transportation analysis jj cavanaugh desirae dunn josh powell 1

TRANSCRIPT

1

Transportation AnalysisJJ CavanaughDesirae DunnJosh Powell

2

What We Are Trying to Accomplish•Overview

▫Total Spend▫By Mode▫By OD Pair▫Carriers in Each Mode▫Average Shipment Sizes

•Consolidation Opportunities▫LTL Improvements

Introduction Overview Opportunities Summary

3

Introduction

Overview

Opportunities Summary

4

Spend by Mode

LTL59.75%

TL26.26%

SP10.43%

IM3.40%

Air0.15%Mode Spend

LTL $100,320,342

TL $44,099,975

SP $17,519,928

IM $5,712,837

Air $257,283

Total $168,000,000

Introduction Overview Opportunities Summary

5

Most Valuable Carriers

135874062.13581%

32036302.32

19%

Most Variable Carriers

Other

Carrier NameFreight

PaidCarrier Type

1 USF HOLLAND INC $ 32,202,459 LTL

2SOUTHEASTERN FREIGHT LINES INC $ 20,484,588 LTL

3 CROUSE CARTAGE $ 17,013,543 TL4 NEW PENN MOTOR EXPRESS $ 13,546,279 SP

5OLD DOMINION FREIGHT LINE INC $ 6,207,804 TL

6U S XPRESS ENTERPRISES INC $ 5,647,193 LTL

7 USF BESTWAY $ 5,554,183 TL

8AMERICAN FREIGHTWAYS INC $ 4,910,105 TL

9 WATKINS MOTOR LINES INC $ 4,824,316 LTL

10BULLOCKS EXPRESS TRANS INC $ 3,617,057 LTL

11 VIKING FREIGHT SYSTEM $ 3,573,925 IM12 USF REDDAWAY TRUCK LINE $ 3,441,433 LTL13 ESTES EXPRESS LINES INC $ 3,421,973 LTL

14CARTER & SONS FREIGHTWAYS INC $ 3,358,866 LTL

15 SWEENEY TRANSPORTATION $ 2,949,194 LTL16 PRESTON TRUCKING CO $ 2,568,849 LTL17 RC TRANSPORT $ 2,552,284 LTL

Introduction Overview Opportunities Summary

6

Top Carriers LTL

Other20%

USF HOLLAND INC32%

SOUTHEAST-ERN FREIGHT

LINES INC20%

U S XPRESS ENTERPRISES

INC6%

WATKINS MO-TOR LINES INC

5%

BULLOCKS EXPRESS

TRANS INC4%

USF REDDAWAY TRUCK LINE

3%

ESTES EXPRESS LINES INC

3%

CARTER & SONS FREIGHTWAYS INC

3%

SWEENEY TRANSPORTATION3%

The top 9 out of 41 carriers have approximately 80% of LTL spend

These are our A and B Customers

Introduction Overview Opportunities Summary

7

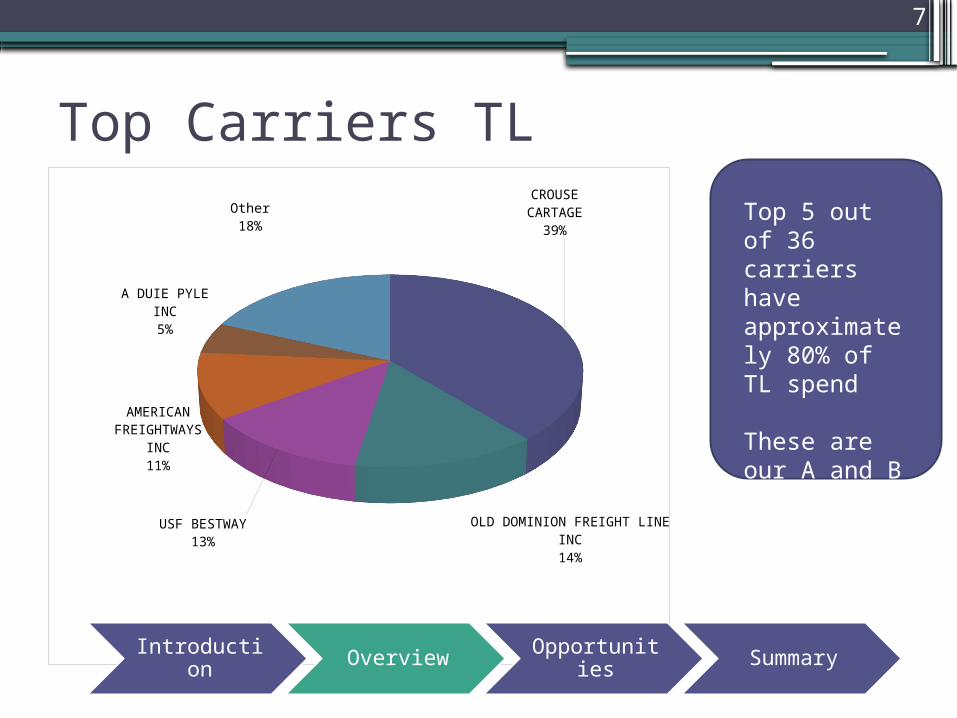

Top Carriers TLCROUSE CARTAGE

39%

OLD DOMINION FREIGHT LINE INC

14%

USF BESTWAY13%

AMERICAN FREIGHT-WAYS INC

11%

A DUIE PYLE INC5%

Other18%

Top 5 out of 36 carriers have approximately 80% of TL spend

These are our A and B customers

Introduction Overview Opportunities Summary

8

Other Carrier Modes•Small Parcel

▫Top carrier is responsible for approximately 77% of SP spend

•Intermodal▫Top carrier is responsible for approximately

63% of IM spend•Air

▫Top carrier is responsible for approximately 52% of Air spend

Introduction Overview Opportunities Summary

9

Top Carriers by Loads Moved

HMES

CRSE

TNT1USXI

WW

ATEXLA

BEXT

CFFWPYLE

VERN

0

5000

10000

15000

20000

25000

30000

Number of Loads

Carrier SCAC Codes

Loads

Our top 19 carriers handle 80% of the loads moved

This is only 21% of our total carriers

This is directly related to most valuable carriers

Introduction Overview Opportunities Summary

10

Top LTL Carriers by Loads Moved

HMES SEFL USXI WWAT RETL EXLA SWEY BEXT RCTV CFFW0

5000

10000

15000

20000

25000

30000

Number of Loads

Carrier SCAC Codes

Loads

Top 10 carriers handle 80% of loads moved

Introduction Overview Opportunities Summary

11

Top TL Carriers by Loads Moved

CRSE TNT1 ODFL ARFW PYLE CRCR0

2000

4000

6000

8000

10000

12000

14000

16000

Number of Loads

Carrier SCAC Codes

Loads

The top 6 carriers handle 80% of loads moved

This is only 17% of TL carriers

Introduction Overview Opportunities Summary

12

Introduction

Opportunities

Overview Summary

13

Spend by Lane•Top 3 OD Pairs

1. Cranbury, NJ to Charlotte, NC Approximately $735,000

2. Cleveland, OH to Milton, PA Approximately $546,000

3. Macon, GA to Charlotte, NC Approximately $492,000

Introduction Overview Opportunities Summary

14

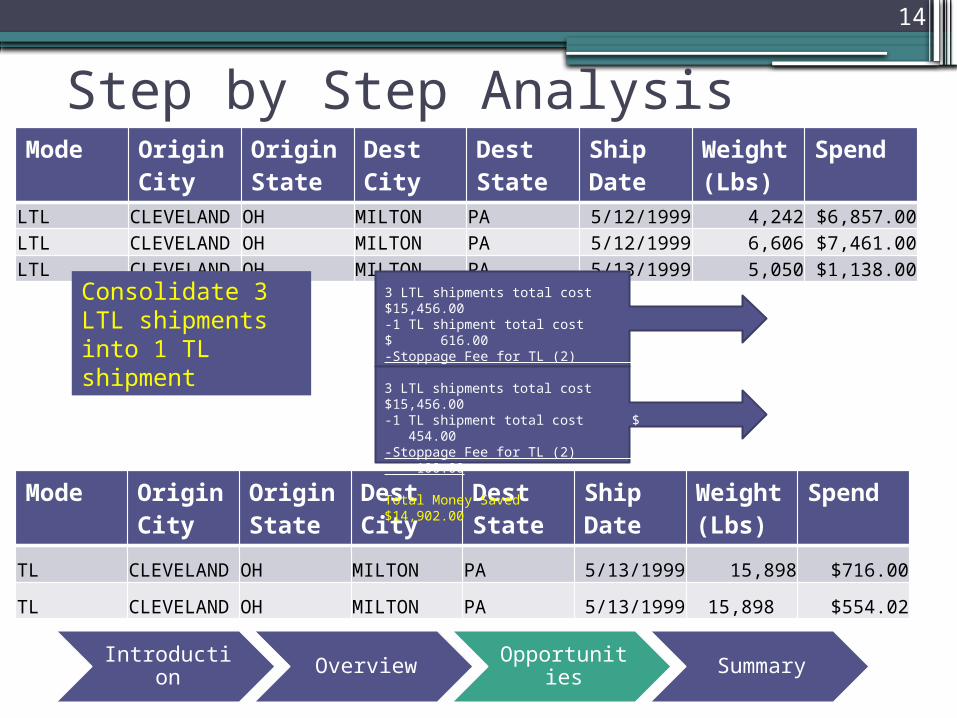

Step by Step AnalysisMode Origin

CityOrigin State

Dest City

Dest State

Ship Date

Weight (Lbs)

Spend

LTL CLEVELAND OH MILTON PA 5/12/1999 4,242 $6,857.00LTL CLEVELAND OH MILTON PA 5/12/1999 6,606 $7,461.00LTL CLEVELAND OH MILTON PA 5/13/1999 5,050 $1,138.00

Mode Origin City

Origin State

Dest City

Dest State

Ship Date

Weight (Lbs)

Spend

TL CLEVELAND OH MILTON PA 5/13/1999 15,898 $716.00

TL CLEVELAND OH MILTON PA 5/13/1999 15,898 $554.02

3 LTL shipments total cost $15,456.00-1 TL shipment total cost $ 616.00-Stoppage Fee for TL (2) $ 100.00

Total Money Saved $14,740.00

3 LTL shipments total cost $15,456.00-1 TL shipment total cost $ 454.00-Stoppage Fee for TL (2) $ 100.00

Total Money Saved $14,902.00

Consolidate 3 LTL shipments into 1 TL shipment

Introduction Overview Opportunities Summary

15

Consolidation Opportunities

1. Cranbury, NJ to Charlotte, NC Consolidated 152 shipments into 51

shipments2. Cleveland, OH to Milton, PA

Consolidated 78 shipments into 27 shipments

3. Macon, GA to Charlotte, NC Consolidated 98 shipments into 36

shipmentsIntroduction Overview Opportunitie

s Summary

16

Carrier Consolidation

•Drop carriers carrying less than 1% of freight paid▫Give this business to those carrying top

80%•LTL

▫Will reduce number of carriers from 41 to 14

•TL▫Will reduce number of carriers from 36 to

12Introduction Overview Opportunitie

s Summary

17

Current Spend vs. Consolidated Spend

Cranbury,NJ to Charlotte,NC

Cleveland, OH to Milton, PA

Macon, GA to Charlotte,NC

$-

$100,000.00

$200,000.00

$300,000.00

$400,000.00

$500,000.00

$600,000.00

$700,000.00

$800,000.00

Current SpendConsolidated SpendSensitivity

Current spend could be drastically reduced by consolidating LTL shipments into TL shipments

Introduction Overview Opportunities Summary

18

Savings

Cranbury,NJ to Charlotte,NC

Cleveland, OH to Milton, PA

Macon, GA to Charlotte,NC

$-

$100,000.00

$200,000.00

$300,000.00

$400,000.00

$500,000.00

$600,000.00

$700,000.00

SavingsSavings 2

NJ – NC$621K - $644K

OH – PA$490K - $503K

GA – NC$429.5K

Introduction Overview Opportunities Summary

19

S.W.O.T. Analysis of Consolidation•Strengths

▫Substantial savings▫Manage less carriers

•Weaknesses▫Higher lead times

•Opportunities▫Possibly better rates from top carriers

•Threats▫Top carriers may not run certain routes

that smaller carriers doIntroduction Overview Opportunities Summary

20

Introduction

Summary

Overview Opportunities

21

Summary

•LTL shipments are the largest percentages of our costs▫Consolidation is key▫Reduces costs

•Remove unnecessary carriers▫Give top carriers a reason to meet your

demands •80/20 rule

▫More volume = Better service and better rates

22

Questions