53aR6 It is an estimate of potential loss Derived from the volatility in the market

3olatility is the standard deviation of the priceover a chosen period

Different methods for 3aR correlation using historical data

$imulation using various parameters Monte Carlo simulation using larger num!er of

parameters

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 26/48

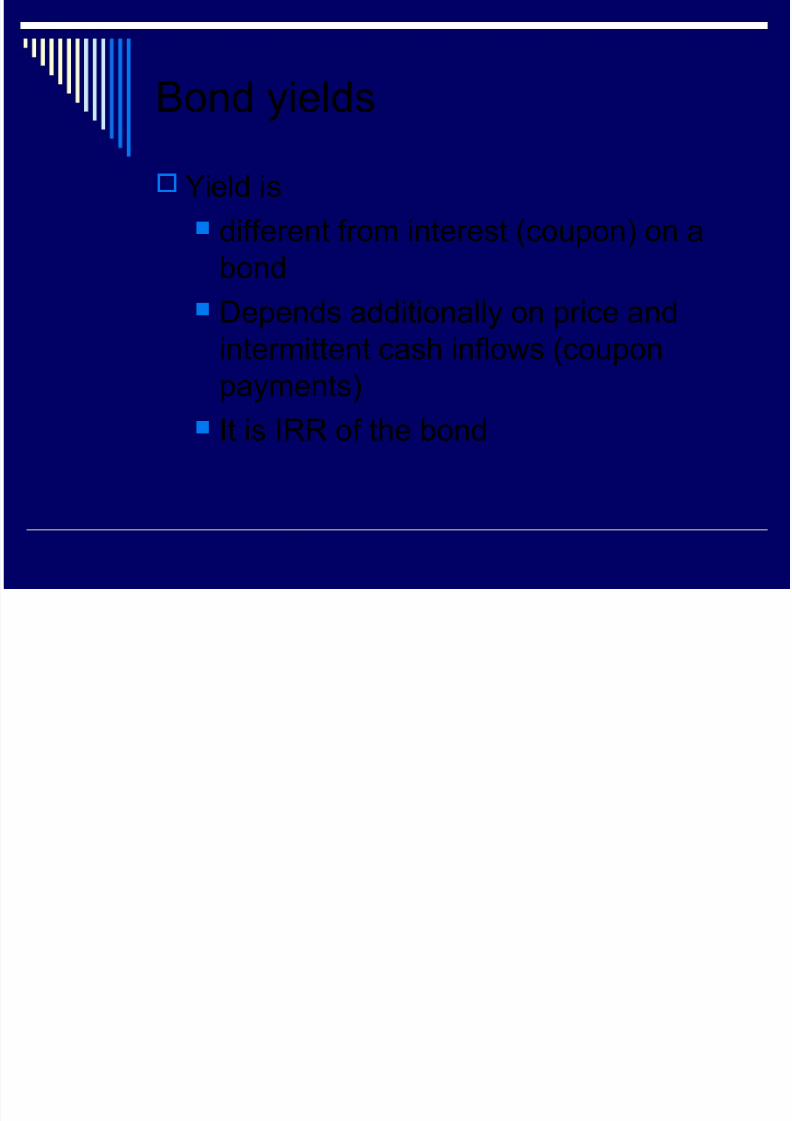

(ond yields

ield is

different from interest 5coupon6 on a

!ond Depends additionally on price and

intermittent cash inflo%s 5coupon

payments6

It is IRR of the !ond

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 27/48

(ond yields

Current yield is coupon divided !y the

current price

ield to maturity is the yield if the !ond isheld till it matures

T%o !onds %ith same TM may have

different prices !ecause of fre'uency of

coupons

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 28/48

Duration

Duration of a !ond is a measure of the time taken to

recover the initial investment in present value terms

Duration is a measure of the average time prior to

receipt of payments

)very !ond has a component of intermittent coupon

payments and repayment at maturity

During the life of the !ond if the market interest changes

the !ond/s price %ill !e effected and also the rate at

%hich these intermittent coupon payments can !e

reinvested1

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 29/48

Duration

Duration takes into account thefre'uency of coupon payments andstudies the price movements of a !ond

The period can !e different for different!onds of same maturity !ecause of si-eof intermittent payments

Duration of a !ond %here there is nointermittent payments coincides %ith thetenor of the !ond

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 30/48

Duration Contd1

It is o!tained as sum of the %eighted

averages of present values of inflo%s

%ith %eights !eing the time in years ofthe respective coupons

Modified duration D8 5> E yield6

+rice variation in percentage terms

2MD change in yield in !ps

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 31/48

Duration Contd11

Longer the duration& higher is the volatility

Treasurer arrives at the duration of a portfolio !y

adding the durations of each of the mem!er of

the portfolio To protect the portfolio from any interest rate

risk & the portfolio is to !e held for a period e'ual

to its duration

This process needs fre'uent shuffling of the

mem!ers since duration %ill change as the

maturity date approaches

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 32/48

Derivative products

Over the counter and e#change traded

For%ards 8 Options

Futures 5stocks& currency 7 interest6$%aps 5 currency & interest rate 7 !asis6

+rice insuring products5 options6

+rice fi#ing products 5others6

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 33/48

Derivatives

Derivatives are used !yGMarket makers

G.edgersG$peculatorsGar!itragers

Take an opposite position in derivative

market to the position in the underlying

8cash market

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 34/48

For%ards

OTC contracts

(oth parties are committed to contract

5definite delivery6+rice fi#ing in nature

+ay offs are linear to the underlying

)#istence of credit risk results in counterparty e#posure limits

For%ard price spot price E cost of carry

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 35/48

Options

Types !y rights Call and +ut

Types !y mode of settlement )uropean

and American

Types !y !enefit At the money& in the money and out of

money

ses of options are as a hedge againstprice risk and also for trading for profit

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 36/48

Options Contd11

In the money& at the money and out of

money depends upon %hether the strike

price is !etter& e'ual or %orse than the

market price of optionCurrent price of an option %ill depend

upon a host of factors like underlying

asset price and its volatility& strike price&

interest rates& time to e#piration All factors have a positive correlation

%ith strike price e#cept the strike price

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 37/48

Options Contd

There is a mathematical relationship

!et%een the current prices of a Call and

a +ut option %ith the same e#piry date

and same strike price and is called+T 4 CALL parity

3 c 4 3 p +a 4 H %here

3 c value of call 3 p value of put+a price of underlying asset and

H +3 of e#ercise price

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 38/48

Futures

Futures are !oth financial andcommodity

Currency futures are similar to for%ardsCurrency& stock and inde# futures are

hedging instruments against pricefluctuations

Interest futures are a hedge againstinterest rate movements

)ither delivery or !ack out

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 39/48

Futures Contd11

Margin re'uirements

Initial margin2 ena!les trading in very

high volumes compared to o%n stake3aria!le margin 4 due to daily MTM

Maintenance margin 5minimum margin to

!e maintained at all times6

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 40/48

)#change traded currency futures

Recently introduced as an e#changetraded product

(anks complying %ith the follo%ing can

!e clearing mem!ers Minimum net %orth of Rs1 ?:: crore1 Minimum CRAR of >: ;1 *et *+A should not e#ceed J ;1

(ank should have made a net profit in lastJ years1

Can trade for themselves8clients

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 41/48

)#change traded interest

futuresnderlying security is >:r @; coupon

02$ec

Contract si-e is Rs 9 lacs

Tenor of the contract is ma#1 >9 months

Availa!le contracts are B 'uarterly ones

Day count convention is JK: days

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 42/48

.edging investments risks %ith

long positions in futures Investor/s risk is a fall in market

interest %hich %ould impact his

return on investment1 "hen interestrates fall price of futures increases1(y going long on futures 5s6he cantake advantage of a reduced interest

situation in case it happens %hich%ill offset his loss in underlyingmarket

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 43/48

+ricing of Futures

$pot price

E cost of !orro%ing

4 income on the asset

Futures price

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 44/48

$%aps

Interest rate & e'uity and currency s%aps Interest rate s%aps can !e

Floating to fi#ed

Floating to floating or a !asis Coupon s%aps

For%ard rate agreement 5FRA6

Currency s%aps

Only principal Only interest +rincipal and interest

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 45/48

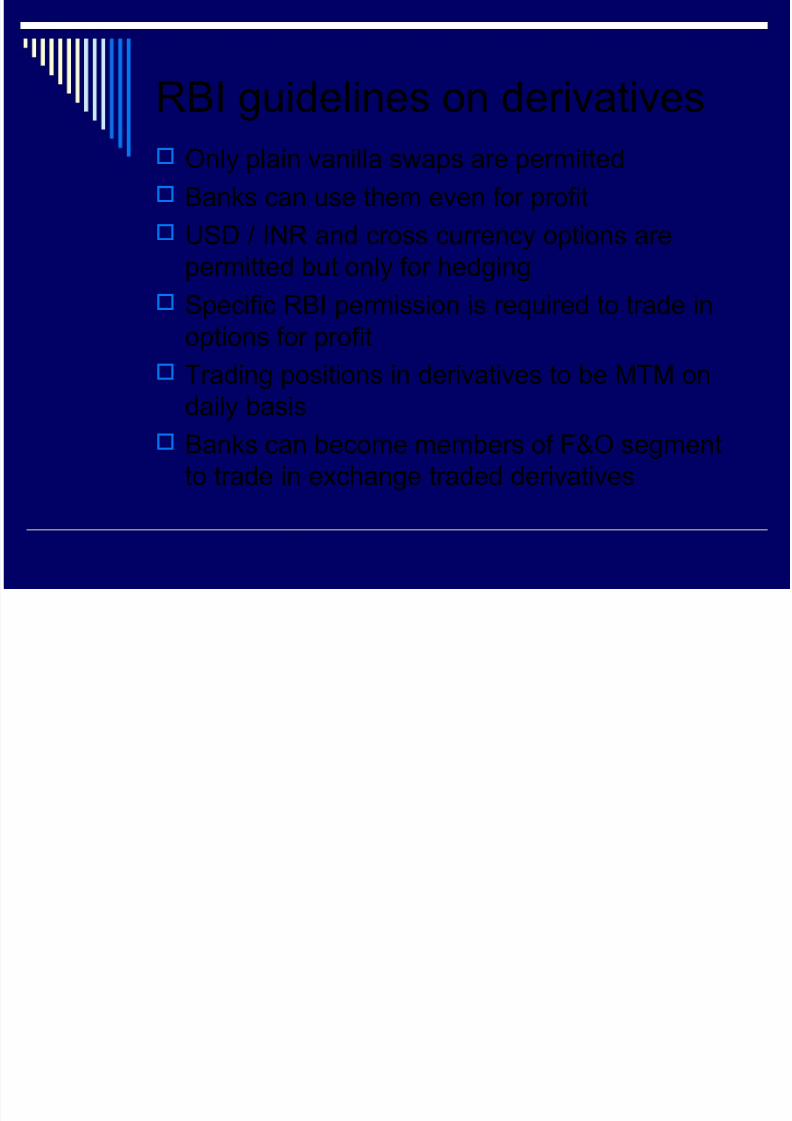

R(I guidelines on derivatives

Only plain vanilla s%aps are permitted

(anks can use them even for profit

$D 8 I*R and cross currency options are

permitted !ut only for hedging

$pecific R(I permission is re'uired to trade in

options for profit

Trading positions in derivatives to !e MTM on

daily !asis

(anks can !ecome mem!ers of F7O segment

to trade in e#change traded derivatives

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 46/48

Treasury/s role in ALM

$ince treasury deals in large volumes offunds it can !oth mo!ilise and deploy thefunds as per the !anks/ re'uirementeither domestically or in overseas

centres(eing in constant touch %ith market

players& treasury can have a !etterestimate of future interest rate

movements in the market Treasury is also engaged in determining

the transfer price mechanism

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 47/48

Important from e#am point of vie%

Role of each segment in treasury

Relation !et%een spot and for%ard ratesRelation !et%een t%o spot rates

Diff1 types in money market

Duration

sage of repo 7 reverse repo in controlling li'uidity

7/17/2019 Treasury Management

http://slidepdf.com/reader/full/treasury-management-56912714710b3 48/48

"I$.I*0 O ALL

$CC)$$ I* )HAM$7

T.A* O

FOROR +ATI)*T .)ARI*0