transitioning to the new normal

TRANSCRIPT

© 2021 PwC. All rights reserved

27 April @ 3pm GST

Middle East updates

Transitioning to the new normal

Resources

PwC ME COVID-19 website -

prior webcasts, insights and resourceswww.pwc.com/me/covid-19

Digital Fitness for the WorldPwC’s upskilling contribution to the world in response to COVID-19.

Access our free Digital Fitness App available from the Apple App

store and Google Play store.

If registering with your personal email, use invite

code (LRNALL) to access today

PwC Middle East - Webcast Series - 27 April 2021

1Economic update

Richard BoxshallChief Economist

PwC Middle East

2‘Reinventing the Gulf Region: Putting local economies,

citizens and innovation first’ viewpoint

Dr Yahya AnoutiPartner

Strategy& Middle East

Agenda

PwC Middle East - Webcast Series - 27 April 2021

Dima SayessPartner

Strategy& Middle East

Quick poll:How would you rate your

confidence levels at this current time?

Economic Update

PwC Middle East - Webcast Series - 27 April 2021

$65

Source: IMF regional economic outlook MENAP - April 2021

‘Reinventing the Gulf Region:

Putting local economies, citizens, and innovation first’ viewpoint

8

https://www.strategyand.pwc.com/m1/en/reinventing-the-gulf-region

GCC governments should adapt to resolve five growing tensions along: “ADAPT”

AAsymmetry

DDisruption

AAge

PPolarization

TTrust

Source: Strategy&9

Growing

imbalances

put recovery

at risk

The speed,

scale, and

pervasive

nature of

technology

Demographic

pressures

continue to

build

The global

consensus

breaks down

as

nationalism

rises

Institutional

expectations

are on the

rise

Asymmetry: Growing imbalances put recovery at risk

AAsymmetry

DDisruption

AAge

PPolarization

TTrust

Exposure to

structural economic

challenges

SMEs struggling to

compete

Pressure on urban

infrastructure and

resources

The need for speed

in Industry 4.0

Dominance of

major tech players

Technology-

enabled, new ways

of living, working,

and consuming

Shift to preventive

and personalized

healthcare

Youth bulge and

employment

challenges

Aging population

and the looming

pension crisis

Jockeying among

superpowers

Global and regional

integration

challenges

“Slowbalization” and

localization

Citizen-centric,

platform

government

Transition to

sustainable, low-

carbon future

Integrated safety

and security

management

Source: Strategy&10

GCC Countries GDP growth rates, already slowing down prior to COVID-19[%, 2011-2019]

2014 2015 2016

1.0%

2018 2019-5.0%

14.0%

4.0%

0.0%

-1.0%

3.0%

8.0%

2.0%

7.0%

2011 2012

6.0%

5.0%

9.0%

2013 2017

KuwaitBahrain QatarOman Saudi Arabia United Arab Emirates

The GCC real GDP growth rates have been slowing down prior to the pandemic, and showed a 5.7% contraction in 2020

Source: World Bank

Exposure to structural economic challenges

• Structural challenges are hindered by:

- High expenditures, especially the wage bill

(above 10% of GDP compared to 5.4% global

average) and subsidies

- Narrow tax base

- Limited diversification

- Restrictive trade policies and low R&D

11

- 5.7%

2020

+1.7% +2.7%

2021 2022Rea

l G

DP

Gro

wth

Slower than global average

of 4% & 3.8%

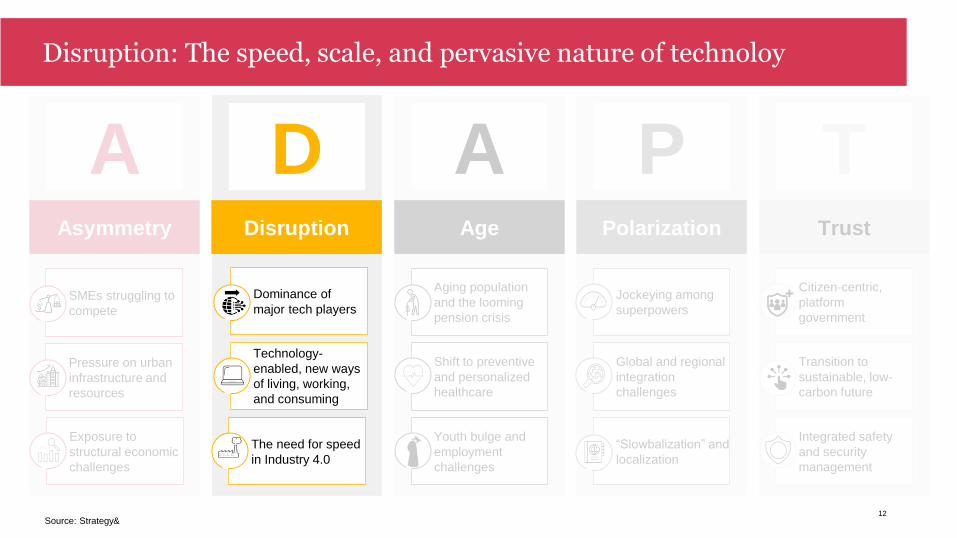

Disruption: The speed, scale, and pervasive nature of technoloy

AAsymmetry

DDisruption

AAge

PPolarization

TTrust

Exposure to

structural economic

challenges

SMEs struggling to

compete

Pressure on urban

infrastructure and

resources

The need for speed

in Industry 4.0

Dominance of

major tech players

Technology-

enabled, new ways

of living, working,

and consuming

Shift to preventive

and personalized

healthcare

Youth bulge and

employment

challenges

Aging population

and the looming

pension crisis

Jockeying among

superpowers

Global and regional

integration

challenges

“Slowbalization” and

localization

Citizen-centric,

platform

government

Transition to

sustainable, low-

carbon future

Integrated safety

and security

management

Source: Strategy&12

A set of challenges should be mitigated to accelerate I4.0 adoption

Source: Strategy&13

Low level of familiarity

with I4.0 technologies

use-cases and

operational benefits

Lack of expertise in

estimating the economic

benefit of I4.0 technology

decreases industrial

players interests in its

roll-out

Limited availability of

local capabilities to drive

adoption and operations /

maintenance of I4.0

technology

UNCLEAR ECONOMIC BENEFITS2

LIMITED I4.0 TALENT POOL4

LIMITED AWARENESS OF I4.0 BENEFITS11 2 4

Limited availability of low

cost financing for SMEs

reduces attractiveness of

I4.0 technologies

business cases

HIGH FINANCING COST33

Age: Demographic pressure in the GCC continues to build

AAsymmetry

DDisruption

AAge

PPolarization

TTrust

Exposure to

structural economic

challenges

SMEs struggling to

compete

Pressure on urban

infrastructure and

resources

The need for speed

in Industry 4.0

Dominance of

major tech players

Technology-

enabled, new ways

of living, working,

and consuming

Shift to preventive

and personalized

healthcare

Youth bulge and

employment

challenges

Aging population

and the looming

pension crisis

Jockeying among

superpowers

Global and regional

integration

challenges

“Slowbalization” and

localization

Citizen-centric,

platform

government

Transition to

sustainable, low-

carbon future

Integrated safety

and security

management

Source: Strategy&14

30

16

12 12 118 7 7

0

5

10

15

20

25

30

35

40

45

50

55

U.S.CanadaSaudi

Arabia

OmanKuwait UAE BahrainSingapore

Youth unemploymentTotal unemployment

Percentage of youth unemployment and total unemployment

(% 2019)

• Youth unemployment is rooted in:

- Labor-market skills mismatch due to poor

alignment with education curricula

- High public sector employment

- Limited labor market flexibility

The GCC youth bulge could be a huge source of economic growth if the current unemployment challenges are addressed

Youth bulge and employment challenges

Source: World Bank15

GCC Youth Population

(age 15-29)

24%

GCC Youth

Unemployment

12% Female YU = 3

× more than

male YU

! Key Challenges

Polarization: The global consensus breaks down as nationalism rises

AAsymmetry

DDisruption

AAge

PPolarization

TTrust

Exposure to

structural economic

challenges

SMEs struggling to

compete

Pressure on urban

infrastructure and

resources

The need for speed

in Industry 4.0

Dominance of

major tech players

Technology-

enabled, new ways

of living, working,

and consuming

Shift to preventive

and personalized

healthcare

Youth bulge and

employment

challenges

Aging population

and the looming

pension crisis

Jockeying among

superpowers

Global and regional

integration

challenges

“Slowbalization” and

localization

Citizen-centric,

platform

government

Transition to

sustainable, low-

carbon future

Integrated safety

and security

management

Source: Strategy&16

• GCC is among regions with lowest FDI

globally (USD 21 billion in 2019); only

1.3% of global FDI

• GCC exports reduced by USD 59 billion in

2020

After decades of globalization, a shift toward regional and local economic activity is underway

“Slowbalization” and Localization

17

50

60

70

80

90

100

110

120

130

140

150

160

170

180

190

200

2013 2014 2015 2016 2017 2018 2019

%

Source: World Bank

United Arab Emirates Qatar

Bahrain

Kuwait

Saudi ArabiaOman

Reduction in GCC merchandise trade (% of GDP 2013-19)

World Trade (2020)

- 9%World FDI

(2020)

- 42%

Trust: Institutional expectations are on the rise

AAsymmetry

DDisruption

AAge

PPolarization

TTrust

Exposure to

structural economic

challenges

SMEs struggling to

compete

Pressure on urban

infrastructure and

resources

The need for speed

in Industry 4.0

Dominance of

major tech players

Technology-

enabled, new ways

of living, working,

and consuming

Shift to preventive

and personalized

healthcare

Youth bulge and

employment

challenges

Aging population

and the looming

pension crisis

Jockeying among

superpowers

Global and regional

integration

challenges

“Slowbalization” and

localization

Citizen-centric,

platform

government

Transition to

sustainable, low-

carbon future

Integrated safety

and security

management

Source: Strategy&18

LOCAL FIRST

CITIZENS FIRSTINNOVATION FIRST

GCC governments could adopt a holistic transformation agenda that hinges on three focus areas

Principal focus areas

19

Redefine economic growth models

Rethink institutionsAdopt a holistic, citizen-centric

approach

GCC governments could adopt new economic growth models

LOCAL FIRST

20

Define a new path to economic

diversification

Establish domestic value chains

Foster private sector competitiveness

Redesign the regional integration model

Competitive high-value added industries

Industry 4.0 in sectors

Test-bed for latest innovations

R&D investment

Local goods, essential for national security

GCC governments could adopt a holistic, citizen-centric approach

CITIZENS FIRST

21

Social safety nets

Social investment models

Hybrid pension schemes

Unified labor market

Design new social contracts

Boost labor market flexicurity and

productivity

Improve quality of life

Citizens' well-being, smart enabled

GCC governments could rethink institutions to put innovation first

INNOVATION FIRST

22

Seamless customer delivery (unique digital IDs)

Citizensco-designing solutions

Low pro-cyclical policies

Sectoral PPPs ESG application

Exploit the power of digital to offer personalized,

predictive, and proactive service delivery

Transition to participatory and agile

governance

Strengthen fiscal resilience

Adopt an integrated sustainability

agenda

23

https://www.strategyand.pwc.com/m1/en/reinventing-the-gulf-region

How would you rate your confidence levels at this current time?

PwC Middle East - Webcast Series - 27 April 2021

19 January

16 February

Quick poll:

23 March

Q&A

Contact us

Stephen AndersonStrategy & Markets Leader

PwC Middle East

Strategy& Middle East

Dr Yahya AnoutiPartner, Energy,

Chemicals, and Utilities

Practice

PwC Middle East - Webcast Series - 27 April 2021

PwC Middle East

Richard BoxshallChief Economist

Dima SayessPartner, Government

and Public Sector

Practice

Strategy& Middle East

Thank you

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Established in the Middle East for 40 years, PwC has 22 offices across 12 countries in the region with over 5,600 people. (www.pwc.com/me).

PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for

further details.

© 2021 PwC. All rights reserved