transition of credit spread preferences in the european ... · transition of credit spread...

TRANSCRIPT

Transition of Credit Spread Preferences in the European Periphery Debt Crisis

George Christodoulakis

Manchester Business School

0

10

20

30

40

50

60

70

80

09

/20

08

10/2

00

8

11/2

00

8

12/2

00

8

01/

200

9

02/

200

9

03

/20

09

04

/20

09

05

/20

09

06

/20

09

07/

200

9

08

/20

09

09

/20

09

10/2

00

9

11/2

00

9

12/2

00

9

01/

2010

02/

2010

03

/20

10

04

/20

10

05

/20

10

06

/20

10

07/

2010

08

/20

10

09

/20

10

10/2

010

11/2

010

12/2

010

01/

2011

02/

2011

03

/20

11

04

/20

11

05

/20

11

06

/20

11

07/

2011

08

/20

11

09

/20

11

Bond PD

CDS PD

CRA PD

Rich History of Political and Economic Events

0

10

20

30

40

50

60

70

80

09

/20

08

10/2

00

8

11/2

00

8

12/2

00

8

01/

200

9

02/

200

9

03

/20

09

04

/20

09

05

/20

09

06

/20

09

07/

200

9

08

/20

09

09

/20

09

10/2

00

9

11/2

00

9

12/2

00

9

01/

2010

02/

2010

03

/20

10

04

/20

10

05

/20

10

06

/20

10

07/

2010

08

/20

10

09

/20

10

10/2

010

11/2

010

12/2

010

01/

2011

02/

2011

03

/20

11

04

/20

11

05

/20

11

06

/20

11

07/

2011

08

/20

11

09

/20

11

Bond PD

CDS PD

CRA PD

Lehman Brothers

Greece Negative Watch

Greek Elections

Greek Deficit > 10%

Greek Downgrades

EU-IMF Offer to Bailout GR

EU-IMF MoUwith GR

EFSF, SMP

EUBankStress T

EU 6-pack

EU-IMF Irish Bailout

Improved GR loan terms

Portuguese Crisis

2nd GR pack PSIESM

FR banksSMP

2

Market-Based Sovereign Risk Measures

• Bond Prices– Long term investors

– Implied default probability

• Credit Default Swap Spreads– Short term investors

– Implied default probability

• Credit Rating Agencies– Institutional

– Mapping to observed forward default frequencies

• Interaction for Sovereign Asset Pricing– Beber et al (2009), Feldhütter and Lando (2008)

– Pan and Singleton (2008). 3

Interactions

• Which part of the market transmits information?

• Standard approaches– Corporate credit literature

– Study the “Basis”

– Longstaff et al (2005) , corporate data

– Fontana and Scheicher (2011), EU sovereign data

Bond Yield – Risk Free Rate ~ CDS Spread

Basis = (Bond Yield – Risk Free Rate) - CDS Spread

4

Joint Market Loss Preferences

• Market Risk Forecasts are jointly determined

– Bond-implied PD

– CDS-implied PD

– CRA-implied PD

• Forecast Optimality

– Find PD to Minimise the loss from mis-forecasting

• Multivariate Loss ≠ Sum of Univariate Losses

• Relative Forecast Errors: forecast A – forecast B

5

Estimating Joint Market Loss Preferences

• Komunjer and Owyang (2012), RESTAT

– GMM algorithm to estimate joint loss preferences

• Define a vector of relative PD forecasts, s-period ahead

– Implied from bonds (b), CDS (c) and CRAs (r)

• Define a vector of relative forecast errors

strstcstb pdpdpd +++ ,,, ,,

( )'e strstcstrstbstcstbst pdpdpdpdpdpd +++++++ −−−= ,,,,,, ,,

6

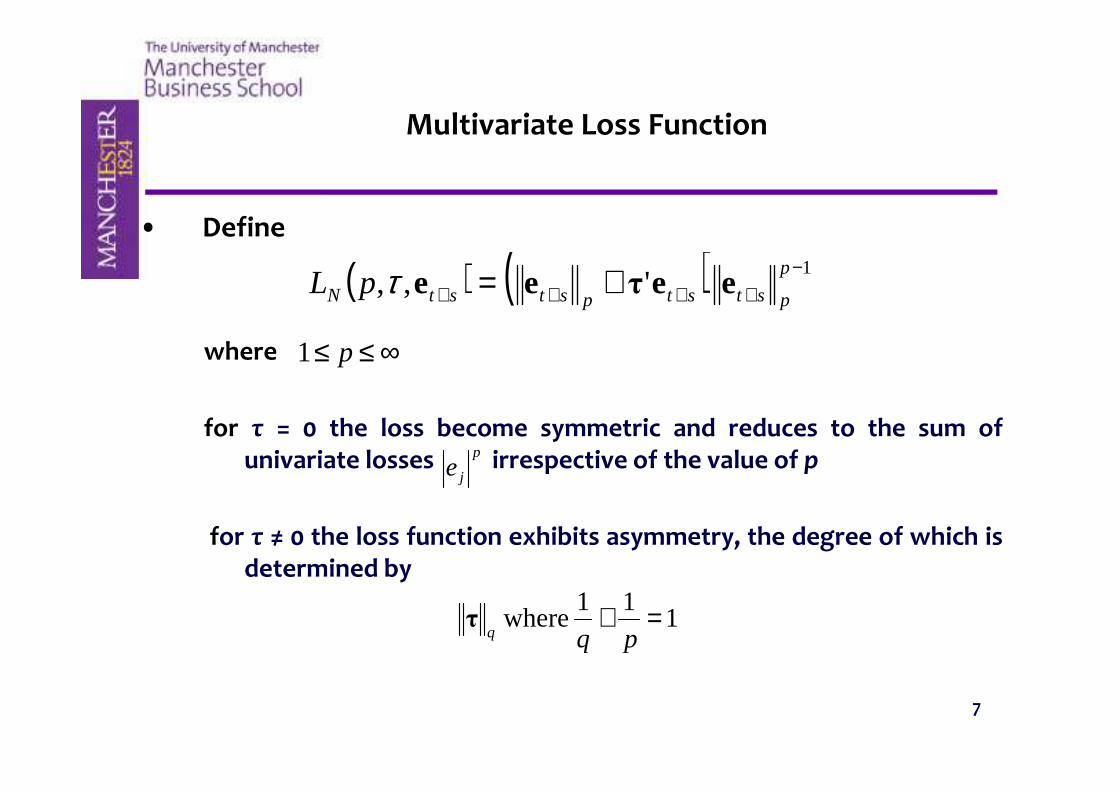

Multivariate Loss Function

• Define

where

for τ = 0 the loss become symmetric and reduces to the sum ofunivariate losses irrespective of the value of p

for τ ≠ 0 the loss function exhibits asymmetry, the degree of which isdetermined by

( ) ( ) 1',,

−++++ += p

pststpststN pL eeτeeτ

∞≤≤ p1

p

je

111

where =+pqq

τ

7

GMM Estimation

• We use the optimality f.o.c’s, so that in the presence of a vector xt ofd instruments, we can construct 3×d orthogonality conditions of theform

• Then

where

• Our GMM estimator then becomes

( ) tpstpst

p

pstpst pp xeveτeτvg ⊗−++= −++

−++

11')1(

[ ] [ ]∑∑ +−−

+−

stst TT gSg'

τ

111 ˆmin

∑ +−= 'ggS ststT _1ˆ

[ ] aSBBSBτ'1' ˆˆˆˆˆˆˆ 11 −−−−=

( ) ( ) ( )( )tp

sttppsttNd

p

pst

pT

pT

xva

exvexIeB '

⊗=

⊗−+⊗=

∑

∑−

+−

+−

+−

1

111

ˆ

1ˆ

8

Empirical Application

• Data set: weekly, Sept 2008 – Sept 2011

• 5yr-Bond prices and coupons

• 5yr-CDS spreads

• CRA ratings

• Greece, Italy, Spain, Portugal, Ireland

• CDS-implied PDs: Inverting Hull & White (2000) CDS pricing

• Bond-implied PDs: solving numerically

• CRA-implied PD: mapping ratings on 5-yr forward default frequencies

( ) ( ) ( ) ( ) ( ) ( )∑∑== ++

+++

+++

=5

155

5

1 1111

1

11 tt

bt

b

btt

bt pdr

pdR

pdrpdr

CP

9

Empirical ResultsTable 1: Loss Preferences, Weekly data, 8.9.2008 – 19.9.2011

10

Greece Italy Spain Portugal Ireland

Multivariate Estimation

τ1 0.53** (0.27) 0.15** (0.08) 0.26*** (0.09) 0.25*** (0.03) 0.57*** (0.03)

τ2

-

1.22** (0.77) 0.77*** (0.02) 0.80*** (0.01) 0.80*** (0.01) 0.79*** (0.01)

τ3

-

3.09*** (1.18) 0.62*** (0.06) 0.53*** (0.07) 0.56*** (0.02) 0.22*** (0.04)

J 128.6 154.0 155.2 146.6 81.42

Norm 3.367 1.004 1.001 1.004 1.002

Interpretation

11

• Two joint loss preference regimes

– Positive parameters for Italy, Spain, Portugal, Ireland

– One positive, two negative parameters for Greece

BondsCDSCRAs ff

CRAsBondsCDS ff

Judgement Breakdowns

12

• Giacomini and Rossi (2009), RES

• Forecasting steps: s

• Split sample T into

– m-in-sample

– n-out-of-sample observations

• Out-of-sample loss

• Surprise loss

where is the average in-sample loss

( )stlstkst pdpdLL +++ −= ,,

sTmtLLSL tstst −=−= ++ ,...,for

tL

Judgement Breakdowns - 2

13

• Average surprise loss

• Null hypothesis: no-breakdown

where under the null

∑−

=+

−≡sT

mtstnm SLnSL 1

,

( ) 0: ,0 =nmSLEH

nm

nm

snm

SLnt

,

,,, σ̂

=

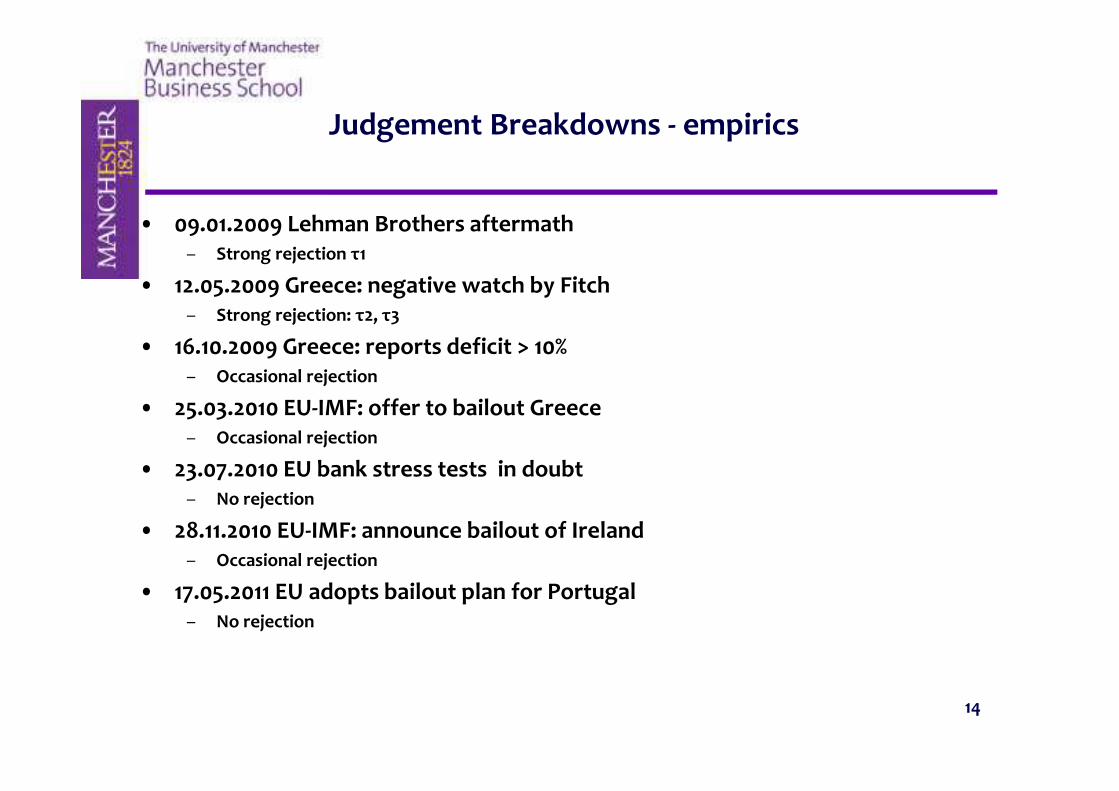

Judgement Breakdowns - empirics

14

• 09.01.2009 Lehman Brothers aftermath– Strong rejection τ1

• 12.05.2009 Greece: negative watch by Fitch– Strong rejection: τ2, τ3

• 16.10.2009 Greece: reports deficit > 10%– Occasional rejection

• 25.03.2010 EU-IMF: offer to bailout Greece– Occasional rejection

• 23.07.2010 EU bank stress tests in doubt– No rejection

• 28.11.2010 EU-IMF: announce bailout of Ireland– Occasional rejection

• 17.05.2011 EU adopts bailout plan for Portugal– No rejection

15

Judgement Breakdowns - empirics

Joint Loss Preferences over time - 1

16

Joint Loss Preferences over time - 2

17

• Emergence of three loss preference regimes

– τ1 , τ2, τ3 > 0 (R1)

– τ1 > 0, τ2, τ3 < 0 (R2)

– τ1 < 0, τ2, τ3 > 0 (R3)

• Regime switching patterns

– Greece: R3, R1, R2 (Hellenic Club)

– Italy, Spain, Portugal: R3, R1 (Latin Club)

– Ireland: R1, R3: (Celtic Club)

CDSBondsCRAs ff

CRAsBondsCDS ff

BondsCDSCRAs ff

Transition of Loss Preference Regimes

18

• Decomposition of joint loss asymmetry magnitude into proportions

• Derivation of vector time series of loss asymmetry proportions

• Markov process

12

2

2

32

2

2

22

2

2

1 =++τττ

τττ

( ) ( ) ( )itjtititjt spspspspsp ====== −−− 111 |PrPr,Pr

( ) ( ) ( )∑ ===== −−i

itjtitjt spspspsp 11 |PrPrPr

Transition of Loss Preference Regimes - 2

19

• Regression representation

• Incorporating constrains via a prior distribution

• Derive Posterior and use Monte Carlo Integration to draw random samples from the posterior. Then

ijβ

X

jijj

jjjj

=>≥=

+=

for5.0,0 ,1

s.t.

ββ

eβP

1'

),0(~ 2IN σe

( ) ( ) ( )2***2***2* ,Prior ,, Likelihood,,Posterior σσσ βPβPβ ×= XX

( ) ( )( ) ( )( )***

1*

**** Posterior 1lim XgE

I

Xg

N

N

i i

ii

Nyβ

β

Pββ=∑

=∞→

Transition of Loss Preference Regimes - empirics

20

Conclusions

21

• Strong evidence for joint asymmetric preferences

– Optimism, Pessimism

• Joint Preference Regimes

(R1)

(R2)

(R3)

• Regime Switching Country Clubs

– Hellenic, R3, R1, R2

– Latin, R3, R1

– Celtic, R1, R3

• Large Internal Transition Probabilities

– Predictability of Joint Preference Regimes

CDSBondsCRAs ff

CRAsBondsCDS ff

BondsCDSCRAs ff

End

Transition of Credit Spread Preferences in the European Periphery Debt Crisis

22